Cryptocurrency Posts

Crypto Briefing

AI integration in finance is reshaping enterprise systems, enhancing efficiency and transforming user interactions globally.

The post Rob Goldstein: Technology is reshaping financial services, AI’s unpredictability challenges accountability, and asset management relies on information processing | Odd Lots appeared first on Crypto Briefing.

Ripple's expansion in Dubai underscores the Middle East's growing influence in the blockchain sector, potentially reshaping global finance dynamics.

The post Ripple expands headquarters in Dubai’s financial hub as regional demand accelerates appeared first on Crypto Briefing.

OKX's protocol could revolutionize AI-driven commerce by enabling autonomous transactions, potentially reducing human intervention in business operations.

The post OKX publishes open protocol enabling AI agents to quote, escrow and settle autonomously appeared first on Crypto Briefing.

The ongoing blockade heightens geopolitical tensions, potentially driving up oil prices and increasing market volatility amid diplomatic uncertainty.

The post Trump rejects Iran proposal, keeps naval blockade amid nuclear deal stalemate appeared first on Crypto Briefing.

The incident underscores vulnerabilities in US air defenses, potentially prompting more aggressive military strategies and policy shifts.

The post Iranian jet bombs US base in Kuwait, challenges air defense systems appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Strike CEO Jack Mallers Announces Lending Proof-of-Reserves, Volatility-Proof Loans, and Backs Tether Merger Plan

Strike CEO Jack Mallers announced a series of product updates and strategic moves Wednesday, including the launch of lending proof-of-reserves, a new “volatility-proof” bitcoin-backed loan structure built with Tether, and a $2.1 billion credit facility.

He also said he supports a proposal by Tether Investments to merge Strike with Twenty-One Capital and bitcoin miner Elektron Energy.

Mallers said Strike’s bitcoin-backed loan and line-of-credit business has grown since launch, with users drawn to the ability to borrow against bitcoin rather than sell it.

He described bitcoin as a savings account for many customers and said Strike cut its rate tiers across the board. Pricing now ranges from approximately 10.5% APR for loans under $250,000 to approximately 7.49% APR for loans above $5 million.

Strike announced the first iteration of its lending proof-of-reserves, which gives borrowers the ability to verify that their collateral is present and segregated in a distinct on-chain address.

“We want you to trust us and know that we are who we say we are,” Mallers said. The disclosure mechanism was developed in partnership with Tether, which Mallers credited with helping Strike build the transparency infrastructure.

The two companies also jointly developed what Mallers called “volatility-proof” bitcoin-backed loans, a structure that removes the risk of forced liquidation when bitcoin prices fall or broader markets drop.

Mallers said the segregated collateral product is available now through Strike’s private client desk, and the volatility-proof loan feature is available to customers as part of the bitcoin-backed lending suite.

Mallers announced that Strike has secured a $2.1 billion credit facility, which he said gives the company capacity to meet demand at any order size within its lending business.

Merger proposal

Earlier Wednesday, Tether Investments published a proposal to merge Twenty-One Capital with Strike and Elektron Energy, a large-scale bitcoin mining operator that manages approximately 50 EH/s, or roughly 5% of the current Bitcoin network hashrate.

Tether said the combined entity would integrate bitcoin treasury holdings, mining, financial services, lending, and capital markets under a single listed platform.

Mallers said he backs the plan. “Simply put, I think it’s a great idea,” he said, adding that building a Bitcoin company — not a narrow payments app — was his founding goal. Elektron founder Raphael Zagury has been proposed as President of the combined entity under the plan.

The bitcoin company quadrant and Maller’s vision

Mallers used a quadrant framework onstage to argue that the Bitcoin industry has a gap at the intersection of high conviction and high operating income.

He placed crypto exchanges in the high-income, low-conviction corner, saying they run profitable businesses but list many coins and build products across asset classes. He placed bitcoin treasury companies in the high-conviction, low-income corner, describing them as deeply committed to bitcoin but limited in operating business scope.

He cited Coinbase as an exchange that could carry more bitcoin on its balance sheet, and praised MicroStrategy executive chairman Michael Saylor while drawing a distinction between a treasury strategy and a product strategy. “I love him and his company,” Mallers said of Saylor, “but I want to build bitcoin products.”

His answer to the gap was a four-pillar model: a financial services arm covering brokerage, custody, lending, payments, treasury, and prime services; bitcoin infrastructure spanning energy, power generation, mining, hardware, and hosting; a capital markets operation built around loan-book securitization, mining revenue securitization, bitcoin-backed debt, and structured products; and a mergers-and-acquisitions function targeting profitable bitcoin businesses across software, custody, payments, energy, and distribution.

The stated goal of the M&A arm, as presented on his slide, is to give “every dollar of operating income one job: buy more Bitcoin.”

Mallers closed by saying a platform of that scope could “change the world with its products” and cited a phrase he has used throughout his career: “Fix the money, fix the world.”

This post Strike CEO Jack Mallers Announces Lending Proof-of-Reserves, Volatility-Proof Loans, and Backs Tether Merger Plan first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Strategy and Blockstream CEOs Paint Vision of Bitcoin’s Financial Future

Strategy CEO Phong Le and Blockstream CEO Adam Back appeared Wednesday on a panel moderated by Natalie Brunell, covering Bitcoin treasury strategy, tokenization, digital credit, and the enduring mystery of Satoshi Nakamoto.

The conversation drew a picture of a financial system in transition, with Bitcoin at its center.

Le opened with a striking observation about Strategy’s Bitcoin holdings. The company now holds 818,334, putting it second behind only one entity.

“There is only one individual entity with more Bitcoin than Strategy,” Le said. “That’s Satoshi.”

The firm is on pace to reach 1 million BTC in the next couple of months, a milestone that would cement its place in financial history.

Digital credit in the bitcoin space

Much of the discussion centered on Stretch, or STRC, Strategy’s perpetual preferred stock that pays an 11.5% annual dividend with proceeds used to purchase Bitcoin.

Le was direct about why the product matters. “This product does good,” he said, contrasting it with industries like tobacco and processed food.

Investors use STRC as a place to park short-term money, and it has served as a lower barrier for people seeking BTC exposure. Layer 2 products and DeFi protocols are now being built on top of it, Le said, describing STRC as “the most important credit product of all time” and a cornerstone for bringing BTC and DeFi together.

Back addressed the intersection of cypherpunk ideology and institutional finance, a tension the Bitcoin community has long wrestled with.

He said BTC’s acceptance by sovereign wealth funds and private funds is “a sign of success,” not a compromise. Cypherpunks, he explained, believed in capital formation and free markets, not just cryptographic privacy.

Back said treasury companies exist to grow Bitcoin per share, and when they do, individual holders benefit too.

Le reinforced the point, saying he learned much from Back when they first met. “Cypherpunks are gifted minds who understand the markets very well,” Le said, framing the movement as one that has always operated at the intersection of technology and capital.

On tokenization, both men saw it as the next structural shift. Le described it as “the digitalization of markets,” with blockchain providing the transparency layer.

He pointed to tap-to-pay as an analogy. “Why can’t you do that to a stock, peer to peer?” he asked. Back added that tokenization enables 24/7 trading, use of assets as collateral, and unlocks value in assets that are hard to discover or trade, like private notes and contracts.

When asked if major banks would compete in bitcoin digital credit, Le said he expected them to. He compared it to Amazon reshaping retail and forcing Walmart to respond.

Then he added: “I’d love to see Morgan Stanley on that list” regarding massive bitcoin companies.

The panel closed on a lighter note. Brunell asked Back about a New York Times investigation published earlier this month that named him as Bitcoin creator Satoshi Nakamoto.

Back, who denied the claim when the story broke, did not address it directly. “We are in a very good place regarding people adopting the technology,” he said.

This post Strategy and Blockstream CEOs Paint Vision of Bitcoin’s Financial Future first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Morgan Stanley Executive on Bitcoin: ‘We Are Still So Early on This Journey’

Morgan Stanley launched its bitcoin exchange-traded product, the Morgan Stanley Bitcoin Trust (MSBT), into a market it believes is still in its infancy.

At a panel on Wednesday moderated by Tyler Evans, Amy Oldenburg, the bank’s head of digital assets, spent the better part of an hour making a case for bitcoin that few clients have heard in full, and said that gap is the industry’s most urgent problem.

“We have to start with bitcoin,” Oldenburg told the audience, citing the asset’s roughly 1.5 trillion dollar market cap and its distance from the rest of the crypto landscape.

She was careful to draw a line between bitcoin and crypto as a broad category, a distinction she said most retail and institutional clients still do not make with confidence. The firm wants to see that distinction anchored in fundamental research, not just narrative.

Oldenburg: Bitcoin has an education problem

The education problem, she said, runs deep. Many investors still associate bitcoin with its early history of use by bad actors, and struggle to see past that frame when weighing an allocation.

Oldenburg said that when clients ask about yield or structured exposure, her team tries to be direct: “you can present it as a yield, but the underlying asset is bitcoin.” That clarity, she said, is still missing from most conversations in the market, and there is “so much more work to do.”

MSBT pulled in more than $100 million in its first week of trading, a strong early signal for a product the bank describes as designed for the full spectrum of its client base rather than a narrow segment.

But Oldenburg was quick to put that number in context. All of the initial flows came through self-directed accounts, because the fund had not yet been made available on the advisory platform.

She noted that the bank has announced a 2–4% crypto allocation recommendation, and that even with that guidance in place, take-up through advisors has been slow. The product, she reminded the audience, has been on the market for less than a year.

To bridge that gap, Morgan Stanley is working from the inside out. Oldenburg said the firm is rolling out internal training so that financial advisors can speak to clients on bitcoin with confidence, and that her team spends “hour after hour after hour” on the phone walking clients through models and allocation frameworks.

She said the bank designs products for clients with different needs and wants its platform to cover each of those needs, including clients who want a direct ETP wrapper, and that spot crypto trading is coming for those on the wealth management side.

On custodians, Oldenburg acknowledged the complexity of the decision. The market has no shortage of providers, and choosing among them was not straightforward, which led the firm to work with more than one. Morgan Stanley ultimately tapped Coinbase and BNY Mellon as custodians for MSBT.

When the conversation turned to high-beta bitcoin plays, Oldenburg called Strategy, the Michael Saylor-led company formerly known as MicroStrategy, “a good friend of Morgan Stanley,” and said the bank has worked alongside it through its evolution.

She said most of the exposure in that vehicle so far is coming from retail and that “digital credit” as a category will take time to develop.

Morgan Stanley buying bitcoin is “not out of the question”

On the question of banks holding bitcoin on their balance sheets, Oldenburg said it is “not out of the question” if regulatory progress continues, but was measured in framing it.

The U.S. needs greater alignment among its financial regulators, she said, and for a global firm like Morgan Stanley, the picture is more complex still — each jurisdiction comes with its own framework.

She closed where she began: on the need for research with reach. The market has commentators and personalities that investors trust and follow, she said, and the work ahead is to bring that kind of accessible, grounded analysis into the mainstream.

“We are still so early on this journey,” she said. “So little allocation. It’s still really early.”

This post Morgan Stanley Executive on Bitcoin: ‘We Are Still So Early on This Journey’ first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin, WikiLeaks, and a Film the Streamers Wouldn’t Touch: Jack Dorsey and Eugene Jarecki Make Their Case

Filmmaker Eugene Jarecki and tech entrepreneur Jack Dorsey took the stage Wednesday to discuss The Six Billion Dollar Man, Jarecki’s documentary on Julian Assange, and the role the bitcoin community may play in getting it to the public — a conversation that stretched from censorship and surveillance to Satoshi Nakamoto and the original principles of the internet.

Dorsey joined the panel virtually. The setting itself carried weight: Jarecki told the crowd that the casino sitting close to where he stood had ties to the private security firm that spied on Assange while he lived inside London’s Ecuadorian Embassy — a revelation the documentary places at the center of its surveillance narrative.

Dorsey: Bitcoin embodies a gatekeeper-free, open network

Jarecki said he went to Dorsey first for money. He needed help distributing a film that, despite premiering at Cannes and earning recognition on the festival circuit, found no takers among major streaming platforms. Dorsey shifted the conversation.

Rather than write a check, he told Jarecki that the bitcoin community represented something larger than a funding source — a constituency built around the same principles Assange had fought to defend.

“Bitcoin is an open protocol for money transmission,” Dorsey said. “It routes around the gatekeepers — Visa, Mastercard, the banks.”

