Cryptocurrency Posts

Crypto Briefing

Skepticism over a ceasefire highlights geopolitical tensions, impacting market confidence and delaying potential diplomatic resolutions.

The post Ceasefire odds drop to 1% for April 7 as traders remain skeptical appeared first on Crypto Briefing.

Market skepticism highlights the fragile nature of diplomatic efforts, with potential geopolitical and economic ramifications if talks fail.

The post US, Iran in talks for potential 45-day ceasefire as market skepticism grows appeared first on Crypto Briefing.

Escalating tensions and military posturing suggest a prolonged conflict, impacting regional stability and global geopolitical dynamics.

The post Iran reactivates missile bunkers as US forces’ entry odds rise to 86% by April 30 appeared first on Crypto Briefing.

Rising odds of U.S. military action in Iran highlight escalating geopolitical tensions, potentially destabilizing regional and global security dynamics.

The post Odds of US forces entering Iran by April 30 surge to 86% amid escalating tensions appeared first on Crypto Briefing.

The liquidation highlights market resilience and cautious optimism, but traders remain wary amid geopolitical tensions and uncertain trends.

The post $65M in short positions liquidated as Bitcoin and Ethereum see price bump appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Charles Schwab Teases Direct Bitcoin Trading With New ‘Schwab Crypto’ Account

Financial services giant Charles Schwab is preparing to expand deeper into digital assets, announcing plans for a forthcoming product that will allow clients to buy and sell cryptocurrencies directly through its platform.

The firm revealed that “Schwab Crypto ” is in development and will be offered through Charles Schwab Premier Bank, positioning the product as a gateway for retail investors seeking direct exposure to leading cryptocurrencies such as Bitcoin. The company has opened a waitlist for clients interested in early access, though availability will be subject to regulatory approval and eligibility requirements.

” is in development and will be offered through Charles Schwab Premier Bank, positioning the product as a gateway for retail investors seeking direct exposure to leading cryptocurrencies such as Bitcoin. The company has opened a waitlist for clients interested in early access, though availability will be subject to regulatory approval and eligibility requirements.

The move marks a notable shift for Schwab, which until now has limited crypto exposure to indirect investment vehicles. Currently, clients can access digital asset markets through exchange-traded products (ETPs), crypto-related equities, and thematic funds. Examples include publicly traded firms like Coinbase, MicroStrategy, and Riot Platforms, as well as funds tied to blockchain and crypto industry performance.

All aboard the Charles Schwab Bitcoin train

Schwab’s entry into spot trading places it in more direct competition with established crypto platforms such as Coinbase, Robinhood, and Webull.

CEO Rick Wurster first signaled the firm’s intent to enter spot crypto markets in late 2024, citing expectations for a shifting regulatory environment under the administration of Donald Trump. The company has since positioned itself to move once conditions allowed for broader participation by traditional financial institutions.

Schwab is also preparing additional crypto-related products, including a potential stablecoin offering following the passage of the GENIUS stablecoin bill.

A recent report from Charles Schwab found that Bitcoin volatility has declined significantly, with historical volatility falling to 42% in 2025 — about half its 2021 level — making it comparable to or lower than major tech stocks like Tesla and Nvidia.

Despite fewer extreme swings, bitcoin still experiences sharp drawdowns, including a 32% drop in 2025 and a 50% peak-to-trough decline over three years.

Long term, volatility remains elevated versus traditional assets. The report suggests bitcoin is maturing as it integrates into mainstream finance, with growing institutional adoption and ETF developments signaling increased acceptance.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Charles Schwab Teases Direct Bitcoin Trading With New ‘Schwab Crypto’ Account first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Jack Dorsey Reveals Bitcoin Faucet Revival with “Bitcoin Day” Announcement

Tech entrepreneur and longtime Bitcoin advocate Jack Dorsey sparked excitement in the BTC community on Friday when he posted a link to a new page titled “Bitcoin Day | Earn Free Bitcoin.”

The post quotes an announcement from the “Bitcoin at Block” account stating that “The bitcoin faucet is back” on April 6, 2026, with a link to btc.day. Dorsey’s shared URL (hosted on AWS CloudFront) currently displays only the bold headline promoting free BTC on “Bitcoin Day,” with a countdown timer.

No further details were given.

In 2010, a site known as the Bitcoin Faucet gave visitors 5 BTC after they completed a simple captcha challenge. This was done to help spread awareness and use of BTC, which at the time was a new digital currency with almost no market value.

The site was created by Gavin Andresen, a software developer who later became one of BTC’s lead developers. Andresen loaded the faucet with his own BTC to distribute to visitors who solved the CAPTCHA.

Over the months the faucet operated, it handed out about 19,700 BTC in total. At today’s prices, that amount would be worth in the billions of dollars.

Bitcoin’s rough price performance

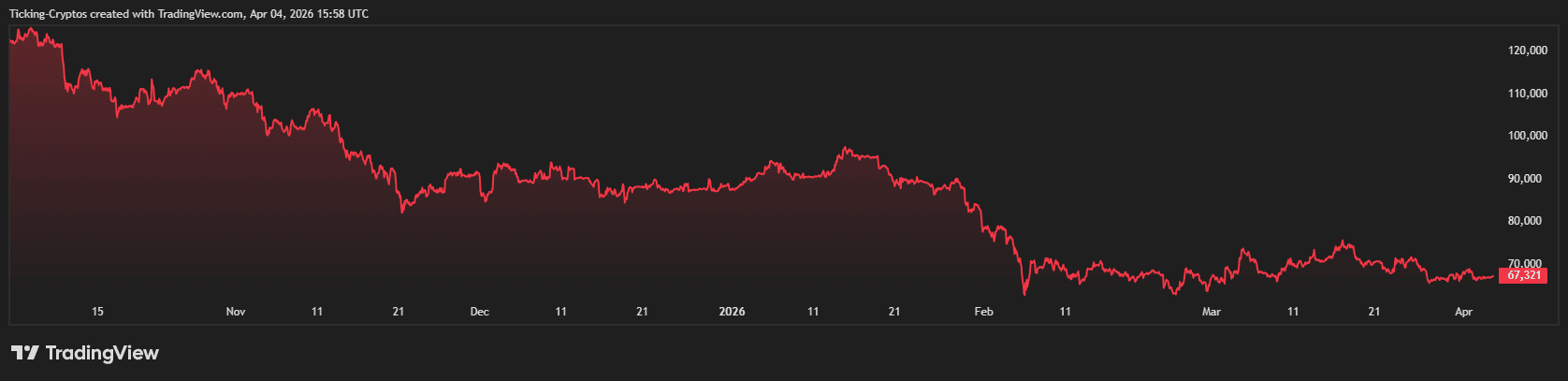

Over the past six months, BTC has experienced one of its weakest performance periods in years, with the price declining sharply from late 2025 highs. According to price history data, BTC’s value is down roughly 50% over the last half-year, reflecting a significant drawdown from levels above $120,000 in November 2025 to around the mid-$60,000s today.

BTC’s retreat has erased gains made earlier in the cycle and marked its worst six-month streak since 2018, driven by a mix of macroeconomic headwinds and reduced risk appetite among investors.

In March, it seems like the price stabilized near the high $60,000s, with market participants watching key technical levels and macro signals for clues on the next move.

Block has held 8,883 BTC since October 6, 2020, currently worth about $593.74 million at an average cost of $32,939 per BTC, for a gain of roughly +102.92% at today’s prices.

The company, trading under ticker XYZ, has a market cap of about $36–$37 billion. At the time of writing, BTC is trading near $67,000.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Jack Dorsey Reveals Bitcoin Faucet Revival with “Bitcoin Day” Announcement first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Cathie Wood Calls Bitcoin’s 50% Crash a “Victory” as Market Tests New Floor

Nearly six months after the Oct. 10 flash crypto crash erased millions of dollars in a single day, Bitcoin remains under pressure, trading well below its recent peak. The asset reached an all-time high of $126,080 on Oct. 6, but has since fallen about 47% to roughly $67,000.

Despite the drawdown, Cathie Wood, a long-time BTC advocate and chief executive of ARK Investment Management, is urging investors to maintain a long-term perspective.

Wood, whose firm was among the first publicly listed asset managers to gain exposure to Bitcoin in 2015, has maintained an active presence in crypto-related equities. ARK Invest continues to trade shares of companies tied to the digital asset sector, including Coinbase, Robinhood Markets, Block, Circle Internet Group, Bitmine Immersion Technologies, and Bullish, adjusting positions in response to market conditions.

In an interview on CNBC’s Squawk Box, Wood addressed the current downturn, framing the magnitude of BTC’s decline as a sign of maturation rather than weakness.

She argued that a roughly 50% drop from peak levels represents a shift from the extreme volatility seen in earlier cycles, when Bitcoin routinely experienced drawdowns of 85% to 95%.

NEW: Ark Invest CEO Cathie Wood says on CNBC that Bitcoin's usual -85% collapses are "DONE"

— Bitcoin Magazine (@BitcoinMagazine) April 3, 2026

"This is a prove technology, it's a proven monetary system, and it's a new asset class."pic.twitter.com/j0OU62hWmj

According to Wood, such severe collapses are unlikely to recur. She described Bitcoin as a “proven technology” and a “new asset class,” suggesting that its market behavior has evolved alongside broader adoption and institutional participation.

In her view, the current correction would be considered a “real victory” within the Bitcoin community if losses remain limited to around half of its peak value.

Bitcoin’s vicious cycles

Historical data supports the comparison to prior cycles, though the current downturn has yet to match earlier bear markets in severity. During the 2021–2022 cycle, Bitcoin fell nearly 80% from its then-record high of about $69,000, eventually bottoming near $15,600.

Onchain data from Glassnode indicates that the present decline, measured against the October 2025 high, has reached roughly 52% at its lowest point.

All this is happening as bitcoin’s price decline forces a growing number of public companies and sovereign entities to unwind their BTC treasuries, marking a sharp reversal from the accumulation trend of the past two years. Firms that once championed long-term holding are now selling to manage liquidity, repay debt, and fund strategic pivots.

Companies like Riot Platforms, Genius Group, Empery Digital, Nakamoto Holdings, and Marathon Digital have all reduced holdings, in some cases significantly. Marathon alone sold over 15,000 BTC for $1.1 billion to cut debt, while Genius Group fully exited its position. Riot has also been offloading bitcoin as it shifts focus toward AI and high-performance computing infrastructure.

Even firms still committed to bitcoin are trimming reserves. Empery Digital sold part of its holdings to repay loans, while Nakamoto Holdings liquidated a smaller portion to support operations. Meanwhile, Bhutan has been reducing its state-backed bitcoin reserves after previously accumulating through mining.

Despite the sell-off, public companies still collectively hold about 1.16 million BTC, over 5% of the total supply.

This post Cathie Wood Calls Bitcoin’s 50% Crash a “Victory” as Market Tests New Floor first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts Toward AI Infrastructure

Riot Platforms sold 3,778 bitcoin in the first quarter of 2026, generating $289.5 million and marking a shift in strategy as the miner redirects capital toward infrastructure and high-performance computing.

The volume sold exceeded the company’s quarterly production of 1,473 BTC by roughly 2.6 times, signaling a drawdown of treasury holdings rather than routine profit-taking. Riot ended the quarter with 15,680 BTC, down 18% from 18,005 BTC at the close of 2025.

The selling appears to have extended beyond the reporting period. Blockchain analytics firm Arkham Intelligence flagged a 500 BTC outflow from a wallet linked to Riot following the end of the quarter, suggesting continued liquidation activity.

The imbalance between production and sales comes as Riot accelerates its expansion into artificial intelligence and high-performance computing colocation. The company has begun repositioning its business model away from sole reliance on bitcoin mining, seeking to monetize its energy assets and data center footprint through long-term infrastructure contracts.

In January, Riot sold 1,080 BTC to fund the purchase of 200 acres at its Rockdale, Texas site. It also entered a ten-year agreement with Advanced Micro Devices to provide 25 megawatts of capacity, with an option to scale to 200 MW. The deal is expected to generate about $311 million in contract revenue over its initial term.

