Cryptocurrency Posts

Crypto Briefing

Rising odds of U.S. ground forces in Iran signal heightened geopolitical tensions, impacting global markets and strategic military dynamics.

The post US odds for ground forces entering Iran by April 30 jump to 86% appeared first on Crypto Briefing.

The increased odds of U.S. military involvement in Iran highlight escalating tensions and potential geopolitical instability.

The post US rescue operation follows claims of downed fighter jet in Iran appeared first on Crypto Briefing.

The rise in tokenized real-world assets amid crypto struggles highlights a shift towards stability and institutional trust during geopolitical tensions.

The post Tokenized real-world asset market hits $27.6B in April 2026 amid crypto downturn appeared first on Crypto Briefing.

Zarif's peace plan highlights the complexities of US-Iran relations, with market optimism suggesting potential diplomatic progress by mid-year.

The post Zarif proposes US-Iran peace plan as ceasefire odds drop to 2% for April 7 appeared first on Crypto Briefing.

Market skepticism highlights the challenges of achieving US-Iran peace, reflecting broader geopolitical tensions and uncertainty.

The post Iran’s former foreign minister proposes peace plan with US, market skeptical appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Cathie Wood Calls Bitcoin’s 50% Crash a “Victory” as Market Tests New Floor

Nearly six months after the Oct. 10 flash crypto crash erased millions of dollars in a single day, Bitcoin remains under pressure, trading well below its recent peak. The asset reached an all-time high of $126,080 on Oct. 6, but has since fallen about 47% to roughly $67,000.

Despite the drawdown, Cathie Wood, a long-time BTC advocate and chief executive of ARK Investment Management, is urging investors to maintain a long-term perspective.

Wood, whose firm was among the first publicly listed asset managers to gain exposure to Bitcoin in 2015, has maintained an active presence in crypto-related equities. ARK Invest continues to trade shares of companies tied to the digital asset sector, including Coinbase, Robinhood Markets, Block, Circle Internet Group, Bitmine Immersion Technologies, and Bullish, adjusting positions in response to market conditions.

In an interview on CNBC’s Squawk Box, Wood addressed the current downturn, framing the magnitude of BTC’s decline as a sign of maturation rather than weakness.

She argued that a roughly 50% drop from peak levels represents a shift from the extreme volatility seen in earlier cycles, when Bitcoin routinely experienced drawdowns of 85% to 95%.

NEW: Ark Invest CEO Cathie Wood says on CNBC that Bitcoin's usual -85% collapses are "DONE"

— Bitcoin Magazine (@BitcoinMagazine) April 3, 2026

"This is a prove technology, it's a proven monetary system, and it's a new asset class."pic.twitter.com/j0OU62hWmj

According to Wood, such severe collapses are unlikely to recur. She described Bitcoin as a “proven technology” and a “new asset class,” suggesting that its market behavior has evolved alongside broader adoption and institutional participation.

In her view, the current correction would be considered a “real victory” within the Bitcoin community if losses remain limited to around half of its peak value.

Bitcoin’s vicious cycles

Historical data supports the comparison to prior cycles, though the current downturn has yet to match earlier bear markets in severity. During the 2021–2022 cycle, Bitcoin fell nearly 80% from its then-record high of about $69,000, eventually bottoming near $15,600.

Onchain data from Glassnode indicates that the present decline, measured against the October 2025 high, has reached roughly 52% at its lowest point.

All this is happening as bitcoin’s price decline forces a growing number of public companies and sovereign entities to unwind their BTC treasuries, marking a sharp reversal from the accumulation trend of the past two years. Firms that once championed long-term holding are now selling to manage liquidity, repay debt, and fund strategic pivots.

Companies like Riot Platforms, Genius Group, Empery Digital, Nakamoto Holdings, and Marathon Digital have all reduced holdings, in some cases significantly. Marathon alone sold over 15,000 BTC for $1.1 billion to cut debt, while Genius Group fully exited its position. Riot has also been offloading bitcoin as it shifts focus toward AI and high-performance computing infrastructure.

Even firms still committed to bitcoin are trimming reserves. Empery Digital sold part of its holdings to repay loans, while Nakamoto Holdings liquidated a smaller portion to support operations. Meanwhile, Bhutan has been reducing its state-backed bitcoin reserves after previously accumulating through mining.

Despite the sell-off, public companies still collectively hold about 1.16 million BTC, over 5% of the total supply.

This post Cathie Wood Calls Bitcoin’s 50% Crash a “Victory” as Market Tests New Floor first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts Toward AI Infrastructure

Riot Platforms sold 3,778 bitcoin in the first quarter of 2026, generating $289.5 million and marking a shift in strategy as the miner redirects capital toward infrastructure and high-performance computing.

The volume sold exceeded the company’s quarterly production of 1,473 BTC by roughly 2.6 times, signaling a drawdown of treasury holdings rather than routine profit-taking. Riot ended the quarter with 15,680 BTC, down 18% from 18,005 BTC at the close of 2025.

The selling appears to have extended beyond the reporting period. Blockchain analytics firm Arkham Intelligence flagged a 500 BTC outflow from a wallet linked to Riot following the end of the quarter, suggesting continued liquidation activity.

The imbalance between production and sales comes as Riot accelerates its expansion into artificial intelligence and high-performance computing colocation. The company has begun repositioning its business model away from sole reliance on bitcoin mining, seeking to monetize its energy assets and data center footprint through long-term infrastructure contracts.

In January, Riot sold 1,080 BTC to fund the purchase of 200 acres at its Rockdale, Texas site. It also entered a ten-year agreement with Advanced Micro Devices to provide 25 megawatts of capacity, with an option to scale to 200 MW. The deal is expected to generate about $311 million in contract revenue over its initial term.

Operational metrics complicate a distress narrative. Riot reduced its all-in power cost to 3.0 cents per kilowatt hour, a 21% decline from the prior year, while increasing deployed hash rate by 26% to 42.5 exahashes per second. Average operating hash rate rose 23% to 36.4 EH/s, reflecting continued investment in mining capacity.

The company also generated $21 million in power credits during the quarter, more than double the year-ago period, through participation in grid services and energy programs.

Bitcoin HODLers like RIOT are selling

Industry conditions remain a factor. Rising energy costs tied to geopolitical tensions have pressured margins across the mining sector, prompting several operators to liquidate holdings. MARA Holdings, Genius Group, and Nakamoto Holdings collectively sold more than 15,000 BTC in recent days, reflecting a broader shift in capital allocation.

Riot’s Q1 activity underscores a turning point for the sector, where bitcoin reserves are deployed as funding sources for diversification rather than held as long-term balance sheet assets.

The trend extends beyond corporate treasuries. Bhutan has continued to reduce its BTC holdings, selling a total of 3,103 BTC. A single transaction on March 30 accounted for 375 BTC, according to Glassnode data.

The country had built its position through state-backed mining operations, reaching more than 13,000 BTC at its peak in October 2024.

Despite the recent selling, public companies still hold about 1.16 million BTC, or more than 5% of bitcoin’s fixed supply of 21 million, according to BitcoinTreasuries.net.

This post Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts Toward AI Infrastructure first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

The Bitcoin Treasury Model With a Built-In Valuation Floor

There is a version of the Bitcoin treasury conversation that has become almost routine at this point. Bitcoin is hard money. Fiat debases. Companies that hold Bitcoin on their balance sheet are making a rational long-term decision. All of this is true, and none of it is the interesting question anymore.

The interesting question is structural. Not should a company hold Bitcoin, but what kind of company should hold it, and what that choice implies for how the company performs across a full market cycle, not just a favorable one.

Three models have emerged. Each reflects a different level of conviction, a different capital structure, and a different set of tradeoffs.

- The pure-play. A company whose primary purpose is accumulating Bitcoin through capital raises, financial engineering, etc, with no core operating business. Lean structure, singular mission.

- The digital credit issuer. The most sophisticated expression of the pure-play thesis. These companies issue Bitcoin-backed financial instruments, preferred stock, convertible notes, and similar products, to fund continued accumulation. At scale, this creates a compounding accumulation engine that simpler models cannot match.

- The operating company with a Bitcoin treasury. A business with real revenue, real clients, and operational activity, which holds Bitcoin as a long-term reserve asset in deliberate strategic relationship with the business itself.

All three are legitimate expressions of the Bitcoin treasury thesis. They are not optimized for the same objectives, and the differences matter more than most treasury conversations acknowledge.

What pure-play gets right

The pure-play case deserves genuine treatment because its strongest version has real force.

Financial engineering pure-plays are capital-efficient in a specific and important sense: every dollar raised goes directly to Bitcoin accumulation with no operational drag. The mission is singular and the structure reflects it. For investors, this creates clarity. Allocators know exactly what they are underwriting, direct Bitcoin exposure at the corporate level, and the investment thesis is legible and short.

The digital credit model extends this further. Companies that have successfully issued preferred instruments and Bitcoin-backed products have built accumulation engines that operating businesses cannot match on a per-dollar-raised basis. The compounding effect of a sophisticated capital structure, at scale, is genuinely powerful. It represents the fullest expression of the Bitcoin treasury thesis, and the destination it points toward is one every operator in this space should understand.

The prerequisite problem and what it means in practice

The digital credit model has a prerequisite that is rarely stated plainly: it requires scale, institutional credibility, and market infrastructure that most companies building a Bitcoin treasury today do not yet have. It is a destination, not a starting point.

The path there runs through an intermediate period where the financial engineering structure carries more exposure than is often acknowledged. During that period:

- There is no operating revenue to fall back on

- The ability to raise capital tracks closely with Bitcoin market sentiment

- Strategic options narrow when conditions are not favorable

- The company’s cost structure depends entirely on capital markets remaining open

This is not a criticism of the model. It is a description of the journey. The question for executives is what structure best serves the company while that journey is underway.

