Cryptocurrency Posts

Crypto Briefing

The Upbit listing highlights the potential for increased integration of Babylon's technology into mainstream DeFi, boosting its market influence.

The post Babylon token BABY surges 53% after Upbit listing appeared first on Crypto Briefing.

Rising Treasury yields and anticipated Fed rate hikes could shift investment from riskier assets to traditional fixed-income securities.

The post Treasuries tumble as traders price in Fed rate hike after strong jobs data appeared first on Crypto Briefing.

The conflict's unpopularity weakens Trump's political standing, reducing the likelihood of escalation and bolstering Iran's regime stability.

The post 100 days into Iran war, Trump struggles with US support and political fallout appeared first on Crypto Briefing.

Space-based computing could revolutionize industries, potentially generating trillions in revenue within the next decade.

The post Andrew Feldman: Going public creates unnecessary burdens, military contracts drive 60% of Planet’s revenue, and space-based data centers could revolutionize computing | All-In Podcast appeared first on Crypto Briefing.

The hefty fine and client outflows highlight the critical need for robust compliance systems to maintain investor trust and market stability.

The post Western Asset Management Company fined $100M by SEC for misconduct appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

The Hyperinflation of 1971 at the Kindergarten

I’m pretty sure it was 1971, but it could have been 1972. In any case, it was in kindergarten, and I was five years old. Our teachers had set up a system to motivate us kids to behave well. They had hung a big board on the wall, with all of our names listed. If you were particularly well-behaved, kind, helpful, or polite, they drew a black dot next to your name. Misbehave, and they gave you a red one. It was all about following the kindergarten rules, and the absolute transparency of it motivated most of us to try our best.

At some point, an extra prize was introduced for exceptionally good behavior: a small piece of fabric. From the group’s standpoint, that was worth much more than the top ranking in a row of black dots. And it was tangible. You could prove your elite status, even out in the sandbox.

Eventually, a trading system developed between us kids. For a scrap of fabric, you could get a bucket of sifted sand. For two, you could get a piece of candy. Suddenly, we could trade labor (sifting sand) for status symbols or sweets.

Then one day, a new teacher arrived. For whatever reason, she much more generously handed out those scraps of fabric. She simply changed the rules governing their distribution. All of a sudden, everyone had them, and you had to spend four for a piece of candy instead of two. Some of the kids started to complain. Their hard-earned scraps of fabric were now worth less, and they demanded more of them.

As you’d expect, the fabric scraps were given out more and more freely. Before long, anyone could take as many as they wanted. Eventually, they were lying around all over the place. They were worthless. No one wanted them anymore. You couldn’t trade them for anything. And so, at just five years old, I experienced genuine hyperinflation.

What does this have to do with Bitcoin?

In kindergarten, the rules were simply changed. The new teacher wanted to be nice, we kids whined, and suddenly more and more fabric scraps were handed out.

The rules of Bitcoin simply cannot be changed.

It’s a completely different story with our fiat currencies. They too have rules. The problem is that no one can ensure those rules are actually followed. Here is an example: the European Central Bank is not allowed to permanently finance governments through bond purchases, yet it does so anyway, brazenly and with no one doing—or even being able to do—anything about it. And who would intervene anyway?

Here’s another example. The Maastricht Treaty’s Stability and Growth Pact stipulated that the budget deficits of EU member states could not exceed 3% of their GDP, although permissible exceptions were built in. However, between 2000 and 2010, the Stability Criteria were repeatedly violated without sanctions—not only by Greece (11 times) but also by larger countries such as Italy (seven times), France (six times), and Germany (five times). According to the Maastricht Treaty, there are clear sanctions for countries that unlawfully fail to adhere to the deficit limit. But not once has such a sanction been imposed. No attempt was ever even made.

This may have been politically expedient and justified for whatever reason, but it shows how difficult it is for us to adhere to the rules. It’s like the New Year’s resolutions that we make with the greatest of convictions, but then usually don’t stick to for very long. The result is what matters. Currencies inflate and, sooner or later, become worthless. The U.S. dollar has lost 97% of its value over the last hundred years. The British pound, which originally represented a pound of silver, has suffered the same fate. All because more and more new dollars, euros, or pounds have been created, or to put it differently, printed.

The outcome is the same: when the fabric scraps become worthless, everyone who holds them loses their wealth.

This cannot happen with Bitcoin. Its rules are fixed, and no one controls the system nor can they simply change those rules.

Discover more in Bitcoin: The Honest Money!

This excerpt is just the beginning. Dive deeper into how inflation devalues your money, your savings, and your time in Bitcoin: The Honest Money by Alex von Frankenberg, Ph.D. The paperback is available now.

Order your copy here!

This post The Hyperinflation of 1971 at the Kindergarten first appeared on Bitcoin Magazine and is written by Alex v. Frankenberg.

Bitcoin Magazine

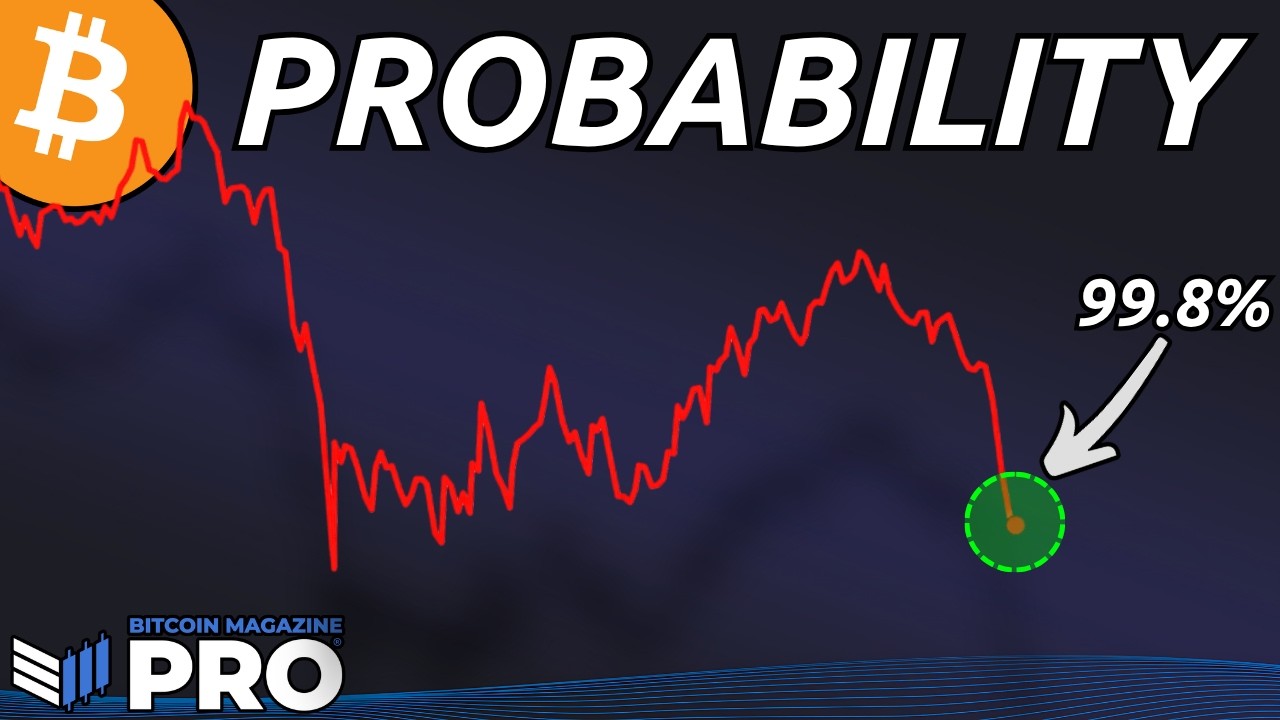

5th Worst Bitcoin Price Action Ever — I’m Buying At 99.8% Probability

The bitcoin price looks bad, but I’m buying. Price might go lower, it always can, but there is value at these levels, and I’m accumulating. I think it’s important to be honest about how I’m actually acting on the analysis I publish, rather than just presenting data from a distance. And right now, the data is saying something that has only been said a handful of times in Bitcoin’s entire history.

Let’s cut to the chase:

- The Crosby Ratio Z-score has one of the lowest readings in history.

- The RSI is at a level we’ve only encountered a handful of times in extreme market lows.

- Bitcoin has bounced off the 200-week moving average.

- The SOPR is in the bottom fifth percentile of all historical readings.

- The Mayer Multiple is also in its bottom fifth percentile.

The Crosby Ratio

The Crosby Ratio Z-score measures bitcoin’s price momentum and standardizes it for Bitcoin’s evolving volatility. It’s not a fixed threshold as it adjusts as the market matures and volatility compresses, making it applicable across every stage of Bitcoin’s history. The current reading is around -1.7. This means 99.8% of all days in Bitcoin’s history have registered a less extreme reading on this indicator.

Figure 1: The Crosby Ratio Z-Score has just dipped to one of its lowest ever values.

The list of instances where this reading has been as low: the recent drop to $60,000, the first break below $20,000 in 2022, the COVID crash in March 2020, and the 2018 bear market low. That’s it. Four occasions in over a decade of price history. Every single one of them turned out to be a significant accumulation opportunity.

The RSI

The Relative Strength Index is one of the most widely used momentum indicators across all markets. Bitcoin’s weekly RSI is currently at one of the lowest levels ever. The previous instances of readings this low were the 2015 bear market low, the 2018 bear market low, the COVID crash, and the recent drop to $60,000.

Figure 2: The Relative Strength Index is comparable to historical lows.

