Cryptocurrency Posts

Crypto Briefing

Covenant AI's exit highlights the challenges of maintaining true decentralization in blockchain networks, impacting investor confidence.

The post Covenant AI exits Bittensor over centralization concerns, TAO falls 15% appeared first on Crypto Briefing.

Buyers are eyeing Geminis UK and EU units for regulatory access after layoffs, overseas retrenchment, and a stock collapse.

The post Gemini may sell parts of Europe business as buyers seek licenses: CoinDesk appeared first on Crypto Briefing.

Market uncertainty looms as Bitcoin's rally faces skepticism, with potential volatility driven by leveraged positions and macroeconomic factors.

The post Bitcoin flirts with $72K while a whale bets $80M it won’t last appeared first on Crypto Briefing.

The improbable solo mining success highlights Bitcoin's decentralization potential, despite dominance by large mining pools.

The post Solo Bitcoin miner wins $222K after beating 1 in 100,000 odds appeared first on Crypto Briefing.

Binance Wallet integrated prediction markets through Predict.fun, letting users trade event contracts with Binance balances and no gas fees.

The post Binance Wallet integrates prediction markets through Predict.fun appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Bitcoin Could Be Quantum-Safe Without Protocol Changes, New Proposal Claims

A new research proposal claims it can make Bitcoin transactions resistant to quantum attacks without changing the network’s core rules, a goal that has drawn attention as concerns grow over future cryptographic risks.

In a paper published on April 9, Avihu Levy of StarkWare outlined “Quantum-Safe Bitcoin Transactions Without Softforks,” introducing a scheme called Quantum Safe Bitcoin, or QSB. The design aims to protect transactions from threats posed by quantum computers while remaining compatible with the existing Bitcoin protocol.

The proposal targets a known vulnerability in Bitcoin’s current design. Standard transactions rely on ECDSA signatures over the secp256k1 curve. In theory, a sufficiently powerful quantum computer running Shor’s algorithm could potentially break this system by solving discrete logarithms, which would allow attackers to forge signatures and spend funds.

QSB replaces reliance on elliptic curve security with hash-based assumptions. Instead of trusting ECDSA, the scheme uses it as a verification mechanism while shifting security to hash pre-image resistance. This approach draws from earlier work known as Binohash, which embeds one-time signature schemes into Bitcoin Script.

JUST IN: Bitcoin developer Avihu Levy introduces "Quantum-Safe Bitcoin Transactions Without Softforks"

— Bitcoin Magazine (@BitcoinMagazine) April 9, 2026pic.twitter.com/enghEoOq10

At the core of QSB is a “hash-to-signature” puzzle. The system hashes a transaction-derived public key using RIPEMD-160 and treats the output as a candidate ECDSA signature. Only a small fraction of random hashes meet the strict formatting rules required for valid signatures, creating a proof-of-work condition. The paper estimates the probability of success at about one in ~70.4 trillion attempts.

Bitcoin resistant to quantum attacks

Because the puzzle depends on hash properties rather than elliptic curve hardness, it remains resistant to Shor’s algorithm. A quantum attacker would gain only a quadratic speedup from Grover’s algorithm, leaving meaningful security margins. The paper estimates about 118-bit second pre-image resistance under a Shor threat model.

The construction works within Bitcoin’s existing scripting limits, including a cap of 201 opcodes and a maximum script size of 10,000 bytes. It uses legacy script structures and avoids any need for consensus changes or soft forks, a feature that may appeal to developers wary of protocol fragmentation.

The transaction process unfolds in three stages, the proposal claims. First, a “pinning” phase searches for transaction parameters that produce a valid hash-to-signature output, binding the transaction to a fixed structure. Next, two digest rounds select subsets of embedded signatures to generate additional proofs tied to the transaction hash. Finally, the transaction is assembled with all required preimages and verification data.

The design introduces tradeoffs. QSB transactions exceed standard relay policy limits, which means they would not propagate across the network under default settings. Instead, they would require direct submission to miners through services such as Slipstream. The scripts also consume significant space and computational resources.

Despite these constraints, the cost of generating a valid transaction appears within reach. The paper estimates total compute expenses between $75 and $150 using cloud GPUs, with the workload scaling across parallel hardware. Early testing reports successful puzzle solutions after several hours using multiple GPUs.

The project remains incomplete. While the paper and script generation tools are finished, parts of the pipeline, including full transaction assembly and broadcast, have not been demonstrated on-chain.

Still, the proposal adds to a growing body of research exploring how Bitcoin could adapt to a future with quantum computing. By avoiding protocol changes, QSB presents one path that relies on existing rules rather than consensus upgrades, a direction that may shape further debate on long-term network security.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Bitcoin Could Be Quantum-Safe Without Protocol Changes, New Proposal Claims first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Strategy’s (MSTR) Bitcoin Ambition Is Reshaping Corporate Finance. Everyone Else Is Falling Behind

The bitcoin numbers from March are hard to ignore and are bullish at first glance. Public and private companies collectively added 47,435 BTC to their treasuries last month — worth roughly $3.2 billion at month-end prices — but strip away one name from the ledger and the picture shifts dramatically.

Nearly every one of those coins was bought by Michael Saylor’s Strategy. Everyone else, collectively, is in retreat, according to bitcointreasuries.net March report shared with Bitcoin Magazine.

That divergence is becoming the defining story of corporate Bitcoin adoption in 2026. Strategy purchased 44,377 BTC in March alone, including one of its largest-ever single-week purchases — 22,337 BTC disclosed on March 16, funded by $1.57 billion in ATM sales from its STRC preferred shares and MSTR common stock.

The company now controls two-thirds of all Bitcoin held by public companies, and its holdings sit at roughly 762,000 BTC with a plausible, if aggressive, path to 1 million.

STRC is helping Strategy build an accumulation machine

To understand how Strategy keeps buying at this scale in what BitcoinTreasuries.net describes as “a bear market,” you have to understand STRC — the company’s variable-rate perpetual preferred share product.

STRC targets a price near $100 and currently yields approximately 11.5% annually, reset monthly. It sits above common shareholders in Strategy’s capital structure, offering more predictable returns than MSTR stock while still being anchored to the Bitcoin treasury underneath.

March was a watershed moment for the instrument. STRC recorded its highest-ever single-day trading volume on March 12 — $746 million — followed by its second-highest on March 31, at $522 million. Weekly volumes hit $2.27 billion from March 9–13 alone. That demand didn’t just set records; it funded Bitcoin buying.

Strategy’s 8-K for the week of March 9–15 reported $1.2 billion in STRC ATM proceeds and $396 million in MSTR proceeds, together financing that record 22,337 BTC purchase.

Now Strategy has filed for a new $42 billion ATM program, split evenly between STRC and MSTR, plus an additional $2.1 billion in STRK. According to BitcoinTreasuries.net modeling, if proceeds arrive at a rate of roughly $2.3 billion monthly over 19 months — and Bitcoin hovers near $75,000 — Strategy could reach 1 million BTC by November 2026.

A more conservative projection using Strategy’s average monthly buy rate of 21,000 BTC since January 2025 pushes that date to March 2027.

A Bitcoin leaderboard in freefall

March also triggered a major leaderboard reshuffling that reflects just how different the playbook looks outside of Saylor’s orbit. MARA Holdings — once the second-largest public Bitcoin treasury — sold 15,133 BTC, worth roughly $1.1 billion, to repurchase convertible senior notes. The sale wiped nearly 28% of its previous holdings.

As BitcoinTreasuries.net’s Tyler Rowe put it: “MARA borrowed aggressively to stack sats during the bull run and is now selling Bitcoin at a loss to service that debt. This is the precise scenario critics of debt-fueled treasury strategies have warned about.”

That opened the door for Jack Mallers’ Twenty One Capital (XXI) to move into second place, currently holding 43,514 BTC — though notably, XXI hasn’t purchased Bitcoin since August. Its rise is purely a function of MARA’s decline. Metaplanet, the Japanese firm that has become one of the most aggressive Bitcoin accumulators outside the U.S., followed in early April by acquiring 5,075 BTC to reach 40,177 BTC, leapfrogging MARA for third place.

GameStop’s story is perhaps the most unusual. The retailer-turned-crypto-treasury pledged 4,709 BTC as collateral in a covered call strategy with Coinbase Credit, leaving just 1 BTC in direct holdings.

The counterparty holds rights to sell or rehypothecate the pledged Bitcoin, though GameStop maintains a contractual right to receive an equivalent amount back. The move dropped the company from the 21st-largest Bitcoin holder to near position 190 on the leaderboard.

Public company bitcoin accumulation is stalling

Beyond the leaderboard drama, the March report surfaced a quieter but more important trend: excluding Strategy, corporate Bitcoin conviction is cooling sharply. Public companies other than Strategy aggressively accumulated last summer, but net buying has declined and outright sales have accelerated since October.

The number of monthly buyers has fallen steadily since September, reaching just 16 in March.

Ryan Strauss of the Bitcoin Consulting Group put it bluntly in the report: “What stands out to me is just how structurally dependent headline holdings growth is on Strategy — once you remove it, the underlying signal flips from strength to clear deceleration. The pullback in both net accumulation and participant count suggests this isn’t just noise, but a broad cooling in corporate conviction following last summer’s aggressive positioning.”

Among the sellers: Exodus Movement, whose Bitcoin holdings fell by an estimated 1,084 BTC as it funds its acquisition of W3C Corp; Fold Inc., down 178 BTC; and Cango Inc., down 331.3 BTC following a mining update.

A new financial ecosystem forming around STRC

What may be most significant about March isn’t the buying or selling — it’s the emerging ecosystem of financial products being built around STRC itself. At least five entities have disclosed allocations to STRC or plans to acquire it. Strive, the asset manager led by CEO Matt Cole, has committed $50 million — over one-third of its corporate treasury — calling STRC “an alternative to a USD reserve mainly made up of cash in low-yield money market funds”.

DeFi protocol Apyx, which describes itself as the first dividend-backed stablecoin, held approximately 450,000 STRC shares worth $45 million as of early April, using the yield to back its apxUSD stablecoin.

Meanwhile, mutual funds and ETFs now hold more than $2 billion in digital credit products in aggregate, with STRC alone accounting for $591 million across datasets from Capital Group, BlackRock, Fidelity, VanEck, and others.

BitcoinTreasuries.net frames this institutional on-ramp as particularly timely amid a private credit crisis in which some issuers have restricted retail fund withdrawals or capped redemptions — a structurally opaque system that, the report argues, compares unfavorably to Bitcoin-backed digital credit where collateral is on-chain and pricing is publicly visible.

Overall, the broader takeaway from March 2026: corporate Bitcoin adoption is not weakening, but it is concentrating. Strategy isn’t just the biggest player — it is increasingly the market itself, with an expanding financial architecture designed to keep accumulating regardless of where the price goes.

This post Strategy’s (MSTR) Bitcoin Ambition Is Reshaping Corporate Finance. Everyone Else Is Falling Behind first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Stacked (formerly Lightning Pay) launches self-custodial Lightning wallet as New Zealand’s last major non-custodial Bitcoin exchange

Formerly known as Lightning Pay, Stacked may be the only Bitcoin exchange left standing after a series of mergers and bankruptcies in the New Zealand crypto industry. Doubling down on their vision to make Bitcoin “useful as money,” they just launched a self-custodied Lightning wallet.