What the operating company model actually provides

The operating company with a Bitcoin treasury does not accumulate Bitcoin faster than a well-run pure-play. At meaningful treasury scale, operating cash flow is not moving the needle on accumulation. The advantage is different, and worth stating precisely.

An operating business generates revenue independently of where Bitcoin is trading. That revenue covers fixed costs, which means the company is not dependent on capital markets remaining open to fund its basic operations. It can continue hiring, serving clients, and accumulating at a measured pace without being forced into capital decisions driven by timing rather than conviction.

The compounding effect works like this:

- Operating revenue covers costs and preserves the Bitcoin position through the cycle rather than drawing it down under pressure

- A preserved balance sheet improves the terms on future capital raises, lower dilution, better access to facilities, stronger negotiating position with partners

- Operational credibility widens the available capital base by providing an investment thesis that reaches allocators who cannot underwrite pure Bitcoin exposure within their current mandates

None of these mechanisms make Bitcoin accumulate faster in favorable conditions. Together, they make the company more durable across the full range of conditions it will face.

The built-in valuation floor

Most Bitcoin treasury company valuations are driven by a single number: mNAV, the premium the market assigns to Bitcoin held at the corporate level. When sentiment is strong and capital is flowing into the space, that premium expands. When the narrative cools, it compresses. The valuation moves with the market’s appetite for Bitcoin exposure, not with anything the company is doing operationally.

The operating company model introduces a second component that behaves differently. A profitable operating business carries an earnings multiple underwritten by revenue, client relationships, and operational track record. It does not expand dramatically when Bitcoin is performing. But it does not compress when sentiment turns either. It is stable in a way that mNAV alone is not.

These two components, Bitcoin NAV and an earnings multiple on the operating business, do not move together. That is the point. When mNAV compresses, the earnings multiple holds. The company retains a defensible valuation floor that a pure-play structure, with a single-component valuation entirely dependent on sentiment, does not have.

In practice this matters in three specific ways:

- Capital raises. A company with a defensible valuation floor can raise capital on reasonable terms even when Bitcoin sentiment is cold. A pure-play with a compressed mNAV and no earnings component has less room to maneuver.

- Talent. Equity compensation tied to a two-component valuation is a more legible and stable proposition for prospective hires than equity tied entirely to Bitcoin’s market sentiment.

- Allocator access. Many institutional allocators cannot underwrite a valuation built entirely on mNAV within their current mandates. The earnings component creates a bridge, opening the door to capital that would otherwise be unable to participate regardless of conviction.

The floor is not just a comfort during difficult conditions. It is a structural advantage that compounds over time, widening the capital base, strengthening the talent proposition, and maintaining strategic momentum across the full cycle.

How to think about the decision

These three models serve different objectives. The right framework starts with honest answers to a few questions:

- What does the existing business look like? A company with established revenue and clients already has the foundation for the operating company model. A company without it is choosing between building that foundation and committing to a pure-play path.

- What is the realistic path to scale? The digital credit model is the most powerful expression of the thesis but requires scale and credibility that takes time to build. The operating company model does not depend on reaching that threshold to function well.

- What does the investor base look like? Pure-play structures appeal most clearly to allocators who want direct Bitcoin exposure. Operating companies reach a broader set of capital partners, including those whose mandates require an operating business to participate.

- What kind of company do you want to be running across a full cycle? This is the question underneath all the others. The answer should drive the structure, not the other way around.

Conclusion

The companies that define the next era of corporate Bitcoin adoption will not all look the same. Digital credit issuers will operate at the frontier of Bitcoin-native capital markets. Financial engineering pure-plays will build toward that destination with focused conviction. Operating companies will build businesses where the treasury and core operations strengthen each other across the cycle.

Each model is a genuine expression of the thesis. The goal of this framework is to make the differences legible, so executives can choose the structure that fits what they are actually building, with clear eyes about what each model asks of them in return.

The question was never which model holds the most Bitcoin. It was always which model fits what you are trying to build.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

This post The Bitcoin Treasury Model With a Built-In Valuation Floor first appeared on Bitcoin Magazine and is written by Nick Ward.

Bitcoin Magazine

![]()

How Real Is The Quantum Threat?

A new panel has officially been announced to take place at Bitcoin 2026 titled “How Real Is The Quantum Threat?” The conversation will bring together five voices at the center of one of the most actively debated technical questions in Bitcoin today, and the lineup reflects the full range of perspectives the topic demands.

The panel features:

Hunter Beast, a senior protocol engineer for the Anduro sidechain platform incubated by MARA, is the co-author of BIP 360, a proposal that establishes a new Bitcoin wallet address type designed to protect the network from quantum computing threats. BIP 360 was merged into the Bitcoin Core BIP repository in February 2026 and was deployed on the Bitcoin Quantum Testnet v0.3.0 in March, marking significant advancements towards upgrading Bitcoin.

James O’Beirne has been a Bitcoin Core contributor since 2015 and leads multiple projects including OP_VAULT (BIP-345) and assumeutxo, having previously worked at Chaincode Labs.

Brandon Black is a Bitcoin software engineer who has spoken publicly on why quantum computing timelines are often misunderstood by the broader market.

Charles Edwards of Capriole has argued that quantum computing is advancing faster than anticipated and has advocated for a 2026 BIP-360 implementation.

Alex Thorn, head of research at Galaxy Digital, has taken a more measured position arguing the quantum threat to Bitcoin is real but limited today, affecting only certain exposed wallets, and that developers are actively building pathways to address it over time.

The panel will cover one of the most actively discussed technical topics in Bitcoin today — how quantum computing is developing, where Bitcoin’s cryptography stands, and what the path to long-term protocol resilience looks like. Developers are already working on multiple solutions, including quantum-resistant addresses and phased upgrade proposals, and this panel brings together some of the brightest minds working on these upgrades. It takes place April 29 on the Nakamoto Stage at Bitcoin 2026, The Venetian Resort, Las Vegas.

— The Bitcoin Conference (@TheBitcoinConf) March 31, 2026

PANEL ANNOUNCEMENT: "HOW REAL IS THE QUANTUM THREAT?"

This conversation will explore the state of quantum technology, the resilience of Bitcoin’s cryptography, and potential paths to safeguard the protocol in the long term.

APRIL 29 • NAKAMOTO STAGE • BE THEREpic.twitter.com/Vdpm2IlSSh

Bitcoin 2026 is Returning to Las Vegas

Bitcoin 2026 will take place April 27–29 at The Venetian, Las Vegas, and is expected to be the biggest Bitcoin event of the year.

Focused on the future of money, Bitcoin 2026 will bring together Bitcoin builders, investors, miners, policymakers, technologists, and newcomers from around the world. The event will feature a wide range of pass types, including general admission passes designed specifically for those new to Bitcoin, alongside premium passes for professionals, enterprises, and institutions.

With multiple stages, immersive experiences, technical workshops, and headline keynotes, Bitcoin 2026 is designed to serve both first-time attendees and long-time Bitcoiners shaping the next era of global adoption.

Past Bitcoin Conferences in the U.S.

Bitcoin’s flagship conference has scaled dramatically over the past five years:

- 2021 – Miami: 11,000 attendees

- 2022 – Miami: 26,000 attendees

- 2023 – Miami: 15,000 attendees

- 2024 – Nashville: 22,000 attendees

- 2025 – Las Vegas: 35,000 attendees

Get Your Bitcoin 2026 Pass

Get Your Bitcoin 2026 Pass

Bitcoin Magazine readers can save 10% on Bitcoin 2026 tickets using code ‘ARTICLE10‘ at checkout.

Stay at The official hotel of Bitcoin 2026, The Venetian, and get a guaranteed low rate plus 15% off your pass. Be in the middle of where the fun is all happening, and where the networking never ends.

And don’t forget:

Volunteer at Bitcoin 2026 and get Pro Pass access plus exclusive perks.

All students ages 13+ can apply for a Student Pass and get free general admission access to Bitcoin 2026.

Location: The Venetian, Las Vegas

Location: The Venetian, Las Vegas Dates: April 27–29, 2026

Dates: April 27–29, 2026

For more information and exclusive offers, visit the Bitcoin Conference on X here.

Why Attend Bitcoin 2026?

Bitcoin 2026 is the definitive gathering for anyone serious about the future of money. With 500+ speakers, multiple world-class stages, and programming spanning Bitcoin fundamentals, open-source development, enterprise adoption, mining, energy, AI, policy, and culture, the conference brings every corner of the Bitcoin ecosystem together under one roof.

From headline keynotes on the Nakamoto Stage to deep technical sessions for builders, institutional strategy discussions for enterprises, and beginner-friendly Bitcoin 101 education, Bitcoin 2026 is designed for everyone—from first-time attendees to the leaders shaping Bitcoin’s global adoption.

Whether you’re looking to learn, build, invest, network, or influence, Bitcoin 2026 is where Bitcoin’s next chapter is written.

Bitcoin 2026 Pass Types: Something for Everyone

Bitcoin 2026 offers a range of pass options designed to meet the needs of newcomers, professionals, enterprises, and high-net-worth Bitcoiners alike.

Bitcoin 2026 General Admission Pass

Ideal for newcomers and those looking to experience the heart of the conference.

- Limited access on Days 2 & 3

- Entry to Main Stage

- Access to Genesis Stage

- Full access to the Expo Hall

Bitcoin 2026 Pro Pass

Designed for professionals, operators, and serious Bitcoin participants.

Includes all General Admission features, plus:

- Full 3-day access, including Pro Day

- Entry to the Pro Pass Reception

- Access to Enterprise Hall, Enterprise Stage, and Networking Lounge

- Conference App networking features

- Access to the Bitcoin For Corporations Symposium

- Entry to Compute Village and Energy Stage

- Complimentary lunch, coffee, tea, and snacks

- Dedicated registration and check-in

- Reserved seating at Main Stage

- Huge savings when you bundle your hotel and Pro Pass

Bitcoin 2026 Whale Pass

Bitcoin 2026 Whale Pass

The all-inclusive, premium Bitcoin 2026 experience.