He described the community as one that views Assange as a hero, someone who stood for the idea that information should remain free and open, values he traced back to the founding culture of the internet itself.

Dorsey pointed to 2011 as a proof of concept. After financial institutions cut off WikiLeaks from donation channels under pressure from the U.S. government, bitcoin stepped in as the only payment rail that could not be blocked.

He called WikiLeaks adopting bitcoin out of necessity one of the most significant moments in the protocol’s early history — not because it was planned, but because it revealed an immediate, real-world use case under conditions of state pressure.

He then drew a line between Assange and Satoshi Nakamoto, the pseudonymous creator of bitcoin. Dorsey said what matters most about bitcoin is that its founder walked away. He called that exit a selfless act — one that made the network founderless, and therefore resistant to the kind of pressure that governments and institutions can apply when a single person stands at the center of a project.

He placed Assange and Edward Snowden in the same category: people who trusted the technology they used, put their lives at risk for principles larger than themselves, and paid for it.

Jarecki said making the film carried its own risks. While shooting in Russia, he said his crew felt they were being followed and monitored — a layer of pressure that shaped the production from the inside. He described the mutual regard between Assange and Snowden, two figures who understood each other’s positions with precision, as one of the documentary’s most striking undercurrents.

A pay-per-view watch party in less than 60 days

The film’s distribution model is the most unusual element of the project. Dorsey proposed a global private pay-per-view watch party as an alternative to the traditional release pipeline. Ticket buyers at thesixbilliondollarman.com receive a credit line on the film itself, turning the audience into participants in the project rather than passive consumers.

Jarecki framed it as a test of whether a community organized around open financial infrastructure could do what media gatekeepers would not — get a film about press freedom in front of the people who need to see it.

Dorsey said the website and the viewing model offer a way to crowdfund and bring the community together around a shared cause.

At the panel, Jarecki showed never-before-seen clips from the documentary — behind-the-scenes footage that gave the audience a direct look at material that has not circulated publicly.

Jarecki and Dorsey are betting that the bitcoin community, which absorbed that argument in 2011 when it mattered most, will carry the film where the streaming industry declined to go.

This post Bitcoin, WikiLeaks, and a Film the Streamers Wouldn’t Touch: Jack Dorsey and Eugene Jarecki Make Their Case first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Eric Trump, John Koudounis Call Bitcoin a Global Reserve Asset, Float $1M Price Target

At Bitcoin 2026 in Las Vegas, Eric Trump and Calamos Investments CEO John Koudounis sat down with Bloomberg senior ETF analyst Eric Balchunas for a panel that covered bitcoin’s maturation from speculative instrument to global reserve contender.

The conversation ranged across institutional adoption, government debanking, currency debasement, and the challenge of winning over ordinary investors who still view bitcoin as too risky, too complex, or both.

It was a panel that reflected how much the room has changed — a mix of long-time bitcoin believers and fresh institutional money that, a decade ago, would have dismissed this gathering entirely.

Trump: Bitcoin is a sticky, limited supply asset

Trump opened on a structural theme, arguing that bitcoin has become “sticky.” The U.S. government now holds approximately 300,000 bitcoin and will not sell, he said, a claim consistent with the creation of a U.S. strategic bitcoin reserve.

Corporate treasury buyers like Strategy and Metaplanet, which surpassed 40,000 bitcoin in holdings by the end of the first quarter of 2026, are doing the same. The world’s largest financial platforms — Trump named Charles Schwab and Morgan Stanley — have also moved in.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) April 29, 2026Eric Trump just dropped a bombshell at The Bitcoin Conference:

"The US government holds 300,000 BTC and will not sell it."

"The middle east is using energy from cities that they don't need to…mine bitcoin."

"The suppression of bitcoin is unbelievable."pic.twitter.com/LdBU50faIs

American Bitcoin, the company Trump co-founded, is mining bitcoin and holding every coin rather than selling.

“We are compressing bitcoin,” Trump said. “There is a limited supply.”

The argument, in essence, is that the natural sellers are leaving the market while a new class of permanent holders takes their place.

Koudounis put the bitcoin supply compression argument in the context of a broader capital shift. He cited research projecting that 124 trillion dollars in wealth will transfer across generations through 2048, and said the 60 billion dollars that have moved into spot bitcoin ETFs so far represent a fraction of what is coming.

For context, 60 billion dollars is roughly the size of a mid-tier U.S. asset manager’s total book. Set against a 124 trillion dollar transfer of accumulated Boomer wealth to Millennial and Gen Z inheritors who are far more comfortable with digital assets, it reads as a starting line.

Koudounis told the audience that the institutional conversation has already moved on. “The question used to be, ‘Are you buying bitcoin?'” he said. “Now it’s, ‘What percent are you allocating?'”

And his conclusion on what full institutional entry means for the asset: “Once institutions get involved, it’s game over.”

How can bitcoin attract retail clients?

Balchunas pressed both men on the retail challenge, asking how they would sell bitcoin to his mother — a stand-in for the generation of older investors who remain nervous about volatility and complexity. It is a question the industry has never fully answered.

Bitcoin’s price history, with its 80% drawdowns and euphoric recoveries, is not a comfortable pitch to someone managing a fixed retirement income.

In response to this quandary, Koudounis said that Calamos has built a line of protected bitcoin ETFs that cap downside and smooth returns, turning a perceived deterrent into a feature for conservative investors who want exposure without the full ride.

The goal, he said, is to add bitcoin exposure to products that already feel familiar to traditional investors.

Trump’s answer to the same question was more direct. Fixed income, he argued, is not a genuine alternative at current yields.

“Do yourself a favor, go invest in fixed income at 4%,” he said. “I’ll invest in bitcoin. I’ll ride out the volatility and we’ll see who wins that equation in a 10-year period of time.”

He claimed BTC has averaged roughly 70% annual growth per year over the past decade and called it “a better gold,” adding that “every country in this world needs it.”

The macro case Trump made was not only about returns. He pointed to currency weakness and geopolitical instability — citing Iran specifically — as reasons traditional store-of-value assets are under pressure, and argued that BTC’s ability to transfer value across borders without a bank intermediary is a feature that becomes more valuable the more fragile existing systems look.

Currency debasement, he said, is real and ongoing, and bitcoin is designed to resist it. “Would you rather have the euro,” he asked, “or would you rather have bitcoin, an asset that’s grown at 70% a year on average, year over year for the last decade? It’s not even close.”

Koudounis: Banks can ‘debank’ you at any time

On the question of why he became an advocate at all, Trump’s answer was personal. He described how major banks shut down hundreds of Trump Organization accounts — covering buildings, golf courses, and restaurants — following the January 6, 2021 Capitol riot.

JPMorgan has since confirmed it closed those accounts. Trump and the Trump Organization later filed suit against Capital One over similar closures.

“They threw us away like dogs,” Trump said on stage.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) April 29, 2026

"I can't tell you had many accounts we had turned off in the middle of the night for not doing a damn thing wrong."

"I became hell bent on taking on these banks and fixing this system."pic.twitter.com/vtNk6qEaDC

The debanking experience, combined with what he described as slow, friction-heavy bank wire transfers, pushed him toward bitcoin’s censorship-resistant architecture. “That’s why I advocate like hell for this industry,” he said.

On usability, Trump conceded that early crypto technology was clunky, but said banks entering the space will be the force that finally makes the experience simple.

“The industry will grow,” he said, “when the user experience is simple and easy and not torturous.”

Koudounis broadened the debanking argument beyond the Trumps. He drew on personal history, recounting Greece’s 2015 debt crisis, when the government imposed daily withdrawal limits on bank accounts that lasted roughly four years before capital controls were fully lifted.

Citizens woke up one day to find the state had placed a ceiling on how much of their own money they could access.

“You don’t have to be the Trumps to be targeted by banks,” Koudounis said. “This can happen to anybody. You, me, any of us.”

Banks told you to stay away, then ‘snuck into’ bitcoin

Koudounis then turned the spotlight on the financial industry’s own behavior. While banks spent years publicly dismissing BTC and warning customers away from it, they were constructing the infrastructure to invest in it out of sight.

“Banks got the clue,” he said, and delivered a pointed summary to the crowd: “You guys won.”

Trump closed with three statements that drew the loudest reaction of the panel. He called government spending “dangerous” and pointed to a federal investigation that found some government spending to be fraudulent, citing it as evidence for why a transparent, programmable, decentralized form of money has real-world value beyond trading.

If fraud of that scale is hard to eliminate in the best-administered country on earth, he argued, it is a structural problem that BTC’s transparent ledger is built to address. He acknowledged the macro backdrop has been rough for holders over the past three months but told the audience to stay the course.

And then he closed his remarks in plain terms: “I have absolute conviction that bitcoin is going to hit one million dollars… I’ve never been more bullish on this asset class in my life.”

This post Eric Trump, John Koudounis Call Bitcoin a Global Reserve Asset, Float $1M Price Target first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

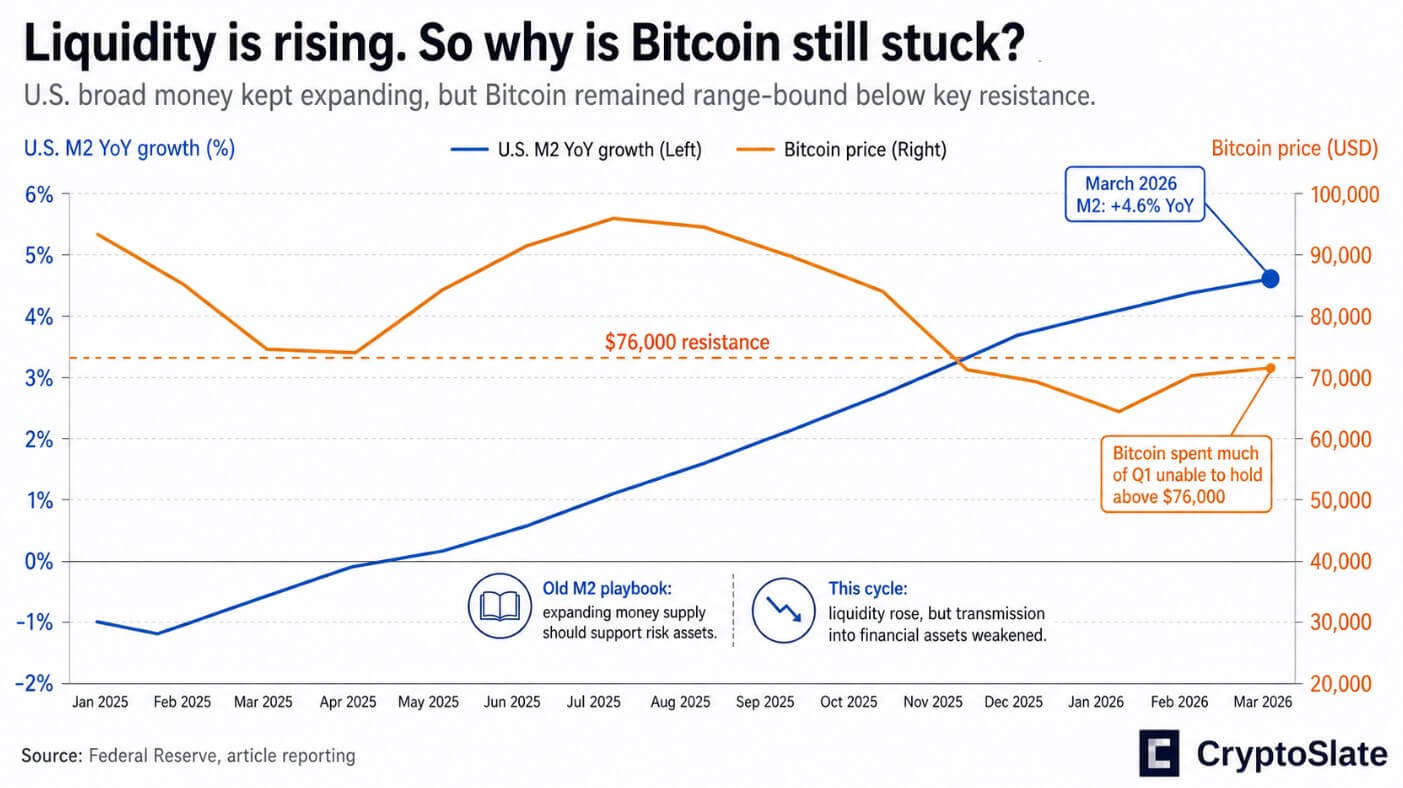

The old Bitcoin playbook ran on the simple logic that when global M2 expands, capital flows into risk assets, and Bitcoin captures a disproportionate share.

