Cryptocurrency Posts

Crypto Briefing

Increased tensions and lack of diplomatic progress heighten the risk of prolonged conflict, impacting regional stability and global markets.

The post Trump’s threat drops US-Iran ceasefire odds to 1% for April 7 appeared first on Crypto Briefing.

Market skepticism highlights the challenge of achieving diplomatic breakthroughs without substantial actions, despite optimistic claims.

The post Trump claims US armed Iranian protesters, predicts deal with Iran by tomorrow appeared first on Crypto Briefing.

Trump's ultimatum heightens geopolitical tensions, impacting market confidence and suggesting prolonged instability in US-Iran relations.

The post Trump’s ultimatum to Iran lowers April ceasefire odds to 1% appeared first on Crypto Briefing.

Market hesitancy underscores the need for substantial institutional actions or regulatory signals to drive Bitcoin's next significant move.

The post Saylor hints at buying more Bitcoin as market awaits signals before June 30 appeared first on Crypto Briefing.

Iran's military resilience amid geopolitical tensions may stabilize its regime, but internal and external pressures could alter this balance.

The post Iran downs US F-15, maintains military resilience as regime stability odds drop to 13.5% appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Charles Schwab Teases Direct Bitcoin Trading With New ‘Schwab Crypto’ Account

Financial services giant Charles Schwab is preparing to expand deeper into digital assets, announcing plans for a forthcoming product that will allow clients to buy and sell cryptocurrencies directly through its platform.

The firm revealed that “Schwab Crypto ” is in development and will be offered through Charles Schwab Premier Bank, positioning the product as a gateway for retail investors seeking direct exposure to leading cryptocurrencies such as Bitcoin. The company has opened a waitlist for clients interested in early access, though availability will be subject to regulatory approval and eligibility requirements.

” is in development and will be offered through Charles Schwab Premier Bank, positioning the product as a gateway for retail investors seeking direct exposure to leading cryptocurrencies such as Bitcoin. The company has opened a waitlist for clients interested in early access, though availability will be subject to regulatory approval and eligibility requirements.

The move marks a notable shift for Schwab, which until now has limited crypto exposure to indirect investment vehicles. Currently, clients can access digital asset markets through exchange-traded products (ETPs), crypto-related equities, and thematic funds. Examples include publicly traded firms like Coinbase, MicroStrategy, and Riot Platforms, as well as funds tied to blockchain and crypto industry performance.

All aboard the Charles Schwab Bitcoin train

Schwab’s entry into spot trading places it in more direct competition with established crypto platforms such as Coinbase, Robinhood, and Webull.

CEO Rick Wurster first signaled the firm’s intent to enter spot crypto markets in late 2024, citing expectations for a shifting regulatory environment under the administration of Donald Trump. The company has since positioned itself to move once conditions allowed for broader participation by traditional financial institutions.

Schwab is also preparing additional crypto-related products, including a potential stablecoin offering following the passage of the GENIUS stablecoin bill.

A recent report from Charles Schwab found that Bitcoin volatility has declined significantly, with historical volatility falling to 42% in 2025 — about half its 2021 level — making it comparable to or lower than major tech stocks like Tesla and Nvidia.

Despite fewer extreme swings, bitcoin still experiences sharp drawdowns, including a 32% drop in 2025 and a 50% peak-to-trough decline over three years.

Long term, volatility remains elevated versus traditional assets. The report suggests bitcoin is maturing as it integrates into mainstream finance, with growing institutional adoption and ETF developments signaling increased acceptance.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Charles Schwab Teases Direct Bitcoin Trading With New ‘Schwab Crypto’ Account first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Jack Dorsey Reveals Bitcoin Faucet Revival with “Bitcoin Day” Announcement

Tech entrepreneur and longtime Bitcoin advocate Jack Dorsey sparked excitement in the BTC community on Friday when he posted a link to a new page titled “Bitcoin Day | Earn Free Bitcoin.”

The post quotes an announcement from the “Bitcoin at Block” account stating that “The bitcoin faucet is back” on April 6, 2026, with a link to btc.day. Dorsey’s shared URL (hosted on AWS CloudFront) currently displays only the bold headline promoting free BTC on “Bitcoin Day,” with a countdown timer.

No further details were given.

In 2010, a site known as the Bitcoin Faucet gave visitors 5 BTC after they completed a simple captcha challenge. This was done to help spread awareness and use of BTC, which at the time was a new digital currency with almost no market value.

The site was created by Gavin Andresen, a software developer who later became one of BTC’s lead developers. Andresen loaded the faucet with his own BTC to distribute to visitors who solved the CAPTCHA.

Over the months the faucet operated, it handed out about 19,700 BTC in total. At today’s prices, that amount would be worth in the billions of dollars.

Bitcoin’s rough price performance

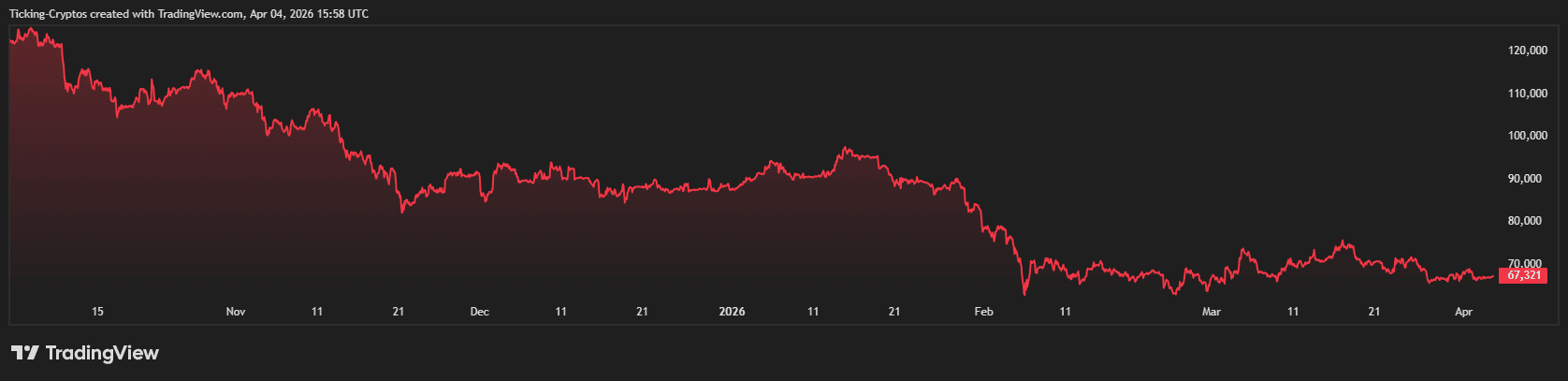

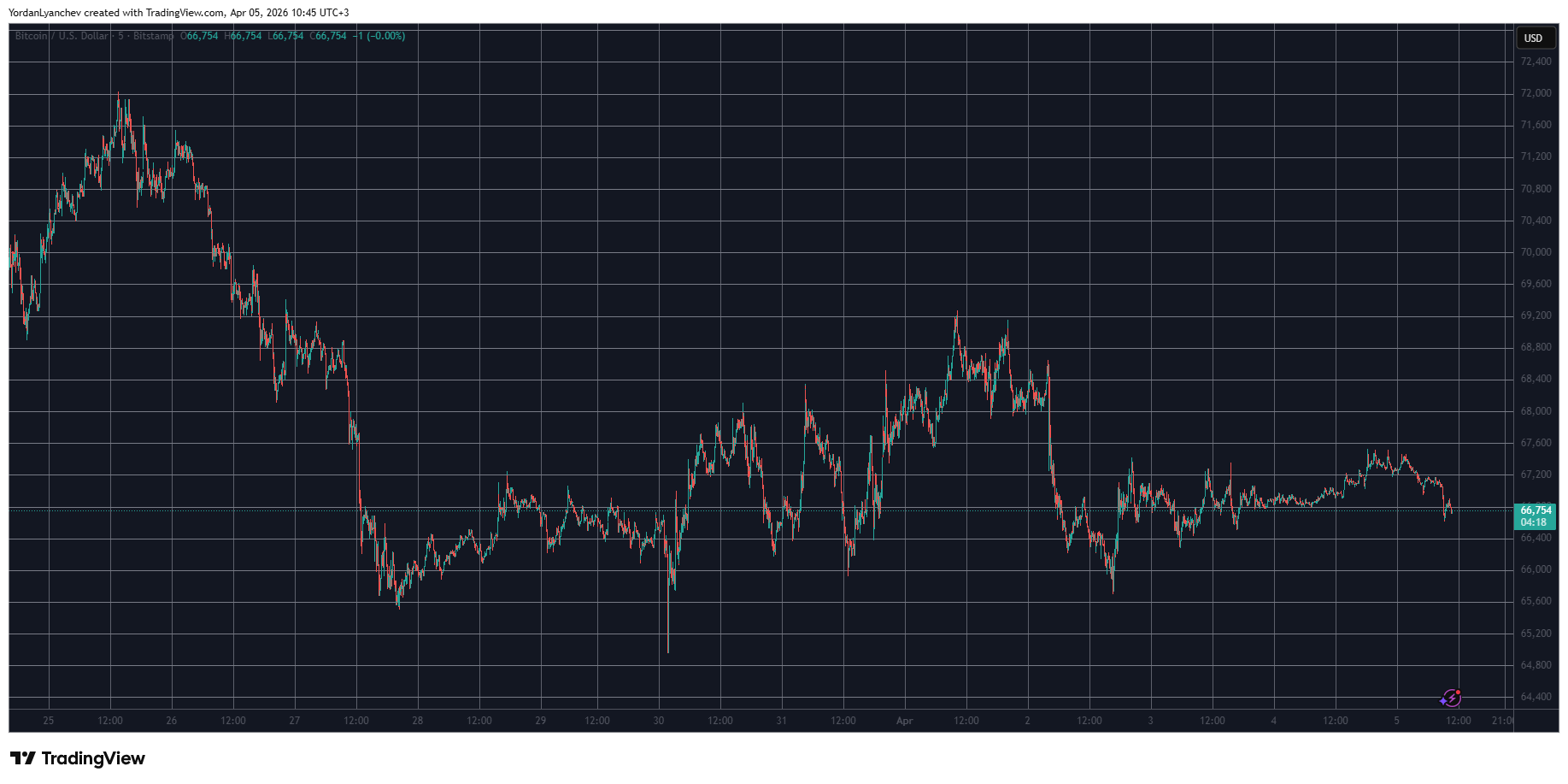

Over the past six months, BTC has experienced one of its weakest performance periods in years, with the price declining sharply from late 2025 highs. According to price history data, BTC’s value is down roughly 50% over the last half-year, reflecting a significant drawdown from levels above $120,000 in November 2025 to around the mid-$60,000s today.

BTC’s retreat has erased gains made earlier in the cycle and marked its worst six-month streak since 2018, driven by a mix of macroeconomic headwinds and reduced risk appetite among investors.

In March, it seems like the price stabilized near the high $60,000s, with market participants watching key technical levels and macro signals for clues on the next move.

Block has held 8,883 BTC since October 6, 2020, currently worth about $593.74 million at an average cost of $32,939 per BTC, for a gain of roughly +102.92% at today’s prices.

The company, trading under ticker XYZ, has a market cap of about $36–$37 billion. At the time of writing, BTC is trading near $67,000.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Jack Dorsey Reveals Bitcoin Faucet Revival with “Bitcoin Day” Announcement first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Cathie Wood Calls Bitcoin’s 50% Crash a “Victory” as Market Tests New Floor

Nearly six months after the Oct. 10 flash crypto crash erased millions of dollars in a single day, Bitcoin remains under pressure, trading well below its recent peak. The asset reached an all-time high of $126,080 on Oct. 6, but has since fallen about 47% to roughly $67,000.

Despite the drawdown, Cathie Wood, a long-time BTC advocate and chief executive of ARK Investment Management, is urging investors to maintain a long-term perspective.

Wood, whose firm was among the first publicly listed asset managers to gain exposure to Bitcoin in 2015, has maintained an active presence in crypto-related equities. ARK Invest continues to trade shares of companies tied to the digital asset sector, including Coinbase, Robinhood Markets, Block, Circle Internet Group, Bitmine Immersion Technologies, and Bullish, adjusting positions in response to market conditions.

In an interview on CNBC’s Squawk Box, Wood addressed the current downturn, framing the magnitude of BTC’s decline as a sign of maturation rather than weakness.

She argued that a roughly 50% drop from peak levels represents a shift from the extreme volatility seen in earlier cycles, when Bitcoin routinely experienced drawdowns of 85% to 95%.