Includes all Pro Pass features, plus:

- Reserved seating at Main Stage

- All-inclusive gourmet food and beverages

- Entry to Whale Night and Whale Reception

- Access to all official after-parties

- Networking app access to connect with other Whales

- Premium access to The Deep — an exclusive networking lounge with intimate speaker sessions

- Complimentary stay at The Venetian when you bundle your whale pass and hotel (use promo code ‘WHALEHOTEL’ here)

This is the most immersive way to experience Bitcoin 2026.

Bitcoin 2026 After Hours Pass

Bitcoin 2026 After Hours Pass

Your ticket to the night.

Most deals are done with a drink in your hand. Get exclusive access to 3 official Bitcoin 2026 after-parties across Las Vegas — each with a 2-hour open bar — where the real conversations happen and the best connections are made.

- Access to 3 official Bitcoin 2026 after-parties

- 2-hour open bar at each event

- Evening events across Las Vegas, April 27–29

- Network with Bitcoiners, builders, and industry leaders after hours

More headline speaker announcements are coming soon.

Don’t miss Bitcoin 2026.

This post How Real Is The Quantum Threat? first appeared on Bitcoin Magazine and is written by Jenna Montgomery.

Bitcoin Magazine

MARA Conducts Ongoing Layoffs Following $1.1B Bitcoin Sale and Debt Reduction Push

Bitcoin miner MARA Holdings has begun a series of company-wide layoffs affecting multiple departments, according to reporting from Blockspace Media, marking the latest shift in the firm’s broader restructuring strategy.

Sources familiar with the matter said the layoffs have been “ongoing” and executed in a piecemeal fashion, with at least two rounds taking place this week on Wednesday and Thursday. The total number of employees impacted — as well as the percentage of the workforce affected — has not been disclosed, and the company has not publicly commented on the cuts.

The workforce reduction comes just days after MARA completed a major balance sheet restructuring that involved selling 15,133 bitcoin for approximately $1.1 billion between March 4 and March 25. The proceeds were used to repurchase portions of its outstanding 0.00% convertible senior notes due in 2030 and 2031, allowing the company to retire debt at an average discount of roughly 9% to par.

In total, MARA repurchased $367.5 million of its 2030 notes for $322.9 million and $633.4 million of its 2031 notes for $589.9 million. The transactions are expected to generate approximately $88.1 million in cash savings and reduce the company’s total convertible debt by about 30%, from roughly $3.3 billion to $2.3 billion.

Following the repurchases, MARA now has $632.5 million in 2030 notes and $291.6 million in 2031 notes remaining outstanding. Other tranches of convertible debt — including $48.1 million due in 2026, $300 million due in 2031, and $1.025 billion due in 2032 — remain unchanged.

CEO Fred Thiel previously framed the bitcoin sale as part of a deliberate capital allocation strategy aimed at strengthening the company’s balance sheet while preserving long-term shareholder value. He said the move would improve financial flexibility and position the firm for expansion beyond traditional bitcoin mining.

Bitcoin miners are pivoting to AI

That expansion includes a growing focus on artificial intelligence and high-performance computing (HPC), areas where MARA is seeking to leverage its expertise in energy infrastructure and data center operations. The company has increasingly positioned itself as a digital energy and compute provider, rather than a pure-play bitcoin miner.

As part of this shift, MARA has also signaled that selling bitcoin could become a recurring element of its treasury strategy. The company stated it plans to sell BTC “from time to time” throughout 2026 to support liquidity needs and fund corporate initiatives.

The developments come amid a challenging environment for bitcoin miners, who are navigating tighter margins, rising competition, and increasing pressure to diversify revenue streams beyond block rewards.

For MARA, the combination of debt reduction, bitcoin sales, and workforce cuts signals a company in transition — prioritizing balance sheet strength and strategic repositioning as it moves deeper into AI and energy infrastructure.

This post MARA Conducts Ongoing Layoffs Following $1.1B Bitcoin Sale and Debt Reduction Push first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

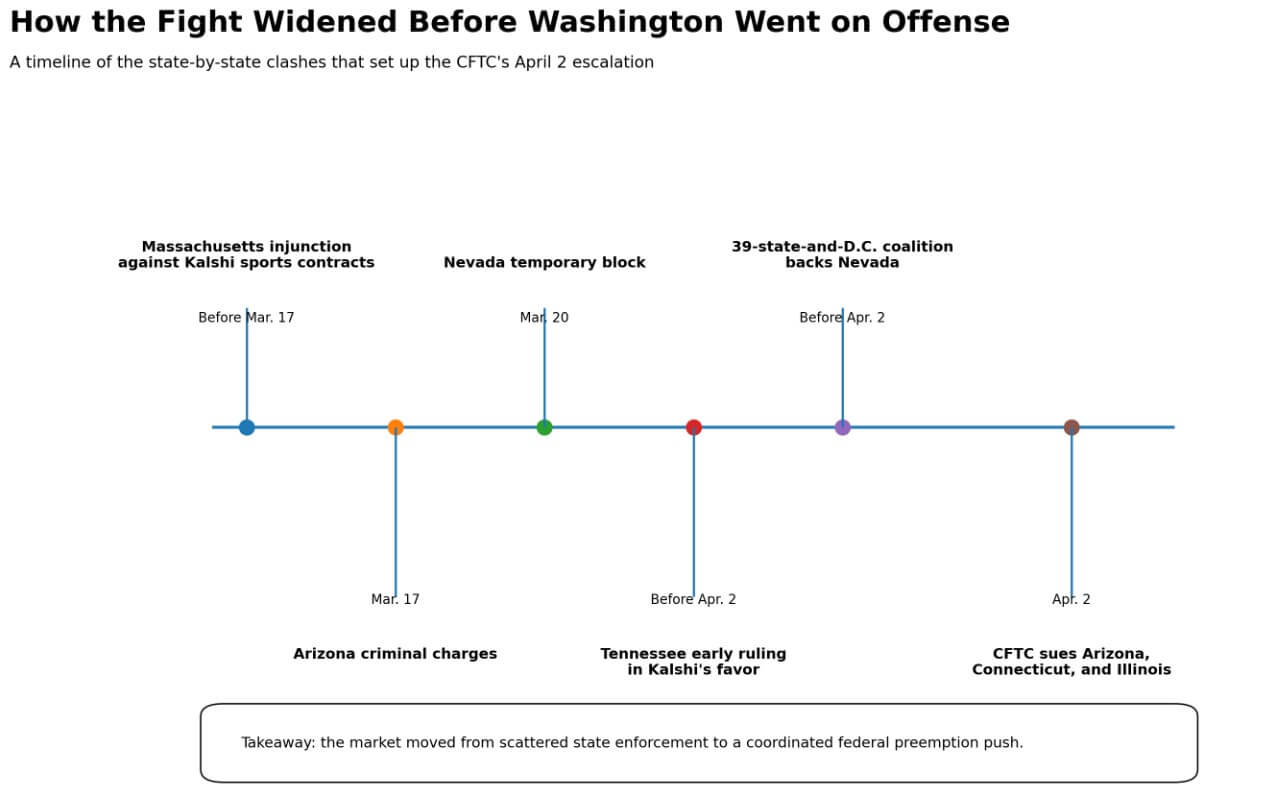

Washington has escalated its fight with states over prediction markets, launching lawsuits that could decide whether these platforms operate as national financial products or state-regulated gambling. The outcome will determine if sports contracts can scale or get forced back into local licensing regimes.

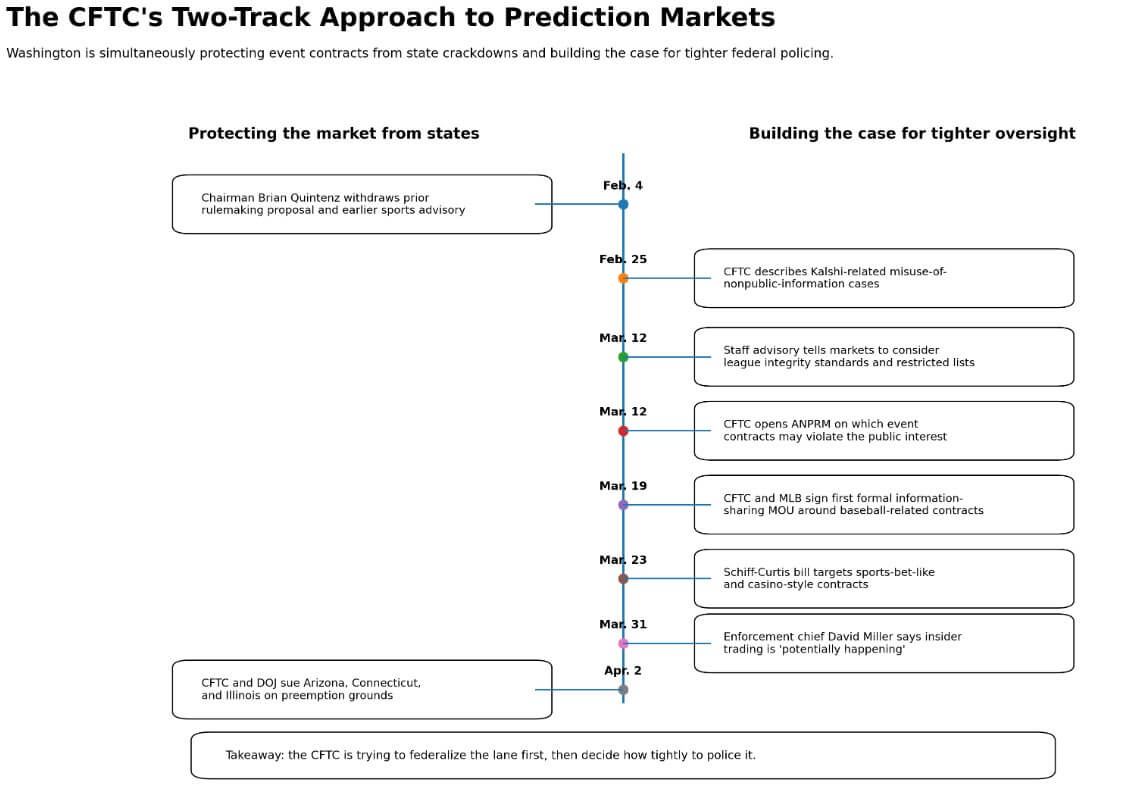

On Apr. 2, the Commodity Futures Trading Commission (CFTC) sued Arizona, Connecticut, and Illinois, with the Department of Justice as a litigation partner.