That relationship powered the 2020-2021 bull market, and crypto Twitter spent the better part of 2024 charting M2 overlays as proof that the next leg was imminent.

Now, the global M2 has been expanding while Bitcoin has continued to underperform.

March 2026 US M2 printed at nearly $22.7 trillion, up 4.6% year over year, and Bitcoin spent much of the first quarter unable to hold above $76,000, a level that Real Vision chief crypto analyst Jamie Coutts identified as key resistance on CryptoQuant's Unbiased podcast.

Coutts' diagnosis was that the transmission mechanism had changed, as the kind of liquidity now determines if the expansion actually reaches financial assets.

In the post-2008 QE era, the Federal Reserve bought assets directly, flooding the system with bank reserves that had nowhere to go but into equities, credit, and eventually crypto.

Today, Treasury issuance, reserve management, cash balance swings, and bank credit creation have replaced the central bank's balance-sheet firehose.

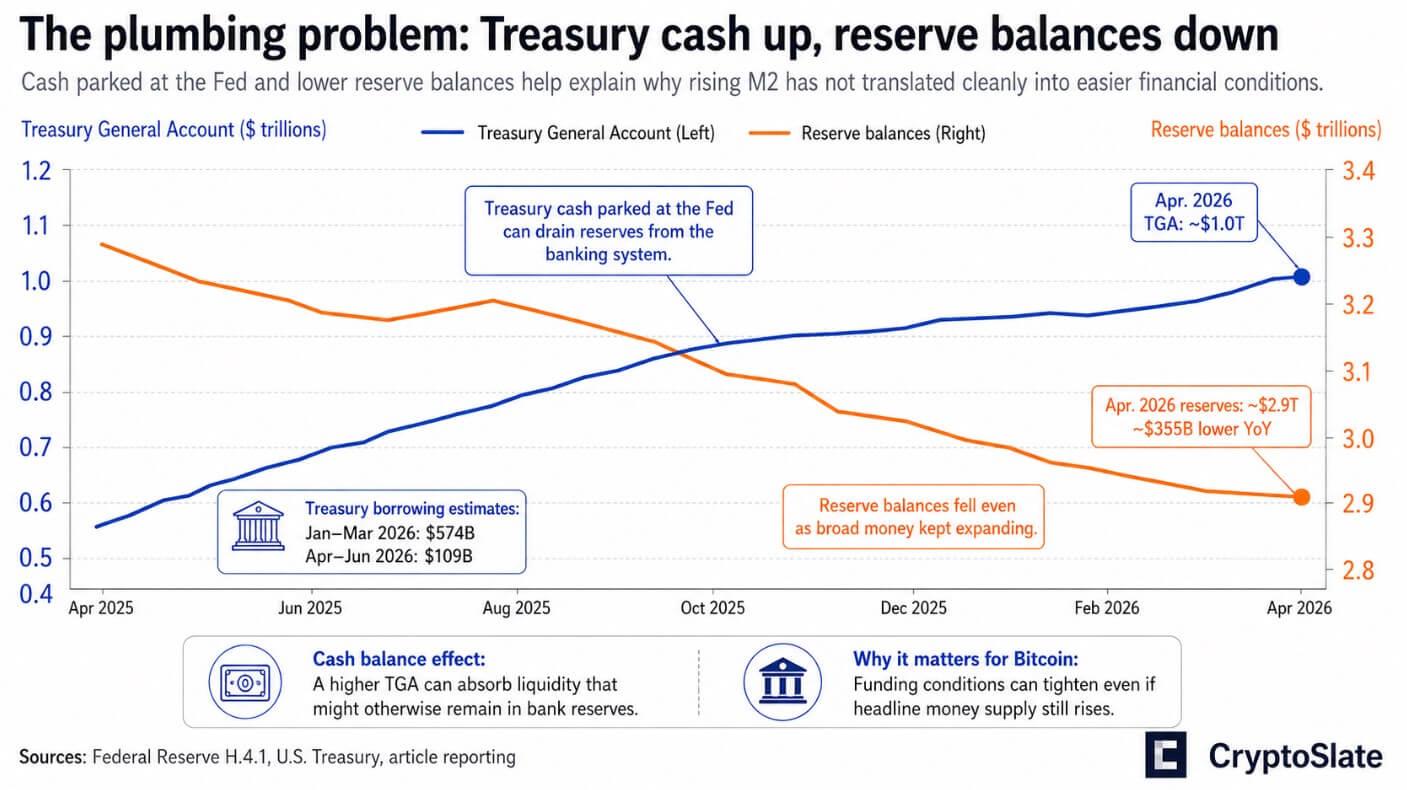

The plumbing problem

The US public debt closed the fourth quarter of 2025 at over $38.5 trillion, up 6.3% year over year. Meanwhile, US M2 grew by 4.6% over the same period.

Based on the most basic numbers available, debt is outpacing broad money by nearly two percentage points annually. The debt stock now equals roughly 1.70x total M2, a ratio with no modern precedent in a supposedly accommodative monetary environment.

The Treasury's own borrowing estimates called for $574 billion in net marketable debt in the January-March 2026 quarter and another $109 billion in April-June, while maintaining a cash balance above $1 trillion.

The Treasury General Account, which sits at the Federal Reserve, held roughly $1 trillion in the latest H.4.1 data. Cash parked at the Fed drains reserves from the banking system even as M2 continues to tick up.

Reserve balances fell to about $2.9 trillion in the Fed's Apr. 22 release, down approximately $355 billion from a year earlier.

Broad money expands on paper while the plumbing that actually moves reserves into financial markets tightens at the margin.

Bank credit is still expanding, with commercial loans and leases reaching roughly $13.7 trillion by mid-April, while that credit appears to be flowing into real-economy absorption.

At the Apr. 29 FOMC meeting, the policy rate was held at 3.5%-3.75%, and total assets stayed around $6.7 trillion. Officials cited inflation as their primary restraint, with no balance sheet expansion on the agenda.

Why the old chart broke

Coutts argued on the podcast that Bitcoin's underperformance reflects plumbing friction.

The selloff from late 2024 into early 2025 drew on tightening reserve conditions in the fourth quarter, Treasury dynamics tied to a government shutdown, derivatives-driven deleveraging, and the expanding role of ETF and derivatives markets in Bitcoin's price structure.

None of those forces appear in a global M2 overlay, as they are features of a financial system in which Treasury supply, reserve management, and funding conditions have become the real battleground.

Gold offers the clearest cross-market confirmation. Central banks bought 244 tonnes of gold in the first quarter, up 3% year over year, with total gold demand reaching 1,231 tonnes and a record $193 billion by value, per the World Gold Council.

Official institutions are hedging sovereign debt credibility at scale, but they are doing it through gold, an asset central banks can legally hold.

The IMF's latest Fiscal Monitor found that global public debt now looks set to reach 100% of GDP by 2029, with the US and China driving most of the acceleration.

The Congressional Budget Office projects a $1.9 trillion federal deficit in FY2026 and debt held by the public expanding from 101% of GDP to 120% by 2036, a structural supply overhang that will continue to compete with risk appetite for the same pool of reserves and capital.

Two outcomes

In the bull case, inflation cools toward the Fed's projected path, the Treasury cash balance declines, reserves rebuild, and bank credit continues to expand without a growth scare.

In that setup, the “liquidity is still expanding” thesis regains traction. Bitcoin can re-rate quickly because the debt-to-liquidity mismatch prevents the tightening of financial conditions at the margin.

Coutts treated the $60,000 zone as a value floor and put the odds that the cycle low is already in at better than 50-50.

In the bear case, debt issuance stays heavy, inflation stays sticky, Treasury funding strain persists, and the Fed cannot ease without reigniting the inflation it has spent two years suppressing.

Bitcoin then behaves less like a monetary hedge and more like a high-beta risk asset exposed to rates, funding conditions, and periodic deleveraging.

The April flash PMI from S&P Global already described growth running close to a 1% annualized pace. This fragile expansion does not need to tip into recession to generate the kind of funding shocks that hit Bitcoin hardest.

| Factor | Bull case | Bear case |

|---|---|---|

| Inflation | Cools toward the Fed’s projected path | Stays sticky enough to keep policymakers cautious |

| Treasury cash balance | Declines, reducing reserve drain | Stays elevated, continuing to absorb liquidity |

| Reserve balances | Rebuild from current levels | Stay tight or fall further |

| Debt issuance | Remains manageable relative to liquidity growth | Stays heavy and outpaces liquidity growth |

| Fed stance | Can ease or soften without reigniting inflation | Cannot ease meaningfully without risking another inflation wave |

| Bank credit | Keeps expanding without a growth scare | Expands weakly or is offset by tighter funding conditions |

| Financial conditions | Loosen at the margin | Stay restrictive and prone to stress episodes |

| Market plumbing | Treasury supply and reserves stop acting as a headwind | Treasury funding strain and reserve friction remain the main battleground |

| Bitcoin behavior | Re-rates higher as the liquidity thesis regains traction; $60,000 holds as a value floor | Trades like a high-beta risk asset, with sharp drawdowns, failed breakouts, and possible retests of lower support |

| Investor takeaway | Expanding liquidity is enough to absorb debt and support risk assets | Liquidity may still be growing, but not fast enough to offset debt, reserves, and Treasury supply |

Coutts separates the long-term monetary case for Bitcoin from the medium-term price behavior that reserve flows actually drive.

In a regime where debt outpaces broad money, where the Fed manages from a restrictive floor, where Treasury cash balances drain reserves even as M2 ticks up, the operative question for investors is whether that expansion is running fast enough to absorb debt, reserves, and Treasury supply simultaneously.

Until debt and reserve conditions turn decisively in Bitcoin's favor, the asset will keep delivering the sharp drawdowns and frustrating consolidations that define a market caught between a constructive long-run thesis and a tighter-than-expected short-run funding environment.

The post Bitcoin’s next risk is hiding in the gap between debt and liquidity appeared first on CryptoSlate.

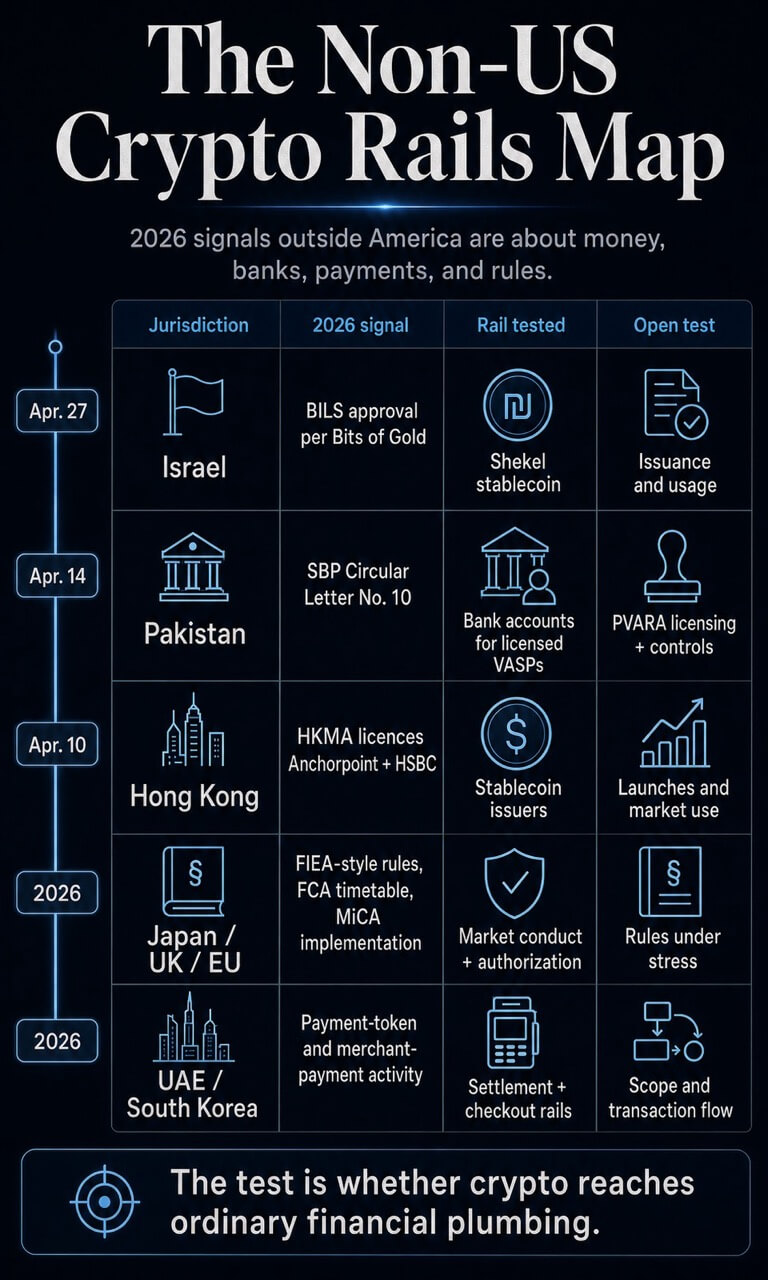

This month, Israel and Pakistan supplied a quieter test for crypto than the one playing out in US capital markets. What if the more important 2026 shift is happening where digital assets meet local money and bank accounts?

