Cryptocurrency Posts

Crypto Briefing

Yirenkyi's goal highlights Ghana's growing talent pipeline, potentially boosting their international competitiveness and player development.

The post Caleb Yirenkyi scores for Ghana in international friendly against Wales appeared first on Crypto Briefing.

Shazeer's move to OpenAI could significantly shift AI innovation dynamics, impacting competitive strategies and technological advancements in the field.

The post Noam Shazeer joins OpenAI after leaving Google appeared first on Crypto Briefing.

The case highlights increased regulatory scrutiny on market influencers, potentially impacting both traditional and crypto markets.

The post Andrew Left loses mistrial bid over court error, for now appeared first on Crypto Briefing.

The BoE's rate hold reflects caution amid persistent inflation and geopolitical uncertainties, impacting economic stability and investor confidence.

The post Bank of England expected to hold interest rates at 3.75% as inflation stays stubbornly above target appeared first on Crypto Briefing.

This digital-first diplomacy could redefine international relations, fostering peace and economic stability through innovative negotiation methods.

The post Iran and US sign historic memorandum of understanding in digital-first diplomatic move appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Fed Signals Possible Rate Hikes as Kevin Warsh Opens ‘New Chapter’ at Central Bank

The Federal Reserve held interest rates steady at its June meeting, but signaled a shift toward tighter policy under new Chair Kevin Warsh, marking a decisive turn away from expectations of near-term easing.

The Federal Open Market Committee left the federal funds rate unchanged at a range of 3.50% to 3.75%, in line with market consensus. The policy statement and updated projections, however, pointed to renewed concern over inflation and a growing willingness among policymakers to raise rates later this year.

Officials now expect the benchmark rate to reach 3.8% by the end of 2026, up from a 3.4% projection in March. Rate expectations for 2027 and 2028 also moved higher, signaling that restrictive policy may remain in place for longer than previously anticipated.

The shift comes as inflation pressures persist across the U.S. economy. The Fed now forecasts headline personal consumption expenditures inflation at 3.6% for 2026, with core inflation at 3.3%, both above prior estimates.

Policymakers pointed to supply shocks tied to the Middle East conflict and elevated energy costs as key drivers.

“Economic activity is expanding at a solid pace despite elevated uncertainty,” the Fed said in its statement, while reaffirming its commitment to restoring price stability.

Bitcoin’s price has dropped after the announcement, trading near $64,000.

BREAKING:

— Bitcoin Magazine (@BitcoinMagazine) June 17, 2026Federal Reserve officially leaves interest rates unchanged. pic.twitter.com/ah1GKCZR7a

Kevin Warsh takes the helm as Fed chair

The meeting marked Warsh’s first as Fed chair following his confirmation last month. His arrival appears to have influenced both tone and communication strategy. The post-meeting statement was shorter and omitted language that had previously suggested a bias toward rate cuts.

All voting members supported the decision, with no dissent for the first time in a year.

Updated projections showed that nine officials now expect at least one rate increase by year-end. In March, none had forecast a hike in 2026.

Futures markets moved in response, with traders pricing in a quarter-point increase by October and a high probability of a second move by early 2027.

Treasury yields rose following the announcement, with the two-year yield climbing to around 4.14%. Equities and crypto assets also reacted. Bitcoin fell from near $66,000 to around $64,000 before stabilizing, while the S&P 500 and Nasdaq 100 each dropped close to 1%, erasing earlier gains.

A ‘good family fight’

Warsh used his first press conference to frame the decision as part of a broader shift in how the Fed approaches policy and communication. He described the meeting as a “good family fight” and emphasized that the central bank is entering a “new chapter.”

He declined to provide forward guidance on the rate path and reiterated skepticism toward the Fed’s traditional use of projections. Warsh did not submit his own rate forecast, underscoring his long-standing criticism of the dot plot as a policy tool.

Instead, he signaled openness to changes in how the Fed interprets economic data. Warsh noted that many official indicators rely on survey-based methods that may lag real-time conditions. He suggested that alternative data sources and improved analytics could play a larger role in future policy decisions.

On the economic outlook, Warsh pointed to mixed signals on how restrictive current policy is. He cited weakness in housing as evidence of tight financial conditions, while noting that strength in broader markets complicates that assessment.

He also highlighted the growing impact of artificial intelligence on the economy, calling it one of the most significant structural shifts in decades. The Fed has established a task force to study how AI could affect productivity, employment, and the transmission of monetary policy.

The policy pivot comes amid political pressure for lower rates, though Warsh stressed the importance of central bank independence. President Donald Trump has called for easing in recent months, but has also stated that the Fed should act without direct influence from the White House.

For markets, the message from June’s meeting is clear: the Fed no longer sees a path toward imminent rate cuts. With inflation above target and growth holding firm, the risk of further tightening has returned to the forefront.

This post Fed Signals Possible Rate Hikes as Kevin Warsh Opens ‘New Chapter’ at Central Bank first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Mexican Billionaire Ricardo Salinas Bets 70% of His Portfolio on Bitcoin, Eyes $1 Million Price

Long before bitcoin existed, Ricardo Salinas Pliego was learning about hard money at the family dinner table.

Born in Mexico City in 1955, Salinas is the founder and chairman of Grupo Salinas, a corporate conglomerate with interests in telecommunications, media, financial services, and retail. In 1987, he took over from his father as CEO of Grupo Elektra — originally a family-owned furniture manufacturing company founded in 1906 by his great-grandfather — and refocused it on appliances, electronics, and consumer credit for Mexico’s emerging middle class.

Today, his empire includes Banco Azteca, TV Azteca, and dozens of other enterprises spanning the country.

But Salinas’ financial philosophy was shaped well before any of that. He traces his deep belief in fiat devaluation to the era when President Richard Nixon severed the U.S. dollar’s direct convertibility into gold, ending the gold standard.

“The conversation at the family table, way back then, with my grandfather and my father was always about gold,” he told CoinDesk in a recent interview, adding that “the famous fiat fraud committed by Richard Nixon” was a constant topic of discussion at home. The Salinas family, long involved in gold and silver mining, had direct skin in the game.

Salinas: Bitcoin is unseizable

Those early lessons hardened into conviction. Salinas has argued for years that bitcoin is unseizable and can be transferred instantly worldwide — advantages he sees as superior to both fiat money and the gold standard, which he says “has always been subject to governmental intervention.”

Salinas didn’t arrive at bitcoin all at once. His bitcoin allocation has grown dramatically — from just 10% of his investment portfolio in 2020 to 70% today, a trajectory that mirrors his deepening conviction in the asset over half a decade.

In June 2021, Salinas publicly announced he was working with his bank, Banco Azteca, to make it the first in Mexico to accept bitcoin — a bold move that drew both applause from the crypto community and swift pushback from Mexican financial regulators, who issued warnings about virtual assets. The banking ambitions stalled, but his personal conviction only grew.

That same year, his hunger for bitcoin exposure led him into one of the stranger episodes of his financial career. Salinas wanted to put $400 million into bitcoin in 2021 but didn’t have the liquid cash readily available, so he borrowed against his shares in Grupo Elektra — pledging $416 million as collateral for a $150 million loan.

His instincts about bitcoin were correct. The only problem was the lender turned out to be a fraud: a firm calling itself Astor Capital Fund, whose CEO “Thomas Astor-Mellon” introduced himself on a video call from what appeared to be a yacht, but was actually a man with prior convictions for forging prescriptions and stealing jewelry.

Even that painful episode didn’t shake him loose. At Bitcoin 2022, Salinas gave a keynote address discussing what he calls the “fiat fraud” — his term for centralized institutions that assure users of generational wealth while quietly destroying their currency’s purchasing power. He told the crowd his conviction was personal, not theoretical: “It’s one thing to understand a theoretical problem, and another to have lived it in your skin.”

The 70% bet — and why you should mortgage your house to buy Bitcoin

As of today, Salinas has placed approximately 70% of his investment portfolio into BTC — a figure he discussed in the interview with CoinDesk.

The allocation dwarfs what most wealth advisers would sanction. But Salinas has never been one for conventional wisdom. He is so convinced of BTC’s long-term superiority that he persuaded his own wife to act.

“I know this is a controversial topic, but I convinced my wife to mortgage the house that she has and take a loan to buy bitcoin,” he said. And she did.

He wants ordinary investors to think similarly. “For most people, the biggest investment, their nest egg, is their home equity,” he said. “Find a way to transform that into some kind of bitcoin exposure to a larger or to a smaller degree.”

His argument is grounded in a straightforward historical comparison. In January 2016, bitcoin hovered near $400 and the average Central London home cost roughly $1.6 million — about 4,000 bitcoin. With London property prices little changed a decade on, that same home would now cost fewer than 30 bitcoin. For Salinas, that comparison is all the proof anyone needs.

“It’s an asymmetrical bet to the upside,” he told CoinDesk. “The more people find out about bitcoin, the more demand there will be.”

When asked on the price predictions of fellow BTC bulls like Cathie Wood and Michael Saylor — who have suggested bitcoin could eventually reach seven figures — Salinas was uncharacteristically brief.

“So it will be a million dollars,” he said. “I just don’t know when.”

This post Mexican Billionaire Ricardo Salinas Bets 70% of His Portfolio on Bitcoin, Eyes $1 Million Price first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

U.S. Congressman Nick Begich Wants America to Stop Selling Its Bitcoin — And Start Treating It Like Gold

Congressman Nick Begich (R-AK) sat down with the Bitcoin Policy Institute at PubKey in New York for a wide-ranging conversation that touched on his path from startup founder to Capitol Hill, his landmark American Reserve Modernization Act, and the dual promise and peril of artificial intelligence.

The interview offered a window into one of Congress’s more technologically fluent members — a distinction Begich traces not to his political career but to the decades before it.

Begich’s resume reads unlike most of his colleagues. After undergraduate studies in entrepreneurship at Baylor University and an MBA from Indiana University focused on information technology and decision sciences, he spent time at Ford Motor Company before returning to Alaska to found a software development firm.

Starting with a credit card and a laptop, he built the company to roughly 150 employees across three countries, with a practice centered on early-stage startups — helping founders transform PowerPoint pitch decks into fundable products, often in exchange for equity stakes.

That background, he said, shapes how he operates in Washington. “Congress can be a frustrating place,” Begich said. “You’re not a CEO. You can’t say, ‘We’re doing this.'”

