Cryptocurrency Posts

Crypto Briefing

Techno4K's victory at IEM highlights the growing prominence of Mongolian talent in the global esports arena, influencing future tournaments.

The post Techno4K secures round victory with decisive kill at IEM appeared first on Crypto Briefing.

The transfer race for Casad highlights the competitive dynamics in European football, impacting club strategies and player career paths.

The post Manchester United monitors Barcelona midfielder Marc Casadó as Monaco leads transfer race appeared first on Crypto Briefing.

Chelsea's potential financial gain from Hall's transfer highlights the strategic value of sell-on clauses and their impact on club finances.

The post Chelsea set to pocket £50M-£60M as Manchester United chase Newcastle’s Lewis Hall appeared first on Crypto Briefing.

The integration of crypto in the World Cup highlights its growing influence in sports, potentially reshaping fan engagement and investment dynamics.

The post Haiti faces Scotland in World Cup 2026 Group C opener as crypto partnerships take center stage appeared first on Crypto Briefing.

Access to compute infrastructure is key for new AI labs to challenge industry giants in AGI development.

The post Anjney Midha: AI development is consuming unprecedented resources, big companies dominate the landscape, and compute infrastructure is crucial for new labs | Odd Lots appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Standard Chartered Calls Crypto Bottom as Bitcoin Price Recovers From $59,000 Low

Standard Chartered’s head of digital asset research, Geoff Kendrick, declared Friday that the crypto market has seen its cycle low, with Bitcoin’s recent dip to approximately $59,000 marking the bottom of the latest downturn — a 53% drawdown from its October all-time high of $126,000.

“Winter is over. Welcome back to crypto spring,” Kendrick wrote in a Friday note, adding, “I think we have now seen the low in crypto asset prices for the cycle.”

Bitcoin had recovered to around $64,000 at the time of Kendrick’s note, representing a roughly 5% gain over the prior week. The bank maintains a $100,000 price target for Bitcoin by year-end — projections it first issued in February.

SpaceX IPO drains crypto liquidity — then frees it

One of the two primary catalysts Kendrick cited is the historic Nasdaq debut of Elon Musk’s SpaceX, which priced its $75 billion IPO at $135 per share under the ticker SPCX on June 12.

Shares opened sharply above their IPO price, gaining roughly 20% on debut day. Kendrick argued that a significant portion of recent Bitcoin ETF outflows — totaling more than $5.72 billion since the second week of May, among the sharpest “since inception” — was driven by investors liquidating crypto positions to secure SpaceX allocations. With the IPO now live, that specific selling pressure may lift, he said.

The overlap between crypto and SpaceX demand was already playing out in real time. On Hyperliquid, perpetual contracts for SpaceX (SPCX) had accumulated over $240 million in open interest and $220 million in 24-hour volume ahead of the debut — ranking it as the eighth-largest asset on the platform.

Iran is a wildcard

The second catalyst involves geopolitics. A potential peace deal between the U.S. and Iran, timed ahead of next week’s G7 summit, could reduce pressure on global oil supplies that have remained tight since Middle East hostilities began.

Lower oil prices would subsequently cool elevated U.S. Treasury yields — which have weighed on risk assets like crypto by making risk-free government debt more attractive.

West Texas Intermediate crude fell roughly 1.5% on Friday to around $85–$86 per barrel. However, the peace deal narrative remained fragile.

President Trump stated Thursday that a breakthrough could come this weekend, only to later post on Truth Social that the deal made public was not what had been agreed, warning Iranian officials to “get their act together” — adding uncertainty to the macro outlook.

Three bitcoin price signals to watch

Kendrick outlined three confirmation signals that would validate his call. First, he is watching for Strategy to announce an additional Bitcoin purchase on Monday, as CEO Michael Saylor’s buying history has served as a reliable demand signal for institutional appetite.

Second, he is expecting U.S. spot Bitcoin ETFs to return to net-positive daily inflows on Friday.

Third, he wants to see continued declines in global oil prices as the Iran diplomatic situation evolves.

If all three materialize, Kendrick’s crypto spring thesis gains its clearest validation yet — suggesting institutional and macro forces are finally aligning to push Bitcoin back toward the bank’s $100,000 year-end target.

This post Standard Chartered Calls Crypto Bottom as Bitcoin Price Recovers From $59,000 Low first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Blockworks Acquires Messari in Deal Highlighting Crypto’s Data Consolidation Race

Blockworks, the New York-based crypto data and investor relations platform, has acquired rival Messari in a deal that underscores the growing consolidation pressure reshaping the digital asset industry — and the steep valuation resets facing once high-flying crypto startups.

The acquisition brings together two of the industry’s largest crypto information businesses. Messari, founded in 2018, built a comprehensive data platform covering more than 40,000 digital assets, along with APIs, market intelligence, research tools, and AI-powered workflows used by funds, exchanges, regulators, and developers.

Blockworks, also founded in 2018, has focused on the issuer side of crypto capital markets, offering standardized disclosures through its Token Transparency Framework and a full-stack investor relations platform for onchain assets.

Blockworks paid more than $10 million for Messari — a steep discount from Messari’s approximately $300 million valuation when it raised a $35 million Series B led by Brevan Howard’s crypto arm in 2022, with Point72 Ventures also among its backers, according to the Wall Street Journal.

The markdown reflects both Messari’s recent difficulties — including the 2024 departure of co-founder and longtime CEO Ryan Selkis and subsequent staff reductions — and broader headwinds gripping the crypto sector.

“This acquisition connects the two sides of the market,” said Jason Yanowitz, co-founder of Blockworks. “Issuers maintain a trusted record of their business, and investors, exchanges, and regulators consume that record through research, APIs, and automated workflows.”

Blockworks raise to consolidate fragmented crypto data market

The deal was funded in part through Blockworks’ recently closed Series A extension, which valued the company at $192 million. That round was co-led by ParaFi and Reciprocal Ventures and included participation from Coinbase Ventures, among others.

Blockworks said it raised capital specifically to consolidate crypto’s fragmented data and information market, drawing comparisons to how Wall Street’s information layer eventually coalesced around dominant platforms like Bloomberg, FactSet, and S&P Global.

Messari CEO Diran Li, who took over following Selkis’s departure and had been repositioning the firm as an “AI-first company,” will join Blockworks as a senior leader under co-founders Yanowitz and Michael Ippolito.

The deal arrives as crypto M&A activity remains elevated despite challenging market conditions. Crypto companies have completed 144 deals totaling $11.8 billion in transaction value so far in 2026 — up roughly 3.5% from the same period last year — according to data from advisory firm Architect Partners.

Still, Eric Risley, founder of Architect Partners, warned that sustained pressure on trading volumes and token prices could force more distressed sales. “We are in the midst of the creation of the haves and the have-nots,” Risley said, per WSJ.

Both Blockworks and Messari executives said the combined platform would prioritize deeper data coverage, stronger APIs, enhanced compliance workflows, and AI-native research tools as digital assets increasingly migrate onchain.

This post Blockworks Acquires Messari in Deal Highlighting Crypto’s Data Consolidation Race first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

SpaceX Officially Joins Public Bitcoin Leaderboard as 8th Largest Holder With 18,712 BTC

Elon Musk’s SpaceX launched trading on the Nasdaq today under the ticker SPCX — and it didn’t arrive empty-handed.

The company officially entered the public Bitcoin treasury leaderboard as the 8th largest holder with 18,712 BTC, a position that had been building for years before its historic IPO debut confirmed the full size of the stash.

SpaceX’s S-1 filing with the Securities and Exchange Commission first disclosed the 18,712 BTC position back in May, valued at approximately $1.29 billion at the time of filing.

The total cost basis was reported at $661 million — an average acquisition price of roughly $35,324 per coin — suggesting the company began accumulating Bitcoin in late 2023 or earlier. At today’s prices near $63,000, the position is worth approximately $1.19 billion.

The disclosure somewhat surprised the market. Blockchain analytics firm Arkham Intelligence had previously tracked SpaceX’s holdings as low as 6,095 BTC, and the BitcoinTreasuries.net May 2026 Corporate Adoption Report noted that its pre-IPO private estimate stood at just 8,285 BTC.

JUST IN: Elon Musk's SpaceX officially becomes 8th largest public Bitcoin holder with 18,712 BTC

— Bitcoin Magazine (@BitcoinMagazine) June 12, 2026pic.twitter.com/04n3AyFC3T

The actual confirmed figure — more than double those estimates — made SpaceX’s reveal the second-largest Bitcoin treasury disclosure of May, trailing only Strategy’s 25,404 BTC in monthly purchases and accounting for more than one-third of all public treasury growth before sales.

“We expect SpaceX to rank among the top ten publicly traded Bitcoin treasuries after its anticipated June 12 IPO,” BitcoinTreasuries.net wrote in its May report — a forecast that has now materialized.

The live leaderboard, updated as of June 11, confirms SpaceX at rank #8, slotting in just behind Strive (19,032 BTC at #7) and just ahead of Coinbase Global (16,492 BTC at #9).

SpaceX shares debut higher than initial pricing

The IPO itself is historic, even without the Bitcoin angle.

SpaceX priced its shares at $135 on June 11, raising roughly $75 billion and valuing the company at about $1.75 trillion.

Reports now indicate the stock could debut at $171 per share with other reports saying $155 a share. At that price, SpaceX’s valuation would climb to approximately $2.2 trillion, potentially making Elon Musk the world’s first trillionaire.

The listing, led by Goldman Sachs and Morgan Stanley, ranks as one of the largest stock market debuts in U.S. history, surpassing Saudi Aramco’s $29 billion IPO in 2019.

The timing of SpaceX’s entry into the public crypto arena is notable given broader market headwinds. Bitcoin has shed more than 50% from its all-time high above $126,000, hovering around $64,000 in recent sessions, with spot Bitcoin ETFs bleeding $2.26 billion in outflows over two weeks.