The regulator demanded expedited rulings that federal derivatives law preempts state efforts to classify event contracts as illegal gambling.

Washington moved to the offensive, trying to establish, as a matter of national market structure, that these products belong under exclusive federal jurisdiction.

Why this matters: This is no longer a niche regulatory dispute. The CFTC is asking courts to confirm that once an event contract is listed on a federally regulated exchange, states lose the ability to shut it down as gambling. If that argument holds, prediction markets become a national product category. If it fails, operators face a fragmented system where their most valuable contracts, especially sports, must comply with dozens of state regimes.

The CFTC's published FAQ makes the ambition explicit. The suits are registrant-agnostic, deliberately detached from any individual company's fact pattern so that courts can rule on the preemptive scope of the Commodity Exchange Act itself.

Washington wants category-wide declarations on CEA preemption, binding regardless of which operator or exchange triggers enforcement.

The CEA's exclusive jurisdiction provision is the lever.

The CFTC's theory holds that once an event contract is listed on a CFTC-regulated exchange, states cannot relabel it as unlawful gambling without destabilizing the uniform national derivatives framework, potentially opening the door for states to assert authority over other exchange-traded derivatives that have operated without controversy for decades.

That framing becomes sharper against the legal map heading into April.

Massachusetts had secured an injunction against Kalshi's sports contracts, and Nevada won a temporary block on Mar. 20. Arizona escalated to criminal charges on Mar. 17. Tennessee produced an early ruling in Kalshi's favor. A 39-state-and-DC coalition filed amicus briefs backing Nevada.

The prediction market category was surviving on patchwork, while the CFTC played defense from the sidelines.

Sports as the fault line

Sports contracts are where the category stops looking like abstract forecasting and starts colliding with the full compliance architecture states built since the Supreme Court's 2018 Murphy decision. The structure consists of licensing, age verification, KYC and AML protocols, self-exclusion databases, suspicious-wager reporting, and integrity monitoring.

Illinois told the CFTC that these platforms entirely bypass its licensing, responsible-gaming, AML, and tax regimes. Connecticut pointed to under-21 access that no licensed operator could legally offer.

The American Gaming Association translated those gaps into fiscal terms, claiming that sports bets on prediction markets have cost states more than $620 million in lost gaming taxes since the start of 2025.

The advocacy estimate converts legal theory into budget politics at a moment when the US sports betting revenue, which reached $1.61 billion in January 2026 alone, shows a market with year-over-year handle declines and incumbents with clear motivation to fight back.

| Regulatory feature | State-licensed sportsbook | Prediction market sports contract | Why states care |

|---|---|---|---|

| Licensing | Must hold a state sports-betting license | Operates under CFTC exchange framework rather than state gaming license | States argue this bypasses the licensing gate they use to control market access |

| Minimum age | Usually restricted to 21+ | Connecticut argued these contracts allowed under-21 participation | Creates a direct conflict with state consumer-protection rules |

| KYC / AML controls | Built into state gaming compliance regime | Illinois argued prediction markets bypass its KYC and AML regime | States see this as a gap in anti-fraud and anti-money-laundering oversight |

| Responsible-gaming rules | Required by state law and regulation | Illinois said these platforms bypass responsible-gaming requirements | States view this as a loss of problem-gambling safeguards |

| Self-exclusion tools | Standard feature in licensed betting markets | Not clearly embedded in the same state-run structure | Weakens the player-protection system states built after sports-betting legalization |

| Suspicious-wager reporting | Expected within sportsbook integrity frameworks | Not described in the article as operating under equivalent state rules | States and leagues worry about manipulation and detection gaps |

| Integrity monitoring | Conducted through state, operator, and league coordination | NBA and MLB argued the oversight framework is not comparable to licensed sportsbooks | Sports contracts are where market integrity concerns become hardest to ignore |

| League information-sharing | Common in regulated sportsbook ecosystems | CFTC only recently created a formal channel via its Mar. 19 MLB MOU | Shows the federal framework is still building tools states already expect |

| Taxes / fees | Operators pay state taxes and licensing fees | AGA says sports bets on prediction markets have cost states more than $620 million in lost gaming taxes since the start of 2025 | Turns the dispute from legal theory into a state-budget fight |

The leagues arrived as actors with a concrete grievance and a clear agenda.

The NBA said sports prediction markets were expanding into single-game contracts through self-certification, without anything resembling the oversight framework states require of licensed sportsbooks.

MLB pressed the same argument directly with the CFTC. On Mar. 19, the agency signed a memorandum of understanding with the league, establishing the first formal agency-league information-sharing channel around baseball-related contracts.

That MOU is both a practical integrity measure and an acknowledgment that the current framework carries a meaningful gap that the litigation leaves open.

The regulator's internal contradiction

The CFTC is simultaneously trying to lock states out of the lane and build the public record that the lane requires far tighter policing.

On Feb. 4, Chairman Brian Quintenz withdrew a prior event-contract rulemaking proposal and an earlier sports advisory, framing the move as a permissive opening for the category. Within weeks, the agency moved in the opposite direction on nearly every other front.

On Feb. 25, the CFTC publicly described two Kalshi-related misuse-of-nonpublic-information cases, imposed penalties and multi-year suspensions, and stated that insider trading, wash trading, fraud, and manipulation rules fully apply to prediction markets.

On Mar. 31, enforcement chief David Miller said insider trading is “potentially happening” in these markets, citing injury-related and person-specific contracts as obvious integrity risks.

On Mar. 12, a staff advisory directed designated contract markets to consider league integrity standards, restricted-participant lists, and cooperation with league investigations. On the same day, the agency opened an advance notice of proposed rulemaking seeking input on which event-contract types may run contrary to the public interest.

Congress arrived in the same space on Mar. 23, when Senators Adam Schiff and John Curtis introduced the Prediction Markets Are Gambling Act, targeting contracts that resemble sports bets or casino-style games on CFTC-registered platforms.

The fight now runs in three venues at once: state courts, federal courts, and the Senate.

In the bull case, Washington's suits in Illinois and Connecticut produce fast rulings endorsing the preemption theory, and a federal circuit affirms that the CEA displaces state gambling law for exchange-listed event contracts.

States lose the tools to block platform expansion, and the Schiff-Curtis bill stalls. Prediction market operators build sports offerings under a federal compliance wrapper consisting of league MOUs, restricted-participant lists, and whatever tighter rulebook emerges from the CFTC's ANPRM process.

The category survives in sports as a regulated national market with a heavier obligation stack than operators currently carry. Developer incentives skew toward exchanges already holding CFTC registration rather than new entrants, compressing the number of platforms that can realistically compete.

In the bear case, state-favorable reasoning from Nevada and Massachusetts spreads at the appellate level.

Courts find that Murphy-era state sports-betting frameworks constitute the kind of traditional police power that federal preemption cannot readily displace.

Congress advances a carveout that pushes platforms listing sports contracts into state licensing processes. Political, macro, and business-event contracts, categories without a natural state-regulatory home, clear the bar more easily, while sports-adjacent contracts migrate toward the same licensing, tax, and integrity regime as conventional sportsbooks.

Operators who built their growth story around sports face a product retreat or a compliance restructuring that they did not price into their models.

The federal bet

Washington is wagering that “listed on a CFTC-regulated exchange” is the decisive jurisdictional fact that overrides states' classifications of the underlying contract.

The courts' acceptance of that wager will determine if prediction markets become a genuinely national product category or a nationally marketed product that still has to negotiate dozens of licensing regimes for its most commercially valuable contracts.

The CFTC's own calendar compresses the timeline, as the ANPRM closes Apr. 30.

The agency expects expedited resolution in Connecticut and Illinois within a few months, and a preliminary injunction ruling in Arizona is due within weeks.

By mid-2026, federal preemption power over event contracts will have a legal foundation or a legal ceiling.

The post CFTC sues 3 states in bid to redefine crypto prediction markets as federal products appeared first on CryptoSlate.

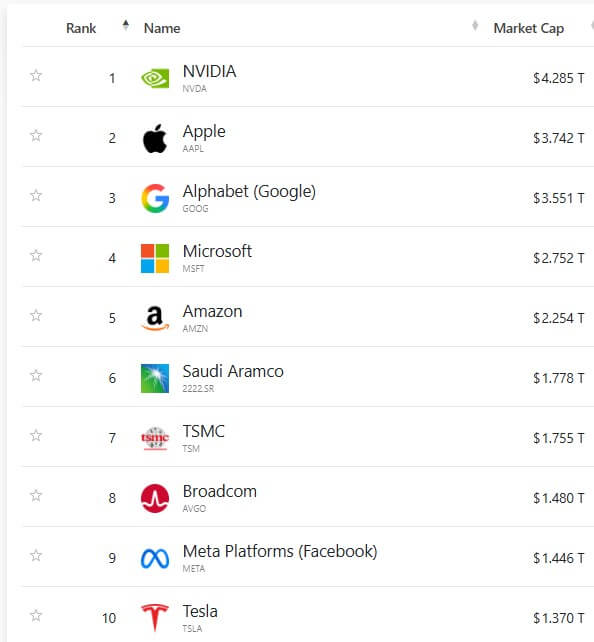

SpaceX is moving toward a public listing that could redefine how Bitcoin shows up in equity markets. The scale of the IPO matters more than the size of its holdings.