Operational metrics complicate a distress narrative. Riot reduced its all-in power cost to 3.0 cents per kilowatt hour, a 21% decline from the prior year, while increasing deployed hash rate by 26% to 42.5 exahashes per second. Average operating hash rate rose 23% to 36.4 EH/s, reflecting continued investment in mining capacity.

The company also generated $21 million in power credits during the quarter, more than double the year-ago period, through participation in grid services and energy programs.

Bitcoin HODLers like RIOT are selling

Industry conditions remain a factor. Rising energy costs tied to geopolitical tensions have pressured margins across the mining sector, prompting several operators to liquidate holdings. MARA Holdings, Genius Group, and Nakamoto Holdings collectively sold more than 15,000 BTC in recent days, reflecting a broader shift in capital allocation.

Riot’s Q1 activity underscores a turning point for the sector, where bitcoin reserves are deployed as funding sources for diversification rather than held as long-term balance sheet assets.

The trend extends beyond corporate treasuries. Bhutan has continued to reduce its BTC holdings, selling a total of 3,103 BTC. A single transaction on March 30 accounted for 375 BTC, according to Glassnode data.

The country had built its position through state-backed mining operations, reaching more than 13,000 BTC at its peak in October 2024.

Despite the recent selling, public companies still hold about 1.16 million BTC, or more than 5% of bitcoin’s fixed supply of 21 million, according to BitcoinTreasuries.net.

This post Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts Toward AI Infrastructure first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

The Bitcoin Treasury Model With a Built-In Valuation Floor

There is a version of the Bitcoin treasury conversation that has become almost routine at this point. Bitcoin is hard money. Fiat debases. Companies that hold Bitcoin on their balance sheet are making a rational long-term decision. All of this is true, and none of it is the interesting question anymore.

The interesting question is structural. Not should a company hold Bitcoin, but what kind of company should hold it, and what that choice implies for how the company performs across a full market cycle, not just a favorable one.

Three models have emerged. Each reflects a different level of conviction, a different capital structure, and a different set of tradeoffs.

- The pure-play. A company whose primary purpose is accumulating Bitcoin through capital raises, financial engineering, etc, with no core operating business. Lean structure, singular mission.

- The digital credit issuer. The most sophisticated expression of the pure-play thesis. These companies issue Bitcoin-backed financial instruments, preferred stock, convertible notes, and similar products, to fund continued accumulation. At scale, this creates a compounding accumulation engine that simpler models cannot match.

- The operating company with a Bitcoin treasury. A business with real revenue, real clients, and operational activity, which holds Bitcoin as a long-term reserve asset in deliberate strategic relationship with the business itself.

All three are legitimate expressions of the Bitcoin treasury thesis. They are not optimized for the same objectives, and the differences matter more than most treasury conversations acknowledge.

What pure-play gets right

The pure-play case deserves genuine treatment because its strongest version has real force.

Financial engineering pure-plays are capital-efficient in a specific and important sense: every dollar raised goes directly to Bitcoin accumulation with no operational drag. The mission is singular and the structure reflects it. For investors, this creates clarity. Allocators know exactly what they are underwriting, direct Bitcoin exposure at the corporate level, and the investment thesis is legible and short.

The digital credit model extends this further. Companies that have successfully issued preferred instruments and Bitcoin-backed products have built accumulation engines that operating businesses cannot match on a per-dollar-raised basis. The compounding effect of a sophisticated capital structure, at scale, is genuinely powerful. It represents the fullest expression of the Bitcoin treasury thesis, and the destination it points toward is one every operator in this space should understand.

The prerequisite problem and what it means in practice

The digital credit model has a prerequisite that is rarely stated plainly: it requires scale, institutional credibility, and market infrastructure that most companies building a Bitcoin treasury today do not yet have. It is a destination, not a starting point.

The path there runs through an intermediate period where the financial engineering structure carries more exposure than is often acknowledged. During that period:

- There is no operating revenue to fall back on

- The ability to raise capital tracks closely with Bitcoin market sentiment

- Strategic options narrow when conditions are not favorable

- The company’s cost structure depends entirely on capital markets remaining open

This is not a criticism of the model. It is a description of the journey. The question for executives is what structure best serves the company while that journey is underway.

What the operating company model actually provides

The operating company with a Bitcoin treasury does not accumulate Bitcoin faster than a well-run pure-play. At meaningful treasury scale, operating cash flow is not moving the needle on accumulation. The advantage is different, and worth stating precisely.

An operating business generates revenue independently of where Bitcoin is trading. That revenue covers fixed costs, which means the company is not dependent on capital markets remaining open to fund its basic operations. It can continue hiring, serving clients, and accumulating at a measured pace without being forced into capital decisions driven by timing rather than conviction.

The compounding effect works like this:

- Operating revenue covers costs and preserves the Bitcoin position through the cycle rather than drawing it down under pressure

- A preserved balance sheet improves the terms on future capital raises, lower dilution, better access to facilities, stronger negotiating position with partners

- Operational credibility widens the available capital base by providing an investment thesis that reaches allocators who cannot underwrite pure Bitcoin exposure within their current mandates

None of these mechanisms make Bitcoin accumulate faster in favorable conditions. Together, they make the company more durable across the full range of conditions it will face.

The built-in valuation floor

Most Bitcoin treasury company valuations are driven by a single number: mNAV, the premium the market assigns to Bitcoin held at the corporate level. When sentiment is strong and capital is flowing into the space, that premium expands. When the narrative cools, it compresses. The valuation moves with the market’s appetite for Bitcoin exposure, not with anything the company is doing operationally.

The operating company model introduces a second component that behaves differently. A profitable operating business carries an earnings multiple underwritten by revenue, client relationships, and operational track record. It does not expand dramatically when Bitcoin is performing. But it does not compress when sentiment turns either. It is stable in a way that mNAV alone is not.

These two components, Bitcoin NAV and an earnings multiple on the operating business, do not move together. That is the point. When mNAV compresses, the earnings multiple holds. The company retains a defensible valuation floor that a pure-play structure, with a single-component valuation entirely dependent on sentiment, does not have.

In practice this matters in three specific ways:

- Capital raises. A company with a defensible valuation floor can raise capital on reasonable terms even when Bitcoin sentiment is cold. A pure-play with a compressed mNAV and no earnings component has less room to maneuver.

- Talent. Equity compensation tied to a two-component valuation is a more legible and stable proposition for prospective hires than equity tied entirely to Bitcoin’s market sentiment.

- Allocator access. Many institutional allocators cannot underwrite a valuation built entirely on mNAV within their current mandates. The earnings component creates a bridge, opening the door to capital that would otherwise be unable to participate regardless of conviction.

The floor is not just a comfort during difficult conditions. It is a structural advantage that compounds over time, widening the capital base, strengthening the talent proposition, and maintaining strategic momentum across the full cycle.

How to think about the decision

These three models serve different objectives. The right framework starts with honest answers to a few questions:

- What does the existing business look like? A company with established revenue and clients already has the foundation for the operating company model. A company without it is choosing between building that foundation and committing to a pure-play path.

- What is the realistic path to scale? The digital credit model is the most powerful expression of the thesis but requires scale and credibility that takes time to build. The operating company model does not depend on reaching that threshold to function well.

- What does the investor base look like? Pure-play structures appeal most clearly to allocators who want direct Bitcoin exposure. Operating companies reach a broader set of capital partners, including those whose mandates require an operating business to participate.

- What kind of company do you want to be running across a full cycle? This is the question underneath all the others. The answer should drive the structure, not the other way around.

Conclusion

The companies that define the next era of corporate Bitcoin adoption will not all look the same. Digital credit issuers will operate at the frontier of Bitcoin-native capital markets. Financial engineering pure-plays will build toward that destination with focused conviction. Operating companies will build businesses where the treasury and core operations strengthen each other across the cycle.

Each model is a genuine expression of the thesis. The goal of this framework is to make the differences legible, so executives can choose the structure that fits what they are actually building, with clear eyes about what each model asks of them in return.

The question was never which model holds the most Bitcoin. It was always which model fits what you are trying to build.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

This post The Bitcoin Treasury Model With a Built-In Valuation Floor first appeared on Bitcoin Magazine and is written by Nick Ward.

CryptoSlate

Wall Street spent the first quarter of 2026 systematically narrowing DeFi's claim to the future of finance.

In January, ICE announced NYSE was building a tokenized securities platform with 24/7 operations, instant settlement, dollar-based order sizing, and stablecoin funding, with BNY and Citi providing tokenized deposits for clearinghouse funding outside normal banking hours.

In February, WisdomTree launched 24/7 trading and instant settlement for tokenized money-market fund shares under SEC relief.

In March, the Fed, FDIC, and OCC jointly said that eligible tokenized securities should receive the same capital treatment as their non-tokenized counterparts, calling the framework technology-neutral.

The SEC then approved Nasdaq's proposal to trade certain securities in tokenized form, with settlement through DTC.

NYSE and Securitize followed with a partnership to build digital transfer-agent infrastructure around institutional operating standards.

That sequence did something concrete to DeFi's competitive position. Regulated exchanges, broker-dealers, and bank-backed clearinghouses can now package 24/7 trading and on-chain settlement inside a supervised market structure, with the capital treatment to match.

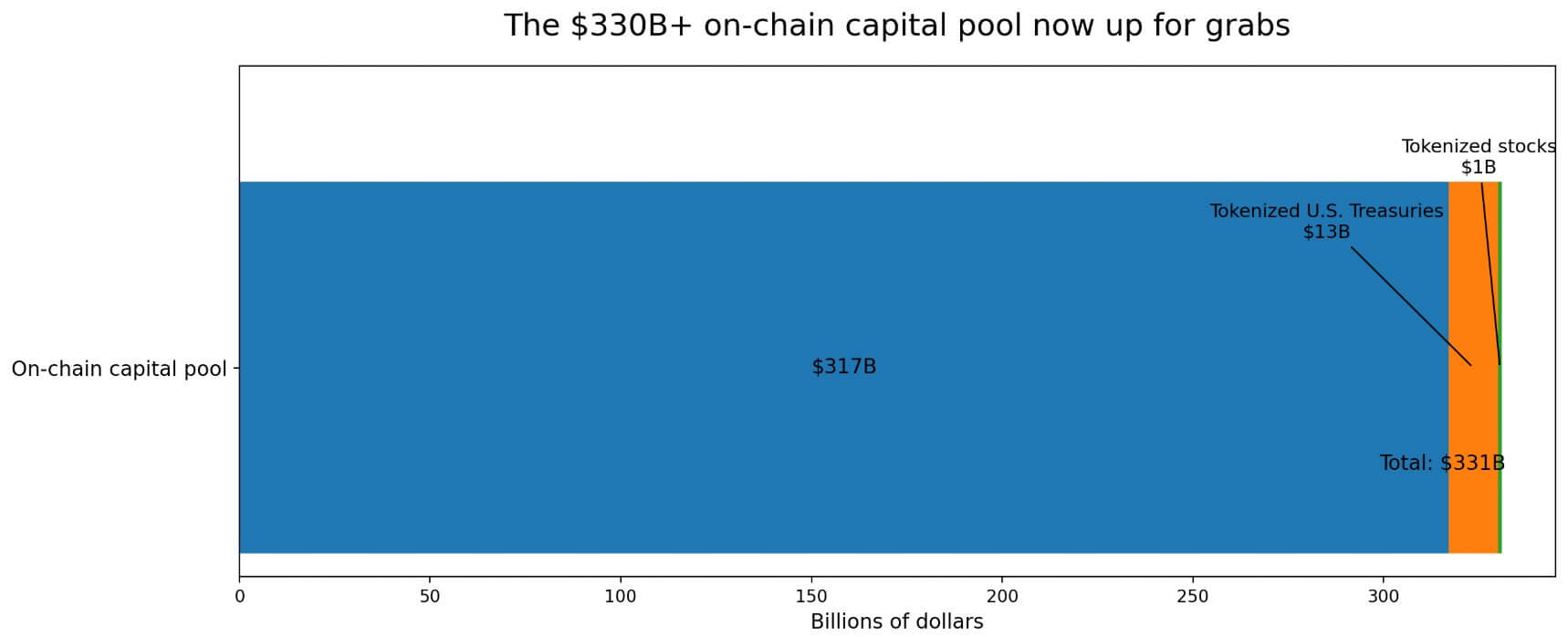

The base pool of on-chain capital these moves target already exceeds $330 billion, including stablecoins at roughly $317 billion, tokenized US Treasuries at nearly $13 billion, and tokenized stocks at $1 billion.

