Cryptocurrency Posts

Crypto Briefing

Central banks' gold buying spree signals a shift towards safer assets, potentially impacting global monetary policies and economic stability.

The post Gold prices surge as central banks buy record 289 tonnes in Q2 2026: WSJ appeared first on Crypto Briefing.

Riot's strategic pivot towards AI infrastructure highlights a growing trend of tech firms diversifying to capitalize on AI demand.

The post Riot Platforms shares soar 25% after-hours on news of $9.1B Anthropic deal appeared first on Crypto Briefing.

Ghostjacking highlights the urgent need for organizations to reassess AI agent permissions, emphasizing security over automation to prevent cascading failures.

The post Ghostjacking attack uses poisoned logs to compromise AI agents appeared first on Crypto Briefing.

The Clarity Act's potential passage could reshape digital asset regulation, affecting market dynamics and regulatory authority distribution.

The post White House committed to passing Clarity Act in September, says advisor appeared first on Crypto Briefing.

The stalled peace talks and escalating conflict may prolong instability, affecting global markets and reducing ceasefire prospects significantly.

The post Trump-Putin peace talks stall, Ukraine conflict escalates appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Blockstream Debuts Swaps, Allowing Bitcoiners to Move Between Lightning and Main Network With Ease

Bitcoin infrastructure company Blockstream has announced a new feature allowing users to make trustless swaps.

Dubbed Blockstream Swaps, the idea is that Bitcoiners will be able to quickly move between the main chain and Lightning network.

It comes after non-custodial Bitcoin swap provider Boltz suspended its service after it said attackers were finding vulnerabilities faster than its team could fix using AI.

“In support of the broader Bitcoin and Liquid ecosystem, Blockstream is launching Blockstream Swaps,” Blockstream said.

“This initiative was already under development to ensure a resilient suite of utility for the ecosystem, and it complements the providers already doing this work rather than replacing any one of them.”

The idea, added Blockstream, is users can move funds across layers while never losing full control over their funds.

To use Lightning, users will not need to run a node or channel — as is normally needed with Lightning — and can simply hold a Bitcoin or LBTC balance and let a swap convert at the moment of payment.

LBTC is the native asset of the Liquid Network, a Bitcoin layer-2 sidechain created by Blockstream.

“This initiative was already under development to ensure a resilient suite of utility for the ecosystem, and it complements the providers already doing this work rather than replacing any one of them,” added Blocksteam’s announcement.

Boltz this month suspended its Bitcoin swap service. It said that a surge in AI-assisted attacks left it unable to continue operating safely.

Crypto hacks have surged, with security experts warning that cybercriminals are using AI to search for bugs in crypto projects and then take advantage of errors auditors may have missed.

This post Blockstream Debuts Swaps, Allowing Bitcoiners to Move Between Lightning and Main Network With Ease first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

BTCPay Server Offers a 3 Bitcoin Bounty for Recovery of Stolen Funds After Wallet Exploit

Supporters of BTCPay Server have committed to funding a bounty of up to three Bitcoins for the recovery of funds stolen through a recently disclosed vulnerability in the open-source bitcoin payment processor, the project said in a statement.

The bounty is set at 10 percent of whatever is recovered, capped at three coins in the event of a full recovery.

The project even extended the offer to the attacker directly alongside anyone else holding actionable information, directing them to a dedicated security address and offering Signal or other encrypted channels on request.

Hackers last week managed to extract Lightning Network admin macaroon credentials from affected BTCPay Server instances. The project published technical details and remediation guidance in a separate security advisory.

“To the users who lost funds: we are sorry,” the project said in a statement. “We will examine our mistakes, but regret alone will not help affected users or secure the project. There is no time to waste. We have to learn, improve, and act quickly.”

The BTCPay Server Foundation said it would donate 0.21 Bitcoins to Sparrow Wallet developer Craig Raw and a further 0.21 Bitcoins to the Bitcoin Red Team fund in recognition of their responsible disclosure of the vulnerability.

Separately, the project said it has been contacted by security teams at exchanges, blockchain analytics firms and law enforcement agencies offering assistance in tracking the stolen coins.

Affected users who have not yet come forward are being asked to share on-chain addresses and transaction details, and to file reports with local authorities and any exchange or service where the funds surface.

Individual reports, the project said, help preserve records and establish a chain of evidence that improves the odds of funds being frozen.

The project added that improving AI models are making it faster and cheaper to comb large codebases for weaknesses, shifting the balance toward attackers, and that Bitcoin projects are feeling it first because they are unusually valuable targets.

This post BTCPay Server Offers a 3 Bitcoin Bounty for Recovery of Stolen Funds After Wallet Exploit first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Bitcoin Exchange-Traded Funds See Spike In Inflows Following Huge Hack

American Bitcoin exchange-traded funds have had their biggest weekly inflow since April, taking in $850 million last week, according to Bloomberg figures.

The major U.S. funds managed by BlackRock, Fidelity, Grayscale, Morgan Stanley and others have received the cash the week after hackers targeted Coinkite’s popular Coldcard product.

Hackers started stealing millions in Bitcoin from Coldcard wallets after discovering a vulnerability in the product’s software. Some estimates put the amount of Bitcoin lost now at over $130 million.

JUST IN: BlackRock tells Bloomberg they've "seen consistently" that Bitcoin ETF investors are buying and holding BTC "long term" on this dip

— Bitcoin Magazine (@BitcoinMagazine) August 10, 2026

"That is being exhibited through this downturn." HODLpic.twitter.com/9D0j9uLJwu

The incident has rattled the BTC community that typically praises cold storage solutions.

Speaking on Bloomberg’s ETF IQ show on Monday, Robert Mitchnick, global head of digital assets at BlackRock, said that since the ETFs’ approval in 2024, investors have wanted a “very simple turnkey trusted vehicle and not have to worry about all the unique elements of Bitcoin and crypto security that generally custody otherwise would require of an investor.”

Speaking about the Coldcard hack, he added: “What’s also important to recognize is that that is not a breach of Bitcoin or any other crypto protocol — those are individual security mismanagement issues that happen from various individuals or providers.”

It isn’t clear whether investors are rotating out of cold storage into the ETFs since the hack but the funds have seen a spike in trading action.

Bitcoin’s price has typically done well when investors have thrown cash at the products but the leading cryptocurrency is now flat over a seven-day period, priced at $63,861.

BlackRock’s iShares Bitcoin Trust took most of last week’s inflows but other funds managed by Morgan Stanley and Fidelity also experienced trading action.

The U.S. Securities and Exchange Commission in 2024 approved the slew of Bitcoin investment funds which went on to have the most successful launch in the history of ETFs.

Investors previously put off from buying Bitcoin due to the complexities of cold storage and private keys can now buy shares that trade on stock exchanges that track the price of Bitcoin.

The ETFs — managed by other top Wall Street fund managers — currently manage nearly $80 billion in assets, according to Coinglass data.

This post Bitcoin Exchange-Traded Funds See Spike In Inflows Following Huge Hack first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

TD Cowen Gives Crypto Clarity Act a 25% Chance of Passing This Fall

Investment bank TD Securities has said that the long-awaited crypto Clarity Act has a slim chance of getting passed in a Monday note, citing last week’s delay and potential stalling from the Democrats.

The bank said that now the bill won’t be passed before the summer, it only has a 25% of getting passed in September.

Lawmakers were hoping a crucial vote on the long-awaited crypto market structure bill was to go ahead before a five-week recess but news dropped last week that there was a delay and now the Senate will vote on the bill in September.

“The bill is not dead, but the path forward is harder,” the bank said. “We assign a 75% probability that Clarity fails to become law this fall.”

TD Cowen said one likely outcome was for cloture to pass initially in September but then for Republicans to block Democratic amendments on the ethics and AML sections, leading Democrats to sink the second cloture vote.

It added that it was also likely no cloture vote ever happens. Cloture is the Senate’s procedural tool for ending debate on a bill so it can move to a final vote.

News dropped last week a vote on the bill would have to wait until lawmakers return from August recess. Bipartisan work has gone into the Clarity Act, which was passed by the House of Representatives last year, but some Republicans have accused Democrats of stalling the bill.

The bill, if passed, would be a federal rulebook for U.S. cryptocurrency markets. The latest draft of the Clarity Act contains language — drafted by Democrats and Republicans — banning government officials from promoting or making money from crypto. It started circulating in July.

Still, Democrats like Senator Elizabeth Warren, who has from the beginning criticized the Clarity Act, have claimed that new legislation will benefit the president and his family.

Major financial institutions — not just crypto companies — have backed the bill, including Goldman Sachs and Fidelity, as well as law enforcement groups.

This post TD Cowen Gives Crypto Clarity Act a 25% Chance of Passing This Fall first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Strategy Sells Bitcoin Again For Cash Buffer, STRC Buyback

Bitcoin treasury company Strategy on Monday announced that it again sold Bitcoin last week, and used the cash to buy back its preferred stock.

In a filing with the Securities and Exchange Commission, the Nasdaq-listed company said it sold 1,690 coins for $108.6 million, bringing its holdings to 840,447 coins, down from 842,138 it had the week before.

The cash, Strategy said, went to buying 1,152,020 STRC shares worth $109 million as part of a buyback program. STRC in June fell far below the $100 stated amount.

Strategy, which went from being an enterprise software company to buying Bitcoin in 2020, hasn’t bought any Bitcoin since June.

The company has reassured investors that selling Bitcoin is just part of its plan to grow its cash buffer. Strategy said Monday that it now holds $4.65 billion in cash.

Strategy’s stock (Nasdaq: MSTR) was trading nearly 3% lower on Monday. The stock has taken a hit since the price of Bitcoin nosedived last year. Investors buy MSTR to get amplified exposure to the biggest digital asset.

But now, as Bitcoin is nearly 50% below its October record, MSTR is down nearly 80% from the all-time high it notched last year.

Despite the sale, Strategy has maintained that its long-term posture toward Bitcoin hasn’t changed.

Strategy — formerly MicroStrategy — began buying Bitcoin in August 2020 as a treasury strategy to boost shareholder returns during the pandemic.

It has since spent more than $63.5 billion buying Bitcoin and remains by far the largest corporate holder of Bitcoin in the world.

Strategy’s approach spawned a wave of copycat companies that have since adopted similar crypto-treasury strategies of their own.

The company maintains that its long-term posture toward Bitcoin is still the same. CEO Phong Le he isn’t worried about the current bear market, and that the company plans to remain a long-term buyer of Bitcoin despite its recent sales.