NEW: Ark Invest CEO Cathie Wood says on CNBC that Bitcoin's usual -85% collapses are "DONE"

— Bitcoin Magazine (@BitcoinMagazine) April 3, 2026

"This is a prove technology, it's a proven monetary system, and it's a new asset class."pic.twitter.com/j0OU62hWmj

According to Wood, such severe collapses are unlikely to recur. She described Bitcoin as a “proven technology” and a “new asset class,” suggesting that its market behavior has evolved alongside broader adoption and institutional participation.

In her view, the current correction would be considered a “real victory” within the Bitcoin community if losses remain limited to around half of its peak value.

Bitcoin’s vicious cycles

Historical data supports the comparison to prior cycles, though the current downturn has yet to match earlier bear markets in severity. During the 2021–2022 cycle, Bitcoin fell nearly 80% from its then-record high of about $69,000, eventually bottoming near $15,600.

Onchain data from Glassnode indicates that the present decline, measured against the October 2025 high, has reached roughly 52% at its lowest point.

All this is happening as bitcoin’s price decline forces a growing number of public companies and sovereign entities to unwind their BTC treasuries, marking a sharp reversal from the accumulation trend of the past two years. Firms that once championed long-term holding are now selling to manage liquidity, repay debt, and fund strategic pivots.

Companies like Riot Platforms, Genius Group, Empery Digital, Nakamoto Holdings, and Marathon Digital have all reduced holdings, in some cases significantly. Marathon alone sold over 15,000 BTC for $1.1 billion to cut debt, while Genius Group fully exited its position. Riot has also been offloading bitcoin as it shifts focus toward AI and high-performance computing infrastructure.

Even firms still committed to bitcoin are trimming reserves. Empery Digital sold part of its holdings to repay loans, while Nakamoto Holdings liquidated a smaller portion to support operations. Meanwhile, Bhutan has been reducing its state-backed bitcoin reserves after previously accumulating through mining.

Despite the sell-off, public companies still collectively hold about 1.16 million BTC, over 5% of the total supply.

This post Cathie Wood Calls Bitcoin’s 50% Crash a “Victory” as Market Tests New Floor first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts Toward AI Infrastructure

Riot Platforms sold 3,778 bitcoin in the first quarter of 2026, generating $289.5 million and marking a shift in strategy as the miner redirects capital toward infrastructure and high-performance computing.

The volume sold exceeded the company’s quarterly production of 1,473 BTC by roughly 2.6 times, signaling a drawdown of treasury holdings rather than routine profit-taking. Riot ended the quarter with 15,680 BTC, down 18% from 18,005 BTC at the close of 2025.

The selling appears to have extended beyond the reporting period. Blockchain analytics firm Arkham Intelligence flagged a 500 BTC outflow from a wallet linked to Riot following the end of the quarter, suggesting continued liquidation activity.

The imbalance between production and sales comes as Riot accelerates its expansion into artificial intelligence and high-performance computing colocation. The company has begun repositioning its business model away from sole reliance on bitcoin mining, seeking to monetize its energy assets and data center footprint through long-term infrastructure contracts.

In January, Riot sold 1,080 BTC to fund the purchase of 200 acres at its Rockdale, Texas site. It also entered a ten-year agreement with Advanced Micro Devices to provide 25 megawatts of capacity, with an option to scale to 200 MW. The deal is expected to generate about $311 million in contract revenue over its initial term.

Operational metrics complicate a distress narrative. Riot reduced its all-in power cost to 3.0 cents per kilowatt hour, a 21% decline from the prior year, while increasing deployed hash rate by 26% to 42.5 exahashes per second. Average operating hash rate rose 23% to 36.4 EH/s, reflecting continued investment in mining capacity.

The company also generated $21 million in power credits during the quarter, more than double the year-ago period, through participation in grid services and energy programs.

Bitcoin HODLers like RIOT are selling

Industry conditions remain a factor. Rising energy costs tied to geopolitical tensions have pressured margins across the mining sector, prompting several operators to liquidate holdings. MARA Holdings, Genius Group, and Nakamoto Holdings collectively sold more than 15,000 BTC in recent days, reflecting a broader shift in capital allocation.

Riot’s Q1 activity underscores a turning point for the sector, where bitcoin reserves are deployed as funding sources for diversification rather than held as long-term balance sheet assets.

The trend extends beyond corporate treasuries. Bhutan has continued to reduce its BTC holdings, selling a total of 3,103 BTC. A single transaction on March 30 accounted for 375 BTC, according to Glassnode data.

The country had built its position through state-backed mining operations, reaching more than 13,000 BTC at its peak in October 2024.

Despite the recent selling, public companies still hold about 1.16 million BTC, or more than 5% of bitcoin’s fixed supply of 21 million, according to BitcoinTreasuries.net.

This post Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts Toward AI Infrastructure first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

The Bitcoin Treasury Model With a Built-In Valuation Floor

There is a version of the Bitcoin treasury conversation that has become almost routine at this point. Bitcoin is hard money. Fiat debases. Companies that hold Bitcoin on their balance sheet are making a rational long-term decision. All of this is true, and none of it is the interesting question anymore.

The interesting question is structural. Not should a company hold Bitcoin, but what kind of company should hold it, and what that choice implies for how the company performs across a full market cycle, not just a favorable one.

Three models have emerged. Each reflects a different level of conviction, a different capital structure, and a different set of tradeoffs.

- The pure-play. A company whose primary purpose is accumulating Bitcoin through capital raises, financial engineering, etc, with no core operating business. Lean structure, singular mission.

- The digital credit issuer. The most sophisticated expression of the pure-play thesis. These companies issue Bitcoin-backed financial instruments, preferred stock, convertible notes, and similar products, to fund continued accumulation. At scale, this creates a compounding accumulation engine that simpler models cannot match.

- The operating company with a Bitcoin treasury. A business with real revenue, real clients, and operational activity, which holds Bitcoin as a long-term reserve asset in deliberate strategic relationship with the business itself.

All three are legitimate expressions of the Bitcoin treasury thesis. They are not optimized for the same objectives, and the differences matter more than most treasury conversations acknowledge.

What pure-play gets right

The pure-play case deserves genuine treatment because its strongest version has real force.

Financial engineering pure-plays are capital-efficient in a specific and important sense: every dollar raised goes directly to Bitcoin accumulation with no operational drag. The mission is singular and the structure reflects it. For investors, this creates clarity. Allocators know exactly what they are underwriting, direct Bitcoin exposure at the corporate level, and the investment thesis is legible and short.

The digital credit model extends this further. Companies that have successfully issued preferred instruments and Bitcoin-backed products have built accumulation engines that operating businesses cannot match on a per-dollar-raised basis. The compounding effect of a sophisticated capital structure, at scale, is genuinely powerful. It represents the fullest expression of the Bitcoin treasury thesis, and the destination it points toward is one every operator in this space should understand.

The prerequisite problem and what it means in practice

The digital credit model has a prerequisite that is rarely stated plainly: it requires scale, institutional credibility, and market infrastructure that most companies building a Bitcoin treasury today do not yet have. It is a destination, not a starting point.

The path there runs through an intermediate period where the financial engineering structure carries more exposure than is often acknowledged. During that period:

- There is no operating revenue to fall back on

- The ability to raise capital tracks closely with Bitcoin market sentiment

- Strategic options narrow when conditions are not favorable

- The company’s cost structure depends entirely on capital markets remaining open

This is not a criticism of the model. It is a description of the journey. The question for executives is what structure best serves the company while that journey is underway.

What the operating company model actually provides

The operating company with a Bitcoin treasury does not accumulate Bitcoin faster than a well-run pure-play. At meaningful treasury scale, operating cash flow is not moving the needle on accumulation. The advantage is different, and worth stating precisely.

An operating business generates revenue independently of where Bitcoin is trading. That revenue covers fixed costs, which means the company is not dependent on capital markets remaining open to fund its basic operations. It can continue hiring, serving clients, and accumulating at a measured pace without being forced into capital decisions driven by timing rather than conviction.

The compounding effect works like this:

- Operating revenue covers costs and preserves the Bitcoin position through the cycle rather than drawing it down under pressure

- A preserved balance sheet improves the terms on future capital raises, lower dilution, better access to facilities, stronger negotiating position with partners

- Operational credibility widens the available capital base by providing an investment thesis that reaches allocators who cannot underwrite pure Bitcoin exposure within their current mandates

None of these mechanisms make Bitcoin accumulate faster in favorable conditions. Together, they make the company more durable across the full range of conditions it will face.

The built-in valuation floor

Most Bitcoin treasury company valuations are driven by a single number: mNAV, the premium the market assigns to Bitcoin held at the corporate level. When sentiment is strong and capital is flowing into the space, that premium expands. When the narrative cools, it compresses. The valuation moves with the market’s appetite for Bitcoin exposure, not with anything the company is doing operationally.

The operating company model introduces a second component that behaves differently. A profitable operating business carries an earnings multiple underwritten by revenue, client relationships, and operational track record. It does not expand dramatically when Bitcoin is performing. But it does not compress when sentiment turns either. It is stable in a way that mNAV alone is not.

These two components, Bitcoin NAV and an earnings multiple on the operating business, do not move together. That is the point. When mNAV compresses, the earnings multiple holds. The company retains a defensible valuation floor that a pure-play structure, with a single-component valuation entirely dependent on sentiment, does not have.

In practice this matters in three specific ways:

- Capital raises. A company with a defensible valuation floor can raise capital on reasonable terms even when Bitcoin sentiment is cold. A pure-play with a compressed mNAV and no earnings component has less room to maneuver.

- Talent. Equity compensation tied to a two-component valuation is a more legible and stable proposition for prospective hires than equity tied entirely to Bitcoin’s market sentiment.

- Allocator access. Many institutional allocators cannot underwrite a valuation built entirely on mNAV within their current mandates. The earnings component creates a bridge, opening the door to capital that would otherwise be unable to participate regardless of conviction.

The floor is not just a comfort during difficult conditions. It is a structural advantage that compounds over time, widening the capital base, strengthening the talent proposition, and maintaining strategic momentum across the full cycle.

How to think about the decision

These three models serve different objectives. The right framework starts with honest answers to a few questions:

- What does the existing business look like? A company with established revenue and clients already has the foundation for the operating company model. A company without it is choosing between building that foundation and committing to a pure-play path.

- What is the realistic path to scale? The digital credit model is the most powerful expression of the thesis but requires scale and credibility that takes time to build. The operating company model does not depend on reaching that threshold to function well.

- What does the investor base look like? Pure-play structures appeal most clearly to allocators who want direct Bitcoin exposure. Operating companies reach a broader set of capital partners, including those whose mandates require an operating business to participate.

- What kind of company do you want to be running across a full cycle? This is the question underneath all the others. The answer should drive the structure, not the other way around.

Conclusion

The companies that define the next era of corporate Bitcoin adoption will not all look the same. Digital credit issuers will operate at the frontier of Bitcoin-native capital markets. Financial engineering pure-plays will build toward that destination with focused conviction. Operating companies will build businesses where the treasury and core operations strengthen each other across the cycle.

Each model is a genuine expression of the thesis. The goal of this framework is to make the differences legible, so executives can choose the structure that fits what they are actually building, with clear eyes about what each model asks of them in return.

The question was never which model holds the most Bitcoin. It was always which model fits what you are trying to build.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

This post The Bitcoin Treasury Model With a Built-In Valuation Floor first appeared on Bitcoin Magazine and is written by Nick Ward.