Two independent momentum indicators, measured completely differently, but producing the same short list of historical comparisons. That kind of confluence across methodologies isn’t something to dismiss.

The 200-Week Moving Average

The 200-Week Moving Average has served as bear market support throughout Bitcoin’s history. The only meaningful exception was the FTX collapse in late 2022, which caused a brief but sharp undershoot before a rapid recovery. Outside of that event, this level has held as a floor every single cycle.

Figure 3: Bitcoin currently sits just above its 200WMA.

View Live Chart

Bitcoin has just bounced off that level again. Directly beneath current prices sits the recent cycle low, creating the structure for a potential double bottom, one of the more reliable technical formations across any market. The 200-week moving average and the Bitcoin Realized Price converge in approximately the same zone, adding further weight to this level as meaningful structural support.

SOPR & The Mayer Multiple

The Spent Output Profit Ratio is currently in the bottom fifth percentile of all historical readings. This means the rate of realized losses across the Bitcoin network, the pace at which holders are selling at a loss, is in the deepest 5% of anything we’ve ever recorded. The selling that has driven this move has been predominantly short-term in nature; value days destroyed data confirms that long-term holders have largely not participated in this liquidation. These are short-term traders and leveraged positions being cleared out, and not the conviction holders capitulating.

Figure 4: The Spent Output Profit Ratio illustrates the severity of recent losses.

View Live Chart

The Mayer Multiple, which measures bitcoin’s price relative to its 200-day moving average, is simultaneously in its own bottom fifth percentile. When these two indicators have historically been in their lower extremes at the same time, the resulting accumulation opportunities have been exceptional. It has happened only a handful of times, and each instance has been followed by significant price appreciation.

Figure 5: The Mayer Multiple has reached levels corresponding to previous bear cycle lows.

To Sum It Up

I’ll be honest, the strength of the decline surprised me. I anticipated a pullback from the $80,000 resistance zone, but the move through $70,000 was sharper than expected. What hasn’t surprised me is the data that’s emerged as a result, because this kind of confluence across technical, on-chain, and momentum indicators has appeared before, and the market has consistently rewarded accumulation at these readings.

Could we go lower? Yes. The realized price sits not far beneath current levels and represents the next meaningful support zone if the low is revisited. I’m prepared for that scenario. But removing all emotion and looking purely at what the data is saying, five independent signals simultaneously in generational territory, this is not the moment to wait on the sidelines for a marginally better price.

Subscribe to Bitcoin Magazine Pro on YouTube for more expert market insights and analysis!

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Always do your own research before making any investment decisions.

This post 5th Worst Bitcoin Price Action Ever — I’m Buying At 99.8% Probability first appeared on Bitcoin Magazine and is written by Matt Crosby.

Bitcoin Magazine

Bitcoin’s Pullback Tests Institutional Adoption Narrative as Pompliano Stays Bullish

Bitcoin’s recent price decline is testing one of the asset’s most prominent bullish narratives: that institutional adoption will stabilize volatility and support long-term growth.

Despite the downturn, ProCap Financial CEO Anthony Pompliano thinks that the broader trajectory remains intact, framing the current weakness as a natural phase in Bitcoin’s maturation into a mainstream financial asset.

Speaking on CNBC’s “Power Lunch,” Pompliano said Bitcoin’s integration into traditional finance is accelerating, pointing to growing interest from major institutions such as BlackRock CEO Larry Fink.

According to Pompliano, this shift represents the realization of a long-anticipated transition from a niche, ideologically driven asset to a widely held portfolio allocation.

“Bitcoin is maturing into a traditional finance asset,” Pompliano said, adding that institutional demand signals “what mass adoption looks like.”

Bitcoin has come under pressure in recent weeks, with prices retreating amid broader risk-off sentiment and capital rotation into equities, particularly in high-growth sectors like artificial intelligence and newly listed public companies.

The downturn has revived concerns that Bitcoin’s adoption cycle may be nearing saturation, limiting its ability to deliver the outsized returns seen in prior cycles.

Some argue that Bitcoin’s earlier growth was driven largely by rapid user adoption and speculative inflows — dynamics that may be harder to replicate now that the asset has reached a more mature phase.

As the CNBC host noted, the “adoption story” may have already peaked.

At the same time, some market participants, including Strategy’s Michael Saylor, have suggested capital could be rotating out of crypto into other high-momentum opportunities, including upcoming IPOs and AI-linked investments.

Pompliano: Rotation from bitcoin is natural, not structural

Speaking with CNBC, Pompliano pushed back on the idea that capital outflows signal structural weakness. Instead, he characterized the movement as typical portfolio rebalancing behavior.

“Capital chases momentum and returns,” he said, noting that Bitcoin’s liquidity makes it a convenient source of funds when investors pursue new opportunities.

The current market environment highlights a tension in Bitcoin’s evolution. While institutional adoption has broadened its investor base, it has also tied Bitcoin more closely to macroeconomic trends and cross-asset flows.

As a result, Bitcoin increasingly behaves like a risk asset during periods of market stress, declining alongside equities rather than acting as an uncorrelated hedge. This dynamic has complicated the narrative of Bitcoin as “digital gold,” particularly in the short term.

Still, Pompliano maintains that Bitcoin’s core fundamentals remain unchanged. He pointed to the network’s continued operation, decentralization, and predictable issuance schedule as evidence that the asset’s long-term value proposition is intact.

“Show me what has changed,” he said. “The network continues to do everything it is designed to do.”

Bitcoin as a ‘Savings Technology’

Pompliano reiterated his long-held view of Bitcoin as a hedge against fiat currency debasement, arguing that persistent government spending and monetary expansion underpin its long-term case.

He described Bitcoin as a “savings technology,” highlighting its historical compound annual growth rates — approximately 60% over the past decade and over 30% in the last three years — as evidence of its ability to preserve and grow capital over time.

In his view, Bitcoin’s role is less about short-term speculation and more about long-term wealth protection, akin to gold or real estate for previous generations.

This post Bitcoin’s Pullback Tests Institutional Adoption Narrative as Pompliano Stays Bullish first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Price Plunges Below ‘Fire Sale’ Territory as Fear Index Reads 12 — Echoing the FTX Crash

Bitcoin price dropped to levels on Thursday that placed it below the “Fire Sale!” band on the Bitcoin Rainbow Chart — a depth not reached since the catastrophic FTX exchange collapse in November 2022 — as the Fear and Greed Index registered a reading of 12 out of 100, deep in “Extreme Fear” territory.

Bitcoin price opened today near $63,500 after sliding below $62,000 last night. That puts BTC below even the most discounted valuation band on the Bitcoin Rainbow Chart — a level the model historically flags as a rare and extreme buying signal.

The Bitcoin Rainbow Chart is somewhat of a logarithmic growth curve overlaid with color-coded sentiment bands. The deepest band — labeled “Basically a Fire Sale!” — represents the lowest tier of the model’s projected fair value range. When Bitcoin trades beneath it, the asset sits outside the historical channel that has contained BTC’s long-term price behavior.

JUST IN: Bitcoin is now below the "Fire Sale" territory for the second time in 4 years

— Bitcoin Magazine (@BitcoinMagazine) June 4, 2026

Buy the dippic.twitter.com/oU6qudhn6M

The last confirmed breach of the “Fire Sale!” floor occurred during the FTX exchange collapse in November 2022, when Sam Bankman-Fried’s crypto empire imploded and BTC cratered under forced selling pressure across the market. That event remains one of the most severe liquidity crises in crypto history.

Per Bitcoin Magazine Pro data from March 2026, Bitcoin price had already begun testing below the “Fire Sale!” zone — described at the time as “its first drop into this area since the FTX-induced crash”.

The renewed descent on June 4 deepens that breach, with the coin shedding ground for the second consecutive week.

Bitcoin price and market in ‘Extreme Fear’

The Fear and Greed Index, which runs on a scale of 0 to 100, registered 12 on Thursday — placing the market squarely in “Extreme Fear”. The index aggregates volatility, market momentum, social sentiment, and derivatives data into a single score.

A reading below 25 signals extreme fear, a condition that, by the index’s own framework, has historically preceded price recovery periods.

February 2026 saw the index touch an all-time low of 5, driven by a 52% drawdown from Bitcoin price’s peak of $126,000. Thursday’s reading of 12 sits just above that nadir, as Bitcoin price continues its slide from cycle highs.

On X today, Strategy’s Michael Saylor argued the sell-off reflects institutional capital rotating into AI infrastructure rather than a deterioration in Bitcoin’s fundamentals. The decline may have been compounded by concerns over Strategy selling 32 BTC to fund preferred-share dividends — its first bitcoin sale since 2022 — despite the company recently reducing debt by repurchasing $1.5 billion of convertible notes at a discount.

This post Bitcoin Price Plunges Below ‘Fire Sale’ Territory as Fear Index Reads 12 — Echoing the FTX Crash first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Schwab Strategist: Bitcoin’s $60,000 Mining Cost Could Mark the Cycle Bottom

Bitcoin is in a bear market. That much is not in dispute.

What Jim Ferraioli, Director of Digital Currencies Research and Strategy at Charles Schwab, argued Wednesday on Bloomberg is more precise and more structural: this selloff has a measurable cost floor, and that floor is built not from sentiment or chart patterns, but from the physics of energy consumption.

The numbers frame the drawdown in context. Bitcoin peaked at $126,000 in the fall before collapsing to roughly $60,000 in February — a 50% correction that, while brutal for recent buyers, falls far short of the 75%-plus implosions that defined prior Bitcoin bear markets.

Ferraioli’s core analytical framework centers on one question: what does it cost to manufacture Bitcoin? The answer creates a natural gravitational floor that has held across multiple cycles.