This post Strategy Sells Bitcoin Again For Cash Buffer, STRC Buyback first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

CryptoSlate

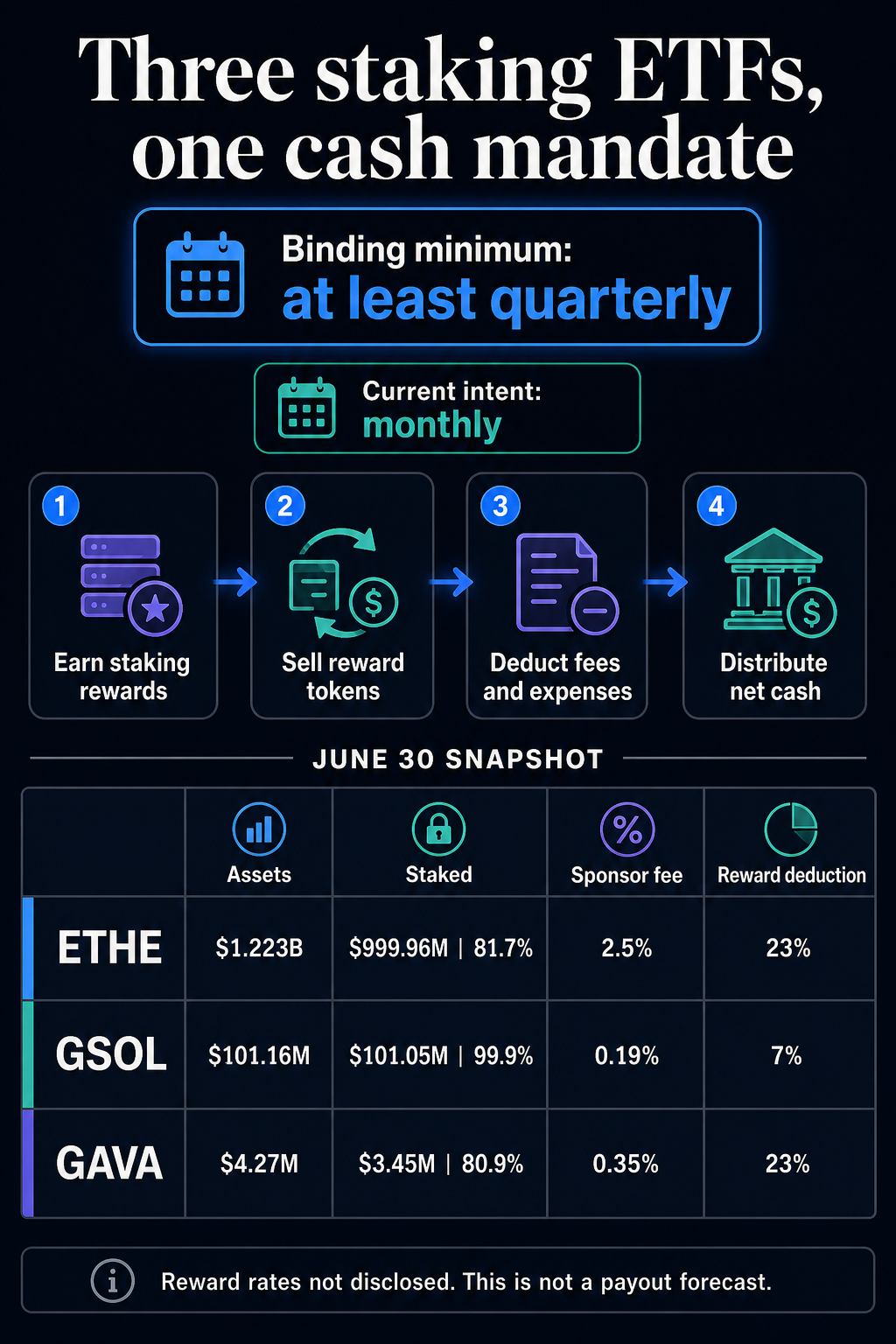

Grayscale has formalized a mandatory minimum cadence for converting staking rewards from three crypto exchange-traded products into cash and paying the net proceeds to shareholders.

Trust amendments executed Aug. 6 for the Grayscale Ethereum Staking ETF (ETHE), Grayscale Solana Staking ETF (GSOL) and Grayscale Avalanche Staking ETF (GAVA) require each product to reduce “Staking Consideration” to cash no less often than quarterly. Net proceeds must then be distributed promptly after applicable fees and trust expenses.

The three trusts currently intend to make distributions monthly, according to Form 8-K filings submitted Aug. 7, but the binding floor is quarterly.

As the trusts receive staking rewards, they must periodically sell that earned consideration and pass the resulting cash to investors. The rule therefore creates a recurring market sell flow for reward tokens.

It does not create scheduled liquidation of the trusts’ principal ETH, SOL or AVAX holdings. The distribution clauses apply to staking consideration earned by the products. Other disclosures still permit token sales for separate purposes, including redemptions, fees and expenses.

The amendments establish that reward tokens will be converted, but not how much will be sold in any future period.

As of June 30, ETHE reported $1.22 billion in total assets and $999.96 million in staked ETH, equivalent to roughly 81.7% of its assets. GSOL reported $101.16 million in assets and $101.05 million of staked SOL, or about 99.9%. GAVA reported $4.27 million in assets and $3.45 million of staked AVAX, or about 80.9%.

The reports do not provide current annualized reward rates. Future sales and payouts will depend on rewards actually received, the amount staked, protocol-level reward rates, token prices, and deductions.

ETHE charged a 2.5% annual Sponsor fee, while its Sponsor staking fee and validator fees together accounted for 23% of gross rewards as of June 30. GAVA disclosed a 0.35% annual Sponsor fee and the same 23% aggregate reward deduction. GSOL disclosed a 0.19% annual Sponsor fee and a 7% aggregate staking-related deduction covering Sponsor and validator fees.

The annual Sponsor fees and the reward deductions use different bases and should not be treated as additive percentages.

ETHE offers an operating precedent without a forecast. The fund paid approximately $9.4 million, or $0.083178 per share, on Jan. 6 after selling staking rewards earned from Oct. 6 through Dec. 31, 2025. Different asset levels, staking participation, fees, reward rates, and token prices make it unsafe to extrapolate that payment across the three products.

Grayscale move creates a tax complexity

The conversion to cash planned by Grayscale may simplify what shareholders receive, but ETHE and GSOL tax disclosures indicate that the underlying activity can create multiple potential tax consequences.

Assuming grantor-trust treatment applies, a US holder is generally treated as receiving a pro rata share of staking income when the trust earns it.

A subsequent trust sale of reward tokens to fund a cash distribution can also allocate a pro rata capital gain or loss to the holder. Under the treatment described in the filings, receiving the cash itself should not be an additional taxable event.

The disclosures caution that the grantor-trust position is not guaranteed. They also flag potential unrelated business taxable income for some tax-exempt holders and unresolved sourcing or withholding questions for non-US investors.

The amendments therefore create a recurring operational loop: earn reward tokens, sell them, and distribute net cash. Its market sell flow will depend on realized rewards and deductions, not headline asset totals alone.

The post Grayscale turned more than $1.1 billion of staked crypto into a recurring reward-sale machine for ETF holders appeared first on CryptoSlate.

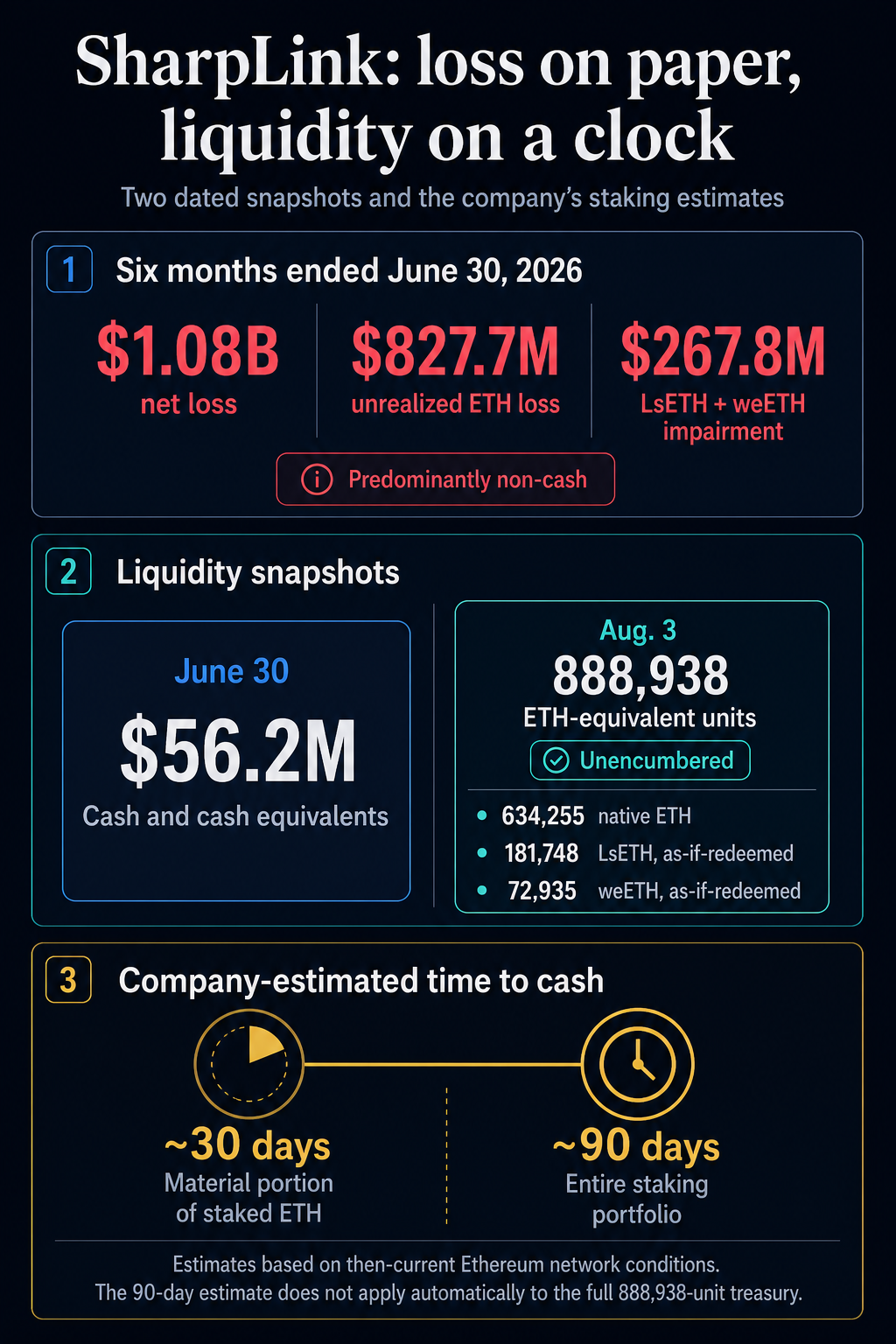

Ethereum treasury company SharpLink reported a $1.08 billion net loss for the six months ended June 30. Its Aug. 7 quarterly filing attributes most of that result to price-related accounting charges. Much of the company’s treasury is staked, making conversion time a material part of its liquidity profile.

The filing attributes $827.7 million of the loss to an unrealized decline in the value of ETH and another $267.8 million to impairments of LsETH and weETH, tokens representing liquid staking and restaking positions. Those predominantly non-cash charges exceeded the net loss because other results partly offset them.

The six-month loss was 934.3% above the roughly $104.4 million recorded a year earlier. The comparison spans different operating profiles because SharpLink launched its ETH treasury strategy on June 2, 2025, near the end of the earlier period.

What Ethereum can become cash, and when

SharpLink held $56.2 million in cash and cash equivalents at June 30. In a separately dated snapshot, it reported 888,938 unencumbered ETH-equivalent units as of Aug. 3: 634,255 native ETH, 181,748 ETH on an as-if-redeemed basis from LsETH and 72,935 ETH on the same basis from weETH.