That pool will attract institutional capital regardless of which rails it flows through.

Why this matters: the contest is no longer over whether finance will move on-chain. It is over who captures the capital once it does. If regulated venues can offer blockchain-based trading and settlement without DeFi’s governance and control-layer risks, open protocols have to prove why institutions should accept the added exposure.

Composability is DeFi's distinct advantage: the ability to build interconnected financial products on shared, permissionless infrastructure, where any protocol can connect directly to any other on open terms.

It is a genuinely DeFi-native feature. Nasdaq-approved tokenized securities still settle through DTC, are subject to exchange surveillance, and operate under existing order types and reporting frameworks.

WisdomTree's tokenized fund sits inside a broker-dealer model. NYSE designed its tokenized platform around transfer agents and institutional operating standards. All of those architectures require a central gatekeeper to approve downstream connections.

Drift and the control-layer problem

Composability's value as a moat depends entirely on whether capital allocators believe the surrounding controls are mature enough to contain localized failures.

Drift's exploit exposed that dependency in the most direct way possible. Drift confirmed the attack exploited durable nonces and a takeover of Security Council administrative powers through a compromise of the access-control layer.

DefiLlama classified the incident as a $285 million hack driven by compromised admin access and price manipulation. Drift's total value locked fell from roughly $550 million to below $250 million.

The contagion framing from post-incident analysis is where the competitive argument becomes sharpest.

Because Drift's infrastructure is connected to downstream vaults, yield strategies, wrappers, and collateral positions across Solana DeFi, the administrative compromise radiated outward before the exposure map was clear.

Chaos Labs publicly said hidden dependencies kept surfacing in real time, leaving the final exposure tally open. Composability, functioning as a transmission channel for losses, precisely drives institutional capital allocators toward permissioned tokenization infrastructure over open protocol stacks.

The Drift incident fits a pattern that extends well beyond Solana.

Chainalysis found that private key compromises accounted for 43.8% of stolen crypto in 2024, the single-largest attack category it tracked.

TRM Labs said attackers stole $2.87 billion across nearly 150 hacks in 2025, with infrastructure attacks targeting keys, wallets, and access control planes driving the majority of losses and outpacing smart contract exploits.

TRM also noted the top 10 incidents accounted for 81% of 2025 hack losses.

The empirical record says the control layer, the governance layer, and the access management layer now carry more systemic risk than contract code alone. DeFi's security culture is still catching up to that empirical record.

| Signal | Article detail | Why it matters |

|---|---|---|

| Drift exploit size | $285M | Large enough to become a sector-wide risk event |

| Attack vector | Durable nonces + takeover of Security Council administrative powers | Shows the failure was in the control layer, not just contract logic |

| DefiLlama classification | Compromised admin access + price manipulation | Reinforces governance/access risk framing |

| TVL impact | From roughly $550M to below $250M | Shows immediate market damage and confidence loss |

| Contagion channel | Vaults, wrappers, yield strategies, collateral positions | Highlights how composability can transmit losses |

| Chaos Labs takeaway | Hidden dependencies kept surfacing in real time | Supports the argument that exposure was not fully visible upfront |

| Broader pattern | Private-key and infrastructure attacks dominate hack losses | Places Drift inside a larger industry trend |

What DeFi has to do

Open composability must adopt the corrective to compete for the institutional capital now pooling on-chain.

Drift's post-incident analysis and the broader Chaos Labs framing converge on the same operational list: stricter signer standards, timelocks on privileged transitions, segmented permission structures so that one compromised key cannot reach the entire control surface, explicit dependency mapping so downstream integrations are visible before a failure occurs, and faster public disclosure that lets the broader network act before contagion spreads.

Post-mortems show Drift's administrative transition used a 2-of-5 multisig with no timelock. This configuration compressed the approval window for a catastrophic change to the point where detection and intervention had no time to operate.

Those fixes are unglamorous. They build the operational credibility that makes a CFO or risk committee comfortable routing institutional capital through open infrastructure.

ICE, Nasdaq, and NYSE are competing for the same pool. The protocols that earn a share of it will be the ones that can demonstrate composability with contained, visible risk, where an interconnection means expanded utility.

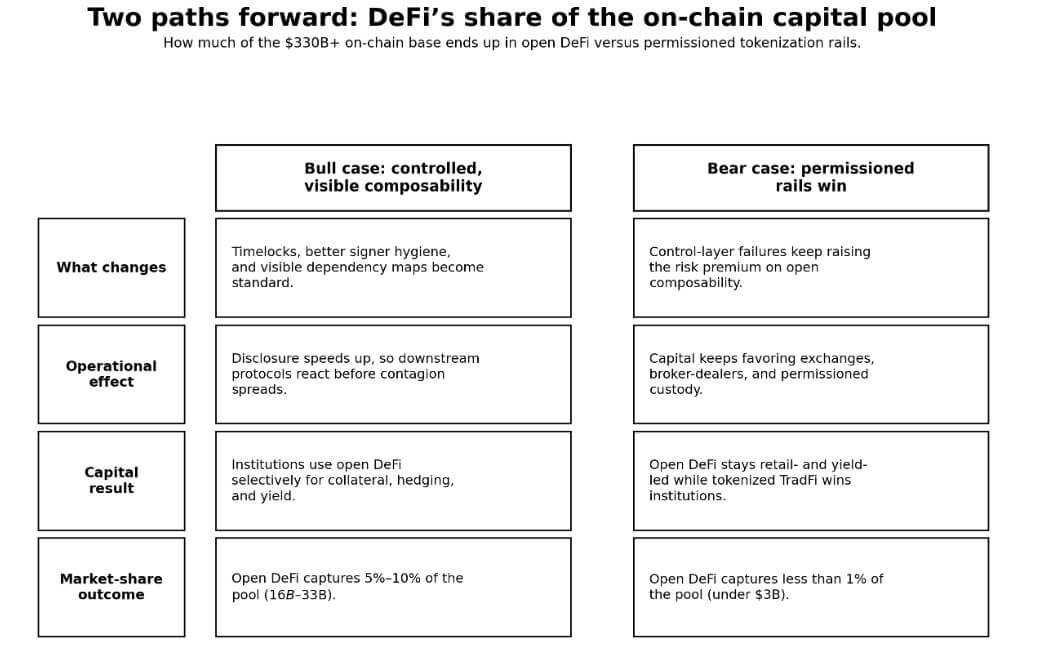

Two paths forward

The on-chain capital base currently sits above $330 billion and will grow as tokenized securities and stablecoin adoption expand.

The contest is over what fraction of that pool flows through open, composable DeFi versus permissioned or semi-permissioned tokenization infrastructure.

In the bull case, DeFi protocols produce a visible, sustained upgrade in governance discipline: timelocks become standard for privileged transitions, signer hygiene improves across major protocols, teams publish dependency maps that let external allocators assess integration risk before committing capital, and disclosure lags shorten from days to hours.

Institutional allocators begin using open composability selectively for structured collateral, cross-protocol hedging, and yield strategies where the control layer is demonstrably stronger than before.

Open DeFi captures 5% to 10% of the on-chain capital pool, or roughly $16 billion to $33 billion. Composability becomes the premium layer atop the tokenization rails that traditional finance is building, running alongside a supervised market structure.

In the bear case, each successive control-layer incident raises the perceived risk premium on open composability faster than the industry can close the governance gap.

Tokenized securities, tokenized funds, and stablecoin settlement volumes have expanded, while capital stays within exchanges, broker-dealers, and permissioned custody structures.

Open DeFi captures less than 1% of the pool, with total assets of less than $3 billion. Traditional finance captures the blockchain upside through tokenization, faster settlement, and extended hours, while open composability captures retail flows and reflexive capital seeking yield on open infrastructure.

Wall Street spent 2025 and the early part of 2026 proving that blockchain rails can carry institutional assets within supervised frameworks.

DeFi's path to winning requires proving that open interconnection is worth the additional governance, disclosure, and control overhead imposed by regulatory mandates on supervised venues.

The post As Wall Street moves on-chain, DeFi faces a $330 billion trust test it can’t dodge appeared first on CryptoSlate.

Algorand has emerged as an early standout in the crypto market’s latest quantum security debate after a recent Google Quantum AI paper highlighted the blockchain as a live example of post-quantum cryptography being deployed on a network.

The attention came as the paper sharpened concerns around Bitcoin and Ethereum, two networks whose size, age, and design choices could make any future migration to quantum-resistant infrastructure slower and more complicated.

Against that backdrop, Algorand’s quieter work on Falcon digital signatures, state proofs, and key rotation suddenly looked less like a niche technical experiment and more like a practical head start.

The shift in attention helped lift Algorand’s token sharply over the past week, with traders treating the Google paper as validation of work already underway on the network.

According to CryptoSlate's data, ALGO, the blockchain network's native token, is one of the top performers over the past week, gaining around 50% to rise to $0.12 as of press time. Notably, the price performance came less than a week after the token fell to an all-time low of $0.08.

Algorand's quiet quantum computing lead over Bitcoin and Ethereum

Algorand’s advantage over Bitcoin and Ethereum is narrower than the recent enthusiasm suggests, but it is also more concrete than what many larger chains can currently show.

In its paper, Google described Algorand as an example of real-world deployment of post-quantum cryptography on an otherwise quantum-vulnerable blockchain.

The distinction was important. It did not say Algorand had solved the problem end-to-end, but it did point to a network that had moved from theory into live implementation.

Algorand’s core consensus and built-in transactions still rely on Ed25519, which remains vulnerable in a sufficiently advanced quantum scenario.

However, the network has already deployed Falcon digital signatures for smart transactions and state proofs, the cryptographic attestations used to verify blockchain state across chains. It has also made Falcon verification available as a primitive for developers building on the Algorand Virtual Machine, giving the ecosystem a working set of tools rather than just a roadmap.

The network executed its first post-quantum-secured transaction in 2025, a milestone that set it apart from many larger rivals that are still debating design paths, governance trade-offs, and implementation timelines.

Algorand also allows users to rotate the private keys associated with their accounts, a feature that does not eliminate the underlying threat but could make future migrations more manageable.

That combination, live transaction capability, developer tooling, state-proof support, and native key rotation, is what turned Algorand into a focal point as the paper circulated through the market.

In a sector where many conversations around quantum risk remain theoretical, Algorand could point to infrastructure already in production.

Bitcoin and Ethereum face quantum computing risk

For Bitcoin, the concern is not only whether quantum computers will eventually be able to derive private keys from public information, but also how much of the network’s legacy footprint would be difficult to migrate in time.

The paper said a quantum computer with fewer than 500,000 physical qubits could crack the elliptic-curve cryptography protecting Bitcoin wallets, a far lower threshold than earlier estimates that ran into the millions.

Google’s own most advanced chip, Willow, remains far below that level, but the revised estimate has intensified scrutiny of how much Bitcoin could be exposed if the technology advances faster than expected.

The burden is particularly acute because some of Bitcoin’s oldest addresses keep public keys visible on-chain.

The paper cited an estimated 6.7 million BTC in older Pay-to-Public-Key addresses, including coins long associated with Bitcoin creator Satoshi Nakamoto.

Even outside those legacy wallets, the migration challenge is politically and technically heavy for a network that prioritizes backward compatibility and moves cautiously on base-layer changes.

Quantum risk, in Bitcoin’s case, is as much a governance and coordination problem as it is a cryptographic one.

Meanwhile, Ethereum’s exposure to the same quantum computing risk is somewhat broader.