For the most efficient miners — those operating at scale with next-generation ASIC hardware and access to the cheapest wholesale energy — the cost to produce one Bitcoin sits at approximately $60,000, Ferraioli said.

That figure is not arbitrary. It represents the all-in expense of powering a facility at roughly $0.07 per kilowatt-hour with the most advanced semiconductor fleets available.

The less efficient miners — those with older ASIC hardware, higher energy costs, and thinner operational margins — carry a production cost of approximately $95,000 per BTC, according to Glassnode data cited in Schwab’s May 2026 research report. That gap between $60,000 and $95,000 defines Bitcoin’s current valuation range.

Bitcoin’s energy floor: Why $60,000 may mark the bottom

Ferraioli argues that in deep bear markets, the cost of production for the best miners has historically served as the bottom. February’s low near $60,000 aligns almost precisely with that level, as well as BTC’s 200-week moving average.

The BTC selling pressure is not random. It is demographically specific. The investors driving forced liquidations are those who acquired Bitcoin during the past 18 months — buyers who rode the asset from sub-$80,000 up to $126,000 and then watched gains evaporate in full.

Schwab tracks two cost-basis metrics to quantify this pressure: the average acquisition cost for U.S. spot ETF and ETP holders, which stands near $83,000, and the active investor cost basis — excluding coins rewarded to miners — which sits near $78,000.

Both figures sit well above current spot prices, putting the majority of recent entrants into unrealized loss positions and reinforcing $83,000 as a ceiling of overhead supply rather than a floor of support.

Glassnode’s on-chain data corroborates this dynamic. Bitcoin’s latest attempted rally stalled at the aggregate ETF cost basis near $83,000, with total realized losses spiking to $1.35 billion per day and long-term holders capitulating from cycle-top positions. Hedge funds represent roughly 30% of spot ETP ownership but are operating market-neutral, executing basis trades rather than taking directional views — meaning they provide no natural bid when prices fall.

Here is where Ferraioli’s analysis turns constructive. Every major publicly traded Bitcoin miner has announced a pivot toward high-performance computing (HPC) for AI inference workloads. The economics on their face appear to favor abandoning mining: inference generates higher net revenue per megawatt-hour than Bitcoin mining during peak demand windows.

But demand for AI inference is not uniform across 24 hours. Models run hard during business hours and sit idle overnight and on weekends.

That creates a structural opportunity that does not displace BTC mining — it layers on top of it. Schwab’s analysis models Bitcoin as the optimal baseload monetization of power during off-peak hours, with inference overlaid during peak business-hour demand.

A data center operating this hybrid model maximizes utilization across the full 24-hour cycle rather than leaving capacity dark when inference demand falls away. For miners, this translates to more stable revenue, reduced forced BTC sales to cover operating costs, and lower structural risk across bear market cycles.

Bitcoin is backed by energy

The underlying thesis is one of energy economics. Bitcoin has no earnings, no free cash flow, and no CEO issuing guidance. Its value, in Ferraioli’s framework, derives from the energy cost required to produce it — a cost that is transparent, verifiable, and historically durable.

In commodity markets, price cannot sustainably trade below cost of production. Producers shut down, supply contracts, and equilibrium resets higher.

Bitcoin follows this same logic: when spot prices fall toward $60,000, the least efficient miners shut down operations, the network’s hash rate adjusts through Bitcoin’s difficulty mechanism, and the cost to produce each new coin falls.

As of May 2026, the average mining cost across all Bitcoin miners sits near $85,604, with the Bitcoin price trading in the mid-$60,000s — meaning the network as a whole is operating at a loss, a configuration that has historically preceded recoveries, not further collapse.

This post Schwab Strategist: Bitcoin’s $60,000 Mining Cost Could Mark the Cycle Bottom first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

For the better part of two years, Wall Street has treated AI as the most bullish trade on the board, a growth engine that turbocharges earnings, underwrites stretched valuations, and promises a productivity windfall somewhere down the road.

However, the Fed has access to the same numbers and seems to be more inclined to treat the AI build-out as a fresh source of demand in a market that's still fighting to drag inflation back toward its 2% target.

Goldman Sachs now expects AI-related capital spending to approach $800 billion in 2026, and it calculates that the surge will lift its full-year business investment forecast to 7.8% while adding roughly 3.3 percentage points to capital-expenditure growth on its own.

TrendForce, tracking the nine largest cloud providers in the world, places their combined 2026 outlay near $830 billion, a jump of about 79% over the previous year. A pretty big slice of that increase reflects rising prices rather than added capacity, with Microsoft attributing some $25 billion of its $190 billion budget to costlier memory and components.

All of it puts quite a bit of weight on the inputs the Fed tends to watch most closely, which could turn this investment boom into a policy headache.

Where does the $800 billion in AI spending actually go?

It helps to imagine this spending in physical terms. All of that money takes the shape of land, steel, transformers, copper wiring, gigawatts of fresh generation capacity, industrial-scale cooling, and the incredibly skilled and incredibly rare trades hired to assemble all of it.

Goldman described this as a wave that reaches across servers, semiconductors, memory, power infrastructure, data centers, software, and research budgets, and the bank's longer-range model traces annual AI capex climbing from around $765 billion this year toward $1.6 trillion by 2031.

Power has become the binding constraint. In a late-May speech, Fed Governor Lisa Cook noted that electricity and water prices have each climbed about 5% over the past year, that chips, high-tech equipment, and software have all grown more expensive, and that wages in specialty construction trades have picked up notably. Households feel some of that pressure on their monthly bills, which began drawing political pushback as several state legislatures move to slow large data-center development.

The central bank's leadership has been unusually clear and honest about where this leads. Speaking back in March, Jerome Powell told reporters that the construction frenzy was “putting pressure on all kinds of goods and services that go into building these things,” and he conceded that the effect was “probably pushing inflation up.”

Cook went further in that same May address, warning that “yet another shock to prices could be layered on from the heightened investment demand due to AI” and pointing out that companies have announced more than $1.5 trillion in data-center plans, only a sliver of which has actually been built.

The demand side of AI, in other words, is showing up in the price data well ahead of any productivity payoff the technology eventually delivers.

What it means for Bitcoin's rate-cut bet

The consequences travel from Silicon Valley balance sheets straight into crypto. Bitcoin spent most of the year leaning on the expectation that cooling inflation would free the Fed to cut rates, loosen financial conditions, and rekindle the risk appetite that powered the 2024 rally.

CryptoSlate has documented how tightly the asset now tracks liquidity cycles, a sensitivity that has overtaken Bitcoin halving as the dominant price driver. An $800 billion demand makes rate cuts unlikely, since every dollar of AI-related price pressure hands the Fed one more reason to stay put.

Markets have already begun repricing that. Futures and prediction markets now put the odds of a hold at the June 16-17 meeting above 93%, which will be the first one chaired by Kevin Warsh following his May handover from Powell. CryptoSlate has tracked the reversal as it unfolded, from a stretch when bond traders were pricing a year-end hike to the inflation prints that kept the Fed frozen.

The repricing has bled into spot prices, with Bitcoin sliding to around $63,600 by June 4 after briefly breaking below $62,000, roughly half its October 2025 record and down more than 13% over the week. Much of that damage comes from exits, since Bitcoin ETFs saw a record 11-session outflow streak worth about $3.45 billion, the longest run of redemptions since the funds launched in 2024. A large share of that capital rotated straight into the AI and semiconductor equities that were driving the macro problem in the first place.

Over a five-year horizon, AI may well do what its champions promise, lowering costs, automating routine labor, and easing inflation through real gains in output per worker. However, the build-out phase tends to work the other way around first. Pulling years of infrastructure demand into a narrow window bids up hardware, energy, and talent long before we see any real efficiency, so the price shock arrives early and the windfall arrives late.

That gap between immediate consequences and delayed benefits is what's been troubling the Fed. Warsh has argued that AI will prove “structurally disinflationary” and usher in “the most productivity-enhancing wave of our lifetimes,” a view that confirms his openness to lower rates. But Cook and Governor Michael Barr lean the other way, with Barr saying flatly that he doesn't believe the AI boom will be a reason for lowering policy rates.

Traders, on the other hand, have been mostly troubled by timing. Bitcoin, alongside equities and the rest of the market, tends to respond to the first decision in front of them. So, a “productivity thesis” that will probably pay off in 2030 does little to positions held this week, month, or even quarter. Inflation running above 3% leaves Warsh little room to act on his convictions in June, regardless of where he'd like to steer.

The same AI boom inflating tech valuations and carrying the indices higher may be the very force keeping the Fed cautious, delaying the liquidity cycle that crypto traders have spent eighteen months waiting for. If policymakers settle on seeing $800 billion in annual spending as one more pillar of sticky demand, Bitcoin's rate-cut trade rests on a foundation considerably thinner than its holders would care to admit.

The post AI’s $800 billion spending boom is becoming Bitcoin’s Fed problem appeared first on CryptoSlate.

The US economy added 172,000 jobs in May, more than double the 80,000 that Wall Street economists had expected, and the unemployment rate held at 4.3%.

The Bureau of Labor Statistics (BLS) also revised March and April higher by a combined 93,000 positions, which left the spring looking much stronger than anyone believed a month ago. For the people who landed those jobs, this counts as good news, and the headline number is certainly something a sitting administration enjoys waving around.

The trouble starts when you ask what a labor market this strong does to the price of borrowing. A report this firm gives the Federal Reserve very little reason to cut interest rates, just as traders, homebuyers, and crypto investors have spent months waiting for that. The market answered fast, with Bitcoin sliding toward $60,000 by Friday in a drop CryptoSlate tracked in real time.

