Cryptocurrency Posts

Crypto Briefing

Jordan's call for activating the Arab defense treaty may escalate regional military alliances, complicating US-Iran peace efforts.

The post Jordan calls for arab defense treaty activation amid US-Iran tensions appeared first on Crypto Briefing.

Trump's speech exacerbates geopolitical tensions, undermining short-term diplomatic efforts and impacting market confidence in conflict resolution.

The post Trump’s speech signals ongoing conflict, dims ceasefire chances appeared first on Crypto Briefing.

Polymarket leverages Pyth's oracle for precise pricing in prediction markets, enhancing asset trading with verified data integration.

The post Polymarket taps Pyth to power stock, commodity, and index prediction markets appeared first on Crypto Briefing.

Crypto markets face volatility due to heavy short positions and long-term holder selling, despite oil price changes easing inflation concerns.

The post Oil reversal and crowded shorts keep crypto traders on edge appeared first on Crypto Briefing.

Circle's inaction during the Drift Protocol attack raises concerns about centralized stablecoin reliability and regulatory oversight effectiveness.

The post Circle took no action during Drift Protocol attack, says investigator appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Coinbase Receives Conditional OCC Approval to Form National Trust Company

Coinbase has received conditional approval from the Office of the Comptroller of the Currency to establish Coinbase National Trust Company, according to a statement from the company.

The approval marks a regulatory milestone for Coinbase as it expands its federally supervised custody and market infrastructure operations.

The company emphasized that the approval does not authorize it to operate as a commercial bank. Coinbase stated it will not take retail deposits or engage in fractional reserve banking. Instead, the charter is intended to provide federal oversight for its custody business, which the firm says has been a core part of its operations for years.

Under the conditional approval framework, Coinbase will be required to meet specified regulatory conditions before the charter becomes fully operational. The company said it intends to use the structure to bring uniform federal standards to its digital asset custody services and related institutional infrastructure.

Coinbase framed the decision as validation of its long-standing approach of working within the U.S. regulatory system. The company said it has invested heavily in compliance and engagement with regulators and views the approval as part of a broader evolution in how digital asset firms interface with federal banking supervision.

The charter is expected to provide clearer regulatory consistency across jurisdictions, particularly for institutional custody services. Coinbase said it believes the structure could support future expansion into additional financial services, including payments-related products, while remaining within the bounds of trust company oversight.

OCC is adopting pro-crypto activities

Over the past year, federal banking regulators have taken a more active role in defining the perimeter of digital asset activities within the traditional financial system. The Office of the Comptroller of the Currency has issued updated guidance on how banks may engage with cryptocurrency custody, stablecoin-related services, and blockchain infrastructure, while continuing to evaluate applications from crypto-native firms seeking trust or banking charters.

Industry participants have pursued federal charters in part to reduce reliance on a patchwork of state licensing regimes and to gain clearer access to national banking rails. Trust bank structures, in particular, have become a focal point for firms seeking to offer custody services without engaging in lending or deposit-taking activities.

The OCC has adapted to institutional interest in regulated custody models and the growing overlap between traditional financial infrastructure and digital asset firms. Exchanges, custodians, and fintech firms have got federal oversight and support for institutional adoption and reduce regulatory uncertainty.

At the same time, policymakers have debated how far federal banking regulators should extend oversight into crypto-native business models, particularly as stablecoins and tokenized assets continue to integrate into payments and settlement systems.

The conditional approval for Coinbase’s trust charter reflects this broader regulatory shift toward structured supervision rather than ad hoc enforcement.

If finalized, Coinbase’s national trust status would place it among a small number of crypto-linked firms operating under direct federal trust oversight, signaling continued convergence between digital asset infrastructure and the U.S. regulated banking system.

This post Coinbase Receives Conditional OCC Approval to Form National Trust Company first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Wall Street Firms and Crypto Companies to Review New Market Structure Proposal in Private Sessions

Crypto and banking industry representatives are set to review a revised stablecoin yield proposal crafted by Senators Thom Tillis and Angela Alsobrooks this week, as lawmakers attempt to break a months-long lobbying standoff over how — or whether — stablecoin issuers should be allowed to offer yield.

According to reporting from Politico, a small group of crypto firms and Wall Street institutions will privately review the updated legislative text over the next two days, with crypto companies expected to see the language as early as Thursday and banks on Friday.

The process remains tightly controlled, with stakeholders permitted to view the draft only in restricted settings and barred from taking copies.

The revised proposal follows a series of staff-level negotiations between industry groups and Senate offices aimed at narrowing disagreements over stablecoin yield provisions. While some participants hope the latest draft will serve as a near-final compromise, it remains unclear whether either side will accept the terms as currently written.

Clarity Act and crypto talks are ongoing

The renewed review of a stablecoin yield proposal comes amid a broader effort in Congress to resolve one of the most contested issues in U.S. crypto regulation: whether stablecoin issuers should be permitted to offer yield-bearing products.

Stablecoins — digital tokens typically pegged to the U.S. dollar and backed by cash and short-term securities — have become a core settlement layer in crypto markets, but their regulatory status remains unsettled, particularly around interest and yield.

The fight over a U.S. crypto market-structure bill stems from a broader effort to build on 2025’s landmark stablecoin legislation, the GENIUS Act, which established a federal framework for stablecoins — requiring full backing, transparency and reserve disclosures for digital dollars.

That law was widely seen in the crypto industry as a breakthrough for regulatory clarity while attempting to align digital assets with traditional financial standards.

After the GENIUS Act’s passage, the Senate turned its attention to more expansive digital asset oversight through what’s often referred to as the CLARITY Act or the crypto market-structure bill.

This legislation aims to define how U.S. regulators would police and oversee trading platforms, tokens, custody services and other infrastructure — essentially the backbone of a regulated digital asset ecosystem.

However, negotiations bogged down over one central issue: whether regulated exchanges should be allowed to offer yield-bearing rewards on stablecoin holdings.

Banks and major financial institutions argue that these rewards resemble unregulated deposit-like products that could siphon funds away from FDIC-insured accounts, potentially threatening lending and financial stability.

Crypto firms — including major issuers like Circle and Coinbase — counter that such incentives are crucial for competitive markets and for user adoption of digital money.

The current tentative deal being negotiated between senators and the White House seeks a middle ground — potentially allowing activity-based rewards while restricting passive yield — in hopes of unlocking Senate committee action by April. Whether that compromise holds both bank and crypto support will be decisive for the future of U.S. digital asset regulation.

This post Wall Street Firms and Crypto Companies to Review New Market Structure Proposal in Private Sessions first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

LNVPN Rebrands to Nadanada.me as Privacy Infrastructure Expands with Anonymous eSIMs and Lightning Payments

Offering anonymous eSIM data plans in over 200 countries, disposable and rental phone numbers for SMS verification, WireGuard VPN access and anonymous AI chat tools, LNVPN has outgrown its original brand. The company has grown into a full-spectrum privacy infrastructure service.

The company started in 2022 as LNVPN. It began as a proof-of-concept Lightning Network VPN built for the Oslo Freedom Forum after Alex Gladstein asked the team to create a Lightning-enabled VPN for activists in oppressive regimes. The original focus was short-term VPN access paid with Lightning, allowing users to buy service by the hour or day instead of monthly subscriptions.

The service grew quickly. Users liked the flexibility of short-term access without accounts or contracts. In 2023 the company won a price in the 2023 bolt.fun hackathon and added SMS verification services. Users pay a Lightning invoice for a disposable phone number and receive a one-time confirmation code. The system uses HODL invoices so that if the code does not arrive the payment is refunded automatically.

The company later introduced eSIM data plans available in more than 200 countries. Customers buy fixed data bundles that can activate anonymously. Rental phone numbers followed last November. These let users rent a unique phone number for three, six or nine months to receive unlimited SMS messages without creating an account. At present the rental numbers are available only in the United Kingdom, with United States numbers planned for May. The team also launched anonymous AI chat services that require no sign-up or login and are free to use.

The name nadanada.me comes from the Spanish phrase for “nothing at all.” As the company stated, “What do we know about our users? Nada. What do we log? Nada. The name is the promise.”

This approach stands in contrast to traditional service providers that collect large amounts of user data, a practice that has led to repeated large-scale breaches at major corporations and government contractors.

In November 2025, analytics provider Mixpanel was hacked, exposing names, email addresses and approximate location data of some OpenAI API users. In early 2025, U.S. government contractor Conduent suffered a ransomware attack that compromised personal and health records of more than 25 million Americans. In January 2026, cryptocurrency hardware wallet maker Ledger reported that customer names and contact information were exposed through a breach at its third-party payment processor Global-e. Such incidents frequently enable identity theft, as stolen personal details like names, emails, addresses and health or financial records can be used to open fraudulent accounts, file fake tax returns or impersonate victims.