Once an Ethereum user sends a transaction, the public key tied to that account becomes permanently visible on-chain. The paper said that this leaves the top 1,000 Ethereum wallets, holding roughly 20.5 million ETH, exposed under a sufficiently advanced quantum attack.

It also identified at least 70 major contracts with administrator keys visible on-chain, which ultimately control far more than the ETH they directly hold, including stablecoin minting authority and other system-critical permissions.

Moreover, the attack surface extends beyond wallets and contract administrators.

Ethereum’s proof-of-stake validator set, major Layer 2 networks, and parts of its data-availability architecture all rely on cryptographic components the paper described as vulnerable.

According to the paper, roughly 37 million ETH is staked, and much of Ethereum’s transaction load now flows through rollups and bridges that inherit assumptions from the base layer.

That means any serious post-quantum migration would have to reach not only users and validators, but also the network of applications and scaling systems built around them.

The post Algorand just jumped 50% after Google flags quantum risk for Bitcoin and Ethereum appeared first on CryptoSlate.

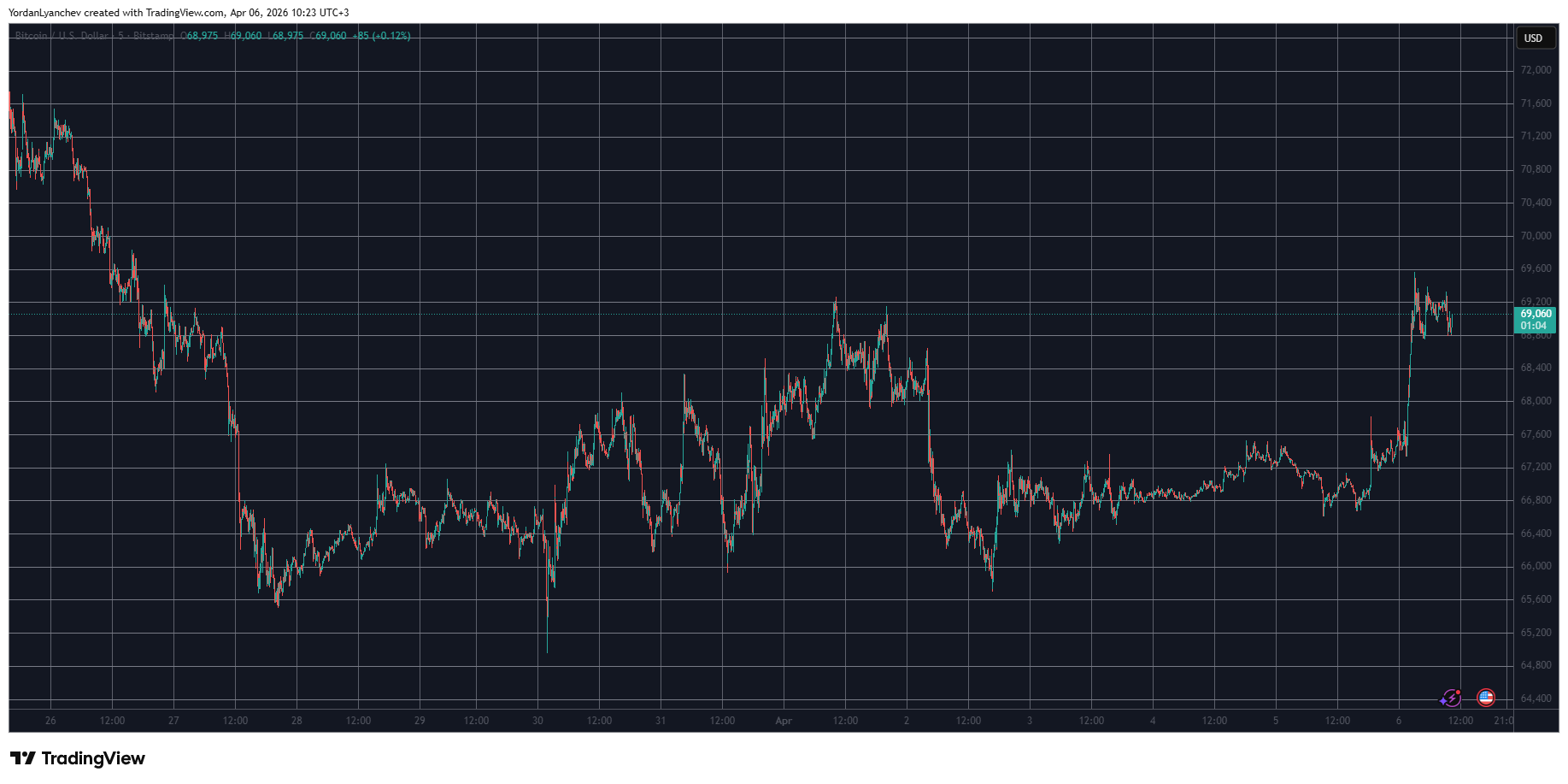

The US economy added 178,000 jobs in March, nearly three times the consensus estimate of 60,000, and unemployment dipped to 4.3%. That is the kind of print that resets macro narratives and hits risk assets before traders finish their first read.

Bitcoin traded around $67,000, unfazed by the data. The 10-year Treasury yield climbed four basis points to 4.35%, and the dollar index ticked up to 100.08.

The market's first-order read was straightforward: a labor market that looks this strong gives the Federal Reserve less reason to cut, which in turn yields tighter financial conditions and weighs on a macro-sensitive asset like Bitcoin.

Why this matters: Bitcoin reacted to more than a jobs beat. The signal was a stronger labor market that reduces the Fed’s urgency to cut rates. If that view holds, yields and the dollar can stay firm, maintaining pressure on liquidity-sensitive assets like BTC.

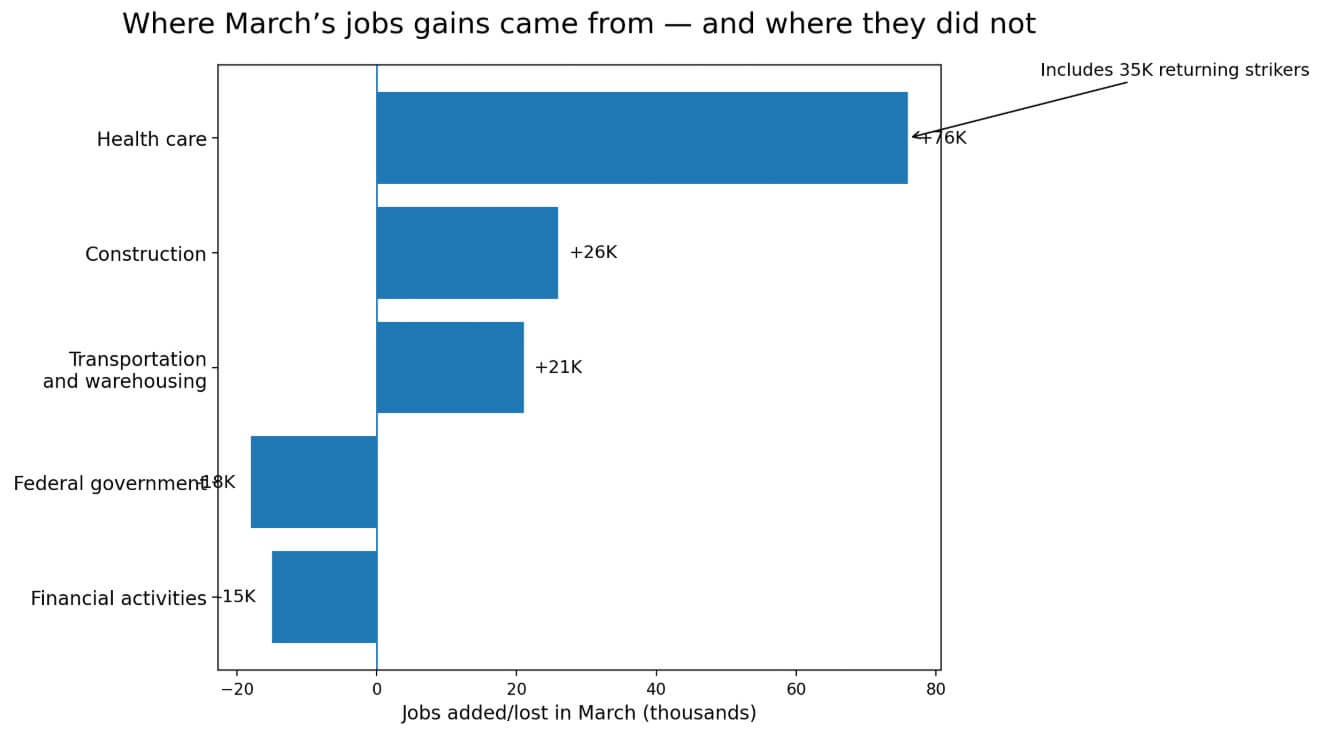

Zoom in on where those 178,000 jobs came from, and the picture gets less clean. Health care alone added 76,000 positions, and 35,000 of those were workers returning from a strike in physicians' offices. The numbers represented a catch-up hiring.

Construction added 26,000, partly weather-aided, and transportation and warehousing contributed another 21,000. Federal government employment fell by 18,000, and financial activities shed 15,000.

BLS noted that total payroll employment had moved little on net over the prior 12 months.

That backdrop makes March read as a rebound from a noisy February, with sector-specific catch-up doing most of the lifting.

The household survey runs the other way

The household survey, which tracks employed and unemployed individuals across the population, moved in the opposite direction from the payroll numbers.

The civilian labor force contracted by 396,000 in March, with participation falling to 61.9%. Household employment declined by 64,000, and the number of people not in the labor force rose by 488,000.

Marginally attached workers jumped 325,000 to 1.9 million, and discouraged workers climbed 144,000 to 510,000. The average workweek is shortened to 34.2 hours.

Average hourly earnings rose just 0.2% month over month and 3.5% year over year, with no wage acceleration to complement the payroll beat.

| Indicator | March reading | Why it matters |

|---|---|---|

| Nonfarm payrolls | +178K | Strong headline beat versus expectations |

| Unemployment rate | 4.3% | Makes the labor market look firm at first glance |

| Civilian labor force | -396K | Suggests weaker labor-market participation beneath the headline |

| Labor-force participation rate | 61.9% | Fewer people working or looking for work |

| Household employment | -64K | The people-based survey moved opposite the payroll survey |

| Not in labor force | +488K | Reinforces the softer under-the-hood read |

| Marginally attached workers | +325K to 1.9M | Shows weaker labor attachment at the margin |

| Discouraged workers | +144K to 510K | Signals more workers are giving up on job searches |

| Average workweek | 34.2 hours | A shorter workweek can point to softer labor demand |

| Average hourly earnings | +0.2% m/m, +3.5% y/y | No wage reacceleration to confirm the payroll beat |

February's revision adds another layer. BLS marked February down to -133,000 from -92,000 and revised January up to 160,000 from 126,000. The net two-month revision was only -7,000, making the pattern noisy and lacking a consistent directional pull.

Payroll growth in the first quarter averaged roughly 68,000 per month, a soft pace by any expansion standard.

BLS revises monthly estimates twice as additional employer reports arrive and seasonal factors reset.

Since 2003, the average absolute revision from the first to the third estimate has been 51,000 jobs. A revision of that size would take March from 178,000 to around 127,000, which is noticeably less dramatic.

To erase the entire beat, March would need a job-creation figure exceeding 118,000, roughly 2.3 times the historical average, and ordinary revision noise does not get there.

BLS's annual benchmark revision stripped 898,000 jobs from the March 2025 payroll level, four times the average absolute benchmark revision of the prior decade.

The revision established that first-print payrolls have recently carried more uncertainty than markets typically price in during the first trading hour following a strong print.

The rates channel behind Bitcoin's drop

The Federal Reserve held its target range at 3.50% to 3.75% in March.

The median participant's projection put 2026 unemployment at 4.4%, PCE inflation at 2.7%, and the year-end fed funds rate at 3.4%. March unemployment at 4.3% and a payroll print of 178,000 gave policymakers no urgency to move.

