Cryptocurrency Posts

Crypto Briefing

AI's rapid evolution raises concerns about autonomy and societal impact, challenging regulation and innovation balance.

The post Duncan Trussell: AI’s heartbeat detection revolutionizes search and rescue, misleading narratives fuel public misconceptions, and the risks of regulation threaten innovation | JRE appeared first on Crypto Briefing.

Bitget launched preSPAX, a token tied to SpaceXs post IPO performance, as Musks company reportedly targets a $1.75 trillion listing.

The post Bitget debuts SpaceX proxy token as Musk’s IPO target climbs above $1.75 trillion appeared first on Crypto Briefing.

Surveillance tech's weak security exposes police data to hackers, raising critical privacy and national security concerns.

The post Benn Jordan: Surveillance technology raises constitutional concerns, data aggregation threatens privacy, and profit-driven motives of data brokers endanger community safety | Jordan Harbinger appeared first on Crypto Briefing.

Balancing authenticity and industry demands challenges rising artists in the competitive world of country music.

The post Ella Langley: Artists must fight for authenticity, resilience is key to navigating public scrutiny, and balancing commercial success with artistic integrity | This Past Weekend appeared first on Crypto Briefing.

Google's AI advancements are reshaping search, moving beyond traditional interfaces to agent-based systems.

The post Sundar Pichai: Google’s transformers revolutionize search and translation, the future of search is agent-based, and speed is key to product differentiation | Cheeky Pint appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

BlackRock Posts Massive Bitcoin ETF Inflows as Morgan Stanley Debuts MSBT With Strong Early Demand

Inflows into U.S. spot Bitcoin ETFs surged Thursday, led by BlackRock’s iShares Bitcoin Trust, which pulled in $269.3 million, its strongest single-day performance in five weeks. The move followed a period of volatility tied to geopolitical tensions and reversed two straight days of net outflows across the sector.

In total, the 12 U.S. spot Bitcoin ETFs recorded $358.1 million in net inflows, signaling renewed investor demand as bitcoin trades below its recent highs, thanks to Farside data.

Fidelity Investments’ FBTC posted the second-largest inflow at $53.3 million. Morgan Stanley’s newly launched Bitcoin Trust (MSBT) brought in $14.9 million on its second day of trading, marking what the bank described as its strongest ETF debut. The firm’s digital asset leadership indicated the product represents an early step in a broader pipeline of offerings.

Other issuers also participated in the rebound. Bitwise Asset Management and ARK Invest’s 21Shares fund added $11.7 million and $4.8 million, while Franklin Templeton and VanEck each saw about $2 million in inflows.

Year to date, BlackRock’s IBIT has attracted $1.5 billion in net inflows, even as bitcoin has declined from a 2026 peak near $97,000 to around $72,100. Company executives have said the fund’s investor base skews toward long-term holders.

U.S. spot Bitcoin ETFs ended 2025 with $56.59 billion in cumulative net inflows and now stand at $56.51 billion, leaving the category about $80 million below breakeven for 2026.

Morgan Stanley launches a bitcoin ETF

Earlier this week, Morgan Stanley entered the spot bitcoin ETF market with the launch of its Bitcoin Trust (MSBT), posting strong early demand and intensifying competition across the sector.

The fund recorded about $34 million in first-day trading volume and $30.6 million in net inflows, which Morgan Stanley’s Amy Oldenburg said marked the “best first day of trading for any of our ETFs.” MSBT carries a 14 basis point fee, undercutting several rival products and adding pressure to an already competitive fee environment.

JUST IN: Morgan Stanley's Amy Oldenburg announces their spot Bitcoin ETF launch had their "best first day of trading for any of our ETFs"

— Bitcoin Magazine (@BitcoinMagazine) April 9, 2026pic.twitter.com/cqpmJYpKKk

Despite the debut, U.S. spot bitcoin ETFs saw $94 million in net outflows. Fidelity’s FBTC and Ark & 21Shares’ ARKB led redemptions, while Grayscale’s GBTC also posted losses. BlackRock’s IBIT bucked the trend with $40.4 million in inflows.

The flows highlight ongoing rotation among institutional investors amid bitcoin price volatility, with traders taking profits after the asset climbed back above $70,000.

Morgan Stanley’s entry is seen as a structural shift, leveraging its $6 trillion wealth management network and thousands of financial advisors to distribute crypto exposure more broadly. Analysts say fee compression and distribution advantages will likely shape the next phase of competition.

Inflows into MSBT will be watched to see if traditional banks can challenge ETF leaders.

This post BlackRock Posts Massive Bitcoin ETF Inflows as Morgan Stanley Debuts MSBT With Strong Early Demand first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

TD Cowen Initiates Coverage on Bitcoin Treasury Companies, Frames PBTC Sector as Investable Equity Category

TD Cowen this week initiated equity research coverage on three public Bitcoin treasury companies (PBTCs) and one Ethereum digital asset treasury, publishing proprietary valuation models and KPIs specific to the sector.

The move marks one of the more concrete steps a major bank has taken to build formal research infrastructure around Bitcoin-focused equities.

The firm’s analysts, led by Lance Vitanza, view Bitcoin as a long-term store of value — framing it in the tradition of digital gold — and project a price of roughly $140,000 by the end of 2026.

TD Cowen’s thesis holds that PBTCs, companies that accumulate Bitcoin on their balance sheets and grow holdings on a per-share basis, now constitute a distinct and “investable equity category,” distinct from both spot Bitcoin ETFs and traditional tech stocks.

Nakamoto receives a buy rating

Among the companies covered, Nakamoto Holdings (NASDAQ: NAKA) received a buy rating and a $1.00 price target, compared to its April 8 closing price of $0.21. TD Cowen’s model projects $394 million in Bitcoin gains for fiscal year 2027, applying a 2x multiple to that estimate.

Nakamoto differentiates from other PBTCs through minority stakes in international Bitcoin treasury firms — Metaplanet in Japan and Treasury BV in the Netherlands — and operating subsidiaries in media, Bitcoin advocacy, and digital asset management.

“We are initiating coverage of Nakamoto Holdings with a BUY rating and a $1.00 price target. Our PT is based on estimated BTC $ Gain of $394 million for FY27E, a 2x multiple, and a Bitcoin price of ~$140k at Dec-26,” the firm wrote.

SharpLink Gaming (SBET) and Strive (ASST) also received Buy ratings, with price targets of $16 and $26, respectively.

On Apr. 9, TD Cowen also cut its price target on Strategy to $350 from $440, citing a lower bitcoin price outlook and a reduced valuation multiple on projected gains, while maintaining a buy rating. The firm lowered its forecast for Strategy’s 2026 bitcoin gains to $7.87 billion from $10.17 billion in 2025.

The decision to initiate coverage carries weight beyond the individual ratings. When a bank formalizes research coverage of a new sector, it creates the analytical foundation that supports other business lines — wealth management, investment banking, and enterprise services — in engaging with the category.

TD Cowen’s stress on this policy cycle

TD Cowen has been vocal in recent months about digital assets’ role in the current market cycle, and the April 9 initiations represent the first instance of the firm publishing company-specific models and ratings within the PBTC space.

Back in January, the U.S. entered what TD Cowen described as a rare pro-crypto policy window, driven by aligned regulators, political momentum, and a deregulatory push under President Trump’s second term.

The firm expects 2026 reforms to come through agency action — such as SEC exemptions, tokenization initiatives, and expanded banking access — rather than sweeping legislation. It warned, however, that these gains must be finalized quickly or risk being weakened or reversed after the 2028 election.

Bitcoin Magazine is published by BTC Inc, a subsidiary of Nakamoto Inc. (NASDAQ: NAKA)

This post TD Cowen Initiates Coverage on Bitcoin Treasury Companies, Frames PBTC Sector as Investable Equity Category first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Japan Moves to Classify Bitcoin and Crypto as Financial Instruments Under New Bill

Japan has taken a decisive step toward reshaping its digital asset framework after its cabinet approved a draft amendment that would classify cryptocurrencies as financial products under the Financial Instruments and Exchange Act (FIEA).

The proposal marks a shift from Japan’s current approach, which treats crypto primarily as a payment method under the Payment Services Act. By bringing digital assets under the same legal structure as stocks and other securities, policymakers aim to align the sector with established financial market standards.

If passed during the current parliamentary session, the law could take effect as early as fiscal year 2027.

Under the proposed rules, insider trading involving crypto assets would be explicitly prohibited. Market participants would face penalties for trading on non-public information, a measure long applied in traditional finance but absent in most crypto markets. Regulators view the change as necessary to address concerns over market fairness and information asymmetry, according to reporting from Nikkei.

The bill also introduces disclosure requirements for issuers. Companies offering crypto-related products would need to publish annual reports, increasing transparency for investors and regulators. Officials say the move reflects the growing role of digital assets as investment vehicles rather than simple payment tools.

Penalties for noncompliance would rise. Operating without registration could result in prison terms of up to 10 years, compared with the current maximum of three years.

Financial penalties would increase to 10 million yen, or about $62,800. Authorities would also expand oversight powers, giving regulators broader authority to monitor trading activity and enforce rules.

Satsuki Katayama, Japan’s minister for financial services, said the reform aims to expand access to growth capital while strengthening investor protection. She noted that changes in financial markets and the rise of digital assets require a more comprehensive regulatory structure.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) April 10, 2026Japan approves bill that will regulate Bitcoin & crypto as financial instruments, Japan's Nikkei reports. pic.twitter.com/dp1O5zKR5S

Japan’s crypto initiatives

Japan has long been an early mover in crypto regulation, introducing exchange registration requirements and custody rules after a series of high-profile hacks in the past decade.

The latest proposal builds on that foundation while signaling a shift toward integrating crypto into mainstream finance.

The timing reflects both domestic and global pressures. Japan now has millions of crypto accounts, and regulators receive hundreds of fraud-related complaints each month.

At the same time, institutional interest in digital assets has increased, pushing policymakers to create clearer rules for market participants.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Japan Moves to Classify Bitcoin and Crypto as Financial Instruments Under New Bill first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Could Be Quantum-Safe Without Protocol Changes, New Proposal Claims

A new research proposal claims it can make Bitcoin transactions resistant to quantum attacks without changing the network’s core rules, a goal that has drawn attention as concerns grow over future cryptographic risks.

In a paper published on April 9, Avihu Levy of StarkWare outlined “Quantum-Safe Bitcoin Transactions Without Softforks,” introducing a scheme called Quantum Safe Bitcoin, or QSB. The design aims to protect transactions from threats posed by quantum computers while remaining compatible with the existing Bitcoin protocol.

The proposal targets a known vulnerability in Bitcoin’s current design. Standard transactions rely on ECDSA signatures over the secp256k1 curve. In theory, a sufficiently powerful quantum computer running Shor’s algorithm could potentially break this system by solving discrete logarithms, which would allow attackers to forge signatures and spend funds.

QSB replaces reliance on elliptic curve security with hash-based assumptions. Instead of trusting ECDSA, the scheme uses it as a verification mechanism while shifting security to hash pre-image resistance. This approach draws from earlier work known as Binohash, which embeds one-time signature schemes into Bitcoin Script.

