Cryptocurrency Posts

Crypto Briefing

Tighter US chip export controls to China could reshape global semiconductor supply chains, impacting international manufacturing strategies.

The post Key Republican urges US to block advanced chips to China appeared first on Crypto Briefing.

Meta's return to open AI models could democratize AI development, challenging the power concentration of closed systems and fostering innovation.

The post Mark Zuckerberg criticizes closed AI rivals as Meta returns to open models appeared first on Crypto Briefing.

Meta's focus on privacy for AI agents could redefine user trust, potentially reshaping revenue models and industry standards in data handling.

The post Meta plans fully private mode for personal agents, ensuring user privacy appeared first on Crypto Briefing.

Tokenized equity dividends in crypto wallets highlight evolving financial landscapes, offering 24/7 trading but posing unique custodial risks.

The post IBM bStock dividends now available in Spot Wallets, $1.69 per share appeared first on Crypto Briefing.

Meta's closed API approach for Muse Spark 1.2 may limit open-source collaboration, impacting innovation and accessibility in AI development.

The post Meta opens weights for Muse Glimmer and announces Muse Spark 1.2 release appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Trump Media Pulls Back From Crypto Deals: Report

The President Donald Trump-backed media company, Trump Media and Technology Group, is pulling back from two of its crypto deals, according to a report by Axios.

The publication reported Friday that the two deals with Crypto.com — a prediction market and treasury — would not go ahead.

Citing comments from fusion energy company TAE’s interim CEO, Kevin McGurn, the publication said that Trump Media had pulled the deals as the market for digital asset treasury companies had become saturated over the past year.

Trump Media last year said it was working with crypto exchange Crypto.com to build a Cronos treasury with $6.4 billion in backing. Cronos is the native coin of Crypto.com’s platform.

It later in 2025 said it was working with Crypto.com on Truth Predict, a betting platform to allow users to put money on sports games, elections and other events.

Digital asset treasuries exploded in popularity last year, with companies following in the footsteps of Nasdaq-listed software company Strategy to build balance sheets with Bitcoin and other cryptocurrencies.

But a slump in prices since October has hurt the stock of a number of companies who adopted the business idea.

McGurn was quoted saying that the decision to scale back was driven more by “competitive dynamics” rather than regulatory concerns surrounding a crypto company backed by the president.

President Trump campaigned on a ticket to help the crypto space and received backing from major players in the space.

The president since taking office has launched a meme coin and he and his family backed a crypto project, World Liberty Financial.

Axios added that the exchange-traded funds debuted last year by Trump Media, special purpose acquisition company Yorkville Acquisition Corp., and Crypto.com would continue.

This post Trump Media Pulls Back From Crypto Deals: Report first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Senators Cynthia Lummis and Angela Alsobrooks Say Bipartisan Work on Clarity Act Continues Despite Delays

The Clarity Act may be delayed — for now — but pro-crypto senators remain committed to the fight.

And not just Republicans: Democratic Senator Angela Alsobrooks accompanied conservative “Bitcoin Senator” Cynthia Lummis in assuring voters that work was being done on the bill.

Lawmakers were hoping a crucial vote on the long-awaited crypto market structure bill was to go ahead before a five-week recess but news dropped Friday that it was too little, too late. Now, the Senate will vote on the bill in September.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) August 7, 2026Senator Lummis releases statement now Clarity Act vote is delayed:

"There will be a time where I can say more, but for now, let me say this, we've come too far to quit"

"I will continue working with my colleagues to get this done — this fight is far from over"pic.twitter.com/ZLzc3pImrw

“We’ve worked for over a year on a bipartisan basis to protect consumers, limit deposit flight, fight illicit finance, and include a fair deal on ethics,” Alsobrooks said in a statement.

Lummis, who had previously blasted Democrats for holding back the bill, added: “There will be a time where I can say more, but for now, let me say this, we’ve come too far to quit. I will continue working with my colleagues to get this done — this fight is far from over.”

Passed last year in the House of Representatives, the Clarity Act started small but its text has grown over the months.

This is partly because of banking lobby chiefs locking horns with crypto exchanges over concerns they pay customers too much yield with their stablecoin products. But Democrats also have wanted more work on the ethics side of the bill.

A bill banning government officials from promoting and making money was circulating among lawmakers in July though some lawmakers said it still fell short.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) August 7, 2026

"We’ve worked for over a year on a bipartisan basis…We will continue our work — getting the Clarity Act right remains our goal."pic.twitter.com/3Hsn0282FU

Lummis last week said she was genuinely “struggling to understand” what else Democrats wanted for the bill. Some suggested they may have been playing politics ahead of the midterms.

A number of Democrats have criticized the way the Trump family has profited from digital asset ventures, such as the President’s memecoin, $TRUMP, and World Liberty Financial project.

Trump and the White House have always denied any conflicts of interest, and the President has also highlighted that Democrats have cashed in trading stocks.

This post Senators Cynthia Lummis and Angela Alsobrooks Say Bipartisan Work on Clarity Act Continues Despite Delays first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Coldcard Bitcoin Hack: Victims Report Median Loss of 1 BTC as Theft Tops $111 Million

New analysis of Bitcoin theft reports reveals that stolen funds overwhelmingly came from long-dormant wallets, with victims reporting a median loss of over one coin.

Data posted on X from Galaxy Research’s Alex Thorn looked at 250 victim reports and found the typical stolen coin had sat untouched for 3.5 years, and a striking 88% of pilfered funds were at least a year old.

By address, losses ranged from a median of 0.014 Bitcoin to a mean of 0.212 Bitcoin, while individual victims reported a median loss of 1.022 Bitcoin and an average of 4.04 Bitcoin — with one unlucky holder losing as much as 58.97 coins.

Hackers started by taking over $35 million in Bitcoin from wallets last week Thursday. Coinkite, which makes Coldcard, said that a firmware bug in Coldcard Mk3 devices — starting with version 4.0.1 in March 2021 — caused seed generation to fall back to a weak software Pseudorandom Number Generator instead of the hardware true random number generator, allowing hackers to essentially guess investor seedphrases.

The theft continued throughout the weekend while Coinkite and other Bitcoiners urged Coldcard users to immediately move their funds.

Galaxy Research said Friday that a total of $111 million has been confirmed stolen but the number could be much higher as it continues its research.

“We have many more coins we are vetting for confirmation — we think total losses likely exceed $130 million,” the firm wrote on X.

Since the attack, cautious investors have been moving their coins to other storage solutions — including exchanges.

Coinkite said in a statement this week that the bug in its software “silently went unnoticed” and “its potential impact grew with every release” of its products.

Days after the first hack, the company urged investors to update their software or move their funds off the popular hardware wallet.

This post Coldcard Bitcoin Hack: Victims Report Median Loss of 1 BTC as Theft Tops $111 Million first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Bitcoin Shrugs off Coldcard Hack and Clarity Act Delays, Price Chops Higher as Investors Buy ETFs

Bitcoin was trading higher on Friday — despite negative news circulating regarding the Clarity Act delay and a massive exploit of the popular Coldcard wallets.

The biggest cryptocurrency was trading above $65,170 today, up nearly 4% over the past week, despite significant headwinds against the asset.

JUST IN: $65,177 Bitcoin!

— Bitcoin Magazine (@BitcoinMagazine) August 7, 2026pic.twitter.com/ZZzVloKXjM

Little over a week ago, hackers started stealing millions in Bitcoin from Coldcard wallets after discovering a vulnerability in the product’s software. Some estimates put the amount of Bitcoin lost now at over $130 million.

The incident has rattled the BTC community that typically praises cold storage solutions.

And news dropped late Thursday night that the crypto market structure bill would be delayed until September as lawmakers break for recess. The bill, if approved, would set in stone digital asset regulation in the U.S. and would be bullish for the biggest cryptocurrency.

Still, Bitcoin made gains as investors carried on buying shares of the exchange-traded funds: BlackRock’s iShares Bitcoin Trust, and Morgan Stanley’s fund have both seen significant inflows this week, according to data from Farside Investors.

Bitcoin’s price has typically done well when investors have thrown cash at the products, managed by Fidelity, Grayscale, and other top asset managers.

Since the beginning of this week, $763.6 million in fresh cash has hit the funds.

Bloomberg Intelligence’s senior ETF analyst, Eric Balchunas, said the flows might not be related to the Coldcard hack, but it would make sense for investors to rotate into the highly successful products.

A firmware flaw in the popular Coldcard hardware wallets, built by Canadian company Coinkite, has allowed an attacker to guess weak private keys.

Millions of dollars in Bitcoin has been drained on a daily basis since the attack, and cautious investors have been moving their coins to other storage solutions — including exchanges.

This post Bitcoin Shrugs off Coldcard Hack and Clarity Act Delays, Price Chops Higher as Investors Buy ETFs first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Bitcoin ETFs Add Nearly $800 Million in the Wake of Coldcard Exploit

One of the biggest Bitcoin security stories of the year unfolded last week as a firmware exploit affecting certain Coldcard hardware wallets renewed industry debate around self-custody and operational security.

At the same time, another story was developing in the background.

Over the same seven trading days, U.S. spot Bitcoin ETFs attracted $790.6 million in net inflows, according to the Bitcoin For Corporations ETF Dashboard. More than $1.0 billion entered the funds while $212.7 million exited, resulting in one of the strongest weekly periods in recent months.

The two developments are not necessarily related. ETF flow data cannot tell us why investors bought Bitcoin. What it does tell us is what they actually did. And during a week dominated by security headlines, institutional capital continued flowing into regulated Bitcoin investment products.

One Red Day Didn’t Change the Trend

The seven-day flow chart tells a simple story. There was one notable setback.

On July 31, U.S. spot Bitcoin ETFs recorded $212.7 million in net outflows, the only negative session during the period.

After that, buyers returned almost immediately.

The next four trading sessions posted consecutive gains:

- Aug. 3: +$170.1M

- Aug. 4: +$207.8M

- Aug. 5: +$241.6M

- Aug. 6: +$99.4M

By the end of the week, the positive days had more than offset the lone selloff.

Instead of focusing on individual trading sessions, the seven-day view shows where capital ultimately moved—and during this period, it moved into Bitcoin.

BlackRock Continued to Lead the Way

As has been the case for much of the ETF era, BlackRock’s IBIT accounted for the majority of inflows.

Over the seven-day period:

- IBIT attracted $757.5 million in rolling net inflows.

- It extended its streak to four consecutive inflow days.

- On the latest trading day alone, it added $128.3 million.

Other issuers also participated.

Fidelity’s FBTC added $11.2 million on the latest session, while Bitwise’s BITB added $1.7 million. A handful of funds experienced modest outflows, but none came close to offsetting IBIT’s continued strength.

The result was a week where inflows remained broad enough to keep total ETF demand firmly positive.

What ETF Flows Can and Can’t Tell Us

ETF flows are one of the clearest windows into institutional participation in Bitcoin. They show where money moved. They do not explain investor motivation.

It’s impossible to conclude from one week’s data whether buyers viewed the Coldcard exploit as insignificant, saw it as an opportunity to buy, or simply continued executing long-term allocation strategies that were already in motion.

What can be observed is that institutional demand remained resilient during a week when Bitcoin security dominated industry headlines.

A security incident involving one custody solution is different from the broader investment case for Bitcoin, and ETF investors appeared comfortable continuing to allocate capital through regulated products.

Why This Matters

Bitcoin is no longer accessed through a single path. Some investors choose self-custody. Others hold Bitcoin through public companies. Many institutions access Bitcoin through regulated ETFs. Each approach comes with its own tradeoffs, operational considerations, and risk profile.