CryptoSlate

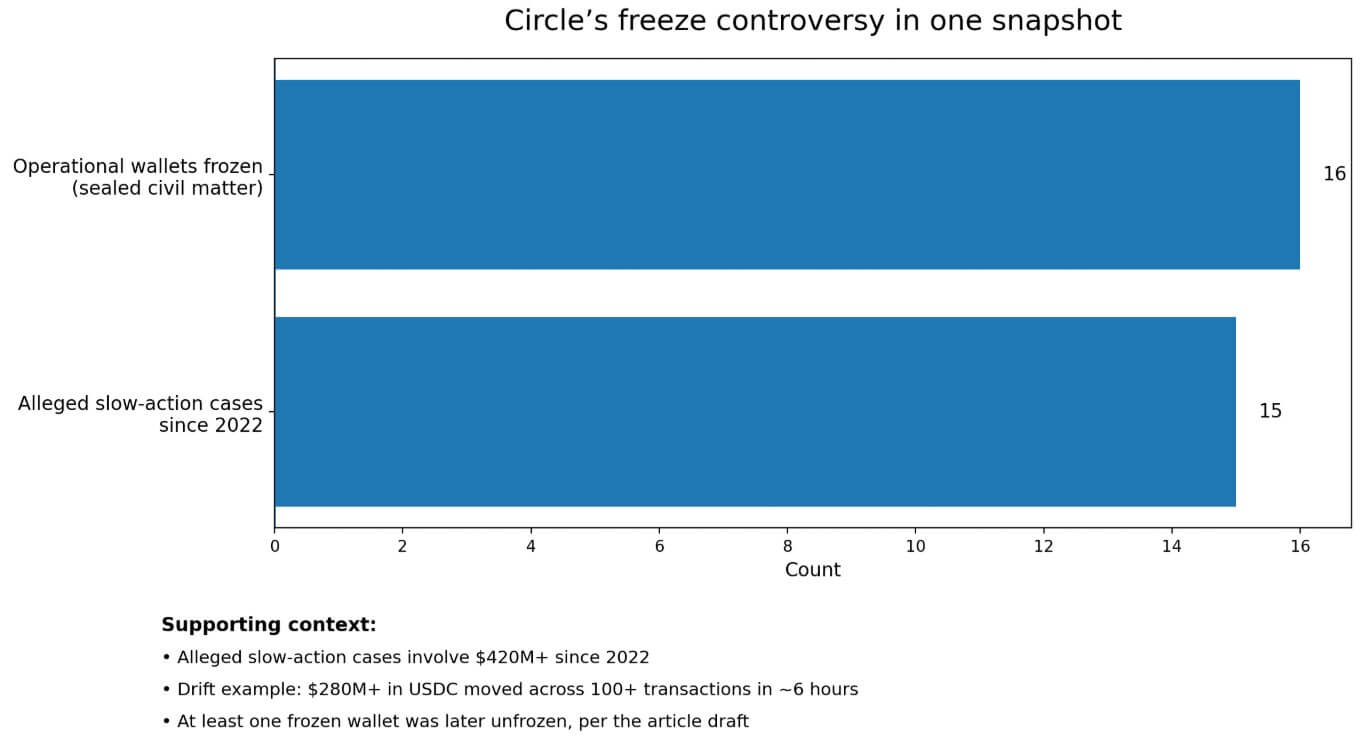

Circle's biggest selling point may be becoming its biggest liability. On-chain investigator ZachXBT's “Circle Files” allege that the USDC issuer has inconsistently applied its freeze powers.

Circle was too slow in 15 cases involving more than $420 million in allegedly illicit funds since 2022, yet broad enough to sweep 16 operational business wallets in a sealed US civil matter. The wallets were tied to exchanges, casinos, and forex services that ZachXBT said did not appear connected.

Why this matters: USDC is a core settlement asset in crypto, widely used by exchanges, traders, payment flows, and DeFi protocols. Circle’s freeze decisions extend beyond individual legal disputes or hack responses and set the boundary for how much operational risk businesses accept when holding or moving dollars on-chain.

The firm later unfroze at least one of those wallets, belonging to Goated.com, adding weight to the question of how precisely Circle reviews the addresses it blocklists.

That sequence of “slow on theft, sweeping on civil process” lands at a difficult moment.

USDC held roughly $77.2 billion in circulation as of April 3, in a total stablecoin market of nearly $316.8 billion, accounting for about 24.5% of that pool. One of the cases ZachXBT cites, the Drift exploit, saw more than $280 million in USDC move across 100-plus transactions in roughly six hours.

At that scale and speed, the gap between “can freeze” and “froze in time” is the entire practical question.

The legal stack Circle built

Circle's control surface has real on-chain teeth. Its EVM stablecoin contract includes a blocklist feature under a blocklister role, and blocklisted addresses cannot transfer or receive tokens.

Circle designed the contract to be both pausable and upgradeable.

That architecture existed long before this controversy arose, and Circle's Access Denial Policy codifies when that power is triggered.

Circle can block individual addresses on every blockchain where its stablecoins are issued. Once denied, the associated balance cannot move on-chain.

The policy limits freezes to two narrow triggers: when Circle decides, in its sole discretion, that failing to act would threaten network security or integrity, or when a valid legal order from a recognized US or French authority requires it.

Reversals require formal confirmation that the legal obligation or security basis no longer applies.

The USDC Terms add a second layer. Nothing in those terms obligates Circle to track, verify, or determine the provenance of users' USDC balances.

Yet, Circle also reserves the right to block addresses and freeze associated USDC that it determines, in its sole discretion, may be tied to illegal activity.

The Circle Mint User Agreement goes further: Circle may suspend accounts in its sole and absolute discretion, including under a court order, and may restrict redemptions or transfers when the law or a court order prohibits them.

The access-denial policy reads narrower and more formally rules-based, blocking sounds exceptional, tied to security events or legal compulsion. The broader USDC terms and user agreement grant the issuer considerably greater discretion.

Circle's legal terms afford the issuer considerably more latitude than the access-denial policy's narrow framing implies. When legal process and user continuity collide, Circle's own hierarchy prioritizes compliance and issuer control.

| Document / layer | What it says Circle can do | Why it matters |

|---|---|---|

| EVM stablecoin contract | Blocklisted addresses cannot transfer or receive tokens; contract is pausable and upgradeable | Shows Circle’s control exists directly in token architecture |

| Access Denial Policy | Can block addresses across chains; freezes tied to network security/integrity or valid U.S./French legal orders | Frames freezing as narrow and exceptional |

| USDC Terms | Circle may block addresses and freeze USDC tied to suspected illegal activity in its discretion | Expands Circle’s room to act |

| USDC Terms | Circle is not obligated to track, verify, or determine provenance for users | Limits what users can expect Circle to do for them |

| Circle Mint User Agreement | Circle may suspend accounts in its sole and absolute discretion, including due to court orders | Shows compliance can override user continuity |

Where the criticism bites

The 16-wallet incident illustrates why that hierarchy now troubles operators. Circle's freeze power executed quickly and broadly when a sealed civil matter arrived at its desk.

ZachXBT's “Circle Files” allege the same power moved too slowly across 15 theft cases since 2022, and the Drift window, $280 million-plus across more than 100 transactions in six hours, is the sharpest example because the scale and transaction count appeared on-chain in real time.

The GENIUS Act, passed in July 2025, created a US regulatory framework for payment stablecoins, treating USDC-type products as regulated financial infrastructure.

The OCC's implementing proposal has a comment deadline of May 1. FATF's March 2026 report stressed that supervisors should assess whether blockchain analytics and controls deliver tangible enforcement outcomes, and that timely public-private coordination is crucial for asset recovery.

That is the precise standard ZachXBT and affected operators are now applying to Circle.

Circle markets USDC as fully backed, transparently managed, and the world's largest regulated stablecoin. Circle's own 2026 Internet Financial System report cited $50 trillion-plus in cumulative USDC settlement, 40% of stablecoin transaction volume, and 29% of stablecoin circulation as of September 2025.

At that scale, freeze governance operates at systemic weight, and the examination it now faces reflects the infrastructure role Circle has claimed for itself.

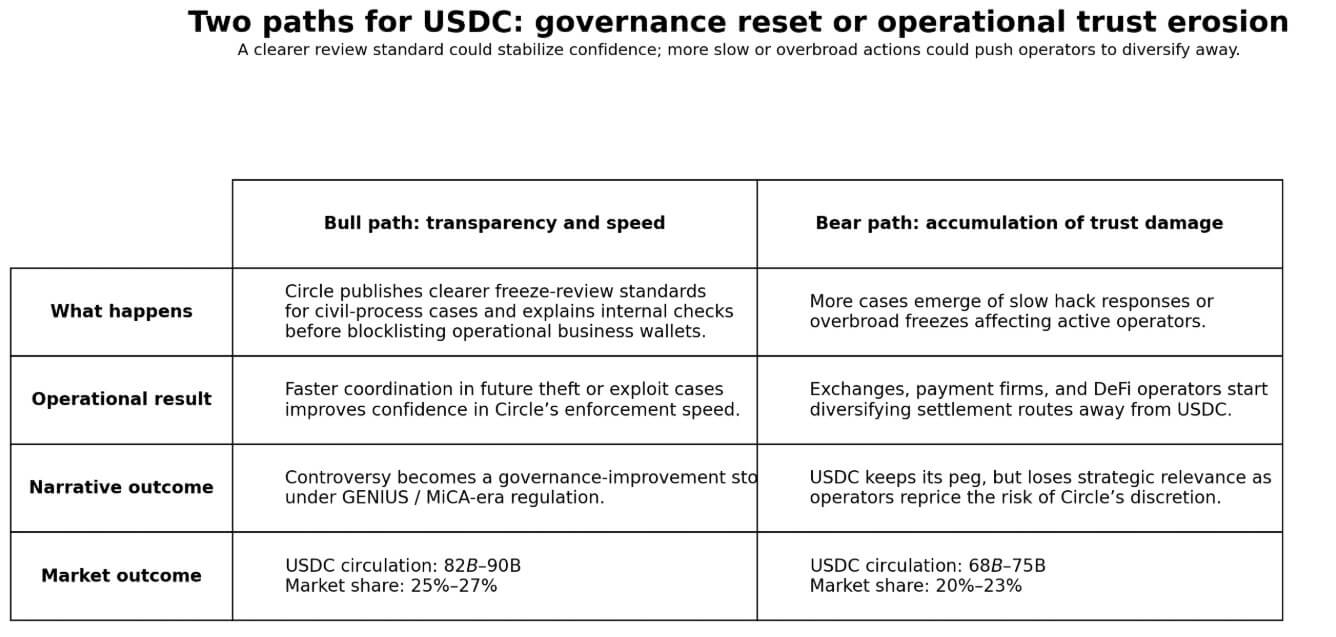

Two paths for Circle

The bull path runs through transparency and speed.

If Circle publishes a clearer review standard for freezes tied to civil process, detailing what internal review fires before Circle blocklists operational business wallets, and demonstrates materially faster coordination in future hack response situations, the controversy becomes a governance maturation story.

In that scenario, regulation under the GENIUS framework and MiCA rewards the most institutionalized issuer, and USDC circulation could recover to the $82 billion to $90 billion range, with 25% to 27% market share.

The 16-wallet incident, with Circle having already restored one wallet, would read as the moment Circle clarified its process.

The bear path runs through accumulation. More examples of slow hack responses or overbroad civil-process freezes, and operators who hold USDC in hot wallets, such as exchanges, payment companies, and DeFi protocols, are starting to diversify settlement routes.

A stablecoin can maintain its $1 peg while losing strategic relevance, and operators diversifying away from Circle would not trigger any depeg alert.

Tether, PYUSD, and a widening field of issuer-specific tokens each give operators a route away from Circle's control stack.

In that outcome, USDC circulation drifts toward a $68 billion to $75 billion range and a 20% to 23% market share, as businesses reprice the operational risk of sitting within Circle's discretion.

The next checkpoint arrives through operational performance, depending on how quickly Circle responds to the next hack, how quickly it restores blocklisted wallets, and if freezes land on operators with a clearer rationale than the last batch.

The OCC comment window closes on May 1, and the regulatory regime for payment stablecoins is taking shape while this dispute is live.

The market now wants to know if the compliance used by Circle model protects users or concentrates power in an issuer whose review standards operators cannot see.

The post Circle’s USDC freeze power faces fresh scrutiny after wallets were blocked while stolen funds moved appeared first on CryptoSlate.