Nadanada.me represents a new generation of privacy services integrated with Lightning in pay-as-you-go models that leave no trace on the financial system or the blockchain, in defense of user privacy.

This post LNVPN Rebrands to Nadanada.me as Privacy Infrastructure Expands with Anonymous eSIMs and Lightning Payments first appeared on Bitcoin Magazine and is written by Juan Galt.

Bitcoin Magazine

Bitcoin Price Continues Sliding as President Trump Signals Iran Escalation, Raising Risk of Drop Toward $60,000

Bitcoin price fell last night after President Donald Trump signaled a potential escalation in military action against Iran, triggering a broad pullback across global markets and raising questions about whether bitcoin price could test lower support levels.

The price of Bitcoin dropped nearly 4% within hours after Trump’s April 1 address, sliding to below $66,000 early April 2. The decline came as investors shifted away from risk assets following remarks that pointed to harder strikes in the coming weeks, with no timeline for de-escalation.

Equity markets also moved lower. The S&P 500 traded in negative territory, while Asia-Pacific equities reversed earlier gains. At the same time, oil prices surged, with Brent crude rising above $106 per barrel as traders priced in the possibility of prolonged disruption in the Strait of Hormuz, a key global shipping route.

The move highlights how closely Bitcoin price is tracking traditional markets during periods of geopolitical stress.

Data shows the 30-day correlation between Bitcoin price and the S&P 500 has climbed to around 0.75, indicating that institutional investors are treating the digital asset more like a high-growth technology proxy than a hedge.

Bitcoin price resilience

Bitcoin had shown some resilience in recent weeks, ending March with a modest gain and snapping a multi-month losing streak. However, it remains down roughly 45% from its prior peak above $126,000, and demand indicators suggest continued pressure.

JUST IN: Bitcoin has closed its first green month after 5 months of red

— Bitcoin Magazine (@BitcoinMagazine) April 1, 2026pic.twitter.com/jVMxXp9w2L

From a technical perspective, Bitcoin is now approaching a key support range between $64,000 and $65,000. The level has held through several recent tests, but a break below it could open the door to a move toward $60,000, near the February low, according to Bitcoin Magazine Pro data.

On the upside, resistance sits around $68,000 and $70,000. Analysts say those levels need to be reclaimed to shift sentiment and support a recovery narrative.

Until then, price action remains constrained by a pattern of lower highs that has developed since March.

Long-term holder data suggests the market may be moving through a late-stage bear cycle. Investors holding Bitcoin for six months or more now control about 80% of supply, approaching levels that have marked past market bottoms.

Even so, previous cycles indicate that extended periods of sideways trading often follow before a sustained recovery begins.

On top of this, Bitcoin treasury firms and public companies are offloading BTC as prices fall, adding fresh pressure to the market as long-term holders turn into sellers. Companies including Riot Platforms, MARA Holdings, and Genius Group have trimmed holdings this week to raise liquidity and service balance sheets.

For now, Bitcoin’s reaction to geopolitical developments underscores its current role within the broader macro environment.

As long as uncertainty around the Iran conflict persists, market direction may remain tied to shifts in risk sentiment rather than a return to the asset’s safe-haven narrative.

This post Bitcoin Price Continues Sliding as President Trump Signals Iran Escalation, Raising Risk of Drop Toward $60,000 first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Treasuries Are Cracking as Public Companies Turn into BTC Sellers

A wave of bitcoin selling from public companies and sovereign entities is adding pressure to the bitcoin market, as firms that once called themselves long-term holders sit on long-term losses and move to shore up balance sheets, repay debt, and fund strategic pivots.

Companies including Riot Platforms, Genius Group, and Nakamoto Holdings have all reduced their bitcoin holdings this week, citing liquidity needs and operational priorities.

The shift marks a drastic change from the accumulation trend that defined the past two years, when firms raced to build BTC treasuries during a period of rising prices.

Bitcoin HODL-ish

Empery Digital (EMPD) said it sold 370 BTC at an average price of $66,632, generating $24.7 million in proceeds. The company used part of the funds to repay its term loan and released about 1,800 BTC that had been held as collateral.

Following the sale, Empery holds 2,989 BTC, down from a peak position of about 4,000 BTC built after it began accumulating in July 2025. Its shares have fallen 75% from a 2025 high of $15.80.

Genius Group (GNS), an AI-focused education company that once held as much as 440 BTC, has exited its BTC position. The firm sold its remaining 84 BTC to repay $8.5 million in debt, completing a series of reductions that began earlier this year.

The company said it may rebuild its bitcoin treasury when market conditions improve.

Riot Platforms (RIOT), one of the largest publicly traded bitcoin miners in the U.S., has also been selling. Blockchain data tracked by Lookonchain indicates the company moved 500 BTC, worth about $34 million, to an exchange-linked address, suggesting a sale. This movement took place on April 1.

The transaction follows roughly $200 million in bitcoin sales in the final months of 2025, as Riot shifts capital toward artificial intelligence and high-performance computing infrastructure.

Other firms are merely tapping their holdings. Nakamoto Holdings (NAKA) sold 284 BTC for about $20 million in March, representing around 5% of its reserves.

The company said the proceeds will support working capital and operations following acquisitions tied to its bitcoin-focused strategy. Nakamoto reported a pre-tax loss of $52.2 million for 2025, driven in part by a decline in the value of its digital assets.

Marathon Digital (MARA) has taken one of the largest steps. The miner sold 15,133 BTC between March 4 and March 25 for about $1.1 billion. It used the proceeds to repurchase $1 billion in convertible notes due in 2030 and 2031, reducing outstanding debt by about 30%. The move lowered its holdings to 38,689 BTC from 53,822 BTC at the start of the year.

The trend extends beyond corporate treasuries. Bhutan has continued to reduce its BTC holdings, selling a total of 3,103 BTC. A single transaction on March 30 accounted for 375 BTC, according to Glassnode data.

The country had built its position through state-backed mining operations, reaching more than 13,000 BTC at its peak in October 2024.

Despite the recent selling, public companies still hold about 1.16 million BTC, or more than 5% of bitcoin’s fixed supply of 21 million, according to BitcoinTreasuries.net.

Bitcoin traded near $66,000 at the time of writing, down about 3% on the day.

Bitcoin Magazine is published by BTC Inc, a subsidiary of Nakamoto Inc. (NASDAQ: NAKA)

This post Bitcoin Treasuries Are Cracking as Public Companies Turn into BTC Sellers first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

A recent paper by the Bitcoin Policy Institute on Taiwan opens with a familiar argument that the country's reserves are overconcentrated in dollars. Gold underperforms its potential, and Bitcoin could complement both.

Readers who stop there miss the more consequential claim buried in the blockade-and-invasion framework on pages 5 through 7, where the paper is trying to redefine what makes a reserve asset fail.

Traditional reserve analysis judges assets on liquidity, price stability, and credit quality. The BPI paper adds a fourth test: can the asset still be moved, spent, or mobilized when shipping lanes are blocked, the host state withdraws custodial access, or another state becomes politically hostile?

By that measure, gold can be stranded, dollar reserves can become conditional, and Bitcoin can stay electronically portable regardless of physical access or diplomatic standing.

That is a larger conceptual move than advocating for a Taiwanese BTC position.

Why this matters: This marks a shift from traditional reserve thinking. Assets like Treasuries and gold can remain valuable on paper while becoming difficult or impossible to use under sanctions, conflict, or political pressure. If reserve managers begin prioritizing access over stability, Bitcoin enters the conversation not as a return play, but as a contingency asset.

From macro bet to sovereignty insurance

For years, the state-level Bitcoin argument ran on a single track: hedge monetary debasement, diversify reserves, capture upside from adoption momentum.

That argument still appears in the BPI paper, particularly in its pages on US debt accumulation and the Federal Reserve's balance sheet expansion. The more original contribution sits elsewhere, where the paper ranks reserve assets by whether they stay accessible under coercion.

A government only needs to accept that Treasuries, correspondent banking networks, physically stored metal, and foreign sovereign paper each carry distinct dependencies.

The policy question centers on which asset stays reachable when custody, transport, or host-country politics go wrong.