ETH traded at $1,916.57 as of Aug. 10, giving the Aug. 3 count an illustrative gross mark of roughly $1.7 billion. That mark mixes dates and includes as-if-redeemed staking positions, so cash proceeds would depend on redemption timing and sale prices.

SharpLink estimates that, under Ethereum network conditions at the time of the filing, a material portion of its staked ETH could be withdrawn and converted to cash in about 30 days.

The company puts the entire staking portfolio at about 90 days, and the filing states the 90-day timing for the staking portfolio and separately reports 888,938 ETH-equivalent units in the total treasury.

Ethereum validator exits vary with network demand and require sweep processing after exit. LsETH redemptions can require validator exits when protocol liquidity is insufficient, while weETH withdrawals can face network-dependent delays despite having no fixed lock period.

SharpLink’s common shares issued and outstanding increased 10.3% to 216.98 million at June 30 from 196.71 million at the end of 2025. In June, the company raised about $75 million gross by selling 10,013,351 shares with accompanying warrants at a combined purchase price of $7.49 per package.

It used part of the proceeds to buy 10,000 ETH for about $16.1 million and repurchased 2.13 million shares.

SharpLink describes its unencumbered crypto assets as additional liquidity support beyond cash. The filing also warns that stressed markets could impede sales or force unfavorable pricing, and its liquidity depends on both conversion time and the price available when cash is needed.

The post SharpLink posts $1B loss as its $1.7B Ethereum treasury could take 90 days to fully convert to cash appeared first on CryptoSlate.

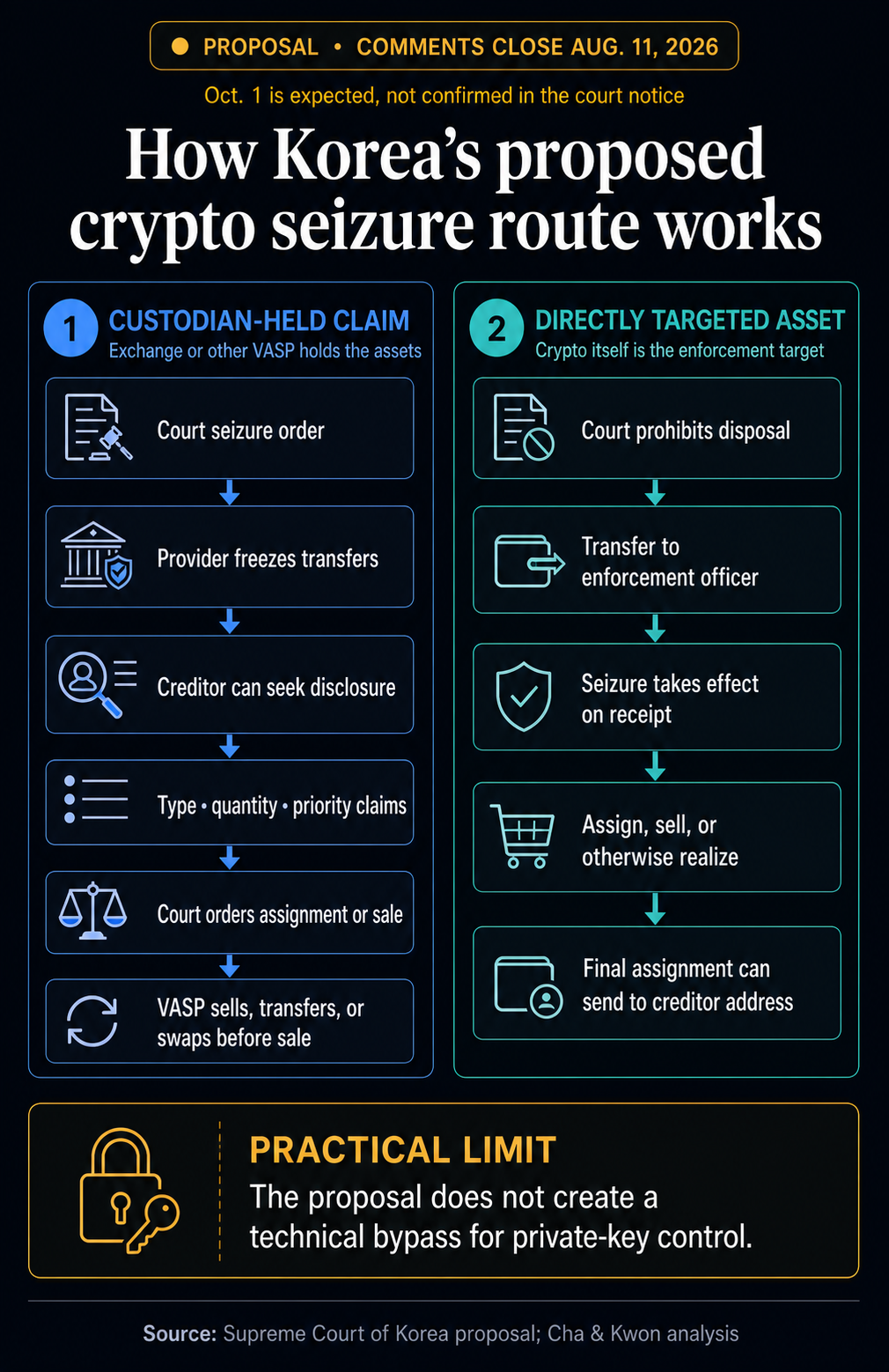

South Korea is nearing an Aug. 11 deadline for public comments on proposed crypto seizure rules that could give exchanges just seven days to disclose customer holdings once served with a court order.

The Supreme Court’s proposed amendments to the Civil Execution Rules would create a standardized process for creditors to freeze, identify and liquidate virtual assets held by debtors. If finalized on the current timetable, the rules are expected to take effect Oct. 1.

That would leave exchanges and other virtual asset service providers roughly seven weeks after the consultation closes to prepare for a more formal role in civil debt enforcement.

For crypto held through a custodian, a court could attach the debtor’s right to receive the assets rather than initially seizing the coins themselves. Once served, the provider would be barred from transferring the corresponding assets to the debtor, who would also lose the ability to dispose of the claim.

Creditors could then ask the court to require the provider to disclose what it holds. The exchange would have one week to state whether it recognizes the debtor’s claim, identify the type and quantity of assets, and disclose competing seizures, provisional orders, or priority rights.

The framework could have broad reach in one of the world’s most retail-heavy crypto markets. As of February 2025, 16.29 million people held accounts across South Korea’s five largest exchanges, equivalent to nearly 32% of the population. The figure exceeded the roughly 14.2 million people who held domestic listed stocks at the end of 2024.

Once assets are identified and frozen, courts could assign them to creditors or order their liquidation. A virtual asset service provider could execute the sale, while crypto could also be transferred to an enforcement officer’s account or converted into more liquid assets before disposal.

However, the process becomes harder when a debtor controls the crypto directly.

A court could prohibit disposal and order a transfer to an enforcement officer, but seizure would take effect only when the officer actually receives the assets, leaving private-key control as a practical constraint.

The proposal also fits into South Korea’s broader effort to build formal rules around a crypto market that has moved deep into the financial mainstream.

Authorities have already introduced statutory protections for virtual asset users and are tightening exchange registration and anti-money laundering requirements, including planned expansion of the travel rule and additional controls around personal wallets and stablecoins.

The seizure rules would extend that regulatory build-out into civil debt collection. They would also apply to proceedings already underway when they take effect, making the period between the Aug. 11 consultation deadline and the proposed Oct. 1 rollout particularly relevant for exchanges preparing to handle court orders.

The post South Korea puts crypto exchanges on a seven-day clock under new seizure rules appeared first on CryptoSlate.

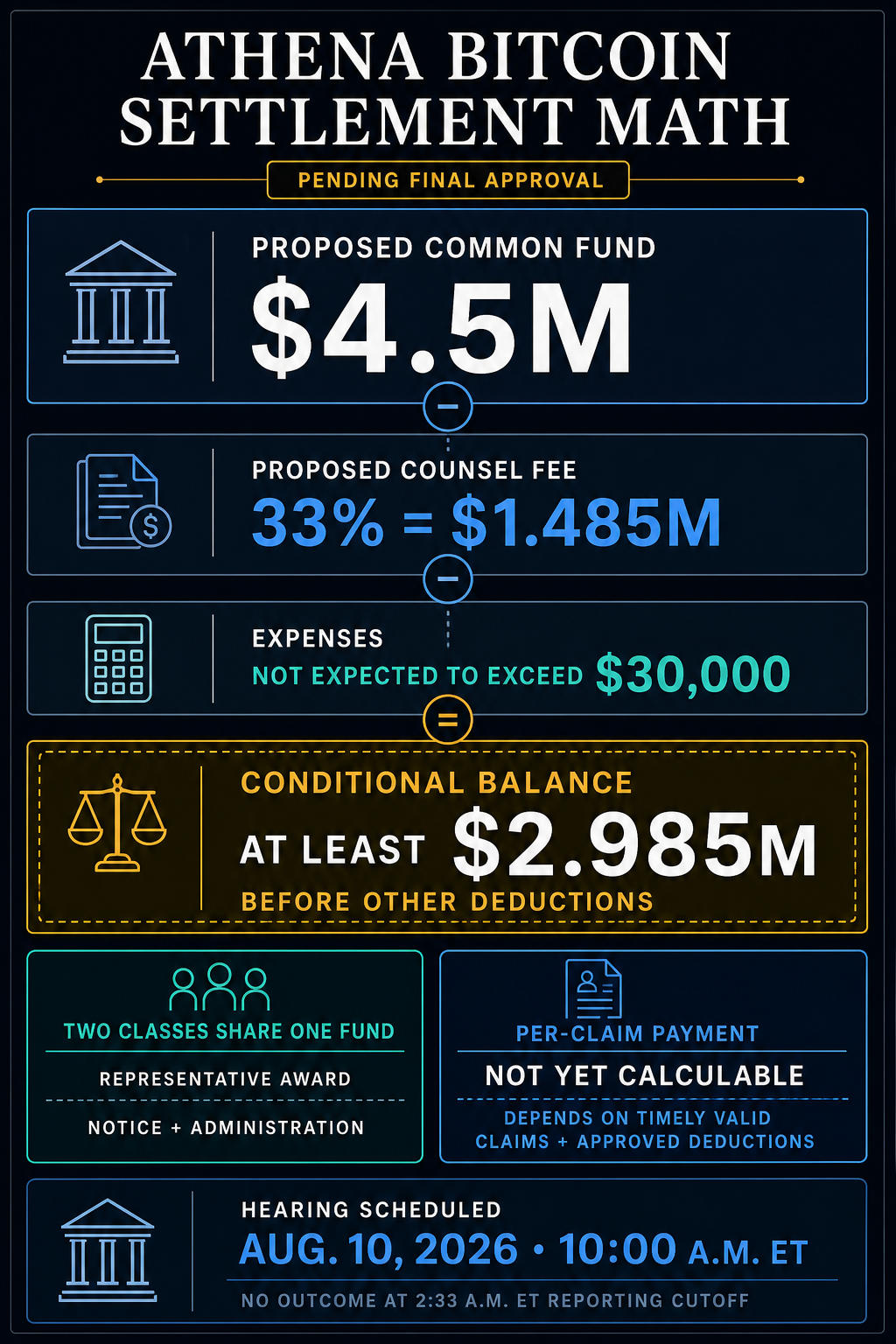

Crypto ATM firm Athena Bitcoin’s proposed $4.5 million settlement over telemarketing texts will face its final review in federal court on Aug. 10. Judge Mark E. Walker will consider whether to approve the agreement, class counsel’s proposed fee and a representative award.