SpaceX has reportedly filed confidentially for an initial public offering with the US Securities and Exchange Commission (SEC), a step that would move Elon Musk’s rocket and satellite company closer to what could become the largest stock market debut in US history.

According to reports, the firm is looking to raise as much as $75 billion at a valuation of about $2 trillion, with a listing as early as June. This would put it more than three times above the largest US IPO to date.

At that level, the IPO would also make the company one of the top 10 global companies by market capitalization.

Why this matters: This would mark a shift in how Bitcoin enters public markets. Until now, exposure has largely come through companies built around holding the asset. A SpaceX listing would introduce Bitcoin into one of the world’s largest industrial and infrastructure businesses, changing the context in which investors encounter it.

Launched in 2022, SpaceX sits at the intersection of commercial space, communications, defense, and infrastructure.

Over the past years, the firm has grown to become the dominant force in commercial launches, NASA’s leading launch partner, and the operator of Starlink, the satellite broadband network that has become central to its broader valuation.

That would give investors exposure to a business with far broader foundations than most recent market debuts.

The most valuable public company with Bitcoin

Apart from the size of the deal, a SpaceX listing could create the most valuable listed company with Bitcoin on its balance sheet.

Data from BitcoinTreasuries.com show the company is holding 8,285 Bitcoin, valued at $569.5 million on its balance sheet. The firm is currently the fourth-largest private corporate holder of BTC.

If SpaceX’s public filings confirm these holdings, the firm would overtake another Musk-led company, Tesla, on that measure. Tesla currently holds more than 11,000 Bitcoin and remains the highest-value public company known to own the token. The automaker is currently valued at $1.37 trillion.

With a planned valuation of $2 trillion, SpaceX would move past Tesla in market value even while holding fewer coins.

Over the past year, the market has seen an avalanche of public firms introducing Bitcoin to their balance sheet. This is a model popularized by Michael Saylor's Strategy, which is currently the largest public corporate Bitcoin holder with 762,099 Bitcoin.

However, SpaceX's stock would not trade like that of Strategy or other Bitcoin holding companies.

Strategy’s equity model is built around Bitcoin accumulation, capital raising, and the token’s price. SpaceX would come public as a launch, satellite, and defense business that happens to own Bitcoin.

The numbers make that clear. SpaceX’s reported Bitcoin stash is worth roughly $569.5 million, which translates to less than 0.03% of its $2 trillion valuation.

Such a valuation is too low to make the stock a Bitcoin proxy. However, it is large enough to become part of the company’s public identity.

Would retail investors gain from the IPO?

The answer is likely yes, but mostly because of what SpaceX is, not because of the Bitcoin on its balance sheet.

Reports indicate that retail investors would get meaningful exposure to the IPO, with allocations of up to 30% of shares and potentially without the standard six-month lock-up.

If that structure holds, it would give ordinary investors access to one of the world’s most sought-after private companies on unusually favorable terms for a deal of this size.

That retail angle would help demand, and the Bitcoin connection would add another layer of interest, particularly among crypto investors who already follow Musk, Tesla, and treasury-holding companies closely.

But the core draw would be elsewhere. Investors would be buying into the dominant launch franchise in commercial space, the Starlink network, and a company whose position reaches into defense and communications.

The stock would appeal because of its scale, strategic relevance, and scarcity value, not because 8,285 Bitcoin sit somewhere on the balance sheet.

The post SpaceX IPO would eclipse Tesla in market value while holding less Bitcoin — challenging the idea of a Bitcoin proxy appeared first on CryptoSlate.

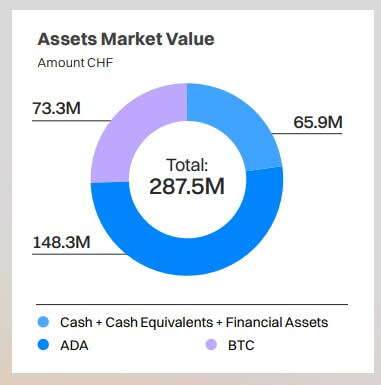

The Cardano Foundation is becoming less dependent on ADA. Its latest report shows Bitcoin and cash now account for a much larger share of reserves after a year of sharp price divergence.

That shift changes how closely the Foundation’s balance sheet tracks the performance of Cardano’s native token.

In its 2025 Activity and Financial Insights Report shared with CryptoSlate, the Foundation said its total assets stood at 287.5 million Swiss francs, or about $361 million. This represents a 45% decline from the $659.1 million assets it held as of the end of 2024.

The drop in headline value reflected a difficult year for Cardano’s native token, ADA, but the more notable shift came in the composition of the Foundation’s holdings.

Why this matters: The Foundation has historically been one of the largest long-term holders of ADA, so changes to its treasury structure affect the degree of internal alignment between Cardano’s ecosystem and its core institution. A lower ADA concentration reduces direct exposure to the token’s price but also weakens the feedback loop linking the Foundation’s balance sheet to ADA’s performance.

A year earlier, the Foundation said 76.7% of its assets were held in ADA, 14.9% in Bitcoin, and 8.3% in cash, cash equivalents, and financial assets.

However, by the end of 2025, ADA’s share had fallen to about 51.6%, while BTC rose to 25.5%, and cash, cash equivalents, and financial assets climbed to 22.9%.

On that basis, the Foundation’s holdings worked out to roughly $186 million in ADA, $92 million in Bitcoin, and $83 million in cash and financial assets.

This essentially means that the Cardano-focused organization's asset was no longer as concentrated in ADA as it had been a year earlier. Now, nearly half of the balance sheet was tied to Bitcoin, cash, and other financial assets.

How Bitcoin gained a foothold in Cardano's Foundation assets

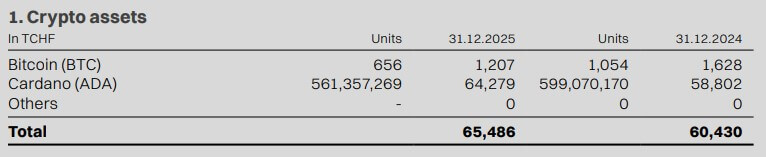

Bitcoin’s greater role in the portfolio did not stem from an increase in the Foundation’s BTC holdings.

In fact, the report showed that the Foundation significantly reduced its BTC holdings last year, down 37% to 656 BTC from 1,054 BTC a year earlier.

That means BTC's increased share of the treasury was driven by relative performance and a broader reshaping of reserves, rather than by an outright accumulation of more BTC.

Market moves help explain the change. Data from CryptoSlate showed that ADA has fallen by roughly 63% over the past year, while Bitcoin has shown more resilience, declining by around 25%.

That divergence meant BTC did not need to rise in absolute terms to claim a larger place in the Foundation’s holdings. Instead, the top crypto's greater resilience during the bear market helped it gain a stronger footing.

Meanwhile, the report also suggests the treasury was becoming more layered, with the Foundation finding more use cases for BTC and also expanding its cash holdings.

The Foundation said part of its Bitcoin allocation was invested in loans and collective investment schemes during 2025.

At the same time, its financial assets, including loans to third parties, investments, and shares, rose to 43.9 million Swiss francs (around $54.9 million) from 14.3 million Swiss francs (equivalent to $17.8 million) a year earlier.

Additionally, the organization's cash and cash equivalents stood at 20.1 million Swiss francs, or $25.1 million.

Taken together, those figures show a reserve base moving beyond a straightforward ADA-and-bitcoin treasury into something more diversified and more actively managed.

Spending priorities shift

The change in portfolio mix was matched by a clearer reset in how the Foundation spent money in 2025.

The report said 23.6 million Swiss francs (equivalent to $29.5 million) was allocated across three strategic pillars, including technology, adoption, and governance.

Technology accounted for the largest share at 40.3%, or 9.5 million francs. Adoption followed at 39.6%, or 9.3 million francs, while governance spending represented 20.1%, or 4.8 million francs.

That marked a change from 2024, when the foundation grouped its work under adoption, operational resilience, and education. The new structure gives a sharper picture of where resources are now being directed and how the Foundation sees Cardano’s next phase.

Technology spending centered on protocol enablement, developer tooling, node diversity, interoperability frameworks, oracle infrastructure, and operational resilience.

The Foundation said it also increased its focus on community initiatives to improve liquidity and adoption in decentralized finance. At the same time, it expanded its Web3 adoption team with an emphasis on integrations, listings, and real-world asset efforts.

A significant part of the technology and adoption story was tied to digital identity. In 2025, the foundation launched Veridian, a privacy-preserving identity platform designed to let organizations issue and verify digital credentials anchored on Cardano.

Meanwhile, adoption spending covered enterprise solutions, identity and traceability systems, regulatory collaboration, education, and ecosystem partnerships.

The report said the foundation made Originate available as an open-source traceability solution, advanced the Reeve platform through internal use and its first enterprise proof of concept, and pushed Veridian into wider deployment, including a white-label rollout for the United Nations Development Program and the launch of the Veridian Wallet.

The Cardano Academy also expanded through new courses, distribution partnerships, and multilingual deployment. The Foundation said course material was extended to Binance Academy, which it said reaches more than 44 million learners, while collaborations also included the Blockchain Research Institute and Coursera.

Lastly, governance took a smaller share of the budget than technology and adoption, but it remained central to the Foundation’s 2025 agenda as Cardano deepened its commitment to decentralized decision-making.

The report highlighted support for the largest on-chain budget submitted so far on Cardano, resulting in 38 separate treasury withdrawal governance actions. It also pointed to the Foundation’s enterprise membership in Intersect and its work across committees tied to civics, budget, technical matters, product, open-source enablement, marketing, and oversight.