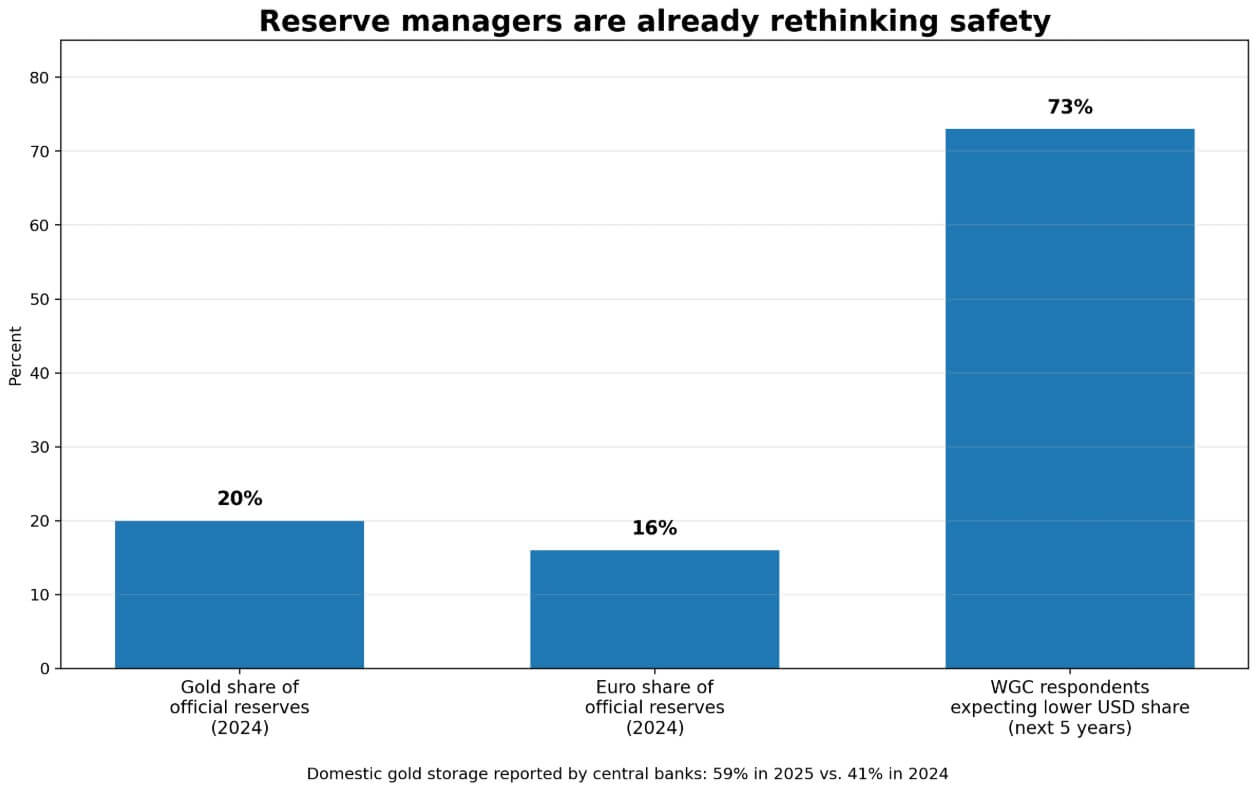

Official reserve behavior already confirms that framing extends well beyond Bitcoin advocates. The IMF reports that total international reserves, including gold, reached 12.5 trillion SDR at the end of 2024.

The ECB reported that gold's share of global official reserves reached 20% by market value in 2024, surpassing the euro's 16%, and that central banks bought more than 1,000 tonnes that year.

The World Gold Council's 2025 survey found 73% of respondents expect lower US dollar holdings in global reserves over the next five years, and the share of central banks reporting domestic gold storage jumped to 59% from 41% a year earlier.

Reserve managers are already broadening the definition of reserve risk, and the BPI paper extends that logic to Bitcoin.

| Asset | Normal-times strength | Crisis vulnerability | Failure mode under stress | Why it matters in the article |

|---|---|---|---|---|

| U.S. dollar reserves / Treasuries | Deep liquidity, high credit quality, global reserve standard | Can become politically constrained by host-country policy, sanctions, or custodial leverage | Freeze / conditional access / political pressure | Shows that a reserve can remain “safe” on paper but become less usable in practice |

| Gold | Longstanding reserve ballast, inflation hedge, widely accepted by official institutions | Hard to move quickly, physically trappable, vulnerable to seizure or transport bottlenecks | Stranding / seizure / logistics failure | Explains why portability and physical control now matter more in reserve analysis |

| Bitcoin | Digitally portable, bearer-like, can be moved without shipping lanes or physical transport | High volatility, governance burden, limited official-sector acceptability | Institutional reluctance / policy hesitation, rather than physical immobilization | Enters the story as a potential asset of last-resort accessibility rather than a conventional safe reserve |

| Diversified non-dollar sovereign paper | Reduces reliance on a single reserve issuer, still fits conventional reserve frameworks | Still depends on external sovereign systems, settlement infrastructure, and market access | External dependency / reduced neutrality | Serves as the bear-case alternative: reserve managers may prefer this over BTC even after accepting access risk |

| Domestically vaulted gold | Improves control over custody while preserving gold’s reserve role | Still suffers from transport friction and limited portability in acute crises | Mobility constraint rather than pure custody risk | Shows why gold can benefit from the same access-risk logic without fully solving it |

The live evidence for access risk

The access-risk argument draws force from concrete recent events.

In March, Russia's central bank challenged the EU freeze affecting approximately $300 billion in sovereign funds. That dispute keeps the central premise operational: reserve assets can become politically immobilized while retaining their face value.

An asset owned on paper yet frozen in practice has already failed as a reserve, regardless of its credit rating.

Brazil's central bank drew a parallel conclusion. On Mar. 31, Brazil lifted gold's share of reserves to 7.19% from 3.55% in a single year, while cutting the US dollar share to 72, citing diversification as the driver.

The BPI paper argues Bitcoin belongs in that same diversification calculus, specifically for reserve decisions driven by geopolitical logic.

The US Strategic Bitcoin Reserve adds a distinct data point. The White House order prioritizes the reserve with forfeited BTC, prohibits outright sale, and contemplates additional acquisition only on a budget-neutral basis.

That pulls Bitcoin reserve language into an actual sovereign administrative structure, setting a precedent regardless of its unconventional funding source.

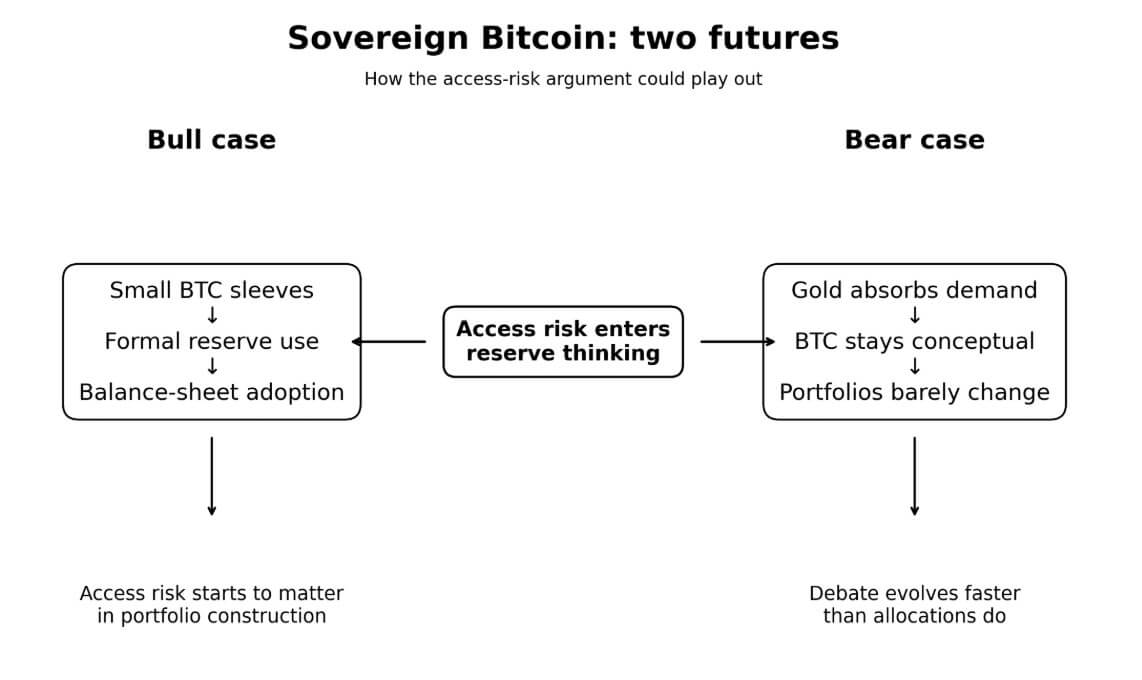

Two futures for the sovereign Bitcoin argument

Scale makes the bull case concrete. Taiwan's reserves total roughly $602 billion, and a 1% Bitcoin sleeve would be about $6 billion, while a 5% sleeve would be $30 billion.