Still, SpaceX’s Bitcoin position appears to be a long-term balance-sheet allocation rather than a trading posture. The S-1 stated: “The Company has ownership of and control over its digital assets, which consist of Bitcoin, and utilizes, and expects to continue to utilize third-party custodians to hold its Bitcoin.”

Analysts at Grayscale noted that SpaceX is poised to become the most valuable public company holding Bitcoin by market capitalization — even as Strategy remains the largest by coin count with over 843,000 BTC.

This post SpaceX Officially Joins Public Bitcoin Leaderboard as 8th Largest Holder With 18,712 BTC first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Sam Bankman-Fried Loses Appeal to Overturn FTX Fraud Conviction

One of Sam Bankman-Fried’s last credible paths to freedom closed Friday as a federal appeals court upheld his fraud conviction and 25-year prison sentence, ruling that the case against him was, in the court’s own words, “conservatively stated, robust.”

A three-judge panel of the Manhattan-based 2nd U.S. Circuit Court of Appeals handed down the 42-page opinion on June 12, rejecting every argument Sam Bankman-Fried’s legal team advanced to undo the November 2023 conviction that cemented one of the largest financial collapses in crypto history, according to Reuters.

At the heart of the appeal was a claim that the U.S. District Judge Lewis Kaplan had stripped Sam Bankman-Fried of a fair defense by barring evidence that FTX held enough assets to cover customer withdrawals.

Defense attorney Alexandra Shapiro told the appellate panel in November 2025 that “Mr. Bankman-Fried’s trial was fundamentally unfair because the jury only got to hear one side of the story.”

Prosecutors countered that Kaplan’s ruling was correct: fraud charges hinge on misappropriation, not on the possibility that assets could have covered liabilities under different circumstances. The appellate panel agreed, finding the trial court’s evidence rulings sound and the government’s case against Sam Bankman-Fried overwhelming.

How FTX Fell

The exchange, once valued at $32 billion, collapsed in November 2022 once it was exposed that the balance sheet of Alameda Research — Bankman-Fried’s affiliated hedge fund — was built on FTX’s own exchange token rather than independent assets. The disclosure triggered a customer run that ripped open an $8 billion hole in FTX’s accounts.

Three of Bankman-Fried’s former deputies — Alameda CEO Caroline Ellison, FTX co-founder Gary Wang, and engineering head Nishad Singh — each pleaded guilty and testified against him. Ellison, the trial’s star witness, told jurors Bankman-Fried gave her the instruction to divert customer deposits to Alameda to repay loans from crypto lenders. “Sam directed me to commit these crimes,” she said from the stand.

The court ordered an $11 billion forfeiture and three years of supervised release following Bankman-Fried’s March 2024 sentencing. Ellison received two years and was released in January 2026 after serving 14 months.

The appeals court ruling lands just weeks after Bankman-Fried also filed a formal clemency petition with the DOJ’s Office of the Pardon Attorney, requesting a presidential pardon from Donald Trump. The application is listed as a “pardon after completion of sentence” — not a commutation — and Trump has said publicly he will not grant it.

Judge Kaplan denied a separate Rule 33 new trial motion in April 2026, calling Bankman-Fried’s claim that witnesses had been threatened by the government “wildly conspiratorial and entirely contradicted by the record.” Bankman-Fried withdrew an earlier version of that motion on April 22 without prejudice.

With the 2nd Circuit now closed, his legal options narrow to a habeas petition — a route with a lower success rate than direct appeals — or a Supreme Court petition.

What’s next for Sam Bankman-Fried

Sam Bankman-Fried remains at a low-security federal prison near Santa Barbara, California, and is not eligible for release until 2044.

In a prison interview with Fox Business this month, he maintained his position: “I didn’t steal user funds.” He pointed to the FTX bankruptcy estate’s recovery of crypto assets, which have allowed the estate to pay creditors more than 100 cents on the dollar — a figure he frames as proof of FTX’s underlying solvency, though courts at every level have rejected that framing.

The Friday ruling closes the chapter on what federal prosecutors called a “fraud of epic proportions” — a case that shook institutional confidence in crypto markets, triggered congressional hearings, and forced exchanges across the industry to overhaul proof-of-reserves practices.

Back in January, President Donald Trump said he would not pardon former FTX CEO Sam Bankman-Fried, rejecting clemency for the convicted crypto executive.

This post Sam Bankman-Fried Loses Appeal to Overturn FTX Fraud Conviction first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Strategy Stock MSTR Offers Bitcoin Exposure At 18% Discount

I’ve been vocal about accumulating Bitcoin aggressively at current levels. Now I’m starting to look seriously at Strategy too. The same kind of confluence that flagged Bitcoin as a sizeable accumulation opportunity is appearing on MSTR, and in some cases, the readings are even more extreme.

This week at a glance:

- The RSI has only been lower on a handful of occasions since Strategy adopted a Bitcoin standard.

- The Mayer Multiple for MSTR has just reached the lower percentiles.

- The BTC vs MSTR ratio is close to entering a zone that has historically preceded sustained MSTR outperformance.

- At the previous Bitcoin all-time high with a 1x net asset value premium, the fair value of MSTR shares would be over $300.

Discount

Strategy currently holds approximately 845,000 BTC with an Average Cost Basis in the mid-$70,000s. That means, at current Bitcoin prices, they’re sitting at a pretty massive loss on their holdings.

Figure 1: Strategy’s Average BTC Cost Basis and other key metrics.

View Live Charts

This has coincided with the NAV dropping even deeper beneath 1.00x; with MSTR’s market cap currently sitting approximately 18% below the USD value of its Bitcoin holdings. In other words, buying MSTR at current prices is the equivalent of buying $1 of Bitcoin for $0.82.

Support

The 200-week moving average is usually pretty notable support for assets, especially those that typically trend to the upside. Strategy’s share price is currently sitting right on this level, the same level that has previously marked significant accumulation zones.

Figure 2: Strategy’s share price tests the 200-week moving average.

A sustained hold and reclaim of this level, combined with Bitcoin showing any upward momentum, historically sets up the conditions for meaningful MSTR recovery. The level is being tested. Whether it holds will be one of the key signals to watch over the coming weeks.

RSI

Since Strategy adopted a Bitcoin standard, the RSI for MSTR has only been lower on a handful of prior occasions, both during previous Bitcoin bear market cycle lows, when the share price was in the low teens. The current reading isn’t quite at those depths, but it’s approaching them, and the direction of travel is continuing downward.

Figure 3: MSTR’s RSI drops beneath 25. Historically, such levels have preceded price appreciation.

The Mayer Multiple, simply the ratio between MSTR’s closing price and its 200-day moving average, recently registered a reading where 99.2% of all prior data points were higher. That’s a historically extreme level of underperformance relative to its own moving average, and it’s occurred at broadly the same time as the RSI signal. Giving two independent momentum indicators, both flashing readings only seen at the most significant cycle lows in MSTR’s history.

MSTR Or BTC?

The ratio between Bitcoin’s price and MSTR’s share price is one of the cleaner ways to gauge whether exposure should be in Bitcoin directly or rotated toward the higher-beta proxy. When the ratio is in the green upper zone, MSTR has historically been positioned to outperform. When it’s in the red lower zone, Bitcoin tends to lead.

Figure 4: The BTCUSD/MSTR ratio is close to the green zone, a level that has previously preceded sustained MSTR outperformance.

The ratio is currently close to entering that green zone again. Previous instances of this were followed by extended periods of significant MSTR outperformance relative to Bitcoin. The ratio is also making lower highs on the long-term trend, indicating the general trajectory is shifting toward MSTR becoming increasingly favorable relative to direct Bitcoin exposure.

Fair Value

At the previous all-time high of around $126,000 and with no additional accumulation priced in, a 1x net asset value premium on MSTR would imply a share price of over $300. That’s roughly a 2.5x from current levels just to reach fair value at Bitcoin’s last peak.

Figure 5: MSTR price targets modeled across varying BTC holdings and NAV premium scenarios.

If MSTR continues accumulating toward the 900,000 BTC range and the NAV premium moves modestly higher toward 1.25x or 1.5x, well below the 3x+ levels seen in the previous cycle, the numbers become pretty enticing! Crucially, the MSTR dilution that drove bitcoin accumulation is increasingly being funded through STRC rather than common share issuance, reducing that particular headwind.

Where Are We?

I’ve been accumulating bitcoin aggressively. I’m now also looking to add more MSTR. The combination of extreme momentum readings, the 200-week moving average support, an implied discount to the underlying Bitcoin holdings, and the BTC vs MSTR ratio close to entering historically favorable territory makes this feel like a no-brainer for a short-term play to increase my own BTC stack.

That said, MSTR is a high-beta Bitcoin play. If Bitcoin continues to struggle, MSTR will struggle more. I’m not treating this as a replacement for Bitcoin exposure, but as an additional asymmetric position at a point where the data suggests the risk-reward is historically favorable.

For more data, charts, and insights into bitcoin price trends, visit BitcoinMagazinePro.com.

Subscribe to Bitcoin Magazine Pro on YouTube for more expert insights!

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Always do your own research before making any investment decisions.

This post Strategy Stock MSTR Offers Bitcoin Exposure At 18% Discount first appeared on Bitcoin Magazine and is written by Matt Crosby.

CryptoSlate

Wall Street got to trade Bitcoin around the clock just in time to watch the market fall apart. CME Group launched 24/7 trading for its crypto futures and options on May 29, and over the first weekend, more than 7,200 contracts changed hands, worth roughly $50 million in notional value.

Within days, Bitcoin had slid below $70,000 for the first time in two months, and the market had to absorb one of its sharpest deleveraging waves of the year, with almost $10 billion in long-futures liquidations over a single week.

Could CME's always-on market become the volatility equalizer Bitcoin has needed for years, giving institutions regulated tools to hedge through the exact windows that used to belong to offshore exchanges, perpetual futures, and retail leverage? Possibly, but the first week of 24/7 trading left us only with more questions.