He drew a parallel between the consensus-building required in the House and the kind of obstacle navigation that defines startup life — facing capital constraints, entrenched competitors, and perpetual skepticism from investors. The difference, he noted, is that in Congress the runway is measured in election cycles, not funding rounds.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) June 17, 2026

"It could be a digital asset."pic.twitter.com/TIWd1NgDIa

The case for a Strategic Bitcoin Reserve

Begich entered Bitcoin in early 2013, operating on the thesis that it could serve as a hedge against dollar depreciation for his business.

He lost roughly 440 Bitcoin in the Mt. Gox collapse — “I got Goxed,” he said — but emerged from the bankruptcy process with what he described as a positive outcome, and his conviction in the asset intact.

That conviction is now law in proposal form. The American Reserve Modernization Act, or ARMA, which attracted significant co-sponsorship, would create a mechanism for the federal government to retain Bitcoin seized through law enforcement rather than auction it off.

The idea, Begich said, stems from a simple question: if Bitcoin can function as a reserve asset for a private company, what could it do for a government?

His argument rests on two properties he considers non-negotiable for reserve assets: scarcity and diffusion. Gold, he said, satisfies both — it is hard to produce, and broad ownership has built consensus around its value over centuries.

Bitcoin, he argued, is approaching that same status within the digital asset ecosystem, representing close to 60 percent of total cryptocurrency market capitalization.

“Once those network effects are in play,” Begich said, “the earlier you are to that cycle, the more advantaged you will be.”

He also framed ARMA as an insurance policy — not a bet on Bitcoin’s dominance, but a hedge against the possibility that the dollar does not remain the world’s reserve currency.

“Every 93 years on average, that reserve currency changes hands,” he noted, pointing to historical transitions through Portugal, Spain, France, and Britain. Holding gold is an acknowledgment of that reality, he argued. Bitcoin should be viewed in the same light.

AI: Promise and peril

The conversation shifted to artificial intelligence, where Begich was measured but direct about the stakes. He described two competing visions of an AI future: one defined by abundance — cheaper healthcare, higher productivity, broader access to economic opportunity — and one defined by displacement, where the removal of human roles at scale creates what he called “a disintermediation of purpose.”

On the question of open-source AI models, Begich pushed back against the idea that openness is an unqualified good at advanced capability levels. He cited the logic behind keeping nuclear and certain biotechnology research restricted — some asymmetric risks, once released, cannot be contained.

“The genie is out of the box,” he said of AI broadly, but argued that the full open-sourcing of frontier models, particularly post-AGI systems, hands negative actors a tool with no practical upper bound on the harm they can cause.

He was pointed in his characterization of China’s open-source model strategy, suggesting it is less a gesture of openness than an economic tool — a way to undermine the investment case for American AI development and collapse the domestic ecosystem from the outside.

This post U.S. Congressman Nick Begich Wants America to Stop Selling Its Bitcoin — And Start Treating It Like Gold first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Oman Launches Mandatory National Bitcoin Mining Pool in State-Backed Push for Regulatory Control

Oman has taken one of the most direct steps by any government to bring bitcoin mining under formal state oversight, launching a mandatory national mining pool that licensed operators across the sultanate are required to join.

The pool, Omanhash.com, was launched by Oman’s Ministry of Transport, Communications and Information Technology and will run in cooperation with Frontier Technologies LLC, an Omani blockchain and Web3 company.

Enegix Global, a vertically integrated digital energy and infrastructure company, built the technology platform and liquidity infrastructure behind it. The company called it the official national cryptocurrency mining pool of the Sultanate of Oman.

Under the approved regulatory framework, Omanhash.om is the sole official and mandatory mining pool for all licensed cryptocurrency mining companies in the country. The pool is expected to consolidate roughly 10 exahashes per second of computing power in its initial phase — a measure of the total computational work directed at securing the Bitcoin network and, by extension, minting new coins.

That hashrate matters for Bitcoin in a direct way. The more concentrated and regulated that hashrate becomes within a national framework, the greater the government’s visibility into mining revenue, energy consumption, and the flow of newly minted bitcoin. It seems the country is not trying to ban or restrict the activity — it is pulling it into a structured, trackable system.

Oman’s mining push

The country has been one of the most active jurisdictions in the Middle East for industrial-scale mining investment since 2022, when the ministry launched a $370 million hydro-cooled mining facility in Salalah.

Total investments in mining and data center infrastructure in the Salalah Free Zone have since surpassed $700 million, including two major facilities built in 2022 and 2023. Alps Blockchain, an Italian firm, brought a 150 MW facility in Salalah to full operation in mid-2025. Oman’s Omanhash.om reflects the government’s next phase: pulling that accumulation of capacity into a regulated, transparent national architecture.

For Enegix, the mandate is its second sovereign-pool contract. The company built and operates btcpool.kz in Kazakhstan, where a 2023 digital assets law requires licensed miners to operate through government-accredited pools and report revenue to tax authorities through an automated system.

The addition of Omanhash.om brings Enegix’s combined pool operations to about 25 EH/s across three pools.

“This is our second sovereign mandate, and it validates the model we have been building since Kazakhstan,” said Olzhas Amirov, chief business development officer of Enegix Global in a company press release, noting that licensing frameworks help miners operate within the law, avoid punitive taxation, and communicate with regulators.

Oman’s approach stands as a contrast to jurisdictions that have pushed back against mining with outright bans or heavy tax burdens. Instead, the sultanate has embedded mining within a broader economic diversification strategy — and is now adding a layer of centralized control that keeps bitcoin production inside the country’s regulatory reach.

Enegix said its next target is to grow its combined pool hashrate to 30 EH/s.

This post Oman Launches Mandatory National Bitcoin Mining Pool in State-Backed Push for Regulatory Control first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

79% of Bitcoin Supply Now Locked by Long-Term Holders. Analyst Sees Bear Market Nearing Exhaustion

Bitcoin is showing signs of stabilization after a brutal stretch, and research firm K33 says the on-chain evidence is difficult to ignore. In its latest market report, K33 Head of Research Vetle Lunde pointed to a record share of Bitcoin supply held by long-term holders — a metric that, historically, has preceded the end of every major bear market in Bitcoin’s history.

Long-term holders now control 79% of Bitcoin’s circulating supply, an all-time high that K33 says reflects a continued accumulation trend and a gradual shift toward a more constructive market environment.

That figure carries weight not as a standalone data point, but as part of a broader pattern: in every prior Bitcoin bear market, the circulating supply has tilted toward long-term holders as the market approached its trough.

The data on old coin reactivation reinforces the picture. As of June 6, only 218,421 BTC aged two years or more had been reactivated in 2026 — a near-historic low. The only year with lower reactivation by the same date was 2012, when 70,600 BTC had been reactivated.

The contrast with 2024 is stark: 1.18 million BTC had been reactivated by June 6 of that year, reflecting the heavy distribution that characterized the top of the previous cycle.

Lunde frames the current environment as one where long-term holders show diminished motivation to sell, with patient buyers absorbing whatever supply reaches the market.

Bitcoin ETF selling has eased

Other on-chain and market-structure indicators align with that thesis. Exchange-traded fund outflows — a dominant source of selling pressure in recent weeks — have eased. Trading volume has retreated to yearly lows, a pattern K33 associates with the late stages of Bitcoin bear markets rather than the beginning of fresh sell cycles.

Last week, Lunde noted that 50% of BTC’s circulating supply is now underwater, a level historically reached only within weeks of major bear market bottoms — though often with one final leg lower before a turn.

Not all analysts share K33’s cautious optimism. Wintermute, Glassnode, and Bitfinex have each flagged that ETF flows, stablecoin growth, and institutional demand have not yet reached levels consistent with a durable reversal.

Some forecasts put Bitcoin as low as $30,000 before any sustained recovery takes hold.

Bitcoin’s macro conditions

Macro conditions add another layer of uncertainty heading into the week. Today’s FOMC meeting — the first under new Fed Chair Kevin Warsh — has drawn close attention from the crypto market.

Rates are expected to hold steady, though markets are still pricing in the possibility of hikes later in 2026. With Bitcoin’s 30-day correlation to the S&P 500 sitting near 0.6, any shift in the Fed’s tone could hit BTC with an amplified reaction, as the asset tends to be more sensitive to macro developments during bear market conditions.

Against that backdrop, BTC posted a 5.5% gain over the past week, clawing back from two consecutive weeks of double-digit losses to trade near the $65,000 region as of this morning, June 17.

Month-over-month, the price remains down roughly 16% from a level near $79,000 in mid-May, and it trades nearly 40% below its all-time high of $126,198 reached in October 2025.

This post 79% of Bitcoin Supply Now Locked by Long-Term Holders. Analyst Sees Bear Market Nearing Exhaustion first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