The settlement remained pending at the reporting cutoff.

The case alleges that Athena sent more than one promotional text within a 12-month period to certain recipients more than 30 days after they had sent a message consisting only of “STOP.” Athena has denied wrongdoing or any violation of the law, and the settlement does not constitute a court finding that the allegations are true.

The federal class covers residential subscribers across the US from Aug. 20, 2020, to Aug. 20, 2024, and excludes business numbers. A separate class covers qualifying Florida recipients under the Florida Telephone Solicitation Act, using different eligibility thresholds.

Both classes would share the same $4.5 million settlement fund, which Athena Bitcoin agreed to create and is subject to final approval.

How much could remain for claimants

The court recorded class counsel’s intent to seek 33% of the fund, or $1.48 million, plus costs and expenses not expected to exceed $30,000, in its March 11 preliminary-approval order.

If the court grants the proposed fee and litigation expenses are $30,000 or less, nearly $3 million would remain before any representative award and the costs of notifying class members and administering the settlement.

The arithmetic does not establish the final pool available for payments.

The court-authorized settlement FAQ says each eligible participant’s payment will also depend on the number of timely, valid claims.

The pre-hearing materials available on Aug. 10 did not provide an accepted-claim count or the final court-approved deductions, so a per-claimant payment could not be calculated.

Both classes draw from the common fund, so every approved deduction reduces the amount available for qualifying claims.

Any payments remain contingent on the court approving the agreement and the settlement becoming final. Until a ruling addresses the agreement and requested deductions, the $4.5 million remains a proposed common fund.

The post Athena Bitcoin agreed to a $4.5 million settlement, but claimants may have less than $3 million to split appeared first on CryptoSlate.

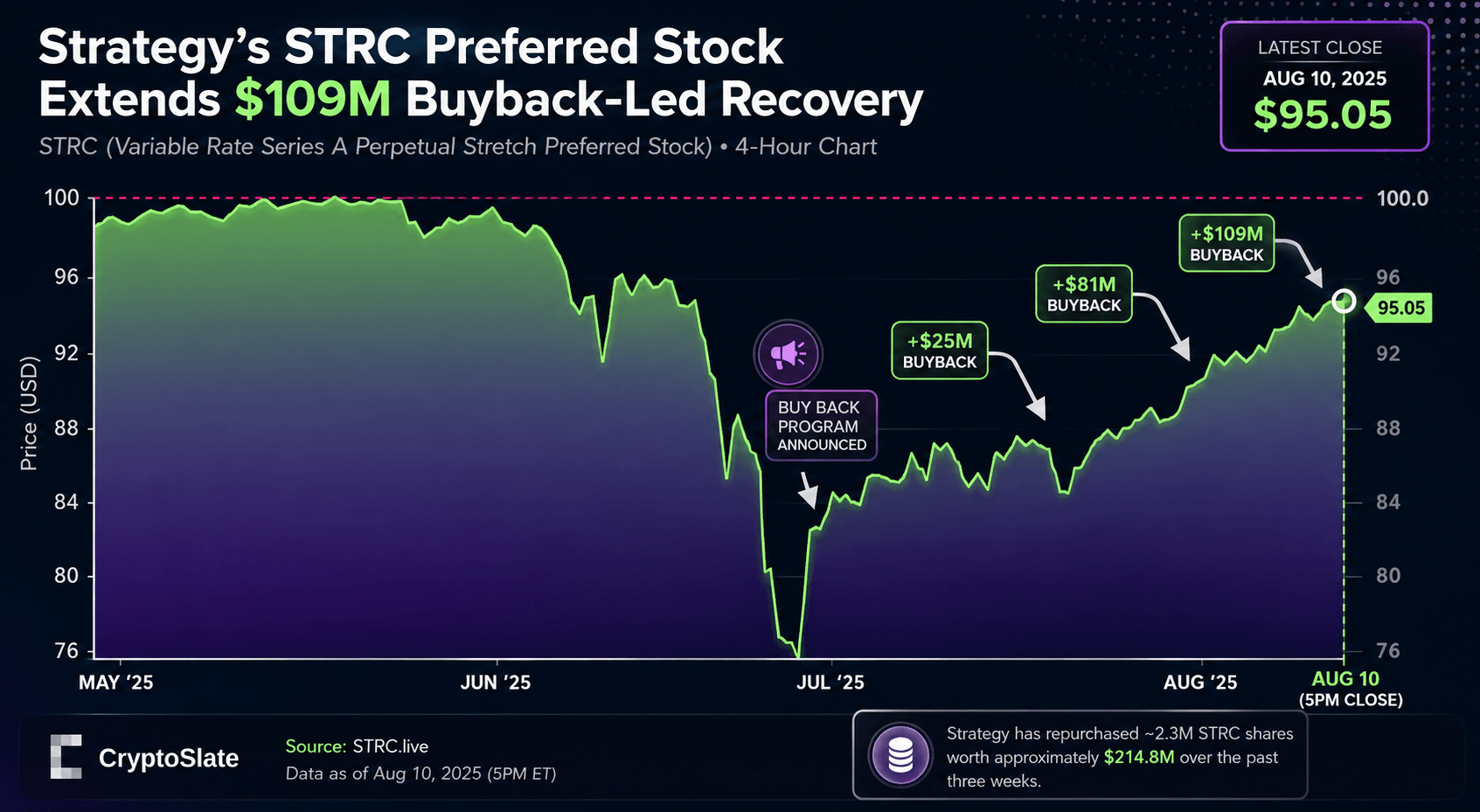

Strategy’s preferred stock STRC is steadily moving back toward its $100 target as the Bitcoin treasury company increases its purchases of the shares.

Data from STRC.live showed that STRC traded around $95 on Monday, extending a recovery from its late-June low of about $74 as Strategy combined open-market repurchases with a 12% annualized dividend to narrow the security’s discount.

Over the past three weeks, Strategy has acquired roughly 2.3 million STRC shares worth approximately $214.8 million. Its latest purchase was also the largest, with the company spending $108.6 million on 1.1 million shares during the week ended Aug. 9.

That followed earlier purchases of $25 million and $81.2 million.

Strategy still has $785.2 million available under the $1 billion Digital Credit Securities Repurchase Program it authorized in June.

Bitcoin sales increasingly fund STRC buybacks

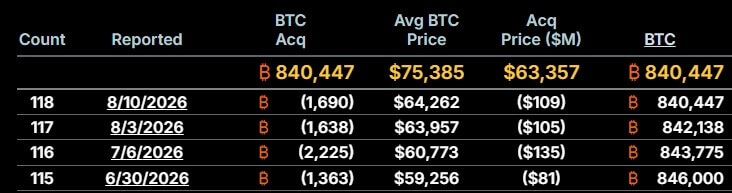

In the past weeks, Strategy has increasingly turned to its Bitcoin treasury to finance the STRC purchases. During the week ended Aug. 9, the company sold 1,690 BTC for $108.6 million at an average price of $64,262.

The transaction followed a similar move a week earlier, when Strategy sold 1,638 BTC for $104.7 million. About $52.3 million of those proceeds went toward an $81.2 million STRC repurchase, with MSTR issuance providing the remainder.

Together, Strategy has sold 3,328 BTC for about $213.3 million over the past two weeks while spending $189.8 million on STRC during the same period.

The latest sale reduced Strategy’s Bitcoin holdings to 840,447 BTC from 842,138 BTC a week earlier. The company’s remaining coins were acquired for $63.36 billion at an average price of $75,385.

These transactions show Bitcoin taking on a broader role under Strategy’s Digital Credit Capital Framework. The company can now monetize portions of its holdings to support preferred securities and other obligations across its capital structure.

Strategy has sold 6,948 BTC so far this year, reducing its holdings from a June peak of 847,363 BTC. The decline remains small relative to its overall treasury, as the firm continues to be the largest corporate holder of Bitcoin globally.

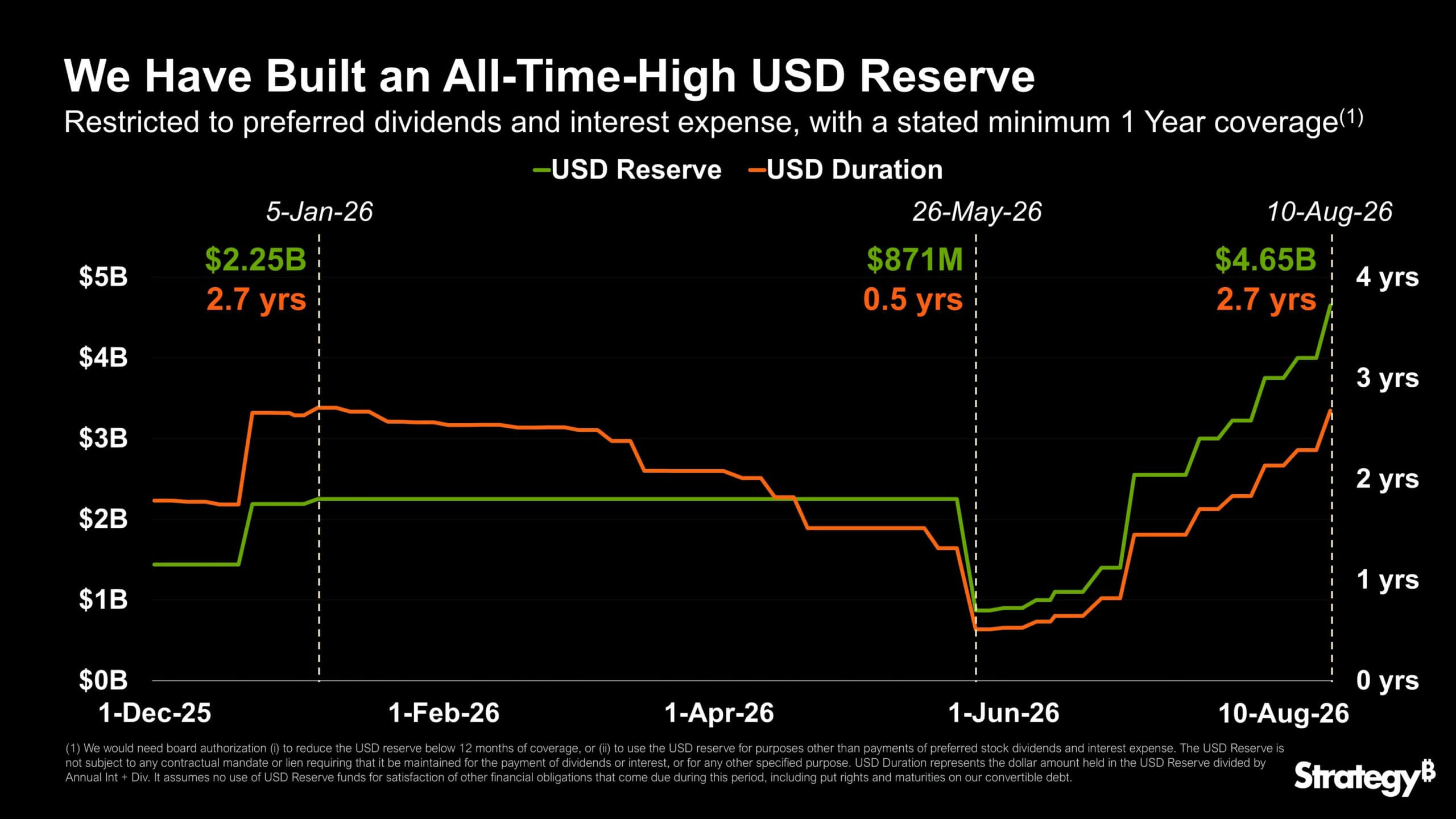

Strategy pushes USD reserve to record $4.65 billion

Strategy also accelerated the buildout of its cash reserves during the week, raising an additional $653.1 million through common stock issuance.