That participation fed into a series of initiatives, including work on the constitutional process, the Cardano 2030 vision and strategy, the Cardano Summit 2025 proposal, and the Cardano 2026 budget process.

The Foundation also said it supported tools aimed at widening participation in governance, including the open-source Cardano Voting Tool, a Proposal Examiner built with Griffin AI, updated governance documentation, and dedicated sessions at Cardano Summit 2025.

The foundation’s DRep Delegation Program distributed 140 million ADA to seven builder DReps, with a further 220 million ADA allocation to adoption and operational DReps announced. It also published the Constitutional Committee’s cold keys and expanded internal frameworks for delegation and elections as the governance transition continued.

2026 will test whether the reset works

The next question is whether the Foundation’s repositioning can translate into a stronger operating story for Cardano itself.

Frederik Gregaard, the Foundation's chief executive, said the organization's focus in 2026 would remain on technology, governance, and enterprise and institutional adoption.

He said the group would continue working to strengthen Cardano’s role in real-world asset infrastructure, support the expansion of stablecoin markets and DeFi liquidity, and build the open-source tooling needed for broader adoption.

Notably, this aligns with the blockchain network's recent efforts to integrate the Pyth network, LayerZero, and Circle's USDCx stablecoin. All of these efforts are geared towards expanding Cardano's DeFi ecosystem and stablecoin supply to attract institutional support.

That leaves Cardano facing a clearer test in 2026 to determine if a more diversified balance sheet, combined with heavier spending on infrastructure, governance, and adoption, can help stabilize the economics around ADA itself.

The post Cardano Foundation shifts away from ADA as Bitcoin and cash take larger share of reserves appeared first on CryptoSlate.

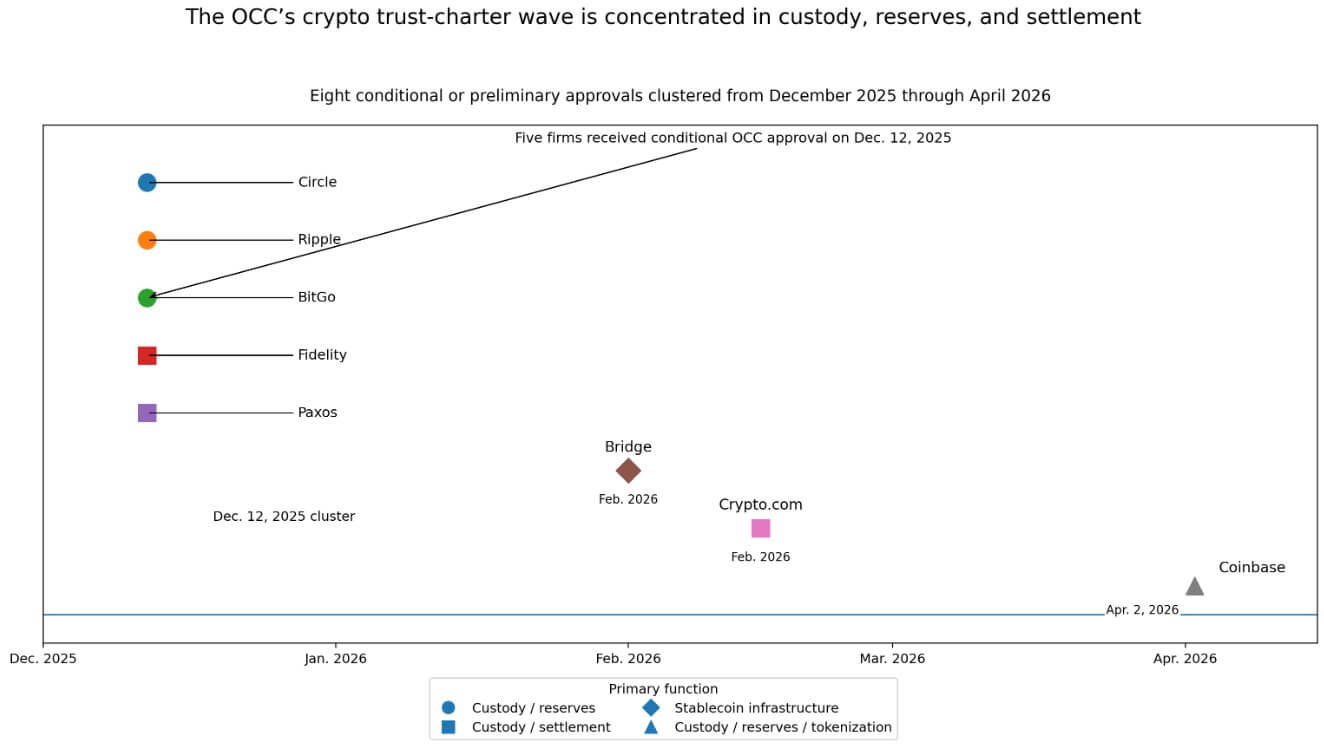

On Apr. 2, Coinbase received conditional approval from the Office of the Comptroller of the Currency for a national trust charter.

Coinbase joined a cluster of at least eight firms that the OCC has moved toward federal trust-charter status since December 2025, and the cluster reveals a deliberate federal decision about which parts of crypto belong inside the supervised system.

Why this matters: The US is shifting from regulating crypto to selecting which parts of the stack sit inside the banking perimeter. That decision defines who can scale nationally, who captures institutional flows, and who remains outside the system.

The OCC conditionally approved Circle, Ripple, BitGo, Fidelity, and Paxos on Dec. 12, 2025. Bridge followed in February, Crypto.com in February, and Coinbase in April.

Eight approvals in roughly four months, all clustered around custody, reserve management, stablecoin infrastructure, and settlement. That density reframes the Coinbase headline as a data point in a federal design decision.

A national trust charter gives firms federal reach under a single OCC supervisor, allowing them to operate across all 50 states without having to assemble a patchwork of state approvals.

National trust banks hold client assets and facilitate settlement under a fiduciary mandate, operating within a purpose-built custody-and-settlement structure. The lane's practical value lies in scope and supervisory clarity: firms can hold client assets and handle settlement functions under a single federal framework.

Paxos explicitly framed its national trust push as a move beyond its New York state trust structure, and that framing reveals an architectural logic.

The functions Washington is comfortable supervising

The approvals cluster around custody, reserves, and settlement because that is where the OCC's comfort level currently sits.

Reports noted that Crypto.com's charter would cover client asset management and trade settlement, keeping the firm within custody and settlement functions. Bridge's approval covered stablecoin issuance and orchestration, as well as reserve management.

The OCC's Circle decision described digital-asset custody and reserve-management services tied to its fiduciary activities. Coinbase said full approval could support tokenized securities and stablecoins.

Washington is drawing a perimeter around the functions tokenized finance needs most, such as asset custody, stablecoin reserve backing, and settlement infrastructure, and extending supervisory authority over firms that provide them.

The firms best positioned in this environment are custodians, reserve managers, and stablecoin infrastructure operators.

Adjacent regulatory moves reinforce that reading. In March 2026, US bank regulators said tokenized securities would not face additional capital charges purely for being tokenized, calling the framework technology-neutral.

The SEC allowed intraday trading of tokenized shares of the WisdomTree money-market fund, approved Nasdaq's tokenized trading proposal, and cleared NYSE's tokenized securities partnership with Securitize.

The OCC charter wave and the tokenization rule stack are moving in tandem, with institutional infrastructure as the common thread.

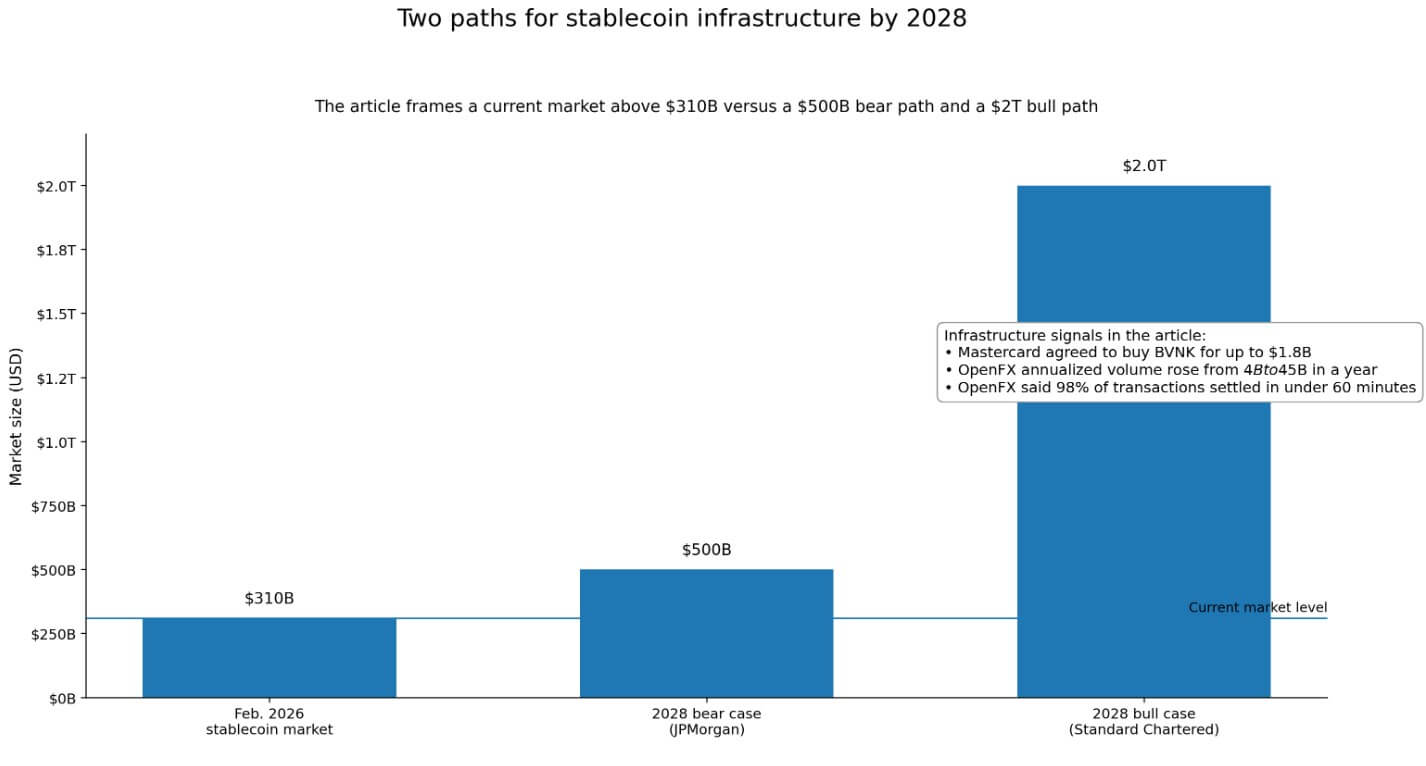

VISUAL 2

The re-intermediation arc

Crypto's original commercial promise was removing the regulated intermediaries that traditional finance required.