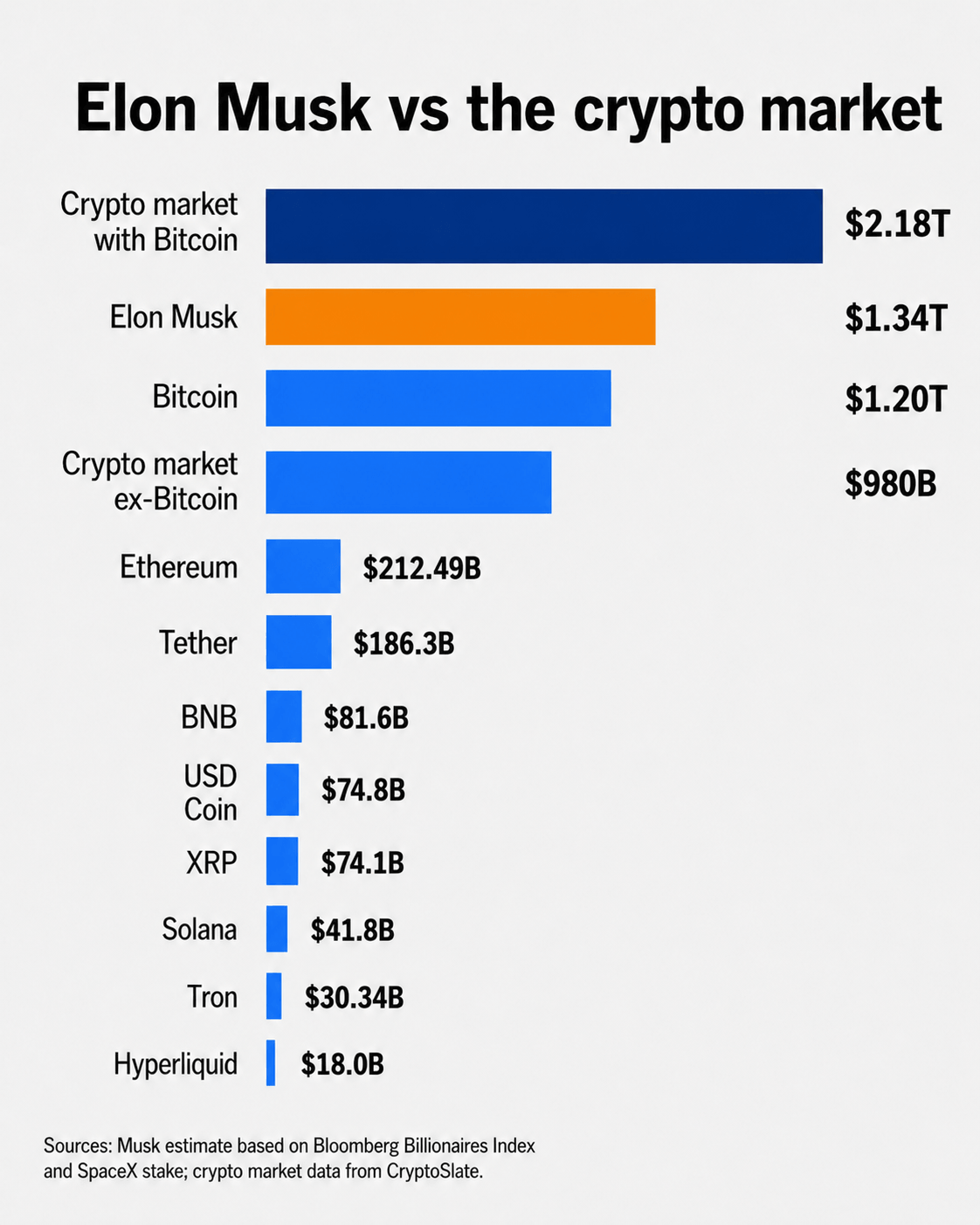

Elon Musk’s personal fortune has surpassed the market value of Bitcoin, a milestone that shows how quickly SpaceX’s public-market debut has reshaped both wealth rankings and the broader conversation around speculative risk.

According to Bloomberg's Billionaire Index, Musk’s net worth rose to about $1.32 trillion as SpaceX shares traded above $200, extending a rally that began with the company’s record initial public offering last week.

At that level, his estimated personal wealth exceeds Bitcoin’s roughly $1.29 trillion market capitalization, based on CryptoSlate's pricing for the digital asset.

While this comparison is imprecise by design, it offers a striking snapshot of how SpaceX's rapid rise has moved into the center of global markets and catapulted Musk's wealth into uncharted territory.

Bitcoin’s pullback makes the comparison possible

Bitcoin remains the largest digital asset by market value, but its lead has narrowed as the broader crypto market has cooled from last year’s highs.

Over the past year, the total cryptocurrency market has fallen from a peak of about $4.21 trillion to roughly $2.23 trillion, according to CryptoSlate data. During this period, Bitcoin has dropped by more than 50% from its late-2025 record high near $126,000, amid months of selling pressure and weaker risk appetite.

The reversal follows a powerful rally that began during Donald Trump’s 2024 presidential campaign and continued through his return to the White House.

At the time, BTC crossed $100,000 for the first time as investors responded to industry-friendly appointments, regulatory proposals, and expectations that Washington would take a softer approach toward digital assets.

However, those gains have since faded this year as crypto exchange volumes have declined, leveraged positions have been flushed out, and capital has moved back toward large technology stocks, private-market proxies, and newly listed growth companies.

That backdrop makes Musk’s wealth milestone less about Bitcoin losing its role as crypto’s benchmark and more about the speed at which SpaceX has become a competing outlet for speculative capital.

Meanwhile, this comparison is even sharper outside Bitcoin. With the crypto market worth about $2.23 trillion and Bitcoin accounting for roughly $1.29 trillion, Musk’s estimated fortune is now larger than the combined value of the rest of the digital-asset market.

SpaceX becomes the market’s new crowded trade

The immediate driver of Musk’s wealth gain is SpaceX, which trades on Nasdaq under the ticker SPCX.

The company priced its IPO at $135 a share and has since rallied by more than 50%, pushing its market value to about $2.7 trillion. The move has placed SpaceX among the world’s most valuable public companies, ahead of Amazon and near Microsoft’s market capitalization.

The rally has been fueled by a rare combination of scarcity, brand power, and momentum. CryptoSlate previously reported that only a limited portion of SpaceX’s equity entered public trading, leaving investors to compete for a small float in one of the most anticipated listings in years. That imbalance has helped turn demand into price pressure.

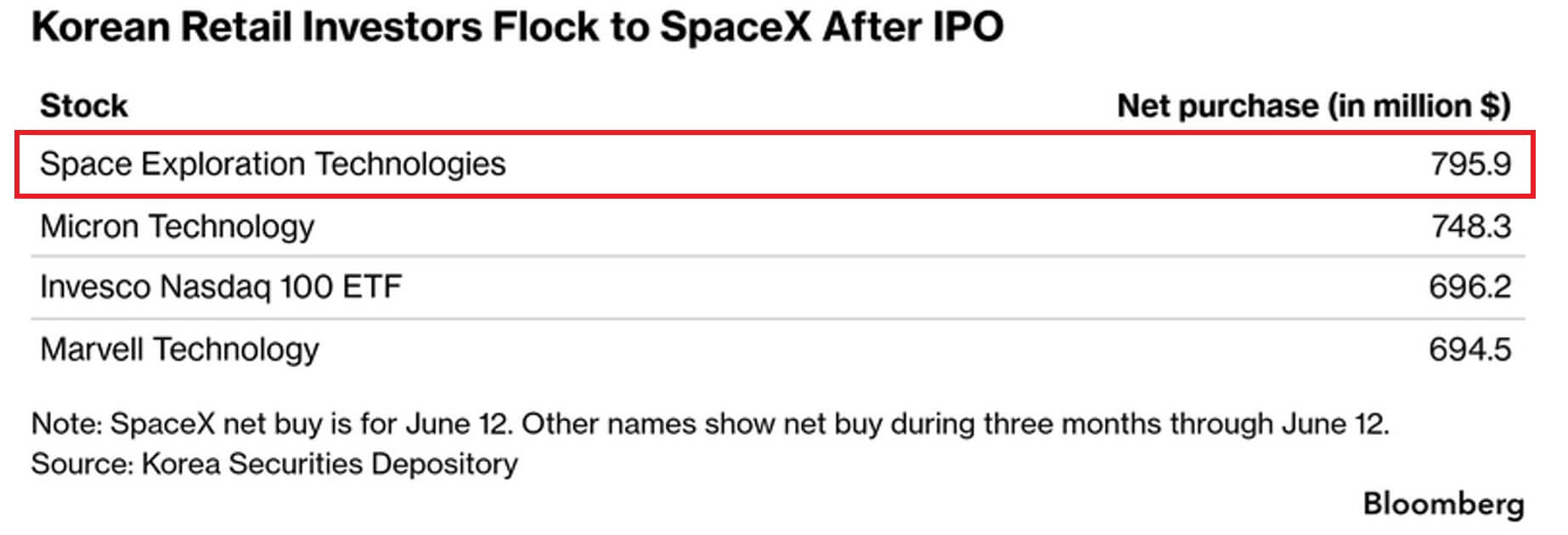

At the same time, retail investors have been central to the stock's rapid rise.

South Korean individual investors bought about $795.9 million of SpaceX shares on June 12, the stock’s first day of trading, according to market-flow data cited by Global Market Investor. That made SPCX the most purchased US stock among South Korea’s retail traders in a single session.

The buying exceeded three-month net purchases in several major US technology names. Over the prior three months, South Korean retail investors bought $748.3 million in Micron Technology, $696.2 million in the Nasdaq 100 ETF, and $694.5 million in Marvell Technology, according to the same data.

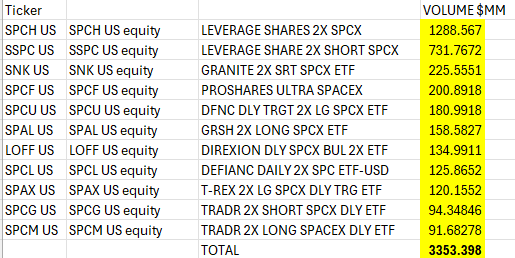

Meanwhile, the rush for SPCX is also evident in leveraged exchange-traded funds tied to the firm, which have seen heavy trading in their first days on the market.

Eric Balchunas, senior ETF analyst at Bloomberg Intelligence, said total volume across 2x SpaceX ETFs topped $3 billion, up from about $1 billion the previous day.

One product, trading under the ticker SPCH, recorded about $1.3 billion in day-two volume. Balchunas said that was the highest second-day trading volume ever recorded by an ETF, above the roughly $500 million logged by BlackRock’s spot Bitcoin ETF (IBIT) on its second trading day.

This demand is notable because many of the products track the same underlying stock and offer similar leverage. That suggests investors are not simply looking for long-term exposure to SpaceX. Many are using the funds to express short-term directional bets.

Ultimately, these numbers show that SpaceX is being treated less like a conventional aerospace listing and more like a global momentum trade.

Investors who missed the IPO allocation have been buying the stock in the open market, while others have turned to exchange-traded funds, options, and crypto-linked derivatives to gain exposure to the same product.

SpaceX valuation questions grow louder

The pace of the rally has intensified questions about whether SpaceX’s valuation is outpacing its business fundamentals.

Musk has said SpaceX could reach $1 trillion in annual revenue by 2030, a target that has helped investors price the company as more than just a rocket-and-satellite business. The market is also assigning value to Starlink, artificial intelligence, launch infrastructure, and Musk’s wider technology ecosystem.

Current financials show a company still spending heavily to build that future. SpaceX reported a net loss of $4.94 billion in 2025 on revenue of $18.67 billion. The company recorded another $4.27 billion loss in the first quarter of 2026, reflecting capital spending on Starlink, launch capacity, computing infrastructure, and artificial intelligence initiatives.

Those losses have not stopped the rally. But they have widened the gap between what SpaceX is today and what investors are paying for it to become.