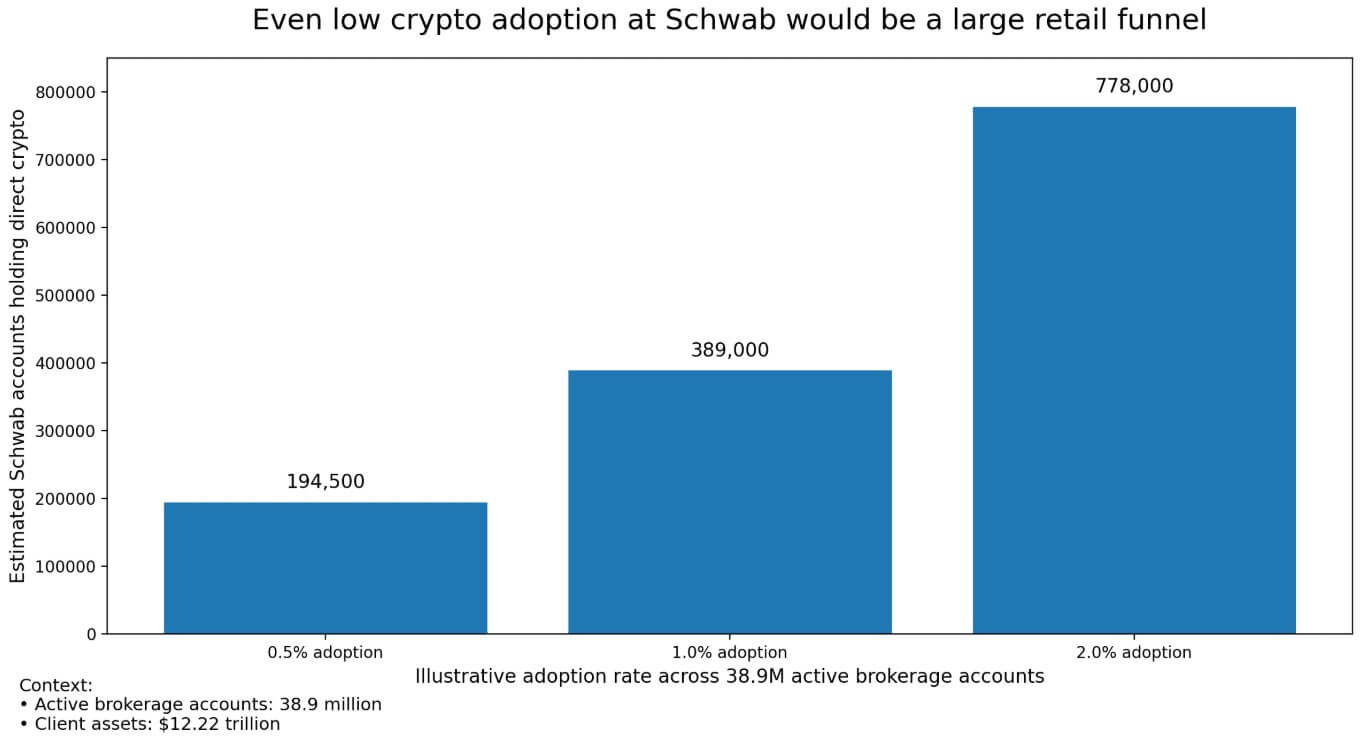

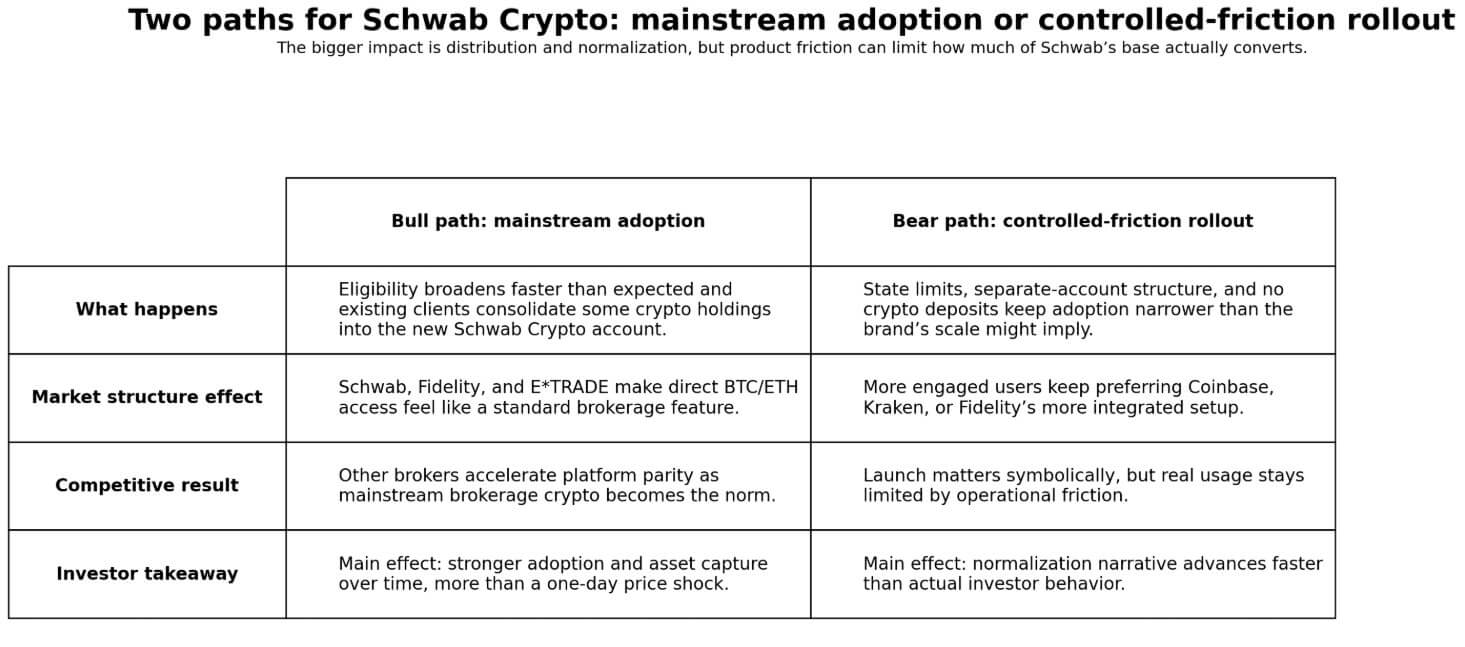

Charles Schwab operates 38.9 million active brokerage accounts and holds $12.22 trillion in client assets. For years, investors in those accounts could reach Bitcoin and Ethereum through ETFs, crypto-related equities, and futures.

A phased launch beginning in the second quarter closes the gap with direct investments. Schwab Crypto, offered through Charles Schwab Premier Bank, SSB, will let qualifying clients buy and sell Bitcoin and Ethereum directly.

The offer is available in all US states except New York and Louisiana, on a timeline that starts with employees and a small initial cohort before broadening.

Why this matters: Schwab is not introducing crypto to a crypto-native audience. It is testing whether direct Bitcoin and Ethereum ownership can sit inside the workflow of a mainstream brokerage customer. If that model gains traction, the implications reach beyond Schwab to product design, broker competition, and the next layer of retail crypto adoption.

The product architecture includes a structural boundary that clients and operators will immediately feel. Schwab Crypto operates through a dedicated account with an affiliated bank subsidiary.

This means that the structure is in a separate account from the brokerage accounts where investors already hold stocks, bonds, and ETFs. The crypto assets carry no SIPC or FDIC protection.

Schwab currently accepts no crypto deposits and does not settle securities or futures transactions in crypto. Mainstream access is real, and it arrives on carefully controlled broker-defined terms.

What drove the timing into 2026 is a policy calendar that dissolved three major institutional frictions within four months.

In January 2025, SAB 122 rescinded the earlier SAB 121 crypto safeguarding guidance that had made custody economics unattractive for traditional banks.

In March 2025, the OCC reaffirmed that crypto custody, certain stablecoin activities, and participation in distributed ledgers are permissible for national banks and removed the supervisory nonobjection requirement.

In April 2025, the Federal Reserve withdrew its earlier crypto guidance and moved to supervise those activities through the standard process.

Schwab CEO Rick Wurster described those regulatory moves as “pretty green” for large firms to expand into crypto, and the launch's timing confirms how directly the policy calendar shaped the product calendar.

| Date | Regulatory / market development | Why it mattered to Schwab |

|---|---|---|

| January 2025 | SAB 122 rescinded SAB 121 | Reduced a key accounting friction around crypto custody |

| March 2025 | OCC said crypto custody, certain stablecoin activity, and DLT participation are permissible; removed supervisory nonobjection requirement | Made bank-linked crypto activity easier to pursue |

| April 2025 | Federal Reserve withdrew earlier crypto guidance and moved to normal supervision | Reduced special-process friction for large institutions |

| March 2026 | Schwab research said Bitcoin had matured into a mainstream asset | Showed internal positioning had shifted toward normalization |

| Q2 2026 | Schwab began phased crypto rollout | Product timing followed the policy shift |

The asset Schwab is normalizing

In March 2026, Schwab published research describing Bitcoin as having matured into a mainstream asset and noting that by some measures it had become less volatile than certain Magnificent 7 stocks.

The research reflects the internal positioning that led to direct trading as the natural next step.

Reuters reported Wurster's view that the target user is an investor who already owns stocks and bonds and wants to hold a small slice of Bitcoin or Ethereum alongside those positions.

That is a narrower and more defensible market than the speculative base that drove 2021 volumes. Schwab is building a product for the mainstream investor who already trusts the brokerage brand and wants direct exposure within the brokerage environment they use.

Schwab enters a market that Fidelity already occupies. Fidelity's crypto account lets customers buy, sell, and transfer crypto through its platform and the Fidelity app alongside their existing brokerage positions.

E*TRADE has published a coming-soon page for direct trading in Bitcoin, Ethereum, and Solana, and reports point to Morgan Stanley plans to run that service through Zerohash in the first half of 2026.

Schwab enters this race as the scale normalizer, being the firm whose distribution footprint turns a multi-broker pattern into an industry default.

When Fidelity launched direct crypto, the market could read it as one firm's idiosyncratic call.

When Schwab, Fidelity, and E*TRADE each offer some version of direct BTC and ETH access, the mental category moves. When Schwab, Fidelity, and E*TRADE each offer some form of direct BTC and ETH access, direct crypto ownership sits on the same mental shelf as any other optional asset sleeve in a diversified brokerage account.

Schwab's own site already markets crypto exposure “from a brand you know,” and the launch extends that branding promise from wrappers to the asset itself.

A distribution thought experiment frames the scale without overclaiming a price surge.

If 0.5% of Schwab's 38.9 million accounts eventually hold direct crypto, that equals roughly 194,500 accounts. At 1%, it becomes approximately 389,000, and at 2% adoption, that funnel reaches roughly 778,000 accounts.

Two paths from here

The bull path opens if Schwab broadens eligibility faster than the phased language implies, and if the product experience proves clean enough for existing clients to consolidate crypto holdings into the new account.

In that scenario, Fidelity, E*TRADE, and Schwab together create a demand flywheel within the mainstream brokerage channel, the kind of end-investor adoption that Citi cited in its bull case of $165,000 for Bitcoin and $4,488 for Ethereum.

Schwab's distribution footprint alone would push every broker that still routes crypto clients exclusively to ETFs or education pages to accelerate its own platform-parity timeline.

The bear path runs through friction. The Schwab Crypto account's state restrictions, bank-subsidiary architecture, absence of crypto deposits, and current transfer limitations each create gaps relative to crypto-native venues that more engaged users will notice.

If those frictions keep adoption narrow and investors who want direct crypto exposure continue to prefer Coinbase, Kraken, or Fidelity's more integrated setup, the launch reads as operationally thin.

An investor who wants crypto to sit alongside equities within a single operational view may find the bank-subsidiary rail an exposure vehicle with tighter product boundaries than the brand's integrated-portfolio framing implies.

The next readable data point arrives when Schwab discloses how quickly the initial second-quarter cohort converts and if the broader rollout accelerates on schedule.

How quickly Schwab moves this cohort to general availability will tell the market whether this launch is a genuine scale ambition or a carefully managed compliance exercise.

The post Charles Schwab’s Bitcoin and Ethereum rollout shows crypto is moving deeper into mainstream brokerage accounts appeared first on CryptoSlate.

Bitcoin's price is still trading far above the depths of past bear markets, and that distance is now making the current moment feel pretty disorienting. Under the surface, a huge share of the market is already back in pain.

On-chain data show that by early April, roughly 46% of Bitcoin's supply was being held at a loss, meaning that nearly half of the coins on the network were last bought at prices above the current market price.

Markets tend to get emotionally unstable when large numbers of people are trapped in losing positions, and the gap between what a price chart shows and what the holder base actually feels can be quite large.

That's why the $60,000 level stands out. The number itself is all nice and round and memorable, but its real importance is in how it affects behavior. A move back there would pull even more of the market underwater and turn a slow grind lower into a vertical drop, a direct test of whether holders keep waiting or finally start selling.

People who bought during the run-up have long since shifted their attention from the next all-time high to harder questions: whether they misread the market, whether they should cut risk, and whether this drawdown has further to run. That's the territory where bottoms tend to form, and where panic, once it finds a foothold, tends to spread.

The deeper floor is still standing

The market is hurting, and the underlying levels that defined older cycle washouts are still holding.