Found at StackedBitcoin.com, the company has taken a different path than larger exchanges in the country, which, according to Simon, co-founder and CRO of Stacked, are going all-in on selling custodial and paper bitcoin. Exchanges like Sharesies are built following the Robinhood model, with no path to withdraw crypto to self-custodied wallets. While EasyCrypto, a popular swap exchange that received user fiat and sent crypto back to user wallets — similar to the Bull Bitcoin model — was recently bought out by SwyFTX and shut down, funneling its userbase to the parent custodial exchange.

Stacked, a 4-person company that’s seen significant growth in the country in recent years, believes this is the wrong direction for the local Bitcoin industry, and as such has launched a self-custodied Bitcoin and Lightning wallet that complements their own swap exchange offering. Users send fiat to Stacked and receive Bitcoin into their self-custodied wallet of choice. They can also pay utility bills or even their rent with Bitcoin through Stacked, who settle out the fiat recipients via New Zealand’s innovative Open Banking payments framework.

launches self-custodial Lightning wallet as New Zealand’s last major non-custodial Bitcoin exchange 1")

launches self-custodial Lightning wallet as New Zealand’s last major non-custodial Bitcoin exchange 2")

launches self-custodial Lightning wallet as New Zealand’s last major non-custodial Bitcoin exchange 3")

The Stacked wallet, which features a sleek and modern design, uses Breez and Spark SDKs in the back end to provide users a stable and easy-to-use Bitcoin experience, with full Lightning Network integration. The app lets users purchase Bitcoin manually and on a schedule via Autostack a DCA style set it and forget it purchase feature. Users can also manage contacts in the app to pay with bitcoin on their end and deliver fiat to recipients. The country has no capital gains tax; instead, Bitcoin profits are taxed as income, resulting in what may be a much more favorable regulatory environment for hyper Bitcoinization.

Stacked has been focusing its efforts to make Bitcoin useful as money in the Bitcoin Basin, a growing circular economy in Queenstown, New Zealand, which boasts around Bitcoin-accepting merchants to date. The company has created a dedicated website for the community and hosts regular events in the area, encouraging the local bitcoin economy.

launches self-custodial Lightning wallet as New Zealand’s last major non-custodial Bitcoin exchange 4")

In the 2025 financial year, 227,000 New Zealanders were identified as unique cryptoasset users partaking in around 7 million transactions. Local cryptocurrency exchange volumes reached approximately NZ$7.8 billion. Stacked projects the local digital asset market will to generate revenue exceeding US$200 million in 2026. Nearly 50% of New Zealanders are current or prospective Bitcoin and digital asset investors, according to 2024 research by Protocol Theory.

This post Stacked (formerly Lightning Pay) launches self-custodial Lightning wallet as New Zealand’s last major non-custodial Bitcoin exchange first appeared on Bitcoin Magazine and is written by Juan Galt.

Bitcoin Magazine

Tim Draper Confirmed as a Bitcoin 2026 Speaker

Tim Draper has been officially confirmed as a speaker at Bitcoin 2026. The founder of Draper Associates, DFJ, and the Draper Venture Network, Draper is one of the longest-standing and most vocal Bitcoin advocates in the venture capital world and one of the few investors who put real money behind the asset before it was widely taken seriously.

In June 2014, Draper made headlines by winning the U.S. Marshals auction of nearly 30,000 bitcoins seized from the Silk Road marketplace, spending approximately $19 million at a price of around $600 per coin. The bet has aged well. Draper has since invested in over 50 crypto companies, leading investments in Coinbase, Ledger, Tezos, and Bancor, among others. More recently, Draper led a $2.5 million pre-seed funding round in Ark Labs, a Bitcoin scaling startup building payment infrastructure, stating that “soon many people around the world will live on the Bitcoin standard.”

Draper Associates manages $2 billion in assets and has seeded some of the most valuable companies in history, including Tesla, SpaceX, Skype, Baidu, Coinbase, and Robinhood. His price conviction on Bitcoin remains intact. In a recent interview, Draper reiterated his $250,000 Bitcoin price target, rooted in the view that Bitcoin is in the middle of replacing the financial system itself describing it as infrastructure where contracts, payments, and ownership all move onchain without the layers of intermediaries that define today’s economy.

With over a decade of conviction behind him, Draper takes the Bitcoin 2026 stage as one of the asset’s earliest and most consistent voices, having put real money behind Bitcoin long before it was considered a credible institutional bet. Hear more from Tim Draper at Bitcoin 2026 taking place April 27–29 at The Venetian Resort in Las Vegas.

Bitcoin 2026 is Returning to Las Vegas

Bitcoin 2026 will take place April 27–29 at The Venetian, Las Vegas, and is expected to be the biggest Bitcoin event of the year.

Focused on the future of money, Bitcoin 2026 will bring together Bitcoin builders, investors, miners, policymakers, technologists, and newcomers from around the world. The event will feature a wide range of pass types, including general admission passes designed specifically for those new to Bitcoin, alongside premium passes for professionals, enterprises, and institutions.

With multiple stages, immersive experiences, technical workshops, and headline keynotes, Bitcoin 2026 is designed to serve both first-time attendees and long-time Bitcoiners shaping the next era of global adoption.

Past Bitcoin Conferences in the U.S.

Bitcoin’s flagship conference has scaled dramatically over the past five years:

- 2021 – Miami: 11,000 attendees

- 2022 – Miami: 26,000 attendees

- 2023 – Miami: 15,000 attendees

- 2024 – Nashville: 22,000 attendees

- 2025 – Las Vegas: 35,000 attendees

Get Your Bitcoin 2026 Pass

Get Your Bitcoin 2026 Pass

Bitcoin Magazine readers can save 10% on Bitcoin 2026 tickets using code ‘ARTICLE10‘ at checkout.

Stay at The official hotel of Bitcoin 2026, The Venetian, and get a guaranteed low rate plus 15% off your pass. Be in the middle of where the fun is all happening, and where the networking never ends.

And don’t forget:

Volunteer at Bitcoin 2026 and get Pro Pass access plus exclusive perks.

All students ages 13+ can apply for a Student Pass and get free general admission access to Bitcoin 2026.

For more information and exclusive offers, visit the Bitcoin Conference on X here.

Why Attend Bitcoin 2026?

Bitcoin 2026 is the definitive gathering for anyone serious about the future of money. With 500+ speakers, multiple world-class stages, and programming spanning Bitcoin fundamentals, open-source development, enterprise adoption, mining, energy, AI, policy, and culture, the conference brings every corner of the Bitcoin ecosystem together under one roof.

From headline keynotes on the Nakamoto Stage to deep technical sessions for builders, institutional strategy discussions for enterprises, and beginner-friendly Bitcoin 101 education, Bitcoin 2026 is designed for everyone—from first-time attendees to the leaders shaping Bitcoin’s global adoption.

Whether you’re looking to learn, build, invest, network, or influence, Bitcoin 2026 is where Bitcoin’s next chapter is written.

Bitcoin 2026 Pass Types: Something for Everyone

Bitcoin 2026 offers a range of pass options designed to meet the needs of newcomers, professionals, enterprises, and high-net-worth Bitcoiners alike.

Bitcoin 2026 General Admission Pass

Ideal for newcomers and those looking to experience the heart of the conference.

- Limited access on Days 2 & 3

- Entry to Main Stage

- Access to Genesis Stage

- Full access to the Expo Hall

Bitcoin 2026 Pro Pass

Designed for professionals, operators, and serious Bitcoin participants.

Includes all General Admission features, plus:

- Full 3-day access, including Pro Day

- Entry to the Pro Pass Reception

- Access to Enterprise Hall, Enterprise Stage, and Networking Lounge

- Conference App networking features

- Access to the Bitcoin For Corporations Symposium

- Entry to Compute Village and Energy Stage

- Complimentary lunch, coffee, tea, and snacks

- Dedicated registration and check-in

- Reserved seating at Main Stage

- Huge savings when you bundle your hotel and Pro Pass

Bitcoin 2026 Whale Pass

Bitcoin 2026 Whale Pass

The all-inclusive, premium Bitcoin 2026 experience.

Includes all Pro Pass features, plus:

- Reserved seating at Main Stage

- All-inclusive gourmet food and beverages

- Entry to Whale Night and Whale Reception

- Access to all official after-parties

- Networking app access to connect with other Whales

- Premium access to The Deep — an exclusive networking lounge with intimate speaker sessions

- Complimentary stay at The Venetian when you bundle your whale pass and hotel (use promo code ‘WHALEHOTEL’ here)

This is the most immersive way to experience Bitcoin 2026.

Bitcoin 2026 After Hours Pass

Bitcoin 2026 After Hours Pass

Your ticket to the night.

Most deals are done with a drink in your hand. Get exclusive access to 3 official Bitcoin 2026 after-parties across Las Vegas — each with a 2-hour open bar — where the real conversations happen and the best connections are made.

- Access to 3 official Bitcoin 2026 after-parties

- 2-hour open bar at each event

- Evening events across Las Vegas, April 27–29

- Network with Bitcoiners, builders, and industry leaders after hours

More headline speaker announcements are coming soon.

Don’t miss Bitcoin 2026.

This post Tim Draper Confirmed as a Bitcoin 2026 Speaker first appeared on Bitcoin Magazine and is written by Jenna Montgomery.

Bitcoin Magazine

SEC Chair Paul Atkins, Treasury Secretary Scott Bessent, David Sacks Push Congress to Pass Crypto Market Structure Bill ‘Now’

Three prominent voices in finance, crypto, and policy urged Congress this week to move quickly on the Clarity Act, a long-awaited bill to define how cryptocurrencies and blockchain-based financial products operate under U.S. law.

Treasury Secretary Scott Bessent called for the Senate Banking Committee to advance the legislation to President Trump’s desk, saying that Congress has spent years debating a framework to “onshore the future of finance.”

“Senate time is precious, and now is the time to act,” Bessent said on social media, echoing points from his Wall Street Journal op-ed that argued U.S. leadership in global finance depends on clear, durable digital-asset rules.

The Clarity Act, seen as a companion to the Genius Act signed by President Trump last year, seeks to establish regulatory boundaries between the Securities and Exchange Commission and the Commodity Futures Trading Commission.

The bill defines when a token qualifies as a security, sets operating pathways for trading platforms, and introduces new anti-fraud and anti-money-laundering measures.

David Sacks, who championed last year’s Genius Act on stablecoins and is the White House’s former Crypto Czar, endorsed Bessent’s call. He said the Clarity Act would provide “rules of the road” for all other digital assets. “Secretary Bessent is right — the time to act is now. Senate Banking, and then the full Senate, should pass market structure,” Sacks wrote. He added that he expects Congress to deliver the bill for President Trump’s signature.

SEC Commissioner Paul Atkins also joined the push. “The project is designed so once Congress acts, the SEC and CFTC are ready,” Atkins said on X. “It’s time for Congress to future-proof against rogue regulators and advance comprehensive market structure legislation.”

Bessent: Crypto innovation is going to other countries

In his op-ed, Bessent warned that the absence of clear crypto regulation has driven innovation overseas to jurisdictions like Abu Dhabi and Singapore. Without consistent U.S. rules, he wrote, developers and investors face uncertainty about registration, compliance, and enforcement.

“Nations that provide clarity attract innovation,” Bessent wrote. “The Clarity Act would restore confidence that digital-asset businesses can build and grow in the United States.”