Events like the Coldcard exploit naturally increase attention on custody practices. At the same time, ETF flow data provides a useful lens into whether institutional demand is changing beneath the headlines.

This week, the numbers suggest demand remained intact.

Follow Institutional Bitcoin Demand in Real Time

Daily ETF flows have become one of the most important indicators of institutional participation in Bitcoin.

The spot Bitcoin ETF Dashboard tracks:

- Daily net inflows and outflows

- Rolling 7-day momentum

- Issuer-by-issuer rankings

- Estimated Bitcoin held by U.S. spot ETFs

- Market share and concentration trends

- Historical flow data across every issuer

Whether you’re monitoring institutional adoption, evaluating market structure, or simply trying to separate headlines from capital flows, the dashboard provides a real-time view of where money is moving.

Explore the live Bitcoin ETF Dashboard: https://bitcoinforcorporations.com/bitcoin-etf-dashboard/

As new flow data is published each trading day, the dashboard updates to help investors and corporate decision-makers track one of the market’s clearest signals of institutional Bitcoin demand.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

This post Bitcoin ETFs Add Nearly $800 Million in the Wake of Coldcard Exploit first appeared on Bitcoin Magazine and is written by Nick Ward.

CryptoSlate

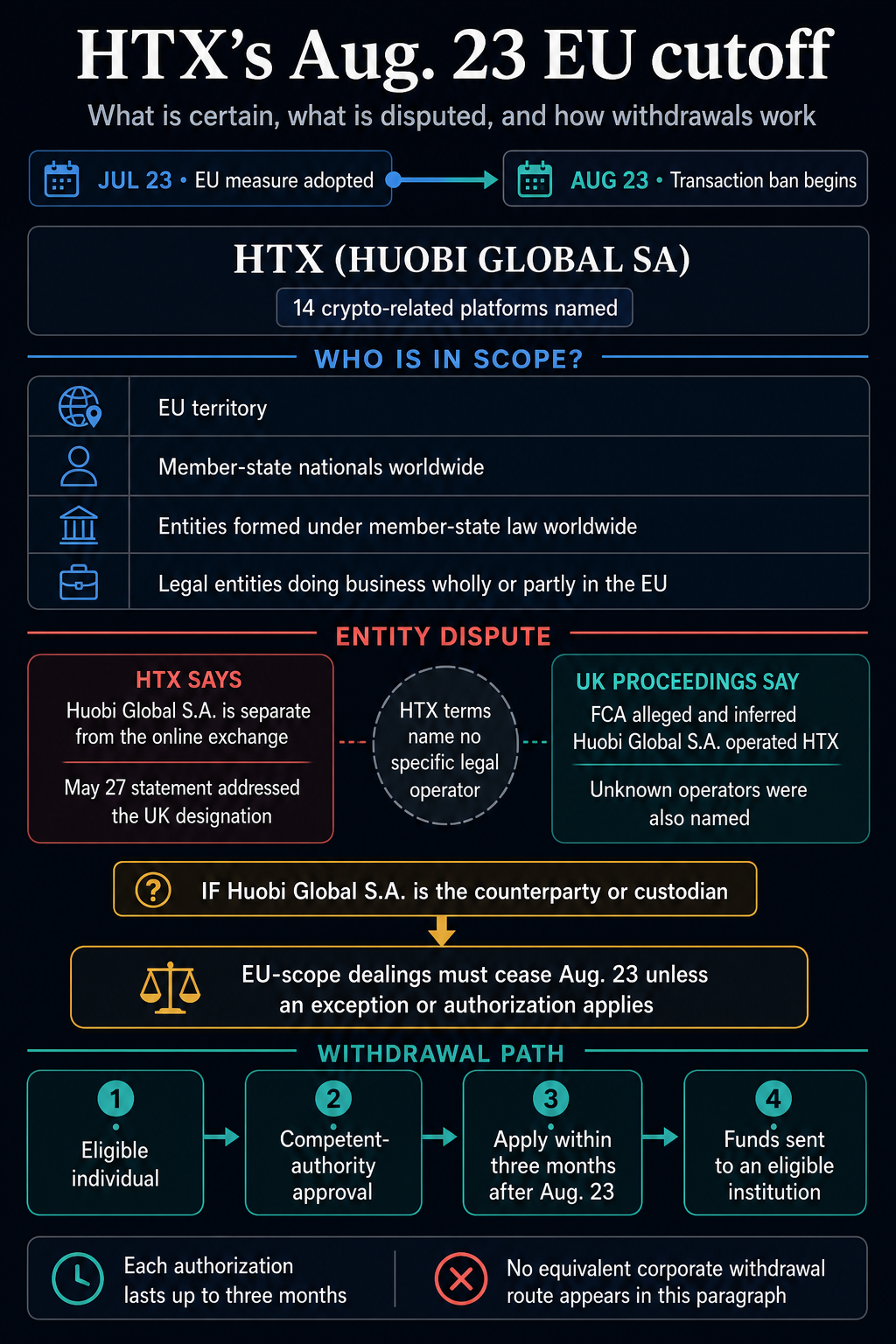

An EU transaction ban will take effect on Aug. 23 against the entity listed as “HTX (HUOBI GLOBAL SA),” giving people and businesses subject to the bloc's Russia sanctions regime a deadline to establish whether that company is involved in their dealings with the online exchange.

The restriction follows the jurisdictional reach of Regulation 833/2014. It covers conduct in EU territory, transactions by member-state nationals and entities constituted under member-state law wherever they operate, and activities of legal entities conducting business wholly or partly within the bloc.

The new measure adds HTX's combined label to Annex XLV Part A, whose named third-country entities are subject to restrictions on direct and indirect transactions. The Council of the EU said the package extends transaction bans to 14 crypto-related service platforms.

Why the entity dispute matters

HTX addressed a separate UK designation in a May 27 statement, saying Huobi Global S.A. was distinct from its online platform and that the UK action should not affect the exchange. The statement predates the EU regulation and does not state whether HTX takes the same position on the later European listing.

That account conflicts with allegations in UK proceedings. The Financial Conduct Authority's particulars of claim alleged and inferred that Huobi Global S.A. became HTX's owner, operator, and controller after a Seychelles predecessor was struck off. The regulator also pleaded alternatives against unknown owners and operators because, it said, HTX had not disclosed their identities.

A separate June interim decision by the High Court described Huobi Global S.A. as the company believed to own HTX and the exchange as believed to hold bitcoin traced in a fraud case. The defendants did not appear, and the ruling left ownership and custody for a later decision on the merits.

HTX's user agreement, updated June 18, defines “HTX Operators” as a changing group without naming a specific legal person, while saying customer crypto is held custodially by “us.” The terms also say users from every EU member state are ineligible for all services. That published restriction shifts the immediate question toward legacy balances and EU-scope counterparties rather than new account access.

For any account where Huobi Global S.A. is the counterparty or custodian, transactions within the regulation's scope must cease Aug. 23 unless an exception or authorization applies. The combined label alone leaves that corporate relationship unresolved for htx.com customers.

The regulation offers a case-by-case exit path for EU, EEA, and Swiss nationals, as well as holders of qualifying temporary or permanent residence permits. A member-state authority may authorize transactions strictly necessary to withdraw funds and close an account when the customer is ending the relationship and applies no later than three months after Aug. 23. Funds must go to an EU-incorporated credit or financial institution, or a third-country institution owned or controlled by one incorporated under member-state law. Each authorization may last up to three months. The text provides no equivalent corporate withdrawal route on its face.

The post Crypto holders face an August 23 deadline to figure out who controls HTX or risk violating EU sanctions appeared first on CryptoSlate.

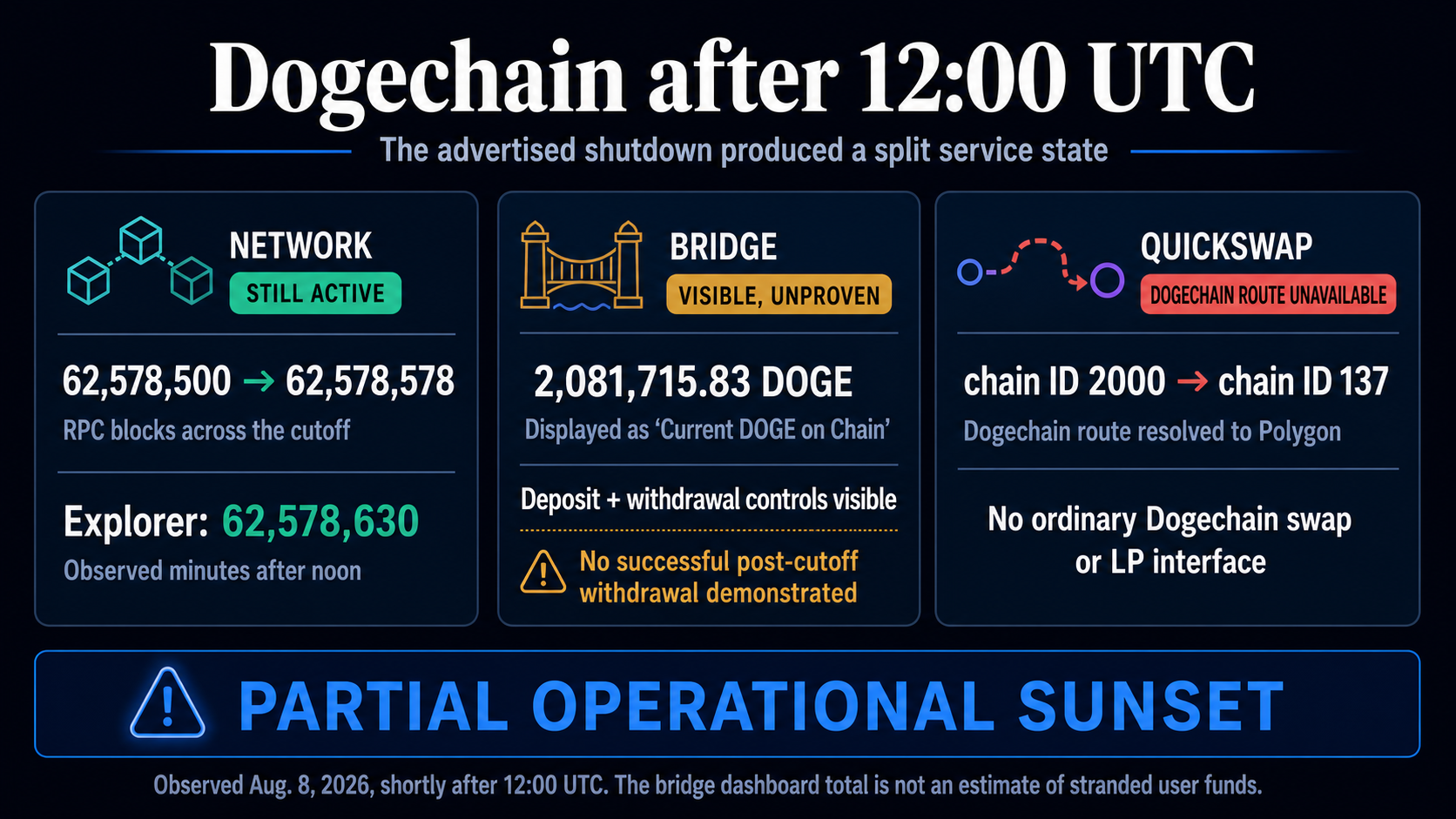

Dogechain, a separate Ethereum-compatible network from the Dogecoin blockchain, kept producing blocks after its announced 12:00 UTC shutdown on Aug. 8. Its project-run bridge page also remained online, while a Dogechain-specific QuickSwap route continued sending users to Polygon.