Wall Street opened its weekend hedge window in the middle of a leverage shakeout, and it remains genuinely unclear whether professional access calmed weekend crypto risk or simply made it trade faster.

CME crypto futures and options now trade continuously on Globex, with a weekly maintenance window, while weekend and holiday trades carry the following business day's trade date, clearing, and regulatory reporting.

As CryptoSlate reported ahead of the launch, execution goes 24/7 while the back office stays tied to business days, which means the famous CME gap effectively dies, and the quality of liquidity and Monday post-trade processing become the biggest problems.

Given the amount of money that changes hands when it comes to crypto futures, it's no wonder CME jumped onto the 24/7 bandwagon. CME's crypto futures and options generated $3 trillion in notional volume in 2025, and 2026 average daily volume reached 407,200 contracts, up 46% year over year, with average daily open interest of 335,400 contracts, up 7%.

Tim McCourt, CME's global head of equities, FX, and alternative products, said the company was “bridging the gap between regulated venues and the always-on nature of crypto assets.”

Launching 24/7 futures in a deleveraging market

The equalizer thesis could have played out in CME's favor if it weren't for the volatility.

The first weekend's $50 million in notional volume looks respectable until you set it against the broader derivatives market. CME Bitcoin open interest had been rolling over since late May, sliding from the 115,000 to 120,000 BTC area toward roughly 100,000 BTC by June 9, and open interest across crypto exchanges fell sharply over the same stretch. Positioning was shrinking, leverage was being forced out, and the new weekend trading window opened directly into that unwind.

The liquidation data showed a concrete sequence of forced exits. Between June 1 and June 5, daily liquidations repeatedly spiked toward and above the $1 billion mark, with the worst days approaching $1.8 billion, and long positions dominated the wreckage.

Bloomberg reported nearly $1.5 billion in liquidations in a single 24-hour window on June 2 as Bitcoin sank to a two-month low, the heaviest forced selling we've seen since February.

CryptoSlate has covered this before: falling prices combined with collapsing open interest usually signal positions being closed through liquidation rather than choice, and that's the pattern the first 24/7 week produced.

The result is a far more interesting natural experiment than a clean institutional debut would have been, because the new weekend market got tested under stress from its very first session.

The volatility we've seen in options won't help in the coming weeks and months either. Deribit's expiry calendar shows large notional clusters around June 26, Sept. 25, and Dec. 25, with the max pain for key expiries near the $75,000 level.

Investing.com reported that the May 29 Deribit expiry alone involved about $7.5 billion in BTC and ETH options notional, including $6.2 billion tied to Bitcoin contracts, with the spot price trading below its $75,000 max-pain level at the time.

Max pain is a positioning map, a snapshot of where options sellers face the least payout pressure. Traders watch it because strike concentration and dealer hedging can pull attention toward certain price zones around big expiries, and that influence tends to fade once the expiry passes.

CME's 24/7 Bitcoin futures: qualizer or accelerant?

The optimistic case for 24/7 regulated derivatives is pretty strong. For years, Bitcoin traded around the clock while institutional hedging tools kept banker's hours, which meant a Saturday crash had to be absorbed by offshore venues and crypto-native liquidity until CME reopened Sunday evening. Continuous access lets desks hedge, roll, and adjust exposure in real time instead of compressing every weekend move into a violent Monday repricing.

That should, in theory, reduce panic gaps, improve price discovery, and narrow the structural distance between regulated markets and the offshore perpetuals complex, a shift CryptoSlate flagged when the plan was first announced last October.

The pessimistic case comes, funnily enough, from CME's own chief executive. Terry Duffy said during a Piper Sandler conference on June 4 that the CFTC's approval of perpetual crypto futures was “a disaster waiting to happen,” warning that products carrying leverage as high as 50-to-1, combined with automatic liquidation models, pose a systemic threat and a particular danger to retail traders who underestimate funding costs.

While Duffy was aiming at competitors' perps rather than his own products, the warning cuts both ways. More trading hours can mean faster hedging and can equally mean faster selling into thin weekend liquidity, with professional leverage now participating in windows when order books have historically been at their shallowest.

The industry is expanding round-the-clock access at the same moment its most prominent executive warns that always-on leveraged crypto products magnify stress.

Alongside the 24/7 rollout, CME made its new Bitcoin Volatility futures available around the clock starting June 1. These contracts settle to the CME CF Bitcoin Volatility Index, a forward-looking measure of 30-day implied volatility derived from CME's own Bitcoin options order books, and they allow traders to take positions on how violently Bitcoin will move without taking a view on direction.

So, the weekend launch and the volatility contracts describe a single project: CME is building a regulated stack around Bitcoin's turbulence itself, turning one of its more infamous traits into a money-making product line.

So the early verdict has to stay honest about what the evidence can and can't support. The equalizer thesis is plausible, the infrastructure now exists, and the first weekend's volume proves there's quite a bit of demand even in the most volatile conditions.

What the first week can't prove, though, is that institutional access smooths anything, because the data shows a market still ruled by deleveraging, liquidation cascades, and offshore options positioning.

Bitcoin's weekend risk survived Wall Street's arrival fully intact; what has changed is that the risk now trades on Wall Street's clock, and the next ugly Saturday will reveal whether the danger zone has become safer or just busier.

The post Are 24/7 CME Bitcoin futures a volatility cure — or a new leverage trap? appeared first on CryptoSlate.

The Securities and Exchange Commission (SEC) is moving to dismantle a stock-trading rule that has governed Wall Street for two decades.

On June 11, the agency submitted a proposal that would rescind Rule 611 of Regulation NMS, the trade-through rule that requires trading centers to prevent stock trades from executing at prices worse than protected quotes displayed elsewhere. It would also eliminate Rule 610(e), which restricts locked and crossed quotations, along with related definitions.

For most of Wall Street, the proposal is a market-structure fight over routing, exchanges, wholesalers, displayed quotes, and execution quality.

For crypto firms and banks exploring tokenized shares, it is something more specific: the SEC is targeting one of the rules that made blockchain-based stock trading difficult to reconcile with the national market system.

A rule built for routed markets

Rule 611 was adopted in 2005 as part of Regulation NMS, a broad overhaul of US equity-market rules. The goal was to protect investors from having their orders executed at inferior prices when a better displayed quote was available on another exchange.

In practice, that system tied stock trading to the National Best Bid and Offer (NBBO), the best displayed bid and offer across protected venues. Broker routers, exchanges, and trading firms built systems around that obligation.

However, that framework is harder to apply to automated market makers (AMMs), the software-based trading pools that power much of decentralized finance.

AMMs do not work like Nasdaq, NYSE, or Cboe. They price trades through liquidity pools, bonding curves, slippage, and block-time execution.

Alex Thorn, Galaxy Digital’s head of research, pointed out that the rule was one of the largest structural barriers to DeFi-based trading of tokenized equities.

“An AMM cannot comply with 611 by construction,” Thorn said. It executes against a bonding curve at the pool price, with slippage and block-time granularity.

The issue is not simply a technical inconvenience. An on-chain pool cannot easily route intermarket sweep orders, ingest consolidated market data with the latency guarantees expected in US equities, or halt a swap because a better quote briefly appears on Nasdaq.

Under the current framework, a pool trading a tokenized version of an NMS stock could repeatedly print prices that differ from protected off-chain quotes. That creates the risk that the pool would be viewed as constantly violating the trade-through rule or functioning as an unlawful trading center.

Rule 610(e) raises a related problem. AMM prices can drift as liquidity shifts and trades move through a pool. That means on-chain prices could lock or cross the displayed NBBO, something current market rules are designed to prevent.

Why crypto sees an opening

Tokenized stocks are blockchain-based representations of company shares or share-linked claims. Supporters argue they could allow around-the-clock trading, fractional ownership, faster settlement, collateral mobility, and broader international access.

The market has been small compared with traditional equities, but interest has increased as banks, crypto exchanges, and asset managers look for ways to bring regulated financial instruments onto public or permissioned blockchains.

Christopher Perkins, chief executive of 250 Digital Asset Management, said Regulation NMS and the NBBO have been among the biggest obstacles to unlocking tokenized equities. If Rule 611 is rescinded, he said, “it’s a whole new ballgame.”

He added:

“Major unlock for DeFi. Incumbents won’t be happy.”

That reaction reflects a view spreading among digital-asset firms: tokenized equities do not need a technological breakthrough as much as a regulatory pathway. Securities are already largely electronic.

In the US, ownership is recorded through a system of depositories, brokers, and transfer agents. Tokenization would change the ledger and settlement architecture, not the economic concept of a share.

The harder question is whether that new architecture can satisfy the obligations embedded in securities law and market-structure rules.

That is where the SEC proposal becomes important. If the trade-through rule is rescinded, the focus would likely shift more heavily toward best execution, the broker-dealer obligation to use reasonable diligence to obtain favorable terms for customers under prevailing market conditions.

Indeed, Thorn said that the framework is more compatible with blockchain trading than a per-trade NBBO protection requirement. A broker routing to an on-chain pool could review execution quality over time, compare venues, and document its routing process.

He said:

“That framework can accommodate an AMM. The old one never could.”

A broader market-structure fight

Meanwhile, the proposal also reaches beyond tokenized shares.

Max Resnick, lead economist at Anza, a Solana-focused development firm, said rescinding Rule 611 could affect long-running debates over exchange design, including asymmetric speed bumps.

Speed bumps are delays used by some trading venues to reduce the advantage of ultra-fast market participants. Asymmetric speed bumps treat different order types or market participants differently, which has made them contentious in the US market structure.

Resnick said Rule 611 made those models harder to approve because a venue with an asymmetric speed bump could post tighter quotes than venues without one. If those quotes were included in the consolidated tape, other exchanges could be forced to match prices they could not economically support.

His point underlines why the SEC move is not only about crypto. Rule 611 has influenced how venues compete, how liquidity is displayed, and how firms route orders. Removing it would change the incentives for exchanges and brokers across the equity market.