The Genius Act last year established a framework for dollar-backed stablecoins, aligning blockchain-based payments with the U.S. dollar’s global role. The Clarity Act would extend that foundation to the broader digital-asset ecosystem, including tokenized securities, decentralized exchanges, and blockchain-based settlement systems.

Supporters argue the crypto bill would enhance financial oversight while keeping blockchain innovation — and its associated jobs and tax revenue — within U.S. borders.

By codifying legal parameters, they say, the legislation would protect investors, reduce regulatory uncertainty, and keep the U.S. at the forefront of financial technology rather than ceding ground to foreign markets.

“The United States became the world’s financial center by leading during moments of technological change,” Bessent wrote. “Passing this legislation ensures that the next generation of finance is built on American rails, backed by American institutions, and denominated in American dollars.”

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post SEC Chair Paul Atkins, Treasury Secretary Scott Bessent, David Sacks Push Congress to Pass Crypto Market Structure Bill ‘Now’ first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

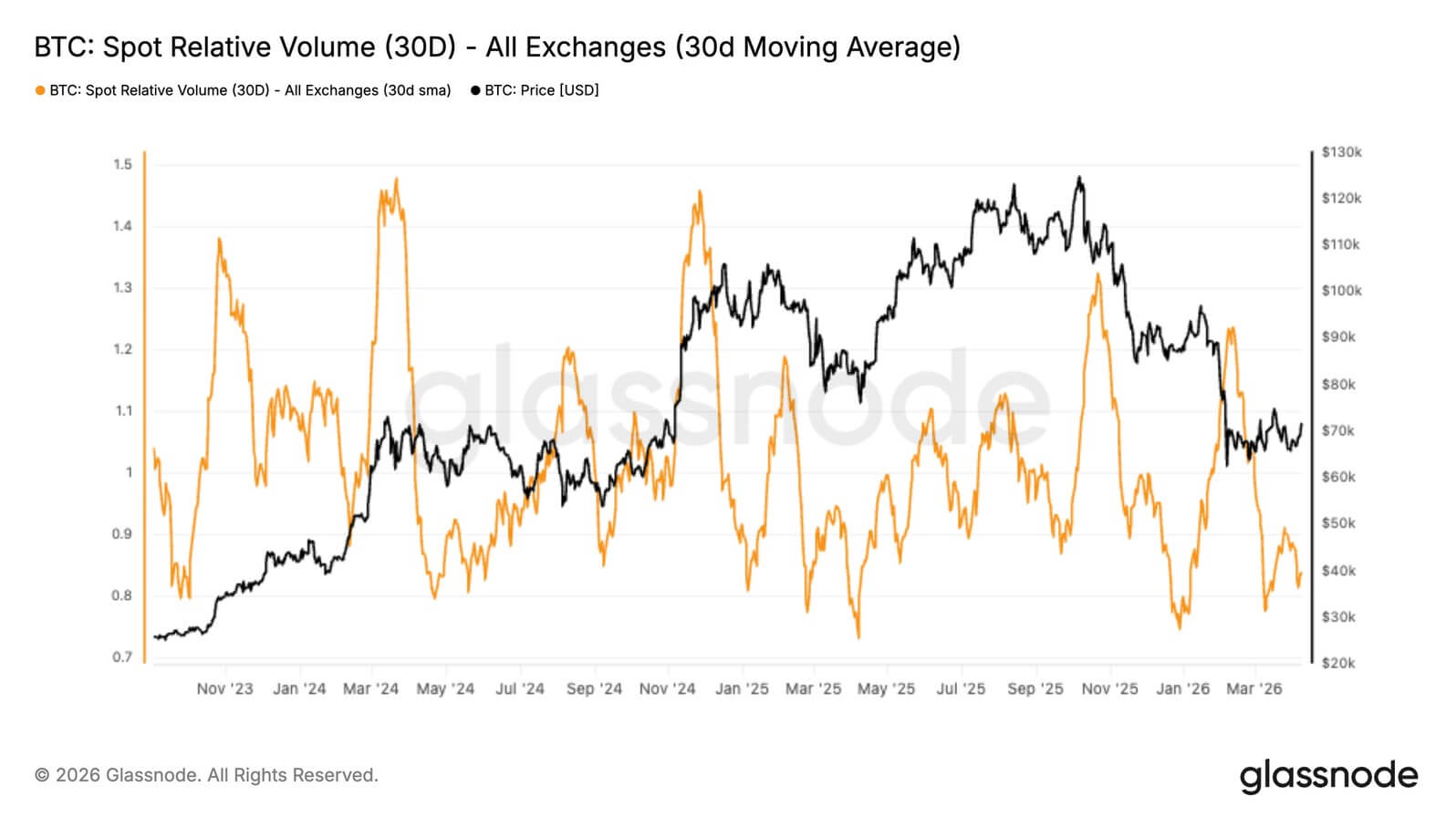

Bitcoin (BTC) moved from roughly $67,000 to $72,000 in the days surrounding the US-Israel-Iran ceasefire announcement, a 7.5% rebound that reduced volatility and lifted sentiment across risk assets.

Glassnode's Apr. 8 Week On-chain report noted that the bounce and stabilization still fit the fingerprint of a bear market rebound. BTC still trades inside a bear market value zone, and the level that would genuinely flip the picture is $81,600.

That number is the Short-Term Holder Cost Basis, which is the aggregate breakeven price for Bitcoin bought in recent months. Glassnode identifies it as the line the market needs to reclaim before rallies can plausibly represent a durable move.

Below it, recent buyers as a cohort carry losses, and the report says every rally into that range is apt to run into supply from trapped holders seeking to exit near breakeven.

The ceasefire eased the macro shock, compressing the volatility of the options markets. Short-dated implied vol fell to the low 40s, and the 6-month tenor settled around 45%.

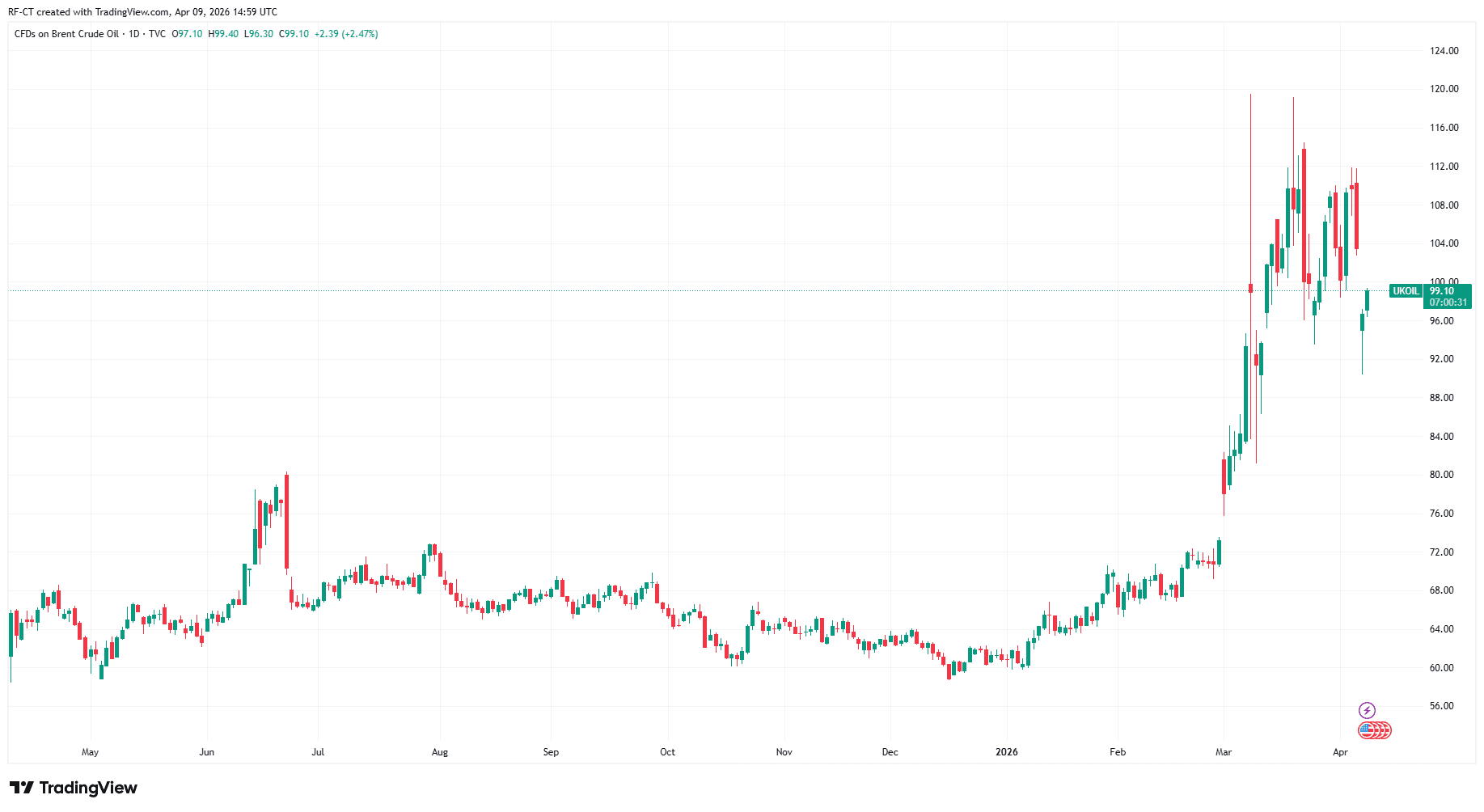

Reuters reported on Apr. 9 that the truce already looked fragile, with oil rebounding and broader risk sentiment softening within a day of the announcement.

Three numbers

Glassnode's framework reduces to a clean progression, pointing to the $69,000-$71,500 zone as to where dealer positioning shows long gamma concentration, a mechanical structure that may help absorb near-term selling.

With BTC trading slightly above $72,000 at press time, the market is above the top of that support shelf. The $78,000 True Market Mean sits 8.5% higher and represents the probable ceiling for any relief rally.

Glassnode places the AVIV Ratio at 0.92, below 1.0 since early February. The firm says that reading is comparable to May-June 2022, a period during a bear market, and is well above the deepest capitulation extremes of late 2022.

The current setup is a bounce inside an ongoing bear phase, with a plausible floor, a probable near-term ceiling, and a more important level above both.

Binance's 30-day relative spot volume holds below its 1.0 baseline, which Glassnode reads as weak organic demand. US spot ETF flows turned modestly positive on a 14-day basis, ending an extended outflow stretch, with Apr. 7 and 8 still showing negative prints.

Futures volume contracted sharply and rolled over on a 30-day basis, while the 25-delta options skew still tilts toward puts, meaning that traders continue to pay a premium for downside protection.

Together, those readings describe a market stabilizing on thin participation.

The architecture of a relief rally

Glassnode says the market has entered a more balanced state, in which catastrophic downside is less imminent, a grind toward $78,000 is plausible, and durability is still an open question. The difference comes down to whether the buyer base is absorbing or distributing.

Below $81,600, recent buyers are carrying losses, creating a mechanical constraint on upside momentum. Each rally toward breakeven delivers an exit opportunity to a cohort that accumulated at higher prices and waited out a drawdown.