The practical outcome of the OCC cluster is re-intermediation: the most commercially durable crypto firms are now competing to become a new class of regulated intermediaries. Tokenized finance needs custodians, reserve managers, and settlement rails before it needs another trading venue with more listed assets.

Capital is already pricing that reality. Mastercard agreed to buy BVNK, a stablecoin infrastructure firm, for up to $1.8 billion. OpenFX raised $94 million and reported annualized payment volume climbing from $4 billion to $45 billion in a year, with over 98% of transactions settling in under 60 minutes.

The global stablecoin market stood at over $310 billion in February 2026. These are backend-plumbing bets, concentrated in custody, settlement, and reserve management.

The competitive map is also narrowing. Anchorage is currently the only digital asset company operating under a full national trust bank charter. The December cluster and subsequent approvals are conditional or preliminary.

Getting to the final operating status requires demonstrating capital adequacy, governance, and operational controls to OCC examiners. This bar will compress the field toward well-capitalized incumbents with existing compliance infrastructure.

Two paths forward

In the bull case, the OCC finalizes its stablecoin implementation in terms that institutions can operationalize.

Tokenized securities pilots on Nasdaq and NYSE move from proof-of-concept to live settlement infrastructure, while firms like Mastercard accelerate the adoption of stablecoin rails across global payment corridors.

If stablecoins approach Standard Chartered's $2 trillion forecast by 2028 and tokenized real-world assets reach comparable scale, federally supervised crypto utilities become the scarce picks-and-shovels of digital finance.

The OCC's chartered custodians and reserve managers collect margin on trillions of dollars in assets that flow through the infrastructure they control.

In the bear case, final approvals move slowly as bank trade groups press their “lighter-touch charter” objection, and the OCC responds by tightening conditions on reserve buffers, liquidity stress tests, and operational controls.

The stablecoin market tracks closer to JPMorgan's $500 billion by 2028 forecast, a ceiling anchored by the fact that payments account for only about 6% of current stablecoin demand, roughly $15 billion of the $310 billion outstanding.

In that world, state trust structures and bank partnerships stay practical, and the federal lane becomes a premium niche.

The federal bet

Washington is sorting crypto's functions into those it wants to supervise and those it does not, or at least not yet.

The charter cluster, the stablecoin reserve rules under the GENIUS Act, and the technology-neutral treatment of tokenized securities together form a regulated stack for crypto-native financial infrastructure.

The power the OCC is extending is real. Still, it carries supervisory costs: monthly public reserve disclosures for stablecoin issuers, weekly confidential reporting under the proposed implementation rule, and full OCC examination authority.

| Comparison point | OCC national trust charter | State trust / state-licensed structure | Bank-partnership model |

|---|---|---|---|

| Primary supervisor | OCC | State regulators | Partner bank’s federal/state bank supervisor plus partner compliance requirements |

| Geographic reach | National, under a single federal framework across all 50 states | More limited; state-based and potentially patchwork | Depends on partner bank structure rather than firm’s own charter |

| Core functions highlighted in article | Custody, reserve management, stablecoin infrastructure, settlement, potential support for tokenized securities | Similar functions can be done, but without the same single federal lane | Practical way to access banking, payments, and settlement functions without own federal charter |

| Strategic value | Supervisory clarity and national scale | Flexibility, but less unified than federal lane | Faster/practical access for firms that do not want or cannot obtain a charter |

| Supervisory burden | High | Lower than OCC lane, based on article’s contrast | Shared/mediated through bank partner requirements |

| Stablecoin disclosure burden | Monthly public reserve disclosures; weekly confidential reporting under proposed implementation rule | Not described in article at the same level | Not described in article at the same level |

| Examination authority | Full OCC examination authority | State examination authority | Bank partner oversight and exam environment, not direct OCC trust-bank status for the crypto firm |

| Firms best positioned | Well-capitalized incumbents with strong governance, capital adequacy, and operational controls | Firms comfortable staying in state-licensed layer | Firms using partnerships as a practical alternative to federal chartering |

| Competitive implication | Could become scarce “picks-and-shovels” infrastructure if tokenized finance scales | Remains viable if federal approvals stay slow or narrow | Remains viable in bear/slower-adoption scenario |

| Main tradeoff | National reach and legitimacy, but heavier compliance and supervisory costs | Less supervisory intensity, but less federal uniformity | Less direct control over infrastructure stack, but easier access route |

| Best fit in article’s framing | Firms aiming to be federally supervised crypto utilities | Firms that stay outside the federal lane | Firms choosing a practical alternative while the federal lane remains selective |

The firms that clear that bar will operate nationally under a single federal supervisor, hold institutional assets, and process tokenized settlements in a framework that traditional finance counterparties can use.

Those who cannot or choose not to will stay in the state-licensed layer, and the charter wave is starting to sort itself out.

The post Washington has started selecting which crypto firms control custody at a national level appeared first on CryptoSlate.

Bitcoin becomes the live market over Easter as oil shocks hit and traditional finance goes dark

The Bitcoin market now has three trading days where it will act as the live venue for geopolitical risk while much of traditional finance is closed.

As of Friday, April 3, Wall Street is closed for Good Friday; several other markets are shut or thinner than normal; and the macro backdrop has become harder, rather than easier, to price.

Iran launched missiles and drones at Israel and the Gulf states. Fires were reported at Kuwait’s Mina al-Ahmadi refinery. The Strait of Hormuz remains the central transmission line through which geopolitical risk is moving into oil, inflation expectations, and broader macro sensitivity.

At the same time, WTI surged 11.4% to $111.54, and Brent rose 7.8% to $109.03 in the latest repricing move.

Bitcoin, by contrast, remains open and is still clearing over $33 billion in volume over the last 24 hours.

It is trading around $67,150 after an intraday range of roughly $65,780 to $67,373.

Availability has become part of the market structure

Throughout 2026, Bitcoin has functioned less like a thesis trade and more like a weekend stress monitor.

So what happens when the world gets a fresh geopolitical shock, oil gaps higher, and many of the usual venues for price discovery are closed for a long weekend?

Put simply, Bitcoin’s role here comes from availability rather than ideology.

When cash equities are closed, parts of the commodities complex are offline, and broader liquidity is fragmented by a holiday calendar, Bitcoin becomes one of the few major liquid assets still offering continuous two-way pricing.

In that sense, the market is using BTC as an immediate expression of changing sentiment.

Thin conditions can amplify moves. Crypto-native positioning can distort the signal. Weekend liquidity is not weekday liquidity. But none of that erases the core point.

If the next leg of geopolitical stress lands while traditional markets are dark, Bitcoin may be the first place investors see an immediate price response rather than the last place they confirm it.

The transmission mechanism is oil, and then rates, inflation expectations, and the dollar.

Oil first, then rates, then validation

That ladder matters. First comes the direct energy shock. Then comes the inflation read-through. Then comes the policy question.

If oil remains elevated because the Strait of Hormuz stays constrained or infrastructure damage widens, the inflation impulse becomes harder to dismiss as temporary.

That can move yields. It can support the dollar. It can also remove some of the macro oxygen that speculative assets need.

Bitcoin sits inside that chain whether crypto investors want it to or not. The move in crude is the mechanism through which geopolitical stress becomes a financing and liquidity question for the wider market.

In that sense, BTC is trading the same macro regime that households, bond markets, and central banks are trying to map. No single directional verdict follows automatically for Bitcoin.

If oil keeps repricing higher and the market starts to harden again around a higher-for-longer policy, BTC will have to show it can absorb a tougher liquidity backdrop rather than merely survive a geopolitical shock.

Holiday calendars are usually treated as scheduling details. This time, they are part of the structure, with a split between assets that can update instantly and those that cannot.

In closure windows, Bitcoin serves as a temporary price-discovery layer for global stress, even if it is not the final destination for defensive capital.

That is a narrower and more defensible claim than saying BTC leads all other markets.

Monday’s reopening can always revise the message.

Equity futures can reopen in a different register. Oil can extend or retrace. Bond desks can reset the macro interpretation. But the availability premium still carries weight.

An open market has the first chance to express fear, relief, or confusion. This weekend, Bitcoin plays a more prominent role in that function than ever before. Even after multiple weekends of Bitcoin absorbing geopolitical developments.

The macro complication is that the geopolitical picture is landing into scheduled economic risk rather than replacing it.

The U.S. March jobs report is due Friday morning, with economists looking for a modest rebound after February’s weather- and strike-distorted weakness.

ADP showed 62,000 private-sector jobs added in March, which is not hot enough to settle the policy debate but not weak enough to clear it either.

Fabian Dori, CIO at Sygnum Bank, told CryptoSlate,

“With US equity markets closed for Good Friday, price discovery indications will be delegated to on-chain markets such as Hyperliquid, or be deferred in traditional markets until Sunday night futures and Monday’s open.