NYDIG's research frames the Bitcoin-to-macro link in the same terms: BTC trades in line with real rates, liquidity, and risk appetite. A Fed that holds its position on a firm labor market removes the near-term catalyst that Bitcoin most needs.

The February JOLTS report reinforces this without turning alarming. Openings held near 6.9 million, but hires fell to 4.8 million, and the hiring rate dropped to 3.1%, the lowest reading since April 2020.

Initial jobless claims for the week ended March 28 came in at 202,000, near cycle lows.

Together, these data points describe a labor market in stasis, with layoffs contained, new hiring tepid, and firms holding headcount steady.

That environment does not trigger a Fed pivot, and a Fed that does not pivot keeps financial conditions tighter for longer.

Potential outcomes for Bitcoin

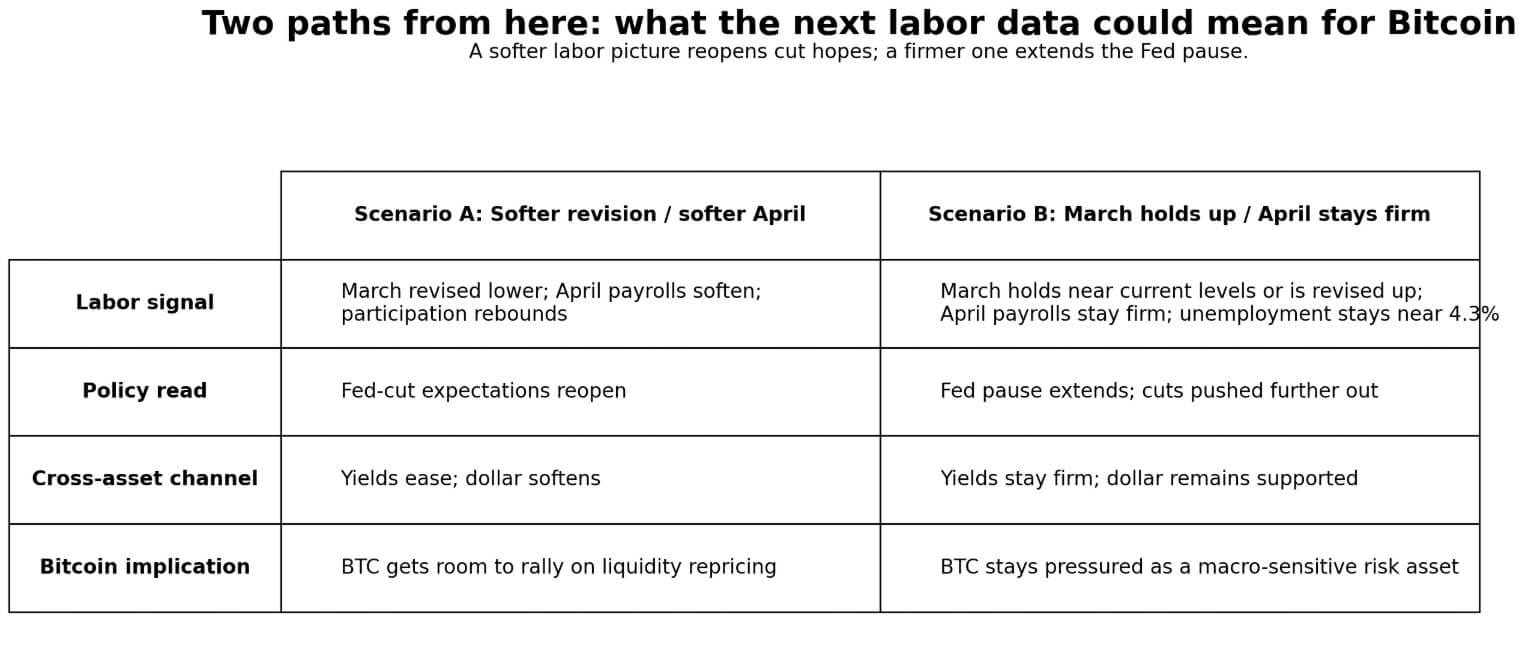

Bitcoin's price action on April 3 ran through the rates channel. Labor strength reduced cut expectations, firmer yields, and a stronger dollar tightened conditions for liquidity-sensitive assets. This channel can reverse.

If BLS revises March payrolls materially lower toward sub-100,000, and April payrolls also land soft while participation rebounds, the “headline-only strength” thesis gains traction.

Cut expectations would reopen, yields would ease, and Bitcoin would have room to rally on liquidity repricing. The weakness in the household survey, the strike-return distortion in health care, and the low-hiring JOLTS backdrop each make that path plausible, but April data on May 8 would need to confirm it.

If March holds near current levels or BLS revises it higher, and April payrolls land above roughly 125,000 while unemployment stays near 4.3% or below, February becomes the clear outlier.

The Fed extends its pause with more confidence, cuts get pushed further out, and Bitcoin keeps trading as a macro risk asset with no near-term liquidity catalyst.

The cross-asset move on April 3, with yields up, the dollar up, and BTC down, showed the market had already begun pricing that path.

The next Employment Situation release is scheduled for May 8 at 8:30 a.m. ET, bringing both April payrolls and the first revision to March.

That makes it the real checkpoint for every argument built on the April 3 print. March CPI is released on April 10, and the next FOMC meeting runs April 28-29, two data points the Fed absorbs before setting policy again.

CPI, in particular, will test if labor market firmness pairs with sticky inflation or with the wage deceleration that the March print already hinted at.

The post US jobs crush forecasts, yet hidden labor weakness could keep Bitcoin under pressure appeared first on CryptoSlate.

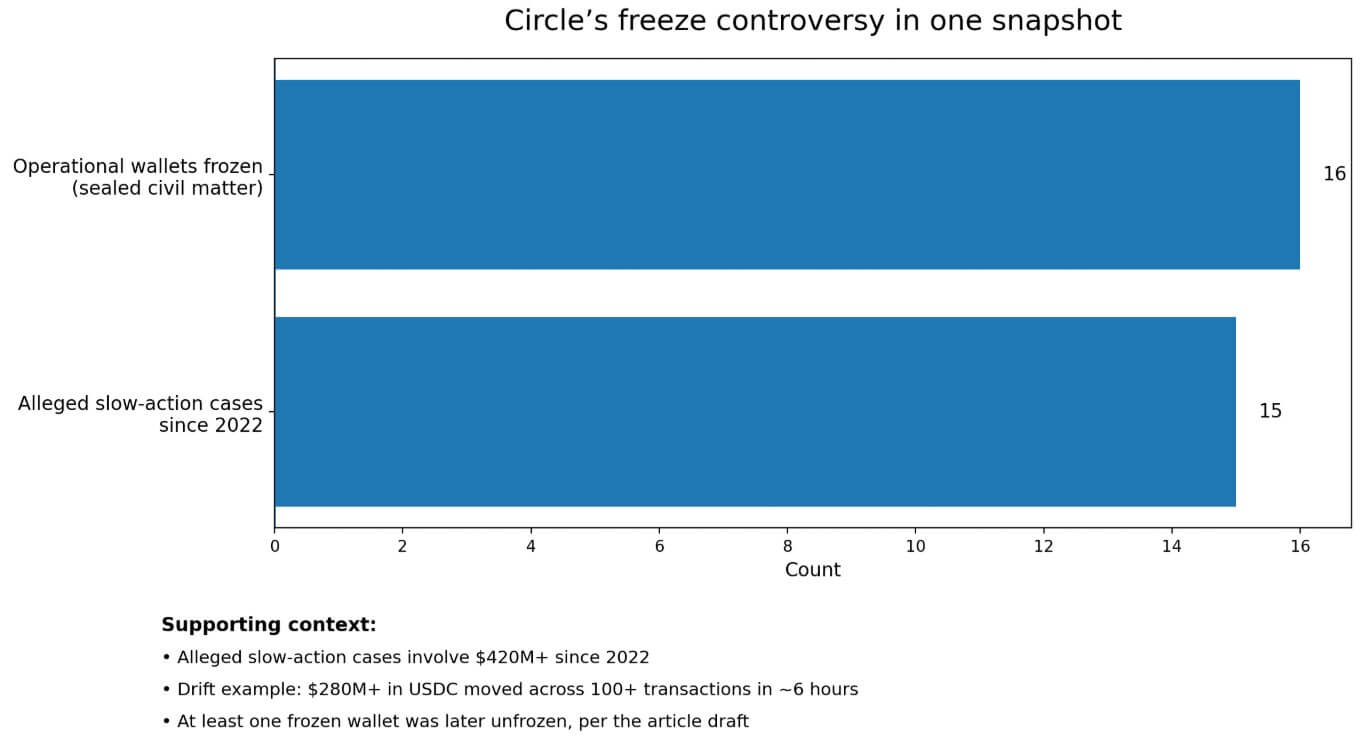

Circle's biggest selling point may be becoming its biggest liability. On-chain investigator ZachXBT's “Circle Files” allege that the USDC issuer has inconsistently applied its freeze powers.

Circle was too slow in 15 cases involving more than $420 million in allegedly illicit funds since 2022, yet broad enough to sweep 16 operational business wallets in a sealed US civil matter. The wallets were tied to exchanges, casinos, and forex services that ZachXBT said did not appear connected.

Why this matters: USDC is a core settlement asset in crypto, widely used by exchanges, traders, payment flows, and DeFi protocols. Circle’s freeze decisions extend beyond individual legal disputes or hack responses and set the boundary for how much operational risk businesses accept when holding or moving dollars on-chain.

The firm later unfroze at least one of those wallets, belonging to Goated.com, adding weight to the question of how precisely Circle reviews the addresses it blocklists.

That sequence of “slow on theft, sweeping on civil process” lands at a difficult moment.

USDC held roughly $77.2 billion in circulation as of April 3, in a total stablecoin market of nearly $316.8 billion, accounting for about 24.5% of that pool. One of the cases ZachXBT cites, the Drift exploit, saw more than $280 million in USDC move across 100-plus transactions in roughly six hours.

At that scale and speed, the gap between “can freeze” and “froze in time” is the entire practical question.

The legal stack Circle built

Circle's control surface has real on-chain teeth. Its EVM stablecoin contract includes a blocklist feature under a blocklister role, and blocklisted addresses cannot transfer or receive tokens.

Circle designed the contract to be both pausable and upgradeable.

That architecture existed long before this controversy arose, and Circle's Access Denial Policy codifies when that power is triggered.

Circle can block individual addresses on every blockchain where its stablecoins are issued. Once denied, the associated balance cannot move on-chain.

The policy limits freezes to two narrow triggers: when Circle decides, in its sole discretion, that failing to act would threaten network security or integrity, or when a valid legal order from a recognized US or French authority requires it.

Reversals require formal confirmation that the legal obligation or security basis no longer applies.

The USDC Terms add a second layer. Nothing in those terms obligates Circle to track, verify, or determine the provenance of users' USDC balances.

Yet, Circle also reserves the right to block addresses and freeze associated USDC that it determines, in its sole discretion, may be tied to illegal activity.

The Circle Mint User Agreement goes further: Circle may suspend accounts in its sole and absolute discretion, including under a court order, and may restrict redemptions or transfers when the law or a court order prohibits them.

The access-denial policy reads narrower and more formally rules-based, blocking sounds exceptional, tied to security events or legal compulsion. The broader USDC terms and user agreement grant the issuer considerably greater discretion.

Circle's legal terms afford the issuer considerably more latitude than the access-denial policy's narrow framing implies. When legal process and user continuity collide, Circle's own hierarchy prioritizes compliance and issuer control.

| Document / layer | What it says Circle can do | Why it matters |

|---|---|---|

| EVM stablecoin contract | Blocklisted addresses cannot transfer or receive tokens; contract is pausable and upgradeable | Shows Circle’s control exists directly in token architecture |

| Access Denial Policy | Can block addresses across chains; freezes tied to network security/integrity or valid U.S./French legal orders | Frames freezing as narrow and exceptional |

| USDC Terms | Circle may block addresses and freeze USDC tied to suspected illegal activity in its discretion | Expands Circle’s room to act |

| USDC Terms | Circle is not obligated to track, verify, or determine provenance for users | Limits what users can expect Circle to do for them |

| Circle Mint User Agreement | Circle may suspend accounts in its sole and absolute discretion, including due to court orders | Shows compliance can override user continuity |

Where the criticism bites

The 16-wallet incident illustrates why that hierarchy now troubles operators. Circle's freeze power executed quickly and broadly when a sealed civil matter arrived at its desk.