Glassnode explicitly describes that mechanism, saying that distribution pressure from trapped holders makes rallies within the current range structurally vulnerable.

Long-term holders have realized losses of over 4,000 BTC per day since November 2025. The report noted that cooling that figure toward under 1,000 BTC per day, alongside a reclaim of $81,600, would constitute the clearest on-chain signal of a genuine regime turn.

Potential pathways

In the bull case, BTC reclaims $81,600, ETF inflows continue to expand, and futures participation re-expands, pulling volume back into the market.

Glassnode's own framework provides that falsification test: a reclaim of the Short-Term Holder Cost Basis, combined with long-term-holder realized losses cooling materially, would be the most credible on-chain confirmation that the current bear phase is giving way to a pre-bull recovery structure.

In that outcome, the ceasefire was the catalyst that began a genuine demand-regime transition.

In the bear case, BTC loses the $69,000-$71,500 support shelf, and weak spot demand fails to absorb supply from trapped holders.

The relief rally stalls well short of $78,000, and the current bounce earns a footnote as a volatility event. Glassnode's data on softer futures, persistently defensive options positioning, and still-weak spot volumes make that outcome consistent with the current participation profile.

The ceasefire reduced near-term volatility and left sustained demand improvement yet to follow.

| Scenario | What price does | What participation does | What it means |

|---|---|---|---|

| Bear-market bounce | Holds or loses $69K–$71.5K, stalls below $78K or $81.6K | Spot stays soft, futures stay weak, options stay defensive | Relief rally inside a bear structure |

| Credible recovery | Reclaims $81.6K | ETF inflows expand, futures re-accelerate, LTH realized losses cool toward under 1K BTC/day | Transition toward pre-bull recovery |

| Failure / relapse | Loses support shelf decisively | Trapped-holder supply overwhelms weak demand | Bounce becomes a volatility event, not a regime change |

Ceasefire late shock

The macro backdrop sets the ceiling on sentiment-driven demand. The US-Israel-Iran truce compressed volatility faster than it rebuilt risk appetite, and the one-day reversal in oil prices that Reuters captured on Apr. 9 illustrates why geopolitical relief rallies carry an expiry date.

Once the acute fear subsides, the demand structure reasserts itself, and Glassnode's data indicate that the underlying structure remains thin.

Realized volatility at 42.5% and implied vol in the low 40s describe a calm market that has yet to turn bullish.

Durable breakouts require expanding volume, improving ETF flows beyond modest, and futures curves showing real speculative appetite. On Glassnode's Apr. 8 data, those conditions have yet to appear.

For now, the cleaner read from Glassnode is that Bitcoin has found enough footing for a bounce.

Below $81,600, the market is still rallying within a bearish structure, and the participants most likely to sell on the next push are the same buyers who have been underwater since the rally peaked.

The post Bitcoin’s rally is still just a bear market bounce unless it reclaims this key level appeared first on CryptoSlate.

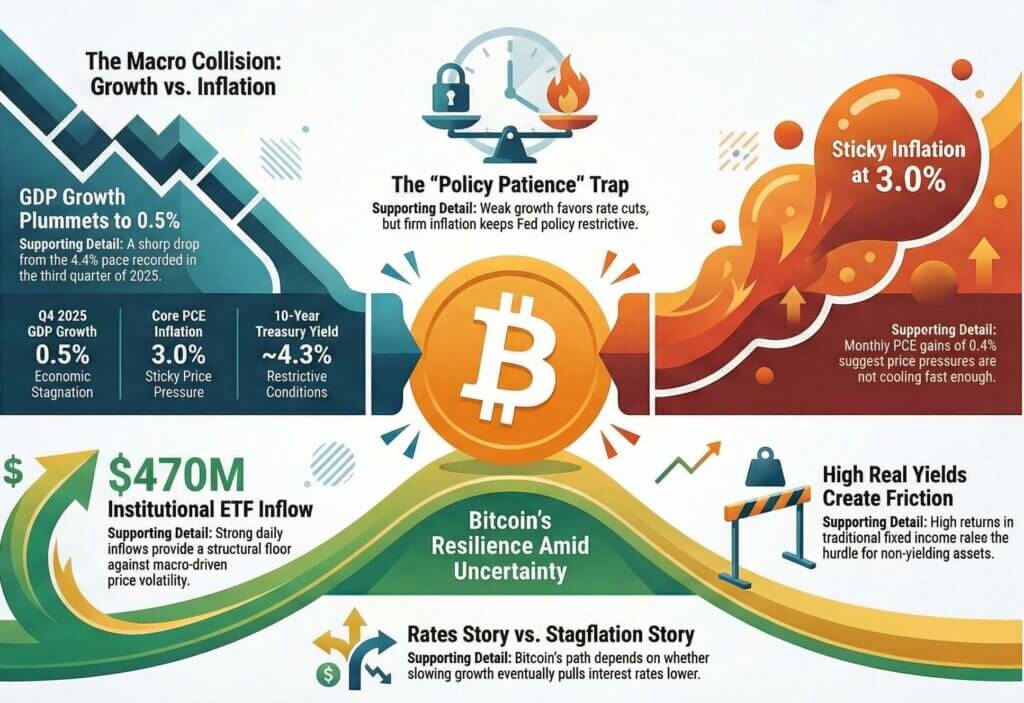

The U.S. economy entered 2026 with far less momentum than markets had priced in a few months earlier. According to the Bureau of Economic Analysis, fourth quarter 2025 GDP growth was revised down to 0.5%, a sharp step down from the 4.4% pace recorded in the third quarter.

On its own, that revision would usually support the view that the Federal Reserve is moving closer to rate cuts. The problem is that inflation has not cooled enough to give policymakers much room.

New PCE data released today shows headline inflation at 2.8% year-over-year in February, with core PCE at 3.0%. Monthly gains in both measures came in at 0.4%, a pace that still points to sticky price pressure rather than a fast return to the Fed’s 2% target.

That combination has become the real macro question for Bitcoin and the broader crypto market. Investors are dealing with an economy losing steam, while inflation remains firm enough to keep the Fed cautious.

The gap between the two trends has begun to shape the risk environment. It shapes the path of Treasury yields, the pricing of future rate cuts, and the willingness of investors to keep allocating into risk assets.

Bitcoin has already shown that it can attract capital amid difficult macro conditions, especially when exchange-traded fund demand remains firm, and supply remains structurally constrained. Even so, weaker growth does not automatically produce an easier backdrop for crypto.

The transmission channel runs through yields, liquidity, and confidence in the policy path.

| Metric | Most recent | Previous benchmark |

|---|---|---|

| U.S. real GDP growth, annualized | Q4 2025: 0.5% | Q3 2025: 4.4% |

| PCE inflation, YoY | Feb. 2026: 2.8% | Jan. 2026: 2.8% |

| Core PCE inflation, YoY | Feb. 2026: 3.0% | Jan. 2026: 3.1% |

| Bitcoin price | $72,129 | 24h: +1.20%, 7d: +7.84%, 30d: +1.43% |

The GDP downgrade changed the macro setup for Bitcoin

As of press time, April 9, CryptoSlate’s Bitcoin price page has BTC trading at $71,201, down 0.72% over 24 hours, up 7.60% over seven days, and up 0.99% over the past month. That profile captures the current market state well.

Bitcoin has bounced, while the move has unfolded inside a macro environment that still feels unresolved. A weak GDP revision can appear to be a simple recession signal at first glance.

The larger point sits elsewhere. The downgrade landed at the same time that inflation remained elevated enough to keep the usual rescue mechanism out of immediate reach.

For Bitcoin, the next move still depends less on one growth print and more on whether incoming data can push rates and real yields lower in a durable way.

The 0.5% GDP reading challenged the idea that the U.S. economy was moving through a controlled slowdown with enough resilience to absorb tight policy and enough disinflation to bring borrowing costs down in an orderly way.

The sequence of official estimates, from the advance release to the second estimate and then the third estimate, showed a clear erosion ofconfidence around late-2025 growth. Markets can usually absorb a weak quarter when inflation is cooling fast enough for the Fed to step in.

This time, the inflation side of the equation has stayed stubborn enough to keep that path uncertain.

February’s PCE report intensified that problem. Headline PCE met expectations at 2.8% year over year, and core PCE came in slightly cooler than expected at 3.0% against a 3.1% consensus.

The monthly details were less comforting. Both headline and core increased 0.4% from the prior month, a pace that still leaves inflation running above where the Fed would want it if the central bank were preparing to pivot aggressively.

That is why the GDP revision and the inflation print belong in the same frame. The growth slowdown points toward easier policy. The inflation data keeps that outcome conditional.

Sticky inflation kept the Fed from offering easy relief

That tension also explains why the market response has been more complex than a standard reaction in which weak growth lifts hopes for faster easing. Treasury yields remain elevated enough to keep financial conditions restrictive.

The 10-year Treasury yield hovered around 4.3% after the GDP and PCE releases, while real yields have stayed high enough to preserve competition from safer assets. For Bitcoin, that creates a meaningful constraint.

Investors can still earn solid nominal and inflation-adjusted returns in traditional fixed income, which raises the hurdle for non-yielding assets. CryptoSlate recently framed this dynamic directly in its analysis of how Bitcoin trades real yields first.

That remains the clearest transmission mechanism here.

The labor market has added another layer to the picture. The latest BLS employment report showed March payroll growth of 178,000 and unemployment near 4.3%.

Weekly claims have moved higher at the margin, with the Department of Labor showing 219,000 initial jobless claims, yet the broader labor backdrop still looks resilient enough to give the Fed cover to wait. A labor market that is softening slowly, rather than cracking quickly, supports the case for policy patience.

Markets are therefore dealing with two incomplete signals at once: weaker growth and inflation that is still warm enough to keep caution in place.

For households, the practical consequence is straightforward. The economy is slowing, household costs still feel high, and interest-rate relief may take longer than many expected.

Mortgage rates, credit card costs, and consumer financing conditions all sit downstream of that same tension. Bitcoin enters this setup as a market that often benefits from looser liquidity, lower real interest rates, and a stronger appetite for alternative stores of value.

Those supports are only partially present right now. The GDP downgrade made the soft-landing narrative harder to defend.

It did not, on its own, deliver a clear all-clear for risk assets.

ETF demand is helping Bitcoin absorb a tougher macro backdrop

Bitcoin’s recent price behavior reflects that ambiguity. The asset has recovered enough to show that demand remains real, yet the move has not carried the kind of decisive follow-through that would signal a fully restored risk-on backdrop.

According to CryptoSlate’s BTC market data, the coin is up strongly on the week while remaining almost flat over the past month. That mix suggests a market willing to respond to supportive flows and tactical optimism, while still respecting that macro conditions have not yet resolved into a clearer pro-risk regime.

One reason Bitcoin has held up is the continuing support from spot ETFs. Spot Bitcoin ETFs drew roughly $470 million on April 6, one of the strongest inflow days of the year.

Those flows provide an important counterweight to macro pressure because they create a persistent source of demand from investors who are allocating through regulated products rather than trading short-term volatility directly on crypto-native venues. ETF demand does not erase macro risk.

It does change the asset's resilience profile. A market with real institutional inflows can absorb more pressure than one driven purely by speculative leverage.

Still, the next phase depends on whether the slowdown becomes a rates story or a stagflation story. The distinction is critical.