The company sold 6.5 million MSTR shares through its at-the-market program and directed $650 million of the proceeds into its US dollar reserve, with the remaining $3.1 million added to its general cash balance.

That increased the dollar reserve to an all-time high of $4.65 billion, up from $4 billion a week earlier.

The reserve provides liquidity for Strategy’s preferred-stock dividends and interest payments, giving the company a larger buffer against the recurring obligations created by its expanding capital structure.

Strategy CEO Phong Le said the reserve has grown rapidly since the company introduced its new capital-management framework in late June. He wrote:

“Our USD Reserve and Duration are now at all-time highs. In 2.5 months, we added nearly $3.8 billion and grew both more than 5X. This is the Digital Credit Capital Framework at work.”

The latest addition extended Strategy’s dollar reserve duration by another 143 days, bringing it to approximately 2.7 years, according to Executive Chairman Michael Saylor.

Strategy now holds enough dollars to cover nearly three years of its current preferred dividends and debt interest obligations, substantially reducing near-term financing pressure tied to those payments.

Roughly $22 billion remains available across its MSTR at-the-market programs, while a separate $1 billion authorization for common-stock repurchases remains unused.

The growing reserve gives Strategy more room to manage its preferred securities and debt obligations without having to raise fresh capital each time those payments come due.

STRC's final $5 could determine what comes next

With STRC now within about $5 of its $100 target, the next test is whether the preferred stock can close the gap without Strategy having to keep increasing its support. The firm has indicated that STRC’s return to par could take time.

During its second-quarter earnings call, management noted that the security took roughly 70 trading days to reach $100 after its 2025 launch. Applying a similar timeline to the current recovery would put STRC on course to return to par around Sept. 8.

The circumstances are different this time because Strategy is actively supporting the market through both dividend adjustments and direct repurchases.

A return to $100 could reduce the need for further purchases and improve STRC’s usefulness as a financing instrument. Issuing new shares near par allows Strategy to raise capital more efficiently than when the security trades at a persistent discount.

If STRC stalls below that level, Strategy still has $785.2 million of authorized buying capacity available to continue supporting the market.

Strategy has already demonstrated its willingness to intervene when STRC trades materially below its intended level. What remains unclear is how much intervention, if any, will be required to get the security the final few dollars back to $100.

The post Strategy has $785 million left to close STRC’s final $5 gap after selling $213 million in Bitcoin appeared first on CryptoSlate.

CryptoTicker.io

Holding Bitcoin as a Business Owner: Private or Business Assets?

Business owners in Austria do not have to allocate Bitcoin to business assets automatically. What matters is the purpose the cryptocurrency actually serves. If it is held purely as a personal investment, it can generally remain private property. Where there is a clear link to the business activity, much points towards business assets. The classification has direct consequences for taxation, bookkeeping and the offsetting of losses.

When Do Bitcoin Count as Business Assets?

Bitcoin are likely to be business assets where a company:

- receives them as payment for goods or services,

- uses them regularly for business payments,

- holds them as part of a crypto, mining or trading operation,

- deliberately deploys them as part of a corporate treasury strategy.

If a self-employed consultant buys Bitcoin purely as a private investment, by contrast, the coins do not become business assets simply because the purchase went through the business account. The decisive factor is the actual business function. The source of the payment or the label on a wallet are only indications.

Sole Traders and Limited Companies Are Treated Differently

In a sole proprietorship the owner and the private individual are legally the same person. For tax purposes, private and business assets still have to be kept apart. The position differs for a limited company (GmbH): Bitcoin bought by the company or received as a customer payment belong to the company. The shareholder may not simply move them to a private wallet. Private use of company assets can be treated as a hidden distribution and trigger additional tax.

What Tax Applies When Business Bitcoin Are Sold?

For sole traders, gains on Bitcoin held as business assets can in principle also fall under the special tax rate of 27.5 percent. That does not apply without limits. Where crypto trading or mining forms the core of the business activity, the gains may be taxed at the ordinary progressive income tax rate. In a limited company, profits are first subject to corporation tax. If they are later distributed to the shareholder, capital gains tax can apply on top.

Moving Bitcoin to a Private Wallet Can Be Taxable

Anyone who permanently moves business Bitcoin into private assets makes a withdrawal for tax purposes. This is generally valued at the current market price.

Example:

- Business acquisition cost: 15,000 euros

- Market value at withdrawal: 40,000 euros

- Possible business gain: 25,000 euros

A pure transfer between two business wallets, on the other hand, is generally not a taxable sale. The business allocation does have to remain documented.

Contributing Private Bitcoin to a Business

Private Bitcoin can also be contributed to a business. An increase in value that has already accrued privately is not automatically wiped out for tax purposes. As a rule, the existing acquisition costs are carried forward. If the current value sits below the original acquisition cost, the lower figure can be the relevant one instead. A contribution should therefore be documented with the date, the amount of Bitcoin, the wallet address, the acquisition cost and the market value.

A Clean Split Prevents Bitcoin Tax Problems

Business owners should avoid keeping private and business holdings in the same wallet. Separate wallets, exchange accounts and transaction histories are the sensible route.

What should be documented in particular:

- date of acquisition and purchase price,

- the purpose of the acquisition,

- business deposits and withdrawals,

- wallet transfers,

- contributions and withdrawals,

- fees and sale proceeds.

Conclusion: What Decides Whether Bitcoin Are Business Assets

Whether Bitcoin belong to private or business assets is not decided by the business account alone. What counts is their actual function. Anyone who receives Bitcoin as a customer payment or uses them directly in the business will normally hold them as business assets. A personal investment can remain private property. Particular care is needed with transfers between the company and the private individual, and with Bitcoin held by a limited company. An unclear or retrospectively altered allocation can create additional tax and documentation problems.

(As of August 11, 2026. This article is not investment advice. Prices and fee structures change; check the terms with the provider before you buy.)

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text. The feature image was generated with AI.

Selling Bitcoin at an ATM: the tax duties Austrian users need to know

Bitcoin ATMs are usually associated with a quick and simple crypto purchase. Some machines, however, work in both directions: you can send bitcoin from your wallet to the operator and receive banknotes in return. In tax terms, that transaction amounts to more than a withdrawal from your own digital assets.

Anyone who sells bitcoin for euros at a machine in Austria generally realises a taxable event. For bitcoin acquired after February 28, 2021, the gain can be taxed at 27.5 percent. The taxable figure is the difference between the sale proceeds and the tax acquisition costs of the coins sold, rather than the full cash amount handed over.

Whether the ATM operator already withholds capital gains tax depends on its tax status and on how the transaction is settled. Where no correct withholding takes place, you generally have to work out the gain yourself and report it in your Austrian income tax return. A cash payout makes a bitcoin sale neither anonymous nor tax free.

How selling Bitcoin at an ATM works

At a so called two-way machine you can buy bitcoin as well as sell it. The machine usually displays a receiving address or a QR code. You send the bitcoin you want to sell from your wallet to that address and receive cash once the required number of blockchain confirmations has been reached.

The Austrian financial market authority explicitly describes two-way machines as devices through which bitcoin can be sold from the customer wallet to the operator, with cash paid out in exchange.

In economic terms, two connected steps take place:

- You transfer bitcoin to the ATM operator.

- The operator pays you euros in cash.

For Austrian income tax purposes this is generally a sale of cryptocurrency for euros. It makes no difference whether the proceeds are transferred to a bank account or handed over immediately in banknotes.

Selling Bitcoin for cash is a taxable disposal

The Austrian Income Tax Act explicitly counts the disposal of cryptocurrencies for euros among income from realised capital gains. An exchange for recognised foreign currencies or for other goods and services can also constitute a taxable disposal.

When you sell at a bitcoin ATM, part of your bitcoin holdings leaves your assets and euros come in. That distinguishes the transaction from a simple transfer between two wallets you own yourself.

Transfer between your own wallets: generally not a sale

Transfer to a machine in exchange for cash: generally a taxable sale

The tax treatment does not change because no conventional exchange account is involved. What counts is the economic substance: bitcoin is disposed of in exchange for legal tender.

Only the gain is subject to tax

Tax is not levied on the entire amount paid out at the machine. As a rule, only the gain is taxed.

The simplified calculation is:

Sale proceeds

minus the acquisition costs of the bitcoin sold

minus any deductible transaction costs

equals the taxable gain

An example:

- bitcoin originally bought for 4,000 euros

- later sold at a machine for 7,000 euros

- taxable gain before further costs: 3,000 euros

- tax at 27.5 percent: 825 euros

The 4,000 euros originally invested are not taxed a second time. They represent the tax acquisition costs.

The Austrian finance ministry confirms that the disposal gain is calculated from the difference between the proceeds and the acquisition costs. Directly attributable incidental acquisition and transaction costs can reduce the taxable gain where the statutory conditions are met.

Which amount counts as the sale proceeds?

At a machine, the economic consideration can differ from the publicly quoted bitcoin market price. Operators frequently apply their own exchange rate and factor their margin or fee into the payout.

If you sell bitcoin with an exchange value of 1,000 euros and receive only 920 euros at the machine, the amount actually obtained is generally decisive for the gain calculation. Whether the difference is treated as a separately deductible fee or as part of the agreed sale price depends on how the operator settles the transaction.

The receipt should therefore show:

- how much bitcoin was sold,

- which euro rate was applied,

- which gross value formed the basis,

- which fee or margin was charged,

- which amount was actually paid out.

Without a detailed statement it may later be unclear which part of the difference stemmed from the exchange rate and which from a separate transaction fee.

Which Bitcoin purchase price applies?

If you bought bitcoin in several tranches at different prices, you cannot simply pick the purchase price of any transaction you like.

For units of the same cryptocurrency acquired one after another and held at the same crypto address or wallet, Austria generally requires the moving average price in euros. This valuation method applies to income from realised capital gains received after December 31, 2022.

An example:

- purchase of 0.05 BTC for 1,000 euros

- later purchase of 0.05 BTC for 2,000 euros

- total holding: 0.1 BTC

- total acquisition costs: 3,000 euros

- average acquisition costs: 30,000 euros per BTC

If you then sell 0.02 BTC at a machine, the calculated acquisition costs of that portion generally come to 600 euros. With several wallets, exchange accounts and a mix of legacy and new holdings, the calculation can become considerably more complex. The machine does not know that history automatically.