ZachXBT's “Circle Files” allege the same power moved too slowly across 15 theft cases since 2022, and the Drift window, $280 million-plus across more than 100 transactions in six hours, is the sharpest example because the scale and transaction count appeared on-chain in real time.

The GENIUS Act, passed in July 2025, created a US regulatory framework for payment stablecoins, treating USDC-type products as regulated financial infrastructure.

The OCC's implementing proposal has a comment deadline of May 1. FATF's March 2026 report stressed that supervisors should assess whether blockchain analytics and controls deliver tangible enforcement outcomes, and that timely public-private coordination is crucial for asset recovery.

That is the precise standard ZachXBT and affected operators are now applying to Circle.

Circle markets USDC as fully backed, transparently managed, and the world's largest regulated stablecoin. Circle's own 2026 Internet Financial System report cited $50 trillion-plus in cumulative USDC settlement, 40% of stablecoin transaction volume, and 29% of stablecoin circulation as of September 2025.

At that scale, freeze governance operates at systemic weight, and the examination it now faces reflects the infrastructure role Circle has claimed for itself.

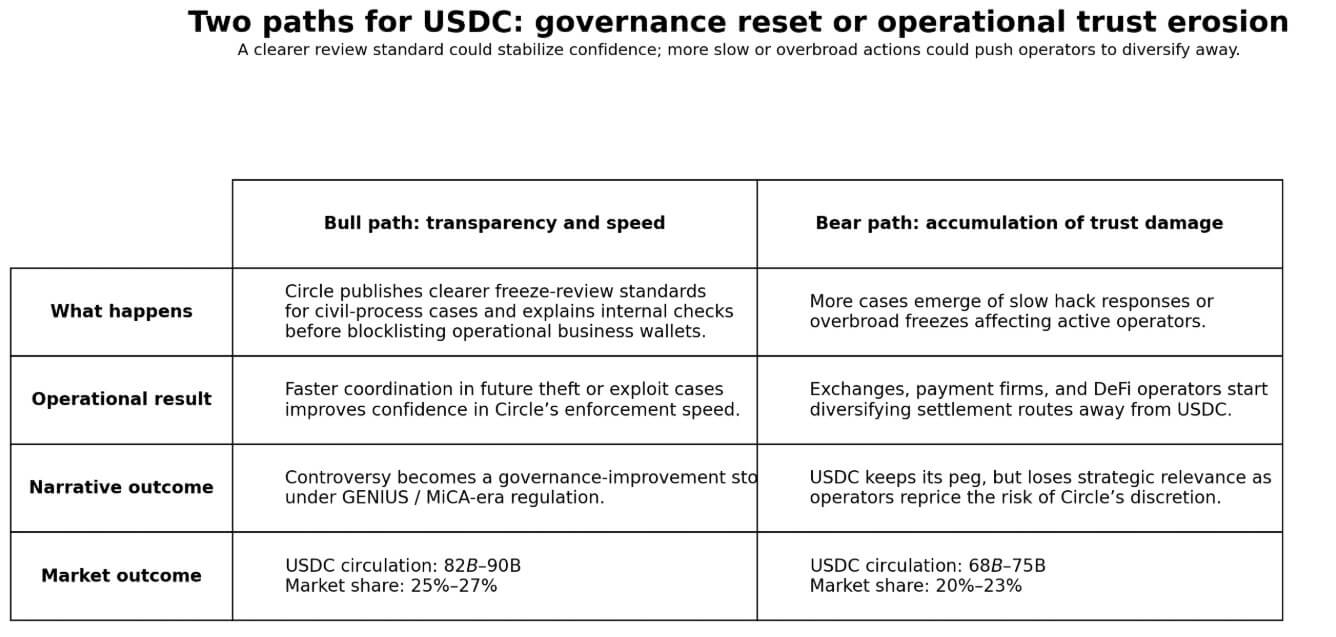

Two paths for Circle

The bull path runs through transparency and speed.

If Circle publishes a clearer review standard for freezes tied to civil process, detailing what internal review fires before Circle blocklists operational business wallets, and demonstrates materially faster coordination in future hack response situations, the controversy becomes a governance maturation story.

In that scenario, regulation under the GENIUS framework and MiCA rewards the most institutionalized issuer, and USDC circulation could recover to the $82 billion to $90 billion range, with 25% to 27% market share.

The 16-wallet incident, with Circle having already restored one wallet, would read as the moment Circle clarified its process.

The bear path runs through accumulation. More examples of slow hack responses or overbroad civil-process freezes, and operators who hold USDC in hot wallets, such as exchanges, payment companies, and DeFi protocols, are starting to diversify settlement routes.

A stablecoin can maintain its $1 peg while losing strategic relevance, and operators diversifying away from Circle would not trigger any depeg alert.

Tether, PYUSD, and a widening field of issuer-specific tokens each give operators a route away from Circle's control stack.

In that outcome, USDC circulation drifts toward a $68 billion to $75 billion range and a 20% to 23% market share, as businesses reprice the operational risk of sitting within Circle's discretion.

The next checkpoint arrives through operational performance, depending on how quickly Circle responds to the next hack, how quickly it restores blocklisted wallets, and if freezes land on operators with a clearer rationale than the last batch.

The OCC comment window closes on May 1, and the regulatory regime for payment stablecoins is taking shape while this dispute is live.

The market now wants to know if the compliance used by Circle model protects users or concentrates power in an issuer whose review standards operators cannot see.

The post Circle’s USDC freeze power faces fresh scrutiny after wallets were blocked while stolen funds moved appeared first on CryptoSlate.

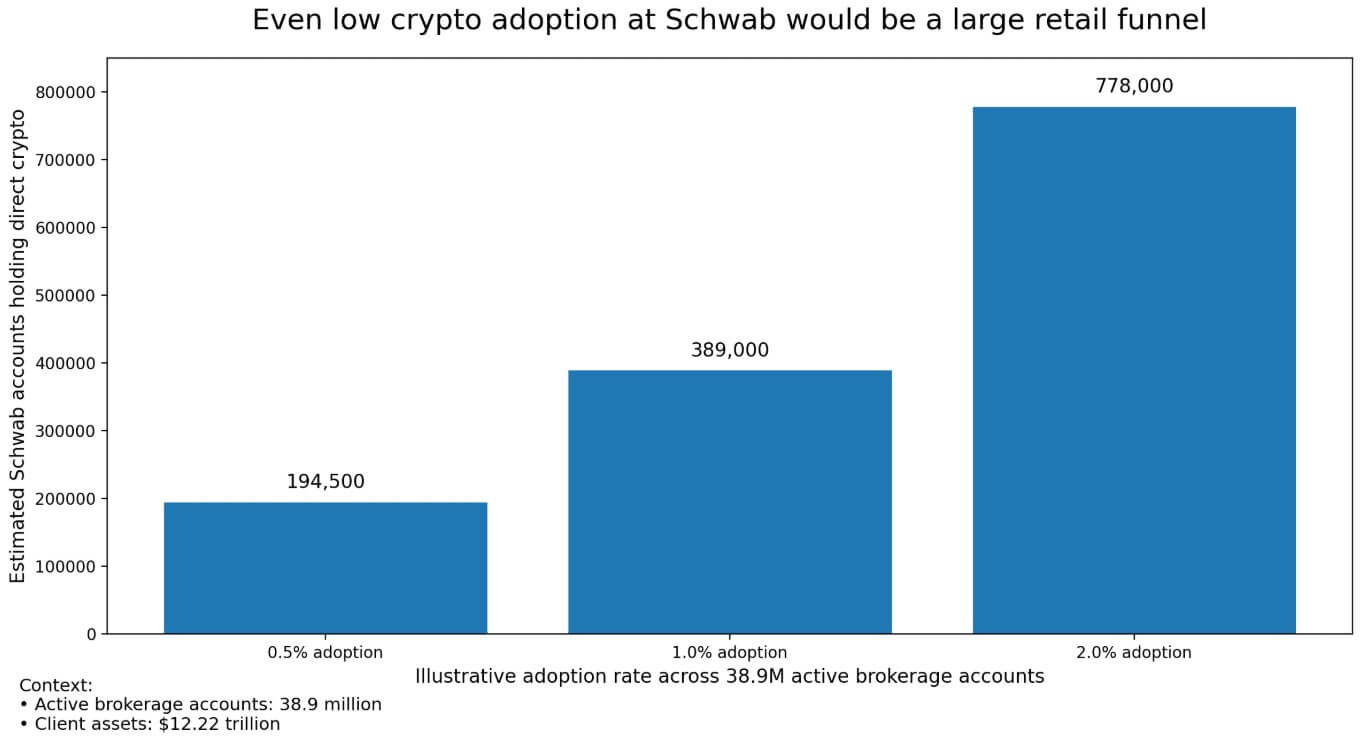

Charles Schwab operates 38.9 million active brokerage accounts and holds $12.22 trillion in client assets. For years, investors in those accounts could reach Bitcoin and Ethereum through ETFs, crypto-related equities, and futures.

A phased launch beginning in the second quarter closes the gap with direct investments. Schwab Crypto, offered through Charles Schwab Premier Bank, SSB, will let qualifying clients buy and sell Bitcoin and Ethereum directly.

The offer is available in all US states except New York and Louisiana, on a timeline that starts with employees and a small initial cohort before broadening.

Why this matters: Schwab is not introducing crypto to a crypto-native audience. It is testing whether direct Bitcoin and Ethereum ownership can sit inside the workflow of a mainstream brokerage customer. If that model gains traction, the implications reach beyond Schwab to product design, broker competition, and the next layer of retail crypto adoption.

The product architecture includes a structural boundary that clients and operators will immediately feel. Schwab Crypto operates through a dedicated account with an affiliated bank subsidiary.

This means that the structure is in a separate account from the brokerage accounts where investors already hold stocks, bonds, and ETFs. The crypto assets carry no SIPC or FDIC protection.

Schwab currently accepts no crypto deposits and does not settle securities or futures transactions in crypto. Mainstream access is real, and it arrives on carefully controlled broker-defined terms.

What drove the timing into 2026 is a policy calendar that dissolved three major institutional frictions within four months.

In January 2025, SAB 122 rescinded the earlier SAB 121 crypto safeguarding guidance that had made custody economics unattractive for traditional banks.

In March 2025, the OCC reaffirmed that crypto custody, certain stablecoin activities, and participation in distributed ledgers are permissible for national banks and removed the supervisory nonobjection requirement.

In April 2025, the Federal Reserve withdrew its earlier crypto guidance and moved to supervise those activities through the standard process.

Schwab CEO Rick Wurster described those regulatory moves as “pretty green” for large firms to expand into crypto, and the launch's timing confirms how directly the policy calendar shaped the product calendar.

| Date | Regulatory / market development | Why it mattered to Schwab |

|---|---|---|

| January 2025 | SAB 122 rescinded SAB 121 | Reduced a key accounting friction around crypto custody |

| March 2025 | OCC said crypto custody, certain stablecoin activity, and DLT participation are permissible; removed supervisory nonobjection requirement | Made bank-linked crypto activity easier to pursue |

| April 2025 | Federal Reserve withdrew earlier crypto guidance and moved to normal supervision | Reduced special-process friction for large institutions |

| March 2026 | Schwab research said Bitcoin had matured into a mainstream asset | Showed internal positioning had shifted toward normalization |

| Q2 2026 | Schwab began phased crypto rollout | Product timing followed the policy shift |

The asset Schwab is normalizing

In March 2026, Schwab published research describing Bitcoin as having matured into a mainstream asset and noting that by some measures it had become less volatile than certain Magnificent 7 stocks.

