Cryptocurrency Posts

Crypto Briefing

Gulf states' diplomatic efforts with Iran could stabilize the region, reducing regime collapse risks and influencing ceasefire prospects.

The post Gulf countries push for normal relations with Iran appeared first on Crypto Briefing.

Diplomatic efforts in the Strait of Hormuz may signal potential de-escalation, impacting market expectations for a US-Iran ceasefire.

The post Trump to pay DHS employees; Iran drafts hormuz protocol with Oman appeared first on Crypto Briefing.

The Iran-Oman protocol may signal diplomatic progress, potentially influencing regional stability and market confidence in ceasefire prospects.

The post Iran drafts hormuz protocol with Oman amid ongoing conflict appeared first on Crypto Briefing.

The revelation strains US-Iran diplomatic efforts, heightening regional tensions and increasing the likelihood of military conflict.

The post Pakistan uncovers israeli plot against iranian officials, impacting ceasefire odds appeared first on Crypto Briefing.

Ripple Prime's BBB rating enhances investor confidence, signaling strong capital support and potential growth, despite economic pressures.

The post Ripple Prime earns BBB rating from Kroll, reflecting robust capital support and early profitability appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Bitcoin Price Continues Sliding as President Trump Signals Iran Escalation, Raising Risk of Drop Toward $60,000

Bitcoin price fell last night after President Donald Trump signaled a potential escalation in military action against Iran, triggering a broad pullback across global markets and raising questions about whether bitcoin price could test lower support levels.

The price of Bitcoin dropped nearly 4% within hours after Trump’s April 1 address, sliding to below $66,000 early April 2. The decline came as investors shifted away from risk assets following remarks that pointed to harder strikes in the coming weeks, with no timeline for de-escalation.

Equity markets also moved lower. The S&P 500 traded in negative territory, while Asia-Pacific equities reversed earlier gains. At the same time, oil prices surged, with Brent crude rising above $106 per barrel as traders priced in the possibility of prolonged disruption in the Strait of Hormuz, a key global shipping route.

The move highlights how closely Bitcoin price is tracking traditional markets during periods of geopolitical stress.

Data shows the 30-day correlation between Bitcoin price and the S&P 500 has climbed to around 0.75, indicating that institutional investors are treating the digital asset more like a high-growth technology proxy than a hedge.

Bitcoin price resilience

Bitcoin had shown some resilience in recent weeks, ending March with a modest gain and snapping a multi-month losing streak. However, it remains down roughly 45% from its prior peak above $126,000, and demand indicators suggest continued pressure.

JUST IN: Bitcoin has closed its first green month after 5 months of red

— Bitcoin Magazine (@BitcoinMagazine) April 1, 2026pic.twitter.com/jVMxXp9w2L

From a technical perspective, Bitcoin is now approaching a key support range between $64,000 and $65,000. The level has held through several recent tests, but a break below it could open the door to a move toward $60,000, near the February low, according to Bitcoin Magazine Pro data.

On the upside, resistance sits around $68,000 and $70,000. Analysts say those levels need to be reclaimed to shift sentiment and support a recovery narrative.

Until then, price action remains constrained by a pattern of lower highs that has developed since March.

Long-term holder data suggests the market may be moving through a late-stage bear cycle. Investors holding Bitcoin for six months or more now control about 80% of supply, approaching levels that have marked past market bottoms.

Even so, previous cycles indicate that extended periods of sideways trading often follow before a sustained recovery begins.

On top of this, Bitcoin treasury firms and public companies are offloading BTC as prices fall, adding fresh pressure to the market as long-term holders turn into sellers. Companies including Riot Platforms, MARA Holdings, and Genius Group have trimmed holdings this week to raise liquidity and service balance sheets.

For now, Bitcoin’s reaction to geopolitical developments underscores its current role within the broader macro environment.

As long as uncertainty around the Iran conflict persists, market direction may remain tied to shifts in risk sentiment rather than a return to the asset’s safe-haven narrative.

This post Bitcoin Price Continues Sliding as President Trump Signals Iran Escalation, Raising Risk of Drop Toward $60,000 first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Treasuries Are Cracking as Public Companies Turn into BTC Sellers

A wave of bitcoin selling from public companies and sovereign entities is adding pressure to the bitcoin market, as firms that once called themselves long-term holders sit on long-term losses and move to shore up balance sheets, repay debt, and fund strategic pivots.