Israeli crypto firm Bits of Gold said Israel's Capital Market Authority approved the issuance and distribution of BILS, a shekel-pegged stablecoin, after a two-year pilot. Days earlier, the State Bank of Pakistan issued BPRD Circular Letter No. 10 of 2026, replacing its 2018 virtual-currency prohibition.

The Pakistan circular allows regulated entities to open bank accounts for PVARA NOC or licensed VASPs and their customers under defined compliance conditions.

Those two moves sit far from the US spot ETF cycle. Yet they point to the operational layer that decides whether crypto becomes more than an investment wrapper. The US has supplied legitimacy, liquidity, and a powerful digital-dollar debate.

Other jurisdictions are testing a different operating layer: whether crypto can connect to local money, bank accounts, merchant checkout, and enforceable market rules.

Perhaps we need to rethink how global adoption should be evaluated. A Bitcoin ETF lets investors buy exposure. A regulated shekel stablecoin lets users hold a domestic currency on-chain.

A central bank circular that lets licensed crypto firms open accounts gives the sector a bridge back into supervised banking. The first validates an asset class. The second and third test whether crypto can become usable financial infrastructure.

The test remains early. BILS still needs proof of issuance and usage. Pakistan still needs licensed VASPs with actual bank relationships. Elsewhere, Hong Kong’s new stablecoin licensees still need business launches, while the UAE, South Korea, Japan, the UK, and the EU are each testing different parts of the same adoption stack: payment tokens, merchant checkout, market conduct, authorization, and supervisory rules.

The UAE still needs clearer public mapping between dirham-token announcements and Central Bank register entries. Still, the pattern is becoming harder to dismiss: in 2026, the practical crypto work is increasingly about where digital assets touch money, banks, merchants, and settlement systems.

Local money and bank access

Bits of Gold says the approved BILS project is a shekel-pegged stablecoin designed initially on Solana, with Fireblocks, QEDIT, EY, and the Solana Foundation involved in the pilot.

The policy signal is the local-currency component. BILS brings the shekel into an on-chain market still dominated by dollar stablecoins and asks whether a national currency can gain a programmable version without ceding the entire payments layer to USD tokens.

That is monetary-sovereignty. Dollar stablecoins have become the working unit of much of crypto's settlement activity.

A shekel token, if issuance and adoption follow approval, gives Israel a way to test domestic-currency rails inside that same infrastructure. The result would be measured less by market attention and more by whether wallets, exchanges, payment firms, and regulated counterparties find a reason to use it.

Pakistan supplies the banking half of the opening. The State Bank of Pakistan circular is concrete because it replaces FE Circular No. 3 of 2018 and permits SBP-regulated entities to open accounts for PVARA NOC or licensed VASPs and their customers.

The circular also ties access to bank controls, documentation, monitoring, customer-risk checks, and compliance with Pakistan's virtual-asset framework.

That changes the operating surface for licensed crypto firms. Bank accounts are basic financial plumbing. They determine whether a regulated VASP can hold client money, reconcile flows, satisfy due diligence, and bring activity into monitored channels.

For a market such as Pakistan, which Chainalysis ranks among leading crypto adoption countries, banking access can decide whether usage remains informal or moves into traceable institutional structures.

Hong Kong offers a licensing comparator for the same rails-first pattern. On April 10, the Hong Kong Monetary Authority granted stablecoin issuer licenses to Anchorpoint Financial Limited and The Hongkong and Shanghai Banking Corporation Limited.

The HKMA register lists both with effective dates of April 10, 2026. That moves the jurisdiction from policy design to named licensed issuers, while leaving the business-launch and user-adoption tests ahead.

The active map is straightforward*:

| Jurisdiction | 2026 signal | Rail being tested | Open test |

|---|---|---|---|

| Israel | Bits of Gold approval statement | Local-currency stablecoin | Issuance, redemption, and user uptake |

| Pakistan | SBP Circular Letter No. 10 | Bank accounts for licensed VASPs | PVARA licensing and bank controls |

| Hong Kong | HKMA stablecoin issuer licenses | Named licensed issuers | Launches and market use |

| Japan, UK, EU | Rulemaking and implementation clocks | Market conduct and authorization | How rules behave under stress |

| UAE, South Korea | Payment-token and merchant-payment activity | Settlement and checkout rails | Scope, transaction flow, and adoption |

* These focus on 2026. Brazil, Singapore, Thailand, and the Philippines are also moving pieces of crypto into regulated financial channels, from VASP licensing and stablecoin rules to tokenized settlement, tourist payments, and bank-supervised activity.

Rulebooks are becoming operating layers

The same movement shows up in conduct rules. Japan's Financial Services Agency has published materials pointing toward a shift from Payment Services Act treatment to Financial Instruments and Exchange Act-style oversight for crypto-assets.

The working-group report recommends information provision, crypto-asset service-provider controls, market-abuse rules, insider-trading rules, SESC powers, and stronger user protection. The FSA's weekly review also notes draft Acts submitted to the Diet tied to FIEA and PSA amendments.

Japan's signal is about classification and conduct. Crypto assets are being pulled toward a framework where disclosure, surveillance, and misconduct rules shape participation. That makes access conditional on behavior, supervision, and accountability.

It also shows why regulatory design can be a form of infrastructure. Markets use law as a routing layer when participants need to know who can list assets, who can custody them, who can market them, and which forms of trading behavior create liability.

The UK is building a similar operating layer with a longer runway. The FCA says firms that want to carry on new regulated cryptoasset activities can apply from Sept. 30, 2026 to Feb. 28, 2027.

The new regime is expected to come into force on Oct. 25, 2027. A related consultation notice shows the regulator moving through authorization, supervision, consumer-duty, custody, prudential, and market-abuse work.

Europe already has the broader framework in place. ESMA says MiCA establishes uniform rules for crypto-assets covering transparency, disclosure, authorization, supervision, consumer information, market integrity, and financial stability.

Our broader global regulatory map has already shown regulation moving as a multi-market process. The 2026 layer adds a sharper point: rulebooks are starting to decide how crypto products enter ordinary financial channels.

The UAE adds a payment-token example, but scope remains the constraint. The Central Bank's Payment Token Services Regulation provides the rulebook for payment-token activity, while a February CBUAE register provides a public check on licensed entities.

Separately, an ADX-hosted release says IHC, Sirius, and FAB received CBUAE approval to launch the dirham-backed DDSC on ADI Chain for institutional payments, settlement, treasury, and trade flows.

For now, the evidence points to a regulated payment-token framework and institutional settlement ambition; broad retail usage would need separate evidence.

South Korea adds a merchant layer. Crypto.com and KG Inicis said in March that they would integrate Crypto.com Pay across KG Inicis's merchant network for foreign travelers and K-commerce users, with merchants able to receive fiat or digital assets.

South Korea's K Bank partnership with Ripple points to another rail where bank and payments activity intersects with crypto. Both examples still need transaction data.

Their relevance is that they move the adoption debate toward checkout, settlement, remittance, and consumer-facing access.

Usage is the harder test

The US-centered interpretation remains powerful because the numbers are large. On April 29, total crypto market capitalization stood near $2.59 trillion, with Bitcoin around $1.56 trillion.

Dollar stablecoins still dominate the working liquidity layer, with Tether‘s 24-hour volume near $111.50 billion and USDC near $47.84 billion.

Those figures explain why US policy and dollar rails keep pulling attention. The dollar stablecoin system is already large. US capital markets supply legitimacy at scale.

The CLARITY Act stablecoin fight shows that the US debate is also about who captures the economics of digital dollars. That benchmark remains essential, because global crypto infrastructure still depends heavily on dollar liquidity.

Usage data complicates that benchmark. Chainalysis said adjusted stablecoin economic volume reached $28 trillion in 2025, with a baseline projection of $719 trillion by 2035 and a catalyst scenario approaching $1.5 quadrillion.

As projections, those figures are scenario math rather than proof of future payment flows. Their direction changes the operating question: stablecoins are being evaluated as payments infrastructure, treasury infrastructure, and settlement infrastructure, alongside their role as trading collateral.

The Chainalysis adoption work shows why emerging markets sit near the center of that debate. It ranked India first, followed by the US, Pakistan, Vietnam, and Brazil, and described adoption as broad-based across income brackets.

It also tied durable adoption to on-ramps, regulatory clarity, and financial and digital infrastructure. Those are the variables being tested by Pakistan's banking circular and by local-currency stablecoin efforts such as BILS.

The IMF adds the risk side. Its March paper on stablecoin inflows and FX spillovers finds that stablecoin flows can affect parity deviations, local currency depreciation, dollar premia, and financial stability.

Put simply, stablecoins become more consequential once they start behaving like a segment of the FX market.

That creates live policy tension. Local-currency stablecoins can help keep domestic units relevant in on-chain finance. Banking access can pull VASPs into monitored channels.

Payment integrations can move crypto from portfolio exposure to checkout and settlement. Each rail also creates new supervisory demands around reserves, redemption, money laundering controls, market abuse, and currency pressure.

The evidence points to a specific split. US ETFs and Wall Street adoption have helped financialize crypto by improving access to exposure. The harder adoption test is happening where regulators decide whether crypto can touch local money, bank accounts, merchants, and FX markets.

That test is still early. BILS needs issuance and usage. Pakistan needs licensed VASPs operating through bank accounts. Hong Kong's new licensees need launches. Japan, the UK, and the EU need rules that work under market stress.

The UAE needs clean issuer and register mapping. South Korea needs merchant activity beyond announcements.

If those signals appear, the global crypto map will look less like a US-led investment-product cycle and more like a set of regional financial systems absorbing crypto under local rules. If they fail to appear, the dollar and US capital markets will keep doing most of the work.

The next test is usage, measured against attention.

The post Everyone is watching America’s crypto boom but Israel and Pakistan may be showing what comes next appeared first on CryptoSlate.