SEC Chairman Paul Atkins has framed the proposal as an overdue review of a rule he believes created unintended consequences. The agency said the change is intended to simplify market structure, reduce costs, and allow competition and innovation to shape equity trading.

That language has drawn attention from tokenization advocates because it overlaps with the SEC’s broader digital-asset agenda.

Atkins and Commissioner Hester Peirce have previously discussed an innovation exemption that could allow limited experimentation with tokenized securities trading through automated market makers and other on-chain systems.

Such an exemption could include safeguards such as volume limits, whitelisting, and a temporary framework while the agency considers permanent rule changes.

Thorn said the sequencing is important. In his view, the SEC is first seeking to remove one of the hardest market-structure obstacles and then address venue-registration issues through an innovation exemption.

At a high level, he said, the agency appears to be following the “Project Crypto” playbook.

The caveats remain large

Despite this potential rulemaking, the risk for investors is that tokenized stocks can mean many different things.

A token may represent a direct share, a custodial claim, a depositary receipt, a derivative, or a synthetic instrument that tracks a stock price without giving the holder voting rights, dividends, or a claim on the underlying security. Those distinctions matter, even if the token trades at a price close to the public share.

That is why rescinding Rule 611 would not, by itself, legalize tokenized equities. Firms would still need to answer questions about whether the product is registered, where it trades, who holds the underlying asset, how corporate actions are handled, whether investors receive shareholder rights, and how settlement works.

Thorn stated:

“Tokenized NMS stocks still face a host of other questions re: exchange/ATS registration questions, clearance and settlement, and many other rules not designed for defi or peer-to-peer trading.”

In view of this, Anthony Bassilli of Coinbase Asset Management described the SEC proposal as a clearing hurdle for tokenizing stocks in the US, while adding that the process remains important to watch.

That caution is shared by traditional-market groups. SIFMA, the trade group representing broker-dealers, investment banks, and asset managers, welcomed the SEC’s review but warned that the US market structure is made up of many interconnected pieces.

It said regulators should study the effect of any changes on investors, execution quality, transparency, and the development of overnight trading and tokenized securities.

Those concerns are likely to shape the public comment period. Critics may argue that removing Rule 611 could fragment markets, weaken displayed quotes, or make it harder for ordinary investors to know whether they received a fair price.

On the other hand, crypto supporters will argue that best execution, competition, and better market design can replace a rule they view as overly rigid.

The post SEC targets 20-year-old rule standing between Wall Street and blockchain trading appeared first on CryptoSlate.

Bitcoin’s largest buyers are no longer behaving like a reliable backstop for the largest cryptocurrency.

The exchange-traded funds, public-company treasuries, and Bitcoin-linked equities that helped define the market’s institutional era are showing signs of strain, just as the world’s largest digital asset struggles to hold above $60,000, one of its most closely watched price levels.

This persistent drawdown has prompted a broader reevaluation of the cryptocurrency’s role in institutional portfolios, raising questions about whether the current environment reflects a temporary profit-taking exercise or a structural retreat from digital assets.

Bitcoin ETF demand turns into a headwind

The clearest reversal has come from US spot Bitcoin ETFs, which entered 2026 as one of the market’s most important drivers of demand.

For much of the period after their January 2024 debut, the funds were treated as evidence that traditional financial investors were steadily adopting Bitcoin.

Their inflows helped create a simple bull-market thesis that showed that access to Wall Street would bring more capital into a fixed-supply asset, giving Bitcoin a durable source of upward pressure.

However, that thesis has been tested heavily in recent weeks.

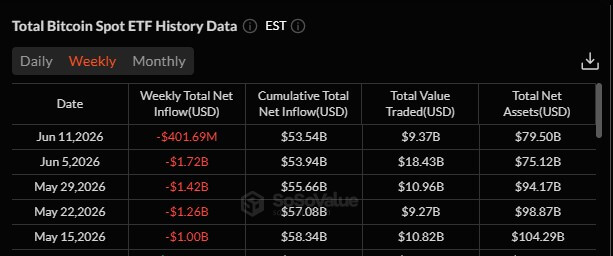

Data from SoSoValue shows US spot Bitcoin ETFs have recorded a five-week outflow streak totaling more than $5 billion.

This is further corroborated by Glassnode data, which shows the 30-day moving average of net ETF flows has fallen to -2,450 BTC per day, the fastest sustained pace of outflows since the products launched.

The size of that flow is significant because it exceeds the network's daily supply of newly created Bitcoin.

After the 2024 halving, miners produce about 450 BTC per day. A sustained ETF outflow of 2,450 BTC a day is more than five times that new supply, turning what had once been a source of absorption into a source of pressure.

Short bursts of ETF selling are not unusual in volatile markets. A negative 30-day moving average carries more weight because it smooths out daily noise and captures broader changes in positioning. Until that trend improves, institutional flows are less likely to provide support for Bitcoin prices.

Moreover, trading in the ETFs has also cooled. The 30-day moving average of daily volume in US spot Bitcoin ETFs has fallen to about $960 million from $4.4 billion in October, a 78% decline, Glassnode reported.

That decline points to more than simple profit-taking. It shows that speculative demand from traditional market participants has thinned even as redemptions have accelerated.

Lower volume can make price moves harder to absorb because fewer buyers are available when selling intensifies.