But how does a single jobs report reach into mortgage costs, credit-card bills, and the Bitcoin selloff?

A strong labor market and the Fed's shrinking room to cut

Nonfarm payrolls come from the BLS establishment survey, a monthly count of the paid jobs sitting on employer books across most of the economy, from restaurants and hospitals to factories, schools, banks, and government offices. That number carries so much weight because it's the best monthly read on whether companies are still hiring or starting to pull back, and that signal affects how the Fed thinks about interest rates.

Farm jobs are left out of the count because the survey is built around the regular employer-payroll economy, and farm work tends to be seasonal, irregular, and full of self-employment and family labor that runs outside standard payroll systems, which would make the monthly numbers jumpy and harder to compare over time. Most of the May gains came from hiring in leisure and hospitality, local government, and health care, so the strength was real despite being concentrated in a handful of corners.

The April revisions carried as much weight as the numbers for May. The first estimate for any month is preliminary, built from whatever employer responses arrive by the deadline, and the government updates it as more data comes in. This time the updates ran in the economy's favor, with April lifted by 64,000 to 179,000 and March raised by 29,000 to 214,000, which made the spring look like a sturdier stretch of hiring than the first estimates had shown.

The Fed has spent 2026 wrestling with an inflation problem that's grown worse through the spring. The war with Iran drove oil prices sharply higher, and April CPI came in at 3.8% year over year, the highest reading since May 2023, with energy responsible for most of the jump. A central bank watching prices run that hot wants clear proof the economy is cooling before it eases, and a labor market adding 172,000 jobs gives it the opposite.

The result is that rates stay higher for longer, and that pressure is building during a leadership change at the Fed that CryptoSlate reported as the year's biggest macro test for Bitcoin. Fed Governor Christopher Waller recently dismissed rate-cut talk as “crazy,” and bond traders had already shifted toward betting on a possible hike by year-end, a turn CryptoSlate described as the rate-cut trade flipping into a hike-risk problem.

That affects everyday costs for households. When the Fed holds its rate high, mortgage rates stay elevated, refinancing stays expensive, credit-card balances keep piling up interest, and car loans hold their bite. The wage growth we've seen over the quarter offers some cushion, though April's inflation was hot enough that real wages slipped over the month, so paychecks bought a little less even while employers kept adding staff. The strong report stretches out the window in which borrowing stays expensive for ordinary people, and it's doing it heading straight into the Fed's June 16-17 meeting, where policymakers now have one more reason to wait.

Why does the pressure from jobs land hardest on Bitcoin?

The pressure squeezing homebuyers is quick to reach crypto traders, because Bitcoin has spent the past 18 months trading as one of the assets most sensitive to liquidity. For all the talk about it, liquidity is just how freely money and credit move through the financial system. So, when investors expect lower rates and easier conditions, that money tends to flow toward riskier bets, with Bitcoin among them.

Bitcoin was down roughly 17% on the week, and more than 50% below its October all-time high near $126,200, after a record run of ETF outflows and a rotation of big-money investors into AI stocks pulled away the steady buying that had been holding the market up. CryptoSlate has shown how Bitcoin's price now follows Treasury supply, real yields, and Fed liquidity far more closely than anything happening inside crypto itself.

Fabian Dori, chief investment officer at Sygnum Bank, said the May report was the most awkward possible outcome for anyone counting on relief.

“Today's strong print is the least comfortable outcome for anyone hoping for rate relief,” Dori said. “With April CPI already at 3.8%, resilient payrolls take a June cut off the table and harden the case that the Fed stays put through the summer.”

His advice to investors was to read the reaction rather than the number itself.

“Watch the repricing rather than the headline,” he said. “For digital assets, that delays the rate-driven liquidity tailwind people are hoping for.”

Dori added that a few liquidity factors could still help at the margin, including possible eSLR reform and the level of cash the Treasury keeps parked at the Fed, though he expects a hot jobs number to set the tone for markets in the near term.

He also believes that Bitcoin responds to the broader cost of money as much as to anything happening inside crypto, and a strong labor market keeps that cost high for longer. The deeper risk CryptoSlate has flagged all year is a stagflation setup of sticky prices alongside a Fed that won't cut, the kind of backdrop that keeps money scarce even while the selloff has left Bitcoin beaten down enough for a sharp bounce.

That leaves the market roughly where it began the spring, waiting on a central bank that keeps getting fresh reasons to wait.

The question underneath every jobs report has always been whether the economy is slowing enough to earn relief or staying strong enough to keep rates high, and for now, May's answer isn't the good one. The economy is still standing, hiring is still happening, and that strength is what's keeping cheaper money, lower mortgage costs, and a Bitcoin recovery further down the road than the people waiting on them would like.

The post May jobs report explained: Why 172,000 jobs means higher rates, pricier loans, and a Bitcoin drop appeared first on CryptoSlate.

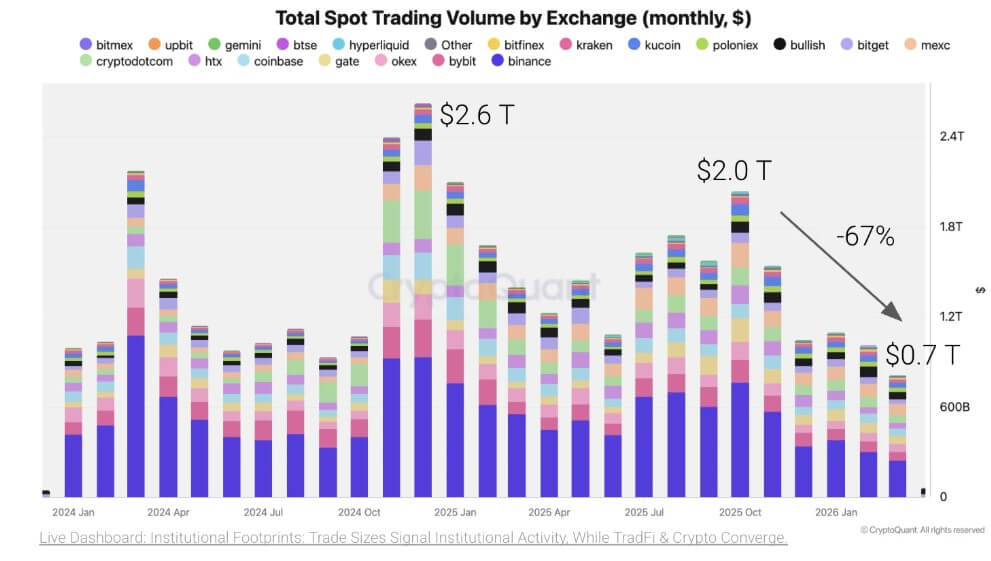

Crypto exchanges are seeing the weakest retail-driven activity in years, but some of the biggest platforms are finding a lucrative new source of volume in Wall Street-style bets on gold, silver, oil, stocks, and indexes.

According to a CryptoQuant report shared with CryptoSlate, the shift is emerging during one of the weakest trading periods for centralized crypto platforms in more than two years.

Spot trading volume fell to $679 billion in April, the lowest monthly level since October 2023, as lower prices and fading retail participation reduced market activity.

At the same time, some exchanges are seeing growth in products that look less like crypto speculation and more like traditional macro trading.

As a result, perpetual futures tied to metals, energy, and equities have become one of the fastest-growing segments on several major crypto venues. This shows how platforms built for Bitcoin and Ethereum are expanding into Wall Street-style markets that trade around the clock.

Retail volume falls to multi-year lows

The collapse in spot market turnover illustrates the sheer magnitude of the post-2025 market contraction.

According to the CryptoQuant report, centralized exchange spot volume in April plummeted 46% year-over-year, and sits a staggering 67% below the market top recorded in October 2025.

That contraction has hit the industry’s core business model, which depends on frequent trading, market volatility, and steady participation from retail users.

Still, Binance remained the largest spot venue by cumulative trading volume in 2026, with $1.3 trillion. Bybit followed with $285 billion, while Gate recorded $253 billion and Crypto.com processed $247 billion.

While these top-tier platforms still capture the lion's share of available trading flow, the underlying data indicate a far less casual ecosystem of participants.

Historically, retail traders are the first demographic to retreat during protracted crypto downturns. Casual investors often exit the market entirely after incurring losses or drastically reduce their positions when prevailing momentum stalls.

Conversely, professional trading desks, automated market makers, and institutional arbitrageurs maintain their presence, as their strategies rely on hedging, executing relative-value trades, and providing market liquidity rather than chasing directional price movements.

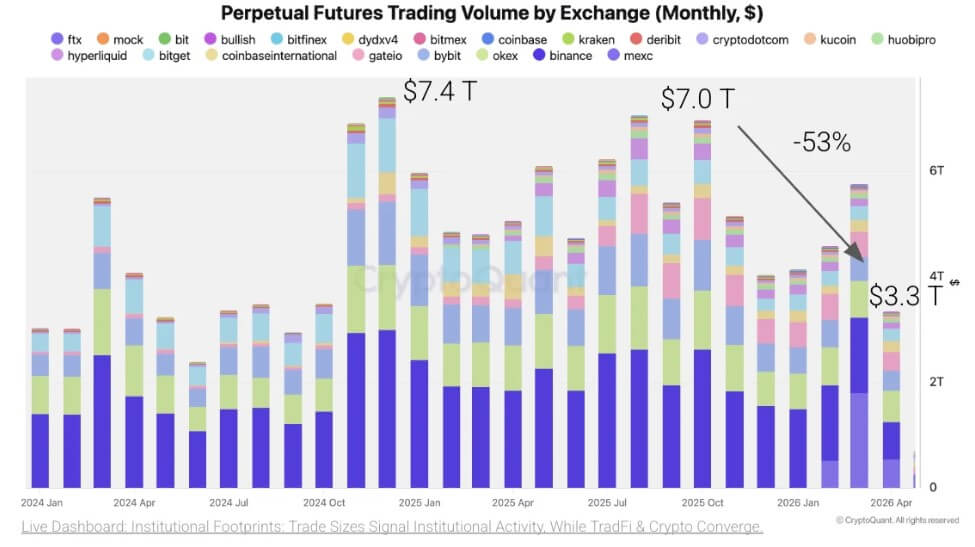

This demographic transition has squarely placed the weakness in the derivatives sector, a domain previously dominated by aggressive retail speculation.