The research reflects the internal positioning that led to direct trading as the natural next step.

Reuters reported Wurster's view that the target user is an investor who already owns stocks and bonds and wants to hold a small slice of Bitcoin or Ethereum alongside those positions.

That is a narrower and more defensible market than the speculative base that drove 2021 volumes. Schwab is building a product for the mainstream investor who already trusts the brokerage brand and wants direct exposure within the brokerage environment they use.

Schwab enters a market that Fidelity already occupies. Fidelity's crypto account lets customers buy, sell, and transfer crypto through its platform and the Fidelity app alongside their existing brokerage positions.

E*TRADE has published a coming-soon page for direct trading in Bitcoin, Ethereum, and Solana, and reports point to Morgan Stanley plans to run that service through Zerohash in the first half of 2026.

Schwab enters this race as the scale normalizer, being the firm whose distribution footprint turns a multi-broker pattern into an industry default.

When Fidelity launched direct crypto, the market could read it as one firm's idiosyncratic call.

When Schwab, Fidelity, and E*TRADE each offer some version of direct BTC and ETH access, the mental category moves. When Schwab, Fidelity, and E*TRADE each offer some form of direct BTC and ETH access, direct crypto ownership sits on the same mental shelf as any other optional asset sleeve in a diversified brokerage account.

Schwab's own site already markets crypto exposure “from a brand you know,” and the launch extends that branding promise from wrappers to the asset itself.

A distribution thought experiment frames the scale without overclaiming a price surge.

If 0.5% of Schwab's 38.9 million accounts eventually hold direct crypto, that equals roughly 194,500 accounts. At 1%, it becomes approximately 389,000, and at 2% adoption, that funnel reaches roughly 778,000 accounts.

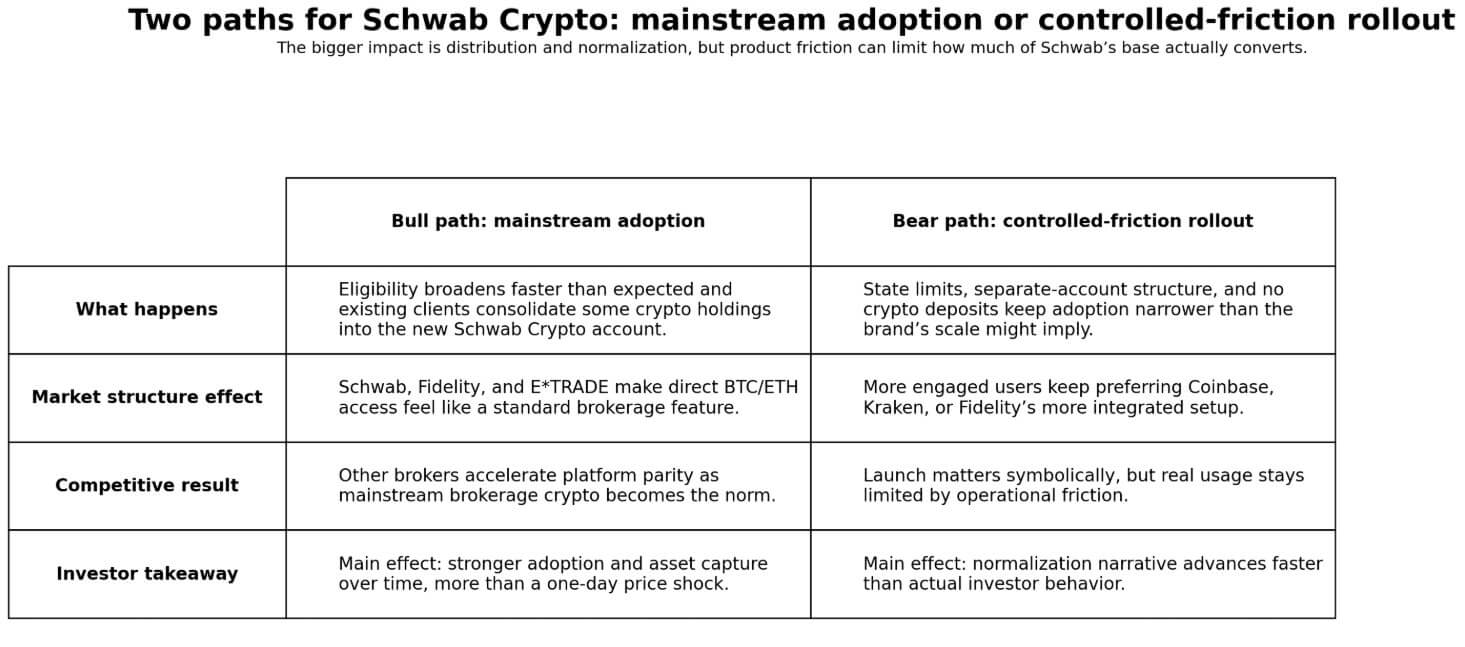

Two paths from here

The bull path opens if Schwab broadens eligibility faster than the phased language implies, and if the product experience proves clean enough for existing clients to consolidate crypto holdings into the new account.

In that scenario, Fidelity, E*TRADE, and Schwab together create a demand flywheel within the mainstream brokerage channel, the kind of end-investor adoption that Citi cited in its bull case of $165,000 for Bitcoin and $4,488 for Ethereum.

Schwab's distribution footprint alone would push every broker that still routes crypto clients exclusively to ETFs or education pages to accelerate its own platform-parity timeline.

The bear path runs through friction. The Schwab Crypto account's state restrictions, bank-subsidiary architecture, absence of crypto deposits, and current transfer limitations each create gaps relative to crypto-native venues that more engaged users will notice.

If those frictions keep adoption narrow and investors who want direct crypto exposure continue to prefer Coinbase, Kraken, or Fidelity's more integrated setup, the launch reads as operationally thin.

An investor who wants crypto to sit alongside equities within a single operational view may find the bank-subsidiary rail an exposure vehicle with tighter product boundaries than the brand's integrated-portfolio framing implies.

The next readable data point arrives when Schwab discloses how quickly the initial second-quarter cohort converts and if the broader rollout accelerates on schedule.

How quickly Schwab moves this cohort to general availability will tell the market whether this launch is a genuine scale ambition or a carefully managed compliance exercise.

The post Charles Schwab’s Bitcoin and Ethereum rollout shows crypto is moving deeper into mainstream brokerage accounts appeared first on CryptoSlate.

Cryptoticker

Crypto markets are about to enter one of the most decisive moments of the year.

After a quiet weekend with low volatility, real trading resumes today as Wall Street reopens — and with it comes the return of institutional capital.

Bitcoin is holding near $67,000. Ethereum remains above $2,000. Altcoins are drifting lower.

👉 But this calm is not stability — it’s compression before a major move.

Why This Monday Is Different

Weekend crypto trading often creates a false sense of direction.

- Liquidity is thin

- Institutions are inactive

- Volume is limited

- Moves lack conviction

👉 That changes today.

With traditional markets reopening:

- Institutional flows return

- ETF activity resumes

- Macro-driven positioning begins

- Correlation with equities strengthens

👉 This is when the real trend forms

A $100B Move Is Not an Exaggeration

Crypto market structure suggests that a large move is building.

When liquidity returns after a compressed weekend:

- Breakouts accelerate quickly

- Liquidations amplify momentum

- Capital rotates aggressively

👉 In past setups like this, total market cap has moved $100B+ within hours

This is exactly the type of environment we are entering now.

The Market Is Sitting on Multiple Triggers

Several major catalysts are converging at the same time:

🌍 Macro Risk

- Rising tensions around the Strait of Hormuz

- Oil price pressure building

- Inflation fears returning

🏦 Institutional Momentum

- Retirement funds opening to crypto

- Major players preparing trading access

- Continued accumulation signals

⚠️ Market Structure

- Low weekend volatility

- Tight price ranges

- Decreasing momentum

👉 This combination creates a pressure cooker setup

Bullish vs Bearish — What Happens Next?

🟢 Bullish Scenario

If markets absorb macro risks:

- Bitcoin breaks resistance

- Institutional inflows push prices higher

- Momentum builds quickly

👉 Expected:

- BTC → $70K+

- ETH follows

- Altcoins rebound sharply

🔴 Bearish Scenario

If macro fear dominates:

- Risk-off hits global markets

- Liquidity pulls back

- Crypto reacts sharply

👉 Expected:

- BTC loses support

- Altcoins drop faster

- Liquidations increase

The First Hours Will Decide Everything

The most important period is not the full day — it’s the first hours after market open.

Watch closely:

- Volume expansion

- Bitcoin direction

- Stock market reaction

- Oil price continuation

👉 If volume confirms the move, it becomes a trend

👉 If not, expect more volatility and fakeouts

Final Take

Crypto is not quiet. Crypto is waiting.

👉 Waiting for liquidity

👉 Waiting for institutional flows

👉 Waiting for direction

And today…

That direction will likely be decided.

The first week of April 2026 has been a study in contrasts. While the broader financial markets grapple with macroeconomic shifts, the digital asset sector is doubling down on technical evolution. We are seeing a move away from the "meme-coin" cycles of the past toward institutional-grade infrastructure and significant protocol overhauls.

Crypto News Today: Market Highlights

The crypto market today is defined by Bitcoin’s price stability near the $67,000 mark and massive anticipation for Ethereum’s Glamsterdam upgrade. Simultaneously, a significant exploit on the Solana-based Drift Protocol has served as a stark reminder of the security risks still inherent in decentralized finance (DeFi).

Market Snapshot: Bitcoin’s Quiet Resilience

Despite a slight 0.42% dip in the last 24 hours, Bitcoin ($BTC) continues to act as a stabilizing force for the entire ecosystem. Trading at approximately $67,000, the asset has shrugged off recent geopolitical volatility.

- Institutional Inflow: Recent reports from Goldman Sachs suggest that institutional "dip-buying" is keeping the floor high.

- Price Tracking: You can monitor live movements on our Bitcoin Ticker.

Ethereum Roadmap: The Glamsterdam Era

The biggest story in the developer community is the finalized scope for Ethereum’s Glamsterdam upgrade. Scheduled for the first half of 2026, this hard fork is expected to be a "game-changer" for scalability.

What is the Glamsterdam Upgrade?

Glamsterdam is the next major evolution of the Ethereum mainnet following the Fusaka update of late 2025. Its primary goals are:

- Gas Fee Reduction: A projected 78.6% reduction in fees for smart contract calls.

- Parallel Processing: Introducing the ability to process multiple transactions simultaneously.

- Throughput: Increasing the gas limit per block from 60 million to 200 million.

This upgrade is essential for $Ethereum to remain competitive against high-speed chains like Solana.

The Solana Hack: Drift Protocol Exploit

While Ethereum builds, $Solana has hit a major speed bump. On April 1, 2026, the Drift Protocol—the network's largest perpetual futures exchange—was drained of $286 million.

"The breach was not a simple code bug, but a sophisticated six-month social engineering operation by highly resourced actors." — Drift Protocol Preliminary Report.

The attackers reportedly posed as a quantitative trading firm to gain the trust of the protocol's security council. This event has reignited discussions on the necessity of hardware wallets for all DeFi participants.

Regulatory Milestone: Coinbase Nabs OCC Approval

In a massive win for US-based crypto, Coinbase has received conditional approval from the Office of the Comptroller of the Currency (OCC) for a national trust charter.

This does not make Coinbase a traditional commercial bank, but it provides federal regulatory uniformity for its custody business. This moves Coinbase into the same regulatory conversation as legacy giants like JPMorgan, further bridging the gap between "crypto" and "finance."

In a market often dominated by volatile meme coins and complex DeFi protocols, UNUS SED LEO ($LEO) has quietly climbed the ranks to become a heavyweight in the digital asset space. Originally launched as a utility token for the iFinex ecosystem, LEO has transitioned from its initial $1 exchange offering to a valuation exceeding $10 per token.