When does the 27.5 percent rate apply?

The current Austrian crypto tax regime generally applies to bitcoin acquired after February 28, 2021. Such coins are treated as new holdings.

Gains from selling them within private assets are generally subject to the special tax rate of 27.5 percent. The holding period does not change that. A bitcoin held for three, five or ten years does not become tax free on account of that holding period alone.

The special rate normally does not push up the progressive tax rate applied to your remaining income. It applies whether the tax is withheld directly as capital gains tax or assessed later through the income tax return.

A different treatment can apply above all where crypto trading goes beyond private asset management and qualifies as a commercial activity.

What applies to legacy Bitcoin holdings?

Bitcoin acquired on or before February 28, 2021 generally counts as a legacy holding. The new tax regime does not automatically apply to it. The earlier legal position has to be examined instead.

For bitcoin held privately and not invested in an interest bearing way, a sale could be tax free under the old rules, in particular where more than one year lay between acquisition and disposal.

An example:

- bitcoin bought privately in 2019

- no interest bearing investment

- sale at a machine in 2026

In a typical case the former one year speculation period may have expired long ago. The sale could therefore remain tax free. The precise assessment depends on how the coins were used at the time.

Particular care is needed where legacy holdings were later:

- lent out,

- used in lending products,

- invested in an interest bearing way,

- swapped for other tokens,

part of a business activity.

You also have to be able to prove that the coins sold really were those old bitcoin. Merely asserting that a holding is legacy stock is regularly not enough where the transaction history is missing.

Does the machine withhold capital gains tax automatically?

Since 2024, certain domestic debtors and crypto service providers have generally been obliged to withhold capital gains tax on relevant crypto income and pay it to the tax office. After a correct withholding, the income concerned is regularly final taxed within private assets.

At a bitcoin ATM you should nevertheless not assume that the tax has already been settled. Among the decisive points are:

- who operates the machine,

- whether the operator qualifies as a domestic withholding agent,

- whether the statutory conditions for the withholding are met,

- whether the operator holds the correct acquisition costs,

whether the receipt actually shows a tax deduction.

A machine receipt showing a general service fee is no evidence of capital gains tax paid. Withheld tax would have to be clearly identifiable as a tax deduction.

Where no capital gains tax was withheld, the tax liability does not disappear. You generally have to calculate the gain yourself and enter it in your income tax return. The finance ministry makes clear that capital income without a possible domestic tax deduction has to be declared in the assessment. The special tax rate can still apply.

Missing acquisition costs are the biggest practical risk

The operator essentially sees how much bitcoin you send and which euro amount you receive for it. It does not necessarily know:

- when the coins were originally bought,

- how high the purchase price was,

- whether they come from an earlier crypto to crypto swap,

- whether they are legacy or new holdings,

- whether the wallet contains several acquisition tranches,

- whether the coins were inherited or received as a gift,

whether a relocation value is decisive.

Without acquisition costs the gain cannot be determined correctly.

You should therefore not wait until the sale to reconstruct your history. Closed exchange accounts, missing CSV files and bank statements that are no longer available can cause serious problems years later.

The records to secure include:

- purchase statements from the original exchange,

- account statements showing payment of the purchase price,

- complete transaction histories,

- wallet addresses and transaction IDs,

- evidence of transfers between your own wallets,

- information on earlier crypto to crypto swaps,

- documents relating to inheritances or gifts,

documentation of your tax relocation to Austria.

Which fees apply when you sell at a Bitcoin ATM?

Several costs can arise on a sale:

- the machine fee charged by the operator,

- the margin built into the exchange rate,

- the bitcoin network fee,

- an additional processing or payout fee.

These fees should be looked at separately.

A machine or transaction fee directly connected with the sale can generally reduce the taxable disposal gain, provided you actually bear it and can document it in a comprehensible way. The finance ministry generally recognises directly attributable transaction fees when the gain is determined.

The bitcoin network fee can carry a tax component of its own. Where it is paid in bitcoin, coins are used that leave the investor assets. The Austrian income tax guidelines generally treat fees paid in cryptocurrency for a transfer to another address as an exchange for a transaction service.

A machine sale can therefore bring two realisations together:

- the sale of the bitcoin transferred to the operator for euros

- the use of further bitcoin to pay the network fee

In practice the second amount is often small, yet it belongs in a complete tax calculation.

A simplified worked example

An Austrian investor sells 0.02 BTC at a machine.

- average acquisition costs: 20,000 euros per BTC

- acquisition costs of the 0.02 BTC: 400 euros

- market value at the general exchange rate: 1,200 euros

- actual cash payout: 1,100 euros

- separately stated machine fee: already reflected in the payout

- additional network fee: 0.00005 BTC

For the sale itself the simplified result is:

Cash proceeds: 1,100 euros

Acquisition costs: 400 euros

Gain: 700 euros

Tax at 27.5 percent: 192.50 euros

You then also have to check whether the bitcoin used for the network fee produced a further small gain.

The example shows why the publicly quoted bitcoin price cannot simply be equated with the sale proceeds for tax purposes. What counts is the actual payout and the specific fee structure.

A cash payout does not mean anonymity

Some users associate bitcoin machines with a sale outside conventional financial accounts. For tax purposes the form of payment is irrelevant. Proceeds received in cash also belong in the tax calculation.

Operators of crypto services can also be subject to anti money laundering duties. These can include establishing the identity of the customer and making flows of funds traceable. The FMA points out that participants in the financial market have to collect customer data and make transactions traceable in order to prevent money laundering.

Depending on the operator, the amount and the risk classification, the machine may ask for:

- a mobile phone number,

- proof of identity,

- a scan of an identity document,

- facial recognition or video identification,

- further information on the source of funds.

Independently of that, the bitcoin transaction remains visible on the blockchain. Choosing a cash payout in order to hide a taxable disposal does nothing to remove the statutory duty to declare it.

Does the sale belong in your tax return?

Where Austrian capital gains tax was withheld correctly, a private disposal gain is generally final taxed and regularly does not have to be included in the income tax return again. A voluntary assessment can still make sense, for example for an overall loss offset or for the option to be taxed at the standard rate.

Where no capital gains tax was withheld, a taxable gain generally has to be declared in the income tax assessment.

- That can apply in particular where:

- the machine operator is not an Austrian withholding agent,

- the receipt shows no capital gains tax,

- the acquisition costs were unknown to the operator,

- the tax calculation of the operator does not match the actual result,

- you sell through a foreign operator.

An ordinary employee assessment is not sufficient in every case. Capital income you have to declare yourself can require a full income tax return.

Losses from a Bitcoin ATM sale

Where the payout falls below the tax acquisition costs, the sale can produce a loss.

An example:

- acquisition costs of the bitcoin sold: 1,500 euros

- cash payout after fees: 1,100 euros

- tax loss: 400 euros

Losses from cryptocurrencies can generally only be offset against certain positive income from private capital assets, and only under the statutory rules. Offsetting them against a salary or against any other income is not possible.

An automatic loss offset across several providers, or between cryptocurrencies and other types of capital assets, does not take place in every case. Any offset beyond that can require an income tax return and the corresponding evidence.

Keep the machine receipt permanently

Users should not treat the printout from the machine like an ordinary till receipt that is thrown away after a few days.

The receipt should be stored together with the following data:

- the date and exact time of the sale,

- the location and operator of the machine,

- the transaction ID on the bitcoin blockchain,

- the amount of bitcoin sent,

- the network fee,

- the exchange rate applied,

- the cash amount paid out,

- machine and service fees,

- any capital gains tax shown,

- the acquisition costs of the bitcoin sold,

- the calculation of the tax gain or loss.

Thermal paper can fade over time. A digital copy of the receipt is therefore advisable, together with an export of the wallet transaction and the underlying acquisition history.

VAT is not the main problem for a private user

Under the case law of the European Court of Justice, the exchange of bitcoin into legal tender and back is generally exempt from VAT. The Austrian finance ministry adopts that classification for the exchange of euros into bitcoin and back.

For a private seller the focus is therefore regularly on income tax on the realised price gain rather than on VAT.

The situation can look different where bitcoin is held as business assets or where sales are carried out in the course of a commercial activity. Additional accounting, record keeping and corporate questions then have to be examined alongside income tax.

Conclusion: a cash sale is an ordinary Bitcoin sale for tax purposes

Anyone who sells bitcoin for cash at an Austrian machine generally realises a sale for euros. For new bitcoin holdings, the difference between the payout and the acquisition costs is regularly taxed at 27.5 percent.

The key points are:

- The cash payout is a sale for euros in tax terms.

- The gain is taxed, not the entire amount paid out.

- Bitcoin acquired after February 28, 2021 is generally taxed at 27.5 percent.

- Legacy holdings can be sold tax free under the earlier rules.

- A machine operator does not necessarily withhold the correct capital gains tax.

- Without a withholding, you generally have to declare the gain yourself.

- Machine, trading and network fees have to be documented separately.

- The receipt alone does not replace evidence of the original acquisition costs.

The greatest tax risk therefore does not necessarily lie in the size of the sale. An incomplete history is the real problem. If you can prove neither the purchase price nor the acquisition date, you risk an incorrect gain calculation and difficulties in a later audit.

(As of August 10, 2026. This article is not investment advice. Prices and fee structures change; check the terms with the provider before you buy.)

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text. The feature image was generated with AI.

The crypto market is red again, and this time the trigger arrived in the middle of what was shaping up to be a decent session. Bitcoin traded above $65,000 this morning on reports that Iran might cut a deal with Oman to reopen the Strait of Hormuz. Hours later that optimism was gone. BTC now changes hands near $63,890, down 1.98% on the day, after Tehran signalled it has no intention of negotiating with the Trump administration at all before 2029.

Oil did the rest. WTI crude jumped roughly 5% back to $80 a barrel, and every risk asset on the board felt it.

Iran War News: What exactly did Iran say?

The comments came from Majid Shakeri, an adviser to Iranian Parliament Speaker Mohammad Bagher Ghalibaf. His position, circulated widely through Iranian outlets and then amplified across financial media, is that Tehran should stop pursuing any agreement with Washington and simply outlast the current US administration until its term ends in January 2029.

The framing he used matters for markets. He described the winning strategy as neither war nor a deal, but the deliberate management of a state in between the two, built on denial, ambiguity and patience. He also argued that publicly confirming negotiations with the United States would be a mistake.

Two caveats belong here, because they change how much weight this should carry. First, Shakeri is an adviser, not a head of state or a foreign ministry spokesman, so this is influential commentary rather than a formal declaration of policy. Second, Iran's official conditions for any settlement have not changed and remain maximalist, including compensation claims, the release of frozen assets, the lifting of sanctions and a US military withdrawal from the region.

But markets do not wait for formal confirmation. They price the direction of travel, and the direction of travel this morning went from "Hormuz might reopen" to "Hormuz stays shut for another two and a half years" inside a single session.

Why did the market reverse so fast?

Because the rally that preceded it was built on exactly the story that just got contradicted.

Bitcoin climbed above $65,000 earlier in the day partly on Iran-Oman deal speculation, with global equities near record levels and a softer dollar helping. That is a positioning trade, not a conviction trade. When the underlying premise flipped, the positions unwound immediately.