That is where the Bitcoin comparison becomes useful. Bitcoin’s market value has always depended on what buyers are willing to pay for scarcity, network strength, and future monetary relevance. SpaceX is now being priced with a similar forward-looking logic, only through the structure of a public company attached to Musk.

For now, public markets are rewarding that story more aggressively than crypto.

While Musk’s fortune may not stay above Bitcoin’s market value forever because SpaceX shares could fall, Bitcoin could rebound, or both could move sharply in opposite directions.

However, the milestone captures the current state of risk appetite: the biggest speculative trade in markets is no longer necessarily a token. It is a rocket company.

The post Elon Musk’s wealth has now surpassed Bitcoin market cap amid SpaceX’s continued rally appeared first on CryptoSlate.

Spain controlled the ball for nearly 75% of the match and took 27 shots at Cape Verde's goal on June 14, a stat line that usually ends in a win.

Cape Verde's 40-year-old goalkeeper, Vozinha, walked away with player-of-the-match honors after a 0-0 draw that cost Polymarket bettors millions and made one obscure wallet roughly $9 million richer in a single day.

The wallet belongs to an account called fishalive, which joined Polymarket in June 2026 and has placed exactly two recorded predictions.

The account redeemed about $4.7 million on a “Spain not to win” contract and another $8.5 million on a Cape Verde +2.5 spread, converting roughly $400,000 in stake into a profit of nearly $9 million.

Polymarket Sports reported a bet of $400,000 at 9% odds cashed out for $4,702,769.23. The size, timing, and newness of the account are drawing attention online, with some commentators noting that a $4.5 million position was landed just eight minutes before kickoff.

A brand-new wallet read Cape Verde's chances better than the market did, and Polymarket's public ledger let everyone watch the payout land in real time.

| Position / metric | Reported amount | What it shows |

|---|---|---|

| Stake on “Spain not to win” | ~$400,000 | fishalive’s contrarian entry at roughly 9% odds |

| Payout on “Spain not to win” | $4,702,769.23 | The draw made Spain fail to win, so the contract paid out |

| Payout on Cape Verde +2.5 spread | ~$8.5 million | Cape Verde covered easily by drawing 0-0 |

| Approx. one-day profit | ~$9 million | The combined upside from betting against a Spain win |

| Spain bettor’s implied position | ~$1 million risked for ~$85,000 gain | Shows the opposite side: heavy favorite, thin upside, total loss on a draw |

Polymarket's World Cup Winner market alone has logged $2.46 billion in volume, with France leading the outright field at roughly 17.6%, Spain next at around 13.9%, and Portugal and England trailing close behind at roughly 10.8% and 10.5%, respectively.

The contract resolves around July 20, and Polymarket says its broader 2026 World Cup lineup spans 362 active markets pulling in over $2.5 billion combined.

That scale turns individual matches into standalone financial events, and the Spain game produced about $64 million in trading on its own.

Favorites keep losing

A trader identified as betoor619 backed Spain to win at roughly 92% implied odds, risking close to $1 million for a potential gain of only about $85,000, and the draw erased the position entirely.

Polymarket Sports had captured the setup days earlier when a separate user placed $1 million on Spain to beat Cape Verde, resulting in a payout of $1,085,943.48. Cape Verde held its line through stoppage time and grabbed the first World Cup point in its history, draining both positions at once.

The pattern repeated within 24 hours, as Inc. reported that a trader called FlickRaw lost about $4.2 million across a $2.7 million bet on the Netherlands to beat Japan, then $1.5 million on Belgium to beat Egypt.

Japan equalized twice, including an 88th-minute goal that finished the match 2-2. Belgium conceded in the 19th minute to Egypt and settled for a 1-1 draw despite leveling the score in the 66th minute.

| Trader | Favorite backed | Stake | Potential payout | Final result | What went wrong |

|---|---|---|---|---|---|

| betoor619 | Spain over Cape Verde | ~$1M | ~$1.085M | 0-0 | Draw killed win-only bet |

| FlickRaw | Netherlands over Japan | $2.7M | $5.83M | 2-2 | Japan equalized late |

| FlickRaw | Belgium over Egypt | $1.5M | $2.4M | 1-1 | Belgium failed to win |

| leeeroyjenkins | Belgium over Egypt | $8.6M | ~$13.1M | 1-1 | Draw erased position |

The same Belgium result wiped out the tournament's largest single bet so far: a trader called leeeroyjenkins staked $8.6 million on Belgium, a position that would have paid roughly $13.1 million had Belgium won.

Polymarket Sports tracked the match in real time, posting Egypt's 1-0 halftime lead before confirming the final draw that erased the wager.

Why now

Spain, the Netherlands, and Belgium were the stronger sides on paper, a read the betting markets shared. Win-only positions pay out for one outcome alone, and soccer's draw rate turns a dominant performance into a worthless ticket the moment the final whistle confirms a tied score.

A 92-cent “Yes” share prices in near-certainty, then collapses to zero the instant the team it tracks fails to score one more goal than its opponent. fishalive's two positions worked because a “Spain not to win” contract and a Cape Verde spread both paid out on a tie, the exact outcome that erased every favorite bet placed that week.

The winner board functions as a sentiment gauge, tracking how the crowd reranks national teams as results come in. Match-level contracts function as the viral engine because they resolve in roughly 90 minutes, generate visible profit-and-loss screenshots, and immediately punish bad sizing.

Whales have concentrated their biggest bets on favorites to win outright matches, while the largest asymmetric payouts have come from spreads and “not to win” contracts that explicitly price in draw risk.

Goldman Sachs' pre-tournament model had given Spain a 26% chance of winning the tournament, ahead of France at 19%. Polymarket's crowd has since repriced France ahead of Spain, a move that followed directly from the Cape Verde result.

The World Cup offers a global audience already fluent in football outcomes, a compressed group-stage schedule that produces a match-driven news cycle every few hours, national-team stakes that carry emotional weight independent of money, and a settlement structure that turns every big bet into a traceable, screenshot-ready story.

These are nearly all the ingredients that make a prediction market spread beyond crypto circles.

Two outcomes ahead

World Cup volume continues to compound as the knockout rounds approach, and the combination of public wallets, live repricing, and emotionally charged national outcomes makes Polymarket a fixture of sports media coverage.

The Cape Verde trade and the Belgium wipeouts become the first entries in a tournament that produces a new viral wallet story every few days, with match markets establishing themselves as a faster, more visceral complement to traditional sportsbooks.

| Scenario | What happens | Market signal to watch |

|---|---|---|

| Volume compounds | Knockout rounds drive more liquidity, more viral wallet stories, and broader sports-media attention. | Rising match-market volume, larger publicized whale positions, faster repricing after upsets/draws |

| Whales pull back | Burned traders reduce oversized favorite bets and liquidity moves toward spreads, hedges, and “not to win” markets. | Lower average favorite-bet size, more spread volume, fewer thin-upside win-only positions |

| Regulatory pressure intensifies | CFTC, states, tribes, gaming interests, and offshore-access questions become part of the tournament story. | More geofencing, enforcement headlines, or exchange-rule changes |

A pullback scenario consists of whales who got burned on thin-upside favorite bets, like the Spain position that risked $1 million for $85,000 in return, scaling back oversized win-only wagers, and liquidity migrates toward spreads and hedges that already price in draw risk.

Regulatory friction adds to the pullback, given that the CFTC's June 10 draft rules aim to formalize federal oversight of prediction markets while acknowledging that sports contracts can aid price discovery.

Yet states, tribes, and gaming interests are fighting the move, and the American Gaming Association points to survey data showing 85% of Americans view these contracts as gambling.

Spain itself briefly blocked Polymarket and Kalshi in late May over licensing gaps, which turns the story away from raw market growth and toward a fight over whether anonymous wallets and sportsbook-sized bets belong in the same regulatory category as financial derivatives.

Whether fishalive is sharp, lucky, or simply early to a structural mispricing in win-only contracts is still an open question, and Polymarket's ledger won't settle it alone.

What the ledger does show, match after match, is a direct flow of money from bettors who priced in certainty to the ones who priced in soccer.

The post World Cup bettors are losing millions on Polymarket’s “safe” favorites appeared first on CryptoSlate.