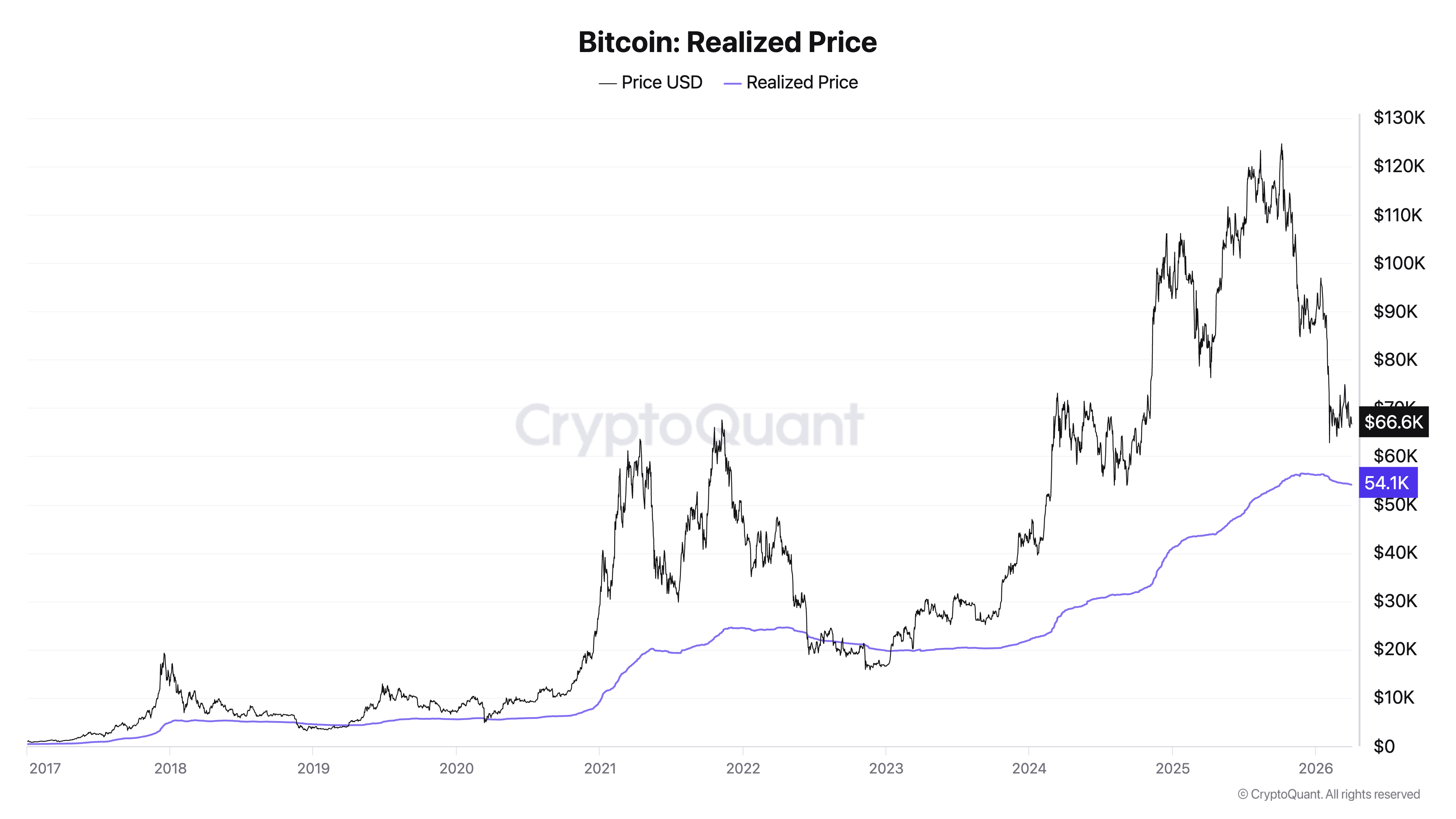

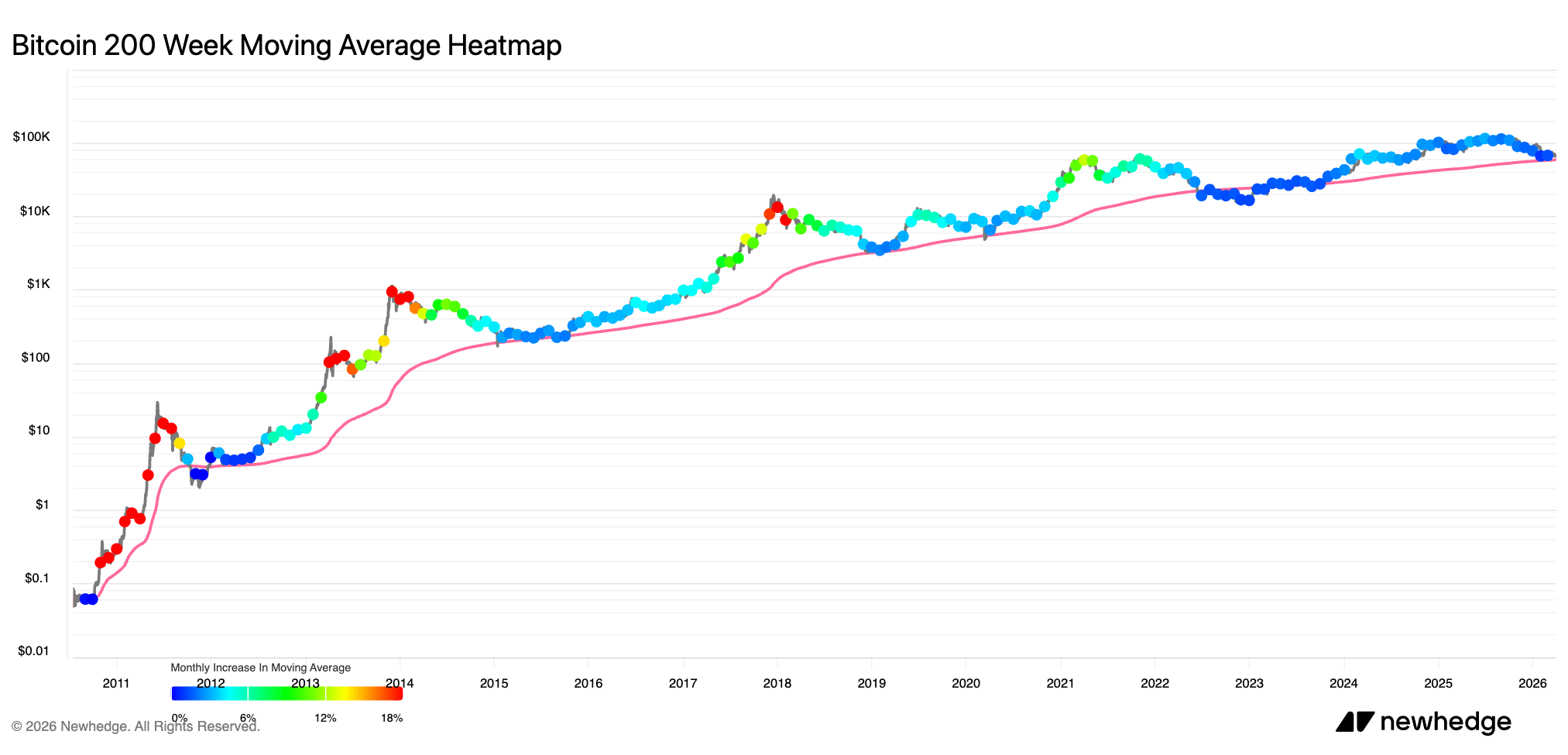

The best example of this is the realized price, one of Bitcoin's simplest long-term anchors. It represents the average price at which the network's coins last changed hands, and it currently sits near $54,100. Bitcoin remains above it even after this slide, which means the average holder across the whole network is still not carrying any losses.

The weekly chart confirms this. Bitcoin is also holding above its 200-week moving average, which sits around the high $50,000s, leaving the market in a very unusual position. It feels weak enough to scare people, sour sentiment, and leave a very large share of holders in the red, while the foundational levels that past bear markets reached remain intact.

That distinction may be the clearest difference between this cycle and earlier ones. Bitcoin still behaves like a volatile asset, and drawdowns still inflict real damage, but the altitude at which that damage is occurring has risen considerably. The pain is happening higher up the chart than it used to.

That elevation likely comes from a broader and sturdier owner base. Bitcoin has attracted more long-duration capital and more institutional exposure over the last few years. That gives the market more structural support than it had in previous cycles, when fear could drag prices straight through every historical floor with very little resistance.

The real question, then, is whether this market can absorb more discomfort before it turns into forced selling.

If Bitcoin falls toward $60,000 and holds, this cycle will have demonstrated something meaningful: nearly half the market is already underwater, and the deeper foundation is still standing. If that level gives way and mass selling begins, it won't be long before we see the familiar bear-market sequence play out again.

The visible and structural damages are operating on different levels right now. Bitcoin can still appear relatively fine on a long-term chart while a huge share of holders already feels squeezed, and for anyone watching from outside the asset, that tension is the most useful way to understand the moment.

The market is absorbing a serious amount of pressure, and the question of how much more it can take before the foundation shifts is one that the next few weeks will start to answer.

The post Why $60,000 decides whether Bitcoin’s recent strength cracks as nearly half the market slips into loss appeared first on CryptoSlate.

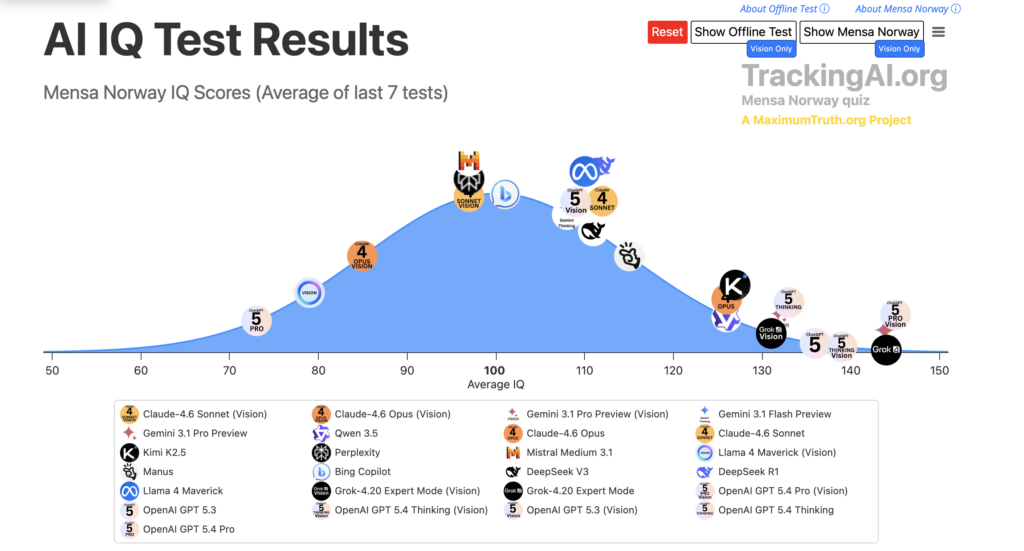

OpenAI’s latest GPT-5.4 Pro model has now achieved an IQ score higher than 99.96% of all human beings, giving markets a fresh signal that AI capability gains are starting to outpace the usual product-cycle noise.

OpenAI’s GPT-5.4 Pro touches 150 on public IQ benchmark as markets enter another macro-heavy week

TrackingAI’s public leaderboard now places OpenAI GPT-5.4 Pro at an IQ score of 150, a sharp step up from the 136 score that OpenAI’s o3 posted on the Mensa Norway test last year.

The jump arrives at a moment when market attention has narrowed around Iran, energy, labor softness, and the next inflation print. That creates a different question for the week ahead: how quickly is machine intelligence compounding, and when will that acceleration begin to overlap with economic positioning?

Why this matters: A move from 136 to 150 on a widely understood benchmark compresses a complex capability shift into a simple signal. For businesses, that signal feeds directly into decisions around automation, software budgets, and headcount planning. For markets, it adds another variable alongside rates, inflation, and growth expectations.

OpenAI introduced GPT-5.4 as its most capable and efficient frontier model for professional work, with stronger coding, tool use, and computer use, and a context window of up to 1 million tokens. In the same release, OpenAI said GPT-5.4 achieved a new state of the art on GDPval and exceeded human performance on OSWorld-Verified.

Those benchmarks are separate from a public IQ test, yet the direction of travel aligns. Capability is rising across separate measurement systems, and that rise is becoming fast enough to influence budgeting, hiring plans, workflow design, and software spend.

A score of 150 on a public IQ-style benchmark compresses a broader capability move into a single, portable signal. The number is easy to understand even before the methodology is debated.

The earlier o3 Mensa result established the benchmark and its limits. GPT-4.1’s one-million-token context window showed how OpenAI was extending model utility across long-horizon code and document tasks, while our analysis of OpenAI’s expanding capital loop linked model progress to hardware expansion, financing loops, and infrastructure demand.