The oil move is the transmission mechanism that crypto traders sometimes underrate. A closed Strait of Hormuz keeps a permanent risk premium in crude. Higher crude feeds into headline inflation. Higher inflation expectations push out rate cut timing. And a market that has spent this year hoping for easier financial conditions treats delayed cuts as a direct hit to risk assets. Bitcoin sits at the far end of that chain, which is why a Middle East headline moves a decentralised asset that has nothing to do with the Middle East.

How far did the top 15 fall?

The damage was broad but shallow, which tells you this was a repricing rather than a panic.

| Asset | Price | 24h % | 7d % | YTD % | Market cap |

|---|---|---|---|---|---|

| Bitcoin ($BTC) | $63,890.76 | -1.98% | +0.20% | -28.00% | $1.28T |

| Ethereum ($ETH) | $1,873.86 | -2.55% | +0.40% | -37.55% | $225.98B |

| $BNB | $599.38 | -1.50% | +1.29% | -30.55% | $79.81B |

| $XRP | $1.02 | -2.17% | -5.62% | -45.66% | $63.80B |

| Solana ($SOL) | $75.90 | -1.69% | +3.17% | -40.12% | $44.18B |

| TRON ($TRX) | $0.3308 | +0.38% | +0.57% | +15.48% | $31.40B |

| Hyperliquid ($HYPE) | $54.82 | -0.10% | +0.60% | +126.56% | $13.85B |

| Dogecoin ($DOGE) | $0.06970 | -1.32% | -0.82% | -44.97% | $10.83B |

| UNUS SED LEO | $9.65 | -0.77% | -0.99% | +0.90% | $8.88B |

| Zcash ($ZEC) | $496.18 | -3.80% | +1.23% | -5.48% | $8.34B |

| Monero ($XMR) | $390.88 | -0.97% | +7.80% | -6.84% | $7.34B |

| Cardano ($ADA) | $0.1955 | -1.27% | +1.92% | -45.10% | $7.14B |

| Chainlink ($LINK) | $8.25 | -0.87% | +0.19% | -34.38% | $6.17B |

Three things stand out.

- TRON was the only asset in the top 13 to hold a gain on the day, and it remains the only large cap besides Hyperliquid that is positive for the year, up 15.48%.

- Zcash took the heaviest 24-hour hit at 3.80%, but Monero is the strongest performer of the entire group over seven days, up 7.80%. Privacy assets catching a bid during a sanctions-driven geopolitical escalation is not a coincidence, and it is a pattern worth watching if the confrontation extends.

- XRP remains the standout laggard. It is down 5.62% on the week while Solana gained 3.17% and Bitcoin held marginally positive, and its year-to-date loss has now widened to 45.66%.

Why does the Strait of Hormuz matter for Bitcoin?

Roughly a fifth of global oil supply normally moves through that waterway. With it closed, the pricing of energy stops being a supply and demand question and becomes a geopolitical one, and every barrel carries a war premium.

For crypto specifically, the chain runs through inflation and central bank policy. US CPI data lands this week, and it is the single most important scheduled event on the calendar. A crude price that just jumped 5% does not show up in this week's print, but it absolutely shapes how traders read the next few. If the market concludes that energy costs will keep headline inflation sticky into the autumn, the case for near-term rate cuts weakens, and the bid under risk assets weakens with it.

There is also a direct crypto angle to this conflict that gets very little coverage. Washington widened its Iran crypto crackdown earlier this month with sanctions targeting two exchanges, part of an effort to close off digital asset channels being used to move value around the blockade. As the conventional Iranian economy seizes up, that enforcement pressure is likely to increase rather than ease.

What about Iran's currency collapse?

The rial has been in freefall, and it is a genuine part of this story, though the specific numbers circulating on social media should be treated carefully.

Iran operates multiple exchange rates simultaneously, so the official rate, the remittance rate and the open market rate can differ substantially, which is why screenshots claiming a precise all-time low often disagree with each other. What is not in dispute is the trend. The rial traded near 800,000 to the dollar before the June 2025 conflict with Israel and has since collapsed past 1.6 million, with open market quotes in recent sessions running well above that.

For a crypto audience the relevant point is behavioural. When a national currency stops functioning as a store of value, domestic demand for dollars, gold and crypto rises regardless of what the government permits. That is precisely why sanctions enforcement has moved toward exchanges.

Is this only about Iran?

No, and treating it that way would be a mistake.

The CLARITY Act failed to reach a Senate floor vote before the August recess and has been pushed to the autumn, removing the regulatory catalyst a lot of positioning was built around. Strategy, the largest corporate holder of Bitcoin, disclosed the sale of 1,690 BTC while raising $653 million through share issuance, an unusual direction of travel for a company whose entire thesis has been accumulation. And Bitcoin's implied volatility recently hit its lowest level since 2025, with options demand collapsing even as downside protection stayed expensive.

That last detail is the most instructive. A market with compressed volatility and expensive puts is a market where nobody expects a big move but everybody quietly wants insurance. Those conditions make sharp, headline-driven reversals like today's more likely, not less.

What should traders watch this week?

Start with US CPI, which will do more for direction than any Middle East headline unless there is actual military escalation. Then watch whether Bitcoin can reclaim $65,000, the level it lost today and the one it has repeatedly failed to hold since mid-July. Below that, the $61,800 area has acted as support through the summer.

On the geopolitical side, the thing to monitor is not rhetoric but the Strait itself. Any credible movement on an Oman-brokered reopening would reverse today's move quickly, because the market has already demonstrated this morning that it is willing to buy that story. Any confirmation from Tehran at an official level that talks are formally dead would push in the opposite direction.

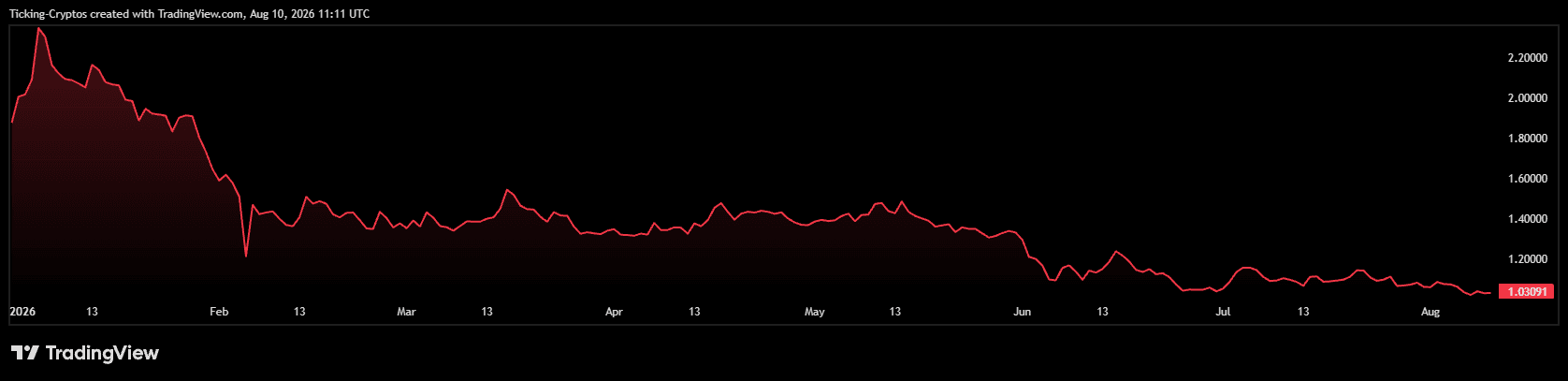

$XRP has just done something it has not done since late 2024. The token closed the weekly candle at $1.09, its lowest weekly close in almost two years, and it has kept sliding since. At the time of writing XRP trades around $1.03, down 0.42% on the day and 3.47% across the past seven days.

What makes the print stand out is not the number itself. It is the company XRP is keeping. Almost every other major asset finished the week in the green.

How bad is the XRP weekly close?

XRP is now the worst year-to-date performer in the entire top 10 by market capitalisation, down 43.94% since January. Its market cap has shrunk to $64.5 billion, keeping it in sixth place but with a visibly thinner cushion above Solana than it had at the start of the year.

The weekly close at $1.09 matters more than the intraday wick. Weekly closes are what swing traders and longer-term allocators actually mark their charts against, and losing a level that has held for close to two years removes a psychological floor that had been treated as reliable.

Why is XRP the only major coin in the red this week?

Here is how the top of the market finished the same seven-day stretch.

| Asset | Price | 7d % | YTD % | Market cap |

|---|---|---|---|---|

| Bitcoin ($BTC) | $64,963.51 | +3.63% | -25.77% | $1.30T |

| Ethereum ($ETH) | $1,916.10 | +3.90% | -35.42% | $231.23B |

| $BNB | $605.92 | +3.36% | -29.81% | $80.68B |

| $XRP | $1.03 | -3.47% | -43.94% | $64.50B |

| Solana ($SOL) | $76.77 | +5.87% | -38.32% | $44.69B |

| TRON ($TRX) | $0.3314 | +1.15% | +16.58% | $31.45B |

| Hyperliquid ($HYPE) | $54.47 | +3.41% | +114.21% | $13.76B |

| Dogecoin ($DOGE) | $0.06990 | +0.70% | -40.40% | $10.86B |

Every single one of those assets posted a positive week except XRP. Solana added almost 6%, Ethereum and Bitcoin both added close to 4%, and even Dogecoin managed a small gain. XRP went the other way by 3.47%.

That is the part worth paying attention to. When an asset falls during a week in which its entire peer group rises, the explanation is usually specific to that asset rather than to the market.

Is a trust problem weighing on XRP?

There is a credibility question hanging over XRP that the other majors do not carry in the same form.

XRP's price has spent years reacting to legal and legislative headlines rather than to network usage. The pattern is well established: a favourable court ruling or a regulatory milestone produces a violent spike, the spike fades within weeks, and the token settles back into a range. The current stall of the CLARITY Act in the US Senate, now reportedly shelved until at least September, has removed the one near-term catalyst that a large part of the holder base was positioned for.

The trading data reinforces the concern. Recent activity has been overwhelmingly derivatives-led, with daily futures volume running at roughly 10 times spot volume. That ratio describes speculation and leverage rather than accumulation. Rallies built on futures positioning tend to unwind quickly because there is no underlying spot demand to absorb the selling.

On-chain sentiment data tells a similar story. Santiment has reported XRP holders sitting on their deepest average unrealised losses on record, a condition that historically accompanies capitulation phases rather than early recoveries.

None of this means the project is finished. Ripple as a company remains well capitalised and continues to build out payments and stablecoin infrastructure. But there is a real gap between what Ripple the business is doing and what XRP the token has priced in, and that gap is what makes some allocators reluctant to hold it through drawdowns.