Perpetual futures volume has cascaded 53% from its October 2025 highs, closely mirroring the spot market contraction. Binance retains its dominant market share in the perpetual futures space, followed by MEXC, OKX, Bybit, and Gate.

The parallel decline in both spot and leveraged trading indicates that users are not merely rotating among product types; overall demand for digital asset exposure has fundamentally weakened.

Larger trades point to a different customer base

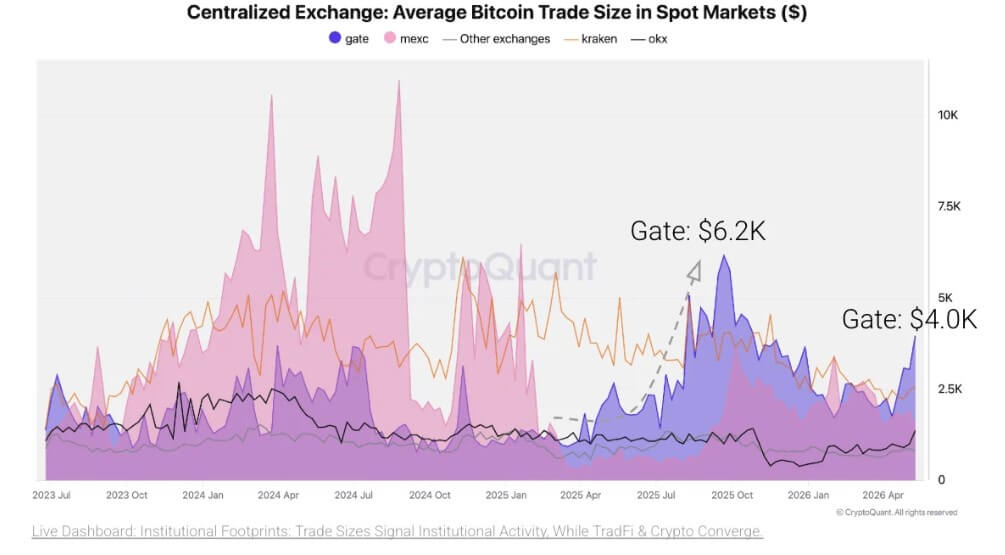

Despite the pronounced drop in absolute trading volume, a granular look at average transaction sizes reveals a market that is steadily institutionalizing.

Average trade size is an imperfect signal, as large transactions can come from institutions, market makers, high-net-worth traders, or professional accounts. Smaller retail orders tend to pull the average down. Still, the metric helps show where bigger participants are most active.

In 2026, Gate logged the highest average Bitcoin spot trade size among major centralized venues, registering approximately $4,000 per transaction. This figure remains elevated even after cooling from a peak of $6,200 during a wave of institutional onboarding in 2025.

CryptoQuant pointed out that several crypto trading platforms, including Kraken, MEXC, and OKX, similarly ranked at the top of the industry for average Bitcoin spot trade sizes.

Kraken’s presence aligns with its long-standing reputation as a compliance-focused hub for professional entities, while OKX and MEXC have cultivated substantial global bases capable of executing bulk orders.

Meanwhile, this institutional footprint is even more pronounced in derivatives trading.

According to CryptoQuant, Gate led the market in average Bitcoin perpetual futures trade size in 2026 at roughly $8,900.

At the height of the 2025 market cycle, this metric briefly reached an astonishing $24,700 in August before normalizing. Kraken and OKX also maintain leading positions in derivatives trade sizes.

This trend suggests Gate has become a more important execution venue for larger Bitcoin trades in both spot and derivatives markets.

Kraken and OKX also remained among the leading venues by average Bitcoin futures trade size, reinforcing the divide between platforms that attract larger execution and those that rely more heavily on broad retail flow.

Notably, this consistency extends to Ethereum markets where Kraken, Gate, MEXC, and OKX continue to dominate average Ethereum spot trade sizes. Gate has also firmly established its presence in this top tier following sustained growth that began in early 2024.

This uniform pattern across multiple assets and product lines indicates that the shift toward wholesale, large-scale execution is a structural market evolution rather than an isolated anomaly.

Liquidity concentrates around fewer venues

This professional consolidation is heavily dependent on the underlying market structure, specifically order-book depth. Institutional participants require deep liquidity to enter and exit substantial positions without triggering severe price slippage or widening bid-ask spreads.

In Bitcoin spot markets, Gate and Binance have maintained among the deepest 1% order books among major exchanges, averaging roughly 200,000 to 250,000 BTC in depth over the period tracked.

The perpetual futures market, while inherently more competitive, displays a similar concentration of liquidity. Gate regularly leads the pack, offering Bitcoin perpetual depth ranging from 750,000 to 1.3 million BTC daily.

Hyperliquid, the leading DEX platform, has surprisingly emerged as a formidable decentralized competitor, maintaining depth above 600,000 BTC.

Meanwhile, traditional heavyweights like Binance and OKX remain robust, generally fluctuating between 500,000 and 850,000 BTC in depth.

These figures show why liquidity has become a central battleground where exchanges with deep books can attract larger traders. In turn, these larger traders can bring greater liquidity, reinforcing the venue’s position as a preferred execution hub.

In a market where retail volume is falling, that feedback loop becomes more important. Platforms with thinner books may struggle to compete for professional activity, while larger venues can use liquidity to expand into new products beyond crypto.

Crypto exchanges push into macro trading

Having secured deep liquidity and professional clientele, the most dominant crypto platforms are now leveraging their infrastructure to encroach on traditional finance.

CryptoQuant noted that trading volume for traditional-finance perpetual futures on crypto exchanges surged in 2026, reaching about $450 billion per month in March. Metals-linked contracts drove most of the activity, with gold and silver accounting for more than 90% of volume during the peak month.

The timing tracks a broader macro backdrop, with gold and silver rallying as investors reacted to inflation concerns.

At the same time, equities reached new highs amid optimism about artificial intelligence, while oil markets became more volatile amid geopolitical tensions involving the United States and Iran.

Crypto exchanges capitalized on this macro turbulence to offer traders a familiar structure in a different venue: perpetual futures that trade 24 hours a day, seven days a week.

Perpetual futures are common in crypto because they allow traders to take leveraged long or short positions without an expiration date.

Extending that structure to gold, silver, oil, and stock-linked products gives crypto-native platforms a way to compete for macro trading activity that has traditionally been concentrated within brokerages, futures exchanges, and contracts-for-difference platforms.

CryptoQuant stated that the early demand has been strongest in metals. Gold and silver became the primary gateway for traders on crypto exchanges to express views on traditional markets.

More recently, oil-linked products have grown as energy volatility increased. Meanwhile, equity-linked contracts remain smaller, but they indicate that exchanges are testing a wider range of traditional assets.

Gate and Binance dominate the new segment

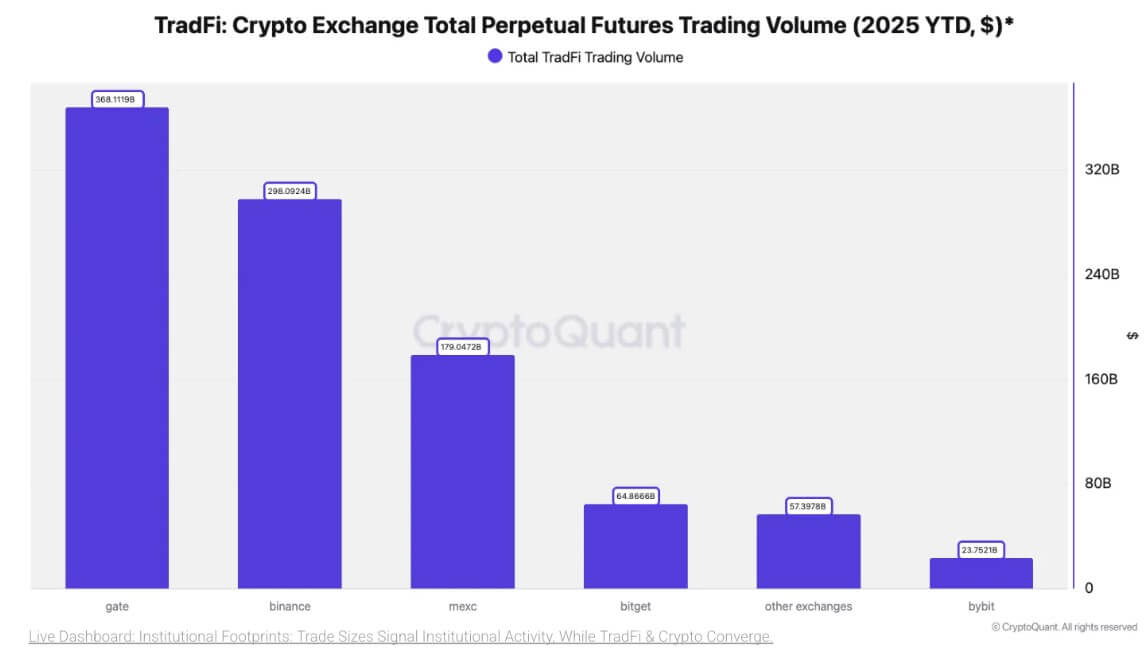

Still, CryptoQuant noted that the booming market for traditional-finance futures is largely dominated by a few exchanges.