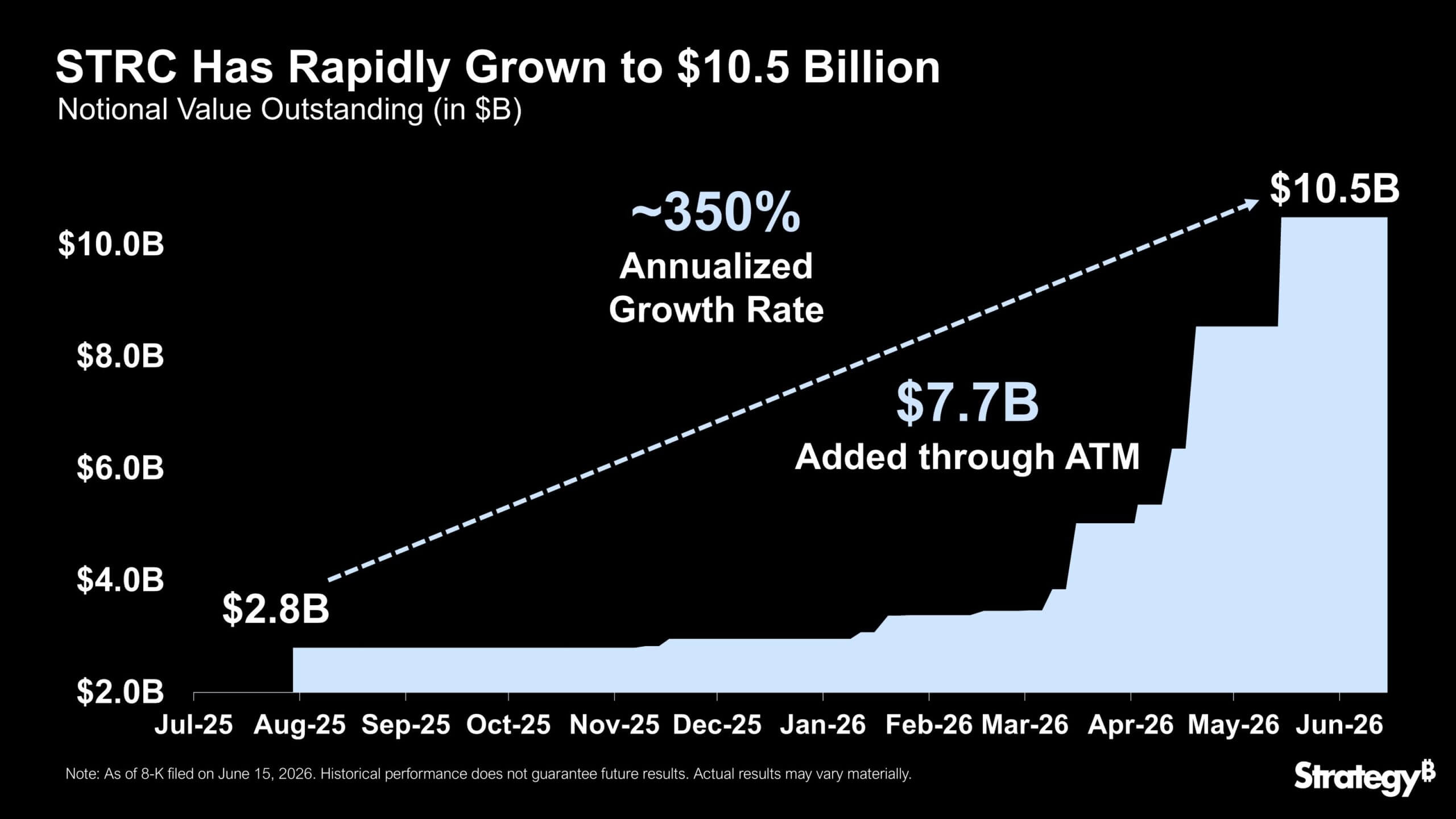

Strategy’s (formerly MicroStrategy) flagship dividend-paying preferred stock is trading at its weakest level this year, pressuring one of the company’s most important tools for raising capital to buy Bitcoin.

The $10.5 billion variable-rate perpetual preferred stock, which trades under the ticker STRC, closed Tuesday at $91.79.

The settlement marked its third-lowest close since trading began in July 2025 and left the security well below the $100 level that the Michael Saylor-led firm has tried to keep it near.

Over the past year, STRC has expanded from $2.8 billion to $10.5 billion, adding $7.7 billion through at-the-market issuance. This made it one of the fastest-growing financial products in history.

So, the decline has turned STRC into a live test of investor appetite for Bitcoin-linked income products. Strategy built the instrument to offer a high dividend while giving the company another way to raise capital.

However, the market is now tacitly demanding a higher yield as Bitcoin pulls back, rival preferred stocks offer more attractive terms, and investors reassess the risks attached to Strategy’s expanding capital structure.

Bitcoin’s pullback reaches the preferred stack

STRC’s weakness shows how quickly Strategy’s income products can start trading under the same pressure as the asset underlying the company’s balance sheet.

During the spring, strong demand and a rising Bitcoin price allowed Strategy to keep the STRC dividend rate unchanged at 11.5%. The stock traded close enough to par that management had little reason to raise the payout.

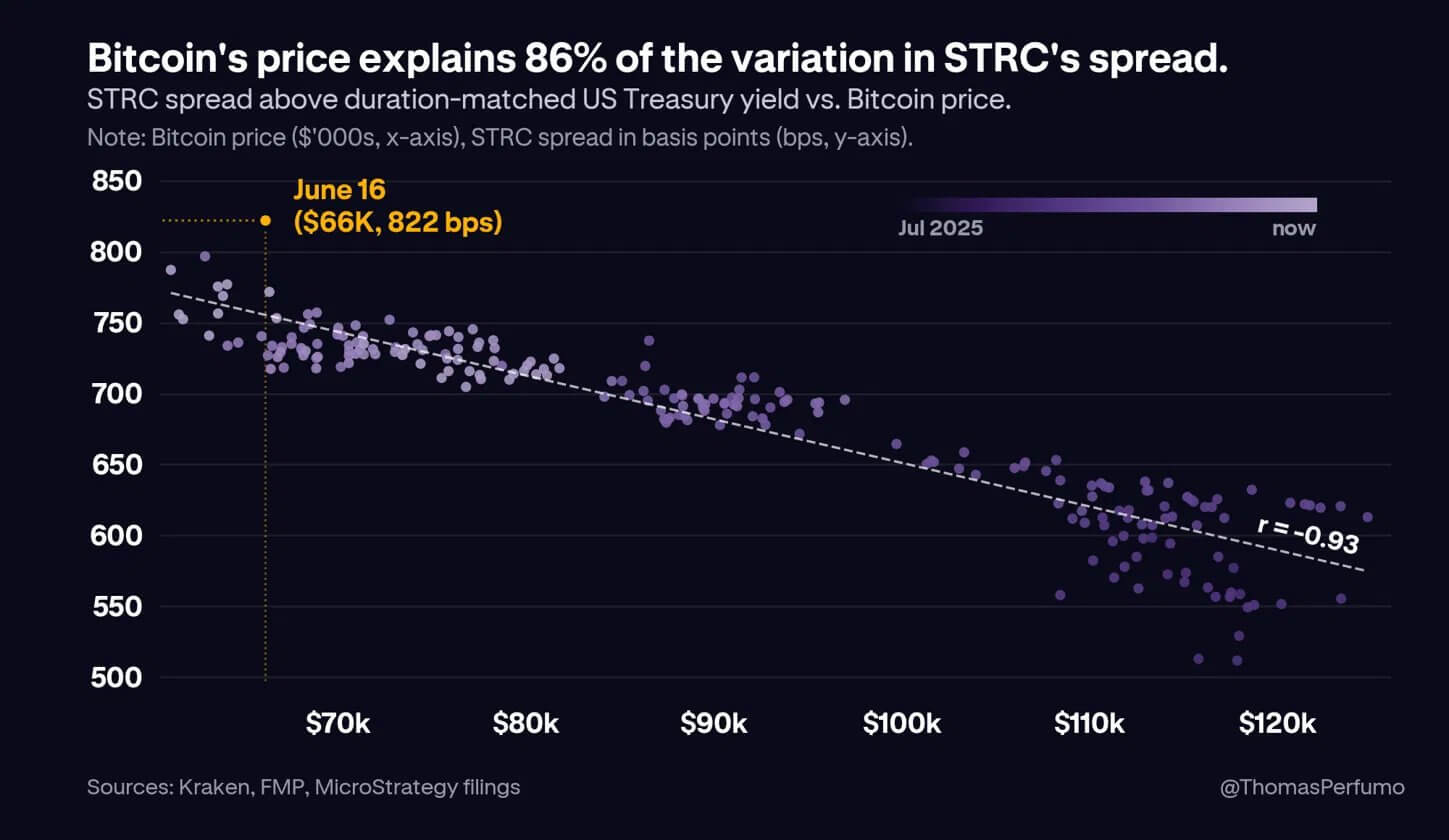

However, that changed as Bitcoin rolled over and investors began asking for more compensation to hold a preferred stock tied to a company whose value is deeply exposed to the cryptocurrency.

Kraken chief economist Thomas Perfumo said about 86% of the variation in STRC’s yield spread can be explained by moves in Bitcoin’s price. His analysis suggests investors are treating STRC less like a stable preferred stock and more like a credit product whose risk premium moves with Bitcoin.

That relationship is not unique to STRC. Other Strategy preferred securities, including STRK, STRD, and STRF, have also shown pressure.

The difference is that investors expect those instruments to move around. STRC was marketed with a stronger price-stability objective, making its extended discount more difficult for holders to dismiss.

The market math is straightforward. STRC pays an annual dividend of $11.50. At a price near $92, investors are earning about 12.6%.

To bring the stock back toward $100, Strategy would likely need to raise the dividend closer to the yield investors are already demanding. Andre Dragosh, Bitwise Europe's head of research, stated:

“Saylor essentially needs to raise the dividend by slightly more than 1$ to pull STRC to par. Equilibrium dividend is at around 12.6$ right now.”

The soft-peg problem

STRC’s design gives Strategy flexibility, but it does not force the market to value the stock at $100.

The product has a stated amount of $100, and Strategy can adjust the dividend rate to encourage trading near that level. But there is no automatic mechanism requiring buyers to step in at par. That distinction has become central to the current selloff.

Parker White, chief operating officer and chief investment officer at DeFi Development Corp., said the product’s soft $100 anchor may have made it vulnerable to short sellers.

He argues that STRC’s retail-heavy investor base expected the stock to stay close to par, so a move even a few dollars below that level can trigger outsized concern.

According to him, short sellers may be able to exploit that reaction because the cost to borrow STRC is relatively low.

White continued that the outright borrowing cost is about 60 basis points, making the trade cheap to maintain compared with similar products. Strategy’s at-the-market issuance program may also limit upside above $100, reducing the risk that short sellers face if they position against the stock.

The theory gives traders a clear pressure point. If investors treat $100 as a promise rather than a target, every move away from that level can weaken confidence.

That risk is more pronounced because some crypto protocols have been built around STRC or use Strategy-linked securities as part of broader yield strategies. A sustained decline could force some holders to reassess collateral values, liquidity assumptions, and expected returns.

Strive's SATA raises the comparison

White also noted that STRC’s discount has become more visible because a rival product is holding up better.

Strive’s bitcoin-backed preferred stock, SATA, has continued to trade close to its $100 par value while offering a higher annualized payout of about 13%. It also pays dividends daily, rather than monthly or semi-monthly, giving investors faster cash distribution and making the product more expensive to short.

That structure has strengthened SATA’s appeal among income-focused investors. Daily dividends reduce the pressure that often builds around ex-dividend dates, when holders decide whether to collect the payout or rotate elsewhere.

They also increase the carrying cost for short sellers, who must account for dividend obligations more frequently.

White estimated that SATA’s baseline borrowing cost is about 460 basis points. Including the effect of daily dividend obligations, he said the annualized cost to short SATA rises toward 17.6%, compared with about 60 basis points for STRC.

The comparison puts Strategy in a difficult position. STRC still offers a high stated payout, but the market is showing a preference for both higher yield and faster payments.

Restoring STRC comes with a cost

STRC’s decline has left Strategy with a narrower path to restore confidence in one of its most important funding channels.

White has argued that the company could stabilize the product by raising the dividend to 12%, calling a shareholder vote to move to daily payments, increasing the call price from $101 to at least $110, and rebuilding the cash buffer to $2.5 billion.

According to him, higher dividends and daily payments would make STRC more expensive to short. A higher call price would give the stock more room to trade above $100, increasing the risk for traders betting against it.