BTC DATs lose momentum

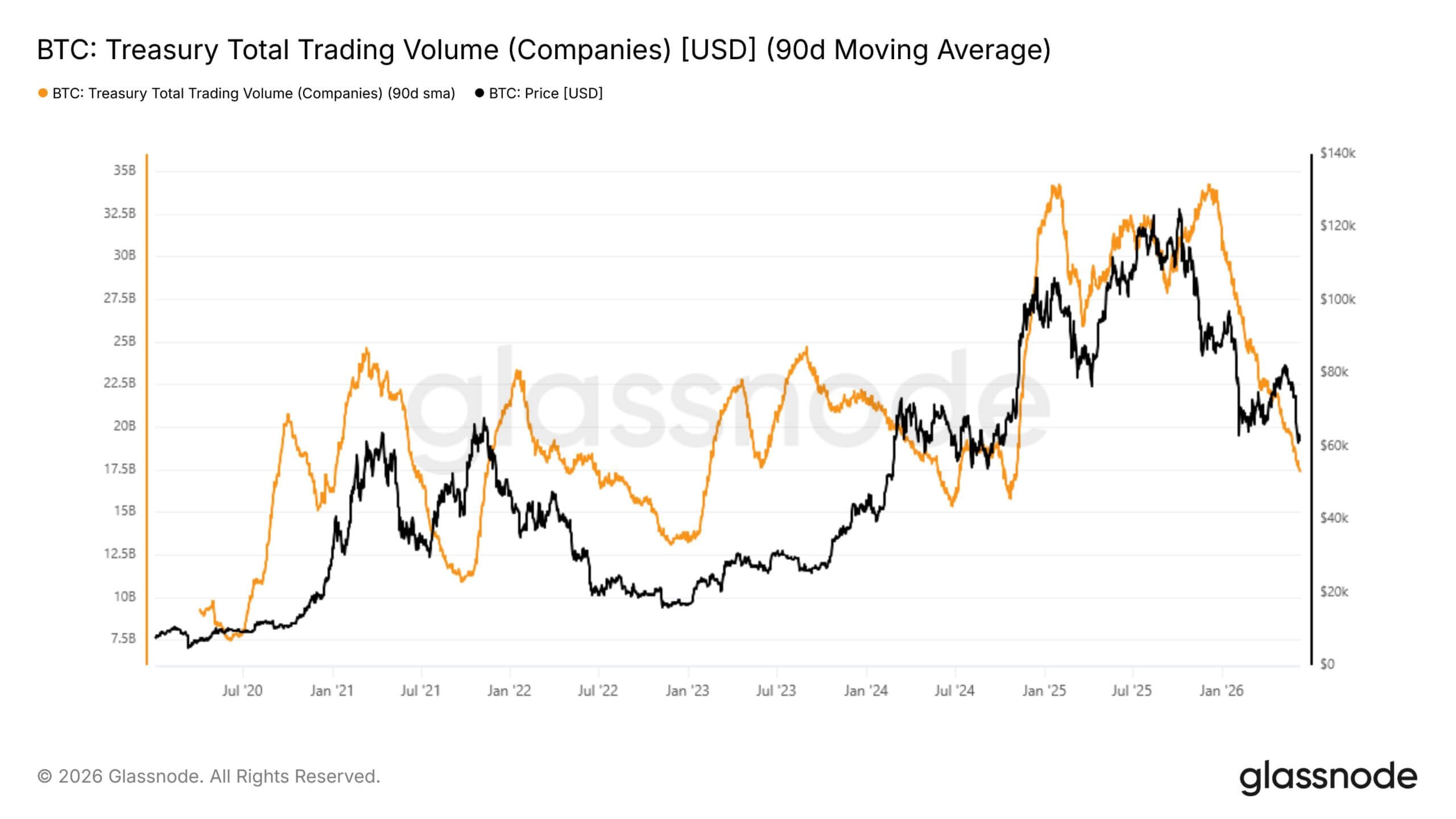

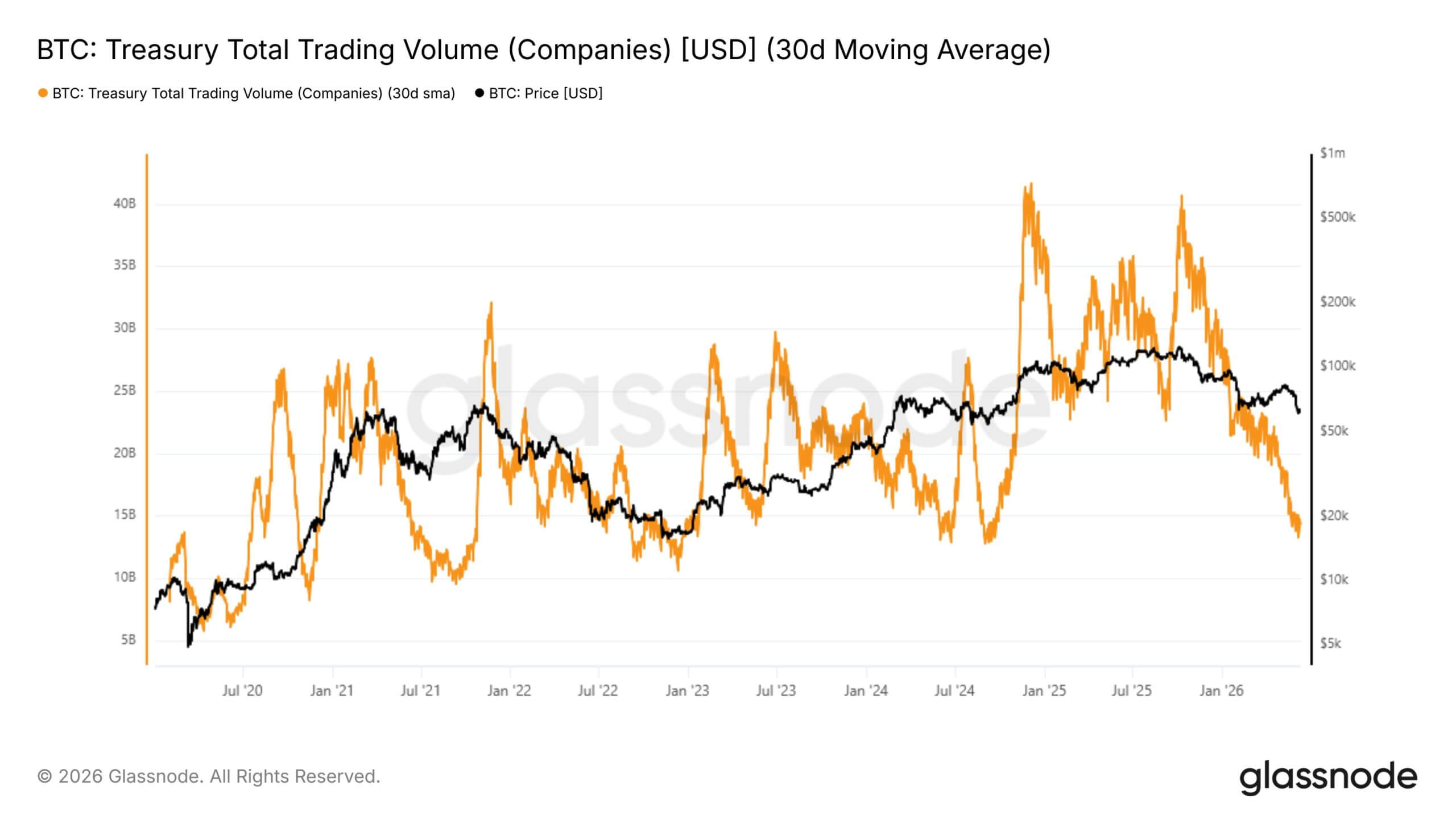

The ETF reversal has coincided with a slowdown in another major source of Bitcoin demand: digital asset treasury companies.

These firms, often listed publicly, raise capital or use balance-sheet resources to accumulate Bitcoin as a treasury asset. Their rise helped extend institutional adoption beyond ETFs, giving investors another way to express demand for Bitcoin through equity markets.

Like the ETFs, their buying has faded in June.

Glassnode analysts noted that while these companies remain net buyers overall, their daily accumulation has slowed to a fraction of the pace seen earlier in the quarter.

According to them:

“Corporate treasury accumulation has slowed sharply, with net inflows falling from peaks above $500 million per day to near-zero levels since June.”

This slower buying removes one of the market’s clearest sources of incremental demand at a time when ETF flows are also negative.

Some of the concerns have centered on Strategy, the largest public corporate holder of Bitcoin. The company disclosed that it sold 32 BTC in the final week of May, a small amount relative to its overall holdings but a symbolically important move because of its role in popularizing the corporate Bitcoin treasury model.

Strategy later returned to the market during the selloff, buying about $100 million worth of Bitcoin. However, the purchase did not stop the price from falling below $60,000.

Other BTC-focused companies have also drawn attention. Fold and Nakamoto have sold part of their Bitcoin holdings, adding to concern that the treasury-company trade is becoming less one-directional than it appeared during the rally.

While these sales do not amount to a broad retreat by corporate buyers, they show that some treasury firms are becoming more selective, more liquidity-conscious, and more willing to adjust positions as market conditions worsen.

That shift matters because the corporate treasury model depends partly on confidence. When share prices are strong, and investor demand is high, companies can raise capital, buy Bitcoin, and benefit from the perception that they are leveraged proxies for the asset.

However, when Bitcoin falls and demand for equities weakens, the model becomes harder to sustain.

Meanwhile, that slowdown is also evident in trading activity in these companies' equities.

Glassnode data show that the total daily trading volume for major publicly listed Bitcoin-holding companies, measured by the 30-day simple moving average, has dropped by 49% over about six months. Their volume fell from $34.2 billion in December to $17.4 billion as of press time.

That decline suggests investors are pulling back from the broader Bitcoin proxy trade, not just from the asset itself.

During stronger market periods, public Bitcoin holders often attract investors seeking leveraged exposure. Their shares could rise faster than Bitcoin's when sentiment improves because they combine treasury holdings, operating businesses, and capital-market optionality.

That made them popular vehicles for traders who wanted equity-market exposure to crypto without directly holding tokens. But as Bitcoin corrected, that demand has significantly weakened.

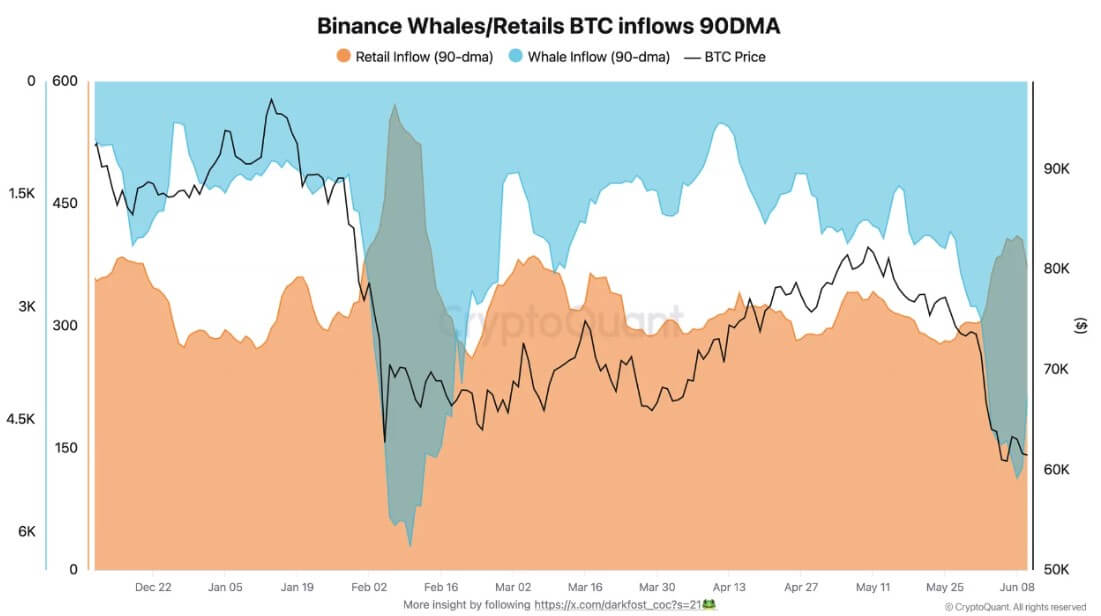

Exchange inflows signal broad market anxiety

The institutional distribution has created a climate of widespread market unease, affecting participants across the wealth spectrum.

Data from CryptoQuant indicates a significant rise in exchange deposits from both large-scale holders and retail investors. Typically, such deposits are associated with an intent to sell.

As Bitcoin briefly breached the $60,000 floor, large holders, or “whales,” accelerated their movement of assets to trading platforms.

Over the past three months, whale inflows to the Binance exchange have averaged 5,280 BTC per day, a sharp increase from the 1,900 BTC daily average observed in March. Retail investors have mirrored this behavioral shift, with their average daily exchange inflows climbing to 410 BTC.

This parallel movement highlights how macroeconomic uncertainty levels the playing field regarding investor psychology.

The current environment marks the second major episode of elevated exchange deposits this year. A similar pattern emerged in early February, when Bitcoin tested the $60,000 threshold, with whale inflows spiking to 6,200 BTC and retail inflows reaching 570 BTC.

Such periods of heightened market stress historically facilitate the transfer of assets from short-term speculators to long-term holders, though the immediate effect is substantial downward price pressure.