Dogechain announced the cutoff in July and warned that assets remaining on the chain might become inaccessible or permanently lost. The split in service availability after noon leaves the recovery path for those assets unresolved.

Blocks continued after noon

The official RPC, the endpoint apps use to communicate with the network, returned block 62,578,500 immediately before noon and block 62,578,578 less than two minutes after the deadline. The latter carried a 12:01:52 UTC timestamp.

The official explorer remained available minutes later and showed the chain at block 62,578,630, with recent blocks attributed to multiple miner addresses. That activity showed the network had not stopped producing blocks immediately after the cutoff, though it did not show whether all project-operated services still worked.

The official bridge interface was also visible after noon, with deposit and withdrawal controls. Its dashboard displayed 2,081,715.83 DOGE as “Current DOGE on Chain.” No successful post-cutoff withdrawal was demonstrated, however, and the dashboard total does not identify which balances are recoverable or controlled by users. It therefore cannot be treated as an estimate of stranded funds.

Dogechain’s bridge documentation describes an administrator-mediated process involving signatures and a service that executes transfers. Continued block production and a visible form do not prove that those operational components can still return DOGE. A holder’s ability to recover funds therefore depends on more than validators continuing to add blocks to the chain.

QuickSwap had warned users to withdraw assets and liquidity positions before the shutdown. Before and after noon, its Dogechain-specific route resolved to QuickSwap on Polygon, chain ID 137. The ordinary QuickSwap interface for Dogechain swaps and liquidity management remained unavailable through that route.

QuickSwap’s original Dogechain interface announcement said it supported trading, liquidity provision, and yield farms. Redirecting the chain-specific route to Polygon removes that ordinary interface for users trying to manage remaining Dogechain positions.

The immediate result was a partial operational sunset: block production, explorer access, and the bridge page persisted, while the tested QuickSwap route did not provide Dogechain access. Whether the bridge can still complete withdrawals and how much value is actually stranded remain unknown. Permanent loss is still Dogechain’s warning, not a demonstrated outcome.

As of press time, the explorer web page now fails to load.

The post Over 2 million DOGE sit trapped in limbo as Dogechain keeps printing blocks past its final deadline appeared first on CryptoSlate.

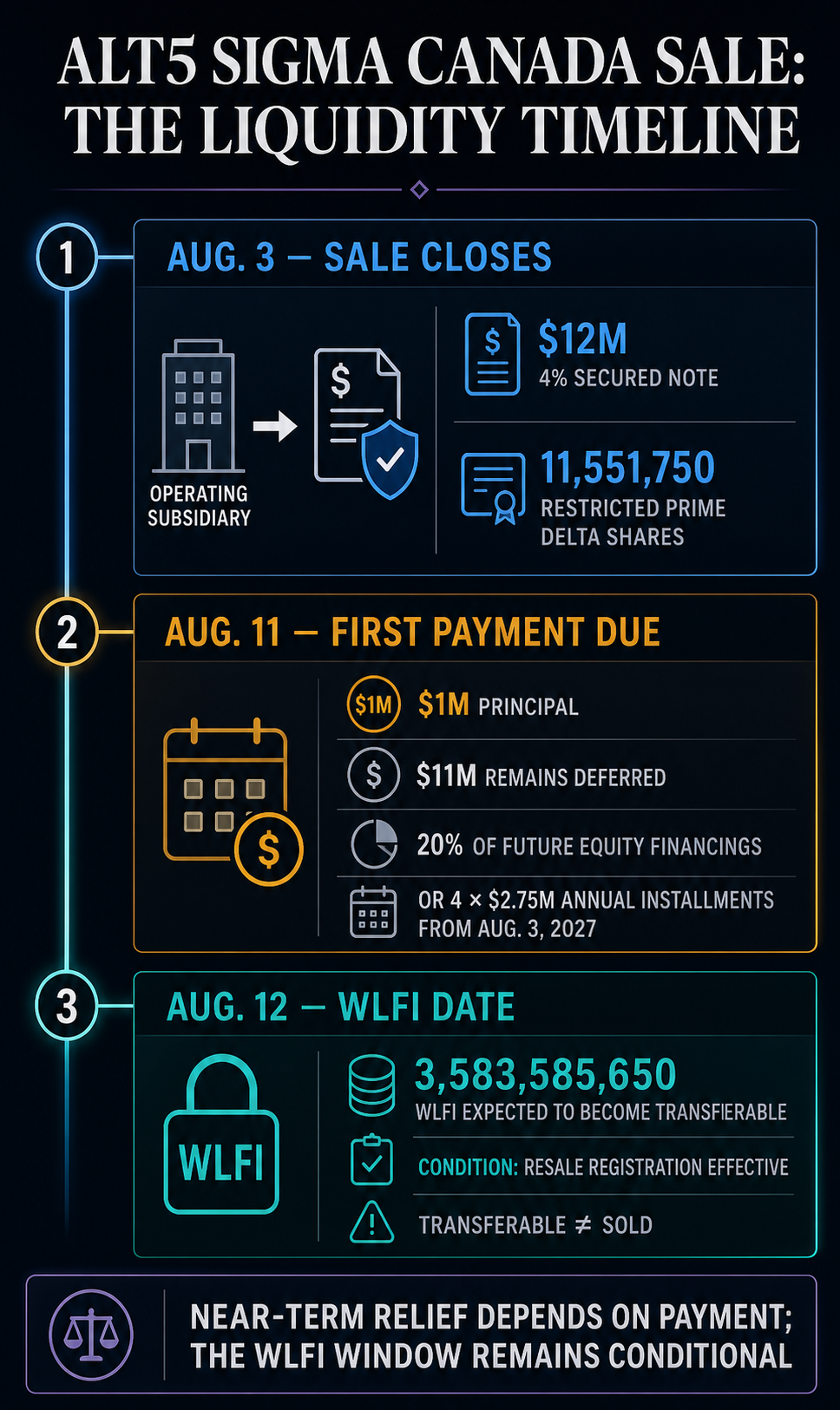

AI Financial Corp. has swapped ALT5 Sigma Canada for a secured note and restricted shares. As a result, only $1 million of note principal is due in the near term, while a separate, conditional WLFI transferability window approaches.

On Aug. 3, the company sold its indirect, wholly owned subsidiary to Prime Delta. Under the terms disclosed Aug. 7, AI Financial received a $12 million secured promissory note and 11,551,750 restricted Prime Delta shares. Prime Delta must pay the first $1 million of note principal on Aug. 11.

Prime Delta must pay the remaining $11 million from 20% of its post-closing equity financings. If those payments do not retire the balance, four annual installments of $2.75 million will begin Aug. 3, 2027. In addition, the note carries 4% annual interest. All of Prime Delta's assets secure it, and three third parties guarantee it.

Overall, the deal exchanges an operating subsidiary for mostly deferred consideration rather than cash at closing. ALT5 Sigma Canada generated $23.5 million of revenue and a $3.3 million net loss in 2025, after recording $15.5 million of revenue and a $600,000 profit in 2024.

Meanwhile, in its May 18 report for the quarter ended March 28, AI Financial disclosed $10.5 million of cash and $12.3 million of operating cash use for the period. Moreover, the company also reported a $271.3 million loss from continuing operations, a working-capital deficit and substantial doubt about its ability to continue as a going concern. Against that baseline, the sale creates a near-term claim on $1 million but leaves most of the note dependent on future financing proceeds or later installments.

The WLFI date remains conditional

On June 10, management said its financial position had improved, pointing to its World Liberty Financial token holdings. In that update, AI Financial expected 3,583,585,650 WLFI to become transferable Aug. 12, subject to the effectiveness of a resale registration statement covering shares issued to World Liberty Financial and shares underlying the warrants granted to it.

However, AI Financial also said token availability should not be read as an intention to sell. Transferability would create an option, not cash by itself.

The company's May 18 quarterly report said it had not yet filed the required resale registration statement. At the same time, the SEC submissions available through Aug. 8 contained no public filing showing that the condition had become effective.

Finally, the transaction does not remove AI Financial's near-term liquidity pressure. The first test is whether Prime Delta makes the $1 million payment due Aug. 11; meanwhile, the next day's larger WLFI liquidity window remains conditional.

The post Swapping a $23M business for $1M cash while banking on locked WLFI tokens shows how dire crypto balance sheets have become appeared first on CryptoSlate.

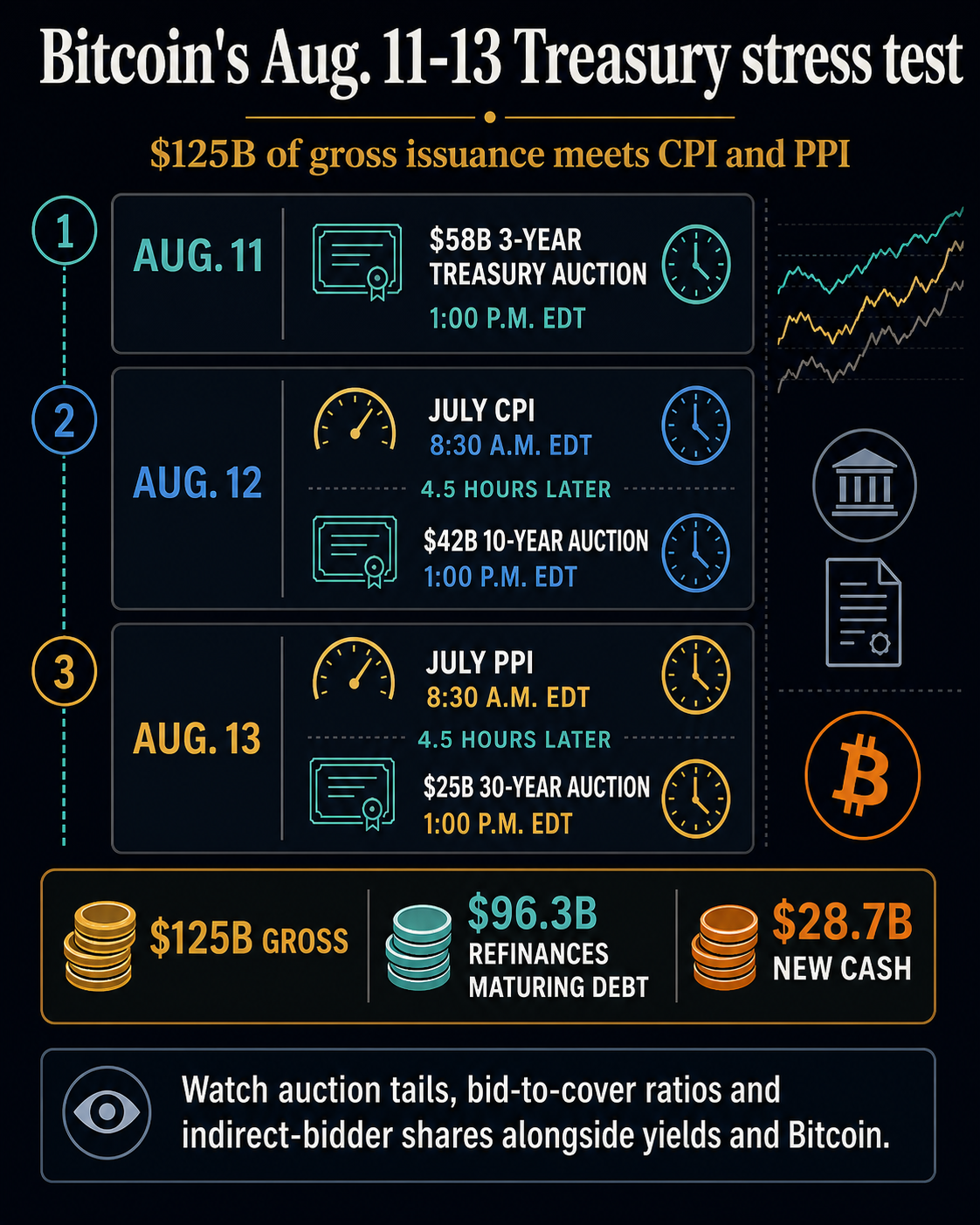

The Treasury auctions will total $125 billion from Aug. 11 through Aug. 13, while two inflation reports land hours before the corresponding 10-year and 30-year sales. The sequence will show whether softer bond demand and any resulting rise in yields coincide with pressure on Bitcoin.