Additionally, the larger cash reserve would reduce concerns about dividend coverage and help reassure income-focused investors.

However, each step would carry a significant trade-off that could impact Strategy.

For context, A higher payout could help pull STRC closer to par, but it would also increase Strategy’s recurring cash burden. Daily dividends may improve market confidence, but would require another structural change. A larger reserve could strengthen the credit profile, but may slow the pace of new Bitcoin purchases.

The larger challenge is the investor base. STRC still appears to be owned heavily by Bitcoin-native buyers, who compare the preferred stock with Bitcoin itself.

When Bitcoin falls, those investors can either collect income from STRC or rotate back into spot Bitcoin at lower prices. That competition forces Strategy to offer a higher return than traditional fixed-income buyers might require.

A broader investor base could reduce that pressure. For money-market, preferred-stock, and fixed-income investors, an 11.5% cash dividend remains large.

However, attracting that capital may require stronger proof that STRC can hold its range even during Bitcoin drawdowns.

The post Strategy’s $10 billion STRC Bitcoin yield product sinks to yearly low as market demands higher payout appeared first on CryptoSlate.

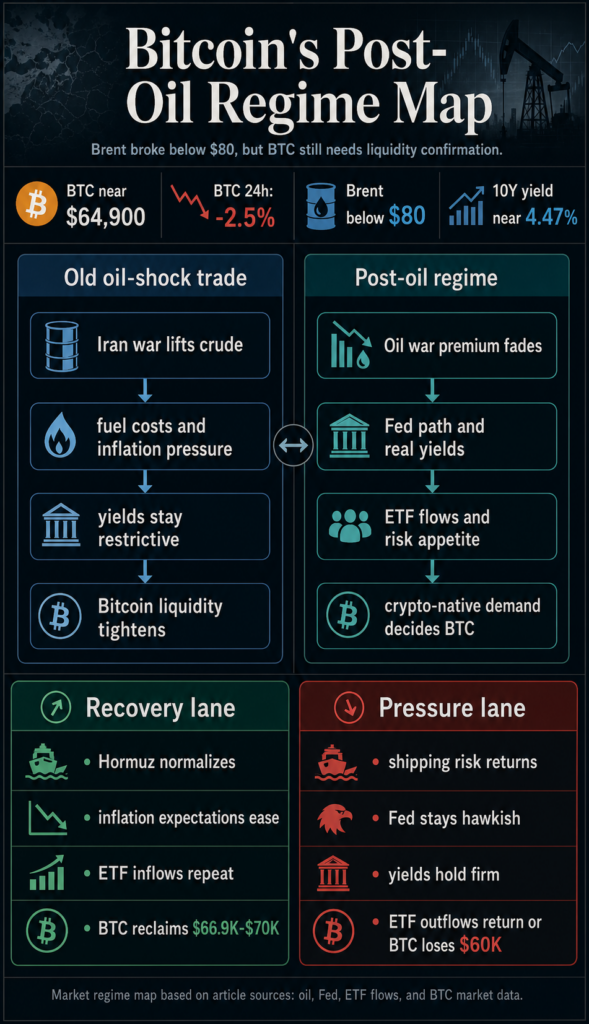

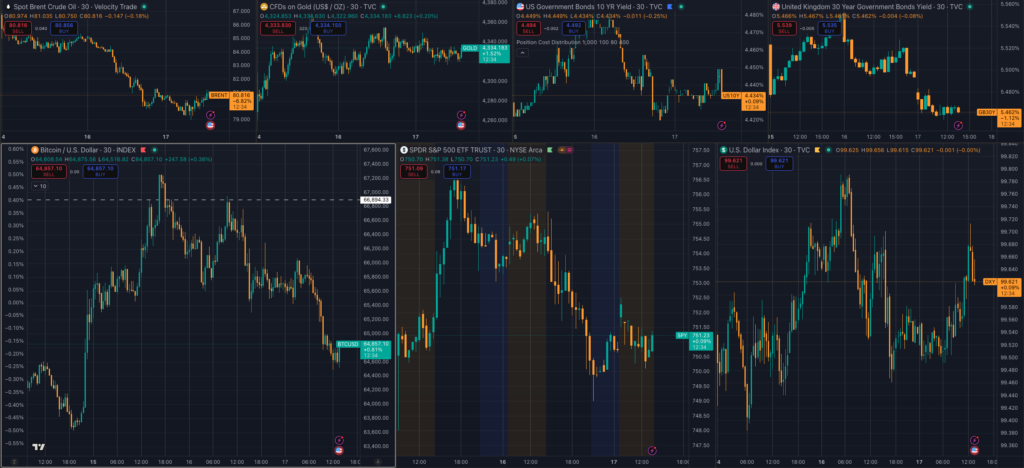

Bitcoin is falling while Brent crude trades below $80 after the US-Iran peace framework.

The oil shock that dominated Bitcoin's 2026 macro trade has eased, yet BTC is still trading near $64,900, down roughly 2.5% over 24 hours on CryptoSlate's Bitcoin price page.

Brent's drop should have given risk assets a cleaner relief trade. Instead, it has exposed the next problem.

The market has moved past the simple oil-up, Bitcoin-down model. Lower crude removes a bearish driver. Restored liquidity support will still have to come from rates, ETF flows, and risk appetite through the end of 2026.

Global oil prices settled below $80 for the first time since the Iran war began, after the US-Iran framework pointed toward reopening the Strait of Hormuz. Ships were still not moving normally through the chokepoint, leaving the peace deal's operational effect unresolved.

President Donald Trump's public message that the Iran deal was complete gave traders the catalyst to remove part of the war premium from crude. Bitcoin's response puts liquidity, rates, risk appetite, ETF demand, and crypto buyers' willingness to step in after the geopolitical pressure at the center of the next trade.

Oil Moves To The Background

The old Bitcoin trade was coherent. When the Iran war lifted crude prices, it threatened to push fuel costs through supply chains, keep inflation expectations elevated, delay Fed rate cuts, and leave risk assets with less oxygen.

That earlier oil-pressure setup was already evident when Bitcoin fell, as higher oil prices, higher yields, and the vanishing of rate-cut expectations tightened financial conditions. Oil became the first signal because it was the fastest way for the war to reach inflation, yields, and the Federal Reserve.

The Iran-deal rally framework made the same point from the other side. A peace framework could help Bitcoin only if lower crude oil prices translated into real oil flows, lower gasoline prices, softer inflation compensation, and a Fed path that looked less hostile to risk assets.

The first link in the confirmation chain has now moved. Crude has broken lower, and Bitcoin is failing to trade like an asset with a clear path back to upside.

Oil has shifted from main driver to background risk. If Hormuz traffic fails to normalize, or if energy markets reprice disruption, oil can still hurt Bitcoin. If crude keeps falling without a matching improvement in Fed expectations, ETF flows, and risk appetite, Bitcoin has less reason to rally.

The Fed remains central. The April FOMC minutes kept energy-driven inflation risk in view, and the 10-year Treasury yield was around 4.47% in the latest visible data.

That is a restrictive backdrop for a non-yielding asset that still trades like high-beta liquidity in stress periods.

The next Fed communication sits directly in that path. Bitcoin needs the market to believe lower oil will give policymakers room to stop leaning against risk.

A hawkish Fed message, sticky inflation language, or another push higher in real yields would leave the peace deal looking like a crude-market event rather than a Bitcoin liquidity event.

That is why the lower oil print places a different burden of proof on Bitcoin. The next confirmation has to come from the parts of the market that set liquidity: Fed communication, Treasury yields, dollar pressure, equity-risk appetite, ETF flows, and derivative positioning.

Liquidity Becomes The Year-End Test

Bitcoin ETF flow data showed a small positive daily flow on June 16, but the magnitude is too small to account for the entire regime shift.

Earlier ETF-flow coverage showed how quickly institutional demand can turn from support into a stress point when oil, rates, and risk appetite move against Bitcoin.

That is why the year-end path depends less on one green ETF print than on repetition. Bitcoin needs several sessions in which lower oil is joined by steady ETF demand, softer yields, and a broader risk appetite.

Without that combination, the market may interpret the latest inflow as a pause in de-risking before any new allocation cycle begins.

Crypto-native liquidity is the final test. BTC open interest and futures volume were large enough to make positioning relevant for short-term price transmission, according to CoinGlass data.

Direction still depends on the catalyst. Any surprise from the Fed, ETF desk, or equity market can travel quickly through leveraged positioning.

| Signal | Oil-shock regime | Post-oil regime |

|---|---|---|

| First market question | Will crude keep inflation and yields high? | Will lower crude reach Fed expectations and risk appetite? |

| Bitcoin pressure point | Higher energy costs tightened financial conditions. | Weak liquidity and uneven ETF demand limit recovery. |

| Confirmation signal | Hormuz flows, gasoline, CPI, and Fed pricing. | ETF inflow streaks, softer yields, weaker dollar pressure, and risk-on equities. |

| Failure signal | Renewed crude stress and no rate-cut path. | BTC loses $60,000, yields rise, or ETF outflows return. |

The base case into year-end is a fragile, liquidity-led recovery attempt.

That is a more cautious view than the oil chart alone would suggest. Brent below $80 removes one of the biggest bearish inputs for 2026, but Bitcoin still has to rebuild the demand side.

The asset can recover if lower crude becomes lower inflation expectations, if yields drift lower, and if ETF flows shift from one-off positive days to steady demand.

The recovery lane is straightforward. Hormuz traffic normalizes, gasoline pressure eases, inflation compensation falls, and the Fed gets enough cover to sound less restrictive.

At the same time, Bitcoin ETF flows stabilize, spot demand improves, and BTC reclaims the $66,900 to $70,000 shelf that recent market-structure coverage highlighted as important.

In that lane, oil's job is to prevent the liquidity trade from being blocked. The upside would come from capital returning to Bitcoin as a scarce, liquid risk asset once rates and flows stop arguing against it.

The pressure lane is just as clear. The peace framework can stall at implementation, tanker traffic can remain impaired, or crude can reprice if shippers and insurers lose confidence in the route.

Even with lower oil, Bitcoin can remain pinned if the Fed removes easing hopes, if Treasury yields hold firm, or if ETF flows return to redemptions.

That is the key shift. Liquidity and risk appetite now carry the trade. Bitcoin's next move depends on whether the market sees the peace deal as a real disinflation shock or as a crude reset that leaves rates, dollar pressure, and ETF demand unresolved.