As of April 2026, LEO has officially broken into the top 10 largest cryptocurrencies by market capitalization, boasting a valuation of approximately $9.3 billion. This article explores the unique fundamentals, the aggressive deflationary model, and the institutional backing that have fueled this 1,000% journey.

What is UNUS SED LEO?

UNUS SED LEO is the native utility token of the iFinex ecosystem, which includes the prominent Bitfinex exchange. Launched in May 2019, the token was designed to provide holders with significant fee discounts and a variety of benefits across the platform's services. Unlike many other assets, LEO is a multi-chain token, existing on both the Ethereum and EOS blockchains to maximize accessibility.

Why is it named like this?

The token's name, "Unus Sed Leo," is Latin for "One, but a lion," a motto emphasizing quality and strength over quantity. It was born out of a crisis: iFinex launched the LEO token to raise $1 billion in capital after a payment processor's funds were seized by government authorities.

While it started as a recovery mechanism, it evolved into a pillar of exchange-based utility. Its primary function is to offer:

- Trading fee reductions: Up to 25% discount for holders.

- Lending fee discounts: Significant reductions for peer-to-peer lenders.

- Withdrawal/Deposit perks: Faster and cheaper transactions on Bitfinex.

The Path from $1 to $10: Why is the Price Rising?

The rise of LEO from its $1 launch to the current $10.05 level is not merely speculative; it is driven by one of the most transparent and aggressive buyback and burn mechanisms in the industry.

1. The 27% Revenue Burn

iFinex is contractually committed to using at least 27% of its consolidated monthly revenue to buy back LEO tokens from the open market and permanently destroy them. This creates a perpetual buy-side pressure. As Bitfinex remains a top-tier exchange for professional traders, this revenue stream provides a "floor" for the token price.

2. The Bitcoin Recovery Catalyst

A major factor in the 2024–2026 rally has been the legal resolution regarding the 2016 Bitfinex hack. Following court orders, nearly 94,643 BTC were earmarked for recovery. According to the token's whitepaper, 80% of recovered funds must be used to repurchase and burn LEO tokens. With $Bitcoin prices reaching new heights, the sheer dollar value of this buyback program has caused massive supply shocks.

3. Low Volatility and Institutional Trust

Unlike highly liquid assets that fluctuate wildly, LEO often shows "resilience" during market crashes. Because so much of the supply is held by long-term investors or is being systematically burned, the circulating supply (currently around 920 million LEO) continues to shrink, making each remaining token more valuable.

How LEO Price Reached the Top 10 Cryptos

Reaching the #10 spot by market cap is a feat of endurance. LEO's ascent was accelerated by the downfall of other exchange tokens (such as FTT) and the growing demand for "safe haven" utility assets.

| Feature | UNUS SED LEO (LEO) |

|---|---|

| Current Price | $10.05 |

| Market Cap Rank | #10 |

| Circulating Supply | ~920.9 Million |

| Max Supply | Decreasing Monthly |

By maintaining a steady growth trajectory while the broader altcoin market experienced massive drawdowns, LEO became a "non-correlated" asset. This attracted portfolio managers looking for stability.

From Digital Gold to Digital Dust

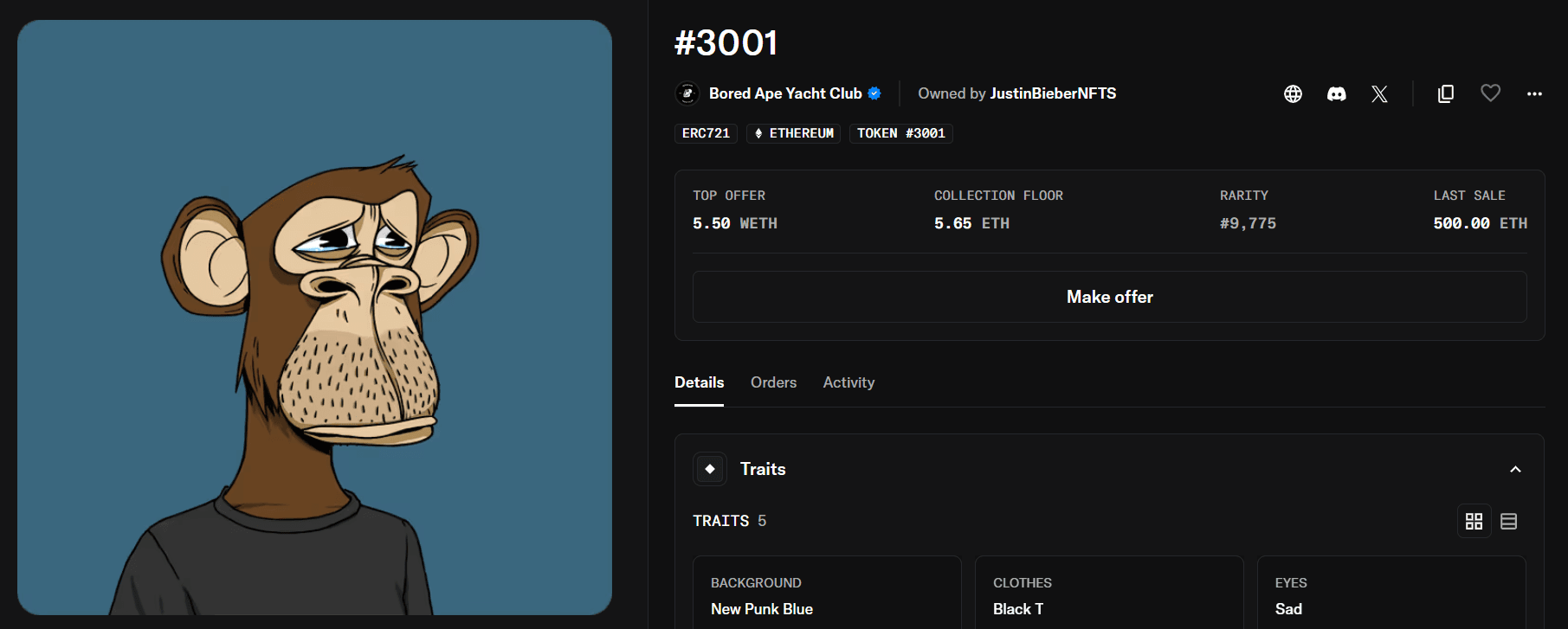

In early 2022, the world of Non-Fungible Tokens (NFTs) was at its absolute zenith. Celebrities were flocking to the space, led by pop icon Justin Bieber, who made headlines by purchasing a Bored Ape Yacht Club (BAYC) NFT for a staggering sum. At the time, it was seen as a bold entry into the future of digital art and web3.

Fast forward to April 2026, and the landscape has shifted dramatically. The speculative bubble that once valued "cartoon apes" at millions of dollars has largely evaporated, leaving high-profile investors like Bieber with massive "paper" losses.

The $1.3 Million Entry: Bored Ape #3001

In January 2022, Justin Bieber acquired Bored Ape #3001 for 500 ETH. At the exchange rates of that time, the transaction was valued at approximately $1.3 million.

The purchase was immediately controversial among NFT collectors. Analysts pointed out that Bieber paid nearly five times the "floor price" for an ape that possessed relatively common traits. While $Bitcoin and $Ethereum were experiencing high volatility, the NFT market was still fueled by extreme hype and celebrity endorsements.

Why Did He Pay Such a Premium?

- Aura of Exclusivity: Ownership of a BAYC acted as a digital "black card" for elite social circles.

- Market Sentiment: In 2022, the belief was that "blue-chip" NFTs would act as a store of value similar to fine art.

- FOMO: Fear of missing out on the next evolution of social media avatars.

The 2026 Reality: A 99% Valuation Wipeout

Today, the secondary market for the Bored Ape Yacht Club collection tells a much different story. As of April 2026, the floor price for the collection has retreated to approximately 5.25 ETH to 6 ETH. With the current Ethereum price stabilizing around $2,000, Bieber’s Bored Ape is now valued at roughly $12,000.

This represents a staggering 99% decline from his initial investment. Even when compared to the broader crypto market news, the drawdown in the NFT sector has been significantly more severe than that of major cryptocurrencies like BTC or ETH.

Celebrity NFT Portfolios in 2026

Bieber isn't the only celebrity facing a "re-valuation" of his digital assets. The following table illustrates the peak vs. current estimates for major celebrity BAYC holders:

| Celebrity | Asset | Purchase Price (Est.) | Current Value (2026) | Total Loss |

|---|---|---|---|---|

| Justin Bieber | BAYC #3001 | $1,300,000 | ~$12,000 | -99% |

| Eminem | BAYC #9055 | $462,000 | ~$78,000 | -83% |

| Stephen Curry | BAYC #7990 | $180,000 | ~$85,000 | -53% |

Note: Differences in loss percentages are often due to the rarity of the specific traits or the timing of the purchase.

Lessons from the NFT Bubble

The collapse of Bored Ape prices serves as a cautionary tale regarding liquidity and speculative assets. Unlike trading on major exchanges, where you can sell a token instantly, NFTs are illiquid. You need a specific buyer willing to pay your asking price for your specific token.

Furthermore, as reported by major financial outlets like Bloomberg, the shift toward "utility-based NFTs"—assets with actual function in gaming or identity—has left purely "profile picture" (PFP) projects struggling to regain their former glory.

Is there a Future for BAYC?

While the dollar value has dropped, Yuga Labs continues to develop the "Otherside" metaverse. However, for investors who entered during the 2022 frenzy, the road to "breaking even" appears nearly impossible. Most experts now categorize early NFT purchases as high-risk speculative plays rather than foundational investments.

Michael Saylor has sparked a fresh wave of debate with his latest X post, claiming it is a "Good Friday to buy Bitcoin." This comes as the $BTC price lingers near $67,400, a staggering 46% drop from its 2025 peak of $125,000.

The "Saylor Signal" vs. Market Reality

MicroStrategy Executive Chairman Michael Saylor is back to his usual bullish antics. On April 3, 2026, he took to X (formerly Twitter) to declare, "It’s a Good Friday to buy Bitcoin." For the "HODL" community, this is a standard rallying cry. However, for investors who watched Bitcoin plummet from a euphoric $125,000 in October 2025 to its current level of approximately $67,400, the message feels different this time.

The market is currently grappling with a "correlation crisis." While Saylor remains the ultimate $Bitcoin maximalist, his firm has shifted focus toward its new "STRC" preferred stock dividends. With significant unrealized losses on recent tranches, many are wondering: Is this a genuine "buy the dip" opportunity, or is the "Saylor Signal" losing its luster?

Should You Buy Bitcoin Now?

Whether "now" is a good time to buy depends on your time horizon. Technically, Bitcoin is in a clear downtrend on the daily charts. However, historically, buying during 40-50% drawdowns from all-time highs (ATH) has been a profitable long-term strategy. The current price of $67,400 represents a significant discount for those who missed the $100k+ rally, but macro headwinds suggest the bottom may not be in yet.

The 2026 Bitcoin Crash Explained

To understand why Saylor is calling for buys now, we must look at why the price crashed. The decline from $125,000 was not a single event but a "perfect storm" of factors:

- Monetary Policy Shifts: Recent hawkish signals from the Federal Reserve have drained liquidity from "risk-on" assets.

- Institutional De-risking: After the euphoria of 2025, major players have been trimming Bitcoin ETF holdings to lock in profits or cover losses in equities.

- The $67k Magnet: Since breaking below the $90,000 support, Bitcoin has been searching for a stable floor, finally resting in the mid-60s.

Historical Performance on Good Friday

While Saylor's post uses the holiday as a backdrop, does Bitcoin actually perform well on Good Friday? Historically, the Friday of Easter weekend sees lower trading volumes as traditional markets are closed. This "thin" liquidity can lead to sharp, erratic moves, but there is no statistically significant "holiday pump" trend. In fact, Bitcoin price action today remains largely sideways, reflecting what analysts call "aggressive caution."

Bitcoin Price Analysis: Analyzing the $67,400 Support

From a technical standpoint, Bitcoin is currently testing a critical psychological floor.

- Support Level: The $65,000 - $67,000 zone is vital. If BTC fails to hold this, the next major support sits at $58,000.