Companies including Riot Platforms, Genius Group, and Nakamoto Holdings have all reduced their bitcoin holdings this week, citing liquidity needs and operational priorities.

The shift marks a drastic change from the accumulation trend that defined the past two years, when firms raced to build BTC treasuries during a period of rising prices.

Bitcoin HODL-ish

Empery Digital (EMPD) said it sold 370 BTC at an average price of $66,632, generating $24.7 million in proceeds. The company used part of the funds to repay its term loan and released about 1,800 BTC that had been held as collateral.

Following the sale, Empery holds 2,989 BTC, down from a peak position of about 4,000 BTC built after it began accumulating in July 2025. Its shares have fallen 75% from a 2025 high of $15.80.

Genius Group (GNS), an AI-focused education company that once held as much as 440 BTC, has exited its BTC position. The firm sold its remaining 84 BTC to repay $8.5 million in debt, completing a series of reductions that began earlier this year.

The company said it may rebuild its bitcoin treasury when market conditions improve.

Riot Platforms (RIOT), one of the largest publicly traded bitcoin miners in the U.S., has also been selling. Blockchain data tracked by Lookonchain indicates the company moved 500 BTC, worth about $34 million, to an exchange-linked address, suggesting a sale. This movement took place on April 1.

The transaction follows roughly $200 million in bitcoin sales in the final months of 2025, as Riot shifts capital toward artificial intelligence and high-performance computing infrastructure.

Other firms are merely tapping their holdings. Nakamoto Holdings (NAKA) sold 284 BTC for about $20 million in March, representing around 5% of its reserves.

The company said the proceeds will support working capital and operations following acquisitions tied to its bitcoin-focused strategy. Nakamoto reported a pre-tax loss of $52.2 million for 2025, driven in part by a decline in the value of its digital assets.

Marathon Digital (MARA) has taken one of the largest steps. The miner sold 15,133 BTC between March 4 and March 25 for about $1.1 billion. It used the proceeds to repurchase $1 billion in convertible notes due in 2030 and 2031, reducing outstanding debt by about 30%. The move lowered its holdings to 38,689 BTC from 53,822 BTC at the start of the year.

The trend extends beyond corporate treasuries. Bhutan has continued to reduce its BTC holdings, selling a total of 3,103 BTC. A single transaction on March 30 accounted for 375 BTC, according to Glassnode data.

The country had built its position through state-backed mining operations, reaching more than 13,000 BTC at its peak in October 2024.

Despite the recent selling, public companies still hold about 1.16 million BTC, or more than 5% of bitcoin’s fixed supply of 21 million, according to BitcoinTreasuries.net.

Bitcoin traded near $66,000 at the time of writing, down about 3% on the day.

Bitcoin Magazine is published by BTC Inc, a subsidiary of Nakamoto Inc. (NASDAQ: NAKA)

This post Bitcoin Treasuries Are Cracking as Public Companies Turn into BTC Sellers first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Metaplanet Surpasses MARA Holdings to Become Third-Largest Corporate Bitcoin Holder

Tokyo-listed Metaplanet has moved into the top tier of corporate bitcoin holders after acquiring 5,075 BTC during the first quarter of 2026, a purchase valued at roughly $398 million.

The company disclosed the acquisition on April 2, confirming the purchases were completed by March 31 at an average price between $78,000 and $79,898 per bitcoin. The latest accumulation brings Metaplanet’s total holdings to 40,177 BTC, pushing it past MARA Holdings, which holds about 38,689 BTC following recent sales tied to debt management.

MARA did recently sell 15,133 bitcoin for roughly $1.1 billion between March 4 and March 25 as part of a broader effort to restructure its balance sheet. The miner, which is expanding into digital energy and AI infrastructure, said the proceeds will be used to repurchase its 0.00% convertible senior notes due in 2030 and 2031.

Metaplanet now ranks as the third-largest publicly traded bitcoin holder, trailing Strategy with more than 762,000 BTC and Twenty One Capital with 43,514 BTC, according to bitcointreasuries.net.