The broader math is starker: 0.1% of global reserves, roughly $16.25 billion, would represent about 1.2% of Bitcoin's entire market cap at current prices near $68,000.

Reserve system participation, even at a marginal scale, would have price consequences well before any central bank made a headline allocation decision.

The bull case requires a handful of politically exposed or sanctions-conscious states first to formalize small BTC positions in the 0.25% to 1% range, or to treat already-held seized or mined Bitcoin as a reserve asset before buying more.

Ferranti's sanctions risk modeling supports the direction: in one sanctions scenario, his model produces an optimal Bitcoin share of around 5% for exposed sovereigns. The sovereign Bitcoin discourse would then move from advocacy papers to actual balance sheet entries.

The bear case accepts the access risk critique and still concludes that Bitcoin loses.

Reserve managers acknowledge that physical gold carries logistical dependencies and that dollar reserves carry political ones, and then decide that Bitcoin's volatility, governance burden, and near-zero official-sector acceptability make it a weaker hold than domestically vaulted gold and diversified non-dollar sovereign paper.

Gold absorbs the diversification demand that the access-risk argument was supposed to generate for BTC, and Bitcoin's role as a reserve asset stays conceptual. The debate evolves while portfolios hold their composition.

Where the argument holds and where it strains

The BPI paper is strongest when it treats portability and seizure resistance as genuine reserve characteristics, grounded in observable reserve behavior.

That framing tracks official data: geopolitics now visibly influences reserve composition, and the desire to hold assets outside concentrated single-counterparty dependency is real and already moving portfolios.

The paper overreaches when adoption momentum or price appreciation enters as evidence that the policy case is settled. Official institutions still weigh acceptability, legal clarity, and operational habit alongside access risk, and those factors carry weight that portability rankings leave unaddressed.

The most credible version of the paper's argument is its own stated position: Bitcoin as a small insurance sleeve alongside gold, optimized for access.

For most of Bitcoin's history as a reserve policy topic, the central question in official circles was whether Bitcoin was safe enough to hold. That framing consistently disadvantaged BTC because its volatility kept it below Treasuries and gold on every conventional measure.

Reserve managers are now focused on which assets stay deployable in the event of a hostile geopolitical environment. Gold's resurgence, domestic vaulting preferences, sanctions-driven reserve disputes, and payment-infrastructure fragmentation all show that reserve managers are already seeking conventional assets.

Bitcoin advocates are inserting BTC into that same conversation, and the BPI paper shows how that argument works at its most sophisticated.

The post Reserve assets face new test as sanctions risk pushes Bitcoin into policy debate appeared first on CryptoSlate.

XRP enters an identity crisis as oil, inflation fears, and dollar strength hit the market all at once

XRP has reached the hardest phase of the cycle. The asset spent much of the year carrying a cleaner institutional narrative than most large-cap altcoins.

CryptoSlate has already tracked institutional migration into Ripple-linked products, ETF resilience tied to Ripple’s expanding footprint, and the growing tension between XRPL adoption and token value capture. The setup has now tightened.

A sharp overnight jump in oil, stronger dollar conditions, and renewed inflation anxiety have pulled XRP into a macro test that feels more direct than the themes that carried it through the first quarter.

That shift came quickly. Following President Donald Trump’s latest remarks on Iran, AP reported that oil surged more than 6%, while a separate market wrap from Business Insider put Brent near $108.

Brent crude pushed to roughly $108, the U.S. Dollar Index climbed back to about 100, and Bitcoin slid toward $66,666.

XRP price held near $1.35 to $1.36, according to CryptoSlate data, though the weekly move still carried visible pressure. 24-hour volume is near $1.32 billion.

Why this matters: XRP’s core pitch hinges on stress in the global financial system. If higher costs, tighter liquidity, and cross-border friction are increasing, the token should be moving closer to its use-case value. Instead, it is still reacting like a high-beta asset, which raises a more practical question for investors: when does utility start to matter in price?

The connection to XRP runs deeper than broad crypto weakness. Bitcoin usually absorbs the first layer of geopolitical and liquidity shock. XRP sits closer to the payment, liquidity, and settlement conversation.

Ripple has spent months building that frame. The company’s GTreasury acquisition and subsequent Ripple Treasury launch widened its reach into corporate cash management, while earlier reporting on Ripple’s trust-bank ambitions and broader licensing footprint gave XRP holders a practical reason to view the asset through a financial-infrastructure lens.

That lens now cuts both ways. When oil climbs, freight and energy input costs rise, and inflation expectations stiffen, the case for faster, cheaper movement of money gains urgency.

The same macro shock also boosts the dollar, tightens financial conditions, and usually pushes risk assets into a tougher zone. XRP now sits at the intersection of those two forces.

The tension is direct because it touches household budgets, portfolio drawdowns, and the cost of moving capital across borders.

Oil and the dollar have turned XRP’s payments pitch into a real-time stress test

XRP’s use-case narrative has always leaned on efficiency. Cross-border transfers, on-demand liquidity, and enterprise settlement create a cleaner economic pitch when payment rails are under strain.

That pitch becomes easier to grasp during a week when the world suddenly has to price a higher energy bill, a firmer dollar, and the risk of another inflation impulse. The macro map on the chart is blunt.

Brent jumped, DXY rose, and Bitcoin rolled over. XRP followed the pressure lower through the week, even though its long-term pitch should, in theory, become more relevant as global money flows grow more expensive and more fragile.

That contradiction is the center of the setup. XRP rallied for much of this cycle on the idea that Ripple’s regulated expansion, enterprise positioning, and capital-market traction were building a more durable floor under the token.

CryptoSlate covered that process through pieces on institutional DeFi ambitions, legacy financial integration, and recent ETF flow softening. Those themes still carry weight.

They now face a harder question. If a stronger dollar and higher oil create deeper friction across the global economy, why has XRP behaved like a pressured altcoin instead of a market leader?

Part of the answer sits in the liquidity hierarchy. Bitcoin still commands the first response in macro stress, because it carries the deepest liquidity, the broadest institutional recognition, and the strongest reflex move during periods of geopolitical uncertainty.

XRP has a narrower lane. It needs investors to believe that utility can translate into token demand on a timeline that the market can price.

That challenge has shown up repeatedly in the split between Ripple’s business traction and XRPL activity and on XRP’s amplified beta during broad crypto drawdowns. The current move forces that same issue into a macro context.

Ripple can broaden into custody, treasury management, and regulated financial software, yet XRP still trades within a market structure that responds quickly to dollar strength and falling crypto risk appetite.

Bitcoin spent the last several sessions slipping back toward the mid-$66,000s, a visible loss of altitude from the higher zones traders had defended earlier in the week.

The dollar index reclaimed the 100 handle, a psychological level that usually feeds tighter global liquidity conditions. Brent then accelerated back above $108. XRP held around the mid-$1.30s.

That set of moves creates a clean economic message. Payment friction may be rising in the real world, but capital is still seeking safety before it seeks efficiency.

For XRP, that leaves the asset in an identity crisis. Its strongest fundamental narrative says a fractured, expensive, slow-moving global financial system should increase the value of its use case.

Its current market behavior suggests investors still classify it as part of the higher-beta branch of crypto exposure.

The coming macro calendar will press on XRP’s weakest seam

The coming week further compresses the issue, as the macro calendar offers three direct tests. The Bureau of Labor Statistics employment report arrives on Friday, April 3.

The Federal Reserve’s April calendar shows the minutes from the March 17-18 FOMC meeting arriving on Wednesday, April 8. The BLS release calendar then places March CPI on Friday, April 10.

Those releases land directly on top of the new oil shock. They will shape whether markets see the latest rise in energy as a temporary disruption or the start of another inflation leg that keeps policy tighter for longer.

XRP’s response to that sequence could define the next phase of its cycle. A hotter payrolls print would strengthen the view that labor conditions remain firm enough to keep the Federal Reserve cautious.

Hawkish signals in the minutes would add another layer of restraint. A hotter CPI print next Friday would confirm that the oil move has arrived inside an already sensitive inflation backdrop.

That combination usually supports the dollar and squeezes speculative assets. XRP would then enter a zone where every part of its identity gets tested at once.

The company behind it has spent months expanding its institutional reach. The token itself would still need to show that investors are willing to price it as a beneficiary of payment-system stress.

There is a sharper retail hook inside that setup. Many people understand inflation as the price of groceries, gasoline, travel, and borrowing.

Far fewer think about what a stronger dollar and higher energy costs do to cross-border settlements, corporate treasury decisions, and the movement of liquidity through financial rails. Ripple’s own enterprise push, as reflected in its treasury platform strategy, brings XRP closer to that conversation, whether the token captures all the value today or not.