For the rest of 2026, liquidity and risk appetite have outpaced oil. Bitcoin's bullish case is still alive, but it now runs through the Fed, ETF desks, and the willingness of crypto capital to buy the dip after the war premium has already come out of crude.

The post Oil finally loses its grip on Bitcoin – but now liquidity takes over the sell pressure appeared first on CryptoSlate.

A megawatt leased to an AI tenant now commands a different price on Wall Street than a megawatt sitting in a Bitcoin miner's pipeline, and the distance between the two has become the central pricing question for the entire sector.

VanEck's latest framework for valuing publicly traded miners shows that companies with signed AI and high-performance computing leases trade at more than 10 times gross energy output, while miners with little or no contracted capacity trade at roughly 2 to 6 times that metric.

Investors have started treating leased megawatts as a distinct, more valuable asset class than mined Bitcoin or unsold power capacity.

| Metric | VanEck figure | Why it matters |

|---|---|---|

| Miners with signed AI/HPC leases | Above 10x gross energized power | Wall Street is assigning a premium to contracted AI capacity |

| Miners with little or no contracted capacity | Roughly 2x–6x gross energized power | Pipeline alone is worth much less than signed leases |

| Delivered AI/HPC capacity | ~25% of leased capacity | Most contracted capacity still has to be built and delivered |

| Near-term funding shortfall | ~$50B | The sector needs major capital before leases become cash flow |

| Long-term capital need if pipelines convert | ~$221B | The AI pivot could become an infrastructure-scale financing cycleA |

The premium is arriving before the capacity

VanEck puts delivered AI and HPC capacity across the peer group at only about 25% of what has been leased. Wall Street is paying for contracts today and for construction outcomes the sector has not yet delivered.

The near-term funding shortfall for that construction totals roughly $50 billion across the group, with long-term capital needs climbing toward $221 billion if the full pipeline of announced projects ultimately converts into built sites.

VanEck's valuation model assumes a baseline net operating income of about $1.5 million per megawatt for AI and colocation sites and applies an enterprise value multiple of 15 times that figure.

The model also offsets the result against greenfield construction costs of roughly $10 million per megawatt, climbing to about $12 million for projects further out as construction inflation compounds.

A single megawatt implies a gross enterprise value near $22.5 million, against a pre-financing value of about $12.5 million after capex, before any probability discount for delivery risk or financing costs is applied.

| Input | Assumption | Implied value |

|---|---|---|

| Net operating income per MW | ~$1.5M | Starting cash-flow base |

| Enterprise value multiple | 15x | Converts NOI into asset value |

| Gross enterprise value per MW | $1.5M × 15 | ~$22.5M |

| Greenfield construction cost | ~$10M/MW | Baseline capex deduction |

| Pre-financing value after capex | $22.5M – $10M | ~$12.5M |

| Further-out project capex | ~$12M/MW | Lower implied equity value if costs rise |

| Main sensitivity | Capex, timing, tenant quality | Small changes can materially alter shareholder upside |

Pushing the capex per megawatt up by a few million dollars, or stretching the delivery timeline by a year, and the equity value attached to that megawatt moves by a proportionally large amount.

VanEck's framework treats a megawatt leased to an investment-grade hyperscaler as supportable at an effective cost of capital between 6% and 10%. A similar megawatt leased to a smaller GPU cloud tenant can warrant a discount rate above 10%, the cost of capital growing directly with tenant risk.

A signed lease and an energized megawatt carry different values once the tenant's balance sheet is factored in. The same power, sold to a weaker counterparty, commands a smaller premium.

Financing the shortfall without giving away the upside

Closing a $50 billion near-term shortfall pulls miners toward financing tools drawn from infrastructure and project finance.

Project finance and debt bring fixed obligations onto balance sheets built around volatile mining margins. Bitcoin treasury sales convert an asset some miners spent years accumulating into construction capital, undercutting the original thesis that drew Bitcoin-focused investors into the stock in the first place.

Strategic partnerships and tenant prepayments offer a softer path, but they typically come with terms that shift a portion of the AI-era upside away from existing shareholders and toward whichever partner supplies the capital.

The International Energy Agency projects that global data center electricity consumption will roughly double from about 485 terawatt-hours in 2025 to around 950 terawatt-hours by 2030, with AI-specific data center consumption tripling over the same period.

McKinsey estimates that global data center spending could reach about $7 trillion by 2030, with roughly $5.2 trillion directed toward AI-capable facilities.

KKR's recently launched $10 billion AI infrastructure venture with Nvidia, and Vistra shows large financial institutions treating power-backed AI capacity as its own asset class, with capital scaling at a pace that matches the size of the opportunity miners are chasing.

Bitcoin's shadow hasn't lifted

The market continues to price miners based on Bitcoin's daily swings, even as VanEck's framework describes a business model migrating toward AI leases.

The peer group's average one-year weekly beta to Bitcoin is near 1.05, meaning the typical mining stock still moves in near lockstep with Bitcoin's price, even as its underlying cash flow story shifts toward AI leases.

Meaningful Bitcoin treasury exposure, the kind that would justify that beta, is concentrated in a handful of names.

| Company / group | BTC holdings as % of market cap | What it suggests |

|---|---|---|

| MARA | ~51% | Still meaningfully tied to Bitcoin treasury value |

| CLSK | ~24% | BTC exposure remains material |

| RIOT | ~11% | Some BTC balance-sheet linkage |

| HUT | ~7% | Limited but visible BTC exposure |

| Most other peers | ~1% or less | BTC beta may overstate actual balance-sheet exposure |

| Peer-group average beta to BTC | ~1.05 | Stocks still move almost one-for-one with Bitcoin |

MARA holds Bitcoin worth about 51% of its market cap, CLSK around 24%, RIOT near 11%, and HUT roughly 7%, while most peers hold Bitcoin at 1% or less of their market cap.

AI-focused winners can trade too cheaply during a Bitcoin selloff, while pipeline-heavy laggards can trade too richly whenever Bitcoin rallies.

VanEck's governance scorecard evaluates insider ownership, management KPIs, executive compensation structure, leadership tenure, and related-party transactions, and finds no company in the group scoring close to a perfect mark, with HIVE and BTDR ranking lower on the relative scale.

Funding tens of billions of dollars in AI infrastructure requires investors to trust management teams with capital budgets several orders of magnitude larger than anything a mining-era balance sheet previously demanded.

Governance gaps carried little consequence in a hash-rate business, and real weight in one that sells power to hyperscalers under long-dated contracts.

Two paths from contract to cash flow

A bull case for the sector is that miner valuations migrate toward the framework already used for data-center REITs and infrastructure landlords.

Hyperscaler demand for power-dense, interconnection-ready sites stays intense, financing markets open up for creditworthy projects, and the miners furthest along in construction begin reporting delivered megawatts and recurring lease revenue.

Multiple-on-delivered capacity holds near or above the 10x level that VanEck already observes, and the premium the market assigned early is validated by the cash flow that eventually follows.

A bear case has the funding shortfall resolved through dilution, as construction costs climb past the $10 million-per-megawatt baseline due to rising labor, equipment, and grid interconnection expenses.

Debt gets priced for a sector with limited operating history as an infrastructure landlord, pushing miners toward equity issuance or Bitcoin monetization to bridge the shortfall before AI revenue materializes.

Shareholders fund the buildout, and a meaningful share of the eventual upside flows instead to lenders, strategic partners, or the buyers of newly issued equity who priced their entry after the dilution.

The test that decides which case plays out has nothing to do with the size of a miner's next AI announcement.

It comes down to delivered megawatts relative to leased megawatts, the credit quality of the tenant signing each lease, and the actual capex required per megawatt once ground is broken.

It also depends on the financing structure chosen to bridge the distance between today's cash and tomorrow's revenue, and on whether each company's governance can support capital allocation at infrastructure scale.

Wall Street has already decided these companies are worth more as AI infrastructure than as Bitcoin miners.

What remains unsettled is whether investors are paying for AI cash flow that has not yet materialized, or for a construction pipeline that still needs tens of billions of dollars before it becomes AI revenue at all.

The post Wall Street is paying up for Bitcoin miners’ AI infrastructure before most of it is built appeared first on CryptoSlate.

CryptoTicker.io

Binance is facing a major regulatory test in Europe, and the timing could not be more important for the crypto market.

According to Reuters, Binance could lose permission to serve European Union clients from next month because its MiCA license application in Greece is reportedly expected to be rejected. The report comes just before the end of the EU’s MiCA transition period, when crypto companies must secure proper authorization to continue offering services across the bloc.

For Binance, this is more than another regulatory headline. It could affect the exchange’s European operations, investor sentiment around BNB, and the way crypto users across the EU access trading, custody, and other digital asset services.

Why Is Binance EU Access at Risk?

Binance applied for a MiCA license through Greece’s Hellenic Capital Market Commission. If approved, that license would allow Binance to operate across the European Union through MiCA’s passporting system.

But Reuters reported that the application is expected to be rejected, citing people familiar with the matter. Binance, however, has said it worked with regulators for months and believes it has met the requirements for MiCA authorization. The exchange also said it plans to provide another update before the June 30 deadline.

That means the situation is still not fully finalized. Binance has not officially announced an EU shutdown, and there has not yet been a confirmed final decision from the Greek regulator. Still, the risk is now serious enough to matter for users, traders, and the broader crypto market.

What Is MiCA and Why Does It Matter?

MiCA, short for Markets in Crypto-Assets, is the European Union’s regulatory framework for the crypto industry. It is designed to create one unified rulebook for crypto companies operating across EU member states.

Instead of dealing with completely separate rules in every country, crypto asset service providers can apply for authorization in one EU member state. Once approved, they can use that license to serve clients across the wider EU through passporting.

This is why the Binance case is so important. A MiCA license is not just a local approval. It can decide whether an exchange has access to the entire EU market.

For crypto users, MiCA is meant to bring more transparency, stronger investor protection, and clearer oversight. For exchanges, it creates a stricter compliance environment where operating without authorization may no longer be tolerated.

What Could This Mean for Binance Users in Europe?

For European Binance users, the biggest question is whether services could be limited, paused, transferred, or restructured if Binance fails to secure MiCA approval in time.

At this stage, users should avoid panic because nothing has been officially confirmed as a final outcome. However, Binance may need to give clear guidance quickly if the deadline arrives without approval.