Taken together, those developments place the latest IQ score within a broader commercial and economic context. A move from 136 to 150 on a public benchmark is striking on its own. A move from 136 to 150 while OpenAI is pushing deeper into tool use, computer use, enterprise productivity, and capital-intensive infrastructure carries broader implications.

Public IQ benchmarks are limited, but the capability curve is still moving higher

Public IQ-style tests remain imperfect instruments for measuring frontier models. TrackingAI runs a public Mensa-style benchmark and also maintains a harder private offline test.

IQ-style tests compress a narrow slice of cognitive performance into a single number, obscuring variation across reasoning types, context handling, creativity, and real-world problem-solving.

For AI and humans alike, scores are sensitive to test design, training exposure, and pattern familiarity, which makes them a noisy proxy for general capability.

An IQ of 150 sits at the extreme upper tail of the distribution, often associated with individuals such as Albert Einstein or Richard Feynman. In practical terms, it implies very fast abstraction, strong pattern recognition, and the ability to navigate complex, multi-step problems with limited guidance.

The platform reports scores as rolling averages across recent completions, and the methodology raises familiar questions around prompt structure, reproducibility, training-set contamination, and format familiarity. Those concerns were already visible when o3 reached 136, and they remain active now that GPT-5.4 Pro sits at 150.

Even with those limits, the broader pattern has become harder to dismiss. One isolated benchmark result can be explained away as a quirk. A cluster of gains across public IQ-style testing, coding, browser use, desktop navigation, and knowledge-work performance carries more analytical weight.

TrackingAI’s latest leaderboard places GPT-5.4 Pro at the top of its public IQ board ahead of all Cluade, Gemini, Qwen, and Grok models, offering an external, legible public benchmark that maps quickly onto the broader capability debate.

Few people need a detailed understanding of benchmark design to grasp that 150 sits in a rare range and investors do not need to accept every premise behind an IQ-style test to recognize that a jump of this size suggests acceleration rather than drift.

Enterprise buyers also do not need to believe that IQ equals general intelligence to see that systems with stronger pattern recognition, stronger tool use, and stronger long-horizon task handling are moving toward economically useful territory, extending far beyond puzzle-solving.

This points toward systems that can search, plan, verify, navigate, and produce real work across extended contexts. In that setting, the IQ score functions less as a novelty number and more as a signal of the density of frontier reasoning.

There is also competitive value in the leaderboard itself. A leadership position on a public benchmark reinforces OpenAI’s standing in the race for visible capability leadership, especially at a moment when model differentiation is becoming harder to discern from architecture notes alone.

Benchmark leadership compresses complexity into a simple hierarchy. It offers developers a signal, enterprise buyers a narrative handle, and investors another proxy for where the capability frontier currently sits.

OpenAI’s benchmark climb is beginning to overlap with the economic week ahead

The week ahead still runs through macro. The Bureau of Labor Statistics calendar clearly lays out the next key releases: the FOMC minutes from the March 17 to 18 meeting, due on April 8; the March Consumer Price Index, due on April 10; and the March Producer Price Index, due on April 14.

That schedule keeps rates, inflation, and growth anxiety in the foreground, but beneath that surface, a second economic track is taking shape, and OpenAI sits near its center.

Capability growth in frontier AI increasingly intersects with capital allocation. A model that pushes higher on public reasoning tests while also improving in coding, search, and computer use changes how businesses think about workflow redesign. It changes what software buyers expect from copilots and agents. It changes how quickly enterprises move from experimentation toward deployment.

Jack Dorsey recently posted that Block is moving “from hierarchy to intelligence,” using AI to take over coordination work once handled by management layers as the company reorganizes around individual contributors, directly responsible individuals, and player-coaches

Capability growth also changes which tasks can be carved out of labor cost structures and reassigned to software. These effects move through narrower channels first, including document workflows, spreadsheet workflows, customer support, research tasks, browser automation, internal operations, code generation, and verification loops.

OpenAI’s commercial direction reinforces that interpretation. In its GPT-5.4 launch materials, the company described stronger performance in professional work, stronger tool search, native computer use, and gains in benchmarked knowledge work across occupations that map directly onto the U.S. economy.

That places AI capability growth inside a familiar market question, where spending flows next if these systems continue improving at this pace.

The answer extends beyond model subscription revenue into cloud demand, chips, data centers, networking, power, software licenses, and labor productivity assumptions. OpenAI’s expanding capital loop already reflects part of that structure, and the benchmark gain adds a simpler public-facing signal on top of it.

That overlap is what gives the latest result broader relevance during a macro-heavy week. Markets already know the CPI setup. Markets already know oil prices can feed into inflation expectations. Markets already know the Fed minutes will be parsed for policy tone.

But is the growth in intelligence itself beginning to behave like a macro variable? Faster capability gains can alter enterprise spending plans, tighten competitive pressure across white-collar functions, support higher infrastructure outlays, and strengthen the case for AI-linked capital expenditure even in a slower nominal growth environment.

When TrackingAI shows GPT-5.4 Pro at 150, the number falls within a market that already views OpenAI as more than a lab. It is a platform company, a deployment company, an infrastructure customer, and a signal generator for adjacent sectors.

The next test sits in two places at once. One is methodological; public IQ-style benchmarks will keep drawing scrutiny, and they should. The other is economic; markets will decide, step by step, whether capability jumps of this size deserve to be priced alongside labor data, rate expectations, and capital spending trends.

OpenAI’s latest benchmark climb pushes that decision closer. The score is compact, legible, and easy to circulate. Its deeper relevance comes from the same place as the company’s broader product push; the frontier is still climbing, and the economic footprint of that climb is becoming harder to keep in a separate category.

The post GPT-5.4 Pro jumps to 150 IQ on MESNA Norway test as OpenAI breaks its own record appeared first on CryptoSlate.

In July 2025, Genius Group announced it was targeting a Bitcoin treasury of 10,000 BTC, framing it as a statement of deep strategic conviction.

This week, however, the company sold its last 84 BTC to pay off $8.5 million in debt and declared its treasury empty. The 18-month gap between those two moments is a perfect example of what's happening to the Bitcoin treasury trade right now.

Why this matters: The Bitcoin treasury narrative has been one of the market’s strongest structural bullish arguments. If corporate and sovereign holders behave like cyclical sellers rather than long-term accumulators, institutional adoption may amplify volatility instead of stabilizing it.

Public companies, including Empery, Genius Group, and Riot, have all sold Bitcoin this week, citing debt repayment, liquidity needs, or strategic pivots into AI and high-performance computing, while sovereign selling accelerates with Bhutan offloading more holdings.

Taken individually, each of these is an easily explainable non-event. But taken together, they expose a structural problem with a trade built on the promise of permanence: for a growing number of holders, Bitcoin is now the first asset they sell when the bills arrive.

The treasury trade rests on a simple pitch. Starting around 2020 and accelerating through 2024, publicly traded companies began buying Bitcoin with corporate cash or borrowed money and presenting it to investors as a reserve asset superior to inflation-eroded cash.

A few high-profile early movers delivered spectacular returns, and the strategy spread. Public companies now hold roughly 1.165 million bitcoin worth approximately $77 billion, more than five percent of the currency's fixed supply of 21 million coins.

The problem is that a reserve asset only functions as advertised if the holder never needs the cash back.

In the Bitcoin treasury trade, the debt comes first

Riot Platforms, one of the largest publicly traded Bitcoin miners in the US, sold 5,363 BTC for approximately $535.5 million in 2025, with its annual filing explicitly tying retention decisions to cash requirements for operations and expansion.

An earlier filing had already disclosed 3,300 BTC pledged as collateral against a $200 million credit facility. Riot continues to tap its treasury to fund a pivot into AI and high-performance computing, a strategy increasingly seen across the mining industry.

MARA Holdings sold 15,133 BTC for around $1.1 billion in March, using the proceeds to retire approximately $1 billion of convertible senior notes. Empery Digital sold 370 BTC for $24.7 million and used the proceeds to repay its outstanding term loan in full, freeing 1,800 BTC it had previously posted as collateral. Its shares are down 75% from their 2025 high.

The sequence is consistent across all of them: Bitcoin accumulated during optimism, pledged when capital was needed, and liquidated when the debt came due.

It's worth noting that the largest and best-capitalized players are still adding to their positions.

Metaplanet acquired 5,075 BTC in the first quarter of 2026, making it the third-largest corporate holder, while Strategy holds over 762,000 BTC as by far the largest treasury position in existence.

This tells us that the treasury trade isn't collapsing uniformly, but sorting into two camps: deep-pocketed accumulators who can afford to wait, and cash-pressured sellers who discover, when conditions tighten, that their strategic reserve is their most liquid asset.

The reserve asset that was always too easy to sell

The Bitcoin treasury trade gets quite a bit of weight when sovereign actors enter it.

Bhutan, a small Himalayan kingdom, built one of the world's more unusual government Bitcoin positions by mining it using surplus hydroelectric power at near-zero cost. The country's stack has fallen from a peak of about 13,000 BTC in late 2024 to roughly 5,400 BTC, a 58% reduction, with activity managed by its state-owned investment arm, Druk Holding and Investments.

Throughout March 2026, Bhutan offloaded tens of millions worth of BTC through controlled, low-impact transfers with no market disruption. This kind of distribution pattern shows that the treasury was running a planned drawdown rather than being shaken out by debt.

A significant portion of the cash from the offloaded Bitcoin was directed toward Gelephu Mindfulness City, a major national development project requiring real capital. Because Bhutan mined its coins rather than bought them, every sale it made was pure profit. The underlying logic, though, is exactly like that of our previously mentioned corporate sellers: the position exists to be monetized when a need for funding arises.

Bitcoin has been struggling to retain support at $67,000, going above and below the critical level for days. Altcoins are also struggling, with larger coins like ETH and SOL losing anywhere between 4% and 8% daily, while smaller tokens keep seeing even wilder volatility. With $200 million to $400 million liquidated every day in the past week, it's safe to say that crypto markets have been feeling the geopolitical pressure hard.

In that environment, treasury selling does more than just add supply to a struggling market. It exposes something the treasury trade's most enthusiastic architects may not have fully reckoned with: they built a buyer base out of the wrong material.

There's a deep irony in this. The very properties that made Bitcoin attractive as a treasury asset in the first place (its liquidity, its 24-hour markets, the frictionless ease of converting it to cash at any hour on any day) are exactly the properties that make it the first thing a cash-pressured CFO reaches for when a debt payment looms.

Compared to gold, Bitcoin is trivially quick and easy to sell, and the Bitcoin treasury promise of having a liquid alternative to cash inadvertently handed companies, well…a liquid alternative to cash.

Liquidity, by definition, gets used. Every company that pledged its BTC as loan collateral was simultaneously creating a forced-selling mechanism and embedding a potential margin call into its own balance sheet.

The longer-term consequence for Bitcoin is harder to quantify but still worth considering seriously. The institutional adoption story has been one of the most durable bullish arguments for Bitcoin over the past four years, resting on the assumption that corporate and sovereign buyers represent a fundamentally different, stickier class of holder than retail speculators.

If the current wave of selling establishes instead that treasury holders are just pro-cyclical, buying during enthusiasm, pledging during expansion, and then liquidating during stress, then the arrival of institutional capital does nothing to change Bitcoin's volatility profile. It just adds a more elaborately dressed version of the same behavior.

The buyers still standing, Strategy with its 762,000 BTC and Metaplanet with its methodical quarterly accumulation, may yet prove the thesis right, but they're proving it almost alone, which was never the point.

The treasury trade was supposed to be a movement, a permanent re-rating of how the world's balance sheets relate to a fixed-supply digital asset. What it turns out to have been, for a significant and growing number of its participants, is a short-term financing strategy wearing the mask of long-term conviction. When the mask comes off, what remains is an asset people buy when they have money to spare and sell when they don't, which is not a reserve but just another position.

The post Bitcoin’s “permanent buyers” are starting to sell as debt and cash pressures mount appeared first on CryptoSlate.

Cryptoticker

The first week of April 2026 has been a study in contrasts. While the broader financial markets grapple with macroeconomic shifts, the digital asset sector is doubling down on technical evolution. We are seeing a move away from the "meme-coin" cycles of the past toward institutional-grade infrastructure and significant protocol overhauls.

Crypto News Today: Market Highlights

The crypto market today is defined by Bitcoin’s price stability near the $67,000 mark and massive anticipation for Ethereum’s Glamsterdam upgrade. Simultaneously, a significant exploit on the Solana-based Drift Protocol has served as a stark reminder of the security risks still inherent in decentralized finance (DeFi).