That gap between corporate utility and token pricing is where the emotional trigger sits. People with market exposure can see oil jumping and Bitcoin sliding.

They can see the dollar catching a bid. The harder question then comes into focus: if the world is becoming more expensive and more fragmented, why is the best-known payments token still struggling to trade like a payment asset?

The answer over the next week may come down to acceptance levels in price and acceptance levels in narrative. If oil cools, DXY softens, and payrolls or CPI relieve some pressure, XRP has room to reclaim its enterprise-infrastructure frame, especially with Ripple’s broader footprint still giving investors a structural reason to stay engaged.

If oil holds firm, the dollar extends, and inflation anxiety deepens, XRP may keep trading as macro beta first and payments infrastructure second. That outcome would widen the contradiction between Ripple’s strategic progress and the token’s market role.

It would also leave holders facing a more uncomfortable conclusion. XRP has spent years being sold as a bridge asset for an imperfect global financial system.

A week of higher oil, stronger dollars, and tighter conditions offers a live test of whether the market actually believes that the bridge deserves a premium.

The post XRP’s use case should benefit from global stress, so why is price acting like a risk asset? appeared first on CryptoSlate.

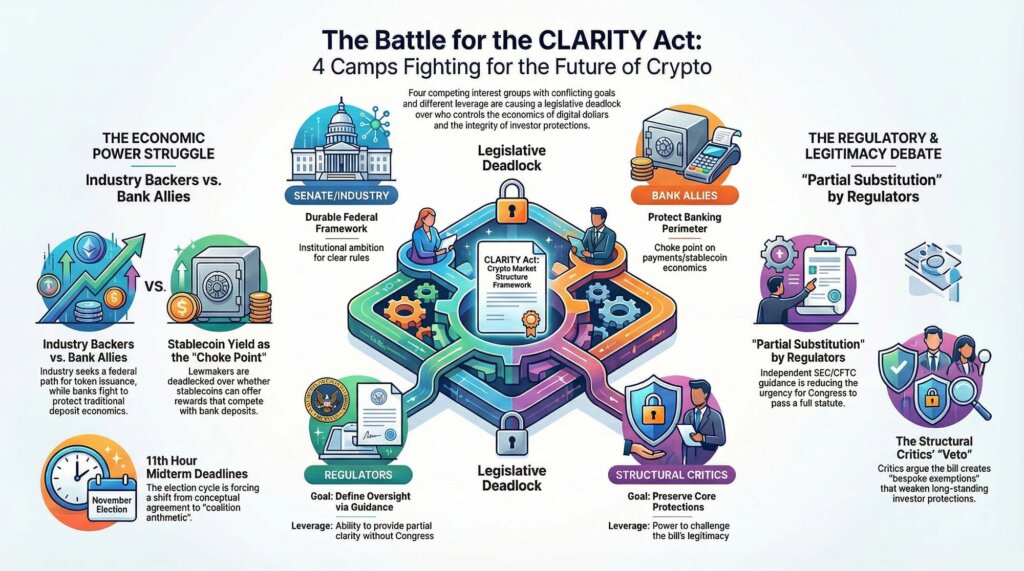

The CLARITY Act entered Washington as a bid to impose a durable market structure on crypto. It now sits at the center of a four-way fight over who gets to define that structure, who gets paid inside it, who supervises it, and how much of the existing financial rulebook survives the rewrite.

The bill still includes broad language for jurisdictional clarity, with the Senate Banking Committee majority outlining a framework that draws lines between the SEC and the CFTC while adding tailored disclosures and anti-fraud protections.

Around that frame, the coalition has fractured into four camps with different definitions of success. Senate and industry backers still want a federal market-structure bill that gives crypto firms a workable path into US regulation.

Bank-aligned critics want to seal off stablecoin yield and keep deposit economics from migrating out of the banking system. Regulators have begun moving through their own channels, with the SEC and CFTC signing a new memorandum of understanding and the SEC issuing a fresh interpretation of crypto assets that begins to deliver some of the clarity Congress had reserved for itself.

Structural critics still argue the bill would carve crypto out of core investor protections, a case advanced by groups such as Better Markets and by former CFTC Chair Timothy Massad in prior congressional testimony.

That collision changed the shape of the bill. What began as a question of statutory design has become a contest over bargaining power.

Each camp can slow the process, each camp can claim some version of consumer protection, and each camp enters the next phase with a different source of leverage. Senate and industry backers hold the broadest institutional ambition.

Why this matters: The CLARITY Act was intended to anchor crypto within US law, with clear rules for exchanges, tokens, and custody. If it stalls or narrows, firms remain in a patchwork regime shaped by enforcement and agency guidance, while banks retain tighter control over dollar-based financial activity. The outcome will determine whether crypto can compete directly with traditional deposits and payment rails, or operate inside a more constrained perimeter.

Banks and their allies hold a choke point around payments, economics, and stablecoin rewards. Regulators hold the power of partial substitution, because every piece of interpretive guidance from the SEC and CFTC narrows the pool of uncertainty that once made CLARITY the singular prize.

Structural critics hold a veto over the debate on legitimacy because their argument speaks to a long-standing Washington fear that crypto bills could create bespoke exemptions that would replace the exemptions older laws once carried.

The calendar tightened the pressure. In January, Senate Banking Chairman Tim Scott said the committee would postpone its markup while bipartisan negotiations continued.

Later that month, the Senate Agriculture Committee advanced related market-structure legislation, keeping momentum alive while underlining that the main bottleneck had shifted into the negotiating room.

By March, the fight over stablecoin rewards had become the central pressure point in the bill, with public reporting and congressional chatter converging on the same conclusion: a framework bill could move forward only if lawmakers found a way to reconcile crypto’s push for broader utility with banking concerns about disintermediation and deposit competition.

That left CLARITY in a familiar Washington posture, broad enough to attract coalitions in theory, specific enough to trigger fracture once the revenue lines came into view.

The first two camps are fighting over the economic core of the bill. The first camp still sees CLARITY as the vehicle that can finally anchor crypto market structure in federal statute.

That camp includes Senate Republicans who have spent months arguing that the industry needs rules written through Congress rather than through case-by-case enforcement, along with a large swath of the industry that wants a lawful path for token issuance, exchange activity, brokerage, custody, and participation in decentralized networks.

The core attraction has always been the same. A federal framework promises a clearer allocation of authority among agencies, a more predictable compliance process, and a narrower zone of ambiguity about what falls under securities law and what falls under commodities regulation.

The Senate Banking majority’s summary reflects that approach, leaning on the idea that a single framework can impose definitional order on a market that has spent years operating inside regulatory overlap.

For crypto firms, the appeal runs deeper than process. A statute holds out the prospect of capital formation under rules that institutions can underwrite, boards can sign off on, and legal teams can defend without having to rebuild the analysis around every enforcement cycle.

Yield politics turned CLARITY into a fight over the economics of digital dollars

The first camp’s ambition runs straight into the second camp, which has focused the fight around stablecoin yield and the economics of digital dollars. The Bank Policy Institute has made the bank-aligned position unusually plain.

Lawmakers, in that view, need to prevent stablecoin structures from recreating deposit-like products outside the traditional banking perimeter, especially if those products begin passing through rewards or yield that look and feel like interest. Under that logic, the danger is structural.

If tokenized dollars can offer returns or functionally similar incentives at scale, then commercial bank deposits face a new form of competition, payments activity migrates, and the prudential perimeter gets thinner exactly where regulators spent years trying to harden it. That is why the stablecoin rewards fight turned into the bill’s main choke point.

It is the place where market structure meets balance-sheet politics.

Those two camps can still describe their goals with overlapping language. Both can say they want consumer protection, operational integrity, and a framework that channels crypto activity into supervised forms.

The overlap ends when the discussion reaches who captures the economics created by digital dollars. The industry camp wants enough room for product development, distribution, and economic pass-through to make federally compliant crypto businesses worth building.

The bank-aligned camp wants a bright barrier around any feature set that could pull value from deposits into tokenized alternatives. That conflict reaches beyond one provision.

It shapes how lawmakers think about payments, exchange design, brokerage economics, wallet architecture, and the degree of freedom crypto firms would have to compete with institutions that already dominate dollar intermediation. Every concession made to one side tends to drain utility from the bill as imagined by the other.

The result is a negotiation whose formal subject is market structure and whose real center of gravity is control over monetary rails. That is why this phase of the CLARITY debate feels more compressed and more political than the earlier debate over jurisdiction.

Jurisdiction can be split in text. Economic control creates winners and losers with organized lobbies, committee relationships, and a direct financial interest in the final wording.