The Treasury refunding plan starts with $58 billion of 3-year notes at 1 p.m. EDT on Aug. 11. It continues with $42 billion of 10-year notes at the same time on Aug. 12 and $25 billion of 30-year bonds on Aug. 13. All three settle Aug. 17.

The gross total is not a $125 billion liquidity drain. About $96.3 billion will refinance privately held debt maturing Aug. 15, leaving approximately $28.7 billion of new cash to raise from investors.

The Bureau of Labor Statistics calendar places July CPI at 8:30 a.m. EDT on Aug. 12, four and a half hours before the 10-year auction. July PPI arrives at 8:30 a.m. the following day, the same interval before the 30-year sale. Together, the releases and Treasury auctions create a tightly timed test of bond demand and Bitcoin’s response.

At the latest official business-day cutoff on Aug. 7, the Treasury's par-yield curve showed 3-year, 10-year and 30-year yields at 4.25%, 4.65% and 5.19%, respectively. A CryptoSlate snapshot retrieved Aug. 9 at 11:25:23 UTC showed Bitcoin at $64,928.71; the live price is timestamp-sensitive.

The Sunday Bitcoin quote and Friday Treasury fixing do not provide simultaneous market evidence. Any link between yields and Bitcoin must be judged around the same inflation releases and auction results.

July sets the demand bar for Treasury auctions

| Tenor | July high yield | Bid-to-cover | Indirect share |

|---|---|---|---|

| 3-year | 4.179% | 2.60 | 67.50% |

| 10-year reopening | 4.580% | 2.59 | 81.49% |

| 30-year reopening | 5.058% | 2.44 | 77.74% |

The July results set a baseline for the August Treasury auctions.

FinancialJuice reported that the July 3-year and 10-year sales stopped through their when-issued yields by 0.6 basis point each, while the 30-year sale stopped through by 0.3 basis point. Treasury does not publish when-issued levels, so the tail comparison is a secondary benchmark rather than an official statistic.

A comparatively weak August result would combine a positive tail with a lower bid-to-cover ratio and lower indirect-bidder share than the matching July sale. One reading alone is not decisive, and auction size plus the July reopening status of the longer securities affect the comparison.

The sharper Bitcoin risk case is conditional: inflation pushes yields higher, several auction metrics point to softer demand, yields remain elevated, and Bitcoin falls in the same event window. Firm auctions or a stable Bitcoin price would weaken that case. New York Fed research found Bitcoin broadly disconnected from monetary and macro news in its historical sample, underscoring why the Treasury auctions should be read as a test of conditions, not an automatic sell signal for Bitcoin.

The post Yields are spiking toward 5.2%, but history shows Bitcoin might completely ignore Wall Street’s $125 billion stress test appeared first on CryptoSlate.

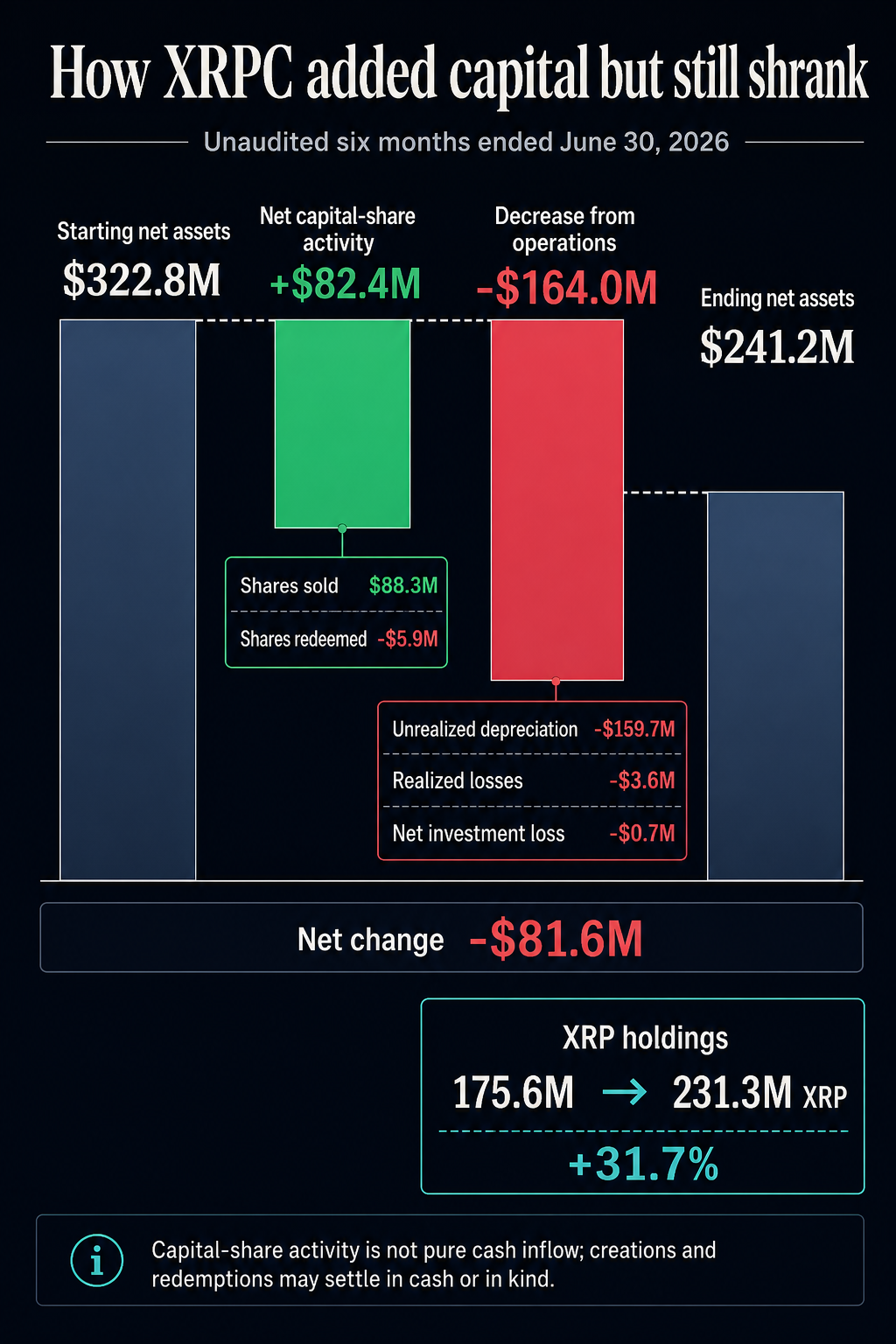

Canary Capital’s Canary XRP ETF (XRPC) ended the first half of 2026 with $81.6 million less in net assets even after capital-share transactions added a net $82.4 million, showing how falling asset values can overwhelm growth in an exchange-traded fund.

The fund’s unaudited Form 10-Q, filed Aug. 7, showed net assets declining from $322.8 million at Dec. 31, 2025, to $241.2 million at June 30, 2026.

The accounting bridge is direct: capital-share transactions increased net assets by $82.36 million, but the accounting decrease from operations, primarily unrealized XRP depreciation, reduced them by $164.00 million. The difference was the $81.65 million decline in net assets over the six-month period.

XRPC attributed $88.26 million to shares sold and $5.90 million to shares redeemed. Because authorized participants place XRPC’s creation and redemption orders and can settle them in cash or in kind, the $82.36 million is not equivalent to cash inflow and does not directly measure retail-investor buying. The filing does not disclose the period’s cash-versus-in-kind split.

Unrealized depreciation overwhelmed net share activity

Unrealized depreciation accounted for $159.70 million of the $164.00 million decrease from operations. The balance comprised $3.59 million of realized losses and a $716,898 net investment loss. All are unaudited figures for the full six months, not the second quarter alone.

The fund’s redemptions therefore did not exceed its new share activity. Net capital-share activity remained positive, but the accounting decrease from operations was nearly twice as large as the value added through capital transactions. Unrealized XRP depreciation, rather than fees or realized losses, dominated that decrease.

The contrast is clearest in XRPC’s holdings. The trust held 231.3 million XRP at June 30, up 55.7 million XRP, or 31.7%, from 175.6 million at the end of 2025. The quantity of XRP rose while unrealized depreciation reduced the dollar value recognized in the portfolio.

The fund also sold 3.93 million XRP to fund share redemptions during the first half, recording a $3.26 million realized loss on those sales. That was a loss recognized by the fund, not a measure of losses realized by individual XRPC shareholders.

XRPC’s filing captures two simultaneous movements: net capital-share activity and XRP units both increased, while depreciation cut the value of the larger token pool. The result was a fund with more XRP but $81.6 million less in net assets at midyear.

The post Investors poured $82 million into Canary’s XRP ETF, but falling prices erased double what they put in appeared first on CryptoSlate.

CryptoTicker.io

Institutional demand for Bitcoin and Ethereum appears to be returning—but anyone looking only at crypto prices might not notice.

U.S. spot Bitcoin and Ethereum ETFs attracted approximately $1.1 billion in combined net inflows during the first full trading week of August. Despite this apparent wave of institutional demand, Bitcoin remains below $65,000 while Ethereum is struggling to move decisively beyond $1,900.

The disconnect raises an important question: If institutions are buying again, why are crypto prices barely moving?

Bitcoin and Ethereum ETFs Record a Strong Week

According to updated data from Farside Investors, U.S. spot Bitcoin ETFs recorded approximately $865 million in net inflows between August 3 and August 7.

Some earlier estimates placed the weekly figure closer to $853.5 million because of differences in reporting times and later data revisions. Either figure represents a significant reversal from the previous week’s outflows.

The most notable part was the consistency. Bitcoin ETFs recorded positive net flows during all five trading sessions:

August 3: $170.1 million

August 4: $211.5 million

August 5: $244.4 million

August 6: $137.6 million

August 7: $101.7 million

BlackRock’s IBIT accounted for approximately $693.5 million of the weekly total, representing around 80% of all Bitcoin ETF inflows.

Ethereum ETFs also had one of their strongest weeks in months. Farside’s Ethereum ETF data shows approximately $244 million in net inflows, despite beginning the week with a small outflow.

Together, Bitcoin and Ethereum ETFs attracted more than $1.1 billion.

Why Did Bitcoin and Ethereum Barely React?

The first explanation is scale.

Bitcoin currently has a market capitalization of approximately $1.3 trillion. While $865 million is a substantial amount of institutional capital, it remains relatively small compared with Bitcoin’s total valuation and daily global trading volume.

ETF demand also represents only one part of the market. Selling on centralized exchanges, over-the-counter desks and derivatives platforms can absorb the buying pressure created by ETF inflows.