For context, Gate handled nearly $290 billion in TradFi futures volume in March, far ahead of other platforms. This jump was mostly driven by gold and silver trading.

Binance ranked second, hitting $109 billion in March and maintaining high activity through May at $64 billion. MEXC, Bitget, and Bybit also saw increases as traders looked beyond metals into other asset classes.

Looking at the year as a whole, the market is highly concentrated. So far in 2026, Gate leads with about $368 billion in TradFi futures volume. Binance follows with $298 billion. Together, these two exchanges account for about two-thirds of the entire market.

MEXC is next with $179 billion, followed by Bitget with $65 billion. Bybit, despite being a major player in crypto derivatives, has handled a smaller $24 billion in traditional futures.

These numbers show how crypto exchanges are trying to adapt to the current market situation. Their original business relied on volatile digital tokens and everyday people making speculative bets.

Now, the focus is shifting to professional traders, deep market liquidity, and giving users access to traditional assets around the clock.

The post Crypto exchanges are losing retail traders but are filling the gap with Wall Street-style bets appeared first on CryptoSlate.

A group of Republican senators is warning US bank regulators that a little-known capital rule could effectively keep banks out of Bitcoin, even as Congress moves to give traditional financial firms a larger role in digital asset markets.

In a May 27 letter to Federal Reserve Vice Chair for Supervision Michelle Bowman, FDIC Chair Travis Hill, and Comptroller of the Currency Jonathan Gould, six senators urged the agencies to build a new capital framework for on-balance-sheet digital asset activities.

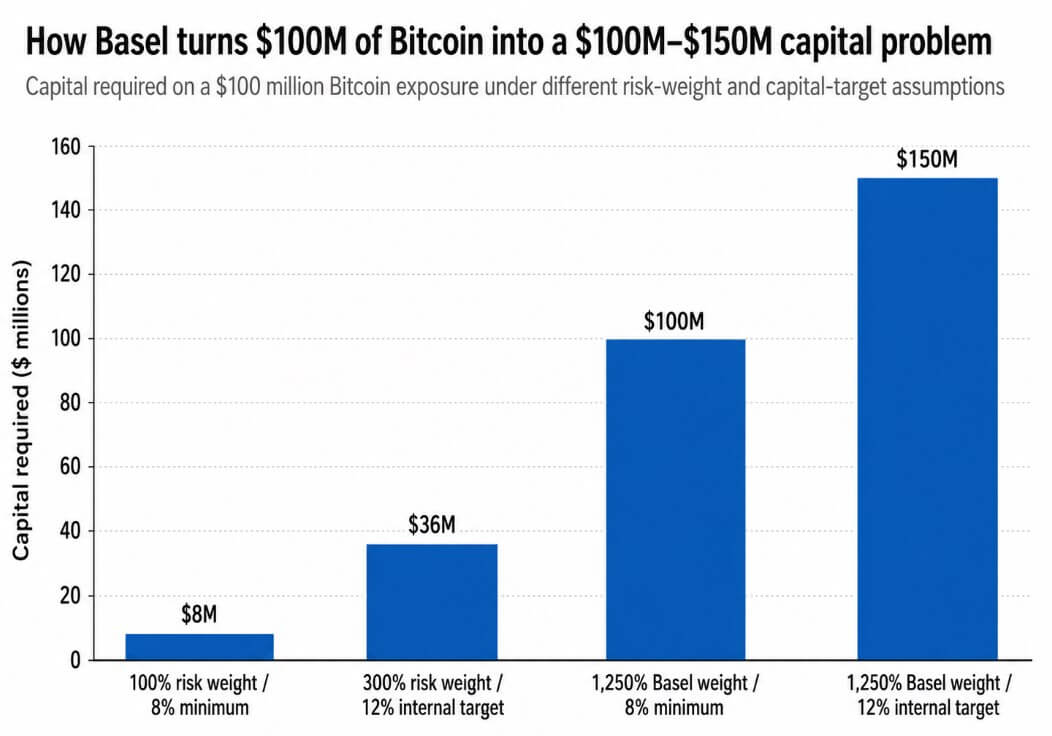

Their target is Basel's 1,250% risk weight for assets such as Bitcoin, which they argue functions as a de facto ban on banks holding crypto.

A 1,250% risk weight multiplied by the 8% minimum capital requirement equals a 100% capital allocation, meaning a bank holding $100 million in Bitcoin needs at least $100 million in capital against it.

For banks that manage to meet internal CET1 targets above the regulatory floor, the burden climbs further. A bank with a 12% internal capital target would need $150 million in capital for that same $100 million exposure, requiring roughly $18 million in annual net profit to clear a 12% ROE hurdle.

Normal custody, trading, or client-service economics rarely generate returns at that threshold, leaving a bank legally authorized to hold Bitcoin but financially unable to justify doing so.

Why this lands now

The Senate Banking Committee advanced the CLARITY Act on May 14 by a 15-9 vote, sending it to the Senate floor.

If passed, the bill would give banks a clearer statutory role in digital asset markets, but the senators argue that legislative permission without capital efficiency leaves banks holding a permission slip they cannot afford to use. A bank can be legally authorized to hold Bitcoin and still be structurally prevented from doing so by a capital charge that makes the position uneconomic before the first trade.

The three regulators the letter addresses have each moved toward crypto permissiveness since early 2025.

The OCC reaffirmed in March 2025 that national banks may engage in crypto custody, stablecoin-related activities, and distributed-ledger payment functions, while removing the prior supervisory non-objection requirement.

The FDIC followed that same month, rescinding its notification requirement and allowing FDIC-supervised institutions to pursue permissible crypto activities without prior approval.

The Fed withdrew its guidance on crypto assets and dollar tokens in April 2025, framing the move as support for innovation.

All three agencies opened the door to crypto activity and left the Bitcoin capital question untouched.

The senators found their sharpest argumentative foothold in a March 2026 interagency FAQ on tokenized securities.

| Regulator | Recent crypto-friendly move | What it allowed or eased | What remains unresolved |

|---|---|---|---|

| OCC | March 2025 guidance | Crypto custody, stablecoin activity, DLT payments; removed non-objection requirement | Capital treatment for bank-held Bitcoin |

| FDIC | March 2025 guidance | Permissible crypto activities without prior FDIC approval | Capital treatment for direct crypto exposure |

| Fed | April 2025 withdrawal | Pulled prior crypto/dollar-token guidance | Capital treatment for on-balance-sheet Bitcoin |

| Fed / FDIC / OCC | March 2026 FAQ | Tokenized securities generally treated like underlying securities | Whether that logic applies to native cryptoassets |

The joint guidance from the Fed, FDIC, and OCC held that eligible tokenized securities should generally receive the same capital treatment as their non-tokenized equivalents, and that the technology used to record or transfer ownership should not determine capital allocation.

If a tokenized Treasury is treated like a Treasury because the underlying risk profile governs its treatment, the logic should extend to Bitcoin, and the asset's volatility and operational risks are measurable and can support a calibrated framework.

The March 2026 guidance covers eligible tokenized securities, and the senators are pressing regulators to carry the same technology-neutral logic forward to native digital assets.

The prudential case for the rule

The Fed, FDIC, and OCC's 2023 joint statement noted price volatility, legal uncertainty regarding custody and ownership rights, contagion from exchange and counterparty failures, governance weaknesses in crypto networks, and operational risks associated with open or decentralized infrastructure.

The Basel standard was built around those risks after the 2022 crypto collapse exposed how quickly losses could spread to interconnected institutions.

A dollar-for-dollar capital charge reflects a genuine judgment that Bitcoin's risk profile does not resemble the assets that populate traditional bank balance sheets.

The senators argue that the risks of volatility, custody complexity, and operational exposure are quantifiable, and a calibrated capital framework can address them without requiring capital equal to or greater than the exposure itself.

The Basel Committee agreed in November 2025 to expedite a targeted review of elements of its cryptoasset standard, and reported progress on that review in February 2026.

Basel Chair Erik Thedéen has said the global crypto rules for banks need to be reworked after the US and UK both declined to implement the current framework.

A coalition of major financial industry groups wrote to Basel in August 2025, arguing that the standard would make meaningful bank participation uneconomical and requesting a pause and revisions.

The senators are pressing US regulators to act at a moment when the international architecture underpinning the 1,250% treatment is under open review.

Two paths from here

If regulators respond by proposing a calibrated framework for liquid digital assets instead of the blanket Basel weight, the capital required on $100 million of Bitcoin exposure could fall from the current $100 million-$150 million range to something closer to $8 million-$36 million under a 100%-300% risk-weight band and standard capital targets.

| Scenario | Capital treatment | Bank role in crypto | Likely market effect |

|---|---|---|---|

| Calibrated framework | 100%-300% risk-weight band; $8M-$36M capital on $100M exposure | Banks can hold inventory, support market-making, custody, prime brokerage and structured products | More institutional liquidity; tighter spreads; banks become balance-sheet participants |

| Basel rule remains | 1,250% risk weight; $100M-$150M capital on $100M exposure | Banks mostly provide custody, settlement and services, but avoid direct BTC exposure | Bitcoin access remains routed through ETFs, nonbanks and offshore venues |

At that level, bank market-making, custody, prime brokerage, and structured crypto products become viable lines of business. Institutional liquidity improves, spreads compress, and banks move from service providers to balance-sheet participants.