Possible outcomes include a last minute regulatory solution, a temporary transition plan, restrictions in some EU markets, or a broader restructuring of Binance’s European business. The exchange may also need to explain how it would protect user access, balances, withdrawals, and account services if the regulatory issue escalates.

The main uncertainty is not whether Binance remains a major global exchange. It is whether Binance can continue serving EU users under the new MiCA framework without disruption.

Could BNB Be Affected?

BNB could come under pressure if the Binance EU situation worsens. The token often reacts to Binance related headlines because traders associate BNB with the strength, reputation, and activity of the Binance ecosystem.

If Binance secures MiCA approval or finds a smooth regulatory solution, BNB could stabilize as uncertainty fades. But if the reported rejection becomes official and Binance announces service restrictions in Europe, the token may face renewed selling pressure.

This does not mean BNB would collapse automatically. Binance remains one of the largest crypto exchanges in the world, and its business extends far beyond Europe. However, Europe is a major regulated market, and losing access or facing uncertainty there would be a negative sentiment event.

For BNB traders, the next major catalyst is likely not only the broader crypto market. It is Binance’s next regulatory update.

Why This Story Matters Beyond Binance

The Binance MiCA issue is also important because it shows how Europe’s crypto market is changing.

For years, many crypto platforms operated across multiple jurisdictions under different national rules. MiCA is changing that model. The EU is moving toward a more formal licensing system where exchanges must meet clear requirements or risk losing access to users.

This could create a stronger divide between regulated and unregulated crypto platforms. Exchanges that secure MiCA licenses may gain credibility with users, banks, institutions, and regulators. Platforms that fail to secure approval could face user migration, liquidity pressure, or enforcement risk.

That makes this story much bigger than Binance alone. It is a test of how strict Europe will be with the world’s largest crypto companies under the new regulatory framework.

Binance EU Outlook: What Happens Next?

The next key date to watch is June 30. Binance has said it will provide another update before that deadline, which makes the coming days critical.

If Binance confirms a clear path to MiCA authorization, the market reaction could become more positive. It would remove a major uncertainty and allow the exchange to continue competing in Europe under a regulated structure.

If the reported rejection becomes official, the consequences could be more serious. Binance may have to limit services, shift users to another structure, or pause certain activities for EU clients.

For now, the safest way to frame the story is clear: Binance has not officially lost EU access yet, but its European operations are under pressure as the MiCA deadline approaches.

Final Thoughts

Binance has faced major regulatory challenges before, but MiCA is different because it affects access to the entire European Union market.

The EU is no longer only asking crypto companies to improve compliance. It is creating a licensing system where authorization determines whether platforms can legally serve users across the bloc.

For Binance, this could become one of the most important regulatory moments of 2026. For BNB, it could become a major sentiment driver. And for European crypto users, it could decide how they access one of the world’s largest exchanges in the months ahead.

SpaceX and Ethereum represent two very different bets on the future — one a stake in the most valuable private space and satellite company ever to go public, the other the leading smart-contract network underpinning most of decentralized finance. Over the past year, their performance has diverged sharply. This comparison measures each on a like-for-like basis: an Ethereum position opened one year ago versus a SpaceX position taken at its IPO, both valued against current prices.

SpaceX (SPCX) vs Ethereum (ETH): Entry Prices and Current Price Compared

The starting and current values for each asset:

- Ethereum ($ETH): ~$2,600 in mid-June 2025 → ~$1,760 today

- SpaceX (SPCX): $135 at IPO → ~$201 today

In percentage terms, that's roughly −32% for Ethereum over twelve months and +49% for SpaceX in a matter of weeks.

What Would $5,000 Invested in SpaceX vs Ethereum Be Worth Today?

Applying a $5,000 investment to each entry point makes the gap concrete.

Ethereum at ~$2,600:

- $5,000 buys ≈ 1.92 ETH

- 1.92 ETH × ~$1,760 ≈ $3,385

- Result: a loss of roughly −$1,615 (−32%)

SpaceX at $135:

- $5,000 buys ≈ 37 shares

- 37 shares × ~$201 ≈ $7,444

- Result: a gain of roughly +$2,444 (+49%)

On identical starting capital, the two positions are separated by more than $4,000 — the SpaceX holding is worth over double the Ethereum holding.

Why Did SpaceX Stock Rise So Much After Its IPO?

SPCX's outperformance reflects a combination of structural and market factors:

- Constrained access. Asian buyers and much of the retail market were excluded from the IPO allocation, leaving unmet demand to chase the stock in open trading.

- A differentiated business. Launch dominance, a clear lead in reusable rockets, and Starlink's recurring revenue give SpaceX a moat that is difficult to replicate.

- Post-IPO momentum. Record-breaking listings attract trend-driven capital, and the tokenized-equity products mirroring SPCX kept demand visible around the clock.

Why Did Ethereum's Price Fall Over the Past Year?

Ethereum's decline is a function of cycle timing rather than any breakdown in its fundamentals. ETH peaked near $4,950 in 2025 before entering a multi-month correction and consolidation phase, weighed down by tighter macro conditions, moderating institutional inflows, and a broad crypto risk-off period. An investor who entered near last year's elevated levels is therefore underwater today, even though the network continues to settle substantial value and remains central to DeFi and tokenization.

The critical variable is entry timing: an Ethereum position opened two years ago would show a gain today, whereas one opened a year ago, closer to the highs, shows a loss. Volatility cuts both ways depending entirely on the entry point.

What Are the Risks of Comparing SpaceX and Ethereum Returns?

A few factors temper the headline result:

- Unequal time frames. SpaceX produced its +49% over weeks; Ethereum's −32% spans a full year. Extrapolating a recent IPO's debut performance over a longer horizon is unreliable, as newly listed stocks are prone to sharp reversals.

- Post-IPO volatility. SPCX at ~$201 sits well above its $135 listing price and could retrace meaningfully if the initial momentum fades.

- Different asset classes. SPCX is equity in a revenue-generating company; ETH is a network asset that generates staking yield and utility rather than corporate earnings. They serve distinct roles and risk profiles within a portfolio.

- Track record versus novelty. Ethereum has weathered multiple full market cycles; SpaceX has a trading history measured in weeks.

Which Is Better Positioned for the Next Year?

Past performance and forward prospects are separate questions. SPCX has delivered the stronger return, but at ~$201 it carries elevated post-IPO risk, and a move back toward its IPO price would not be unusual for a stock that has risen this quickly. Ethereum, at ~$1,760, trades closer to historically oversold territory than to euphoria, which gives it clearer room to recover should the crypto cycle turn on easing macro conditions and renewed risk appetite.

SpaceX vs Ethereum: Which Was the Better Investment?

Measured strictly on the trades described, SpaceX is the clear winner, converting $5,000 into roughly $7,444 while the same amount in Ethereum declined to about $3,385. The decisive factors were entry price and timing rather than any inherent superiority of one asset over the other.

The broader takeaway is that returns are driven primarily by entry point, time horizon, and asset type — not by which name carries more momentum at any given moment. SpaceX was the better investment over the past year; the better investment over the next year remains an open question that depends on each asset's distinct trajectory from here.

Two of the most talked-about assets of the past year sit at opposite ends of the performance table right now. SpaceX (SPCX) just completed a record-shattering IPO and has been ripping higher ever since, while $Bitcoin — the original "number-go-up" asset — is actually well below where it traded a year ago. So if you had money to put to work, which one would have rewarded you more?

Let's run the numbers on both, using a clear apples-to-apples comparison: a SpaceX investor who bought at the IPO launch versus a Bitcoin investor who bought one year ago, both measured against today's prices.

*Investments carry risks. Trade responsibly.

SpaceX or Bitcoin: The Headline Numbers

Here's where each asset stands today versus its entry point:

- SpaceX (SPCX): IPO priced at $135, now trading at ~$201 — a gain of roughly +49% since launch.

- Bitcoin ($BTC): Trading around ~$105,000–$107,000 in mid-June 2025, now at ~$65,200 — a decline of roughly −38% over the past 12 months.

On the surface, it's not close: the SpaceX IPO buyer is sitting on a near-50% gain in a matter of weeks, while the year-ago Bitcoin buyer is deep in the red.

What $1,000 Would Have Become

Numbers feel more real in dollars. Imagine you put $1,000 into each:

SpaceX at IPO launch ($135):

- $1,000 ÷ $135 ≈ 7.4 shares

- 7.4 shares × $201 ≈ $1,489

- Profit: roughly +$489 (+49%)

Bitcoin one year ago (~$106,000):

- $1,000 ÷ $106,000 ≈ 0.00943 BTC

- 0.00943 BTC × $65,200 ≈ $615

- Loss: roughly −$385 (−38%)

Same $1,000, wildly different outcomes. The SpaceX position nearly grew by half; the Bitcoin position lost more than a third of its value. The gap between them is over $870 on a $1,000 stake.

Why SpaceX Price is up so Hard

SpaceX's debut wasn't just big — it was the largest IPO in history, opening at a ~$1.77 trillion valuation. A few forces drove SPCX higher out of the gate:

- Scarcity of access. Asian buyers and many retail investors were shut out of the IPO book, leaving unfilled demand chasing the stock in the open market.

- A unique, hard-to-replicate business. Launch dominance, Starlink's recurring revenue, and a clear lead in reusable rockets give SpaceX a moat few companies can match.

- Momentum and narrative. Hot IPOs attract trend-followers, and the tokenized-equity stack mirroring SPCX kept it in front of crypto-native traders around the clock.

Why Bitcoin Price is Down

Bitcoin's decline isn't a knock on the asset's long-term thesis — it's a reminder of its volatility. The past 12 months saw BTC hit an all-time high near $126,000 in late 2025 before a sharp retracement, dragged lower by tightening macro conditions, ETF outflows, and a months-long geopolitical conflict that crushed risk appetite. At ~$65,200, Bitcoin sits well off both its highs and its year-ago level.

The key nuance: your Bitcoin return depends enormously on when you bought. A buyer from two years ago is still comfortably in profit; the year-ago buyer who caught the top is not. That timing sensitivity is the whole story with a volatile asset.

Difference between Bitcoin and SpaceX Investment

Before crowning SpaceX, a few critical caveats matter:

- Different time frames. SPCX's +49% came in weeks; Bitcoin's −38% is over a full year. Annualizing a few weeks of a hot IPO is misleading — new listings are extraordinarily volatile and can give back gains just as fast.