Market Snapshot: Bitcoin’s Quiet Resilience

Despite a slight 0.42% dip in the last 24 hours, Bitcoin ($BTC) continues to act as a stabilizing force for the entire ecosystem. Trading at approximately $67,000, the asset has shrugged off recent geopolitical volatility.

- Institutional Inflow: Recent reports from Goldman Sachs suggest that institutional "dip-buying" is keeping the floor high.

- Price Tracking: You can monitor live movements on our Bitcoin Ticker.

Ethereum Roadmap: The Glamsterdam Era

The biggest story in the developer community is the finalized scope for Ethereum’s Glamsterdam upgrade. Scheduled for the first half of 2026, this hard fork is expected to be a "game-changer" for scalability.

What is the Glamsterdam Upgrade?

Glamsterdam is the next major evolution of the Ethereum mainnet following the Fusaka update of late 2025. Its primary goals are:

- Gas Fee Reduction: A projected 78.6% reduction in fees for smart contract calls.

- Parallel Processing: Introducing the ability to process multiple transactions simultaneously.

- Throughput: Increasing the gas limit per block from 60 million to 200 million.

This upgrade is essential for $Ethereum to remain competitive against high-speed chains like Solana.

The Solana Hack: Drift Protocol Exploit

While Ethereum builds, $Solana has hit a major speed bump. On April 1, 2026, the Drift Protocol—the network's largest perpetual futures exchange—was drained of $286 million.

"The breach was not a simple code bug, but a sophisticated six-month social engineering operation by highly resourced actors." — Drift Protocol Preliminary Report.

The attackers reportedly posed as a quantitative trading firm to gain the trust of the protocol's security council. This event has reignited discussions on the necessity of hardware wallets for all DeFi participants.

Regulatory Milestone: Coinbase Nabs OCC Approval

In a massive win for US-based crypto, Coinbase has received conditional approval from the Office of the Comptroller of the Currency (OCC) for a national trust charter.

This does not make Coinbase a traditional commercial bank, but it provides federal regulatory uniformity for its custody business. This moves Coinbase into the same regulatory conversation as legacy giants like JPMorgan, further bridging the gap between "crypto" and "finance."

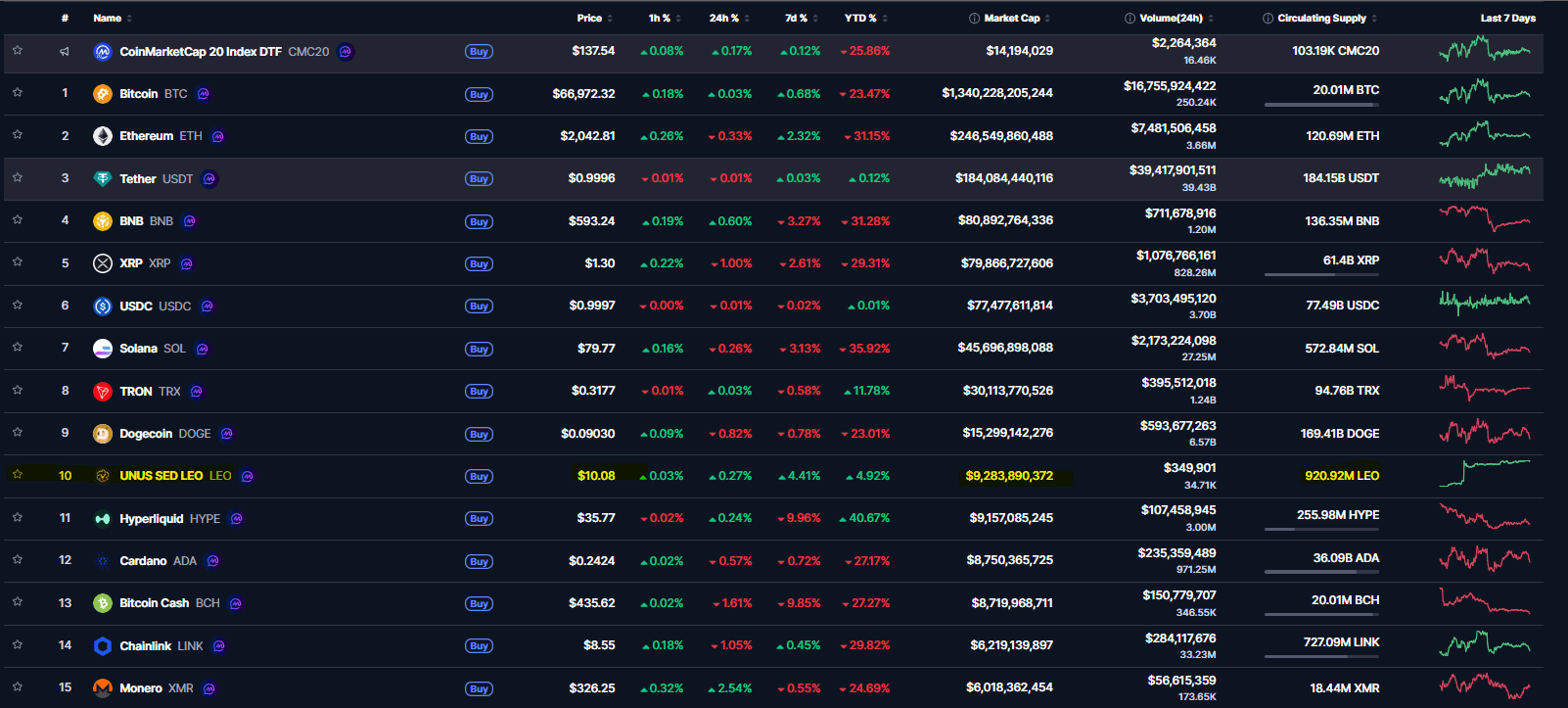

In a market often dominated by volatile meme coins and complex DeFi protocols, UNUS SED LEO ($LEO) has quietly climbed the ranks to become a heavyweight in the digital asset space. Originally launched as a utility token for the iFinex ecosystem, LEO has transitioned from its initial $1 exchange offering to a valuation exceeding $10 per token.

As of April 2026, LEO has officially broken into the top 10 largest cryptocurrencies by market capitalization, boasting a valuation of approximately $9.3 billion. This article explores the unique fundamentals, the aggressive deflationary model, and the institutional backing that have fueled this 1,000% journey.

What is UNUS SED LEO?

UNUS SED LEO is the native utility token of the iFinex ecosystem, which includes the prominent Bitfinex exchange. Launched in May 2019, the token was designed to provide holders with significant fee discounts and a variety of benefits across the platform's services. Unlike many other assets, LEO is a multi-chain token, existing on both the Ethereum and EOS blockchains to maximize accessibility.

Why is it named like this?

The token's name, "Unus Sed Leo," is Latin for "One, but a lion," a motto emphasizing quality and strength over quantity. It was born out of a crisis: iFinex launched the LEO token to raise $1 billion in capital after a payment processor's funds were seized by government authorities.

While it started as a recovery mechanism, it evolved into a pillar of exchange-based utility. Its primary function is to offer:

- Trading fee reductions: Up to 25% discount for holders.

- Lending fee discounts: Significant reductions for peer-to-peer lenders.

- Withdrawal/Deposit perks: Faster and cheaper transactions on Bitfinex.

The Path from $1 to $10: Why is the Price Rising?

The rise of LEO from its $1 launch to the current $10.05 level is not merely speculative; it is driven by one of the most transparent and aggressive buyback and burn mechanisms in the industry.

1. The 27% Revenue Burn

iFinex is contractually committed to using at least 27% of its consolidated monthly revenue to buy back LEO tokens from the open market and permanently destroy them. This creates a perpetual buy-side pressure. As Bitfinex remains a top-tier exchange for professional traders, this revenue stream provides a "floor" for the token price.

2. The Bitcoin Recovery Catalyst

A major factor in the 2024–2026 rally has been the legal resolution regarding the 2016 Bitfinex hack. Following court orders, nearly 94,643 BTC were earmarked for recovery. According to the token's whitepaper, 80% of recovered funds must be used to repurchase and burn LEO tokens. With $Bitcoin prices reaching new heights, the sheer dollar value of this buyback program has caused massive supply shocks.

3. Low Volatility and Institutional Trust

Unlike highly liquid assets that fluctuate wildly, LEO often shows "resilience" during market crashes. Because so much of the supply is held by long-term investors or is being systematically burned, the circulating supply (currently around 920 million LEO) continues to shrink, making each remaining token more valuable.

How LEO Price Reached the Top 10 Cryptos

Reaching the #10 spot by market cap is a feat of endurance. LEO's ascent was accelerated by the downfall of other exchange tokens (such as FTT) and the growing demand for "safe haven" utility assets.

| Feature | UNUS SED LEO (LEO) |

|---|---|

| Current Price | $10.05 |

| Market Cap Rank | #10 |

| Circulating Supply | ~920.9 Million |

| Max Supply | Decreasing Monthly |

By maintaining a steady growth trajectory while the broader altcoin market experienced massive drawdowns, LEO became a "non-correlated" asset. This attracted portfolio managers looking for stability.

From Digital Gold to Digital Dust

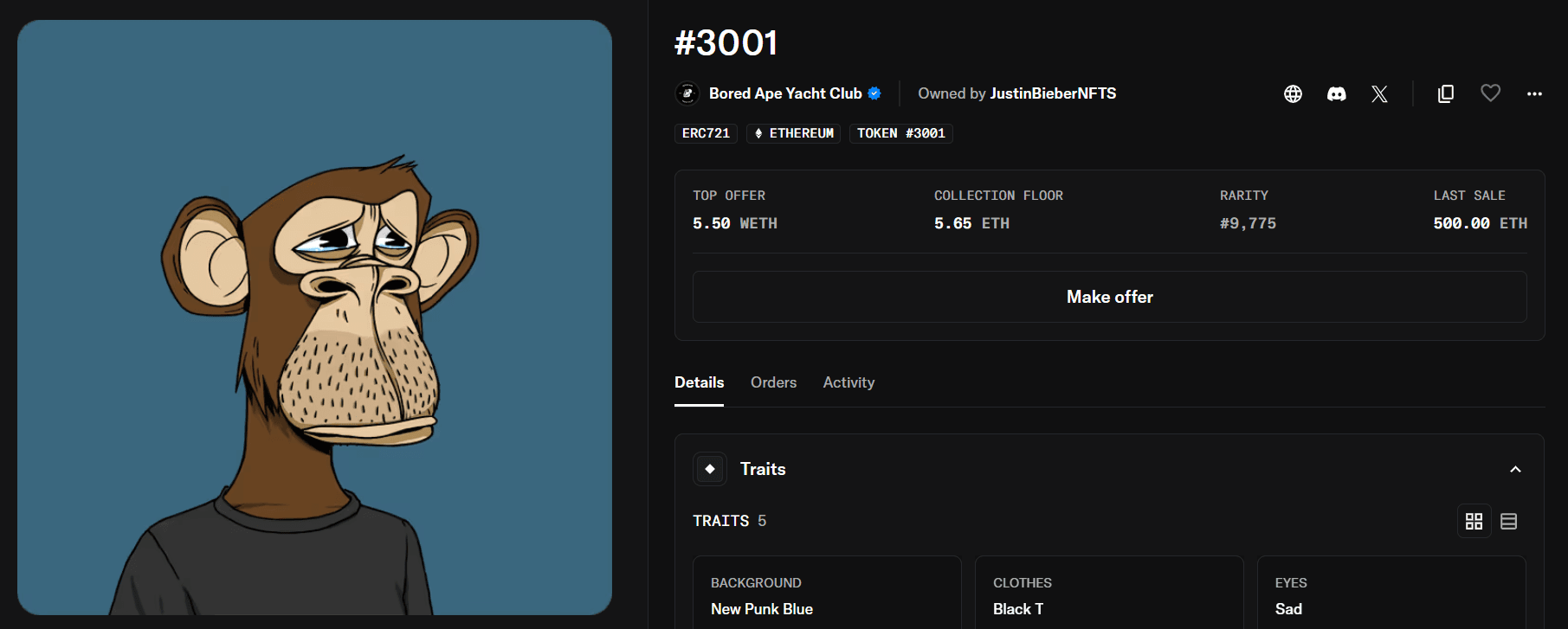

In early 2022, the world of Non-Fungible Tokens (NFTs) was at its absolute zenith. Celebrities were flocking to the space, led by pop icon Justin Bieber, who made headlines by purchasing a Bored Ape Yacht Club (BAYC) NFT for a staggering sum. At the time, it was seen as a bold entry into the future of digital art and web3.

Fast forward to April 2026, and the landscape has shifted dramatically. The speculative bubble that once valued "cartoon apes" at millions of dollars has largely evaporated, leaving high-profile investors like Bieber with massive "paper" losses.