JUST IN: Bitcoin developer Avihu Levy introduces "Quantum-Safe Bitcoin Transactions Without Softforks"

— Bitcoin Magazine (@BitcoinMagazine) April 9, 2026pic.twitter.com/enghEoOq10

At the core of QSB is a “hash-to-signature” puzzle. The system hashes a transaction-derived public key using RIPEMD-160 and treats the output as a candidate ECDSA signature. Only a small fraction of random hashes meet the strict formatting rules required for valid signatures, creating a proof-of-work condition. The paper estimates the probability of success at about one in ~70.4 trillion attempts.

Bitcoin resistant to quantum attacks

Because the puzzle depends on hash properties rather than elliptic curve hardness, it remains resistant to Shor’s algorithm. A quantum attacker would gain only a quadratic speedup from Grover’s algorithm, leaving meaningful security margins. The paper estimates about 118-bit second pre-image resistance under a Shor threat model.

The construction works within Bitcoin’s existing scripting limits, including a cap of 201 opcodes and a maximum script size of 10,000 bytes. It uses legacy script structures and avoids any need for consensus changes or soft forks, a feature that may appeal to developers wary of protocol fragmentation.

The transaction process unfolds in three stages, the proposal claims. First, a “pinning” phase searches for transaction parameters that produce a valid hash-to-signature output, binding the transaction to a fixed structure. Next, two digest rounds select subsets of embedded signatures to generate additional proofs tied to the transaction hash. Finally, the transaction is assembled with all required preimages and verification data.

The design introduces tradeoffs. QSB transactions exceed standard relay policy limits, which means they would not propagate across the network under default settings. Instead, they would require direct submission to miners through services such as Slipstream. The scripts also consume significant space and computational resources.

Despite these constraints, the cost of generating a valid transaction appears within reach. The paper estimates total compute expenses between $75 and $150 using cloud GPUs, with the workload scaling across parallel hardware. Early testing reports successful puzzle solutions after several hours using multiple GPUs.

The project remains incomplete. While the paper and script generation tools are finished, parts of the pipeline, including full transaction assembly and broadcast, have not been demonstrated on-chain.

Still, the proposal adds to a growing body of research exploring how Bitcoin could adapt to a future with quantum computing. By avoiding protocol changes, QSB presents one path that relies on existing rules rather than consensus upgrades, a direction that may shape further debate on long-term network security.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Bitcoin Could Be Quantum-Safe Without Protocol Changes, New Proposal Claims first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Strategy’s (MSTR) Bitcoin Ambition Is Reshaping Corporate Finance. Everyone Else Is Falling Behind

The bitcoin numbers from March are hard to ignore and are bullish at first glance. Public and private companies collectively added 47,435 BTC to their treasuries last month — worth roughly $3.2 billion at month-end prices — but strip away one name from the ledger and the picture shifts dramatically.

Nearly every one of those coins was bought by Michael Saylor’s Strategy. Everyone else, collectively, is in retreat, according to bitcointreasuries.net March report shared with Bitcoin Magazine.

That divergence is becoming the defining story of corporate Bitcoin adoption in 2026. Strategy purchased 44,377 BTC in March alone, including one of its largest-ever single-week purchases — 22,337 BTC disclosed on March 16, funded by $1.57 billion in ATM sales from its STRC preferred shares and MSTR common stock.

The company now controls two-thirds of all Bitcoin held by public companies, and its holdings sit at roughly 762,000 BTC with a plausible, if aggressive, path to 1 million.

STRC is helping Strategy build an accumulation machine

To understand how Strategy keeps buying at this scale in what BitcoinTreasuries.net describes as “a bear market,” you have to understand STRC — the company’s variable-rate perpetual preferred share product.

STRC targets a price near $100 and currently yields approximately 11.5% annually, reset monthly. It sits above common shareholders in Strategy’s capital structure, offering more predictable returns than MSTR stock while still being anchored to the Bitcoin treasury underneath.

March was a watershed moment for the instrument. STRC recorded its highest-ever single-day trading volume on March 12 — $746 million — followed by its second-highest on March 31, at $522 million. Weekly volumes hit $2.27 billion from March 9–13 alone. That demand didn’t just set records; it funded Bitcoin buying.

Strategy’s 8-K for the week of March 9–15 reported $1.2 billion in STRC ATM proceeds and $396 million in MSTR proceeds, together financing that record 22,337 BTC purchase.

Now Strategy has filed for a new $42 billion ATM program, split evenly between STRC and MSTR, plus an additional $2.1 billion in STRK. According to BitcoinTreasuries.net modeling, if proceeds arrive at a rate of roughly $2.3 billion monthly over 19 months — and Bitcoin hovers near $75,000 — Strategy could reach 1 million BTC by November 2026.

A more conservative projection using Strategy’s average monthly buy rate of 21,000 BTC since January 2025 pushes that date to March 2027.

A Bitcoin leaderboard in freefall

March also triggered a major leaderboard reshuffling that reflects just how different the playbook looks outside of Saylor’s orbit. MARA Holdings — once the second-largest public Bitcoin treasury — sold 15,133 BTC, worth roughly $1.1 billion, to repurchase convertible senior notes. The sale wiped nearly 28% of its previous holdings.

As BitcoinTreasuries.net’s Tyler Rowe put it: “MARA borrowed aggressively to stack sats during the bull run and is now selling Bitcoin at a loss to service that debt. This is the precise scenario critics of debt-fueled treasury strategies have warned about.”

That opened the door for Jack Mallers’ Twenty One Capital (XXI) to move into second place, currently holding 43,514 BTC — though notably, XXI hasn’t purchased Bitcoin since August. Its rise is purely a function of MARA’s decline. Metaplanet, the Japanese firm that has become one of the most aggressive Bitcoin accumulators outside the U.S., followed in early April by acquiring 5,075 BTC to reach 40,177 BTC, leapfrogging MARA for third place.

GameStop’s story is perhaps the most unusual. The retailer-turned-crypto-treasury pledged 4,709 BTC as collateral in a covered call strategy with Coinbase Credit, leaving just 1 BTC in direct holdings.

The counterparty holds rights to sell or rehypothecate the pledged Bitcoin, though GameStop maintains a contractual right to receive an equivalent amount back. The move dropped the company from the 21st-largest Bitcoin holder to near position 190 on the leaderboard.

Public company bitcoin accumulation is stalling

Beyond the leaderboard drama, the March report surfaced a quieter but more important trend: excluding Strategy, corporate Bitcoin conviction is cooling sharply. Public companies other than Strategy aggressively accumulated last summer, but net buying has declined and outright sales have accelerated since October.

The number of monthly buyers has fallen steadily since September, reaching just 16 in March.

Ryan Strauss of the Bitcoin Consulting Group put it bluntly in the report: “What stands out to me is just how structurally dependent headline holdings growth is on Strategy — once you remove it, the underlying signal flips from strength to clear deceleration. The pullback in both net accumulation and participant count suggests this isn’t just noise, but a broad cooling in corporate conviction following last summer’s aggressive positioning.”

Among the sellers: Exodus Movement, whose Bitcoin holdings fell by an estimated 1,084 BTC as it funds its acquisition of W3C Corp; Fold Inc., down 178 BTC; and Cango Inc., down 331.3 BTC following a mining update.

A new financial ecosystem forming around STRC

What may be most significant about March isn’t the buying or selling — it’s the emerging ecosystem of financial products being built around STRC itself. At least five entities have disclosed allocations to STRC or plans to acquire it. Strive, the asset manager led by CEO Matt Cole, has committed $50 million — over one-third of its corporate treasury — calling STRC “an alternative to a USD reserve mainly made up of cash in low-yield money market funds”.

DeFi protocol Apyx, which describes itself as the first dividend-backed stablecoin, held approximately 450,000 STRC shares worth $45 million as of early April, using the yield to back its apxUSD stablecoin.

Meanwhile, mutual funds and ETFs now hold more than $2 billion in digital credit products in aggregate, with STRC alone accounting for $591 million across datasets from Capital Group, BlackRock, Fidelity, VanEck, and others.

BitcoinTreasuries.net frames this institutional on-ramp as particularly timely amid a private credit crisis in which some issuers have restricted retail fund withdrawals or capped redemptions — a structurally opaque system that, the report argues, compares unfavorably to Bitcoin-backed digital credit where collateral is on-chain and pricing is publicly visible.

Overall, the broader takeaway from March 2026: corporate Bitcoin adoption is not weakening, but it is concentrating. Strategy isn’t just the biggest player — it is increasingly the market itself, with an expanding financial architecture designed to keep accumulating regardless of where the price goes.

This post Strategy’s (MSTR) Bitcoin Ambition Is Reshaping Corporate Finance. Everyone Else Is Falling Behind first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

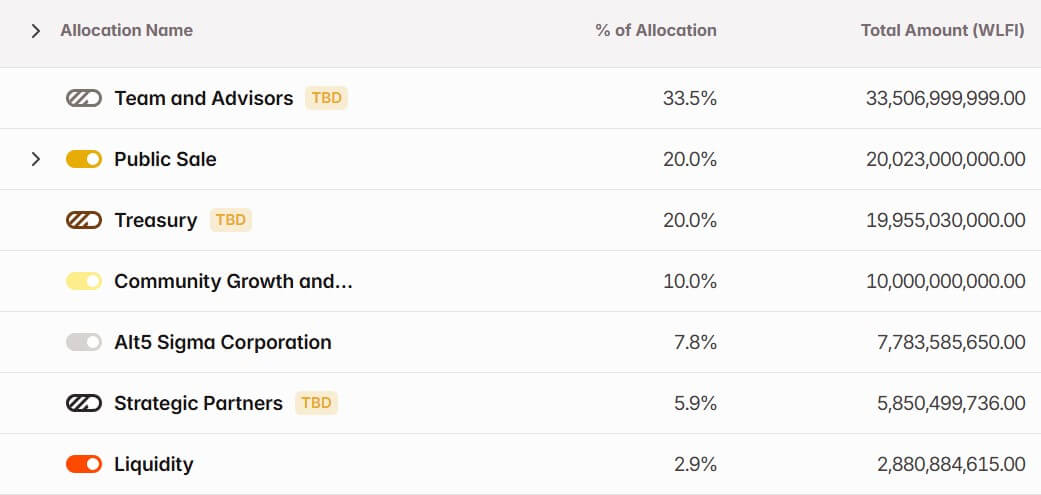

World Liberty Financial, the decentralized finance project co-founded by the Trump family, is hastily preparing to unlock a massive tranche of its WLFI tokens after a nearly two-year holding period.

The impending release will likely target a portion of the remaining 80% of public investors' allocations to the project. According to Tokenomist data, this translates to over 16 billion WLFI tokens, valued at $1.28 billion.

While the project’s leadership frames the move as a long-awaited reward for early adopters, crypto analysts and retail investors are accusing the team of using the unlock as a smokescreen to distract from a mounting liquidity crisis and questionable on-chain lending practices.

The decision to release the remaining 80% of investor allocations comes just days after early investors filed lawsuits against the protocol.