This means traditional markets will need to digest any significant miss or beat simultaneously with the weekend's geopolitical developments tied to the ongoing conflict in Iran.”

That leaves Bitcoin trading into a layered setup.

First, there is a live war risk. Second, there is a live oil shock. Third, there is an incoming labor print that could still affect how quickly the market relaxes on rates.

That is what makes the current weekend different from a routine risk-off spell.

What Bitcoin is showing now, and what still needs confirmation

Bitcoin around $67,000 is a dangerous level for such a potentially volatile long weekend.

BTC has already absorbed a material oil repricing move, a worsening geopolitical backdrop, and the closure of major traditional venues without losing continuous market function.

Bitcoin is acting as an open circuit for macro stress at a moment when other circuits are partially unavailable.

Being an open circuit does not make BTC a safe haven, a superior hedging tool, or predictive in any strong causal sense.

It does mean the asset is temporarily serving a role that goes beyond the usual crypto narrative. It is one of the few major markets still speaking.

The clear way to assess Bitcoin over Easter is through three layers: availability, transmission, and validation.

| Layer | What it shows now | Why it matters |

|---|---|---|

| Availability | Bitcoin is still trading while many traditional markets are closed or thinner than normal | It becomes an immediate venue for price expression |

| Transmission | War risk is moving through oil and Hormuz, not through fear alone | That links BTC to inflation, yields, and liquidity conditions |

| Validation | Monday’s reopening and the post-jobs cross-asset reaction will test whether Bitcoin’s market signal was durable | The first move has value, but acceptance carries more weight |

The framework is historical first and causal second.

It organizes the next 48 to 72 hours without pretending Bitcoin has become an oracle for all global assets.

First comes the live signal. Then comes the cross-asset confirmation. Then comes the question of whether the move will be accepted once the full market returns.

Bitcoin will likely trade reactively to developments around Iran, Hormuz, and oil, while investors treat the market action as an early signal rather than a settled verdict.

If there is de-escalation or at least stabilization from some relief around Gulf infrastructure, fewer signs of direct spillover, and an oil market that stops repricing upward in an orderly fashion, then Bitcoin’s resilience through the closure window could be constructive rather than fragile.

However, if the conflict expands further, refinery damage worsens, or the NATO call on opening the Strait of Hormuz by force goes badly, the market may spend the weekend repricing in light of a more durable inflation shock.

In that environment, Bitcoin faces the harder test. It would have to trade through a rising oil regime and a tightening macro backdrop simultaneously.

That leaves the next test unchanged. The first move will have value, but acceptance on Monday carries more weight.

If Bitcoin continues to absorb the Easter weekend stress while oil, war risk, and the jobs narrative stay unresolved, the market will use BTC price as a barometer for Monday's open. However, anything that happens this weekend could easily be reversed and repriced within moments of Monday's pre-market open.

Until then, the market is left trading signals without confirmation, more of a placeholder than a conclusion.

The question is whether Bitcoin is delivering something real, or just leaving a trail of clues for others to interpret, like an Easter bunny that may or may not have actually passed through.

The post Bitcoin is the financial Easter Bunny this weekend as markets close Friday amid critical jobs report appeared first on CryptoSlate.

Cryptoticker

The first quarter of 2026 has concluded, leaving the cryptocurrency market in a state of significant reassessment. After a bullish end to 2025, the start of the year brought a harsh "risk-off" reality. Major assets, led by Bitcoin (BTC) and Ethereum (ETH), saw substantial drawdowns as investors grappled with a perfect storm of geopolitical conflict, surging energy costs, and a hawkish shift in global monetary policy.

Why did Crypto Crash in 2026?

If you are looking for the primary reason for the crash: Q1 2026 was defined by a liquidity drain. As Bitcoin fell 23%, capital fled volatile assets in favor of traditional safe havens. While the broader market bled, specific utility-driven tokens like Tron (TRX) and UNUS SED LEO (LEO) managed to defy the trend, posting gains of 10% and 4.6% respectively.

Q1 2026 Market Performance Overview

The following table summarizes the Year-to-Date (YTD) performance of the top cryptocurrencies as of the end of March 2026:

| Cryptocurrency | Q1 2026 Performance (YTD) |

|---|---|

| Bitcoin ($BTC) | -23% |

| Ethereum ($ETH) | -30% |

| Solana ($SOL) | -36% |

| Binance Coin ($BNB) | -32% |

| XRP ($XRP) | -28% |

| Dogecoin ($DOGE) | -22% |

| Tron ($TRX) | +10% |

| UNUS SED LEO ($LEO) | +4.6% |

The Macroeconomic "Pressure Cooker"

To understand the Q1 crash, one must look at the "Macroeconomic Pressure Cooker." This refers to the simultaneous rise in inflation expectations and interest rates. In early 2026, the US Federal Reserve signaled that interest rates would remain "higher for longer" to combat a sticky 2.7% inflation rate. This strengthened the US Dollar, making riskier assets like Ethereum less attractive to institutional desks.

Crypto Crash Reasons

The downturn was accelerated by significant global events:

- Geopolitical Conflict: Escalating tensions in the Middle East—specifically involving Iran—reignited fears of a broader war. This uncertainty historically triggers a flight to quality.

- Oil Prices: Crude oil prices surged in Q1, with Brent crude hitting over $118/bbl. High energy prices act as a tax on the global economy and increase the operational costs for Bitcoin miners, often leading to "miner capitulation" sell-offs.

- The Gold & Silver Hedge: Unlike crypto, Gold posted steady gains of roughly 8% earlier in the quarter, reaching near-record levels as investors sought a store of value that doesn't rely on digital network uptime or speculative sentiment.

Why Altcoins Suffered More

While Bitcoin’s 23% drop was painful, Solana (SOL) and BNB were hit harder, losing 36% and 32% respectively. This is a classic "beta" move; altcoins typically amplify Bitcoin's movements. When liquidity dries up, speculative "high-growth" ecosystems are the first to see capital outflows. Investors moved their holdings from high-risk dApp platforms into stablecoins or exited the market entirely.

The Outliers — Tron and LEO

Why did Tron (+10%) and UNUS SED LEO (+4.6%) survive the carnage?

- Tron (TRX): Tron has solidified itself as the "Global Settlement Layer" for USDT. During a crash, the demand for stablecoin transfers spikes. As users move to safety, the burning of TRX for transaction fees increases, creating deflationary price pressure that supported the TRX price.

- UNUS SED LEO (LEO): As a utility token for the Bitfinex ecosystem, LEO benefits from a consistent buy-back and burn mechanism. In periods of high volatility, exchange-based tokens often act as a "defensive" play, as trading volumes (and thus burn rates) remain elevated.

Institutional Sentiment and ETF Outflows

The latest crypto news highlights that Bitcoin ETFs saw their first sustained period of net outflows in Q1 2026. Institutional investors, who were the primary drivers of the 2025 rally, shifted their focus to the S&P 500 and banking stocks, which showed more resilience during the "war-inflation" scare.

Crypto Markets Are Moving — But Something Is Missing

Over the past 24 hours, the crypto market has reacted to a wave of major geopolitical and macroeconomic developments. Rising tensions, escalating military actions, and a sharp surge in oil prices have already introduced volatility across Bitcoin and altcoins.

Yet despite all this, the overall market remains relatively stable.

Bitcoin is holding near the $66,000–$67,000 range, Ethereum is hovering around $2,000, and total crypto market capitalization remains largely flat.

👉 At first glance, this may seem like resilience.

👉 In reality, it signals something else: the market has not fully reacted yet.

Why the Real Move Hasn’t Started

The most important factor right now is simple:

👉 Wall Street is closed.

Due to the Good Friday holiday, U.S. stock markets are not trading. This means:

- Institutional investors are inactive

- ETFs are paused

- Large capital flows are temporarily frozen

At the same time, major developments are unfolding:

- Escalation in U.S.–Iran tensions

- Announcements targeting critical infrastructure

- Oil prices surging above key levels

- Gold behaving unexpectedly under pressure

👉 These events are happening without full market participation.

As a result, crypto is currently trading in a partial-information environment, where only retail and limited global flows are active.

Monday Is the Real Catalyst

👉 The U.S. market will reopen on Monday at 9:30 AM ET (3:30 PM Central European Time).

This moment could act as a major reset point for global markets.

Why?

Because all the news that broke during the market closure will be priced in simultaneously:

- Equity markets will react

- Oil markets will continue adjusting

- Institutional portfolios will rebalance

- Risk exposure will be reassessed

👉 In short: Monday is when the real repricing begins.

Why the Pressure Is Building

Markets are currently sitting in a fragile equilibrium.

On one side:

- Bullish crypto fundamentals (institutional adoption, regulatory progress)

- Bitcoin holding key levels

On the other:

- Rising oil prices tightening global liquidity

- Escalating geopolitical risk

- Uncertainty around further military actions

👉 This creates a compression phase — where price stays relatively stable while pressure builds underneath.

When markets reopen, that pressure is likely to release quickly.

How Big Could the Move Be?

Bearish Scenario (Higher Probability Short-Term)

If macro pressure dominates:

- Bitcoin could break below $66K, targeting $64K or lower

- Ethereum may lose the $2,000 level

- Altcoins could see sharper declines

👉 This would likely happen if:

- Oil continues rising

- War headlines intensify

- Equity markets open significantly lower

Bullish Scenario (Lower Probability but Possible)

If markets interpret the situation as contained:

- Bitcoin could push toward $68K–$70K

- Short squeezes could accelerate upside

- Risk appetite may temporarily return

👉 This would require:

- De-escalation signals

- Oil price stabilization or drop

- Strong dip-buying from institutions

Most Likely Outcome: Volatility First

Regardless of direction, one thing is highly likely:

👉 Volatility will expand sharply.

Expect:

- Fast moves in both directions