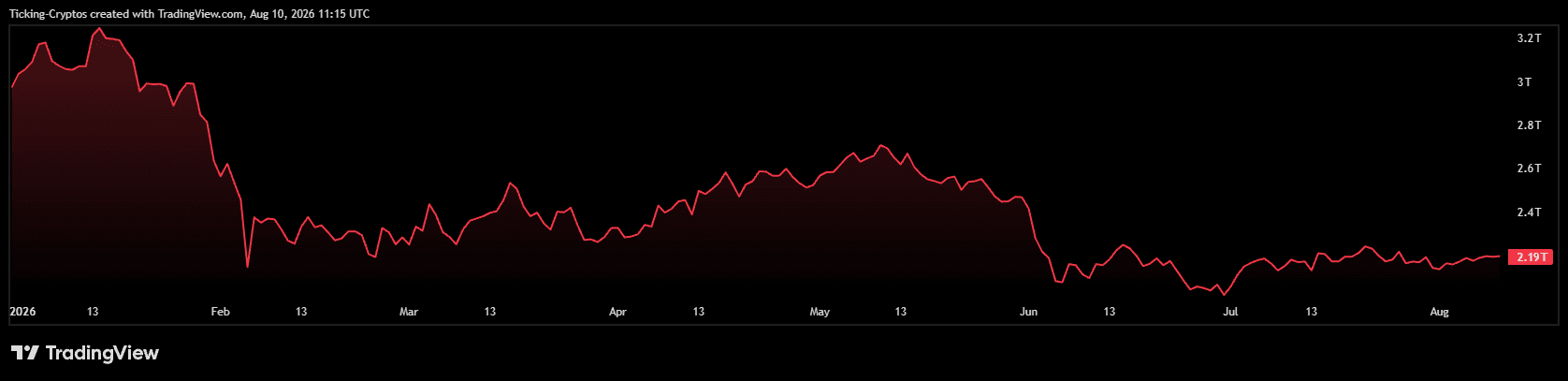

Is the whole crypto market simply down?

This is the point that gets lost in most XRP coverage, and it is arguably the most important one.

The entire crypto market is in a deep drawdown. Bitcoin peaked at $126,198 in October 2025 and now trades near $65,000, roughly 49% below that high. Total crypto market capitalisation has fallen from a peak above $4.2 trillion to around $2.3 trillion. Ethereum is down more than 35% year to date. Solana is down more than 38%. Dogecoin is down more than 40%.

In that context, XRP being down 43.94% is not an outlier. It is at the harsher end of a spectrum that almost every asset is sitting on. Only TRON and Hyperliquid are positive on the year, and both have idiosyncratic drivers behind them.

The green week across the top 10 is also worth framing correctly. A 3% to 6% bounce after a 50% market-wide decline is a relief move inside a downtrend, not a reversal. Bitcoin has repeatedly failed to clear resistance around $65,500 since mid-July, and August has historically been one of its weaker months.

So the honest read is layered. XRP has a genuine narrative problem, and that explains why it lagged this specific week. But the reason it is at $1.03 instead of $3 has far more to do with the fact that the entire asset class has spent a year repricing lower.

What levels matter for XRP now?

The $1.00 mark is the level everything hinges on. On-chain cost-basis data shows more than 830 million XRP concentrated between $1.00 and $1.06, the densest cluster of coins anywhere near the current price. That is a real support band because those holders are close to break-even and have an incentive to defend it.

Below $1.00, the picture thins out badly. Cost-basis data shows very little accumulated supply between $1.00 and $0.80, which means a clean break of the dollar could see price move quickly through empty territory before finding buyers.

On the other side of the ledger, XRP's weekly RSI dropped below 30 in June, only the second oversold reading on the weekly chart in 12 years. The first was the 2022 bear market bottom near $0.29. That signal eventually preceded a 1,100% move, but with a critical caveat: the rally did not begin until November 2024, nearly two and a half years after the signal fired. Oversold does not mean imminent.

What should traders watch next?

Three things will decide the next move. First, whether the $1.00 to $1.06 support band holds on a weekly closing basis. Second, whether the CLARITY Act gets a Senate floor date in September, which is the single largest binary catalyst on XRP's calendar. Third, whether Bitcoin can reclaim $65,500 and then $68,500, because in a market this correlated, no altcoin recovery gets far without BTC leading.

Until at least two of those three resolve positively, the base case for XRP is continued consolidation in the low dollar range, with the risk skewed toward a test of the psychological $1.00 level.

Bitcoin lending in Austria: when the ongoing income is already taxed

Anyone who lends Bitcoin through a crypto exchange, a lending platform or a DeFi protocol usually receives a recurring payment in return. Depending on the product, providers call this interest, rewards, yield or earn income. For Austrian tax purposes, the name of the offer carries no weight.

Where Bitcoin is made available to another market participant for consideration, the payments received generally count as ongoing income from cryptocurrencies. Tax normally falls due as soon as the investor can dispose of the rewards. Selling the Bitcoin received for euros is not a requirement.

That creates a particular risk for investors. The tax is calculated on the euro value at the moment of receipt. If the Bitcoin price falls afterwards, the tax bill can exceed the value the coins still hold later on.

What is Bitcoin lending?

In Bitcoin lending, the investor hands over coins for a limited period to a platform, a company, a borrower or a decentralised protocol. A payment is made in return.

Depending on the product, the Bitcoin made available may be used to:

- fund loans to other users,

- supply trading positions with liquidity,

- provide Bitcoin to institutional market participants,

- fund a centrally managed credit pool,

- provide liquidity inside a DeFi protocol.

The payment can be made in Bitcoin, stablecoins, other tokens or fiat currency. It is often credited to the platform account daily, weekly or monthly.

The Austrian Income Tax Act explicitly captures payments for making cryptocurrencies available as ongoing income from cryptocurrencies. The finance ministry names interest from lending cryptocurrencies as well as consideration for providing crypto assets to liquidity and credit pools.

Bitcoin lending is generally taxed at the point of receipt

The decisive moment is not the later sale of the lending rewards but their receipt. All ongoing crypto income has to be valued at the moment it reaches the investor.

An asset is generally treated as received once the recipient can dispose of it in legal and economic terms. On a lending platform, that may be the point at which the payment is credited to the user account and the investor can withdraw it, swap it, transfer it or lend it out again.

A payout to a bank account is not necessary. A credit in Bitcoin or another crypto asset can already amount to taxable income.

Typical moments of receipt include:

- the daily credit to an accessible platform account,

- the monthly payout to a wallet,

- the allocation of freely transferable reward tokens,

- the automatic credit with immediate reinvestment,

- the payout at the end of a fixed lending term.

Whether a payment that is merely displayed as a figure, without being available yet, has already been received depends on the contractual terms. Where the investor can neither dispose of the coins nor demand their payout, receipt for tax purposes may occur only later.

A sale for euros is not required for the first tax charge

A common misconception holds that crypto gains only become taxable once money lands in a bank account. That does not apply to lending.

Ongoing income is taxed on its value at the moment of receipt. As a rule it makes no difference whether the investor:

- sells the Bitcoin received for euros straight away,

- leaves it sitting on the platform,

- transfers it to a hardware wallet,

- lends it out again automatically,

- swaps it for another cryptocurrency.

The Austrian finance ministry states explicitly that for ongoing crypto income the value of the cryptocurrencies or other payments received at the moment of receipt forms the taxable base.

How the taxable Bitcoin lending income is calculated

Where lending interest is paid in Bitcoin, the amount received has to be valued in euros at the moment of receipt. The reference is generally an available price from a crypto exchange. If no exchange price is available, the price quoted by a cryptocurrency dealer can be used.

This euro value serves two purposes:

- It forms the immediately taxable ongoing income.

- It becomes the tax acquisition cost of the coins received.

The Austrian Cryptocurrency Ordinance prescribes this valuation explicitly. A valuation carried out as part of a capital gains tax deduction is generally binding for the assessment as well.

Example: lending income paid in Bitcoin

An investor lends Bitcoin through a platform. In June the payment amounts to 0.0005 BTC. At the time of the credit the Bitcoin price stands at 60,000 euros.

The calculation runs as follows:

Payment received: 0.0005 BTC

Bitcoin price at receipt: 60,000 euros

Taxable income: 30 euros

Tax at 27.5 percent: 8.25 euros

Those 30 euros also count as the acquisition cost of the 0.0005 BTC received.

The investor therefore has to account for 8.25 euros of tax even though no euros were received and no coins were sold.

A second calculation can follow when the coins are sold

Taxation at the moment of receipt settles the ongoing lending income only. If the value of the Bitcoin received changes afterwards, a further gain or loss arises on the later sale.

Continuing the example:

- value of the Bitcoin received at receipt: 30 euros

- later disposal: 45 euros

- taxable disposal gain: 15 euros

- additional tax at 27.5 percent: 4.13 euros

The 30 euros are not taxed a second time. They form the acquisition cost. What is taxed on the sale is generally only the increase in value of 15 euros that arose afterwards.

If the value instead drops from 30 to 20 euros, the later disposal generally produces a loss of 10 euros. That loss can be set against certain other investment income within the statutory loss offset rules.

Falling prices can create a liquidity problem

Immediate taxation on the value at receipt can turn awkward when the Bitcoin price drops sharply after the credit.

An example:

- lending rewards at receipt: 10,000 euros

- tax at 27.5 percent: 2,750 euros

- value of the rewards when the tax falls due: only 5,000 euros

The original tax charge does not shrink automatically because the Bitcoin price fell later. The loss in value is generally recognised only once it is realised for tax purposes.

If the investor later sells the coins for 5,000 euros, that produces a loss of 5,000 euros against acquisition costs of 10,000 euros. Whether the loss can be used in full depends on whether suitable positive investment income is available in the same period for an offset.

Investors should therefore not assume that lending income is fully available for reinvestment. Part of the value may be needed to fund the tax that follows.

The special tax rate of 27.5 percent generally applies to lending

Ongoing income from cryptocurrencies is subject in Austria to the special tax rate of 27.5 percent. Crypto income therefore does not usually push up the progressive rate applied to the rest of an investor's income.

That typically holds for publicly offered lending products from exchanges and crypto service providers, provided the activity stays within private assets and does not go beyond straightforward asset management.

The 27.5 percent rate generally covers both:

- the ongoing lending payments,

- and later realised increases in value of the coins received.

An exception can apply to private cryptocurrency loans. Where the underlying agreement was not publicly offered in legal and factual terms, the income can fall under the progressive income tax tariff. Depending on total income, that rate can be lower or considerably higher than 27.5 percent.

The label «staking» offers no shelter from the lending tax

Many platforms market interest-bearing crypto products as staking even though no coins are technically deployed to validate a blockchain. In practice the assets are often made available to the platform or to other market participants.

Genuine, classic staking is treated differently in Austria. Where new cryptocurrencies are acquired by participating in transaction processing or block validation, no tax generally arises at the moment of receipt. The coins received are instead recorded with acquisition costs of zero, so the entire sale proceeds can become taxable on a later disposal.

This exception applies only to actual staking. The finance ministry warns explicitly that products merely described as staking can amount to lending for tax purposes. Where the arrangement is economically a supply of cryptocurrencies for consideration, the payment is taxed on receipt.

What matters is therefore the substance rather than the product name, and in particular:

- Who can dispose of the Bitcoin during the term?

- Are the coins deployed for blockchain validation?

- Does the platform obtain the economic use of the assets?

- Is there a claim to repayment in Bitcoin of the same type and amount?

- Is a fixed or variable return promised?

- Does the investor carry a credit or counterparty risk?

An offer labelled Bitcoin staking warrants particularly close inspection, because Bitcoin itself uses no classic proof-of-stake mechanism.

DeFi and liquidity pool income can also count as lending