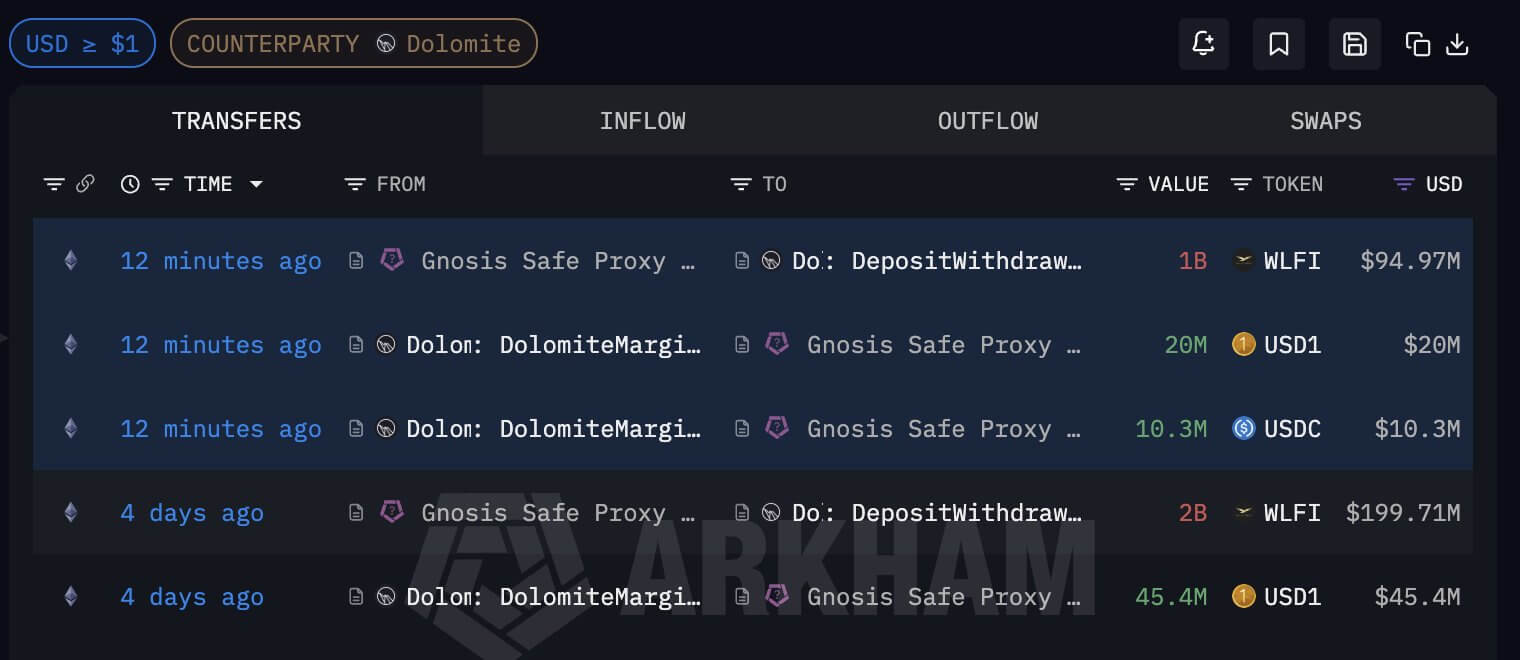

It also arrives as the project faces intense scrutiny over a massive, highly concentrated borrowing position on the DeFi lending platform Dolomite. Notably, CryptoSlate has previously reported that this position has essentially trapped millions of dollars in retail deposits.

For months, World Liberty Financial has been engaged in a continuous loop of value extraction, utilizing its own highly illiquid governance token as collateral to borrow tens of millions in stablecoins.

According to blockchain data analyzed by multiple independent researchers, the structural integrity of this debt is heavily reliant on a single, insider-controlled treasury.

Understanding WLFI's Dolomite debt trap

The controversy centers on how World Liberty Financial manages its treasury via Dolomite, a DeFi lending protocol. Dolomite’s co-founder Corey Caplan concurrently serves as a technical advisor to World Liberty Financial.

According to on-chain tracking from Arkham Intelligence and independent DeFi researchers, the WLFI team has deposited over 3 billion WLFI tokens, nominally valued at roughly $300 million, into the Dolomite.

Using this massive pile of their own token as collateral, the team has borrowed an estimated $75 million in stablecoins, including its proprietary USD1 and Circle’s USDC.

This strategy has effectively consumed the Dolomite platform. WLFI now sits at the top of Dolomite's supplied-assets list, representing more than 50% of the protocol's total value locked (TVL).

The structural concern, however, lies in Dolomite's USD1 lending pool. USD1 currently has $180 million supplied against $167.5 million borrowed, creating a staggering utilization ratio of 93%.

Because of this extreme utilization, ordinary retail depositors who lent their stablecoins to the pool, expecting to withdraw at will, are now unable to access their funds. Their capital is effectively locked until the WLFI team decides to repay its massive debt.

To entice these deposits, the pool aggressively inflated its lending rates, with yields climbing as high as 35%.

However, analysts warn that this yield was a symptom of a liquidity crisis, not organic market demand.

Yashas, a prominent DeFi educator, said:

“The 35% APR that depositors saw wasn't organic demand. It was one insider treasury consuming the entire pool… You're earning yield you can't withdraw on principal you can't access. That 35% wasn't compensation for a risk you understood. It was a price tag for a risk nobody explained to you.”

If the WLFI token, which currently suffers from incredibly thin market depth, were to experience a sharp price drop, the resulting liquidation would crash the token's price long before the collateral could be successfully unwound. The resulting bad debt would fall squarely on the retail depositors.

WLFI's “trust me bro” economics

Faced with a barrage of criticism on social media, the World Liberty Financial team dismissed concerns of a looming liquidation cascade.

In an April 9 social media post on X, the team wrote:

“We are one of the largest suppliers and borrowers on WLFI Markets. Yes, we supplied WLFI as collateral and borrowed stablecoins. No, we are nowhere near liquidation — and frankly, even if markets moved dramatically against us, we'd simply supply more collateral. That's not a risk. That's how this works.”

The team further defended its operations by pointing to its USD1 stablecoin, which it claims is generating a $159.5 million annual revenue run rate, and highlighted that it has executed $65.58 million in open-market buybacks over the last six months.

Yet, veteran crypto analysts were quick to point out that promising to “simply supply more collateral” is a historically disastrous strategy in decentralized finance.

Ethan DeFi, a digital asset analyst, called the response “pathetic,” comparing it to the catastrophic collapses of earlier crypto giants. According to the analyst, this was not the first time a team has opened a massive stablecoin loan against their illiquid shitcoin.

He pointed to 2024, when Curve Finance founder Michael Egorov borrowed nearly $100 million in stablecoins against his own CRV token, eventually saddling lending protocols with bad debt when the price crashed. Egorov repaid these debts.

Prior to that, in 2022, Sam Bankman-Fried’s bankrupt FTX borrowed massive amounts of stablecoins against its native FTT token, leaving protocols like Abracadabra Money with millions in unrecoverable debt upon FTX's collapse.

If a similar downward spiral hits WLFI, the resulting bad debt on Dolomite would likely fall directly onto the retail depositors who currently cannot exit their positions.

Is WLFI distracting the market with an unlock?

It is against this backdrop of illiquidity and insider dealing that World Liberty Financial has decided to finally unlock WLFI tokens.

The public sale of WLFI raised more than $590 million, with buyers purchasing the tokens at prices between $0.015 and $0.05.

With the token trading at $0.08, this means that early investors are technically sitting on massive, yet inaccessible, paper profits. However, their profit margins continue to shrink significantly amid the current bear market, which has seen the Trump-linked asset drop by 64% over the past year.

For context, blockchain firm Bubblemaps stated that Tron founder Justin Sun, who bought $75 million worth of WLFI and was named a project advisor, has lost an estimated $80 million as the asset's prices have slid.

As a result, early investors have reportedly begun filing lawsuits against the project's team.

In response, the protocol announced that a governance proposal to unlock the remaining tokens will be posted next week for a community vote. The team framed it as a “structured, phased approach designed with the long-term health of the ecosystem in mind.”

However, many holders are skeptical that unlocking billions of tokens into an illiquid market will do anything but crash the price.

This means that token unlocking may prove to be a hollow victory for retail investors who bought into the Trump-branded DeFi vision.

With billions in new supply preparing to hit the market and a lending protocol teetering under the weight of insider debt, the long-awaited liquidity event may end up being the very thing that breaks the ecosystem.

The post Trump’s World Liberty Financial borrows $75M against illiquid WLFI tokens with 16B token dump incoming appeared first on CryptoSlate.

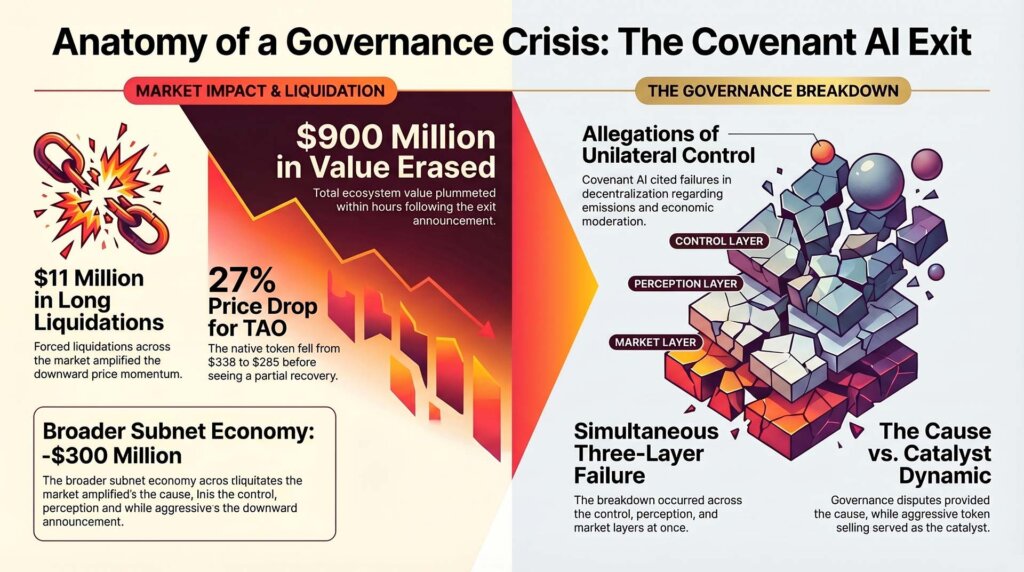

A high-profile departure from Bittensor has triggered a steep sell-off in the decentralized artificial intelligence network, wiping out nearly $900 million from its market capitalization in a matter of hours as internal disputes spill into public view.

On April 10, Covenant AI, the development team behind one of the network’s largest subnets, announced that it is abandoning the Bittensor ecosystem.

The exit of the developer who built a groundbreaking 72-billion-parameter AI model sent shockwaves through the crypto-AI sector and exposed deep ideological rifts over the network's governance.

Data from CryptoSlate showed that the price of Bittensor’s native token, TAO, plummeted 27% following the announcement, falling from $338 to a low of $285 within a two-hour window before recovering slightly to $294.