A rates story would involve weaker growth gradually pulling yields and policy expectations lower, thereby improving the environment for Bitcoin, growth equities, and other duration-sensitive assets. A stagflation story would involve weaker growth alongside sticky inflation pressure that even re-accelerates, leaving the Fed constrained and risk assets facing a more difficult backdrop.

CryptoSlate’s recent explainer on why stagflation is becoming a market word again is useful here because it translates the jargon into something people already understand: costs stay high while the economy feels weaker.

Oil, inflation, and policy risk are colliding in the same window

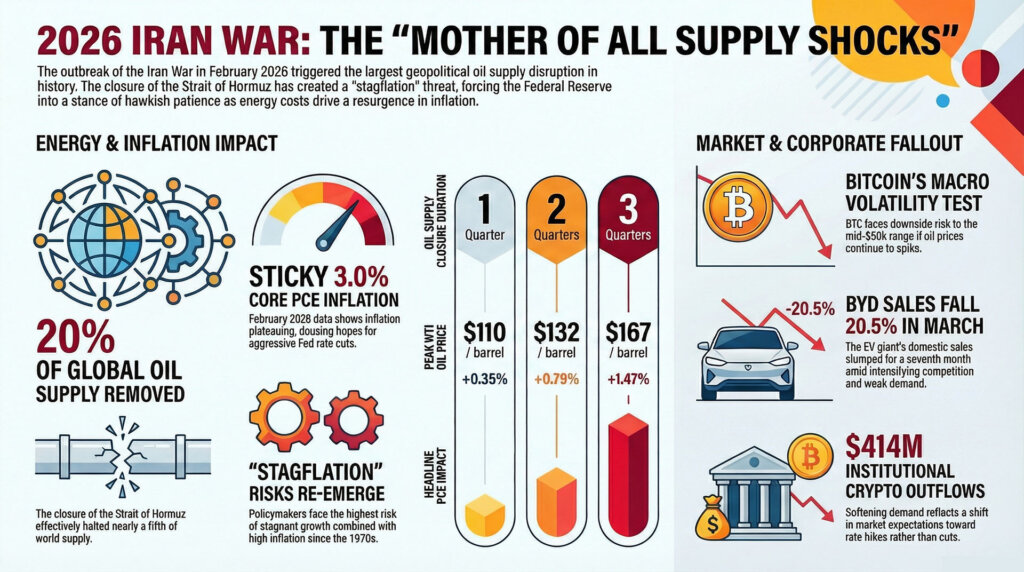

That is where the outside-world collision becomes more important than any single crypto-specific catalyst. Energy is back in the macro conversation.

CryptoSlate recently noted that oil risk and reduced rate-cut expectations are starting to converge in the market narrative. If energy price pressures feed through into inflation expectations, the growth slowdown becomes harder for risk assets to celebrate.

The same weak GDP print that might usually lift hopes for faster easing could instead deepen concern that the Fed is losing room to respond.

Bitcoin fits into this environment through several layers. The first layer is policy expectations, which govern the path of front-end rates and shape broader liquidity conditions.

The second layer is real yields, which influence the opportunity cost of holding BTC. The third layer is structural crypto demand, particularly ETF inflows and spot accumulation. The fourth layer is risk sentiment, which determines whether markets interpret incoming data as easing-friendly or growth-threatening.

Bitcoin can perform well when one or two of those layers improve. Sustained upside usually becomes easier when three or more align.

Right now, structural demand looks constructive, while policy and rates remain mixed. That is why the market still feels lively rather than settled.

The slowdown has opened the door to a more supportive macro path for Bitcoin. The inflation data has kept that door only partially open.

The next test has a clearer roadmap; inflation, yields, ETF flows, and the incoming growth data will tell markets whether the 0.5% GDP print was a late-2025 air pocket or the start of something more durable.

The next 30 to 90 days will decide which side of the contradiction gives way first

The next quarter has enough scheduled data to force that choice. The immediate checkpoints are the next inflation releases, the April Federal Reserve meeting, and the first estimate of the first quarter GDP.

The Atlanta Fed’s GDPNow model will shape expectations into that report, while the Cleveland Fed’s inflation nowcast offers a live look at how sticky price pressure may remain before the official numbers arrive. These indicators keep the focus on what changes next rather than on a backward-looking debate over whether fourth-quarter weakness was large or merely surprising.

A constructive scenario for Bitcoin would start with a renewed disinflation trend. That could come from softer monthly CPI and PCE readings, easing energy pressure, or clearer signs that demand is cooling without a deep labor-market break.

In that setup, yields would have room to fall, Fed cuts would move closer in the market’s calendar, and Bitcoin would gain from a lower-rate environment while still enjoying structural support from ETF demand. The Federal Reserve’s March Summary of Economic Projections still points to 2.4% GDP growth in 2026, 2.7% PCE inflation, and a year-end fed funds rate of 3.4%.

Those numbers show that the official baseline still leans toward a slower but intact expansion. If incoming data moves in that direction, the current growth scare could become a bridge to easier conditions rather than a warning of broader deterioration.

A more difficult scenario would involve inflation staying close to current levels or moving higher again, especially if oil or other supply-driven pressures keep monthly prints firm. In that case, the growth slowdown would feel less like an invitation for policy relief and more like a constraint on the Fed.

Bitcoin could still attract demand as a scarce asset and as a hedge against long-term policy stress, yet the first-order market reaction would likely stay tied to broader risk sentiment. High real yields and delayed rate-cut expectations would continue to compete with the bullish structural case coming from ETFs and long-term accumulation.

There is also a middle path, and it may be the most realistic one over the next several weeks. Growth could stay soft without collapsing, inflation could cool slowly without offering immediate comfort, and Bitcoin could continue to grind inside a range where each positive impulse meets a macro counterweight.

That kind of market often frustrates directional conviction while still rewarding selective accumulation. It also tends to favor disciplined interpretation over dramatic conclusions.

The broader global backdrop reinforces the need for balance. The IMF’s latest World Economic Outlook update still projects global growth of 3.3% in 2026.

That keeps the U.S. slowdown in perspective. It is a serious signal, especially because it coincides with inflation that remains above target, yet it has not become a full-system global break.

Bitcoin sits in the middle of that distinction. It remains exposed to macro tightening and sensitive to real yields, while also benefiting from stronger market infrastructure, deeper institutional access, and a structural demand base that did not exist in prior cycles.

One conclusion stands above the rest. The GDP downgrade exposed real weakness in the soft-landing narrative.

The inflation data kept the Fed from offering immediate reassurance. Bitcoin is therefore trading an unresolved macro contradiction, one that will likely be settled by the next sequence of inflation, labor, and growth data rather than by today’s revision alone.

Growth has slowed sharply, inflation still has a grip on policy, and Bitcoin’s next sustained move will depend on which side of that tension gives way first.

The post Bitcoin reacts to US economy moving close to stalling, but inflation still too hot for easy Fed rescue appeared first on CryptoSlate.

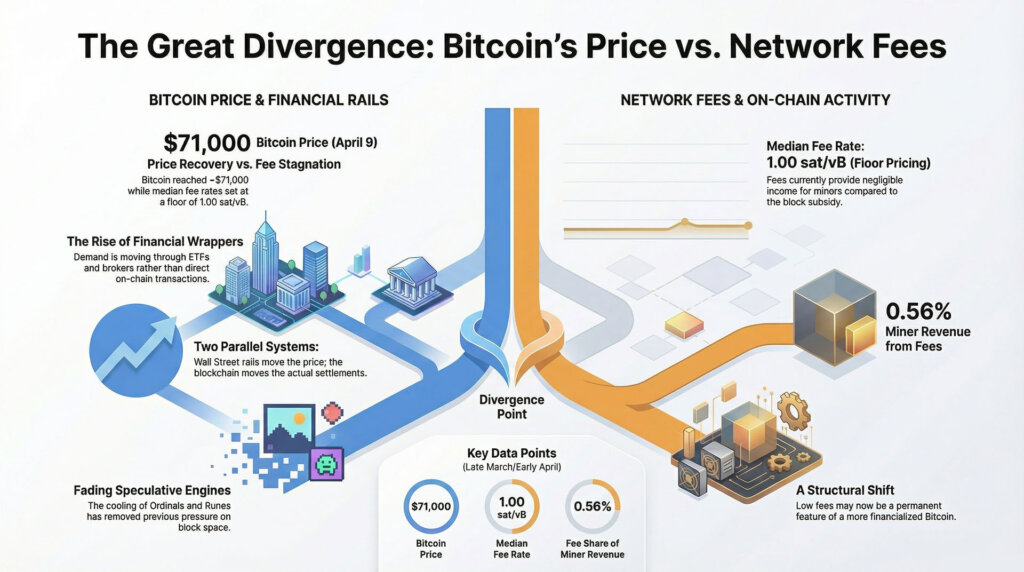

Bitcoin’s rebound to around $71,000 has reignited a familiar bullish conversation about price, liquidity, and positioning. It has also exposed a less comfortable fact inside the network itself.

The fee market has barely moved.

For a market that still treats on-chain congestion as a sign of organic demand, that divergence deserves more attention than another recap of macro tailwinds or ETF flow streaks.

On CryptoSlate’s Bitcoin price page, BTC was last trading at $70,990 on April 9, down 0.86% over 24 hours, up 6.11% over seven days, and up 0.85% over 30 days.

Price has clearly recovered from the lower end of its recent range, while the base layer still looks calm, cheap, and uncrowded.

The disconnect says something important about where this move is actually happening. More Bitcoin demand is being expressed through financial wrappers, broker channels, and ETF rails than through users competing for block space on-chain.

The price move can still be durable under that setup. The signal it sends is different.

A recent Bitcoin block space report covering March 19 to March 26 found that the median fee rate opened at 1.13 sat/vB and remained at 1.00 sat/vB for the rest of the week. In practical terms, that is floor pricing.

Users were still able to get confirmed without paying up for scarce space. Across 1,028 blocks, the report counted just 18.03 BTC in total fees, or roughly 0.0175 BTC per block.

Even more striking, those fees accounted for only 0.56% of miner revenue for the week, compared with 3,212.5 BTC from subsidy.

Price has recovered, while the fee market still looks half asleep

Those numbers are unusually soft for a market trading back around $71,000. Earlier cycle logic conditioned the market to expect a rising Bitcoin price to coincide with busier blocks, more contested inclusion, and a fee market that starts climbing before most people notice.

That reflex still shapes how many crypto participants interpret demand. The current market is sending a different message.

Price can recover even while on-chain urgency remains muted.

One reason the fee market looks so subdued is that Bitcoin has already lost one of the speculative demand engines that distorted block-space pricing in prior phases. Ordinals and other inscriptions once created a visible burst of non-monetary demand for inclusion, while the Runes launch briefly did the same on an even larger scale around the 2024 halving.

That impulse has faded materially. The chain is no longer dealing with the same inscription-driven scramble for block space, which means today’s low-fee environment is not just a story about healthy efficiency or quiet user behavior.

It also reflects the absence of a category that had previously inflated transaction counts and put pressure on fees.

That context helps explain why a rebound in BTC can coexist with such a soft fee backdrop. Earlier in the cycle, Ordinals, inscriptions, and later Runes gave miners an extra revenue stream and gave observers a reason to treat mempool stress as proof of expanding demand.

Today, that support looks much thinner. The speculative traffic that once crowded the chain has cooled, leaving Bitcoin more dependent on either organic settlement demand or price-led financial flows to do the heavy lifting.