In other words, ETFs may be buying, but other investors are still selling.

This could explain why Bitcoin has remained trapped around $64,000 to $65,000 instead of immediately breaking higher. The inflows may be supporting the price and preventing a deeper correction without being large enough to overcome the supply waiting near resistance.

Ethereum has reacted slightly better. ETH climbed from approximately $1,845 at the beginning of the week to around $1,914. However, it has yet to break decisively above the $1,920 resistance area or challenge the psychological $2,000 level.

ETF Inflows Do Not Always Mean Immediate Price Growth

Another factor is how institutional investors use ETFs.

Not every ETF purchase represents a simple bullish bet on rising crypto prices. Some professional investors use ETF shares as part of hedged positions, arbitrage strategies or longer-term portfolio allocations.

This means ETF inflows can increase without generating the same immediate price pressure associated with direct spot purchases from investors who withdraw their coins from exchanges.

Institutional accumulation also tends to be less emotional than retail activity. Large investors can gradually build positions over several weeks instead of chasing a sudden breakout.

The recent inflows may therefore be an early signal rather than an immediate price catalyst.

Is This Silent Accumulation or a Warning?

The optimistic interpretation is that institutions are quietly accumulating Bitcoin and Ethereum while prices remain relatively low.

Five consecutive days of Bitcoin ETF inflows suggest that demand is not based on a single large transaction. The concentration of capital in Bitcoin and Ethereum also shows that institutional investors continue to favor the two largest cryptocurrencies over more speculative altcoins.

If these flows continue, available selling pressure could eventually weaken and allow prices to move higher.

However, there is also a more cautious interpretation. If more than $1.1 billion in ETF inflows cannot push Bitcoin beyond $65,000 or Ethereum toward $2,000, the market may be facing stronger overhead supply than the headline numbers suggest.

In that scenario, ETF demand is being absorbed by sellers rather than creating a genuine breakout.

What Happens Next?

For Bitcoin, the $65,000 to $66,000 area remains the immediate test. A sustained break above this zone, supported by another week of positive ETF flows, would suggest that institutional demand is finally beginning to influence the broader market.

Failure to break higher could keep Bitcoin trapped inside its current range. Losing the $64,000 area would weaken the argument that ETF demand is providing reliable support.

Ethereum must first establish itself above approximately $1,920. A successful breakout could open the path toward $2,000, while rejection would leave ETH vulnerable to another test of the $1,880 to $1,860 area.

The $1.1 billion ETF week is undoubtedly positive, but it has not yet produced a confirmed market breakout. For now, institutional demand appears to be supporting crypto prices—not driving them.

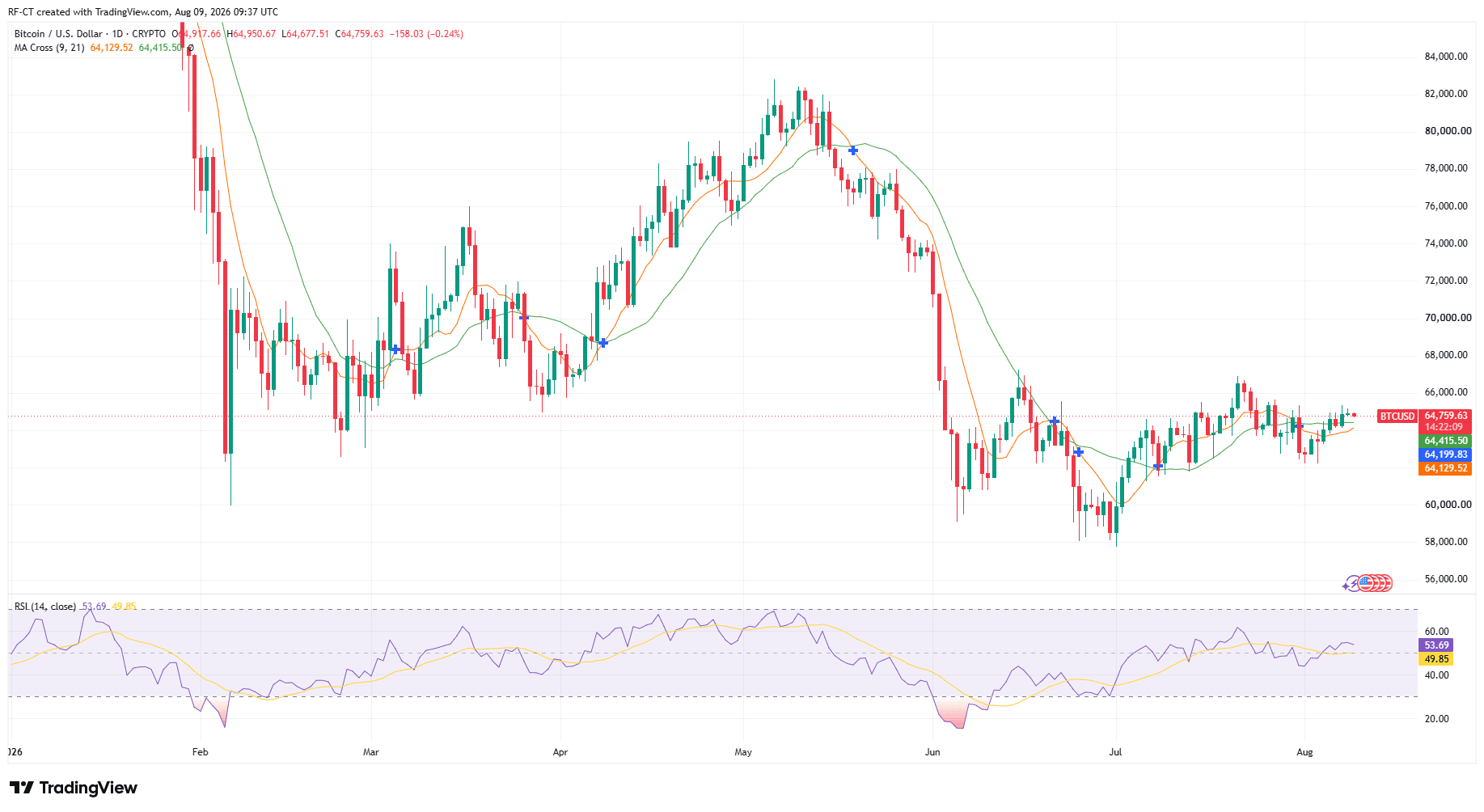

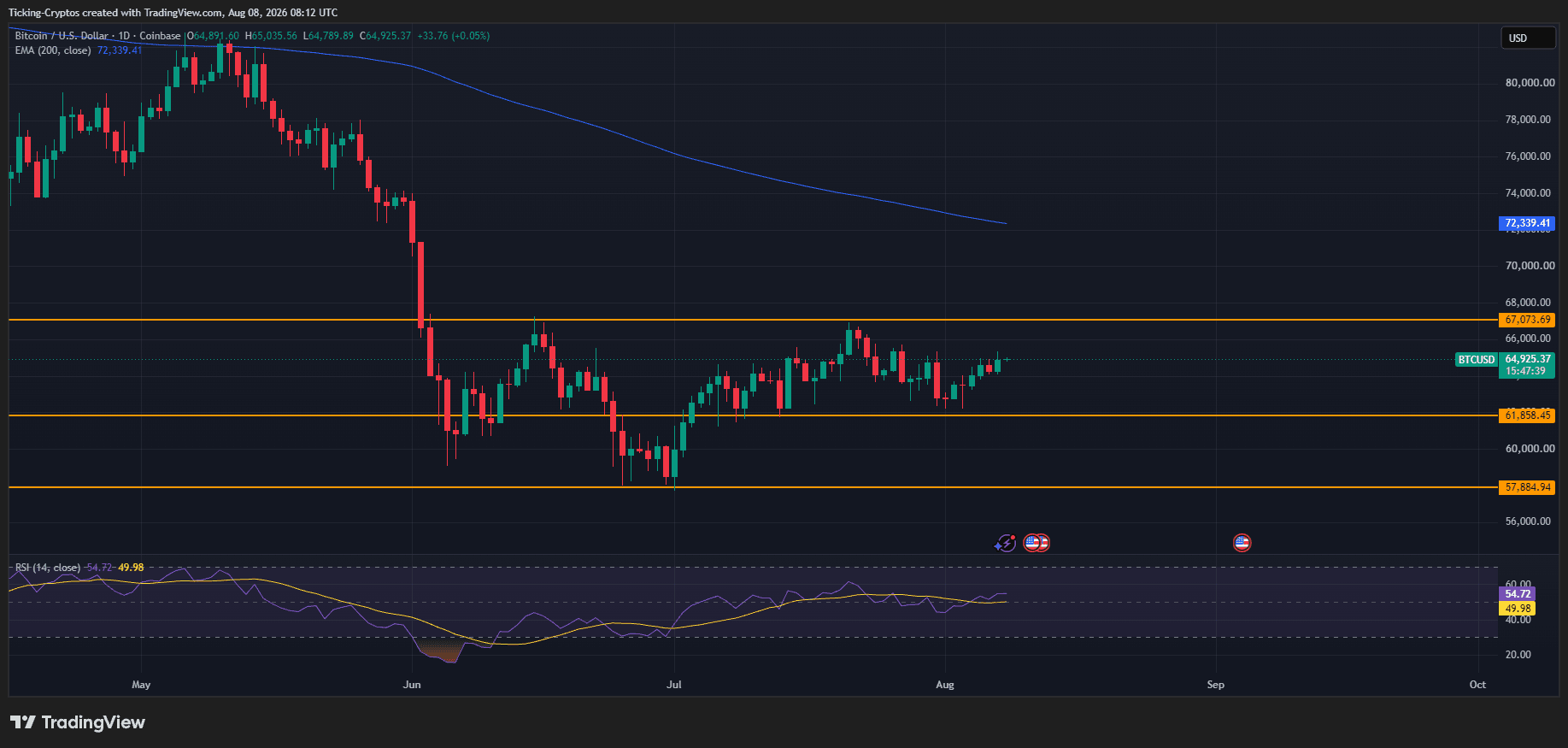

Bitcoin is trading around $64,925 on the daily chart, barely moved on the session at +0.05%. That flat close hides how tight the setup has become. Price is pressed up against the upper half of a two month range, and the levels above and below are close enough that the next daily candle could set the direction for weeks.

The chart has been range bound since the June breakdown. Bitcoin lost the low $70,000s in early June, dropped hard toward the high $50,000s in July, and has been grinding back up ever since. Now it is back at the top of that range with the same question in front of it: does resistance break, or does the range hold again?

Why Is $67,000 The Level Bitcoin Has To Break?

The $67,073 area is the single most important line on the daily chart right now.

- It capped the bounce in mid June after the crash.

- It capped the rally again in early August, where Bitcoin pushed toward it and got rejected.

- It sits directly above the current price, which means every bid from here is buying into known supply.

Two rejections from the same zone turn it into a reference point that both sides of the market are watching. $BTC coin is targeting it, and a daily close above it changes the structure of this chart.

Until that happens, the move off the July low is a range recovery, not a trend reversal.

What Happens If Bitcoin Breaks Above The Resistance?

A clean break and hold above $67,073 opens the door to $74,000.

That is not an arbitrary number. The $74,000 area is where the June sell off began, the origin of the large breakdown candle that took Bitcoin out of the low $70,000s. There is very little structure between $67,000 and $74,000 because the drop through that zone was fast and vertical. Price tends to move quickly back through areas it fell through quickly.

So the bull path is simple:

- Daily close above $67,073 confirms the breakout.