CoinGlass data also showed that the crash triggered $11 million in liquidations of long positions. Meanwhile, the collateral damage extended well beyond the core token; according to CoinGecko, over $300 million was wiped out from TAO’s broader subnet ecosystem.

Notably, the crisis abruptly halted a period of significant growth for the subnets. Over the past month, TAO has rallied 30%, driven by institutional interest and technological milestones. Just days before the crash, the network’s subnet token category boasted a combined market capitalization of over $1.5 billion.

Covenant leadership alleges Bittensor runs a ‘decentralization theatre'

At the center of the conflict are allegations of centralized control.

In a blistering statement on X, Covenant AI Founder Sam Dare accused Bittensor Co-founder Jacob Steeves, widely known in the community as Const, of operating the network as a “decentralization theatre.”

Dare wrote:

“The entire premise of Bittensor, the promise that drew builders, miners, validators, and investors into this ecosystem, is that no single entity controls it. That promise is a lie.”

Dare alleged that Steeves utilized unilateral power to reassert dominance over Covenant AI after the project grew too large to manage.

According to Dare, these actions included the sudden suspension of token emissions to Covenant's subnets, the revocation of the team's moderation capabilities over its own community channels, and the application of direct economic pressure through large, visible token sales timed to coincide with operational disputes.

Bittensor operates on a delegated structure, managed by a triumvirate that oversees a multisignature wallet for network upgrades.

However, Dare claimed this setup merely serves as a legal shield, arguing that Steeves maintains effective control and deploys network changes without decentralized consensus.

The statement reads:

“When a single actor can suspend a subnet's emissions, override an owner's authority… and use token sales as a coercive mechanism to compel compliance, that is not decentralization. It is centralized control with decentralized branding.”

Steeves has rejected these allegations on X, saying that he did not have “the ability to suspend emissions” to Covenant AI nor did he “deprecate Covenant’s channels and remove moderation rights.”

The Bittensor co-founder also stated that he sold less than 1% of what he had invested in Dare's projects.

A costly departure and ‘exit liquidity'

Despite the high-minded rhetoric regarding network governance, Covenant’s departure was marred by aggressive financial maneuvering that infuriated market participants.

Prior to the public announcement, Dare reportedly orchestrated a massive sell-off, liquidating 37,000 TAO worth of subnet alpha tokens across the Templar, Grail, and Basilica subnets.

The dump injected intense selling pressure into an already fragile market, functionally wiping out the portfolios of retail followers and investors tied to Covenant’s projects.

Crypto traders and analysts widely condemned the move as a blatant extraction of value.

The optics deteriorated further when a video on social media platform X purportedly showed Dare expressing exhaustion with the blockchain industry and a desire to “make a couple million dollars and leave.”

The juxtaposition of Dare’s governance complaints with his aggressive token dumping led to severe community backlash. Multiple users blasted the exit strategy as an egotistical and dishonorable way to settle internal network disputes, leaving retail investors to hold the bag.

A Discord spat turned into a market crash?

Inside accounts suggest the $900 million market wipeout may have stemmed from surprisingly trivial origins.

Siam Kidd, Chief Investment Officer of the Bittensor-focused DSV Fund, characterized the fallout as the culmination of an escalating interpersonal conflict rather than a genuine ideological crusade.

According to Kidd, the dispute ignited in a Discord server when Dare began deleting community messages amidst mounting user criticism. Steeves intervened by technically revoking Dare's ability to delete those messages.

This minor administrative clash reportedly escalated, prompting Steeves to sell a portion of the alpha tokens and prompting Dare to completely abandon the ecosystem.

Defending the network’s co-founder, Kidd argued that Steeves’ motives remain aligned with Bittensor’s long-term health.

He stated that “Const isn't some power-hungry troll reluctant to release control,” while brushing off the current volatility as standard “growth and teething issues” inherent to permissionless systems.

Bittensor's technical triumphs overshadowed

The acrimonious split is a major blow to Bittensor’s technical prestige as Covenant AI was not a fringe player within its ecosystem.

The project was the architect behind Subnet 3 (Templar), a decentralized training environment that essentially operated like Bitcoin mining for AI models.

Through this infrastructure, the team successfully trained Covenant-72B. Processing 1.1 trillion tokens across more than 70 independent contributors using standard consumer hardware, the project proved that decentralized, permissionless LLM training was viable.

The model achieved a 67.1 score on the standardized MMLU benchmark, putting it in direct competition with AI giants like Meta's Llama 2 70B.

This achievement drew high-profile validation from traditional tech titans. NVIDIA CEO Jensen Huang and venture capitalist Chamath Palihapitiya publicly praised the training methodology, framing it as a critical counterbalance to the proprietary models hoarded by Silicon Valley giants.

Covenant has vowed to take this technological framework with them to a new, undisclosed ecosystem.

Bittensor promises ecosystem resilience

In the wake of the crisis, Bittensor leadership is signaling a structural pivot to prevent future network destabilization.

While avoiding direct engagement with Dare’s specific accusations, Steeves announced that Bittensor will introduce “lock-based subnet ownership.”

This new framework is designed to explicitly tether a project's valuation to the long-term commitment of its development team.

Under the proposed mechanics, investors will have transparent, advanced notice if a subnet owner unlocks their tokens. This would allow the open market to proactively reprice a subnet before founders can use their communities as exit liquidity.

Furthermore, the system will allow investors to fluidly transfer their staked capital to alternative management teams. Steeves claims this will birth the first subnets that run “headless and as true commodities.”

At the same time, proponents of the network remain unfazed by the short-term market carnage as institutional interest in the project remains robust.

For context, Digital Currency Group’s Yuma continues to build across 14 different subnets. Additionally, the network is pressing ahead with plans to expand from 128 to 256 active subnets later this year, while the potential approval of a Grayscale TAO spot ETF looms.

The post Bittensor sheds $900 million in market value as key AI developer exits amid in-fighting appeared first on CryptoSlate.

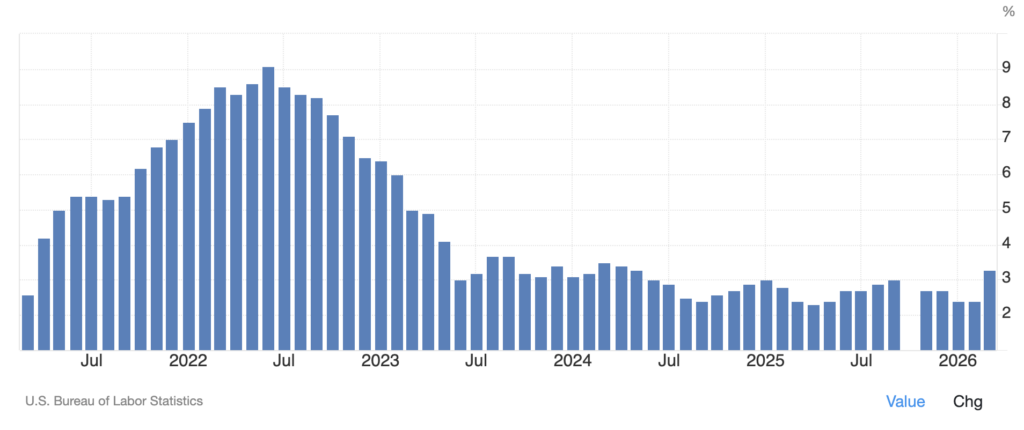

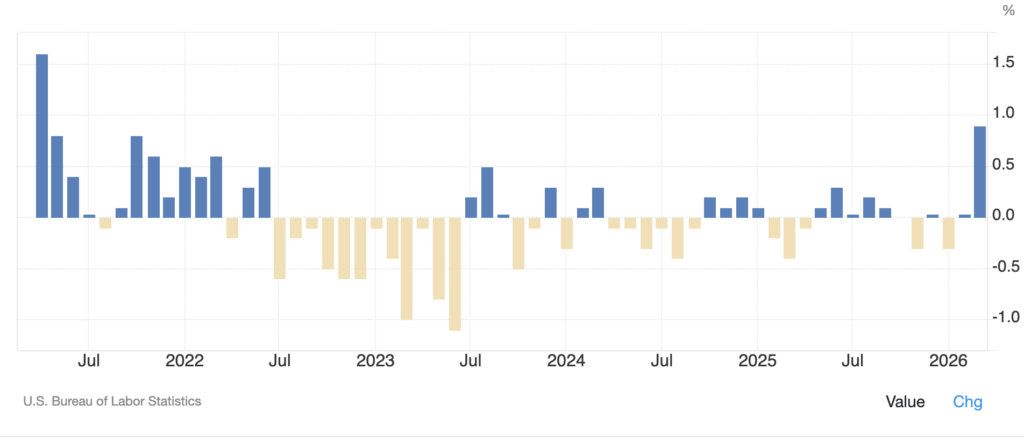

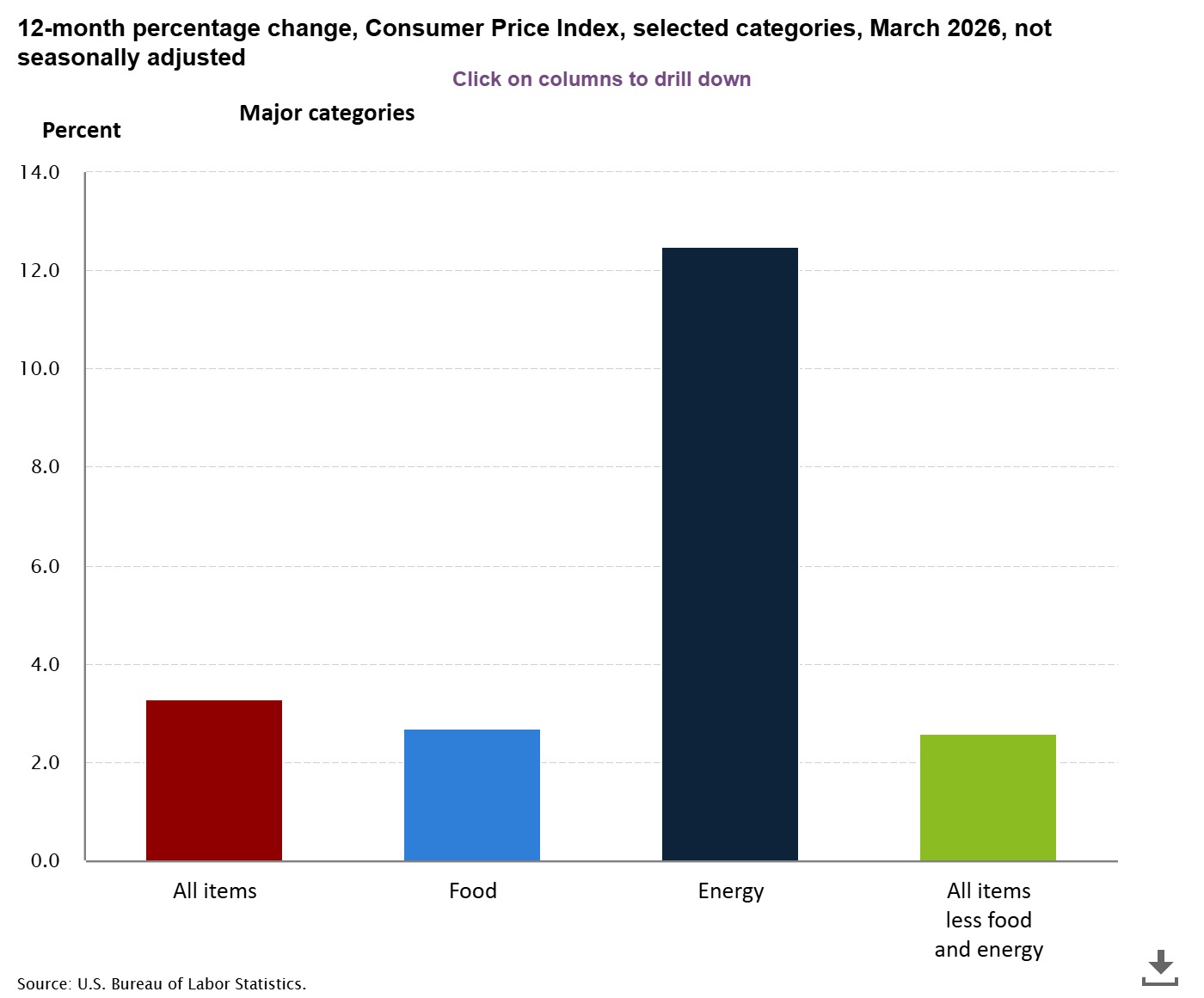

March inflation has delivered a split result with one immediate consequence. US consumer prices accelerated hard enough to keep the Federal Reserve boxed in, while the softer core reading kept the next month alive as the real test.