If regulators keep 1,250% treatment as the practical standard for native crypto on-balance-sheet exposure while continuing to open other pathways, banks would continue offering custody and settlement, while direct Bitcoin exposure stays with nonbanks and ETF wrappers.

US-traded spot Bitcoin ETFs already saw roughly $4.4 billion in outflows through May 15 to June 3, showing that institutional access to Bitcoin has routed around bank balance sheets.

That channel will deepen if the capital rule stays intact.

The letter does raise the political cost of inaction while Congress is actively writing the market structure rules that will govern bank participation in digital assets for the next decade, and legal authorization to hold Bitcoin means little if the capital charge required to do so makes the position uneconomic from the first day it hits the balance sheet.

The post A little-known 1,250% rule could lock US banks out of Bitcoin appeared first on CryptoSlate.

Charles Hoskinson raised the possibility of splitting Cardano after the collapse of one of its best-known ecosystem tools exposed a deeper fight over money, governance, and who has the power to keep builders alive on the network.

This week, the Cardano founder floated what he called a “nuclear option,” saying a new Cardano could be launched through proof of burn if the existing ecosystem cannot change how it funds and commercializes projects.

The statement came after TapTools, one of Cardano’s most widely used analytics and infrastructure platforms, said it would begin winding down operations over the next two weeks following leadership departures, mounting costs, and the loss of key technical capacity.

Hoskinson responded with a long, emotional address that turned a project closure into a broader indictment of Cardano’s governance and commercial strategy.

Hours later, he posted on X:

I’m taking a break. TTYL.

More Cardano DeFi apps will die, Hoskinson warns

Hoskinson said TapTools’ closure was unlikely to be an isolated failure, saying:

This year is going to be very hard, especially the second half of the year for Cardano. We are probably going to see more dApps in DeFi die and a consolidation happen

The warning landed as Cardano’s DeFi economy remained small by broader crypto standards and under renewed strain.

DeFiLlama data showed about $115 million in total value locked on Cardano, with the network’s DeFi TVL down more than 5% over 24 hours. Cardano’s 24-hour DEX volume stood near $6.3 million, while its stablecoin market was roughly $55 million.

Those figures point to the commercial problem behind Hoskinson’s remarks. Cardano still has a large brand and a committed community, but the financial activity available to sustain infrastructure providers, exchanges, lending apps, and analytics platforms remains limited.

For teams that rely on subscriptions, API revenue, token activity, treasury funding, or outside investment, a thin market can quickly become an operating crisis.

Indeed, TapTools had framed its closure as the result of that pressure rather than a loss of belief in Cardano.

The platform said it had served more than 1 million users, supported hundreds of projects through its API, published hundreds of articles, and generated hundreds of millions of social impressions for Cardano builders.

However, the team said the departure of co-founders, including its chief technology officer and chief operating officer, had created a gap it could not quickly repair. A backend developer had stepped into the CTO role, but that replacement also decided to leave.

The company said it had tried to lower infrastructure costs, improve efficiency, and develop new products. Still, it concluded that it could not responsibly commit to the future without a credible acquisition path or fresh resources.

For Hoskinson, the announcement confirmed a problem he said had been visible for months. He said TapTools had been part of his daily routine and called its closure a loss for the broader ecosystem.

He also pointed to JPEG Store as another sign that older Cardano projects were struggling to survive the current cycle. He added:

I would suspect others are coming very soon. There’s going to be a wave of failures in the ecosystem.

The founder says he does not hold the levers

Hoskinson’s central argument was that Cardano’s public market still treats him as the person responsible for the network’s direction, even though the formal powers needed to change that direction now sit elsewhere.

He said he does not control Cardano’s treasury, does not hold governance keys, cannot initiate a hard fork, cannot change protocol parameters, and does not own the Cardano trademark.

He said the resources created to grow and govern the ecosystem were assigned to separate entities rather than to him personally.

The comments cut into one of Cardano’s most sensitive political tensions. The network has spent years moving toward community governance, with delegated representatives, treasury rules, and other bodies taking on greater responsibility for funding and protocol decisions.

That structure limits founder control by design. It also means there is no single executive authority able to rescue struggling businesses, redirect treasury funds, or impose a commercial strategy when market conditions worsen.

Hoskinson said he had proposed multiple ways to prepare for that pressure, including a sovereign wealth fund, stablecoin reserves, an ecosystem index, and acquisitions of struggling infrastructure projects.

He argued those efforts were either rejected, delayed, or criticized by voters and community members who opposed spending treasury funds or feared centralization.

He noted:

There is a deranged psychopathy that has infected Cardano. You can see it at the bottom of each of my tweets. There are people whose only purpose now is to attack me. Every video I make, every tweet, every output, it is a growing chorus.

His frustration was aimed at that contradiction. When he tries to acquire or commercialize projects, he said critics accuse him of consolidating power. When he does not intervene, those same critics blame him for allowing builders to fail.

He stated:

You do not want commercialization, but then you punish everybody when commercialization does not occur. You say Cardano is not a ghost chain, but the things needed to prevent that, you do not care about.

Cardano's treasury politics move into the market

The speech landed at a difficult moment for Cardano as the blockchain network's ADA token fell below $0.20 for the first time in more than five years.

This extends a yearlong decline that has erased much of the token’s value and deepened pressure on builders whose businesses depend on user activity, treasury funding, or investor confidence.

Meanwhile, the decline has also sharpened the debate over whether Cardano’s governance system can fund growth quickly enough to keep pace with rival blockchain ecosystems.

According to Hoskinson:

Every person who has tried to use the treasury for commercialization gets attacked. Every program has to be pushed through with enormous effort to reach two-thirds voting, and most people do not have the political power, will or grit to get through that process.

For context, Cardano’s flagship 2026 Summit in Singapore was canceled after a treasury funding proposal failed to meet the two-thirds approval threshold required under the network’s governance rules.

Hoskinson argued that Cardano’s technology has continued to advance, citing expected work such as Leios. But he said technology alone would not be enough if the ecosystem could not fund businesses, support builders, and create incentives for commercial use.

His remarks were unusually blunt. He accused parts of the community of creating a hostile environment for builders and said some critics appeared more interested in proving Cardano had failed than helping the network recover.

According to him:

We as a community have to have a schism. We can no longer admit people whose only purpose is to burn the entire ecosystem down. It is the builders versus the non-builders, the doers versus the pessimists and cynics.

He said teams seeking treasury money or commercial support are often attacked before and after funding votes, making the system unattractive for serious operators.

A break raises the stakes

Hoskinson did not announce a formal exit from Cardano. His later post saying he was taking a break appeared to reflect exhaustion with the public fight rather than a resignation from the ecosystem.

Still, the timing amplified the message. A founder who remains Cardano’s most recognizable public advocate had just told the community that more projects may collapse, that he lacks the authority to stop it, and that the network must choose leadership, strategy, and funding mechanisms or risk managing decline.

Meanwhile, he pointed out that his “nuclear option” could be a way to separate builders from hostile critics and reset tokenomics and institutional funding.

He stated:

There are options. We could launch a new Cardano and have a proof of burn. That would be the most extreme option because those people would not migrate. They would be left behind in the environment they created, with no market, no volume and no commercialization. That is the nuclear option.

That suggestion reflected how far the conflict has moved from routine governance debate. Hoskinson’s complaint is no longer simply that voters rejected a proposal or that ADA’s price has fallen.

He argues that Cardano lacks an executive function capable of turning treasury resources, technical progress, and community support into a coordinated growth plan.

The consequences are now visible through business closures. TapTools said it remained open to acquisition or sustainable funding, but its shutdown notice gave Cardano a concrete example of what can happen when useful infrastructure cannot cover costs or retain key staff.

Considering this, Hoskinson told delegators to examine whether their DReps are helping the ecosystem grow or blocking the decisions needed to support builders.

He urged the community to take a week, study the failures, and decide whether it wants constitutional changes, treasury changes, executive changes, or even a more radical protocol path.

The post Cardano founder floats splitting his own blockchain after warning more apps will die appeared first on CryptoSlate.

CryptoTicker.io

Bitcoin has done it again: From an all-time high of around $120,000, it has dropped to about $60,000 within a few months – a decrease of around 50%. Those who invested at the peak are now staring at a halved portfolio. However, those who invested with a clear plan and the right investment strategy are already familiar with this scenario from previous cycles and know: Right now is when the foundation for future returns is being laid.

Key Insights

- Bitcoin fell from about $120,000 to around $60,000 in 2025/2026 – a decline of about 50%, which is historically not unusual in the crypto space (comparable to 2017/18 and 2021/22).

- Dollar cost averaging (DCA) is a proven strategy where you regularly invest a fixed amount – regardless of the current price. This smooths out your entry price and helps you avoid the trap of market timing.

- Large investment funds and pension funds operate on the same principle: they invest regularly over decades instead of reacting to short-term market fluctuations.

- During crash phases, you as an investor have three options: continue DCA consistently, partially shift into stablecoins, or pause your savings plan and wait for recovery signals.

- The perfect entry point is less important than having a clear plan with defined risk, time horizon, and discipline – our savings plan and crypto savings plan comparison can help you find the right provider.

From Bitcoin's All-Time High to Crash – What DCA Has to Do with It

In early 2025, Bitcoin reached a new all-time high of around $126,000 – approximately $120,000. What followed is familiar to experienced customers of the crypto market: profit-taking, panic selling, and a price drop of around 50%. The price fell to values between $60,000 and $70,000.