A thinner market waits for a catalyst

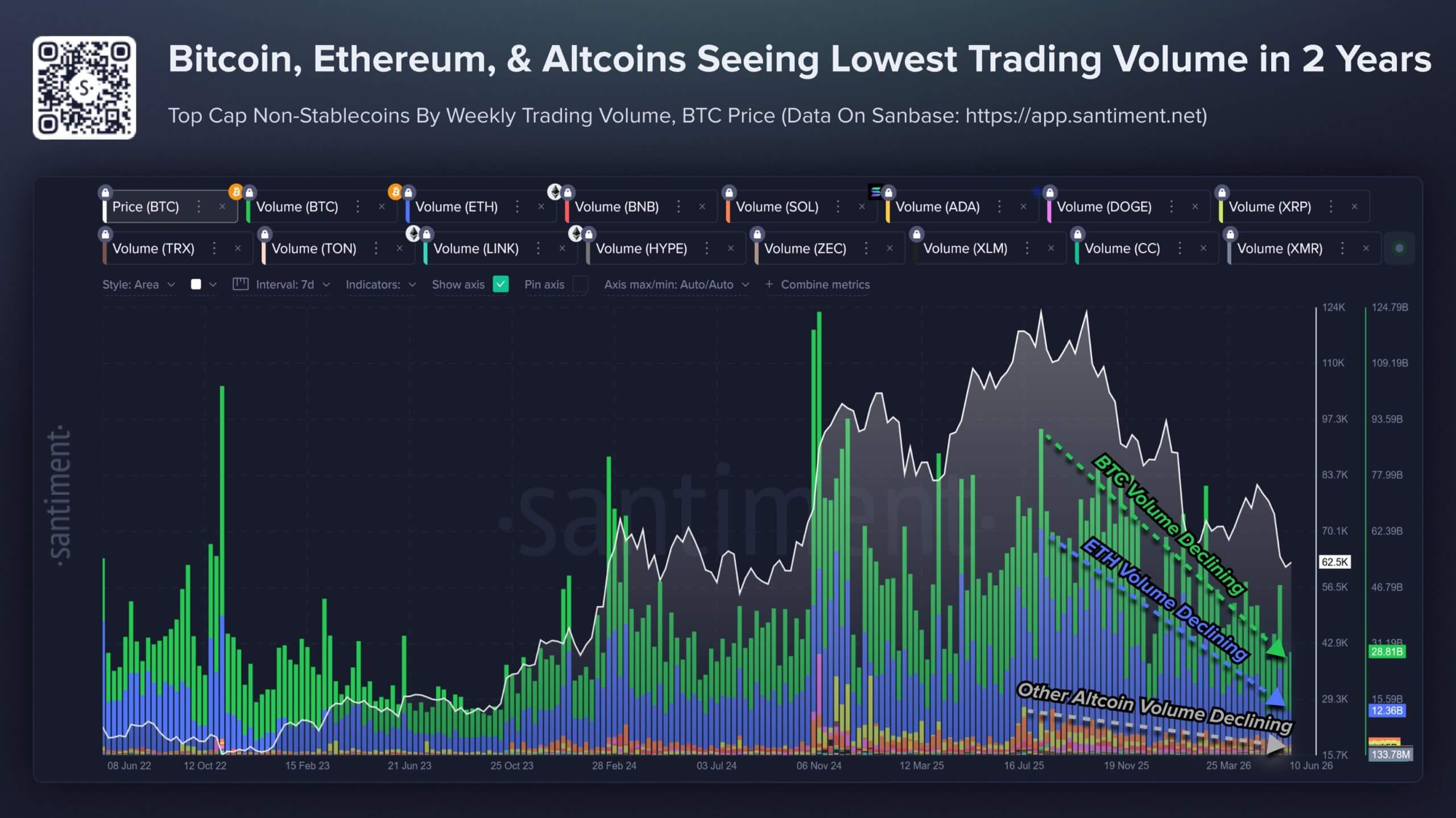

This overall market has arrived as broader crypto trading activity has also cooled.

Santiment data show trading volume across the largest non-stablecoin crypto assets has fallen to levels last seen in mid-2024. The decline reflects a market in which many traders appear unwilling to chase prices higher or sell aggressively amid recent liquidations, macro uncertainty, and geopolitical risks.

For Bitcoin, that creates a two-sided setup.

On one side, a thin volume can leave the market vulnerable. When participation is low and large buyers are less active, even moderate selling can have an outsized effect on price. A negative ETF flow trend, slower treasury accumulation, and weaker proxy-stock demand can therefore weigh more heavily than they would in a stronger liquidity environment.

On the other side, low volume can also indicate exhaustion. Some of crypto’s stronger rebounds have followed periods when trading activity, attention, and conviction were weak. Markets often recover when positioning has already been reduced and sidelined capital begins to return.

That possibility keeps the current setup from being a straightforward bear-market call. Bitcoin continues to have institutional holders, public-company buyers, and long-term investors. Development across the broader digital asset industry has not stopped, and the ETF market remains an established bridge between Bitcoin and traditional finance.

But the immediate question is narrower. Bitcoin does not need institutions to abandon it to face pressure. It only needs the largest buyers to slow down, sell selectively, or stop absorbing supply at the same pace.

That is what the market is confronting now.

Until ETF flows stabilize, treasury-company demand recovers, or trading activity returns to Bitcoin-linked equities, the market may remain exposed to a more difficult reality: the institutional bid is still there, but it is no longer strong enough to carry the trade on its own.

The post Bitcoin price faces new risk as big buyers lose conviction appeared first on CryptoSlate.

XRP is trading at $1.11, down roughly 17% from its June opening, having set a new 2026 low on June 5 and shed $8 billion in market cap over three sessions.

The correction happens as the asset posted its strongest ETF inflow month of the year, with $131.94 million captured in May, ahead of both Bitcoin and Ethereum products.

Glassnode's June 9 data points to loss realization as the primary pressure on XRP's price, with the token's 90-day realized profit-to-loss ratio falling to 0.38, meaning holders are booking roughly 38 cents in profit for every dollar of realized loss.

At the speculative peak in 2025, that ratio reached 50, with gains outpacing losses by 50 to 1.

Glassnode described the current reading as intense capitulation, with XRP's aggregate realized price sitting near $1.48, placing the average holder underwater at current prices.

On the XRP Ledger, the 90-day average of total fees paid fell from 5,900 XRP in February 2025 to 500 XRP by June 9, a 91.5% decline that Glassnode attributed to a near-total contraction in organic transaction demand since the prior speculative phase ended.

| Signal | Latest reading | Direction | What it means |

|---|---|---|---|

| XRP price | $1.11 | Bearish | Down roughly 17% from June open and at fresh 2026 lows. |

| May ETF inflows | $131.94M | Bullish | Regulated demand remains active despite price weakness. |

| 90-day realized profit/loss ratio | 0.38 | Bearish | Holders are realizing far more losses than profits. |

| Aggregate realized price | $1.48 | Bearish | Average holder is underwater at current prices. |

| XRP Ledger fees | 5,900 XRP → 500 XRP | Bearish | Organic transaction demand has collapsed 91.5%. |

What whales are actually doing

CryptoQuant’s exchange-flow analysis shows XRP whale outflow dominance reached 91.4% on Binance and 90.5% across centralized exchanges.

Whales dominate XRP's exchange flows, and the data describes that structural control without resolving whether it reflects selling pressure or accumulation.

A separate CryptoQuant post frames declining XRP inflows to Binance as a possible sign of growing whale confidence, arguing that subdued exchange inflows could keep available selling supply limited.

Large-holder accumulation has historically preceded recoveries, and Glassnode's loss-realization and fee data show that the current supply of loss-realizing sellers and the collapse in organic network demand are absorbing that accumulation before it reaches price.

| Data source | Metric | Reading | Bearish interpretation | Bullish interpretation |

|---|---|---|---|---|

| CryptoQuant | XRP whale outflow dominance on Binance | 91.4% | Whales dominate exchange flows, so large holders can pressure price. | Outflow dominance does not prove whales are selling into exchanges. |

| CryptoQuant | XRP whale outflow dominance across CEXs | 90.5% | Centralized-exchange flows are structurally whale-driven. | Concentrated flows may also reflect custody movement or accumulation behavior. |

| CryptoQuant | XRP inflows to Binance | Declining | Weak demand may reduce the need to send coins to exchanges. | Lower inflows may mean reduced available selling supply. |

| Santiment | Wallets holding 10M+ XRP | 45.83B XRP | Concentration risk remains high. | Largest wallets held the most XRP since May 2018. |

| Santiment | Wallets holding 10K+ XRP | 332,230 | Accumulation has not yet created a price floor. | Mid-to-large wallet count reached an all-time high. |

Santiment's May data note that wallets holding at least 10 million XRP controlled 45.83 billion XRP, the most since May 2018. The number of wallets holding at least 10,000 XRP reached an all-time high of 332,230.

Large-holder accumulation has historically preceded recoveries, and Glassnode's loss-realization and fee data show that the current supply of loss-realizing sellers and the collapse in organic network demand are sufficient to absorb that accumulation without forming a price floor.

The ETF layer

Seven US spot XRP ETFs are now live, holding approximately 923.7 million XRP in custody as of June 10, with combined AUM near $1 billion.

Cumulative net inflows since the November 2025 launch have approached $1.45 billion, and May's $131.94 million monthly inflow was the strongest since December and ran for 20 consecutive days before a $5.34 million outflow on June 3 broke the streak.

CoinGlass ETF data show that regulated demand for XRP exists and has been persistent, while price action indicates that demand has been absorbed by spot market selling or loss realization, without producing a sustained rebound.

Standard Chartered has projected $4 billion to $8 billion in XRP ETF inflows for 2026 if the CLARITY Act passes, a figure far above cumulative inflows to date.

That upside depends on a Senate floor vote, which Polymarket currently prices at a 47% likelihood of passing in 2026.

Goldman Sachs liquidated its entire $154 million XRP ETF position in the first quarter, a reminder that institutional positioning on XRP runs in both directions simultaneously.

Two ways this resolves

In the bull case, ETF inflows continue to expand as the CLARITY Act advances toward a floor vote, the 332,230 large-wallet holders who accumulated amid price weakness provide a bid at current levels, and Glassnode's loss-realization ratio begins to recover as capitulating sellers exhaust their supply.

XRP stabilizes above $1.00, network fees find a floor, and the ETF bid becomes visible in price.

Under that sequence, $0.90 stays a reference point on the chart where a multi-year rising trendline sits, with the ETF bid absorbing sell pressure before that level is reached.

In the bear case, the Glassnode capitulation metrics persist long enough for the ETF bid to prove insufficient to defend the $1.00 psychological level. Loss-realization selling continues at a higher rate than profit-taking, network fees stay depressed, and the gap between institutional demand and organic on-chain demand widens further.