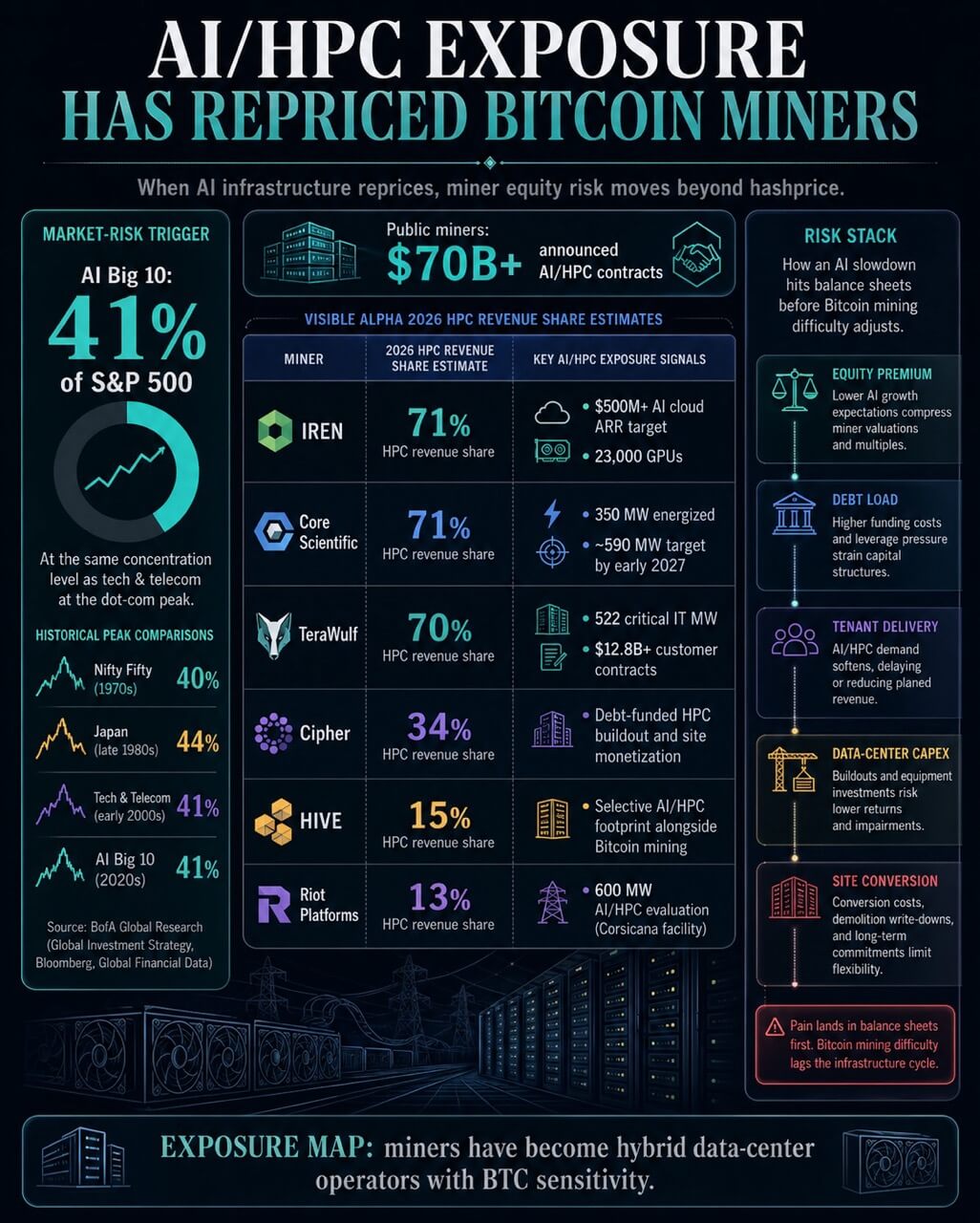

The 10 largest AI stocks now make up about 41% of the S&P 500, according to a BofA Global Research chart circulated online.

That puts the AI basket at the same concentration level that tech and telecom reached around the dot-com peak. The BofA chart put the Nifty Fifty at 40% in the 1970s and Japan at 44% in the late 1980s.

The comparison turns a stock-market concentration warning into a stress test for a corner of crypto that has spent the past year selling investors a new identity.

The market concentration is the stress trigger. Miner disclosures and mining reports supply the exposure map.

Public Bitcoin miners increasingly trade as hybrid infrastructure companies with BTC exposure. Many have signed AI or high-performance computing contracts, raised capital for denser data centers, converted premium power sites, or shifted investor attention toward long-term lease economics.

If the AI infrastructure premium fades, those companies face a different kind of pressure. The risk moves from hashprice alone into debt, contract durability, construction execution, and equity multiples.

At the same time, Bitcoin gets a second-order test. A weaker AI buildout could ease the scramble for power, rack space, interconnections, cooling equipment, and GPUs.

That would hurt miners whose new valuations depend on AI growth, while possibly helping remaining miners if scarce infrastructure becomes easier to secure.

Miners Have Repriced Themselves Around AI

The miner pivot is now measurable in revenue forecasts. A projected revenue mix cited by S&P Global Market Intelligence showed listed miners, including IREN, Riot Platforms, Core Scientific, HIVE, Cipher, and TeraWulf, shifting into AI and HPC workloads.

The projected revenue mix is already large enough to change how these companies are assessed.

Visible Alpha expected HPC to account for 71% of 2026 revenue at IREN and Core Scientific, 70% at TeraWulf, 34% at Cipher, 15% at HIVE, and 13% at Riot.

That spread shows the sector has split into cohorts. Some miners are becoming data-center operators with Bitcoin exposure.

Others are preserving mining as the core business while keeping AI optionality at sites that have power and grid access.

The scale shows up in miner economics. Public miners have announced more than $70 billion in aggregate AI/HPC contracts, according to CoinShares.

The firm also said WULF, Core Scientific, Cipher, and Hut 8 are effectively becoming data-center operators that still mine Bitcoin.

That changes the market link from an AI stock selloff. A falling AI multiple would flow through miner equities because investors have assigned value to the HPC pipeline.

Lower AI demand would also pressure the financing case for projects built around long-duration tenants, higher-density cooling, and premium grid positions.

Mining margins would still depend on BTC price and difficulty, but the equity case would have another variable.

The leverage data points in the same direction. CoinShares said several miners had taken on large debt loads for AI buildouts, including $3.7 billion in convertible notes at IREN, $5.7 billion in total debt at WULF, and $1.7 billion in senior secured notes issued by Cipher.

CryptoSlate has separately tracked how miners have been funding the AI pivot with debt while selling BTC. Put simply, the AI pivot has added a credit cycle to a business that already lived with a Bitcoin cycle.

The table below mixes 2026 revenue estimates, 2025 company disclosures, and contract updates, so each row signals exposure across different time horizons.

| Miner | AI/HPC exposure signal | Repricing pressure point |

|---|---|---|

| Core Scientific | Visible Alpha projected 71% HPC revenue share in 2026 | CoreWeave delivery, customer-funded capex, conversion execution |

| TeraWulf | 522 critical IT MW under long-term leases | Financing, tenant timelines, and credit-enhanced contract delivery |

| IREN | AI cloud ARR target above $500 million from 23,000 GPUs | GPU contract duration, utilization, equipment economics |

| Riot | 600 MW Corsicana AI/HPC evaluation | Value of using premium power for AI versus mining |

| Cipher | Visible Alpha projected 34% HPC revenue share in 2026 | Debt-funded HPC buildout and site monetization |

Cipher's rebrand toward HPC adds another example of the shift. TeraWulf's Fluidstack expansion shows how miners have paired large power portfolios with AI tenants and credit support.

The Risk Is In The Sites, Contracts, And Capital Stack

Core Scientific is the clearest example of the shift from mining sensitivity to infrastructure execution. In its fourth-quarter 2025 results, the company said it had energized about 350 MW under its CoreWeave contract and remained on track to deliver about 590 MW by early 2027.

It also reported that Q4 colocation revenue rose to $31.3 million from $8.5 million a year earlier, while digital asset self-mining revenue fell to $42.2 million from $79.9 million.

That is the pivot in operating form. Power and buildings once tied mainly to Bitcoin production are being monetized through colocation.

Core Scientific also said $226.2 million of its $279.2 million in fourth-quarter capital expenditures was funded by CoreWeave under existing agreements. That customer funding reduces some capital strain, but it also shows how deeply the buildout depends on an AI tenant's growth path.

The conversion also introduces accounting complexity. Core Scientific said it was restating prior financial statements after identifying improper capitalization of assets committed to demolition during facility conversion from mining to HPC colocation infrastructure.

The issue was company-specific, but it illustrates a broader point. Moving from mining halls to high-density AI infrastructure goes beyond marketing language.

Core Scientific's canceled CoreWeave merger agreement shows that AI-linked value already sits inside shareholder decisions.

CoreWeave's 2025 Form 10-K adds counterparty context, including large contracted power commitments and disclosed risks tied to AI demand.

The miner exposure is, therefore, linked to both site delivery and the financial health of the AI cloud ecosystem.

TeraWulf shows the same shift at a larger contracted scale. In its full-year 2025 results, the company reported long-term data center lease agreements totaling 522 critical IT MW, more than $12.8 billion in long-term credit-enhanced customer contracts, and $6.5 billion in long-term financings.

It said HPC hosting had become its primary growth engine while it continued to operate legacy mining infrastructure opportunistically.

CoinShares reported that WULF mined 262 BTC in Q4 alongside $9.7 million in HPC lease revenue. The same report said WULF's cost-per-BTC figures were distorted by the company's transition, including interest, SG&A, and depreciation linked to the new infrastructure base.

That distinction is crucial. Once a miner becomes an AI infrastructure company, per-BTC cost metrics can distort the business unless the balance sheet is separated from the rest of the mining fleet.

Riot's Corsicana decision shows how AI optionality can alter Bitcoin's capacity path before a final AI contract even exists. The company's Corsicana update said it was evaluating AI/HPC uses for about 600 MW of remaining power capacity, halting a previously announced 600 MW Phase II Bitcoin mining expansion, and cutting expected year-end 2025 self-mining capacity from 46.7 EH/s to 38.4 EH/s.

IREN adds a different exposure type. Its October 2025 AI cloud update targeted more than $500 million in annualized AI cloud revenue from 23,000 GPUs by the end of Q1 2026, with 11,000 GPUs contracted for about $225 million of ARR on average two-year terms.

That creates a faster repricing channel than long-term colocation. GPU cloud economics can shift as hardware supply, utilization, and customer budgets change.

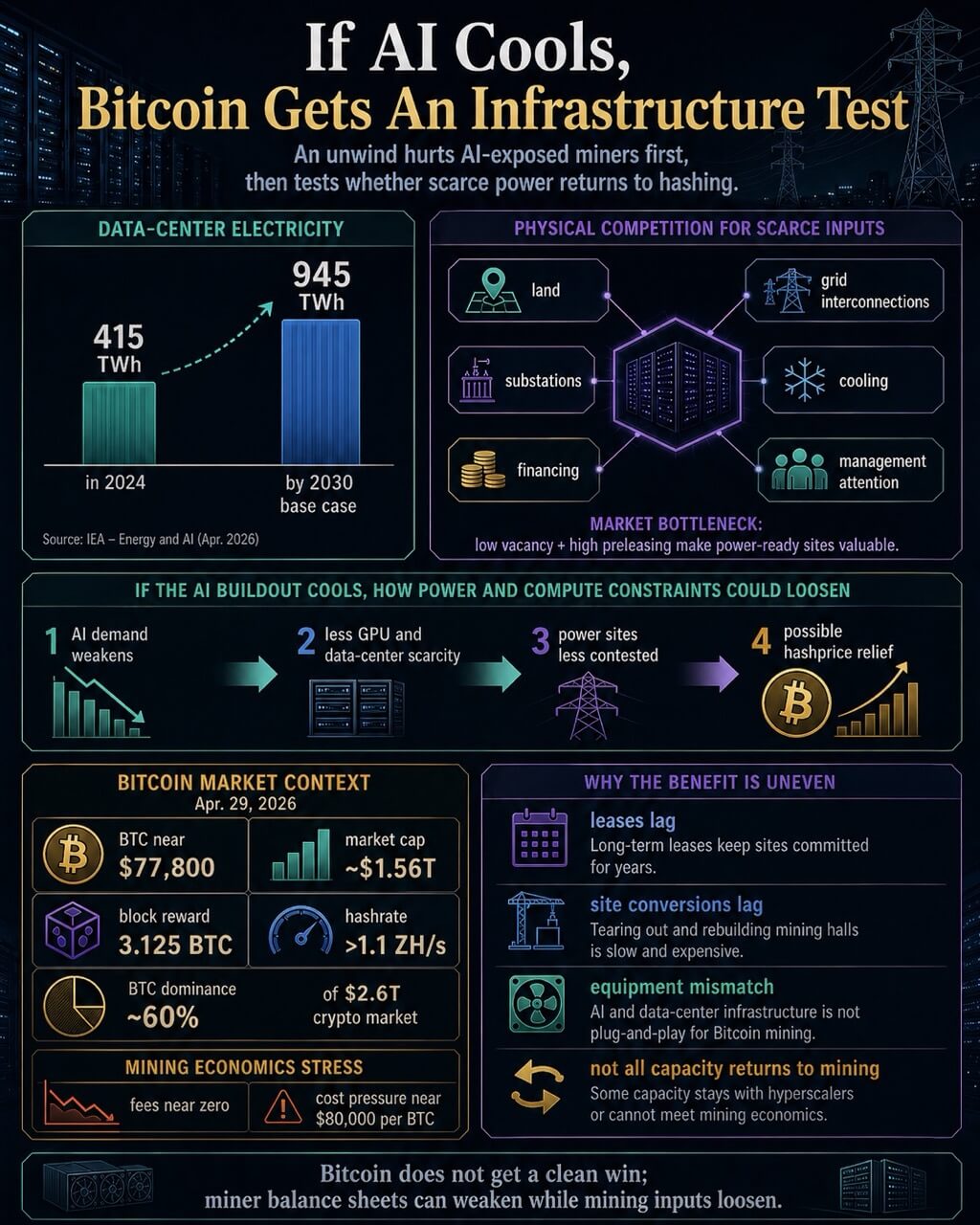

Power Scarcity Sets Bitcoin's Side Of The Trade

The Bitcoin side of the trade is less direct. A weaker AI infrastructure cycle would first pressure AI-exposed miners through equity valuation, funding costs, and contract expectations.