In that sense, it's also about what has already left the building.

Part of that dynamic comes from the fact that the pipes carrying demand have changed. A buyer using a spot ETF, a broker product, or a treasury vehicle can push capital into Bitcoin exposure without creating the same base-layer footprint as a user moving coins directly across the chain.

That distinction has grown more important as Bitcoin access has become more financialized. Farside’s daily ETF flow data showed a $471.4 million inflow on April 6, followed by outflows of $159.1 million on April 7 and $124.5 million on April 8.

The day-to-day swings were relatively modest, yet the broader point is that flows through these wrappers remain an active transmission channel for demand. Spot Bitcoin ETFs recorded $1.3 billion in net inflows for the month, the first positive month since October.

That is the hidden mechanism behind the current divergence. Bitcoin demand is being split across two systems.

One system moves price through funds, adviser platforms, and broker access. The other system moves transactions through the blockchain itself.

Right now, the first system looks more active than the second. That leaves the fee market looking sleepy even as the asset itself regains altitude.

The result is a rebound that feels bullish on screens, while the network’s own pricing of block space remains subdued. That combination carries a different implication than a full-on-chain revival.

It suggests the recovery has broad distribution through financial rails, while direct pressure on Bitcoin’s settlement layer remains limited. For anyone still treating mempool stress as a simple proxy for demand, the current setup is a reminder that the market structure around Bitcoin has changed faster than many of the instincts people still use to interpret it.

Glassnode’s April 1 weekly market note described Bitcoin as rangebound between $60,000 and $70,000 and argued that spot demand was showing early signs of absorption, while still lacking the conviction needed for a sustained breakout. Glassnode also flagged dense overhead supply between $80,000 and $126,000.

That range framework fits the current divergence well. Bitcoin has bounced, yet the fee market has not repriced to indicate broad urgency, widespread settlement demand, or a sudden scramble for base-layer access.

Low fees point to where demand is landing, and to what miners still are not getting paid for

A separate report citing Glassnode data on March fee activity said Bitcoin’s 30-day simple moving average for daily transaction fees had fallen to 2.5 BTC per day in March 2026. The article described that as the lowest level since March 2011.

The precise historical framing requires caution until the underlying primary chart is checked directly, yet the directional message lines up with the broader evidence. Fee conditions have tightened significantly, and they have stayed tight even as BTC regained ground.

That compression creates an important divide between price strength and network monetization. Users get a friendlier chain. Miners get very little incremental revenue from transaction demand.

After the halving, that revenue mix carries more weight than it did when the subsidy was doing even more of the work. The March 19 to March 26 block space report quantified the issue cleanly, with fees contributing just 0.56% of miner revenue for the week.

For miners, a rally that does not trigger a fee response still helps through price, while leaving the network’s internal revenue base largely unchanged.

The difference becomes easier to see once Bitcoin is framed as both an asset and a network, with each side expressing demand in different ways. The asset side benefits from ETF adoption, adviser access, treasury accumulation, and improved risk appetite.

The network side benefits from actual users, transfers, settlements, and transactions that compete for limited capacity. These two layers can reinforce each other.

They can also drift apart for meaningful stretches. That is where the market sits now.

There is also a practical point in the current setup. A calm mempool does not automatically translate into weak Bitcoin.

It suggests that the rebound offers less evidence of resurgent on-chain intensity than the price alone might imply. A base-layer fee response would indicate that financial demand was spilling over into actual settlement contention.

Without that response, a different interpretation moves closer to the center: one in which Wall Street distribution is doing more of the immediate lifting than users transacting natively on-chain.

That outside-world collision gives the current divergence its explanatory power. Bitcoin is increasingly embedded in mainstream financial plumbing.

Morgan Stanley has just launched a low-fee spot Bitcoin ETF, and Charles Schwab is preparing direct spot Bitcoin and Ethereum trading by mid-2026. The access channels around Bitcoin continue to widen.

As they widen, price can move along those rails long before the mempool signals a similar demand pulse.

The next test sits in the fee market, the miner revenue mix, and whether price strength spreads into actual settlement demand

The immediate question is whether the current divergence is temporary or structural. There are credible arguments on both sides, and the next few weeks should help narrow the range of plausible outcomes.

The first path is a continuation of the current pattern. ETF and broker demand continue to support the price; Bitcoin holds near the upper end of its recent range, and fee rates remain close to the floor.

That would strengthen the case that this rebound is being carried primarily by wrapper-led flows rather than a broad-based return of native transaction demand. It would also reinforce the idea that price can recover through distribution and access to capital, while the chain’s own fee market remains calm.

The second path is a catch-up move in block-space demand. If the price recovery begins to spill over into actual transaction competition, the market should start to see higher fee estimates, deeper backlogs, more sustained pressure in the mempool, and a larger fee share in miner revenue.

That shift would change the interpretation of the rally. It would suggest that the move is spreading from exposure into usage, which would give the recovery a different kind of durability.

The third path would leave the current divergence looking more like a warning than a curiosity. If ETF flows roll over again, price slips back into the lower half of Glassnode’s recent range, and fee conditions still stay weak, the market will have stronger grounds to treat the rebound as a positioning move that never developed into broader transactional demand.

In that setup, the mempool’s quietness would stop looking incidental and start looking diagnostic.

A fourth path sits closer to miner economics than price direction. If fees remain this subdued while miners continue operating in a post-halving environment, attention will shift toward how the network is being monetized.

CoinShares’ Q1 2026 mining report described the final quarter of 2025 as the toughest quarter for miners since the 2024 halving, with a sharp price drawdown and near-record hashrate weighing on margins. A prolonged stretch of low fees would keep that pressure in focus.

Price appreciation helps, while a broader fee contribution would help more.

That is why the fee market deserves to sit much closer to the center of the current Bitcoin conversation. A move back toward $71,000 is meaningful.

It also leaves an open question. Where, exactly, is the demand becoming real?

Right now, the strongest answer is that demand is becoming real in financial products faster than it is in Bitcoin’s own block space.

That carries a measured but important implication for how this market should be understood. The rebound has gained traction through the channels Bitcoin spent years trying to enter: funds, advisers, brokers, and mainstream portfolio plumbing.

The blockchain itself has yet to show the same urgency in its pricing of access. For anyone watching Bitcoin as both a monetary asset and a network, that gap is the signal.

The market has moved higher. The chain has barely flinched.

The next round of evidence will come from whether that calm finally breaks, or whether Bitcoin’s most powerful demand engine now lives one layer removed from Bitcoin itself.

The post The Bitcoin network is currently a ghost town as price is being controlled elsewhere appeared first on CryptoSlate.