If $1.00 fails, $0.90 becomes the next zone where accumulation would be tested, roughly 19% below current prices and near the cost basis of long-term holders who built positions through the 2024-2025 cycle.

Polymarket's June crowd prices the bear case as the most probable outcome, assigning a 47% probability to XRP losing $1.00 before month-end.

| Scenario | What needs to happen | Key level | Confirmation signal | Market meaning |

|---|---|---|---|---|

| Bull case: ETF bid absorbs supply | ETF inflows continue, CLARITY odds improve, and loss-realization pressure fades. | Above $1.00 | Realized profit/loss ratio rises from 0.38, fees stabilize, ETF inflows remain positive. | XRP forms a floor before testing $0.90. |

| Base case: weak range chop | ETF demand persists, but organic network activity remains depressed. | $1.00–$1.11 | Price fails to reclaim higher levels, but $1.00 holds. | ETF demand offsets selling, but does not create a rally. |

| Bear case: $1.00 breaks | Capitulation metrics persist and ETF inflows are absorbed by spot selling. | $0.90 | XRP loses $1.00, fees remain near lows, realized losses keep dominating. | $0.90 becomes the next accumulation test. |

| Stress case: ETF bid reverses | ETF outflows, broader crypto weakness, or CLARITY failure hits during capitulation. | Below $0.90 | ETF demand turns negative and large exchange inflows rise. | XRP shifts from reset risk to structural breakdown risk. |

ETF inflows show that regulated buyers exist and have been accumulating at steadily lower prices. Glassnode's data shows that spot holders are capitulating, and organic network demand has contracted sharply.

Both conditions can coexist until one overwhelms the other, and at a 90-day realized profit-to-loss ratio of 0.38, the capitulation arithmetic still has further to run.

The post XRP aims for $0.90 as ETF demand battles selling pressure from whales appeared first on CryptoSlate.

Google blocked or removed 8.3 billion ads in 2025 and suspended 24.9 million advertiser accounts, with 602 million of those ads tied directly to scams.

Those numbers show that the volume of fraudulent material attempting to reach users has grown large enough to require an AI system operating at an industrial scale to contain it.

Gemini now analyzes hundreds of billions of signals in real time, such as account age, behavioral cues, and campaign patterns, catching over 99% of policy-violating ads before they run.

The fraction that cleared that filter still reached users across one of the world's largest ad networks.

Generative AI has made fake ads, fake users, fake clicks, and fake devices cheaper to produce and harder to distinguish from legitimate activity.

Traditional solutions have proved inadequate as AI-driven fraud evolves faster than detection methods. Google's answer of using more AI deployed faster commits both sides to continuous escalation.

A separate group of companies is building verification systems that record who saw an ad and make that record permanent.

| Metric | Figure | What it shows |

|---|---|---|

| Ads blocked or removed by Google in 2025 | 8.3B | Fraudulent or policy-violating ad volume is massive. |

| Advertiser accounts suspended | 24.9M | Bad actors are operating at account-farm scale. |

| Scam-related ads removed | 602M | Scams are a major category inside the broader fraud problem. |

| Policy-violating ads caught before serving | 99%+ | AI defense is working, but only by processing enormous signal volume. |

| Signals analyzed by Gemini | Hundreds of billions | Ad safety is becoming an AI-vs-AI infrastructure fight. |

The verified attention model

Hakuhodo, the Japanese advertising giant, partnered with Tools for Humanity and LG Electronics to test a “Human-Verified Ad Network” that served ads exclusively to human-verified users, with every impression logged to LG's blockchain infrastructure.

The pilot ran in Japan from July through August 2025, involving more than 3,500 participants and ten advertisers across electronics, travel, food, cosmetics, and education.

Hakuhodo integrated its “boba” mini-app with World ID verification and LG's blockchain ledger, creating a closed loop where only human-verified users received ads and every impression was recorded on-chain.

World ID lets users prove they are unique humans without revealing personal information. Under that architecture, advertisers pay for impressions that carry a verification receipt tied to a confirmed human identity.

According to figures reported by the companies involved, the pilot produced a 50% increase in click-through rates and a 15-point improvement in bounce rates.

A mainstream electronics company and Japan's second-largest advertising agency ran a blockchain verification test on a live campaign and published the results, separating this move from white paper proposals.

The verified conversion model

In January 2025, Coinbase acquired Spindl, an on-chain ads and attribution platform rebuilding the ad-tech stack on-chain, to address what Coinbase called the “on-chain discovery problem” for blockchain app builders.

Spindl was founded by Antonio García Martínez, an early member of the Facebook ads team who shipped Facebook's first version of keyword targeting, audience targeting, and Facebook's programmatic ad exchange FBX.

Spindl focuses on proving that an ad drove real action, such as a wallet interaction, an app install, a token purchase, or a staking event.

Traditional attribution systems infer causality from cookies, click paths, and probabilistic matching. Spindl traces a user journey from a web click to an on-chain action, providing advertisers with a ledger entry and a verifiable chain of custody.

Spindl operates on Base, Coinbase's Ethereum layer-2 network, and maintains open standards for publishers and advertisers.

The two models address different parts of the same problem: Hakuhodo and LG verify that a human saw the ad, and Spindl verifies that the ad resulted in a real action.

| Model | Example | What it verifies | How blockchain is used | What advertisers get |

|---|---|---|---|---|

| Verified attention | Hakuhodo + LG + World ID | A real human received the ad | Impression history is recorded on-chain after proof-of-human verification | A receipt that the ad reached a verified human user |

| Verified conversion | Coinbase + Spindl | An ad led to a real action | User journey is traced from click to wallet or app event | Attribution from campaign spend to on-chain outcome |

| Conditional payout layer | Future extension | Whether a verified event occurred | Smart contracts or rules-based systems release payment after proof | Pay-for-outcome ad settlement |

| Wallet-based targeting | Crypto apps, gaming, commerce | Audience relevance based on on-chain behavior | Wallet activity helps define segments or campaign eligibility | Targeting without relying only on cookies or device IDs |

Why this matters beyond crypto

Dentsu's May 2026 global ad forecast puts worldwide ad spend at $1.06 trillion, with digital accounting for 69% of that total. IAB and PwC reported that US digital ad revenue reached $294.6 billion in 2025, with programmatic advertising up 20.5% to $162.4 billion.

The same automated systems that make programmatic buying efficient also expand the surface area where fake inventory, fake users, and fake outcomes get monetized.

Juniper Research estimated that global ad spend lost to fraud would rise from $84.2 billion in 2023 to $172.3 billion by 2028, as AI enables fraudsters to mimic human behavior and evade detection systems.

DoubleVerify found that bot fraud accounted for 65% of all fraud in CTV environments in 2024, with compromised devices simulating real user behavior to deceive measurement systems.

When a fake device can convincingly impersonate a living room viewer watching premium inventory, the platform's reported delivery numbers are unverified claims.

Blockchain's pitch to advertisers in that environment is a receipt: an immutable record of what the system observed, attached to a verified identity and fixed at the moment of delivery.

What blockchain cannot do on its own

A blockchain faithfully and permanently records inputs, but its trustworthiness depends on the verification layer that precedes it.

If the identity verification layer is gamed, the fraudulent identity receives the same permanent record as a legitimate one.

The hard problem is the oracle layer: confirming that the viewer was human before the record is written, that the device was legitimate, that the impression was viewable, and that the downstream action was genuine.

World ID's design separates proof of personhood from personal identity, allowing users to prove uniqueness without revealing their identity.

Advertising is a trust-sensitive use case, and combining human verification, ad targeting, and wallet behavior into a single system will face regulatory and consumer scrutiny in markets where biometric data collection is actively contested.

The adoption constraint is the third. Google, Meta, Amazon, and the major CTV platforms control their own measurement systems and have little incentive to adopt a neutral blockchain-based receipt layer that would weaken their hold on attribution.

Blockchain's most practical near-term path runs through markets where platform owners have an incentive to increase advertiser trust: crypto apps, independent CTV inventory, rewards campaigns, wallet-based commerce, and gaming.

Two ways this develops

In the bull case, advertisers running high-value performance campaigns demand verifiable logs as proof that probabilistic measurement can no longer supply.

Blockchain verification integrates with existing ad stacks as a parallel audit trail for campaigns where fraud risk justifies the additional infrastructure.

Juniper projects $172.3 billion in ad fraud losses by 2028, and redirecting even 1% to 3% of that figure through verified proof systems points to a protected value pool of roughly $1.7 billion to $5.2 billion.

| Scenario | What happens | Value pool | Where adoption happens first | What blocks adoption |

|---|---|---|---|---|

| Bull case | Advertisers demand verifiable logs for high-fraud campaigns and performance outcomes. | $1.7B–$5.2B protected value pool if 1%–3% of projected 2028 ad-fraud losses move through proof systems. | Crypto apps, rewards campaigns, independent CTV, gaming, wallet commerce, high-value performance ads. | Integration with existing ad stacks and privacy-safe identity design. |

| Base case | Blockchain becomes a parallel audit trail for specific high-risk channels, not a full replacement for Google or Meta measurement. | Niche but commercially meaningful fraud-protection market. | Web3 apps, CTV experiments, on-chain commerce, affiliate attribution. | Advertiser education and fragmented standards. |

| Bear case | Google, Meta, Amazon, and CTV platforms improve AI fraud detection enough to keep measurement in-house. | Blockchain remains a niche verification layer. | Crypto-native apps and limited proof-of-human pilots. | Platform resistance, biometric scrutiny, weak advertiser adoption. |

The Hakuhodo model scales through mainstream platforms, Spindl extends attribution beyond crypto-native apps, and the user never knows that the infrastructure beneath it is a blockchain.

In the bear case, Google, Meta, and CTV platforms improve AI-based fraud detection fast enough that the marginal value of a blockchain receipt layer stays narrow.

Regulatory pushback against biometric proof-of-human systems slows adoption of the verified attention model in key markets.