- $74,000 becomes the next meaningful target and the next major resistance.

- A retest of the broken $67,000 zone as support would strengthen the case.

One caveat worth keeping in mind: the 200 EMA sits at $72,339 and is still sloping down. Bitcoin would run into it on the way to $74,000. That makes the $72,000 to $74,000 band the real test of whether this is a genuine trend change or another lower high.

Where Does Bitcoin Go If $64,000 Fails To Hold?

The downside map is more detailed, and that is exactly why the $64,000 area matters.

If $Bitcoin cannot stay above $64,000, the sequence of supports below is:

- $61,858 first, the range floor that has been defended repeatedly since June.

- $60,000 next, the round number where the July basing action took place.

- $57,884 last, the July low and the deepest level on this leg.

Losing $61,858 would be the more serious signal. That line has held every meaningful test for two months. A daily close below it would turn the entire July recovery into a failed bounce and put the July low back in play.

What Do The Indicators Say About Bitcoin Right Now?

The momentum picture is neutral, and that is worth saying plainly instead of forcing a bias.

- RSI is at 49.98, sitting right on the midline. There is no overbought stretch to unwind and no oversold spring to load.

- RSI is below its own moving average at 54.72. Momentum has cooled since the early August push, even though price has held up.

- The 200 EMA at $72,339 is above price and declining. On a higher timeframe, Bitcoin is still in a downtrend.

That combination describes a market that has stopped falling but has not started trending. It is the classic profile of a range that resolves with a breakout, not a slow drift.

What Is Driving Bitcoin Right Now?

The macro backdrop is doing the heavy lifting this week. The July US jobs report came in far weaker than expected, with the economy shedding jobs against forecasts for solid growth and the unemployment rate ticking higher. Weak labour data pushes rate cut expectations forward, and futures markets moved to price in a meaningful chance that the Fed pauses at its September meeting.

Lower rates are generally supportive for risk assets, and Bitcoin caught a bid on the news. That is what carried price back toward the top of the range. Whether it is enough to break $67,073 is the open question, because the last time Bitcoin reached this zone it was rejected.

What Should Traders Watch Next?

The setup reduces to two lines and a bit of patience.

- Above $67,073 on a daily close: structure flips, $74,000 becomes the target, with the 200 EMA around $72,339 as the checkpoint on the way.

- Below $64,000: momentum shifts down, with $61,858, $60,000 and $57,884 as the levels in order.

- Between the two: the range is still the range. Chasing moves inside it has been punished repeatedly since June.

Volume on the breakout attempt matters more than the first candle that pokes through. A high volume daily close above resistance is a signal. A thin wick above it that closes back inside is the same rejection Bitcoin has already produced twice.

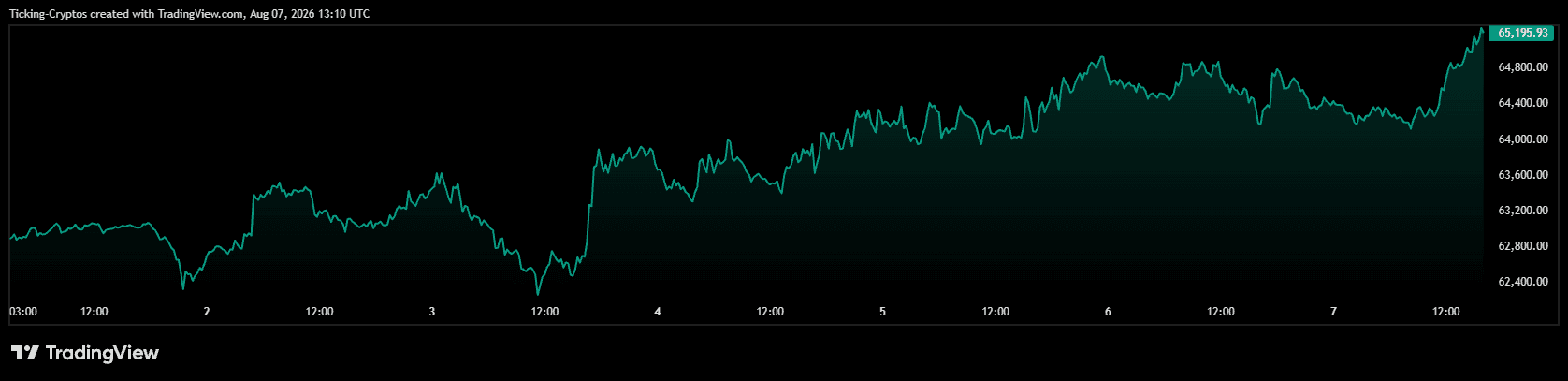

Bitcoin is trading around $65,167 on Coinbase, up roughly $900 on the day for a gain of about 1.4%. That comes less than 24 hours after the US Senate confirmed it would not vote on the CLARITY Act before the August recess.

Bad news for regulation. Green candles anyway. Here is what the chart actually says.

What Is Bitcoin Price Doing On The Chart Right Now?

The daily chart shows a market that has stopped falling, not a market that has broken out.

- $Bitcoin sits at roughly $65,167, having opened at $64,267 and printed a daily high near $65,231.

- Price is trading inside a well-defined range with resistance at $67,074 and support at $61,858.

- Below that sits a deeper floor at $57,885, which marked the summer low.

- From here, resistance is only about 2.9% away. Support is roughly 5.1% below. The risk-reward from the middle of a range is rarely attractive.

- The 200 EMA sits at $72,417 and is still sloping downward. Bitcoin is trading roughly 10% beneath it.

That last point is the one that matters most. As long as price is below a falling 200 EMA, the higher timeframe trend is still down. What we are watching is a recovery inside that downtrend, not a reversal of it.

Momentum supports the short-term bounce without confirming anything bigger. The RSI reads about 55.8 against its own moving average near 49.8. Momentum has crossed higher, which is constructive, but 55.8 is a mid-range figure. There is no exhaustion here, and no conviction either.

Why Did The Market Ignore The CLARITY Act Delay?

Three reasons, and none of them are especially bullish on their own.

- The delay was already priced in. Traders had been discounting the odds of a pre-recess vote for over a week. Prediction market odds on the bill passing this year had already fallen from around 30% to roughly 15% before the confirmation landed. By the time Thune spoke, the disappointment was old news.

- Bitcoin is trading on macro, not on Washington. June CPI came in at 3.5% year over year with core inflation easing, and the market is positioning around the latest US jobs data and what it implies for Fed policy. Rate expectations are moving this tape far more than committee negotiations are.

- The delay is not a rejection. The bill cleared Senate Banking in May and merged text landed in July. Nothing was voted down. The calendar moved, not the substance.

There is a fourth reason worth naming: the CLARITY Act was never a near-term price catalyst for Bitcoin specifically. It matters far more for altcoin classification, exchange listings and US custody rules than it does for the asset with the clearest regulatory status in the market.

Is The Whole Market Actually Bullish Here?

This is where the popular framing gets ahead of the data.

- $BTC is still well below its May peak near $82,000.

- It is trading about 10% under a declining 200 EMA.

- It has not reclaimed range resistance at $67,074, a level it has been rejected from repeatedly since June.

- Broader risk assets are outperforming it. Equities have pushed to fresh record highs this month while Bitcoin has added only a couple of percent, which is relative weakness, not leadership.

A better description of the current tape is resilient. Bitcoin absorbed a genuine regulatory disappointment without breaking down, and it did so while sitting above its June and July lows. That is meaningful. It is not the same thing as a bull market.

Bitcoin Price Prediction: What Levels Matter Next For Bitcoin Price?

Keep it simple and watch three prices.

- $67,074. Range resistance. A daily close above it turns the structure constructive and opens the path toward the 200 EMA.

- $72,417. The 200 EMA. Reclaiming this on a closing basis is what would actually flip the higher timeframe trend. Until then, rallies are counter-trend.

- $61,858. Range support. Losing it puts the summer low at $57,885 back in play quickly.

The realistic base case is continued chop between $61,858 and $67,074 into September, when the Senate returns and the CLARITY Act gets its next window. If the bill clears then, the assets most likely to react are not Bitcoin but the altcoins whose legal status the bill would finally define.

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text.

The most important piece of crypto legislation in the United States was supposed to move this week. It did not. Senate Majority Leader John Thune confirmed late Thursday that the CLARITY Act will not get a floor vote before lawmakers leave for the August recess, pushing the whole thing into September.

For an industry that has spent more than a year lobbying for exactly this vote, the timing stings.

What Exactly Happened With The CLARITY Act?

The short version is that the window closed without a deal.

- Thune confirmed the Senate is delaying a vote until lawmakers return from the August recess.

- He said the bill would be queued up first thing when the chamber reconvenes in September.

- Procedural steps such as filing cloture could still happen, but the actual floor vote is off the table until next month.

- The delay reverses expectations set by Senate Banking Committee Chair Tim Scott, who had pushed for a vote before recess.

The bill itself is not dead. It cleared Senate Banking 15 to 9 back in May, and negotiators released merged text in July. What it lacks is 60 votes.

Why Did The Senate Push The Vote To September?

Ethics. Specifically, whose crypto holdings get scrutinised.

- Democrats declined to agree to a time agreement that would have cleared a path to the floor before recess.

- The sticking point is a proposed divestment rule from Senators Thom Tillis and Ruben Gallego, which would force the president and senior federal officials to sell stakes in digital asset companies above a certain size threshold.

- Democrats are also pushing for changes to enforcement provisions and to the commodities section of the bill.

- Illicit finance concerns remain unresolved, with some lawmakers arguing the bill leaves law enforcement without adequate tools. The industry disputes that reading.

- Banks and crypto firms are still fighting separately over rules on rewards paid on stablecoin balances.

Republican support has also wavered, which means this is not a simple one-party holdout.

What Does The Delay Mean For Crypto Markets?

Mostly it means the uncertainty premium stays on the table for another month.

- Prediction market odds on the bill being signed into law this year dropped sharply, falling to roughly 15% from around 30% a week earlier.

- The regulatory question of who supervises what, the SEC or the CFTC, stays open. That keeps listing decisions, custody arrangements and token classifications in limbo for US firms.

- September puts the bill uncomfortably close to the November midterms, when floor time gets scarce and every vote becomes a campaign issue.

Industry reaction was disappointed but not defeated. The Digital Chamber and the Crypto Council for Innovation both framed the delay as a setback in timing rather than direction.

What Happens Next For The CLARITY Act?

Three plausible paths from here:

- Talks continue through August. The White House and congressional leaders hammer out ethics language during recess, and the Senate votes early in September.

- Revised text lands first. Senators return with new language on ethics, stablecoin yields and enforcement, then schedule a fresh procedural vote.

- It slips again. A crowded autumn calendar and campaign season squeeze the bill out, and the whole thing rolls into 2027.

Even if the Senate passes it, the bill goes back to the House before it reaches the president's desk. That is another step, and another calendar.

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text.

Nikita Bier announced on Wednesday that he is stepping down as X's head of product. After a little more than a year, in his own words: "time to pass the torch and demote myself to my natural state: a poster." He stays on as an adviser.

Crypto circles have been treating his exit as a turning point since yesterday. That overstates it — Bier was not the crypto lead at X. The timing is interesting all the same, for one concrete reason: he leaves a few weeks after X launched its payments product, and the question of whether cryptocurrencies will ever arrive there remains unanswered.

What Bier actually built at X

Bier took over product in July 2025. Across roughly 400 days, around 30 new products shipped under his responsibility, and practically every major part of the platform was reworked: the timeline feed, the Android app, new-user onboarding, the notification system, chat and direct messages. TechCrunch has the detail.