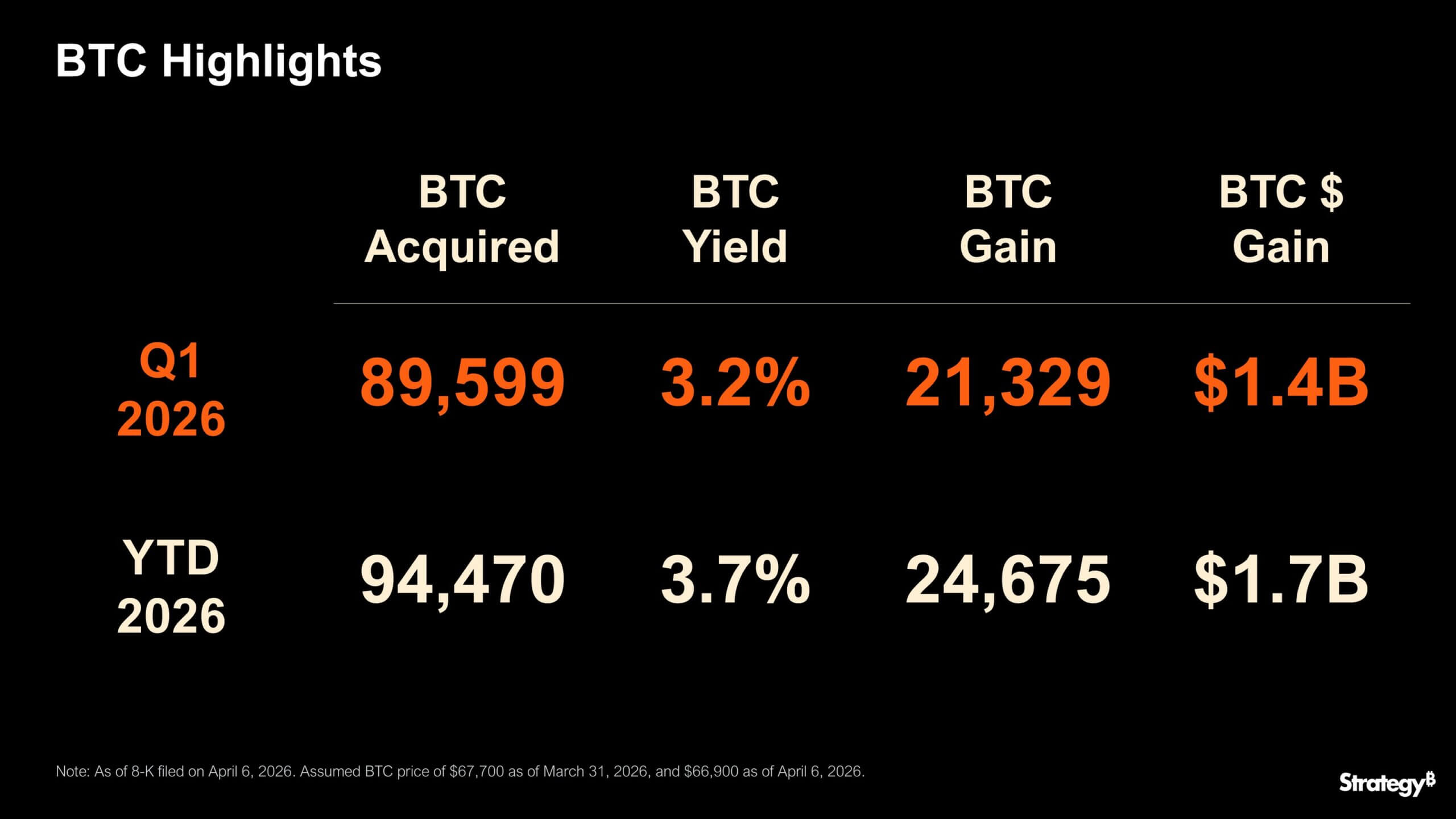

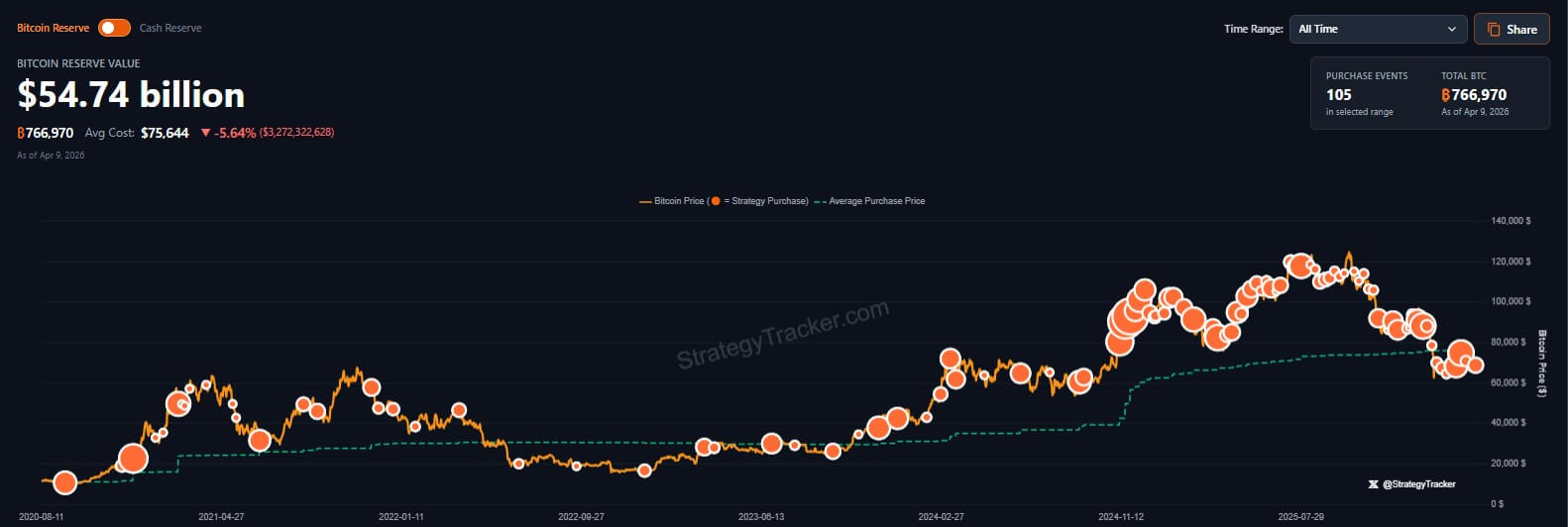

Strategy (formerly MicroStrategy) is claiming its aggressive Bitcoin purchases have yielded a nearly $2 billion gain this year despite the top asset's clear price struggles.

However, a close look at the enterprise software company's legally binding regulatory filings tells a much redder story: under standard accounting rules, the firm is nursing a multi-billion dollar unrealized loss, and its aggregate Bitcoin stack sits firmly underwater.

Despite the paper losses, the company shows no signs of slowing. Armed with a highly liquid capital markets engine, Strategy continues to issue equity to fund massive daily purchases, completely unfazed by the disconnect between its curated corporate dashboard and its sobering regulatory reality.

A bespoke winning streak

By its own metrics, Strategy’s Bitcoin treasury playbook is flawless despite the prevailing bear market situation in the broader crypto market.

On X, the company said its BTC purchasing strategy has generated nearly $1.7 billion in Bitcoin gains since January this year.

That metric caps off a historic accumulation streak that has fundamentally warped the crypto market's supply dynamics.

Notably, Strategy disclosed that it has acquired an astonishing 2.2 times the newly mined Bitcoin supply over the period. This equates to more than 94,000 BTC since the beginning of the year.

To quantify this, Strategy's management points to two proprietary metrics: “BTC Yield” and “BTC Gain.” Strategy reports achieving a BTC Yield of 3.7% this year, generating a BTC Gain of 24,675 coins (roughly $1.7 billion).

For retail investors and crypto advocates, these figures are definitive proof that the company’s leveraged accumulation strategy is working.

Strategy’s Bitcoin gain metric is designed to reward balance-sheet expansion on a per-share basis. In its annual report, the company says BTC Yield measures the percentage change in Bitcoin Per Share (BPS) from the beginning to the end of a period.

BTC Gain then converts that percentage change into an absolute Bitcoin figure by multiplying the amount of Bitcoin held at the start of the period by BTC Yield. BTC $ Gain goes one step further by multiplying BTC Gain by the market price of Bitcoin.

The $14 billion SEC reality

However, the transition from the company's marketing materials to its Securities and Exchange Commission filings, and the $1.7 billion gain, is eclipsed by a staggering accounting deficit.

Strategy's quarter-end filing states the firm recorded a $14.46 billion unrealized loss on its digital assets for the three months ended March 31.

Under the fair-value accounting rules adopted in January 2025, market price fluctuations must flow directly through the income statement. Because Bitcoin's price slipped between year-end and March 31, Strategy was forced to slash the official carrying value of its digital assets from $58.85 billion down to $51.65 billion.

Beyond the quarter-end accounting losses, the company’s aggregate cost basis is also underwater. Strategy bought heavily into a weakening market through the first quarter, pushing its total holdings to 766,970 BTC. The total acquisition cost was $58.02 billion, averaging $75,644 per coin.

With Bitcoin currently trading near $71,192, that reserve is worth approximately $54.60 billion, placing the company roughly $3.41 billion below its aggregate cost.

Strategy's Bitcoin buying continues with STRC

Despite billions in paper losses and an average purchase price that exceeds the open market value, Strategy insists it will not sell a single coin. Instead, it is doubling down.

The ultimate proof of the market's willingness to fund this conviction lies in the company's STRC preferred stock issuance.

STRC is a high-yield credit structure that pays an 11.5% annual dividend. The asset is designed to trade closely to its par value of $100, and Strategy can efficiently leverage its at-the-market (ATM) issuance program to fund aggressive Bitcoin acquisitions.

In fact, STRC.live estimates show that STRC saw its daily volume reach $333 million, the seventh-highest trading volume since launch, on April 8. This day's trading could fund the purchase of more than 2,000 additional Bitcoins.

The numbers are a critical indicator of financial health for Strategy's specific playbook, signaling that demand for the firm's equity remains bottomless.

As long as Wall Street eagerly absorbs equity offerings at a stable valuation, Strategy faces no immediate pressure to halt its operations.

Where the pressure sits

The company’s own disclosures show why the dashboard metric and the ongoing buying streak do not settle the larger balance-sheet question.

Strategy acknowledges that its Bitcoin KPIs do not take into account existing and future liabilities, nor the preferential rights of preferred stockholders to dividends and assets in a liquidation scenario.

The annual report adds that purchases financed with non-convertible notes or preferred stock can simultaneously artificially lift BTC Yield, BTC Gain, and BTC $ Gain while also increasing overall indebtedness and senior claims on the asset pool.

That qualification has become increasingly important as the capital structure expands. Strategy said in February that it had established a $2.25 billion USD Reserve providing about 2.5 years of dividend and interest coverage.

However, STRC has scaled to a $3.4 billion market cap, and cumulative preferred distributions paid had reached $413 million at a blended annual rate of 9.6%.

Crucially, the annual report explicitly states that the software business is not expected to generate sufficient operating cash flow over the next 12 months to meet the company’s financial obligations and liquidity needs, meaning that continuous financing remains the lifeblood of the model.

This means that a significant decline in the market value of Strategy's Bitcoin holdings, or a negative shift in investor sentiment and financing conditions, could impair the firm's ability to raise enough equity or debt financing to meet obligations.

These risks are most likely to materialize when Bitcoin is trading below its carrying value or cost basis. If the company cannot secure financing in time or on acceptable terms, Strategy has conceded that it may be required to sell Bitcoin to satisfy financial obligations or liquidity needs.

For now, the machine is still running. Strategy is adding Bitcoin, the marketing dashboard still shows positive Bitcoin gain, and STRC remains anchored near par while supplying fresh capital.

The post Strategy’s near $2 billion profit on Bitcoin is eclipsed by huge losses SEC filing shows appeared first on CryptoSlate.

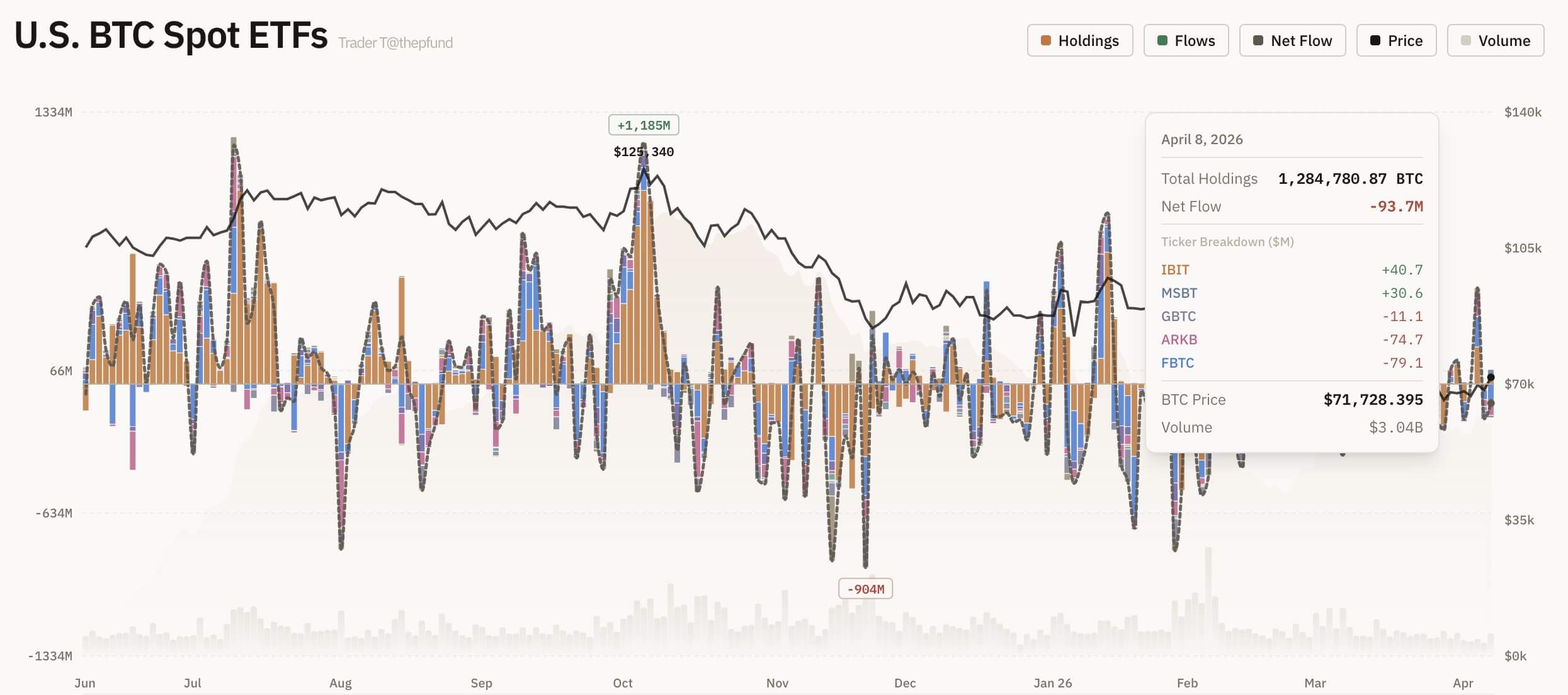

On April 8, Morgan Stanley’s spot Bitcoin exchange-traded fund began trading on the NYSE Arca under the ticker MSBT, logging 1.6 million shares and roughly $34 million in volume on its highly anticipated first day.

The MSBT fund purchased 430 Bitcoin on day one, following $30.6 million in net inflows.

Speaking on this performance, Bloomberg ETF analyst Eric Balchunas noted that MSBT's achievement comfortably places it among the top 1% of all ETF launches over the past year.