The first camp still wants a durable federal framework. The second camp wants that framework shaped tightly enough that it does not redraw the economics of digital money in a way that benefits crypto firms at the expense of banks.

Both camps can live with progress. Each one defines progress differently, and that difference is what keeps the bill from moving forward.

The third camp sits within the regulatory apparatus itself and introduced a fresh complication into the bill by moving ahead with practical coordination and interpretive guidance. On March 11, the SEC and CFTC announced a new memorandum of understanding designed to improve coordination on crypto oversight.

Days later, on March 17, the SEC issued a new interpretation clarifying how federal securities laws apply to crypto assets, with the CFTC aligning publicly with the effort. By March 20, the CFTC had added crypto-related FAQs that continued the same line of work.

Those actions did not write a statute, and they did not resolve every contested edge case, yet they changed the terrain around CLARITY in a way lawmakers can feel. Congress had been negotiating a bill designed to provide clarity.

Regulators started supplying pieces of that clarity themselves.

Regulators are shaping the field while structural critics keep the legitimacy fight alive

That shift created two immediate effects. First, it gave industry participants some of the operational breathing room they had been seeking, particularly regarding how certain crypto activities are analyzed through the lens of securities law.

Legal practitioners quickly seized on the importance of the change. In a March 19 analysis, Katten described the SEC and CFTC guidance as a major event for the sector, pointing to a more legible treatment of activities such as airdrops, mining, staking, and wrapping.

Second, the guidance changed congressional leverage. Every increment of clarity delivered through agency action reduces the urgency that once surrounded CLARITY as the exclusive route to order.

That creates a subtle but powerful dynamic. A bill under pressure usually gains energy from scarcity.

Once regulators start producing partial substitutes, lawmakers face a harder sell when they ask wavering factions to make politically costly concessions in the name of a breakthrough.

That shift does not weaken the case for statute across the board. A regulatory interpretation sits lower in the durability hierarchy than a congressional framework, and industry participants with long investment horizons still prefer statutory architecture to agency guidance.

Yet the third camp need not erase the case for CLARITY to affect the negotiation. It only needs to be shown that immediate passage is the only way to restore order.

That is already happening. The more the agencies coordinate, the easier it becomes for lawmakers to accept delay, narrower text, or a compromise version of the bill that settles the most acute fights while leaving some larger structural ambitions for another cycle.

For some senators, that can feel like prudence. For some industry players, it can feel like the center of the bill is being negotiated away in real time.

The regulatory camp also exerts pressure in a second way. It offers a political release valve.

Lawmakers who want to say Washington is making progress on crypto can point to the SEC and CFTC without forcing immediate resolution of every issue inside CLARITY. That lowers the cost of postponement and raises the threshold for what kind of final agreement is worth bringing to the floor.

A bill that once looked indispensable now has to demonstrate added value against the backdrop of agency-led adaptation. That is a difficult standard, especially for a coalition already carrying internal conflict over stablecoin rewards, federal preemption, DeFi treatment, and investor-protection language.

The fourth camp continues to ask the question that lies beneath every crypto bill in Washington: Does this framework integrate the sector into existing law, or does it carve out a special lane that weakens protections the rest of finance still carries?

That concern has animated groups such as Better Markets and has appeared in prior testimony from former CFTC Chair Timothy Massad, who argued that proposals such as CLARITY can create artificial distinctions between securities and commodities in ways that reduce the reach of investor protections.

This camp does not have to win the whole argument to shape the bill. It only has to keep the legitimacy challenge alive.

Once that challenge enters the center of the debate, every provision gets viewed through a second lens. A disclosure regime becomes a question about whether disclosure replaces stronger obligations.

A jurisdictional transfer becomes a question about whether oversight is being softened through classification. A pathway for token markets becomes a question about whether the path relies on exemptions that older sectors would never receive.

This is where the four camps collide most sharply. Senate and industry backers want a framework that firms can use at scale.

Bank-aligned critics want to close off yield dynamics that could pressure deposits and payments economics. Regulators are already showing that some clarity can emerge through agency action, reducing the pressure to accept a broad legislative bargain on weak terms.

Structural critics keep pushing on the question of whether the bill preserves the integrity of long-standing protections. A compromise that satisfies the first camp by preserving broad utility may alarm the second and fourth camps.

A compromise that satisfies the second and fourth camps by tightening the perimeter may leave the first camp with a framework that carries less strategic value. A compromise that leans heavily on regulator-led clarity may satisfy lawmakers seeking incremental progress while leaving industry participants with a less durable settlement.

That is why the final question has become a matter of coalition arithmetic rather than conceptual agreement. All four camps can say they want order.

Their conditions for the order point are in different directions.

Midterm pressure is turning a policy negotiation into coalition arithmetic

The midterm calendar sharpens every one of those contradictions. November imposes deadlines on attention, legislative bandwidth, and political appetite for complex financial legislation, generating cross-pressures within both parties.

As the calendar advances, the value of waiting rises for any camp that thinks the current bargain costs too much. Banks can wait if the alternative is stablecoin economics they dislike.

Structural critics can wait if the alternative is a framework they view as too permissive. Regulators can keep moving within their own lane.

Industry groups can keep arguing that delay carries a cost, yet that message weakens if the agencies continue to supply enough guidance to keep large parts of the market functioning.

The coalition that can pass CLARITY, therefore, needs more than a shared talking point around clarity. It needs a settlement that provides the first camp with enough usable structure, the second camp with enough protection around dollar economics, the third camp with a role that fits the statute rather than competes with it, and the fourth camp with enough assurance that core protections remain intact.

That path is narrow. It is still navigable, although the room for error has tightened.

A workable reconciliation would likely require lawmakers to frame the bill less as a maximal rewrite and more as a disciplined allocation of authority, paired with narrow guardrails on stablecoin rewards and stronger language on anti-fraud, disclosure, and supervisory obligations. Even then, the politics stay hard.

Each camp would have to accept a result that falls short of its preferred endpoint. The first camp would accept tighter limits than many crypto firms want.

The second camp would accept a federal framework that still gives compliant crypto business lines room to grow. The third camp would accept that agency guidance is a bridge into statute rather than a substitute for it.

The fourth camp would accept that integration can occur without dismantling the regulatory perimeter. Whether that bargain is possible before November is now the central test around CLARITY.

The bill can still move. The harder question is whether these four camps can converge on a version of movement that each side can live with once the votes are counted.

The post A four-way deadlock is now blocking the US Clarity Act crypto bill — and each side can stop it appeared first on CryptoSlate.

Bitcoin spent the past 24 hours returning to the key levels on my channel map rather than continuing its breakout. It tested a boundary, failed to convert that test into acceptance, and rotated lower into the next pocket of support memory.

Bitcoin price slid from the upper $68,000s and low $69,000s to around $66,400 by late morning in Europe on April 2. The 24-hour move came in at roughly 3%, with the high near $69,170 and the low near $66,218.

Over 48 hours, the net change stayed close to flat, yet the path inside that window shifted the balance of the chart lower. Price gave up the white shelf near $66,894, rejected a retest, and left the market trading beneath a level that had previously held the local structure together.

Why this matters: What changed is not just the price move but the level it broke. Bitcoin lost a support zone that had been holding the recent structure together, and failed to reclaim it on the first retest. At the same time, the dollar and oil moved higher together, a combination that tends to pressure liquidity and risk appetite. That pairing raises the bar for any immediate recovery and puts the next lower support zones back into focus.

That pattern sits squarely inside the 2024 channel framework, first laid out in Bitcoin channel predictions, aligning with market movements over 6 months. The premise was simple and practical.

Repeating close prices on the 30-minute chart can identify where leverage, stop placement, and spot liquidity tend to cluster. Those shelves have kept showing up at the turning points.

They have framed rebounds, capped rallies, and guided the path between them with more consistency than many of the more elaborate narratives built around Bitcoin.

The last two days developed in three steps. First, Bitcoin spent time in the upper half of the near-term range, pushing back toward the yellow boundary near $67,995.

Second, the move stalled before any real acceptance could build above that shelf. Third, the chart rolled over sharply and carried price through the white line at $66,894 before finding a temporary footing in the mid $66,000s.

That sequence shows where control sits right now. Buyers still have a path back into the range, though that path starts with repair.

Price needs a reclaim of $66,894, then a push back through $67,995, before the structure looks constructive again.

Bitcoin lost the shelf it needed to hold, and the near-term structure turned lower

The same logic that led Bitcoin to fail 7 times to break $71,500. Repeated failure at a level adds weight to the next test.

A ceiling becomes a lid when sellers step down and meet price earlier, and a floor becomes vulnerable when buyers lose the urgency to defend it on first contact. In that February piece, the key level was $71,500, with the next friction zones above at around $72,000 and then $73,700 to $73,800.