His responsibilities are being split rather than refilled: design, core product engineering and mobile engineering go to three different leads. For a company standing up a financial service, that is a notable choice — payment products tend to depend on one hand holding the whole thing together.

The crypto connection: two points, both documented

The first is Smart Cashtags, announced in January 2026. Cashtags have been X's shorthand for tickers for years — a dollar sign in front of a symbol. The smart version was meant to turn that into a financial toolkit. That feature is still described in reporting as the most likely entry point through which cryptocurrencies could reach the platform.

The second point is less flattering. Also in January, X changed its algorithm, and the consequences hit the platform's crypto corners harder than most: shifted reach, a noticeable rise in automated accounts, and a discussion culture that got worse for many users. Anyone following on-chain debate in real time follows it mostly on X — so the complaints were loud.

X Money is running — without crypto

At the end of July, X rolled out its payments product in the US, initially by invitation for Premium and Premium+ subscribers. Two years of groundwork sit behind it, including money transmitter licences across most US jurisdictions. What it does:

| Capability | Status, August 2026 |

|---|---|

| Peer-to-peer payments, wires, bill pay | available |

| Direct payroll deposit into the X account | available |

| Visa debit card, physical and virtual, Apple Wallet | available |

| Yield on balances | up to 6 percent a year |

| Cash back on qualifying purchases | 3 percent |

| Cryptocurrencies | not included |

The figures and terms are documented at crypto.news. Six percent on balances is an aggressive offer, and it shows what this is about first: gathering deposits, not selling bitcoin.

That is the real finding of the week. Elon Musk has talked about crypto for years and says he holds bitcoin, ether and dogecoin — and the payments product of his own platform launches with Visa and interest. Not with a wallet.

Why that makes sense

A payments product needs licences, and licences come more easily without crypto. In the US, X acquired money transmitter licences state by state. Any crypto capability would have extended that process and brought additional supervisors into it. Launching without them is not a rejection; it is the order every payment provider chooses.

The US Senate wrote to Musk in April about the planned launch and asked questions about oversight — a preview of how closely this will be watched once digital assets are added.

For European users it is further away still

X Money exists only in the US so far. An EU launch would require an e-money licence and, once cryptocurrencies were involved, a MiCA authorisation as a crypto-asset service provider on top. Neither is known to have been applied for.

For a sense of how long that takes: Coinbase received its MiCA licence via Luxembourg in June 2026, after a process that ran for months. The last MiCA transition period expired on 1 July 2026 — since then that authorisation decides who may offer crypto services in Europe at all. Binance withdrew its application in June and is winding down its EU business accordingly.

So anyone waiting to buy bitcoin through X in Europe is waiting on two approvals, neither of which is in progress. Realistically, that is not a 2026 story.

What to take away

A product chief leaving is not, by itself, news that moves a portfolio. What it makes visible is:

- The platform where the crypto debate happens is building a bank — without crypto. That is a more realistic signal about the coming months than any announcement.

- Smart Cashtags remain the thing to watch. If cryptocurrencies come to X, they will likely come there, and likely no earlier than late 2026.

- A feed is not a broker. Buying crypto requires an authorised platform — and those exist today, with names and supervisors.

The concrete step, if you were considering it anyway: check whether your exchange is still permitted to operate under regulation in Europe after 1 July. Since this summer that is no longer a formality but the dividing line between providers who stay and providers who leave. The overview is in our comparison of regulated crypto exchanges. If you buy regularly rather than speculate, the terms are in our guide to buying bitcoin.

And the lesson that outlasts this personnel change: reach does not replace a licence. X built the two separately — first the users, then, slowly and laboriously, the permission. That the crypto capability sits at the end of that sequence rather than the start says more about the maturity of this industry than any announcement on the platform itself.

(As of 6 August 2026. This article is not investment advice. Details of X Money products and terms refer to the US market at the time of publication.)

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text. The feature image was generated with AI.

Decrypt

The bank has now set 2030 targets for Uniswap, Aave, Morpho and Chainlink, all resting on one 37x forecast for DeFi growth.

The exchange says it has recovered $48.4 million and frozen $30.5 million more, a fraction of what the Lazarus Group took in February 2025.

The breakaway chain drew just 2.53% of mining support, leaving its blocks hours apart and roughly 350 days from a difficulty adjustment while the main network powered ahead.

A volunteer security effort says it has scanned 150 Bitcoin repositories, disclosed more than a dozen vulnerabilities, and is building an open-source AI platform to automate software security reviews.

Senate Majority Leader John Thune filed the motion to proceed early Saturday, setting up a mid-September showdown.

U.Today - IT, AI and Fintech Daily News for You Today

Bitcoin's active addresses have made a return to a stage that many considered a norm back in 2018.

A crypto whale has placed a $14.3 million leveraged bet that Monero (XMR) will rally toward $516, underscoring renewed bullish sentiment around the privacy-focused cryptocurrency despite its continued association with illicit fund flows.

While Tether pumps $1 billion into Tron retail channels, Ripple's strategic $10 million RLUSD injection signals a deeper corporate shift.

Shiba Inu isn't giving up as price successfully bounces off of the local resistance level.

Veteran trader Peter Brandt is leaning bearish on Bitcoin’s next move, pointing to a head-and-shoulders pattern.

Blockonomi

TLDR

- BIP-110 supporters launched a breakaway Bitcoin chain on Saturday at block 961,632.

- The fork mined only two blocks in about eight hours before it stalled.

- Just 2.53% of mining power backed the fork, far below the 55% threshold needed to activate the change.

- The breakaway chain inherited Bitcoin’s difficulty setting and would need roughly 350 days to reach its next adjustment.

- Michael Saylor and Jameson Lopp both publicly criticized the fork and its supporters.

A group of Bitcoin supporters launched a breakaway chain over the weekend. The split centered on a proposal known as BIP-110.

The fork began Saturday at block 961,632. Nodes running BIP-110 software started rejecting any block that failed to signal support for the change.

The new chain struggled from the start. It mined only two blocks in about eight hours before it stopped producing blocks at a normal pace.

Meanwhile, the main Bitcoin network kept working as usual. It continued adding a new block roughly every ten minutes.

What Is BIP-110?

BIP-110 is a proposal to change how Bitcoin handles certain types of data. It would temporarily block ways of embedding images, text, and other non-financial data into transactions.

Supporters say this data, often tied to Ordinals inscriptions, clogs the network. They argue it raises fees for people making normal payments.

Critics see it differently. They argue that anyone who pays for block space has earned the right to use it however they choose.

Opponents also worry about the precedent. They say letting miners and node operators filter transactions could weaken Bitcoin’s resistance to censorship.

The numbers show how small support for the fork really was. Only 2.53% of recent blocks signaled backing for BIP-110.

That is far below the 55% needed for the change to activate without splitting the network. Because of this, the breakaway chain kept Bitcoin’s current difficulty setting despite having very little mining power behind it.

Bitcoin adjusts its difficulty every 2,016 blocks. The main chain reaches that mark roughly every two weeks.

The breakaway chain would need close to 350 days to hit the same milestone. This left its blocks arriving hours apart instead of minutes.

Reactions From the Bitcoin Community

Strategy’s Michael Saylor commented on the outcome early Sunday. He said the network worked as designed and that about 99.85% of hash power stayed with the main Bitcoin chain.

Bitcoin security expert Jameson Lopp also weighed in. He said he would not support unblocking or welcoming back anyone who backed BIP-110.

Lopp added that some supporters spread false claims and targeted people who have worked on improving Bitcoin for years. His comments reflected the tension the debate caused within the community.

There is also a risk for anyone holding coins from the new chain. Because both chains accept the same kind of transactions, a coin sold on the minority chain could be copied over to the main Bitcoin network.

This means a buyer could end up receiving real Bitcoin from the same seller twice. The signaling window for BIP-110 closes at block 963,647.

The fork has fallen so far behind that it has no real chance of reaching that mark before support runs out. For now, the main Bitcoin network remains the dominant chain by a wide margin.

The post Bitcoin BIP-110 Fork Stalls After Mining Just Two Blocks appeared first on Blockonomi.

Key Takeaways

- Bank of America expanded its IREN holdings by 58.4% during Q1, accumulating 2.14 million shares valued at approximately $73.3 million

- Shares opened Monday at $41.23, representing a significant decline from the 52-week peak of $76.87, with current market capitalization at $14.73 billion

- Current price-to-earnings ratio stands at 85.9x, substantially exceeding the software sector average of 32.5x

- Most recent quarterly results disappointed, with IREN posting a $0.25 per share loss alongside $144.79M in revenue versus analyst expectations of $219.69M

- Wall Street maintains a “Moderate Buy” rating with a consensus target price of $82.71

Major financial institutions continue accumulating IREN stock despite mounting questions about its premium valuation. Bank of America expanded its stake by 58.4% during the first quarter, positioning itself with 2.14 million shares worth approximately $73.3 million. This strategic move occurred while shares traded at $41.23 on Monday, representing less than 54% of the stock’s 52-week peak at $76.87.

IREN Limited, IREN

Bank of America isn’t alone in its conviction. Situational Awareness LP expanded its holdings by 34.5% in Q1, accumulating nearly 11.7 million shares valued above $401 million. Meanwhile, BNP Paribas and Clear Street Group initiated fresh positions worth $158.6 million and $137 million respectively. Combined, institutional shareholders now control 41.08% of outstanding shares.

The 52-week low of $17.22 provides perspective on the stock’s volatility, showing shares have still more than doubled from their floor. Looking at a three-year window, IREN has delivered approximately 6.3x returns. Such performance naturally prompts investors to question how much growth potential remains.

Premium Valuation Creates Headwinds

IREN currently carries a price-to-earnings multiple ranging from 85.9x to 93.2x based on different calculation methods. For context, the software industry trades at an average of 32.5x, while IREN’s direct competitors average 64.2x. Simply Wall St estimates a fair value P/E around 73.2x, suggesting current pricing exceeds even adjusted benchmarks.

According to Simply Wall St’s comprehensive valuation framework, IREN fails all 6 assessment criteria. This complete miss across the board signals a stock priced for exceptional future performance with limited margin for error.

The company’s $625 million all-stock purchase of Mirantis, a cloud software provider, forms the foundation of the optimistic thesis. This transaction deepens IREN’s positioning within AI and cloud infrastructure markets, supporting elevated revenue forecasts. However, the capital-intensive nature of data center operations demands that cash flow generation matches strategic ambitions.

Recent Results Disappoint and Analyst Perspectives

IREN’s latest quarterly performance, released May 8th, added pressure to the valuation debate. The firm disclosed a $0.25 per share loss, falling short of the $0.22 consensus forecast. Revenue reached $144.79 million, missing analyst projections of $219.69 million by a substantial margin.

Looking ahead to the complete fiscal year, analysts project IREN will record a $1.96 per share loss.

Wall Street opinions vary considerably. Cantor Fitzgerald maintains an overweight stance with a $99 price objective. HC Wainwright established a $90 target. Canaccord Genuity holds a buy recommendation at $79. Conversely, JPMorgan assigns an underweight rating with a conservative $46 target.

The aggregated analyst view settles on “Moderate Buy” with a mean price target of $82.71, representing roughly 100% upside from current levels.

With a beta of 4.29, the stock demonstrates significant volatility compared to broader market movements. Technical indicators show the 50-day moving average at $46.59 and the 200-day average at $46.67, both positioned above the current $41.23 trading price.

The post IREN Stock: Bank of America Boosts Holdings 58% — Should Investors Follow? appeared first on Blockonomi.