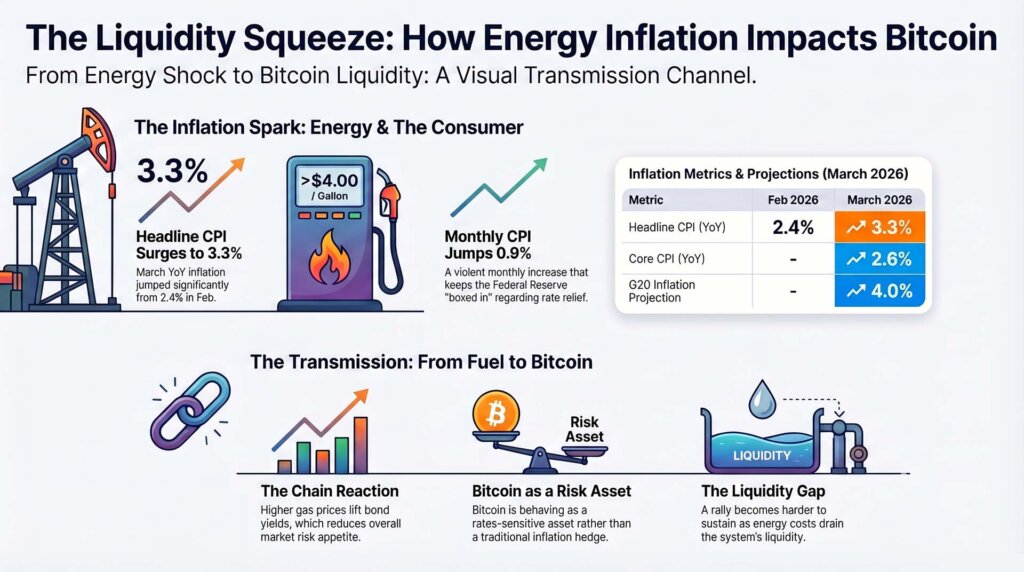

That tension reaches well beyond macro calendars. Bitcoin has spent much of 2026 trading through rates, liquidity, and the price of money. When inflation jumps because fuel prices rise, the chain reaction runs from the pump to bond yields to risk appetite, and then into crypto.

The March data shows headline CPI rose 3.3% year over year, up from 2.4% in February, while monthly CPI came in at 0.9%. Core CPI rose 2.6% year over year and 0.2% month over month.

The jump is the biggest single-month increase since March 2021.

That leaves two truths sitting side by side. Inflation jumped, and the jump still looks concentrated enough that April and May data will decide whether this was a violent energy shock or the start of something broader.

For Bitcoin, that distinction shapes the path of liquidity, the odds of rate relief, and the room for any recovery rally to keep climbing.

Inflation jumped where households feel it first, and Bitcoin feels it a step later

The easiest way to understand this print is to start outside finance. US gasoline prices pushed back above $4 a gallon in early April, after the March energy shock that followed the disruption around the Strait of Hormuz. OECD estimates already reflect that wider energy shock, with G20 inflation now projected at 4.0% in 2026, 1.2 percentage points above the group’s previous projection.

In plain English, households saw fuel costs rise first, and the CPI report caught up with what drivers already knew.

That transmission channel is where crypto enters the picture. Bitcoin can rally on inflation in the long run when the market is focused on fiat dilution, scarce supply, and the value of hard assets. In this cycle, the market has worked through a different mechanism.

Bitcoin has behaved much more like a rates-sensitive risk asset, which CryptoSlate recently noted after job revisions and softer inflation data shifted the market’s focus back to discount rates and financial conditions.

A hot CPI print, especially one driven by fuel, lifts the barrier for easier money. That raises the cost of patience for every asset that depends on looser policy and stronger liquidity conditions.

The March report sharpens that tension. Headline inflation came in hot, exactly where the household squeeze lands. Core stayed softer, which keeps the door open to a one-off shock.

For markets, the next question sits with the Federal Reserve and the next round of inflation data. For anyone holding Bitcoin, the practical implication is even simpler.

A rally that depends on easier money becomes harder to sustain when inflation surges back into the system through energy, transport, and the cost base that feeds into everything else.

That also explains why consensus offers limited comfort here. The issue lies with the level and the direction. Inflation re-accelerated. The jump was large enough to keep pressure on real yields and the broader cost of capital, even if economists were already bracing for a strong print.

CryptoSlate’s March coverage captured the same dynamic during the oil panic, when Bitcoin sold off instead of acting like a safe haven. The market treated the shock as a liquidity problem first, and the March CPI provides another layer of evidence for that interpretation.

The Fed already leaned hawkish, and this print keeps the burden of proof on disinflation

The Federal Reserve entered April with a narrow path. In the March Summary of Economic Projections, officials lifted their 2026 inflation outlook and still showed a year-end fed funds median of 3.4%, with PCE inflation at 2.7% and core PCE also at 2.7%.

That forecast carried a simple message. Inflation was expected to remain above target, and policy relief would arrive slowly, if at all. The March CPI print adds stress to that framework because it raises the risk that energy keeps inflation elevated long enough to harden the Fed’s stance.

That risk sits at the center of Bitcoin’s macro problem. When policymakers worry that energy shocks will spill into broader prices, they hesitate to ease. When they hesitate to ease, real yields stay firm, and the hurdle rate for risk stays high.

Bitcoin then has to climb with less help from the macro backdrop. CryptoSlate’s recent stagflation analysis already framed that dilemma after markets swung from expecting cuts to entertaining a far more restrictive path. March CPI keeps that pressure alive.

Core inflation offers the only immediate counterweight. A 0.2% monthly core reading and 2.6% annual core reading suggest the shock has yet to spread cleanly through the whole inflation basket. That creates a live divide between the household pain of headline inflation and the narrower policy question of persistence.

The Fed will care about whether services, wage-sensitive categories, and the broader core complex begin to re-accelerate. Bitcoin holders should care for the same reason. If March proves temporary, the market can begin rebuilding a case for easier financial conditions later in the year. If April extends the pattern, the path tightens again.

This is where the next checkpoints carry more weight than the March print alone. Upcoming BLS releases, the next PCE report, and the April 28- 29 FOMC meeting will determine whether this was a sharp energy flare or the beginning of a broader price problem.

Oil prices have already responded to ceasefire headlines and renewed doubt over whether shipping disruptions will truly ease. Oil volatility around the ceasefire keeps the data live because every move in crude feeds back into the inflation path the Fed is trying to judge.

For now, Bitcoin remains downstream from that process.

Bitcoin still has one cushion, and it now needs macro pressure to cool fast

Bitcoin entered April in better shape than the first quarter suggested. On CryptoSlate’s Bitcoin price page, in the aftermath of the inflation data release, BTC traded around $72,100, up around 1% over 24 hours, 7% over 7 days, and 4% over 30 days, while remaining 43% below its October 2025 all-time high of $126,198.

That profile tells its own story. Bitcoin has stabilized, though the recovery still leaves limited room to absorb another macro headwind without help.

The main support has come from institutional demand, which has returned after a bruising period for ETF flows. CryptoSlate documented roughly $3.8 billion in spot Bitcoin ETF outflows over five weeks, then tracked the reversal as buyers stepped back into regulated wrappers.

That shift carries real weight because the market structure around Bitcoin now leans heavily on regulated capital flows and more lightly on purely crypto-native speculation. When the ETF pipe is open, Bitcoin can absorb more macro friction. When that pipe narrows, every inflation shock cuts deeper.

That leaves Bitcoin balancing on a narrow but understandable framework. The bullish path starts with energy pressure fading, headline inflation settling, and core staying contained enough for markets to rebuild confidence in eventual policy relief.

The bearish path starts with fuel costs bleeding further into transport, services, and inflation expectations, keeping yields firm and forcing risk assets to operate under tighter financial conditions for longer. CryptoSlate’s oil analysis laid out a similar structure weeks ago, when oil above central bank assumptions raised the bar for any immediate recovery in Bitcoin.

The live question now sits with the outcome. March CPI already told the market that inflation jumped. The next layer asks whether the jump remains concentrated enough to fade or continues spreading through the economy.

For Bitcoin, that difference decides whether April becomes a reset month that restores a path back toward easier money, or another reminder that the asset is still bound to the cost of capital and the discipline of macro data.

The next readings on inflation, oil, and Fed language will decide which path gains control.

The post US inflation soars to 3.3% in largest jump since 2021 – so why did Bitcoin barely move? appeared first on CryptoSlate.

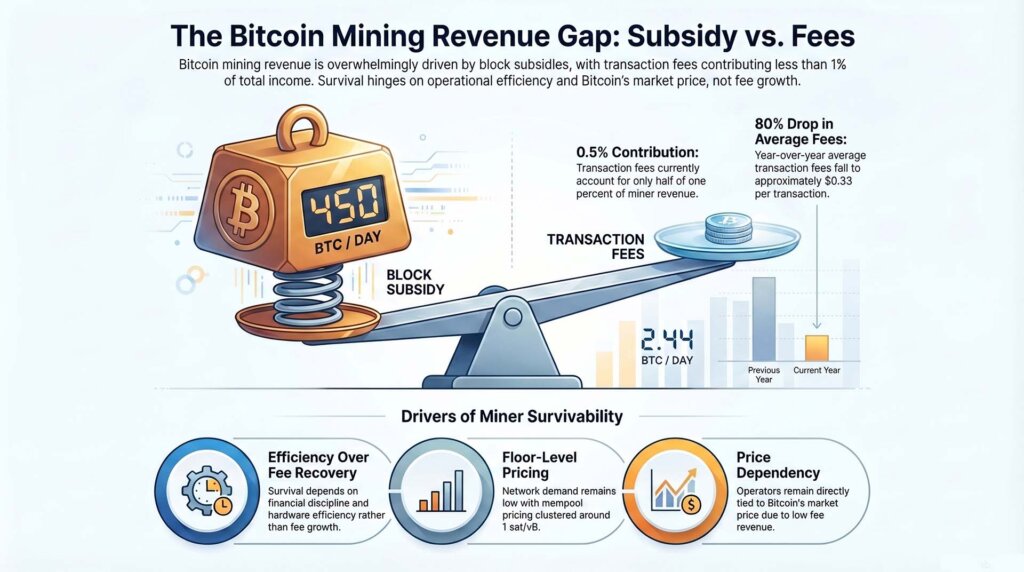

Bitcoin mining is still running on the subsidy, not demand.