Blockchain ad tech stays useful inside crypto apps and niche high-fraud channels but fails to cross into the programmatic mainstream.

The $162.4 billion US programmatic market continues flowing through the existing measurement stack, with its fraud losses treated as an accepted line item.

AI has made fake behavior cheap enough that detection systems may permanently lag behind fraud generation. If advertisers conclude that probabilistic measurement can no longer be trusted, blockchain proof systems are positioned to absorb that budget.

The post Firms are turning to blockchain to fight an ad fraud problem AI is making worse appeared first on CryptoSlate.

CryptoTicker.io

SpaceX did what a heavily oversubscribed mega-IPO is supposed to do — it popped, held most of the gain, and closed comfortably above its offer price. The more interesting story sits one layer down, in the tokenized and crypto-native products that launched alongside it. There, the day split cleanly into two outcomes: products that actually controlled the underlying shares worked, and the one model that relied on a middleman to find shares at the last minute did not. That divide, more than the stock's 19% gain, is what this debut will be remembered for.

How SPCX Actually Traded

The headline numbers were strong without being euphoric. Shares opened at $150, peaked at $176.52 intraday, and closed at $160.95 — up about 19% from the $135 offer price. That close translated to roughly a $2.1 trillion market cap, making SpaceX the seventh-largest public company in the world on its first day. The raise itself — about $75 billion on more than 555 million shares — locked in the record as the biggest IPO in history.

What's worth reading into the shape of the day: the stock hit its high in the early afternoon and then gave back a chunk into the close. Shares pared gains heading into the closing bell but still finished up around 19%, and analysts framed the day as a success given the healthy gain, limited volatility, and record retail demand. A debut that opens high, spikes, and settles back is the textbook signature of strong-but-rational demand — not the kind of disorderly first-day mania that often unwinds painfully in week two.

The Gap Nobody's Talking About: Expectations vs. Reality

Here's a nuance most recaps gloss over. A 19% pop is excellent by historical IPO standards — but it landed below what speculative markets had been signaling for weeks. IPO researcher Jay Ritter called the open "disappointing relative to what betting markets had been predicting," while noting it was still clearly positive, and that if the price holds, the dollar value of early returns would exceed any IPO in history.

That gap is the tell. In the run-up, pre-IPO perpetual futures had priced SpaceX as much as 60% above the offer at one point. By debut day, the Hyperliquid SPCX-USDC perpetual was trading around $176, roughly 30% above the IPO price, before easing toward $172. So the public market essentially met the floor of crypto's expectations but undercut its earlier highs. The speculative premium was real, and it compressed as the actual print arrived — a useful reminder that pre-IPO derivative prices are sentiment gauges, not forecasts.

And the valuation question the market shelved for a day hasn't gone away. SpaceX remains unprofitable, with $18.7 billion in revenue last year and an $8.7 billion loss between the start of 2025 and the end of March 2026. A $2 trillion price tag on those fundamentals is a bet on Starlink and Starship execution, not current earnings — which is exactly why the Monday open and the weeks after matter more than Friday's fireworks.

How the Crypto Market Reacted

The crypto angle here isn't incidental — for two weeks, SpaceX had been actively pulling money out of digital assets. Capital rotation into the listing compressed crypto liquidity for over two weeks, and analysts expected sidelined capital to gradually rotate back into risk assets once SPCX began trading. So when the overhang finally cleared on Friday, the majors caught a bid.

Bitcoin ($BTC) held the line as the market's anchor. Bitcoin traded near $63,262, up about 0.4% on the day; it briefly retraced after a hot US Producer Price Index print of 6.5% year-over-year, but buyers defended the demand zone and BTC recovered. Ethereum ($ETH) was steadier than spectacular. Ether sat broadly flat at around $1,653.

The standouts were further down the cap table. XRP ($XRP) put in its best session in a week. XRP added about 2.39%, its strongest session in over a week, as improving legal clarity and institutional appetite returned to the asset. And Solana ($SOL) was the most directly tied to the SpaceX story, since it hosted the tokenized stock. Solana advanced about 2.84%, supported by the tokenized SPCX share launch and elevated FIFA World Cup fan-token volumes on its network.

The bigger read: the market shifted from two weeks of relentless selling to cautious optimism, helped by easing US-Iran tensions and the SpaceX IPO finally pricing. The relief was real, but worth keeping in perspective — the hot inflation print and the June 17 Fed meeting are the next macro tests, so Friday's green board is a tone shift, not an all-clear.

Where the Tokenized SpaceX Trade Split in Two

This is where the debut got genuinely instructive. Several tokenized versions of SPCX were built to go live the moment the stock did, letting non-US and crypto-native traders get exposure without a traditional brokerage. Most of them delivered. The products that issued tokens against shares they actually held — onchain or via a regulated broker-dealer — opened and traded as planned.

Then there was the route that didn't hold any shares of its own. Four platforms had to scrap their allocation campaigns outright. Binance, Bybit and Bitget canceled their tokenized SpaceX allocation campaigns and refunded subscribers in full after xStocks, the provider routing the deals, could not source the underlying shares — even as xStocks' own onchain token and rival protocols launched the same morning. MEXC was caught in the same shortfall.

*Investments carry risks. Trade responsibly.

The amount of money that got parked and then unwound is the part that should make exchanges think twice. Binance's campaign alone had taken in over $557 million in USDC before being cancelled for "circumstances outside of our control." Bybit told users that "due to xStocks' inability to deliver the underlying assets, no SpaceX allocations were received," and Bitget said it couldn't secure and distribute the tokens it had promised. The consolation packages tell you how much goodwill was at stake: Bybit added a 10% reward and Bitget offered fee refunds plus future whitelisting and a gas voucher, while Binance pledged $1 million in shares via its own bStocks product, with CZ posting "Protect users when things don't go as planned."

--> Check out here all the options to Trade SpaceX stocks

Why This Is the Real Headline

Strip away the branding and the failure maps the architecture of tokenized equity perfectly. The deciding variable wasn't whether a product was onchain, decentralized, US-listed, or a perp — it was who controlled the shares. Everything backed by real, held inventory settled. The one design that outsourced share-sourcing to an intermediary at the last moment is the one that collapsed under demand.

That matters because the usual pitch for tokenized stocks is access and speed. As industry participants put it, the problem wasn't tokenization itself but getting the underlying asset — SpaceX's retail demand simply overwhelmed the shares available, leaving many orders unfilled. And the fine print had warned about exactly this: xStocks' own disclaimers stated its IPO tokens offered price exposure only, with no guaranteed allocation and no direct ownership. The lesson for the next blockbuster listing — Anthropic and OpenAI are both circling the public markets — is concrete: allocation-campaign tokens now carry a proven sourcing risk that platforms will either have to price honestly or stop offering.

What to Watch Next

Friday answered the easy question (does SpaceX pop?) and left the harder ones open. Three things worth tracking: whether SPCX holds above its $160 close once first-day euphoria fades, the index-inclusion buying wave that could hit as early as July as trackers are forced to add the stock, and whether the refunded crypto exchanges return for the next mega-IPO with a share-backed model instead of a promise to source. As one outlet put it, when markets reopen Monday, SPCX will be closely watched all over again

SpaceX has officially entered public markets, and its long-awaited IPO is already one of the biggest market events of 2026. After years of speculation around when Elon Musk’s space and satellite giant would finally go public, SpaceX shares began trading today under the ticker SPCX, immediately attracting massive investor attention.

The stock opened around $152, already well above its IPO price of $135, before climbing further during early trading. At the time of writing, SpaceX stock is trading around $172, marking a strong first-day jump and showing just how intense demand has become for one of the most anticipated listings in market history.

Why Is SpaceX Stock Surging Today?

The first-day rally is mainly being driven by a mix of hype, scarcity, and long-term growth expectations. SpaceX is not just viewed as a rocket company anymore. Investors are also pricing in the future of Starlink, satellite internet, space infrastructure, government contracts, possible AI-related expansion, and Elon Musk’s broader tech ecosystem.

The IPO has also created a strong fear of missing out among retail and institutional investors. With SpaceX now trading publicly, many investors who were previously unable to access the private company are rushing to gain exposure.

This strong demand helped push the stock from its IPO price of $135 to an opening level near $152, before the rally continued toward the $170 zone.

Is a SpaceX Crash Coming After the IPO Pump?

The big question now is whether SpaceX stock can continue climbing or whether the first-day excitement could quickly turn into a sharp correction.

A short-term pullback is definitely possible. IPO stocks often experience extreme volatility during their first trading sessions, especially when the opening price rises far above the original IPO price. Early investors may take profits, traders may exit after the initial hype, and valuation concerns could pressure the stock if momentum slows.

SpaceX is already trading at a massive valuation, which means expectations are extremely high. If the market starts questioning whether the company can justify that valuation through revenue growth, profitability, and future expansion, SPCX could face a strong correction.

In that scenario, the stock could fall back toward the $150 opening area, or even retest levels closer to the $135 IPO price if selling pressure increases.

*Investments carry risks. Trade responsibly.

Could SpaceX Stock Keep Going Higher?

On the other hand, SpaceX could continue moving higher if demand remains strong. The company has a rare position in the market, combining space exploration, satellite internet, defense contracts, and futuristic growth narratives. Few public companies offer the same level of exposure to the commercial space economy.

If buyers continue to dominate and the stock holds above the $170 level, the next psychological target could be the $180 to $200 range. A move above $200 would likely confirm that investors are willing to pay a significant premium for SpaceX’s long-term potential.

However, the higher SPCX climbs in the first days of trading, the greater the risk of a sharp correction if momentum fades.

What Should Investors Watch Next?

The most important levels to watch now are the $170 area, the $150 opening zone, and the $135 IPO price.

If SpaceX holds above $170 and continues gaining volume, bullish momentum could stay in control. But if the stock drops below $150, it may signal that the IPO hype is cooling down and that early buyers are starting to take profits.