Below, I flagged the same shelves visible on the current chart: $68,000, then $66,900, with deeper support in the low $61,000s. That ladder remains intact today.

The difference is that Bitcoin has now moved one rung lower.

The practical sequence is straightforward. The market had room to recover while it held above the white shelf.

Once it lost that level and failed the retest, the burden shifted to buyers to prove that the drop was a flush rather than a new acceptance at a lower level. So far, the rebound has lacked authority.

A brief pop back toward the broken shelf printed the kind of weak retest that usually accompanies a market still under pressure. The candles after the drop look smaller, the bounce looks labored, and the range compression is taking place under resistance rather than above support.

The 24-hour numbers reinforce that view. Bitcoin fell around 3.02% from the close 24 hours earlier, while the 48-hour change stayed only marginally positive.

That combination often appears when a market has spent one day building a base and the next day giving it back. In other words, the chart preserved the wider range while damaging the near-term structure.

For a general audience, that distinction keeps the analysis anchored to thresholds rather than emotion. The market remains inside a ladder of known shelves.

It has moved from one shelf to the next. The immediate job for bulls is to recover $66,894, then $67,995.

The immediate risk for anyone leaning bullish is that continued trading below those levels draws attention to the lower white boundary around $61,726.

That lower target should already be familiar from my original channel work, where the channels were built to identify support and resistance rather than force a single directional call. It also lines up with the roadmap in “Bitcoin to $73k? Be prepared with the price levels to watch during a bear market“, where the key point was to treat lower shelves as historical liquidity pools.

The chart here fits that framework closely. Bitcoin is trading beneath a broken support shelf, and the next meaningful repair level sits above the current price.

Until that changes, the burden of proof remains on the upside.

Support memory still follows the same channel logic that shaped the earlier calls

These levels have held up well because they are built from where the market repeatedly closed, paused, and built positioning. Some zones carry memory because they spent hours or days there.

Other zones looked dramatic on the way up or down, yet offered weaker support because Bitcoin moved through them quickly, and the market built less inventory there.

That distinction shaped my October 2024 analysis in “Above the all-time high of $73.7k these could be the new resistance levels to watch”, where I argued that Bitcoin was trading at the top of a core price channel between $67.9k and $71.5k and that the zone between $71.5k and $73.7k had relatively little historical price action.

The implication was clear. Above the well-traded shelf, the market entered thinner territory where movement could become more abrupt.

The same logic applied later on the downside. In “It’s foolish to pretend Bitcoin’s story doesn’t include $79k this year”, I described the green band around $79,000 as a more substantial region because Bitcoin had spent time consolidating there during earlier legs of the cycle.

Below that sat the deeper structural supports in the red and blue channels, roughly $49,000 to $56,000, the area Bitcoin defended repeatedly before the move toward six figures. Then, in “Akiba’s medium-term $49k Bitcoin bear thesis – why this winter will be the shortest yet“, I framed $49,000 as a cyclical support case tied to miner stress, fee share, hashprice, and ETF flow elasticity.

Those longer-horizon calls operate on a different scale than the current 30-minute move, though they all rely on the same discipline: identify the shelf, assess how well the price is holding it, and define the next level that becomes relevant when it breaks.

The current move fits that sequence cleanly. Bitcoin approached the lower yellow boundary near $67,995 and could not hold it.

It then slid beneath the white shelf near $66,894. A 30-minute breakdown candle early on April 2 accelerated the move from the high $68,000s into the upper $67,000s, and follow-through selling pulled the price down toward the low $66,000s.

Once there, the market printed a small rebound and then drifted sideways beneath broken support. That behavior usually signals a market still negotiating lower inventory rather than preparing for an immediate reversal.

Anyone following the latter channel work through the six-figure phase will recognize the same design principle in “Bull or Bear? Today’s $106k retest decided Bitcoin’s fate” and “Bitcoin price next move: $92k or $79k? Let’s break it down”. The exact prices changed as Bitcoin moved through new territory, yet the method stayed the same.

A retest that holds opens the next band. A retest that fails hands control to the lower shelf.

The current chart falls into the second category. Price still sits below the broken shelf, which keeps the lower ladder in play.

Dollar strength and higher oil arrived at the same time as the breakdown, leaving reclaim levels above and deeper support below

The broader market context over the last 24 to 48 hours adds another layer to the chart. Alongside Bitcoin moving lower, the comparison view showed the U.S. Dollar Index rebounding above 100 while Brent crude pushed toward $108.

That combination tightens conditions around risk assets. A firmer dollar usually weighs on global liquidity at the margin, and higher oil prices can amplify inflation concerns, rate sensitivity, and geopolitical caution.

Bitcoin tends to trade with greater friction when both markets are moving in the same direction, against a softer risk backdrop.

That setting sits comfortably inside the framework of the later channel pieces. In the $79k piece, I wrote that liquidity could become the problem if ETF outflows intensified and risk appetite faded.

In the $49k bear thesis, I argued that negative 20-day ETF flows, alongside weaker miner economics, would increase the probability of sharper downside legs. In the seven failures at $71,500 analysis, I pointed to a macro environment where yields remained high enough to keep conditions tight.

The current move reflects that same type of pressure from a shorter time frame; a structurally important shelf gave way while the macro backdrop offered little relief.

For the practical map, the levels now do the heavy lifting. Resistance begins with $66,894, then expands to $67,995.

If Bitcoin regains both and spends time above them, the near-term damage begins to heal, and the next higher levels come back into view: $71,523, then $72,017, then the pair around $73,519 and $73,764, and then the upper extension near $77,056. Those higher levels are already familiar from the price discovery work above the old all-time high.

Support begins with the intraday low in the low $66,000s, though the stronger structural memory sits much lower, near $61,726. That leaves Bitcoin in a narrow but important condition.

It is close enough to reclaim broken support if buyers return with urgency, and close enough to invite a deeper sweep if they do not.

The conclusion remains the same one the chart has been offering since these channels were first drawn in early 2024. Bitcoin respects shelves until one gives way, and when one breaks, the next shelf tends to become the destination.

Over the last 24 hours, Bitcoin lost the shelf it needed to hold to keep the bounce credible. Over the last 48 hours, it preserved the wider range while shifting the short-term structure lower.

The next move now hinges on whether the price can climb back above $66,894 and $67,995 quickly enough to change the feel of the chart. Failing that, the lower white boundary near $61,726 moves back into focus as the next serious test on the ladder.

The post Bitcoin breaks critical support as dollar and oil move together, raising risk of a deeper drop appeared first on CryptoSlate.

Treasury's first proposed GENIUS rule landed on April 1 as a notice of proposed rulemaking.

The text inside it builds the operational architecture for US stablecoin governance, addressing which institutions may issue payment stablecoins, under what conditions, and at what scale before federal oversight becomes mandatory.

Why this matters: This shifts stablecoins from a fragmented regulatory patchwork toward a nationally coordinated system. For users, it affects how safely dollars can be redeemed and moved. For issuers, it defines whether they can scale independently or must transition into a federal regime as they grow.

By defining when a state licensing regime qualifies as “substantially similar” to the federal framework, Treasury is now defining those terms.

The stablecoin market already holds roughly $316 billion, with USDT accounting for about 58% of the supply, per DeFiLlama.

Retail-sized volume for USDC, USDT, and PYUSD grew from $500 million to $69.8 billion between 2019 and 2025. FSOC's 2025 annual report described the GENIUS framework as a federal prudential system designed to onshore stablecoin innovation, protect holders in the event of insolvency, and support the US dollar's international role.

Treasury's NPRM now shows how that prudential vision operates on the ground.

The hidden fight over who governs

The Treasury chairs the interagency review committee that certifies state stablecoin regimes, which includes leadership from the Fed and the FDIC.

That committee's judgment rests on the “substantially similar” test, and Treasury's proposal defines that test to include the GENIUS Act itself, as well as the implementing regulations and interpretations issued by federal agencies over time.

Treasury says that substantial similarity would be hard to administer, and state and federal standards could “starkly deviate.”

As OCC, Treasury, the Fed, FinCEN, and OFAC add implementing rules, the standard Washington uses to measure states shifts with them. State regimes approved today must track a benchmark that Washington keeps building.

Treasury organizes the rule around two categories. The first, called uniform, covers the parts that establish trust in the instrument itself: reserve assets, redemption, monthly reserve publication, limits on rehypothecation, accountant examinations, BSA/sanctions compliance, lawful-order capability, and core activity limits.

State implementation of each uniform requirement must be consistent with the federal framework “in all substantive respects,” with no material deviations in definitions or scope. For BSA and sanctions specifically, states must cross-reference federal rules directly, with no room for state-drafted substitutes.