Such crashes are not anomalies. In previous cycles – such as 2017/18 or 2021/22 – losses ranged from 40% to over 80%. Nevertheless, Bitcoin recovered each time and reached new highs.

The problem: Many beginners enter at the top, driven by FOMO and media hype, and sell in panic at the first major decline. DCA – dollar cost averaging – is the method that cushions this behavior. Instead of waiting for the supposedly perfect moment, you invest a fixed amount regularly in cryptos like $Bitcoin or $Ethereum.

In this article, we will show you how DCA works in crypto, how to strategically use crash phases, and how to invest step by step with a crypto savings plan – for example, through Bitpanda.

What is Dollar Cost Averaging (DCA) in the Crypto Space?

Dollar-Cost-Averaging (DCA) means that you regularly buy a fixed amount of an asset – for example, €100 in Bitcoin every month. DCA allows for regular investments in cryptocurrencies without having to worry about the current price.

The cost averaging effect works like this:

- When prices are low, you automatically buy more units (e.g., more Satoshis). Investors buy more units at low prices and fewer at high prices.

- When prices are high, you buy fewer units – this creates an averaged entry price over time.

- DCA can lower the average cost per unit because you don’t buy everything at a single (possibly unfavorable) moment.

- DCA eliminates the stress of timing the purchase – you don’t need to understand technical chart analysis or market forecasts.

This method comes from traditional investing: ETF savings plans, mutual funds, and retirement plans operate on the same principle. DCA is simple for beginners and does not require extensive knowledge of cryptocurrency markets. It does not guarantee profits, but it limits psychological errors such as panic selling and impulsive trading.

Why DCA Makes Sense in Volatile Cryptocurrency Markets

The crypto market is notorious for its volatility. Daily movements of ±10% are not uncommon, and cycles where prices like Bitcoin drop from $120,000 to $60,000 are part of everyday life. DCA is particularly advantageous in volatile markets like cryptocurrencies because it allows you to take advantage of these fluctuations.

Market timing is extremely difficult in these markets. Even professional traders and analysts regularly miss the mark when it comes to identifying tops or bottoms. DCA reduces the risk of investing just before a market downturn because you spread your capital over many points in time.

DCA aims to reduce the effects of market volatility. Instead of letting market fluctuations control you, you automatically buy in bull and bear markets. This way, you benefit on average from the long-term trend of the asset.

Pension funds and retirement savings plans set the example: They regularly invest large sums in broadly diversified assets over decades without trying to perfectly time short-term fluctuations. DCA works particularly well for long-term crypto investors with a time horizon of 5 to 10+ years who believe in the fundamental value of Bitcoin and Ethereum.

Strategies for Crash Phases: DCA, Stablecoins & Waiting

Bitcoin halves from $120,000 to $60,000. Many altcoins fall 70–90%. The monetary value in the portfolio shrinks. Emotions run high. Right now, the plan separates from the panic. Here are three options you have as an investor in such phases:

Option 1 – Continue Investing via DCA: Many long-term investors simply let their existing crypto savings plan continue. DCA allows for the purchase of more units at low prices – and that is the core of the strategy. Those who consistently invest during the crash significantly lower their average entry price. An example of DCA is a monthly investment of €100 – regardless of whether Bitcoin is at $120,000 or $60,000.

Option 2 – Partially Shift to Stablecoins: Some investors park a portion of their position in stablecoins (e.g., USDT, USDC, EURS). This secures liquidity and allows for larger special purchases when signs of recovery or further downward exaggerations appear.

Option 3 – Pause the Savings Plan and Monitor the Market: Some investors temporarily stop their DCA and analyze the situation: macro data like interest policy, on-chain data like hash rate or wallet activity, regulatory developments. Only when there are signals like rising trading volumes or breaking through important resistance levels do they become active again.

None of these options are “always right.” The right choice depends on your risk tolerance, liquidity, and time horizon. What matters is a pre-defined plan rather than spontaneous panic decisions.

Applying DCA Specifically: Examples and Avoiding Typical Mistakes

Imagine you invest €200 a month in Bitcoin over 24 months. Month 1 starts at the all-time high of $120,000. In the following months, the price falls to $60,000, partially recovers, and continues to fluctuate. DCA can lower the average purchase price of an asset – your averaged entry price will end up significantly below the top, perhaps at $80,000–90,000.

Here’s how to implement DCA correctly:

- Choose a fixed interval: monthly is standard, weekly smooths out more but incurs more fees.

- Determine an amount you can afford – e.g., €50, €100, or €500 per month. Never use money that you need in the short term for rent or emergencies.

- Focus on established coins with high market capitalization: Bitcoin and Ethereum have the longest history and the broadest acceptance.

Typical mistakes to avoid:

- Starting DCA and stopping after the first significant loss

- Constantly adjusting amounts up and down based on news

- Going completely “all-in” shortly after a hype or due to a QR code in an advertisement

- Buying too many speculative altcoins instead of focusing on quality assets

DCA is particularly suitable for established crypto assets. High-risk altcoins are often more cyclical and less predictable – DCA does not protect against permanent losses in those cases.

How to Start with DCA through Bitpanda (Step-by-Step Guide)

Bitpanda is a user-friendly platform that is particularly suitable for starting with DCA. DCA is suitable for beginners and long-term investors – and Bitpanda makes the process as easy as possible. Bitpanda is the only regulated crypto exchange under BaFin, which offers a high level of security.

Step 1 – Registration via Our Link: Click here, open a free account, and confirm your email address. The registration takes only a few minutes.

Step 2 – Identity Verification (KYC): Crypto exchanges must verify users with an ID. As a regulated provider, Bitpanda requires verification via ID or passport, possibly also via video identification – comparable to opening an account at a bank.

Step 3 – Deposit Euro Balance: Transfer euros to your Bitpanda account via SEPA or other payment methods. A SEPA deposit typically takes 1–2 banking days. Other deposits like credit cards are also possible depending on the region.

Step 4 – Set Up Crypto Savings Plan (Auto-Invest): In the app or on the website, you can create a savings plan for Bitcoin or other crypto assets. Choose your amount (e.g., €50 monthly), the interval, and the payment source. Many crypto exchanges offer automated savings plans for DCA – Bitpanda's Auto-Invest function is among the most convenient.

Step 5 – Regularly Check Your Portfolio, But Don’t Trade Daily: Review your plan at intervals of 3–6 months. Adjust the strategy as needed, but avoid frantic reactions to every price fluctuation. DCA requires long-term discipline and consistent purchases.

Our savings plan comparison provides additional information on how Bitpanda compares to other providers.

How to Find the Right Savings Plan Provider (Including Our Savings Plan Comparison)

A comparison of crypto savings plans is crucial because the differences in fees, coin selection, minimum amounts, and regulatory status are significant. Transaction costs can diminish returns with frequent purchases – that’s why it’s worth taking a close look at the fee structure.

Here’s an overview of the fees of important providers:

| Provider | Trading Fees | Special Features |

|---|---|---|

| Bitvavo | 0.25% | 2-Factor Authentication, lowest spread |

| Kraken Pro | 0.25–0.4% | Founded in 2011, high security standards |

| BSDEX (Stuttgart Exchange) | 0.35% | Regulated in Germany |

| Bitcoin.de | 1.0% | Marketplace model |

| Bison (Bison App) | 1.25% | Multi-layer security concept, ISO certified |

| Coinbase | up to 2.5% | High fees, especially for altcoins |

| Bitpanda | variable | Only regulated crypto platform under BaFin |

SMS-TAN procedures are considered less secure than app-based 2FA – ensure that your provider offers modern authentication. Bitvavo uses 2-Factor Authentication for added security. Kraken was founded in 2011 and has high security standards. Bison has a multi-layer security concept and is ISO certified.

A good DCA provider should meet the following criteria:

- Transparent fee structure without hidden costs

- Real cryptocurrencies (not just certificates or stock-like products)

- Regulated custody and licensing

- Easy setup for recurring purchases

Our crypto savings plan and exchange comparison presents these points clearly. Bitpanda offers a particularly straightforward way to get started: a wide selection of crypto assets, a convenient savings plan function, staking options, and the Bitpanda Card. Getting started through our referral link takes just a few minutes.

Still, keep in mind: The choice should always fit your own needs – risk profile, desired coins, additional features like rewards or payouts. The Trade Republic card or other financial products can also be sensibly used depending on your goals. Investors in the Netherlands may have different provider options than users in Germany.

Psychology & Long-Term Thinking: What We Can Learn from Investment and Pension Funds

Successful investing has less to do with “secret knowledge” than with discipline, patience, and a clear system. Large companies, pension funds, and retirement funds regularly invest large sums into broadly diversified portfolios over the years – monthly or quarterly. They do not try to time short-term fluctuations.

Individual investors can approach a Bitcoin or crypto savings plan similarly on a smaller scale: regular amounts, long investment horizon, clear strategy, no frantic trading or selling.

DCA promotes disciplined investing without emotional decisions. Emotional control is achieved through the automation of DCA – you don’t have to check the price every day and ponder over buying or selling. DCA minimizes emotional decisions while investing and reduces the impact of market volatility on your well-being.

In crash phases – such as the drop from $120,000 to $60,000 – the DCA investor knows: They are buying at a lower price now. The focus is on the long-term trend, not the daily price. This psychological influence is enormous and makes the difference between panic selling and calmly moving forward.

Long-term thinking also means viewing crypto only as part of the overall portfolio. Timeframes of 5 to 10+ years are realistic – just like with traditional investments in funds or stocks.

Risks & Limits of Dollar Cost Averaging in Crypto