The $1.3 Million Entry: Bored Ape #3001

In January 2022, Justin Bieber acquired Bored Ape #3001 for 500 ETH. At the exchange rates of that time, the transaction was valued at approximately $1.3 million.

The purchase was immediately controversial among NFT collectors. Analysts pointed out that Bieber paid nearly five times the "floor price" for an ape that possessed relatively common traits. While $Bitcoin and $Ethereum were experiencing high volatility, the NFT market was still fueled by extreme hype and celebrity endorsements.

Why Did He Pay Such a Premium?

- Aura of Exclusivity: Ownership of a BAYC acted as a digital "black card" for elite social circles.

- Market Sentiment: In 2022, the belief was that "blue-chip" NFTs would act as a store of value similar to fine art.

- FOMO: Fear of missing out on the next evolution of social media avatars.

The 2026 Reality: A 99% Valuation Wipeout

Today, the secondary market for the Bored Ape Yacht Club collection tells a much different story. As of April 2026, the floor price for the collection has retreated to approximately 5.25 ETH to 6 ETH. With the current Ethereum price stabilizing around $2,000, Bieber’s Bored Ape is now valued at roughly $12,000.

This represents a staggering 99% decline from his initial investment. Even when compared to the broader crypto market news, the drawdown in the NFT sector has been significantly more severe than that of major cryptocurrencies like BTC or ETH.

Celebrity NFT Portfolios in 2026

Bieber isn't the only celebrity facing a "re-valuation" of his digital assets. The following table illustrates the peak vs. current estimates for major celebrity BAYC holders:

| Celebrity | Asset | Purchase Price (Est.) | Current Value (2026) | Total Loss |

|---|---|---|---|---|

| Justin Bieber | BAYC #3001 | $1,300,000 | ~$12,000 | -99% |

| Eminem | BAYC #9055 | $462,000 | ~$78,000 | -83% |

| Stephen Curry | BAYC #7990 | $180,000 | ~$85,000 | -53% |

Note: Differences in loss percentages are often due to the rarity of the specific traits or the timing of the purchase.

Lessons from the NFT Bubble

The collapse of Bored Ape prices serves as a cautionary tale regarding liquidity and speculative assets. Unlike trading on major exchanges, where you can sell a token instantly, NFTs are illiquid. You need a specific buyer willing to pay your asking price for your specific token.

Furthermore, as reported by major financial outlets like Bloomberg, the shift toward "utility-based NFTs"—assets with actual function in gaming or identity—has left purely "profile picture" (PFP) projects struggling to regain their former glory.

Is there a Future for BAYC?

While the dollar value has dropped, Yuga Labs continues to develop the "Otherside" metaverse. However, for investors who entered during the 2022 frenzy, the road to "breaking even" appears nearly impossible. Most experts now categorize early NFT purchases as high-risk speculative plays rather than foundational investments.

Michael Saylor has sparked a fresh wave of debate with his latest X post, claiming it is a "Good Friday to buy Bitcoin." This comes as the $BTC price lingers near $67,400, a staggering 46% drop from its 2025 peak of $125,000.

The "Saylor Signal" vs. Market Reality

MicroStrategy Executive Chairman Michael Saylor is back to his usual bullish antics. On April 3, 2026, he took to X (formerly Twitter) to declare, "It’s a Good Friday to buy Bitcoin." For the "HODL" community, this is a standard rallying cry. However, for investors who watched Bitcoin plummet from a euphoric $125,000 in October 2025 to its current level of approximately $67,400, the message feels different this time.

The market is currently grappling with a "correlation crisis." While Saylor remains the ultimate $Bitcoin maximalist, his firm has shifted focus toward its new "STRC" preferred stock dividends. With significant unrealized losses on recent tranches, many are wondering: Is this a genuine "buy the dip" opportunity, or is the "Saylor Signal" losing its luster?

Should You Buy Bitcoin Now?

Whether "now" is a good time to buy depends on your time horizon. Technically, Bitcoin is in a clear downtrend on the daily charts. However, historically, buying during 40-50% drawdowns from all-time highs (ATH) has been a profitable long-term strategy. The current price of $67,400 represents a significant discount for those who missed the $100k+ rally, but macro headwinds suggest the bottom may not be in yet.

The 2026 Bitcoin Crash Explained

To understand why Saylor is calling for buys now, we must look at why the price crashed. The decline from $125,000 was not a single event but a "perfect storm" of factors:

- Monetary Policy Shifts: Recent hawkish signals from the Federal Reserve have drained liquidity from "risk-on" assets.

- Institutional De-risking: After the euphoria of 2025, major players have been trimming Bitcoin ETF holdings to lock in profits or cover losses in equities.

- The $67k Magnet: Since breaking below the $90,000 support, Bitcoin has been searching for a stable floor, finally resting in the mid-60s.

Historical Performance on Good Friday

While Saylor's post uses the holiday as a backdrop, does Bitcoin actually perform well on Good Friday? Historically, the Friday of Easter weekend sees lower trading volumes as traditional markets are closed. This "thin" liquidity can lead to sharp, erratic moves, but there is no statistically significant "holiday pump" trend. In fact, Bitcoin price action today remains largely sideways, reflecting what analysts call "aggressive caution."

Bitcoin Price Analysis: Analyzing the $67,400 Support

From a technical standpoint, Bitcoin is currently testing a critical psychological floor.

- Support Level: The $65,000 - $67,000 zone is vital. If BTC fails to hold this, the next major support sits at $58,000.

- Resistance: To turn bullish, BTC must reclaim the $72,000 level to break the current series of "lower highs."

Hedge funds have reportedly unwound nearly a third of their Bitcoin exposure according to recent Bloomberg market data. This institutional exit is the primary reason the price hasn't bounced as aggressively as retail traders hoped.

Bitcoin Strategy: How to Position Your Portfolio

If you are following Saylor’s advice, risk management is paramount:

- DCA (Dollar Cost Averaging): Instead of going "all-in," spread purchases over several weeks.

- Self-Custody: Given the volatility, moving assets to hardware wallets is recommended to avoid exchange risks.

- Monitor the DXY: A stronger U.S. Dollar usually correlates with further drops in the crypto market.

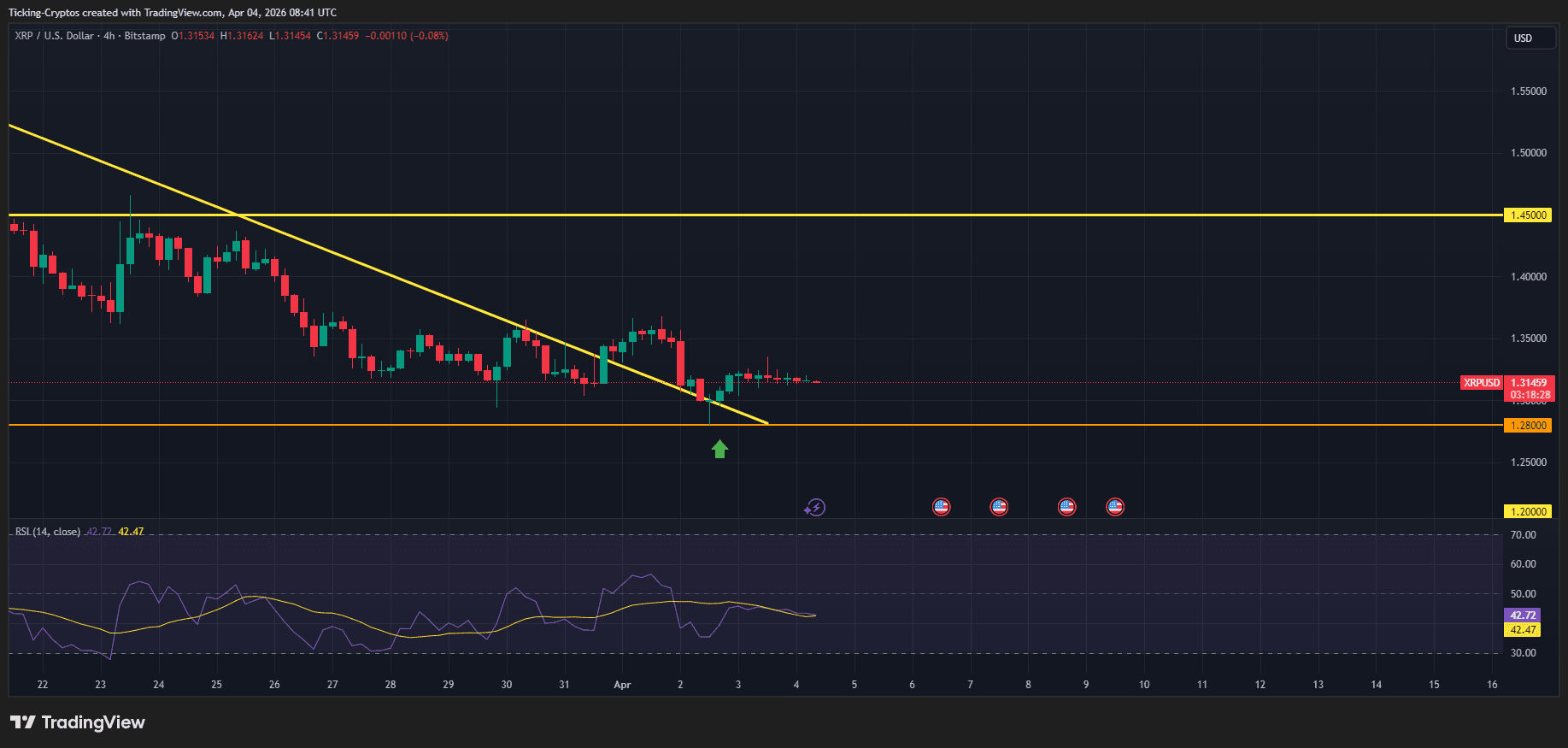

- XRP enters a pivotal 2026 phase despite weak price action

- Ripple is expanding utility via XRP Ledger and RLUSD

- Strong fundamental growth continues, especially in Asia and institutional adoption

XRP Price Today: Bulls Struggle at Key Support

As of April 4, 2026, the XRP price (referenced against major pairs) is trading near the $1.31 mark. Following a rejection at the $1.60 resistance level in late March, the token has entered a period of consolidation. Technical indicators like the Money Flow Index (MFI) are currently hovering around 35, suggesting that XRP is approaching oversold territory.

Traders are closely watching the $1.25 support level. A breakdown below this could see a retest of the 52-week low near $1.21. Conversely, a daily close above the 7-day Moving Average ($1.33) is required to signal a short-term trend reversal.

Ripple News Today with RLUSD

A major highlight in today's news is the continued expansion of Ripple’s dollar-pegged stablecoin, RLUSD.

- South Korean Expansion: Ripple recently secured a listing for RLUSD on Coinone, one of South Korea's premier regulated exchanges. This allows for direct KRW/RLUSD trading, tapping into one of the world's most active XRP trading communities.

- Institutional Minting: On-chain data reveals significant activity, including a massive 69 million RLUSD mint earlier this month linked to Gemini.

- SWIFT Partnership: Ripple Treasury has officially joined the SWIFT partner program, a move designed to bridge traditional banking infrastructure with digital asset settlement.

The CLARITY Act: A Double-Edged Sword?

The legislative landscape is shifting with the introduction of the CLARITY Act in the U.S. Senate. This bill aims to provide a definitive framework for stablecoins and digital assets.

The latest draft of the CLARITY Act proposes a ban on yield for passive stablecoin holdings. While this could hurt competitors like USDC, analysts suggest that RLUSD is uniquely positioned. Because RLUSD’s growth is driven by cross-border payments and institutional collateral rather than retail yield incentives, it may emerge as a primary beneficiary of these new rules.

XRP Price Prediction for 2026

Despite the current price stagnation, institutional sentiment remains cautiously optimistic. Many analysts, including those from Standard Chartered, maintain year-end targets for XRP above $2.50, citing the eventual "re-risking" of the market as regulatory clarity settles.

Decrypt

Claude developer Anthropic registered an employee-funded PAC amid a legal battle with the White House and rising election-year scrutiny of AI.

Researchers say internal emotion-like signals shape how large language models make decisions.

Financial giant Charles Schwab is set to launch spot buying of Bitcoin and Ethereum by the end of the quarter, the firm said Friday.

The FIFA World Cup will feature a prediction market platform built on ADI Chain, with the network’s token hitting a new high Friday.

Publicly traded Bitcoin miner MARA cut 15% of its staff this week after selling $1.1 billion in Bitcoin to fuel an AI push.

U.Today - IT, AI and Fintech Daily News for You Today