That is the more useful place to start as we head into the next Bitcoin difficulty adjustment window, which CoinWarz now estimates for April 18, 2026, with difficulty projected to fall from 138.97 trillion to 132.14 trillion, a decline of 4.91%.

The schedule matters less than the structure underneath it. YCharts, using Blockchain.com data, showed daily Bitcoin transaction fees at 2.443 BTC on April 8, down 69% from a year earlier.

With the block subsidy fixed at 3.125 BTC and the network producing roughly 144 blocks a day, fees are still contributing only a sliver of miner revenue in BTC terms.

That leaves the next few weeks framed by a narrower and more useful question. If fees stay pinned near the floor, what actually determines miner survivability?

The answer starts with the revenue stack, then moves to the cost stack, then to the adaptation stack. Revenue still depends overwhelmingly on the subsidy and Bitcoin price.

Costs still depend on power, fleet efficiency, debt, and treasury policy. Adaptation depends on how much flexibility an operator has when mining alone no longer offers an attractive enough return on power and infrastructure.

The role of the coming difficulty is secondary. A lower difficulty target can ease pressure on operators by improving output per unit of hash when price and fees hold steady. In the current environment, that distinction shapes the entire operating map for miners.

Subsidy carries the revenue stack while fees stay close to the floor

Bitcoin miners get paid from two sources: the subsidy and fees. Subsidy is the protocol-level issuance attached to each block. Fees are the extra amount users pay to get transactions confirmed.

In stronger on-chain environments, the fee layer becomes a genuine contributor to miner economics. In weaker ones, it shrinks back toward irrelevance, leaving miners tied much more directly to Bitcoin's market price.

That is where conditions sit now. A recent snapshot from mempool.space showed low-, medium-, and high-priority transactions clustered around 1 sat/vB. YCharts put the average Bitcoin transaction fee at $0.3335 on April 8, down 80.53% from a year earlier. The network is still functioning smoothly, blocks are still getting mined, and users are still getting access to block space cheaply.

For miners, the revenue implication is straightforward. Fee income is providing very little incremental support. Bitcoin sits around $71,800 on April 10, up 7.4% over the past seven days and 3.1% over the past 30 days. That move helps, though mainly through the value of the subsidy rather than through any revival in user-paid demand for block space.

The scale of the imbalance is large enough to define the frame on its own. Bitcoin still produces about 144 blocks a day. At 3.125 BTC per block, that means around 450 BTC in newly issued subsidy every day before fees. Against that base, the April 8 total fee figure of 2.443 BTC suggests fees contribute roughly half of 1% of miner revenue in BTC terms.

This is why the live question is what keeps miners alive when the fee layer is barely helping. The next reset still belongs in the analysis, though it belongs in the right place.

A lower difficulty setting can improve economics at the fleet level because miners require less computational work to find a block. It can ease the pressure. Miner survivability over the next few weeks will still be determined largely by price, efficiency, power costs, debt, and treasury discipline. Power costs, machine quality, debt loads, and treasury policy decide who bends first

Once the revenue side is stripped down to subsidy plus price, the cost stack becomes much easier to see. Miner survivability depends on who can produce Bitcoin at a cost that still leaves room for operating cash flow.

That comes down to the price of electricity, the efficiency of the fleet, the cost of hosting, the level of debt on the balance sheet, and whether management has sufficient treasury flexibility to avoid selling in weak conditions.

CoinShares gives the clearest external framework for that hierarchy. In its Q1 2026 mining report, CoinShares said Q4 2025 was the toughest quarter for miners since the 2024 halving and put the weighted average public-miner cash production cost near $79,995 per BTC in Q4 2025.

That figure does give a clear sense of how narrow the spread had become across the listed space. CoinShares also said any miner below an S19 XP paying 6 cents per kilowatt-hour or more was losing money at $30 per PH/day.

That helps build a much sharper three-tier hierarchy.

The first tier is made up of low-cost operators with modern fleets, favorable hosting or self-mined power, and balance sheets that can absorb volatility without immediate forced selling.

These miners still face pressure in a low-fee market, though they have sufficient efficiency and financial flexibility to ride it out. Their problem is margin compression, not immediate survivability.

The second tier is the disciplined middle. These operators can remain viable, though only with tighter treasury management, more selective deployment, slower expansion, and a harder filter on capital spending.

They can survive the next few weeks if Bitcoin price holds up and if the projected difficulty cut lands close to current expectations. They still have much less room for error than the top tier because the fee layer is offering so little support.

The third tier is where the real strain sits. These are higher-cost legacy fleets, operators running older machines, miners with weaker power economics, and firms carrying capital structures that do not give them much time.

This group breaks first because weak fees remove the one revenue line that could have softened a difficult quarter. For them, the question is often no longer about growth. It is about curtailment, site-by-site triage, machine shutdowns, opportunistic treasury sales, and whether any part of the fleet still deserves incremental capital.

This is the operating leverage point that mining coverage often blurs. Price still matters here, although mainly as an input into hashprice and cash margins. CoinShares estimated that hashprice could rise to around $37 per PH/day if Bitcoin recovered to $100,000 and to roughly $59 per PH/day if it retested $126,000.

Those ranges show how quickly conditions can improve when the price moves far enough. They also show why the current environment still feels tight. Bitcoin has stabilized, though it remains well below the levels that would create broader comfort across the mining stack.

That leaves treasury policy as a more important variable than usual. Operators with stronger treasuries can hold through periods of weak fees and middling hashprice.

Operators with less flexibility have to decide sooner whether to sell BTC, cut capex, idle older rigs, or pull back from marginal sites. In a market where the subsidy is doing almost all the work, treasury management becomes part of the production model.

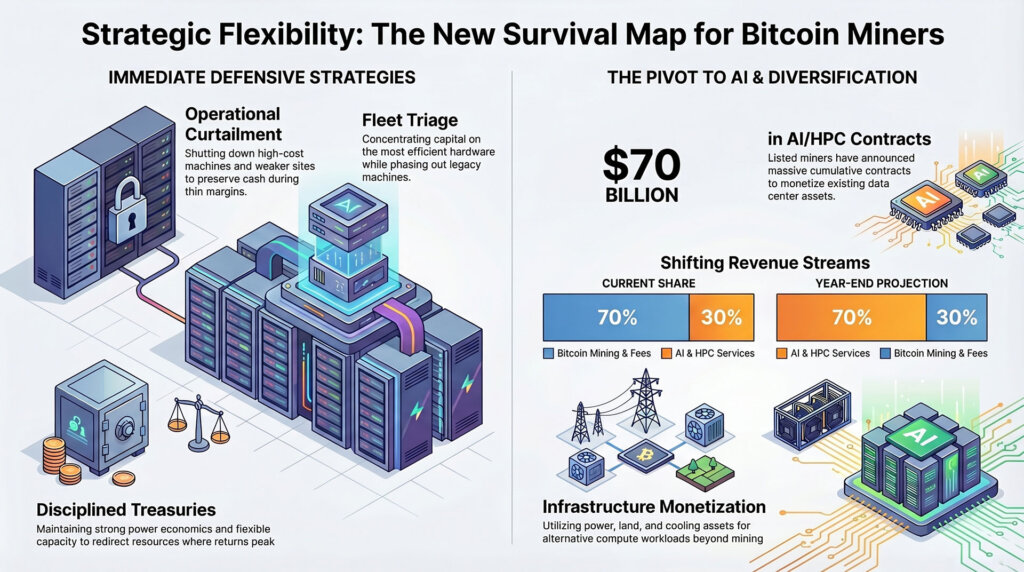

Curtailment, fleet triage, and the AI pivot define the adaptation stack into the next reset window

Once revenue stays thin and the cost stack tightens, the next question is adaptation. What do miners actually do when pure Bitcoin mining stops offering enough operating leverage?

The first adaptation is curtailment. Operators shut off higher-cost machines, reduce exposure at weaker sites, and preserve cash while waiting for better price conditions or a more favorable difficulty profile.

The second is fleet triage. Capital is directed toward the most efficient hardware and the best-performing sites, while older machines remain online only if they can still cover power and hosting costs.

The third is strategic diversification, where miners begin looking beyond Bitcoin mining itself and ask what their power, land, cooling, and data center assets might earn in adjacent markets.

In its report, CoinShares said listed miners have announced more than $70 billion in cumulative AI and HPC contracts and could derive as much as 70% of revenue from AI by year-end, up from about 30% now.

That projection says a great deal about how miners are ranking their options. A site with sufficient power access and data center potential may earn more from another workload than from mining Bitcoin in a low-fee environment.

Weak fees also lower the relative attractiveness of mining compared with other compute-intensive businesses competing for the same infrastructure footprint. A miner does not need ideological conviction to make that shift.

The next reset window still gives the market a clear near-term test. CoinWarz places the next difficulty adjustment on April 18, with the projected move pointing lower to 132.14 trillion. If that adjustment lands near expectations, miners should get some marginal relief on output economics. The sharper question comes after that. Does anything in the fee layer actually change?

A meaningful improvement would require a firmer Bitcoin price, a visible fee rebound, or both. Without a fee recovery, a lower difficulty setting still leaves miners dependent on subsidy and price.

Over the next few weeks, the winners are likely to be miners with efficient fleets, better power economics, stronger treasury control, and enough strategic flexibility to shift capacity where returns are highest.

The losers are likely to be miners that need fee support to compensate for legacy equipment, high power costs, or fragile balance sheets.

Bitcoin mining is still producing blocks on schedule, and the next difficulty adjustment may give operators some relief.

The deeper condition remains the same. Demand for block space is contributing very little, and miner survivability is being determined by who can endure a weak-fee environment long enough for either price, fees, or both to improve.

The post Bitcoin miner fees are close to zero as cost to mine nears $80,000 with difficulty about to drop 5% appeared first on CryptoSlate.

The Trump administration and the broader crypto industry have initiated an unprecedented, multi-agency pressure campaign aimed at forcing the Senate to pass the Digital Asset Market Clarity Act, signaling a decisive final push to overhaul the regulatory framework of the $2.4 trillion cryptocurrency market before the 2026 midterm elections.