Key Takeaways

- Rocket Lab shares have declined 57% from their $151 peak, currently priced at $82.83

- Wall Street consensus shows “Moderate Buy” with price targets averaging $110.29

- First quarter fiscal 2026 revenue reached $200.35 million, representing 63.4% annual growth

- The company recently won approximately $663 million in contracts from the U.S. Space Force

- Company insiders have divested $362.8 million in shares during the last three months

Shares of Rocket Lab (RKLB) began Monday’s session at $82.83, representing a significant 57% retreat from the $151 all-time peak reached in June. Despite this substantial correction, Wall Street analysts maintain optimism. Their collective price target of $110.29 suggests potential gains of approximately 49% from present levels.

Rocket Lab USA, Inc., RKLB

The aerospace company holds a “Moderate Buy” consensus among market analysts, backed by three Strong Buy recommendations, thirteen Buy calls, five Hold positions, and a single Sell rating. Morgan Stanley maintained its “Overweight” stance in July, while New Street Research established a $150 target during May.

First quarter fiscal 2026 results showed revenue of $200.35 million, marking a 63.4% year-over-year surge and surpassing the Street’s $189.65 million projection. The firm met expectations for a loss of $0.07 per share.

The company’s backlog paints an encouraging picture. Rocket Lab secured 31 launch agreements during Q1 alone—exceeding its entire 2025 contract total. Overall backlog climbed to $2.2 billion, reflecting 108% growth compared to the prior-year quarter.

The adjusted EBITDA loss improved to $11.8 million, significantly better than the anticipated $26 million deficit. Following these results, no fewer than seven analysts lifted their price projections.

Major Military Contracts Boost Outlook

Recent contract victories warrant attention. Rocket Lab landed a $397 million agreement with the U.S. Space Force for developing, launching, and operating sophisticated flat-panel satellites utilizing its forthcoming Neutron rocket. An additional $266 million Space Force deal encompasses 12 suborbital missions plus up to six optional launches, with initial deployment expected by year-end.

Combined, Rocket Lab has captured roughly $663 million in Space Force business in recent months. The Neutron vehicle, critical to executing the larger agreement, remains in development without operational flights to date.

The company also successfully executed its 92nd Electron mission and 13th launch of 2026, placing a satellite into orbit for returning customer iQPS.

Notable Investment Concerns

Profitability remains elusive. The firm recorded a $45 million net loss during Q1, with analysts projecting a full-year deficit of $0.26 per share. The stock’s price-to-sales multiple stands at 53—dramatically higher than the technology sector’s typical ratio near 7.

Insider transaction activity merits consideration. Throughout the previous three-month period, company insiders offloaded 3.85 million shares valued at roughly $362.8 million. SVP Arjun Kampani disposed of 88,000 shares during June at an average $107.98 price point. Portions of these sales related to tax liabilities from vesting equity compensation.

Institutional ownership accounts for 71.78% of outstanding shares. PensionDanmark expanded its position by 224.2% in Q2, purchasing 28,358 shares to reach a total holding of 41,008 shares valued at approximately $4.17 million.

With a beta coefficient of 2.60, the stock demonstrates pronounced volatility. The 52-week trading range spans from $37.57 to $151.00.

Rocket Lab will announce Q2 earnings following Monday’s closing bell on August 10. Key focus areas include revenue trajectory, Neutron development progress, and management commentary regarding the pathway to achieving profitability.

The post Rocket Lab (RKLB) Stock Down 57%: Should You Buy Before Monday’s Q2 Earnings? appeared first on Blockonomi.

Key Takeaways

- Super Micro Computer is set to announce fiscal Q4 results on August 11, with analysts projecting earnings per share of $0.92 and revenue reaching $11.60 billion—representing approximately 101% year-over-year growth.

- The company issued a preliminary report showcasing a backlog exceeding $60 billion and updated gross margin expectations to 15%–17%, nearly doubling previous estimates.

- The options market anticipates a volatile reaction, with a potential price movement of 16%–19% following the earnings announcement.

- Wall Street’s consensus rating stands at Hold, with the average analyst price target around $39.21, suggesting approximately 25%–30% potential upside from current trading levels.

- During Q2, Czech National Bank expanded its position by 16.9%, while institutional ownership has reached 84.06% of outstanding shares.

Super Micro Computer (SMCI) began Monday’s session at $31.13, hovering close to its 50-day moving average of $31.26. Over the trailing twelve months, shares have fluctuated between $19.48 and $58.78.

Super Micro Computer, Inc., SMCI

Market participants are focused squarely on August 11, when the company unveils its fiscal fourth-quarter financial results. Consensus estimates call for earnings per share of $0.92—more than doubling the prior-year figure—alongside revenue of approximately $11.60 billion, representing a 101% annual increase.

Options pricing suggests a potential swing of 16%–19% in either direction following the release. This volatility forecast underscores substantial uncertainty about the company’s near-term trajectory.

Ahead of the formal earnings release, Super Micro issued a preliminary business update that caught market attention. Management disclosed a record order backlog surpassing $60 billion and revised gross margin guidance upward to 15%–17%, significantly above earlier projections.

Optimistic investors interpreted the massive backlog as confirmation that appetite for AI server solutions and rack-scale infrastructure remains robust. Rosenblatt responded to the update by increasing its price target, characterizing the stock’s recent decline as an attractive entry point.

Wall Street Perspectives and Price Targets

However, sentiment across Wall Street remains divided. Mizuho reduced its price objective from $44 down to $34, pointing to intensifying competitive pressures, memory component constraints, and postponements in data center construction projects. Similarly, Wedbush lowered its target from $42 to $34.

Conversely, Needham upgraded its target from $40 to $46 while maintaining a Buy recommendation. Barclays adjusted its outlook higher from $34 to $38 but retained an equal weight stance.

Currently, four analysts have assigned Buy ratings to SMCI, twelve recommend Hold, and two advise Sell. The average price target across all analysts stands at $39.21.

SMCI trades at a price-to-earnings ratio of 16.47 and a price-to-earnings-growth ratio of 0.37, metrics that some market observers believe reflect valuation levels near multiyear lows.

Institutional Investment Trends

Czech National Bank boosted its SMCI holdings by 16.9% throughout the second quarter, now owning 160,189 shares valued at approximately $4.7 million. Multiple other institutional investors similarly expanded their stakes during the same period.

Baird Financial Group increased its position by 54.9%. EverSource Wealth Advisors raised its allocation by 42.4%. Collectively, institutional investors and hedge funds control 84.06% of the company’s shares.

Vanguard holds the largest institutional stake at slightly above 10%, positioned just ahead of CEO Charles Liang’s ownership.

The company has encountered scrutiny regarding its financial position. Super Micro has historically reported negative free cash flow and recently executed a $7 billion equity offering to support operational funding needs.

Another concern highlighted by analysts involves SMCI’s reliance on Nvidia. High-profile customers including SpaceX are reportedly constructing AI computing infrastructure centered on Nvidia processors, potentially intensifying supplier concentration risks.

The company maintains a debt-to-equity ratio of 0.88, a current ratio of 2.66, and a market capitalization of $18.72 billion.

Financial results are scheduled for release before market opening on August 11.

The post Super Micro Computer (SMCI) Stock Earnings Preview: $60B Backlog Highlights Key Results appeared first on Blockonomi.

TLDR

- BNB is trading at $608.22, up 1.3% in the past 24 hours.

- Chart structure points to $620, $660, and $700 as the next price targets.

- Analyst Umair Orakzai says BNB has moved past a 1:1 risk-to-reward setup.

- Binance’s bStocks added $594.4 million to the tokenized stock market in 90 days.

- BNB Chain leads all networks in tokenized stock growth at $519.6 million.

BNB is trading at $608.22 as of August 9, 2026. The token is up 1.3% over the past 24 hours.

Its trading volume over the last day reached $975.77 million. BNB’s market cap now sits at $80.99 billion, according to CoinMarketCap.

Traders are watching for a breakout that could push the price higher. The next levels being tracked are $620, $660, and $700.

Crypto analyst Umair Orakzai shared his view on X this week. He said BNB’s chart has moved above a 1:1 risk-to-reward ratio.

Orakzai pointed out that the earlier stop-loss near $542 marked about 5% downside. The trade has since moved into profit territory.

He suggested traders could shift their stop-loss closer to the entry point. This would protect gains while leaving room for the setup to play out.

BNB Eyes Key Resistance Levels

Orakzai’s analysis places $620 as the first test for BNB. A clean move above that level could open the path to $660 and then $700.

The BNB/BTC trading pair is also showing strength. This adds support to the idea that buyers still hold the upper hand.

For now, BNB’s price action remains neutral. This lines up with Bitcoin’s own sideways movement across the broader market.

Binance bStocks Drives Tokenized Stock Growth

Data platform Token Terminal posted on X that Binance’s bStocks led growth in the tokenized stock market over the last 90 days. The platform added $594.4 million during that period.

Binance bStocks led tokenized stock market cap growth over the past 90 days, adding $594.4M

xStocks added $192.8M, followed by Securitize (+$183.3M) & Reality (+$137.6M)

Assets on BNB Chain added $519.6M in market cap, ahead of Ethereum (+$218.3M) & Solana (+$201.0M) pic.twitter.com/cfPJv2ua22

— Token Terminal

(@tokenterminal) August 6, 2026

xStocks came next with a $192.8 million increase. Securitize and Reality added $183.3 million and $137.6 million.

BNB Chain led all blockchain networks in tokenized stock growth, adding $519.6 million. Ethereum grew by $218.3 million, and Solana added $201 million.

These numbers show tokenized stocks are expanding across several blockchains. BNB Chain currently sits at the front of that growth.

BNB was trading at $608.22 at the time of writing, up 1.3% over the past day. The $620 level remains the next point traders are watching for a possible breakout.

The post BNB (BNB) Price: Analysts Eye $700 Target After Bullish Chart Breakout appeared first on Blockonomi.

CryptoPotato

Bitcoin’s price hasn’t made a major move for days, as it continues to remain stuck at around $65,000 since Friday. The good news for the bulls is that it now stands on the upper side.

Most larger-cap alts perform similarly, with little to no actual moves. XMR is up by 3%, NEAR by 2.5%, while WLD and PUMP have stolen the show.

BTC Rises Above $65K (Slightly)

The previous business week began on a significantly more volatile note. At first, BTC was rejected at $64,000 after an eventful weekend on the Middle East war front, and dipped to $62,200 within hours. However, the bulls stepped up and helped it recover the lost ground almost immediately.

The following few days were more positive as bitcoin tapped $65,000 by Wednesday. It remained at around that level before the CLARITY Act faced another setback in the US Senate, and BTC dipped toward $64,000. The weak US jobs report from Friday, though, brought some hopes that the Fed won’t hike the rates in September, and BTC reacted with a price pump to $65,400.

That was short-lived, though, as the cryptocurrency failed to maintain its run. It retreated to around $65,000 and has spent the following 72 hours or so trading sideways. It currently sits above that level after dipping to $64,800 yesterday, but more volatility is expected as the week progresses.

Its market cap has seemingly reclaimed the $1.3 trillion level, while its dominance over the alts remains above 57% on CG.

3 Alts Pump Hard

Bitway (BTW) is the altcoin that has entered the top 100 coins by market cap, after surging by another 20% in the past day. The asset has rocketed by triple digits since this time last Monday.

WLD and PUMP follow suit in terms of daily gains. Both assets have jumped by around 13% to $0.345 and $0.0028, respectively. VVV is up by 9% to $12.