Bitcoin's network would feel the change through the industrial base that competes for the same power and sites.

The AI-mining link is physical. Bitcoin mining remains the larger aggregate revenue pool in key BTC price scenarios, while AI has become an immediate economic risk to the network's industrial security base.

AI and mining compete for land, grid interconnections, substations, cooling design, financing, and management attention.

Energy demand from AI explains why the competition is durable. The IEA estimated that data centers consumed about 415 TWh of electricity in 2024 and projected that global data-center consumption would roughly double to 945 TWh by 2030 in its base case.

AI-driven accelerated servers account for a major share of the increase. Data centers can be built faster than power systems can add transmission, substations, and generation, which makes location and grid access valuable.

A North America data-center trends report adds the market bottleneck behind that argument. Low vacancy and high preleasing make power-ready capacity more valuable.

For miners, the scarce asset is often the energized site, with the ASIC fleet only one part of the stack.

As of press time, Bitcoin market data show BTC trading near $76,800, with a market cap of around $1.5 trillion, a current block reward of 3.125 BTC, and a network hashrate above 1.1 ZH/s.

CryptoSlate's aggregate market page shows Bitcoin's dominance at around 60% of the $2.6 trillion crypto market. Those figures put miner economics under pressure even before AI competition is considered.

BTC price, fees, difficulty, and energy costs still determine how much security Bitcoin can support.

A cooling AI cycle could ease one part of that pressure. If hyperscaler demand, GPU scarcity, or data-center preleasing weaken, miners that stayed closer to Bitcoin could find power sites and infrastructure less contested.

Difficulty could adjust if capacity exits mining, raising hashprice for remaining operators. That mechanism appears in CryptoSlate's analysis of miners as AI utilities.

That relief has limits. The fee and cost picture keeps the upside qualified, with fees near zero and cost pressure near $80,000 per BTC.

Difficulty relief alone leaves weak miner economics unresolved. Long-term AI leases, customer-funded buildouts, interconnection agreements, equipment specialization, and site conversion costs also create lag.

An AI unwind would release capacity unevenly, and some of it may remain unusable for mining at attractive returns.

Two Outcomes Depend On AI Demand

The market risk signaled by the AI concentration chart leads to two different outcomes for miners.

In the first, AI demand holds. Public miners with high-quality power campuses keep signing HPC contracts because AI tenants can offer longer revenue visibility than Bitcoin mining.

Premium sites keep drifting toward AI, while mining concentrates around flexible power, demand response, stranded energy, and geographies where interruption is acceptable.

In that scenario, public miner equities become less reliable proxies for BTC because enterprise value comes from leases and data-center execution as much as mined Bitcoin.

In the second, AI infrastructure prices. The miners most exposed to AI growth face pressure through leverage, equity multiples, contract assumptions, and construction pipelines.

Debt raised for data-center buildouts becomes harder to carry if expected AI returns fall. GPU cloud contracts with shorter terms can reset faster.

Long-term colocation leases may offer more protection, although they also lock sites into a path that may take years to reverse.

Bitcoin's possible benefit sits downstream from that damage. The upside is a loosening of scarce inputs, lower competition for power, and a better hashprice environment for operators still focused on mining.

It is an industrial-security argument, with BTC price sitting outside the direct claim.

That is why the AI concentration chart belongs in a discussion of Bitcoin-miner balance sheets. The chart raises the possibility that the AI trade has become crowded.

The miner data shows which crypto companies have built around that trade. The unresolved test is whether those AI/HPC contracts remain durable enough to justify the shift, or whether the same infrastructure that pulled public miners away from Bitcoin becomes a source of stress.

For Bitcoin, the result would be mixed instead of clean. A repricing could weaken some of the best-capitalized public miners while making energy and data-center inputs less scarce for the miners that remain.

The next signal will come less from AI rhetoric than from financing terms, tenant delivery schedules, new power contracts, and hashprice. Those are the variables that will show whether miners bought a stronger business model or imported a second cycle into Bitcoin's security base.

The post Concentration of AI stocks inside S&P 500 hits dot-com bubble peak – and Bitcoin miners are now exposed appeared first on CryptoSlate.