In a highly synchronized effort this week, the Treasury Department, the White House Council of Economic Advisers, the Securities and Exchange Commission (SEC), and the Commodity Futures Trading Commission (CFTC) unleashed a barrage of reports, op-eds, and proposed rules.

The coordinated moves are designed to strip away the traditional banking lobby’s remaining arguments against the bill and corner the Senate Banking Committee into holding a long-delayed markup.

The overarching message from the executive branch to lawmakers is stark: The regulatory infrastructure is built, the economic risks have been debunked, and time is running out.

In an April 8 post on X, Treasury Secretary Scott Bessent said:

“Congress has spent the better part of half a decade trying to pass a framework to onshore the future of finance. It is time for the Senate Banking Committee to hold a markup and send the CLARITY Act to President Trump’s desk.”

Ripple CEO Brad Garlinghouse expressed similar support for the bill, while pointing out that “progress [was better than] perfection.”

The CLARITY Act, which passed the House with a bipartisan 294-134 vote in July 2025, has languished in the Senate for nearly a year. The primary bottleneck has been an intense lobbying war between traditional financial institutions and the digital asset industry over how the legislation treats yield-bearing stablecoins.

Banks have argued that allowing stablecoins to pay interest could trigger a massive flight of deposits, crippling traditional lending. However, the White House has moved aggressively to neutralize that narrative.

White House dismantles banking industry arguments

In a direct challenge to banking groups, the White House Council of Economic Advisers released a report concluding that stablecoin yields pose no significant threat to traditional lending.

The council estimated that banning yields on stablecoins would increase total US bank lending by just $2.1 billion. In the context of the $12 trillion US lending market, that represents a negligible 0.02% shift, with community banks projected to gain just $500 million.

Conversely, economists warned that prohibiting stablecoin yields would impose an $800 million annual welfare loss on American consumers, depriving them of interest on their digital assets.

According to the report:

“The conditions for finding a positive welfare effect from prohibiting yield are similarly implausible. In short, a yield prohibition would do very little to protect bank lending, while forgoing the consumer benefits of competitive returns on stablecoin holdings.”

The public dismantling of the bank lobby’s economic defense removes crucial political cover for Senate Republicans who have hesitated to advance the bill.

It frames the delay not as a matter of systemic economic protection, but as the entrenchment of the financial status quo at the expense of American innovation.

Notably, President Donald Trump had previously amplified the administration's stance, publicly criticizing traditional banks for obstructing the legislation. The president accused the banking sector of using the disagreements over stablecoin yields to hold both the CLARITY Act “hostage.”

Against this backdrop, James Thorne, chief marketing strategist at Wellington Altus, noted that “the entrenchment of the status quo has significantly impeded the societal integration of blockchain technology.”

He added:

“A coordinated alignment of interests between the administration and Wall Street has effectively delayed technological progress, setting back innovation by several years relative to its potential trajectory. Can we please finally get the Clarity Act passed for heaven’s sakes.”

Regulators signal readiness for CLARITY Act with ‘Project Crypto’

As the White House provided intellectual cover for the bill, the nation’s top financial market regulators moved to eliminate another frequent congressional excuse: bureaucratic unreadiness.

In separate posts on X, SEC Chair Paul Atkins and CFTC Chair Mike Selig publicly declared that their respective agencies have already laid the groundwork to implement the sweeping jurisdictional changes required by the CLARITY Act.

The legislation fundamentally alters market structure by creating a mechanism for digital assets to transition from SEC-regulated securities to CFTC-regulated digital commodities once they achieve sufficient decentralization.

“Project Crypto is designed so once Congress acts, the SEC and CFTC are ready to implement the CLARITY Act,” Atkins said Wednesday. “Secretary Bessent is right. It’s time for Congress to future-proof against rogue regulators and advance comprehensive market structure legislation to President Trump’s desk.”

Selig echoed the sentiment, explicitly framing the legislation as a necessary bulwark against future shifts in political winds. He wrote:

“It’s time to future-proof digital asset markets in America with legislation that can’t be undone by rogue regulators under a new administration. Chair Atkins and I stand ready to implement CLARITY.”

Treasury deploys the regulatory stick

While the administration dangled the carrot of market-structure clarity, it simultaneously wielded a heavy regulatory stick.

On April 8, a joint proposal from the Treasury’s Financial Crimes Enforcement Network and the Office of Foreign Assets Control outlined strict new controls for stablecoin businesses.

The rules serve as the implementation phase of the Guiding and Establishing National Innovation for US Stablecoins, or GENIUS Act, which Trump signed into law in July 2025.

The proposed framework formally classifies stablecoin issuers operating in the US as “financial institutions” under the Bank Secrecy Act. The rules mandate that issuers establish rigorous anti-money-laundering and sanctions-compliance programs, effectively turning crypto firms into bank-like gatekeepers.

Crucially, the proposal requires stablecoin issuers to engineer their tokens with the technical capability to “block, freeze, and reject” transactions that violate US law or sanctions. Issuers will also be expected to serve as active allies in FinCEN’s pursuit of entities identified as primary money-laundering concerns.

However, the Treasury Department signaled a degree of deference to the industry, noting that firms running appropriate prevention programs would generally be safe from enforcement actions absent a “significant or systemic failure.”

The timing of the FinCEN and OFAC rules is highly strategic. By aggressively tightening the leash on stablecoin issuers regarding illicit finance, the Treasury Department is demonstrating to skeptical lawmakers that the administration takes national security seriously.

Bessent said in a statement:

“This proposal will protect the US financial system from national security threats without hindering American companies’ ability to forge ahead in the payment stablecoin ecosystem.”

Without the broader market structure provided by the CLARITY Act, the stablecoin framework established by the GENIUS Act is incomplete, leaving decentralized exchanges and tokenized assets in a regulatory gray area.

Midterm pressures and global competition

Meanwhile, the administration’s full-court press is driven by a closing legislative window. With the 2026 midterm elections fast approaching, the political calendar threatens to consume congressional bandwidth. A shift in the balance of power in Congress could stall cryptocurrency legislation indefinitely.

Industry advocates warn that the United States cannot afford further delays. Nearly one in six Americans currently holds some form of digital asset, and regulatory uncertainty has actively pushed crypto development offshore to jurisdictions with clearer rules, such as Abu Dhabi and Singapore.

Jake Chervinsky, CEO of the Hyperliquid Policy Center, said:

“The CLARITY Act is the most urgent policy priority in D.C. right now. The bill has improved dramatically since the Senate Banking markup in January. If those changes hold, the bill is a ‘must pass’ for crypto. But time is short. Congress must act soon, or we’ll miss our chance.”

David Sacks, chair of the President's Council of Advisors on Science and Technology, noted that the executive branch has done its part, and the burden now rests entirely on Capitol Hill. He said:

“The GENIUS Act established US leadership on stablecoins. The CLARITY Act would do the same for all other digital assets by providing clear rules of the road…Senate Banking, and then the full Senate, should pass market structure. I’m confident that they will. And then President Trump will sign this landmark bill into law.”

Whether the Senate Banking Committee relents to the administration’s pressure campaign before election-year politics overtake the legislative agenda will determine the future of the U.S. digital asset market for years to come.

The post CLARITY Act faces White House blitz as Treasury and SEC flood Senate with coordinated pressure this week appeared first on CryptoSlate.

Cryptoticker

Pulse, a player in the health-wearable DePIN space, has officially announced it is shutting down its independent operations.

In a candid message to its community, Pulse revealed that it has entered an agreement to transition its users to the JStyle app, its OEM partner. This move marks the end of a vision that sought to reward users for health data, falling victim to the "unforgiving" capital requirements of the hardware industry and a shifting investment landscape that has pivoted toward AI.

Is Pulse Shutting Down?

Yes, Pulse is sunsetting its app and website. The company has confirmed it can no longer scale due to a lack of capital. Users have until May 14, 2026, to migrate their data and transition to the JStylePro app to maintain device functionality.

What is DePIN and Why is it Struggling?

DePIN (Decentralized Physical Infrastructure Networks) refers to protocols that use crypto-incentives to build and maintain real-world hardware networks—from WiFi routers to health sensors.

While software-based protocols can scale with minimal overhead, DePIN projects face massive "CapEx" (Capital Expenditure). They must design, manufacture, and ship physical goods. Pulse’s failure stems from a DePIN funding gap, where venture capital for physical infrastructure lagged behind the hype of liquid tokens and AI agents, leaving hardware-heavy firms with empty treasuries.

The Pivot to AI: A Case of "Too Little, Too Late"

The Pulse team admitted that they attempted to pivot toward Artificial Intelligence to capture the 2026 market momentum. However, the complexity of integrating AI into a failing hardware business proved insurmountable.

In the current crypto news cycle, projects that didn't secure long-term runway during the 2024-2025 bull run are now facing a "liquidity wall." Pulse’s experience shows that in the high-speed world of Web3, a pivot must happen before the burn rate consumes the core product.

Action Plan for Pulse Users: How to Save Your Data

If you own a Pulse wearable, the transition is mandatory to keep your device from becoming "e-waste."

Step-by-Step Transition Guide

- Firmware Upgrade: Open your existing Pulse app and install the latest firmware. This is required for compatibility with the new partner app.

- Download JStylePro: Access the new interface via the Google Play Store or Apple App Store.

- Data Export: Visit pulse.site/export immediately to download your historical health metrics.

- The Deadline: The Pulse ecosystem will be sunset on May 14, 2026. After this date, no data recovery will be possible.

Analyzing the 2026 Market: Why Companies Build and Quit

Pulse is part of a larger trend of "build and quit" cycles in the crypto space. Many projects raised significant seed rounds during the 2024 craze but failed to build a sustainable business model that didn't rely on token price appreciation.

| Factor | Challenge for Pulse & DePIN |

|---|---|

| Manufacturing | High costs and supply chain delays. |

| Funding | Investors moved from "Physical" to "AI & Agents." |

| Regulation | Increasing scrutiny on health data privacy. |

| Competition | Dominance of Bitcoin and established L1 ecosystems. |

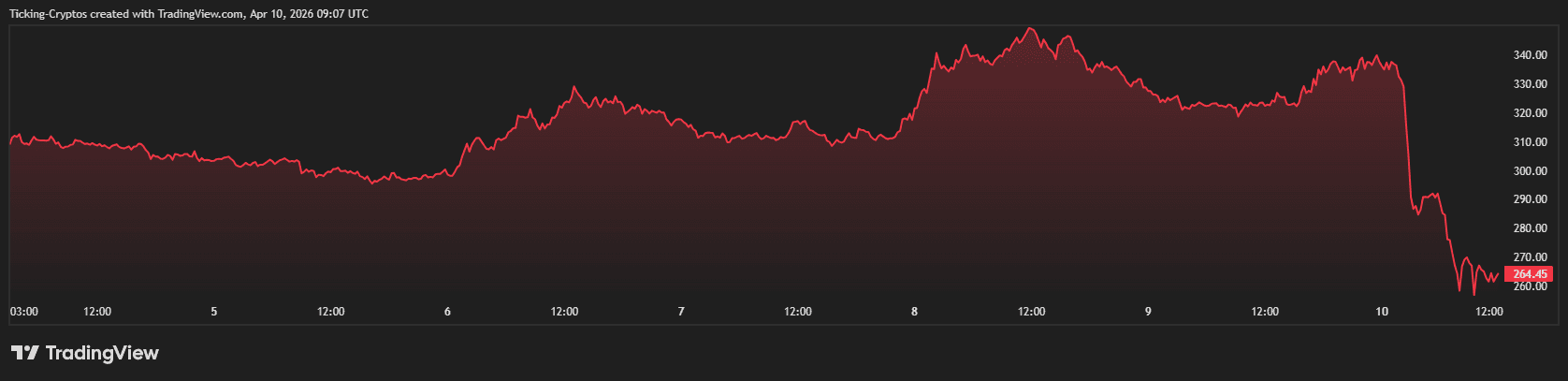

Bittensor (TAO) is currently weathering its most significant crisis to date. In a staggering 12-hour window, the TAO price crashed by 27%, effectively erasing nearly $900 million from its total market capitalization.