For comparison, the vast majority of newly launched ETFs across all asset classes average $1 million or less on their first day of trading.

Meanwhile, the performance is particularly notable given the broader market context. On its first trading day, the broader Bitcoin ETF sector saw $124 million in outflows, with only MSBT and BlackRock’s iShares Bitcoin Trust (IBIT) managing to register positive inflows.

This underscores the immediate market traction of Morgan Stanley’s offering and signals a potential shift in how institutional capital flows into the sector.

Igniting a race to the bottom on fees

With this launch, Morgan Stanley became the first major United States bank to issue a spot Bitcoin ETF under its own name, breaking the ice for traditional financial institutions that had previously remained on the sidelines.

The Wall Street heavyweight isn't just relying on its century-old brand prestige; it has deliberately ignited a fierce fee war in the Bitcoin ETF market.

MSBT charges a unitary delegated sponsor fee of 0.14%, making it the absolute cheapest spot Bitcoin ETF available to American investors today. This aggressively undercuts the market-leading IBIT, which currently charges a 0.25% expense ratio, and Grayscale’s Bitcoin Mini Trust ETF at 0.15%.

Industry experts note that this rock-bottom fee structure may force other established asset managers to slash their own expense ratios to remain competitive, echoing the wave of fee waivers and aggressive undercutting seen when the first slate of 10 spot funds debuted in early 2024.

The low cost of MSBT presents a compelling mathematical argument for fee-conscious institutional allocators.

MSBT's competitive moat

Despite the cheap fees, market observers have noted that Morgan Stanley’s true competitive moat rests on its unparalleled distribution network.

The firm employs approximately 16,000 wealth management advisors who oversee a staggering pool of client wealth, with estimates placing firmwide client assets at up to $9.3 trillion and those directly managed by the wealth advisory arm at $6.2 trillion.

Nate Geraci, president of NovaDius Wealth Management, emphasized that distribution is “king in the ETF space.” He noted that combining Morgan Stanley’s vast advisor network with the industry’s lowest fee creates a remarkably strong formula for massive asset gathering.

For growth-oriented portfolios, the firm's advisors are currently recommending a 2% to 4% allocation to Bitcoin, while advising a strict 0% allocation for conservative and income-focused portfolios.

This systematic, firm-endorsed integration into traditional portfolio construction signals a monumental shift in how legacy finance views and utilizes digital assets.

Behind the scenes, MSBT operates strictly on institutional-grade infrastructure. The fund seeks to track the asset's performance as measured by the CoinDesk Bitcoin Benchmark 4PM NY Settlement Rate.

To ensure security and operational efficiency, Morgan Stanley tapped Coinbase and BNY to provide digital asset custody services, with BNY additionally serving as the administrator handling accounting, recordkeeping, and cash management.

Amy Oldenburg, head of digital asset strategy at Morgan Stanley, captured the firm's thesis, noting that MSBT reflects a firmwide approach to “thoughtfully building digital asset capabilities grounded in traditional governance and market infrastructure that seeks to meet long-term client needs.”

Market outlook for MSBT

This measured institutional approach aligns seamlessly with the current macroeconomic backdrop.

Bitcoin’s newest traditional finance wrapper arrives as the underlying digital asset consolidates near the crucial $70,000 level.

This represents a healthy cooling-off period following the cryptocurrency's most recent all-time high above $126,000, presenting a potential accumulation window for traditional capital that may have missed the earlier, retail-driven run-up.

Investor interest in risky assets got off to a slightly sluggish start in 2026, though demand for Bitcoin ETFs showed signs of recovery. The nine funds saw $1.3 billion in aggregate inflows in March, pushing cumulative assets across all American Bitcoin ETFs past the $90 billion mark.

Still, Balchunas predicts the MSBT fund could eventually amass $5 billion in assets under management in its first year of operation.

Despite the monumental launch and strategic advantages, questions remain about whether MSBT can truly topple the established early movers.

BlackRock currently dominates the space, holding over $55 billion in net assets in its IBIT fund. When asked if MSBT could eventually surpass BlackRock's behemoth, Balchunas was blunt, saying:

“Outside of a miracle, no.”

Whether MSBT can sustain its initial momentum against IBIT’s deep liquidity and dominance of the options market will ultimately determine whether Wall Street’s direct entry fundamentally reshapes the competitive balance.

But for now, the arrival of a legacy titan into the arena stands as undeniable confirmation of BTC's permanent fixture in traditional finance.

The post Morgan Stanley’s new Bitcoin ETF puts pressure on BlackRock’s IBIT after strong debut appeared first on CryptoSlate.

Cryptoticker

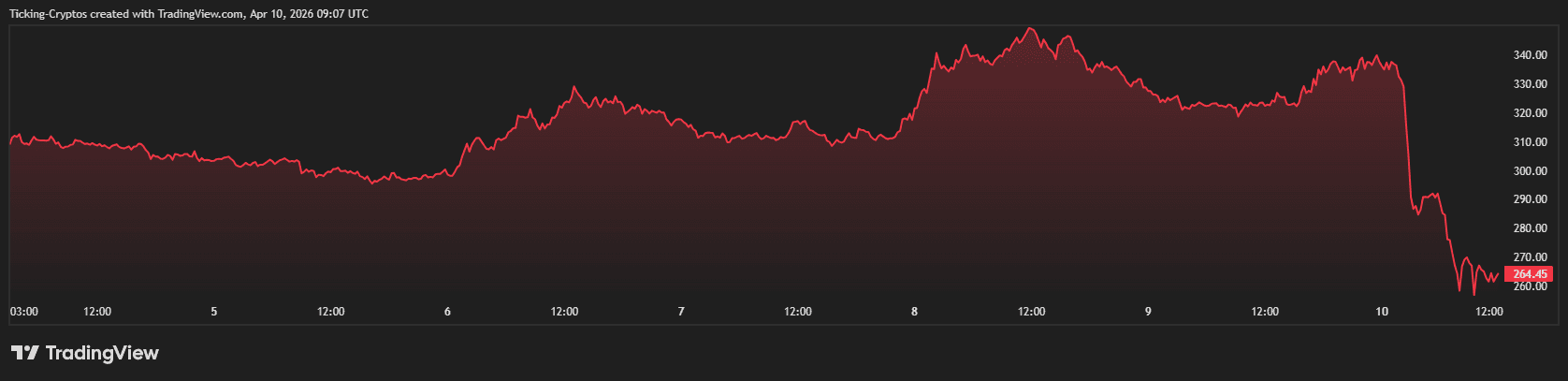

Bittensor (TAO) is currently weathering its most significant crisis to date. In a staggering 12-hour window, the TAO price crashed by 27%, effectively erasing nearly $900 million from its total market capitalization.

The sell-off was triggered by the sudden departure of Covenant AI, one of the network's most prominent contributors. This exit was not a quiet one; the team accompanied their withdrawal with a scathing critique of the protocol's governance, accusing the leadership of maintaining a "decentralized theater" while exercising absolute control.

Did TAO Price Crash?

As of April 10, 2026, the Bittensor ($TAO) price sits at $263, representing a 24-hour decline of approximately 19%. This volatility has resulted in over $9 million in TAO long positions being liquidated, as the market reacted to reports that Covenant AI offloaded 37,000 TAO tokens, valued at more than $10 million.

What is Bittensor and who is Covenant AI?

Bittensor is a decentralized machine learning protocol that allows various "subnets" to compete and provide AI services in exchange for TAO rewards. Covenant AI was the developer behind some of the most successful subnets, including Subnet 3 (Templar), which recently made headlines for training large-scale AI models on decentralized infrastructure.

Why did Covenant AI Abandon Ship

The turmoil began when Sam Dare, founder of Covenant AI, published an open letter announcing the immediate withdrawal of their three subnets: Templar, Basilica, and Grail. The decision comes after months of behind-the-scenes friction regarding how the network is managed.

According to the statement, Covenant AI alleges that:

- Centralized Control: The founder of Bittensor, Jacob Steeves (known as "Const"), reportedly holds unilateral power over emission schedules.

- Economic Sabotage: The team claims their emissions (rewards) were halted as a punitive measure during a private dispute.

- Market Manipulation: Allegations surfaced that the core team used their large token holdings to apply downward pressure on the market during negotiations.

Market Impact and Liquidations

The exit of such a pivotal player created a vacuum of confidence. According to data from CoinMarketCap, TAO fell from its weekly high near $337 to a local low of $263. This sharp move caught many leveraged traders off guard.

- Total Liquidations: ~$9.2 million (primarily longs).

- Market Cap Loss: ~$880 million in 12 hours.

- Subnet Performance: Related subnet tokens collapsed by over 55% following the news.

Should you Sell TAO Coin?

While the broader AI crypto sector has been bullish throughout early 2026, Bittensor's internal governance issues have created a "decoupling" effect. While competitors are trading on utility and growth, TAO is currently trading on reputational risk.

Investors are now questioning the "Triple Multi-sig" governance structure that Bittensor has long championed. If one of the largest subnet operators can be forced out through administrative pressure, the "decentralized" label becomes difficult to defend.

| Metric | Value (Before Crash) | Value (Current) | Change |

|---|---|---|---|

| TAO Price | $337 | $263 | -21.9% |

| Market Cap | ~$3.1 Billion | ~$2.2 Billion | -$900M |

| Long Liquidations | N/A | $9 Million | Spike |

The road ahead for Bittensor depends on two factors:

- Founder Response: Whether the Bittensor Foundation can provide transparent evidence refuting the centralization claims.

- Subnet Migration: Whether other developers follow Covenant AI's lead or stay to fill the gap left by the Templar subnet.

Japan has officially moved to recognize cryptocurrency as a financial asset. This legislative pivot marks a departure from the previous "payment instrument" classification under the Payment Services Act (PSA), transitioning oversight to the more rigorous Financial Instruments and Exchange Act (FIEA).

The move is not merely a semantic change; it is a strategic maneuver by the Japanese government to integrate digital assets into the traditional financial system. This transition aims to enhance investor protection, foster institutional entry, and significantly reform one of the world's most debated crypto tax regimes.

Japan Crypto News: A New Status for Crypto

To address the core development: Yes, the Japanese Cabinet has approved the bill to reclassify 105 cryptocurrencies—including $Bitcoin and $Ethereum—as financial assets. This bill is expected to pass through the Diet (Japan's parliament) in the second quarter of 2026, with full enforcement slated for early 2027.

From "Money" to "Investment"

Previously, Japan treated crypto as a "property value" used primarily for payments. Under the new framework:

- Old Status (PSA): Regulated as a means of payment, similar to prepaid cards or electronic money.

- New Status (FIEA): Regulated as a financial instrument, putting it on the same legal footing as stocks, bonds, and derivatives.

This reclassification allows for more sophisticated financial products, such as spot Bitcoin ETFs, to potentially gain approval in the Japanese market.

The Tax Revolution: A Flat 20% Rate

One of the most significant implications of this bill is the long-awaited reform of crypto taxation. Historically, Japan has been known for its "punitive" tax rates, where crypto gains were treated as miscellaneous income, subject to progressive rates as high as 55%.

| Feature | Current System (Miscellaneous Income) | New System (Financial Asset) |

|---|---|---|

| Tax Rate | Progressive (Up to 55%) | Flat 20% |

| Loss Carryover | Not allowed | 3-Year Carryforward |

| Separation | Combined with salary | Separate Taxation |