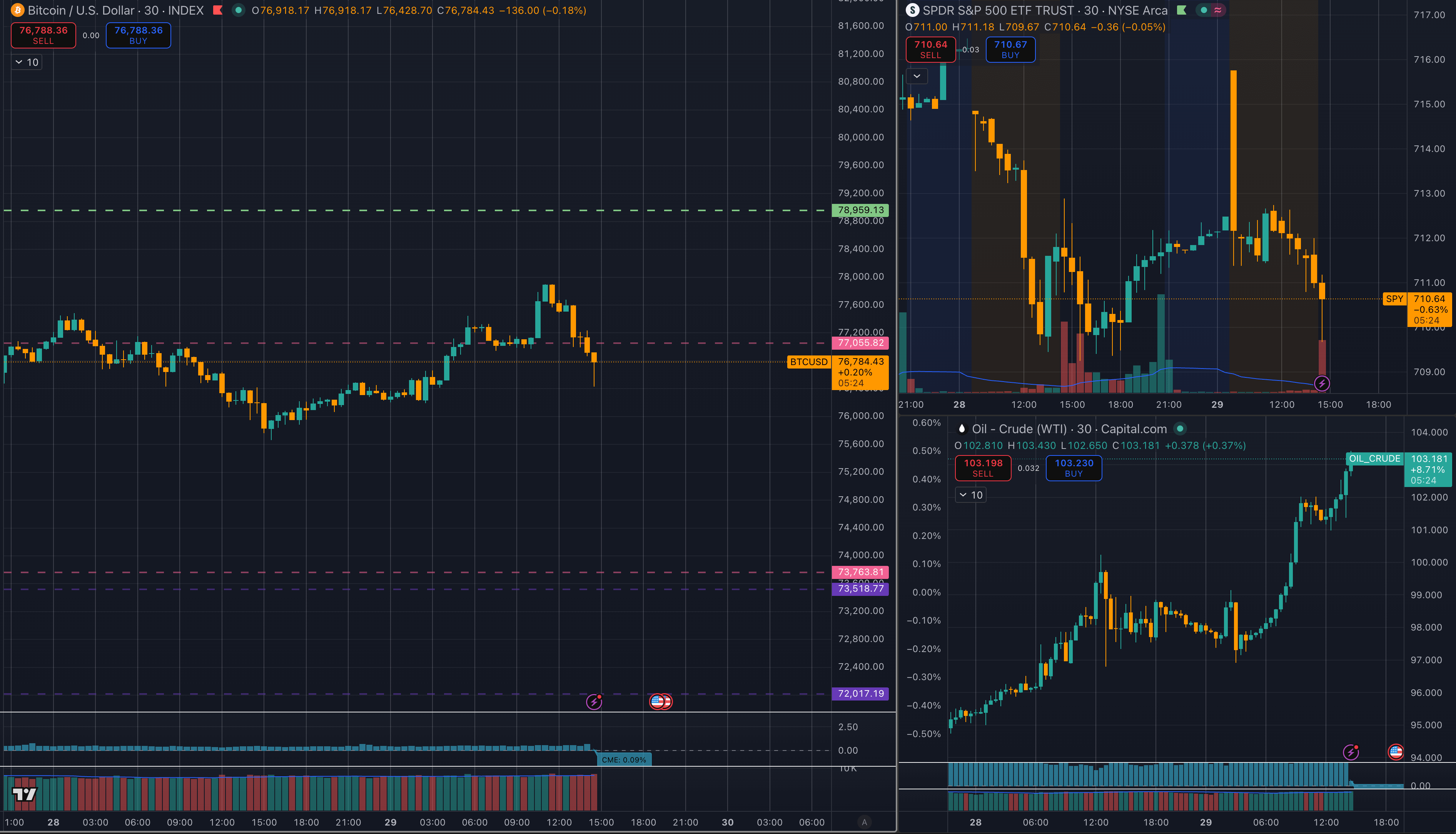

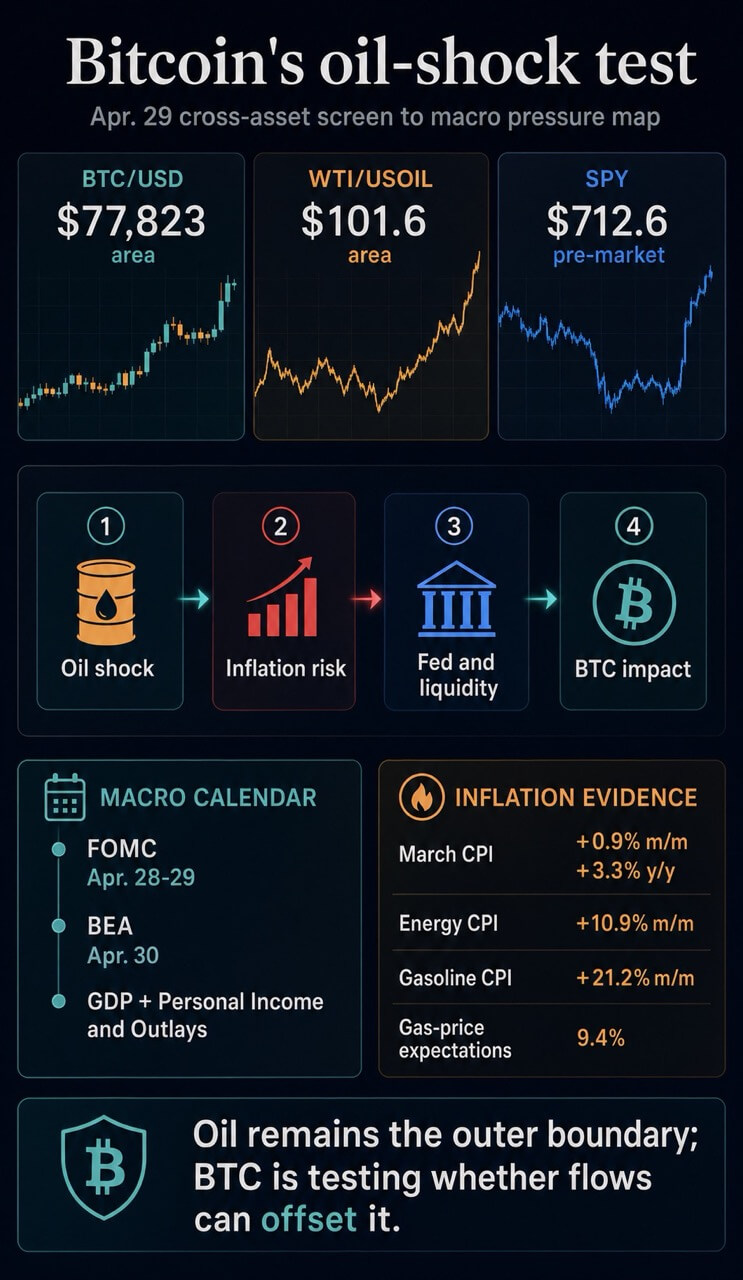

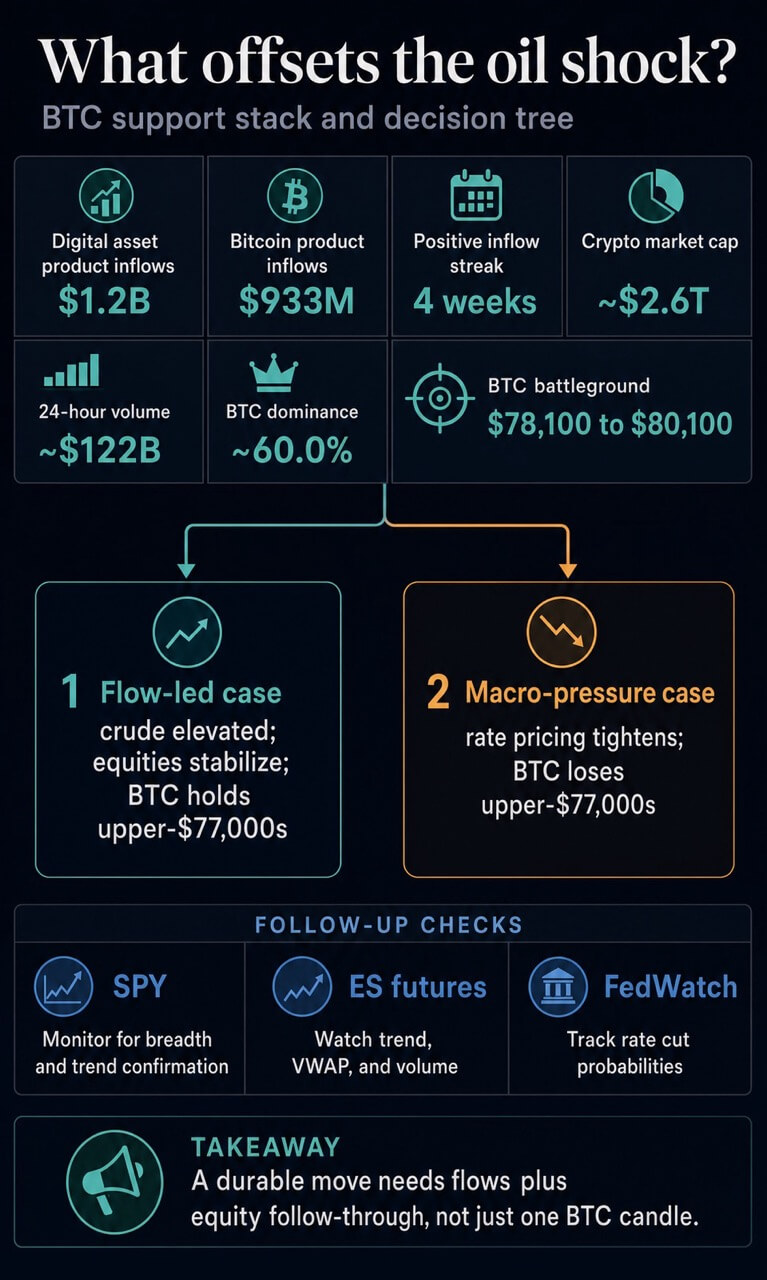

Bitcoin is trading near $76,600 after reversing from an earlier intraday push toward $78,000, while crude oil trades near $103 and the S&P 500 fell as the US stock market opened.

Before the US cash session, Bitcoin rose even as crude oil kept climbing, suggesting crypto-specific positioning was strong enough to resist the oil-inflation trade for part of the day.

After the open, the picture turned back toward equities. The chart below shows Bitcoin rolling over as the S&P 500 moved lower, while crude oil remained elevated.

That leaves two signals in tension: Bitcoin can trade independently of stocks while cash equities are closed, but US equity risk appetite can still pull it back once the main session begins.

Broader market data shows roughly $2.6 trillion in crypto market cap, about $122 billion in 24-hour volume, and Bitcoin dominance near 60%.

CryptoSlate's Bitcoin market page showed Bitcoin in the upper-$77,000s earlier today up about 1.6% over 24 hours, with market cap around $1.56 trillion. The latest chart shows why that intraday strength fell off: the US open turned the move from a simple oil-shock divergence into an equity follow-through test.

The open made equities the trigger

The first phase of the session weakened the simple April template that higher oil automatically means lower Bitcoin. Crude oil climbed through the $100 area, yet Bitcoin still moved toward $78,000 before US cash equities opened.

The second phase restored the equity branch of the trade. Once the S&P 500 fell at the open, Bitcoin slipped back toward the mid-$76,000s even as crude oil pushed higher.

Bitcoin showed it can resist the oil shock for part of a session. The same session also showed that the equity open can pull the asset back into the broader risk trade.

This is also consistent with prior CryptoSlate coverage. On Apr. 23, Bitcoin's drop below $78,000 looked more like an equity and risk-appetite impulse than a direct oil move, because crude was comparatively flat while the S&P 500 softened.

Today's chart adds a sharper version of that setup. Oil is rising, Bitcoin initially resisted the pressure, and the S&P 500 open then became the event that pulled Bitcoin lower.

Oil still controls the outer boundary

The oil channel has already been built into Bitcoin's April setup. On Apr. 24, Bitcoin held near $78,000 as oil climbed past $100, turning the asset into a test of whether scarce-asset demand could survive a stronger dollar, higher real-yield pressure, and weaker liquidity conditions.

A separate analysis of the global oil shock and the Fed said fuel, freight, and input costs can move from commodity screens into realized inflation.

That channel can keep setting rates and liquidity conditions even when Bitcoin finds a short-term bid.

The official inflation data keeps that risk concrete. The Bureau of Labor Statistics said March CPI rose 0.9% from February and 3.3% from a year earlier.

Energy rose 10.9% on the month, led by a 21.2% jump in gasoline. The New York Fed's March survey then showed year-ahead gas-price expectations at 9.4%, the highest reading since March 2022.

Energy-market structure adds another caveat. The Energy Information Administration described a wider Brent-WTI spread and disrupted navigation through the Strait of Hormuz as part of the global crude-market backdrop. Crude stress can move from commodity pricing into inflation expectations, which keeps the Fed channel open.

The calendar concentrates that pressure. The Federal Reserve calendar places the Apr. 28-29 FOMC meeting directly over this cross-asset move.

The BEA schedule lists Q1 GDP and March Personal Income and Outlays for Apr. 30. That same late-April window had already been framed as a volatility cluster around options, oil, and the Fed.

The next policy and data prints can still decide whether the oil move becomes a persistent financial-conditions problem.

Flows are the offset, equities are the confirmation

The counterweight is demand. CoinShares' latest weekly report showed digital asset investment products taking in $1.2 billion, the fourth positive week in a row.

Bitcoin accounted for $933 million of that total. CoinShares also said the Apr. 28-29 FOMC decision was likely adding caution at the margin.

On Apr. 28, fund flows and spot demand were strong enough to rebuild the bid, but the Fed still had the next hard test.

That helps explain the pre-open resilience. Bitcoin can rise even while crude oil stays elevated when fund demand, positioning, or crypto-specific liquidity is strong enough for a session. The post-open reversal shows why that alone is incomplete.

CME's E-mini S&P 500 futures remain a strong follow-up check for whether the equity branch supports or undermines the next Bitcoin move.

| Signal | What supports Bitcoin | What pressures Bitcoin |

|---|---|---|

| Crude and inflation | Scarce-asset demand can return during policy stress. | Higher fuel costs can lift inflation expectations, keep the Fed cautious, and tighten liquidity. |

| Flows and positioning | CoinShares reported $933 million of Bitcoin product inflows in the latest week. | Flow strength still faces the FOMC and bond-market test. |

| Equities | S&P 500 and futures follow-through would support a risk-appetite interpretation. | A weaker equity open can pull Bitcoin back into the risk-asset trade. |

The Apr. 22 setup gave this move a useful threshold. It said Bitcoin holding flat or firming around $78,000 while oil stayed high would weaken the war-era template that higher oil automatically means lower Bitcoin.

So far today, Bitcoin met that test before the US equity open and then lost momentum once the S&P 500 turned lower.

A later Apr. 28 bond-market analysis placed the Bitcoin battleground around the $78,100 to $80,100 area.

Below that zone, sellers can argue that the rally is another failed attempt into resistance. Above it, flows have a better chance of turning the recent rebound into a durable demand signal.

CME FedWatch remains the live market-implied check on how rate expectations are moving through that test.

Two scenarios follow from the updated chart. In the flow-led case, crude oil stays elevated but does not accelerate, the S&P 500 stabilizes, and Bitcoin reclaims the upper-$77,000s before testing the $78,100 to $80,100 band.

In the macro-pressure case, crude keeps inflation expectations warm, Fed pricing moves against risk assets, the S&P 500 weakens, and Bitcoin remains below the upper-$77,000s. That would restore the familiar April sequence: oil pressure first, equity stress second, Bitcoin liquidity last.

Bitcoin ignored crude oil long enough to prove the oil shock is not the only intraday force. Once the US market opened, equities became the trigger that pulled Bitcoin back. The regime test now depends on whether flows can rebuild the bid while crude oil and the Fed keep pressure on risk assets.

The post Bitcoin surges alongside oil as BTC price finally decouples from the war narrative… until US markets opened appeared first on CryptoSlate.

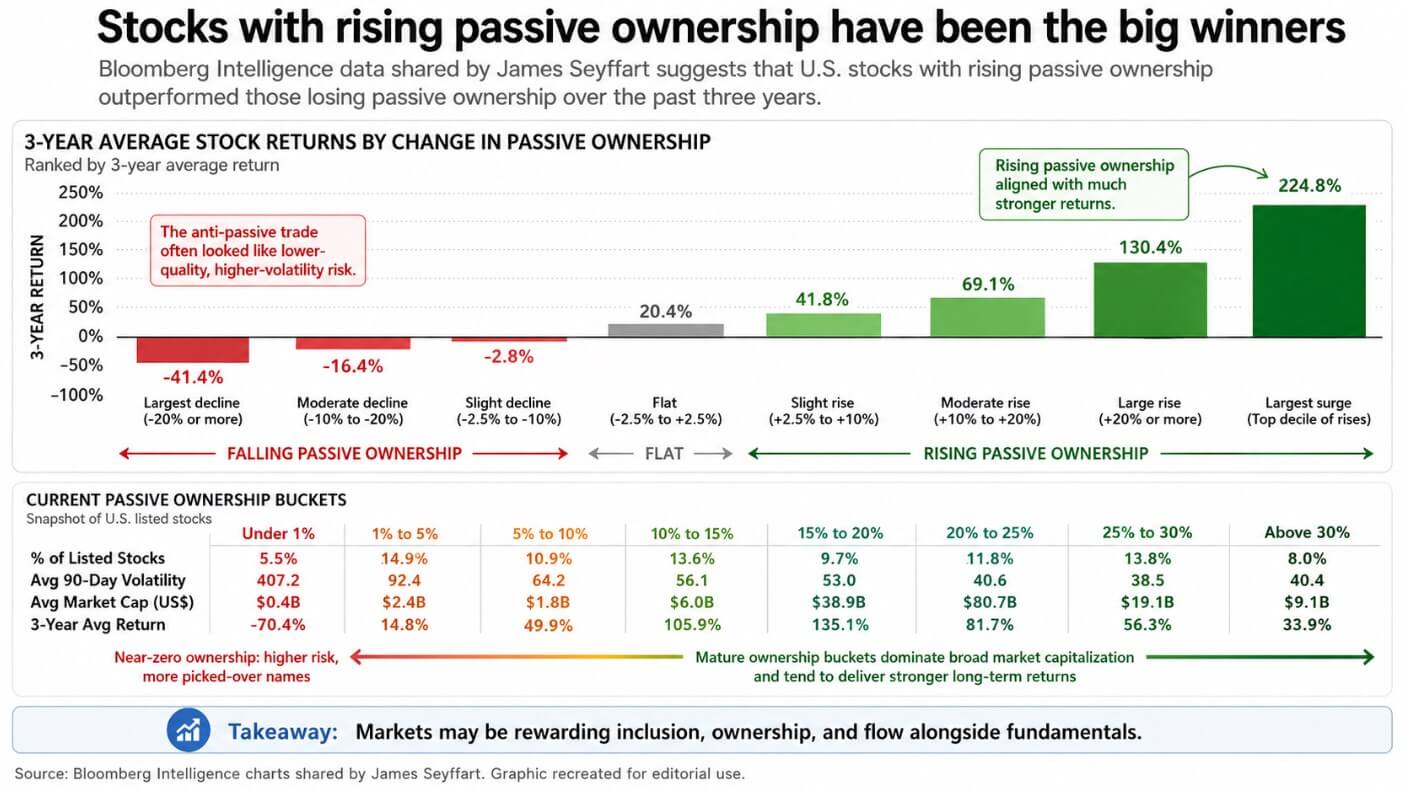

Passive investing has become one of the most powerful forces reshaping equity markets, and the evidence is accumulating in the returns data.

Bloomberg Intelligence data compiled by ETF analyst James Seyffart shows stocks with rising passive ownership have dramatically outperformed those losing passive ownership over the past three years.

The market has been rewarding inclusion, ownership, and flow alongside fundamentals. The chart's most uncomfortable implication is that the anti-passive trade has often resembled a junk drawer with small, volatile, newly listed, low-quality names that structural flows have left behind.