The second category allows calibration around some capital, liquidity, reserve diversification, risk management, applications, licensing, and certain redemption mechanics. Treasury still constrains that room, and state choices in the flexible bucket must produce outcomes “at least as stringent and protective” as the federal framework.

For example, a state may allow additional reserve assets only if the OCC has already approved them as similarly liquid federal government-issued assets. That is federal pre-clearance administered through state paperwork.

| Category | Requirement area | Treasury standard | State discretion | Why it matters |

|---|---|---|---|---|

| Uniform | Reserve assets | Must align with the federal framework in all substantive respects | No material deviation | Defines trust in the stablecoin itself |

| Uniform | Redemption | Must track the federal baseline closely | No narrower state substitute | Protects holders’ ability to redeem |

| Uniform | Monthly reserve publication | Must match federal expectations | Very limited room to vary | Supports transparency and market confidence |

| Uniform | Limits on rehypothecation | Must conform to the federal framework | No meaningful carve-out | Prevents riskier use of backing assets |

| Uniform | Accountant examinations | Must be consistent with federal requirements | Little to no variation | Standardizes verification of reserves |

| Uniform | BSA / AML / sanctions | States must cross-reference federal rules directly | No state-drafted alternative | Keeps compliance under national control |

| Uniform | Lawful-order capability | Must track federal expectations | Minimal discretion | Preserves enforcement and legal access |

| Uniform | Core activity limits | Must align with the federal framework | No material divergence | Keeps issuers inside a nationally defined model |

| Flexible / calibrated | Capital | Outcomes must be at least as stringent and protective as the federal framework | Some calibration allowed | Lets states tune prudential standards without weakening them |

| Flexible / calibrated | Liquidity | Must be at least as protective as the federal baseline | Some calibration allowed | Gives limited room for state tailoring |

| Flexible / calibrated | Reserve diversification | May vary, but only within outcomes at least as protective as the federal framework | Narrow flexibility | States can adjust, but not create a looser reserve regime |

| Flexible / calibrated | Risk management | State framework can differ in form | Must still meet protective federal-equivalent outcomes | Allows administrative variation, not a different philosophy |

| Flexible / calibrated | Applications / licensing | State administration is allowed | Cannot create a genuinely different regime | Keeps the state lane administrative, not alternative |

| Flexible / calibrated | Certain redemption mechanics | Some room to calibrate | Must remain at least as protective as the federal system | States can adjust process, not weaken substance |

| Flexible / calibrated | Additional reserve assets | Allowed only if the OCC has already approved comparable assets | Federal pre-clearance still governs | Shows state flexibility is still bounded by Washington |

The $10 billion ceiling and what it produces

The GENIUS Act caps the state option at issuers with no more than $10 billion in consolidated outstanding payment stablecoins.

Treasury adds that state transition rules cannot impede a move to federal oversight once an issuer crosses that line, and issuers in a state that fails certification must either stop issuing payment stablecoins or move into the federal licensing framework.

The $10 billion ceiling is the structural tell, since the state lane functions as an entry point for smaller issuers. At scale, the federal framework becomes the only durable home.

Citi's updated 2026 forecast puts its base-case estimate for the 2030 stablecoin market at $1.9 trillion. Standard Chartered projected the market could reach $2 trillion by the end of 2028.

A market at that scale runs on uniform reserve, redemption, and compliance standards and rewards issuers capable of absorbing national-style regulatory overhead.

Visa's concentration data already reflects the current destination: as of October 2025, more than 97% of the stablecoin supply had converged on USDT and USDC. Treasury's design standardizes the conditions that large, compliant issuers are already built to meet.

Standard Chartered estimated stablecoins could pull roughly $500 billion in deposits out of US banks by the end of 2028.

The number frames the context correctly: stablecoins are becoming claims on dollar liquidity that sit alongside traditional bank deposits, and the institution that governs the terms of stablecoin issuance governs an expanding piece of dollar infrastructure.

Treasury's proposal positions Washington as that institution.

| Scale marker | Amount | What it represents | Regulatory implication | Why it matters |

|---|---|---|---|---|

| State-lane ceiling | $10 billion | Maximum consolidated outstanding payment stablecoins for an issuer to remain in the state option | Above this line, the issuer must transition to federal oversight or stop issuing new payment stablecoins | Shows the state path is a limited entry lane, not the durable home for large issuers |

| Current stablecoin market | ~$316 billion | Approximate current total stablecoin market size | The market is already far larger than the state-lane threshold | Suggests Treasury is designing rules for a systemically meaningful market, not a niche one |

| Citi base case (2030) | $1.9 trillion | Citi’s updated 2026 base-case estimate for the stablecoin market by 2030 | A market at this scale would likely rely on uniform national standards rather than fragmented state variation | Reinforces the article’s argument that scale points toward federalization |

| Standard Chartered forecast (end-2028) | $2 trillion | Standard Chartered’s projection for stablecoin market size by the end of 2028 | Implies that if growth continues, large issuers will almost inevitably end up in the federal framework | Supports the view that the state lane functions more like a launch ramp than a long-term alternative |

| Bank deposit migration estimate | ~$500 billion | Standard Chartered estimate of deposits stablecoins could pull from U.S. banks by end-2028 | Stablecoin issuance becomes a question of dollar-system governance, not just crypto regulation | Helps mainstream readers see this as a financial-architecture story, not a niche policy update |

Two paths through the same architecture

The bull case runs from clarity to scale. Uniform national rules on reserves, redemption, and compliance remove the uncertainty that has kept banks, card networks, and enterprise treasury teams cautious about deep integration with stablecoins.

Along that path, supply tracks toward the Citi and Standard Chartered forecasts, Visa's 130-plus card programs are overlaid on stablecoin wallets, and the state lane serves as a launch ramp for smaller issuers before they graduate to federal supervision.

Treasury's tight architecture then reads as the operating manual for US digital dollar expansion, which is a framework that made the market credible enough to absorb institutional demand at scale.

The bear case runs the same architecture in reverse. The forthcoming BSA/AML and lawful order rules, which both Treasury and the OCC have flagged as still pending in separate rulemakings, could entail heavy operational requirements.

If certification proves slow, costly, or politically fraught, smaller issuers may find the state lane functionally inaccessible even before they approach the $10 billion threshold.

The result would be a market that is legally cleaner but structurally oligopolistic, with innovation relocating to distribution and infrastructure, away from issuance.

Treasury frames a different goal. The predictable market response to high uniform compliance floors and a hard ceiling on state-lane scale is concentration, and Visa's existing market data shows the market was already moving in that direction before the rule arrived.

Washington holds the baseline

This NPRM is part of a larger regulatory framework. OCC's February proposal covered the required GENIUS regulations, except those tied to BSA, AML, and OFAC sanctions, which will be addressed in a separate rulemaking coordinated with Treasury.

Treasury's own NPRM flags that rules on lawful-order compliance are forthcoming as well. The full compliance map for stablecoin issuers awaits completion.

The $316 billion market and $10 trillion transaction volume settled the question of stablecoins belonging in the US finance. Treasury is deciding who gets to shape them as they enter it.

The first proposed GENIUS rule makes the answer clear: Washington accepts state participation in stablecoin issuance within a federal architecture that the Treasury continues to build, on Washington's terms.

The post US Treasury’s first GENIUS rule now redraws who controls stablecoins at scale appeared first on CryptoSlate.

Cryptoticker

What Just Happened in the Markets?

Global markets surged after reports that Iran and Oman are working on a protocol to secure shipping through the Strait of Hormuz.

The reaction was immediate:

- Over $1.5 trillion added across US markets

- Nasdaq, S&P 500, and Dow all moved higher

- Risk sentiment briefly flipped bullish

👉 On the surface, this looks like the start of a recovery.

But crypto is telling a completely different story.

Crypto Is Not Following — And That’s the Warning

Despite the bullish backdrop:

- Bitcoin is still trading under pressure

- Ethereum and major altcoins continue to decline

- No strong follow-through from crypto markets

👉 This kind of divergence is rare — and important.

When crypto fails to react to good news, it often signals that something deeper is broken beneath the surface.

The Market Got Bullish News — A Lot of It

Over the past hours, several developments should have supported crypto:

- IMF signaling that tokenization could reshape global finance

- Coinbase gaining conditional approval for a US national trust charter

- $500 million USDC minted, signaling fresh liquidity entering the system

- Equity markets recovering sharply

👉 Under normal conditions, this would trigger a strong crypto bounce.

But it didn’t.

Why Crypto Is Ignoring the Rally

The answer lies in liquidity and macro pressure.

Even though headlines are turning positive, the underlying conditions remain tight:

- Oil prices are still above $110