The sell-off was triggered by the sudden departure of Covenant AI, one of the network's most prominent contributors. This exit was not a quiet one; the team accompanied their withdrawal with a scathing critique of the protocol's governance, accusing the leadership of maintaining a "decentralized theater" while exercising absolute control.

Did TAO Price Crash?

As of April 10, 2026, the Bittensor ($TAO) price sits at $263, representing a 24-hour decline of approximately 19%. This volatility has resulted in over $9 million in TAO long positions being liquidated, as the market reacted to reports that Covenant AI offloaded 37,000 TAO tokens, valued at more than $10 million.

What is Bittensor and who is Covenant AI?

Bittensor is a decentralized machine learning protocol that allows various "subnets" to compete and provide AI services in exchange for TAO rewards. Covenant AI was the developer behind some of the most successful subnets, including Subnet 3 (Templar), which recently made headlines for training large-scale AI models on decentralized infrastructure.

Why did Covenant AI Abandon Ship

The turmoil began when Sam Dare, founder of Covenant AI, published an open letter announcing the immediate withdrawal of their three subnets: Templar, Basilica, and Grail. The decision comes after months of behind-the-scenes friction regarding how the network is managed.

According to the statement, Covenant AI alleges that:

- Centralized Control: The founder of Bittensor, Jacob Steeves (known as "Const"), reportedly holds unilateral power over emission schedules.

- Economic Sabotage: The team claims their emissions (rewards) were halted as a punitive measure during a private dispute.

- Market Manipulation: Allegations surfaced that the core team used their large token holdings to apply downward pressure on the market during negotiations.

Market Impact and Liquidations

The exit of such a pivotal player created a vacuum of confidence. According to data from CoinMarketCap, TAO fell from its weekly high near $337 to a local low of $263. This sharp move caught many leveraged traders off guard.

- Total Liquidations: ~$9.2 million (primarily longs).

- Market Cap Loss: ~$880 million in 12 hours.

- Subnet Performance: Related subnet tokens collapsed by over 55% following the news.

Should you Sell TAO Coin?

While the broader AI crypto sector has been bullish throughout early 2026, Bittensor's internal governance issues have created a "decoupling" effect. While competitors are trading on utility and growth, TAO is currently trading on reputational risk.

Investors are now questioning the "Triple Multi-sig" governance structure that Bittensor has long championed. If one of the largest subnet operators can be forced out through administrative pressure, the "decentralized" label becomes difficult to defend.

| Metric | Value (Before Crash) | Value (Current) | Change |

|---|---|---|---|

| TAO Price | $337 | $263 | -21.9% |

| Market Cap | ~$3.1 Billion | ~$2.2 Billion | -$900M |

| Long Liquidations | N/A | $9 Million | Spike |

The road ahead for Bittensor depends on two factors:

- Founder Response: Whether the Bittensor Foundation can provide transparent evidence refuting the centralization claims.

- Subnet Migration: Whether other developers follow Covenant AI's lead or stay to fill the gap left by the Templar subnet.

Japan has officially moved to recognize cryptocurrency as a financial asset. This legislative pivot marks a departure from the previous "payment instrument" classification under the Payment Services Act (PSA), transitioning oversight to the more rigorous Financial Instruments and Exchange Act (FIEA).

The move is not merely a semantic change; it is a strategic maneuver by the Japanese government to integrate digital assets into the traditional financial system. This transition aims to enhance investor protection, foster institutional entry, and significantly reform one of the world's most debated crypto tax regimes.

Japan Crypto News: A New Status for Crypto

To address the core development: Yes, the Japanese Cabinet has approved the bill to reclassify 105 cryptocurrencies—including $Bitcoin and $Ethereum—as financial assets. This bill is expected to pass through the Diet (Japan's parliament) in the second quarter of 2026, with full enforcement slated for early 2027.

From "Money" to "Investment"

Previously, Japan treated crypto as a "property value" used primarily for payments. Under the new framework:

- Old Status (PSA): Regulated as a means of payment, similar to prepaid cards or electronic money.

- New Status (FIEA): Regulated as a financial instrument, putting it on the same legal footing as stocks, bonds, and derivatives.

This reclassification allows for more sophisticated financial products, such as spot Bitcoin ETFs, to potentially gain approval in the Japanese market.

The Tax Revolution: A Flat 20% Rate

One of the most significant implications of this bill is the long-awaited reform of crypto taxation. Historically, Japan has been known for its "punitive" tax rates, where crypto gains were treated as miscellaneous income, subject to progressive rates as high as 55%.

| Feature | Current System (Miscellaneous Income) | New System (Financial Asset) |

|---|---|---|

| Tax Rate | Progressive (Up to 55%) | Flat 20% |

| Loss Carryover | Not allowed | 3-Year Carryforward |

| Separation | Combined with salary | Separate Taxation |

By treating crypto as a financial asset, investors can now offset losses against gains over a three-year period, a standard practice in the equities and stock markets.

Institutional and VC Expansion

The bill also codifies earlier initiatives allowing Japanese Venture Capital (VC) firms to hold and invest in crypto assets directly through Limited Partnerships (LPS). Previously, Japanese VCs were restricted to equity, forcing many Web3 startups to seek funding from foreign entities.

This change, supported by the Ministry of Economy, Trade and Industry (METI), is a cornerstone of Prime Minister Fumio Kishida's "New Capitalism" policy, which identifies Web3 as a pillar for Japan's future economic growth.

Market Integrity and Investor Protection

By moving under the FIEA, crypto exchanges in Japan will now be subject to:

- Strict Disclosure Requirements: Mandatory reporting for all listed tokens.

- Insider Trading Prohibitions: Applying the same anti-manipulation rules found in the stock market.

- Segregation of Assets: Strengthening the already robust requirements for holding user funds in cold storage.

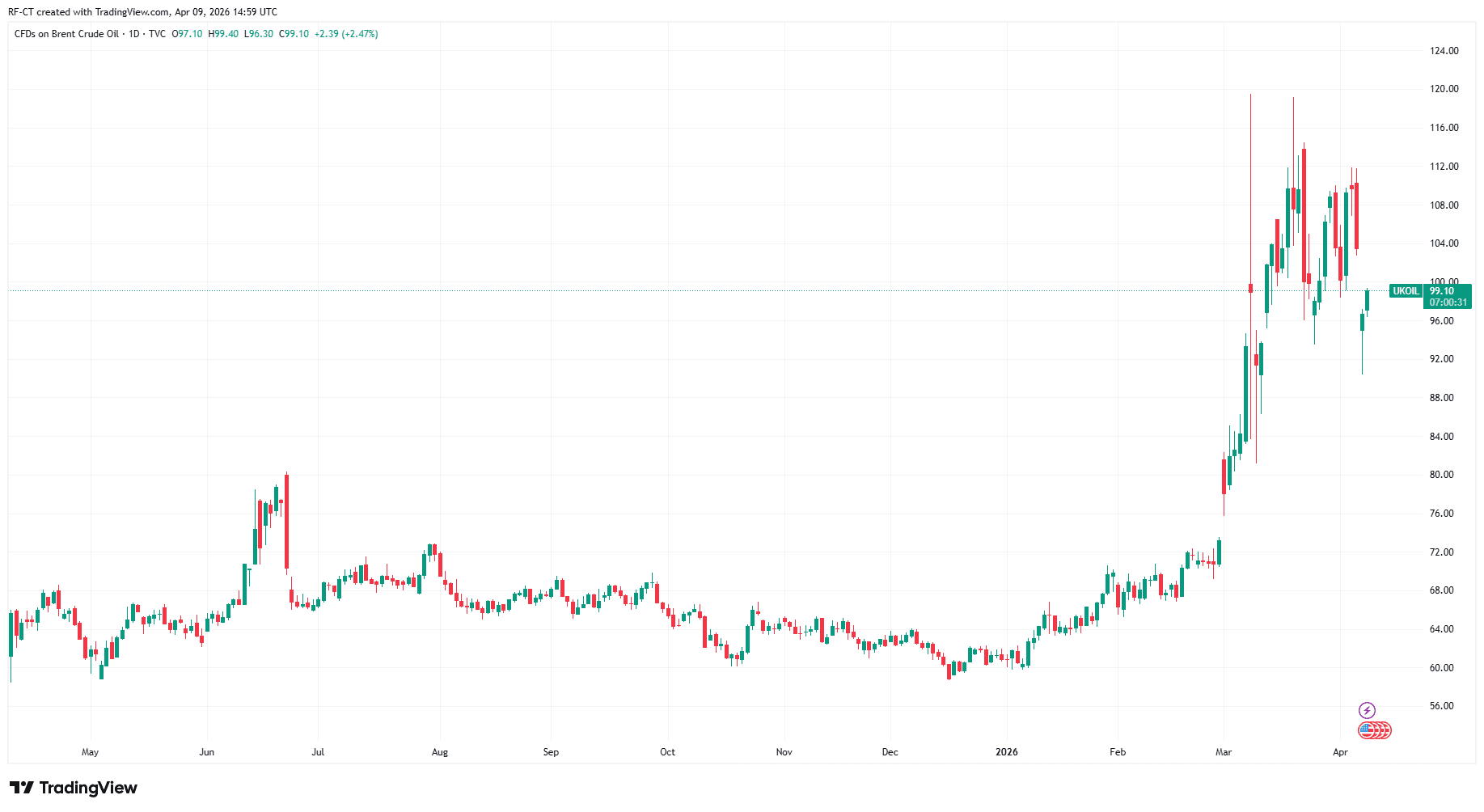

Oil Back at $100 Is Shaking Global Markets

Global markets are entering a critical phase as oil prices surge back above the $100 mark. This move is not just a headline — it is a macro shock that is already impacting equities, bonds, and crypto markets alike.

The rise in oil is driven by escalating tensions around the Strait of Hormuz, a key global energy route. Even limited disruptions are enough to tighten supply expectations and push prices higher.

👉 And crypto is reacting — but not fully yet.

Bitcoin is holding above $70,000, while Ethereum and altcoins are showing mild weakness. This suggests hesitation rather than panic — a market waiting for confirmation.

Why Oil Prices Matter for Crypto More Than Ever

At first glance, oil and crypto may seem unrelated. In reality, they are now deeply connected through macroeconomic conditions.