Ownership concentration compounds over time, and the stocks inside the passive machine tend to stay there.

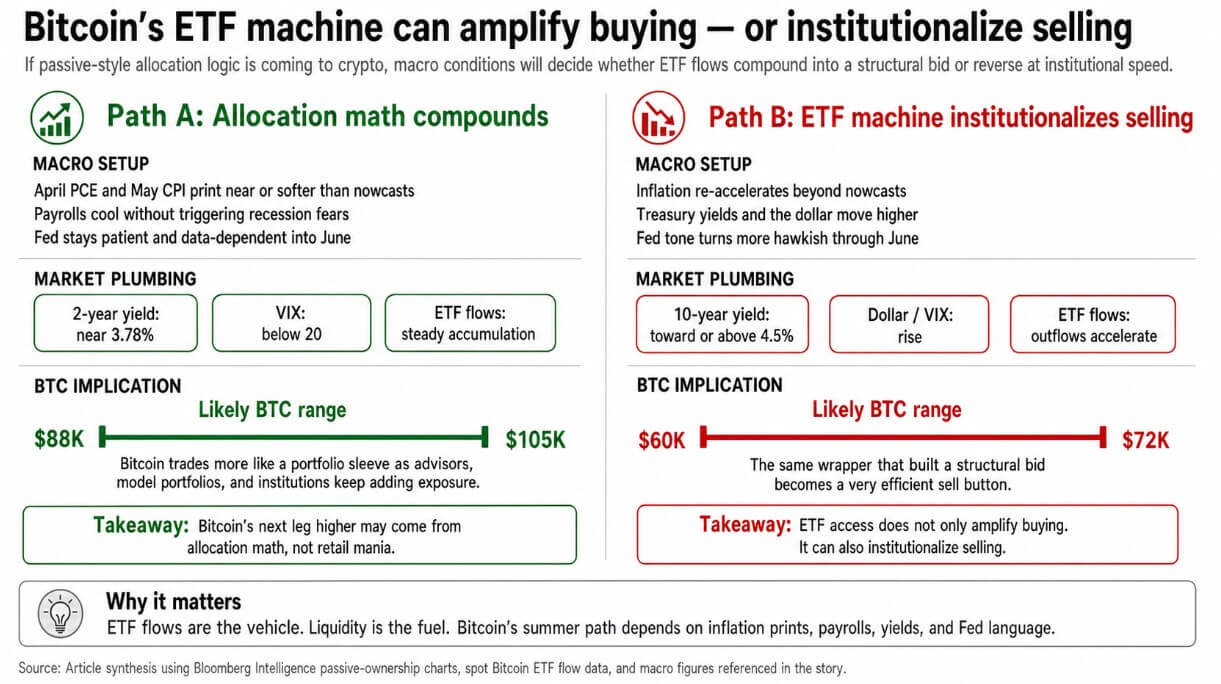

Bitcoin is now building a similar infrastructure. The SEC approved spot Bitcoin ETF listings in January 2024, and the two years since have redrawn how institutional capital reaches BTC.

US spot Bitcoin ETFs have accumulated roughly $58.4 billion in cumulative net inflows as of late Apr. 28, with BlackRock's IBIT carrying approximately $61.9 billion in net assets.

Euronext listed BlackRock's iShares Bitcoin ETP in Europe in March 2025, describing it as giving investors access to Bitcoin without the complexity of directly trading and holding it.

Deutsche Börse's Clearstream extended its institutional crypto custody and settlement services to include Bitcoin alongside conventional assets.

Bitcoin has become a wrapper investment accessible through standard brokerage rails, and that access has reshaped who can own it.

The wrapper changes the market

Recurring flows into funds holding the same names create a persistent, price-insensitive bid that compounds over time, and that is the engine behind passive equity outperformance.

Bitcoin ETFs work through investor demand, with purchases arriving as creation flows and sales clearing through redemptions on a discretionary timeline, independent of any reconstitution schedule or index mandate.

A BlackRock portfolio note from December 2024 described a 1% to 2% Bitcoin allocation as a reasonable range for multi-asset portfolios for investors who accept the risk of rapid price plunges and believe in wider adoption.

When the world's largest asset manager frames a volatile asset in allocation-sizing terms, it becomes a line item that advisors can discuss in portfolio construction terms.

A 2025 Fed note found that crypto ETP bid-ask spreads are comparable to those of other ETFs and ETPs of similar size. It argued that NAV premiums in crypto funds warrant monitoring as a measure of the extent to which crypto and equity markets have become interconnected.

The flows confirm the plumbing works, as from Apr. 14 through Apr. 24, US spot Bitcoin ETFs added about $2 billion in net inflows, based on Farside Investors' daily totals. Then Apr. 27 produced a $263.2 million single-day outflow.

In two weeks, the same vehicle demonstrated both its capacity to build a structural bid and its capacity to reverse it with institutional speed.

Allocation math becomes the driver

If April PCE and May CPI print near or softer than Cleveland Fed nowcasts, which put April CPI at 3.56% and April PCE at 3.60% year-over-year as of Apr. 28, April payrolls cool without triggering recession fears, the Fed can stay data-dependent through its June 16-17 meeting.

That keeps the 2-year Treasury yield anchored near its late-April level of 3.78%, holds the VIX below 20, and allows advisor and institutional allocations to accumulate through the June Fed window.

In that environment, Bitcoin trades as a portfolio sleeve, receiving recurring flows from model portfolios, registered investment advisors, and institutional mandates that size a position once and let it ride.

BlackRock's Spring 2026 outlook frames the current macro setup as a mild stagflationary trade-off, with the Fed on pause and moving toward gradual easing only if inflation continues to cool or growth moderates.

That is the backdrop where the wrapper bid can compound through steady accumulation by buyers watching portfolio weights, with allocation math as the driver.

If Bitcoin's weight in discretionary model portfolios continues to expand, the next leg could resemble what happens when an asset earns a permanent seat in a standard allocation framework.

The bull scenario puts BTC in an $88,000-$105,000 range into the summer, driven by allocation math alone. IBIT's cumulative net flows stand at $65.37 billion, while GBTC has bled $26.26 billion in cumulative outflows.

The allocation battle inside the Bitcoin wrapper market has already produced a winner, and the winner controls the institutional distribution network.

| Metric | Figure | Why it matters |

|---|---|---|

| U.S. spot Bitcoin ETF cumulative net inflows | ~$58.4B | Shows scale of institutional adoption through the wrapper |

| IBIT net assets | ~$61.9B | Shows BlackRock’s dominance in institutional distribution |

| IBIT cumulative net flows | $65.37B | Indicates where the structural bid is concentrating |

| GBTC cumulative outflows | -$26.26B | Shows legacy-wrapper capital rotation |

| Apr. 14–24 ETF net inflows | ~$2B | Evidence of a fast-building institutional bid |

| Apr. 27 ETF net outflow | -$263.2M | Evidence the same vehicle can reverse quickly |

The machine institutionalizes selling

The same wrapper that built a $2 billion bid in ten days produced a $263.2 million outflow in one.

If inflation re-accelerates beyond nowcasts, as Cleveland Fed models already put April PCE at 3.60% year-over-year, Treasury yields back up, the dollar strengthens, and risk appetite contracts, ETF outflows can clear Bitcoin's order book at institutional speed and scale.

March CPI already came in at 3.3% year-over-year, core CPI at 2.6%, February PCE at 2.8%, and core PCE at 3.0%.

The inflation data has consistently held above target, and if April's prints land above the nowcasts, the Fed's Apr. 28-29 meeting sets a hawkish tone that runs through June.

In that environment, Bitcoin trades as a high-beta macro asset with a very efficient sell button. The 10-year Treasury yield was 4.31% as of late April, and a move toward or above 4.5% would compress equity multiples and remove the liquidity backdrop that makes small portfolio allocations to Bitcoin comfortable to hold.

Advisory models that sized a 1% to 2% position when risk appetite was supportive face the same rebalancing logic. Whether Bitcoin falls far enough relative to the portfolio, the allocation comes out.

The bear scenario puts BTC in a $60,000-$72,000 range, pulled lower by the same institutional machinery that had been carrying it higher.

The passive equity analogy carries a corresponding implication for the broader crypto market. The anti-passive bucket in Seyffart's data, stocks losing ownership share, has often been home to thinner, more volatile names dependent on stock-picking narratives, with structural flows consolidating around the dominant wrapper.

Bitcoin holds the dominant ETF wrapper and the institutional distribution. The long tail of tokens instead competes for discretionary attention.

If passive logic is genuinely migrating into crypto through the ETF channel, Bitcoin concentrates the structural bid while everything else competes for a shrinking pool of discretionary allocation.

The ETF machine amplifies whatever liquidity the macro environment supplies and directs it through a cleaner, more visible channel into Bitcoin's order book.

If Bitcoin's next move comes from allocation math compounding in a patient macro environment or from institutional exits clearing the book in a hawkish one, it depends on the same sequence of inflation prints, payroll data, and Fed language that governs every other risk asset in the portfolio.

The post Passive money is eating stocks and Bitcoin may be next to get a huge liquidity injection appeared first on CryptoSlate.

Cryptoticker

Meta Platforms Inc. is reportedly preparing to launch stablecoin payouts for content creators across Facebook, Instagram, and WhatsApp. According to recent industry reports and internal leaks surfacing in April 2026, the social media giant is targeting the second half of 2026 for a rollout that leverages third-party infrastructure rather than a proprietary token.

Meta’s New Crypto Strategy: Distribution Over Issuance

Unlike the ill-fated Libra (Diem) project, Meta’s new approach is focused on being a "distribution channel." By integrating existing, regulated stablecoins—likely USDC—Meta aims to solve the high-cost friction of international creator payments.

This "arm's length" strategy allows Meta to avoid the regulatory hurdles that crushed its previous attempts to act as a currency issuer. Instead, the company has issued Requests for Proposals (RFPs) to external infrastructure firms to handle the heavy lifting of compliance and settlement.

Will Stripe be Part of Meta Crypto Payments?

The leading candidate for this partnership is Stripe, specifically utilizing its Bridge platform. This connection is bolstered by the fact that Stripe CEO Patrick Collison joined Meta’s board in 2025. Stripe’s acquisition of Bridge for $1.1 billion and its recent OCC approval for a national trust bank charter position it as the ideal bridge between Web2 social platforms and Web3 liquidity.

Why Will Meta Use Stablecoins as Crypto Payments?

For Meta, the primary motivation is the efficiency of the engagement flywheel. Currently, creators in emerging markets receiving small payouts (around $100) lose a significant percentage to wire fees and foreign exchange margins.

- Traditional Payouts: 1–3 business days with 3%–7% fees.

- Stablecoin Payouts: Near-instant settlement with estimated fees below 1%.

By lowering these barriers, Meta ensures that creators remain on its platforms rather than migrating to rivals like Telegram or X, which have already made strides in crypto-integrated payments.

Fed Rate Decision Today

Today, Wednesday, April 29, 2026, the Federal Open Market Committee (FOMC) will release its third interest rate decision of the year. This specific meeting carries historic weight as it marks the final policy announcement and press conference for Jerome Powell before he concludes his tenure as Fed Chair.

What to Expect at 2 PM ET

Market participants are currently pricing in a near 99% certainty that the Fed will keep interest rates unchanged at the current target range of 3.50% to 3.75%. However, the "early query" for crypto investors isn't the rate itself, but the language used regarding inflation and the transition to incoming leadership.

- Announcement Time: 2:00 PM ET (Statement release)

- Press Conference: 2:30 PM ET (Jerome Powell’s final Q&A)

- Crypto Context: Bitcoin (BTC) is hovering around $77,200, showing a "wait-and-see" approach.

Why the Fed Announcement Matters for Crypto Today

Cryptocurrencies are widely categorized as "risk-on" assets. Their prices are heavily influenced by global liquidity conditions, which are directly controlled by the Federal Reserve's monetary policy.

When the Fed keeps rates high, borrowing becomes more expensive, and the US Dollar typically strengthens, which can put downward pressure on $Bitcoin and altcoins. Conversely, if Powell’s tone today leans "dovish"—suggesting that the peak of the rate cycle is behind us—it could provide the fuel needed for Bitcoin to break past the $80,000 psychological resistance level.

How does the Fed Rate Affect Crypto Prices

Historically, the minutes following a Fed announcement see "stop-hunting" behavior, where prices swing wildly in both directions before establishing a trend.