Metaplanet is holding bitcoin at a loss

Despite the scale of its accumulation, the company is sitting on a paper loss. With bitcoin trading near $66,400 on the day of the announcement, the firm’s holdings carried a market value of about $2.67 billion, compared with an average cost basis near $97,593 per BTC. That gap implies an unrealized loss of about 32 percent.

Metaplanet has signaled it will continue buying. Chief executive Simon Gerovich has framed bitcoin as a long-term reserve asset suited to Japan’s inflation conditions and yen depreciation. The firm has maintained a steady acquisition pace since shifting to a bitcoin-focused treasury strategy in April 2024.

To fund purchases, Metaplanet relies on equity issuance, capital markets activity, and a growing bitcoin income operation. During the first quarter, the company generated about 2.97 billion yen in revenue from options strategies tied to its holdings. That income offsets acquisition costs and lowers the firm’s effective purchase price per bitcoin.

Metaplanet’s growth in bitcoin per diluted share

The company also raised capital twice during the quarter through share issuances and warrants sold to institutional investors. A January placement raised about 12.24 billion yen, followed by a March raise that brought in roughly 40.8 billion yen. Proceeds from both offerings were directed toward further bitcoin accumulation.

Metaplanet tracks performance through a metric it calls BTC Yield, which measures growth in bitcoin per diluted share. The company reported a BTC Yield of 2.8 percent for Q1 2026, a decline from 95.6 percent in the same period last year when dilution had a smaller impact on the ratio.

Metaplanet began accumulating bitcoin in April 2024 with less than 100 BTC. Holdings reached 1,761 BTC by the end of that year, then expanded to more than 30,000 BTC by September 2025. The latest quarter extends that trajectory as the company scales its treasury model.

The company has set a target of holding 210,000 BTC by the end of 2027, equivalent to about 1 percent of bitcoin’s fixed supply. Reaching that level would require sustained access to capital and continued execution of its income strategies.

Shares of Metaplanet closed at 302 yen, or about $1.89, on April 2, down about 2 percent on the day, in line with broader market movement.

This post Metaplanet Surpasses MARA Holdings to Become Third-Largest Corporate Bitcoin Holder first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Interactive Brokers Adds Bitcoin Trading in European Economic Area

Interactive Brokers has launched crypto trading for eligible retail investors across the European Economic Area, extending its digital asset offering through Interactive Brokers Ireland Limited, an authorized crypto-asset service provider.

The rollout gives users access to 11 digital assets, including Bitcoin, alongside equities, options, futures, currencies, bonds, and mutual funds within a single account interface.

The offering is enabled through an integration with Zero Hash, which provides backend crypto and stablecoin infrastructure for institutional platforms. The partnership expands an existing relationship between the two firms and opens access to a market of roughly 450 million people across the EEA.

Clients can trade these assets across Interactive Brokers’ platform suite, including Trader Workstation, IBKR Desktop, Client Portal, IBKR Mobile, and IBKR GlobalTrader.

The company said the integration allows investors to manage digital assets and traditional securities in one place. The platform provides a unified portfolio view and shared infrastructure for execution, risk monitoring, and capital allocation.

“Our clients want the flexibility to diversify into crypto-assets while maintaining the tools, pricing, and trust they rely on,” said CEO Milan Galik. He added that combining asset classes within one platform supports more efficient management of liquidity and portfolio exposure.

Interactive Brokers set commission rates between 0.12% and 0.18% of trade value. The firm said the service avoids spreads, markups, and custody fees, while allowing limit orders for price control. Crypto markets on the platform operate on a continuous basis, reflecting the 24/7 structure of digital asset trading.

Growing bitcoin offerings in Europe

The EEA expansion builds on existing crypto offerings in other regions. Interactive Brokers already provides digital asset trading in the United States through its domestic entity and in the United Kingdom through Interactive Brokers (U.K.) Limited.

The latest rollout marks a continuation of the firm’s effort to integrate crypto within its global brokerage framework.

The move comes as European regulators implement new digital asset rules that formalize licensing requirements for crypto service providers. By operating through its Irish affiliate, Interactive Brokers aligns its offering with regional regulatory standards while expanding product access for retail clients.

The firm said the launch addresses demand from investors seeking exposure to crypto markets without relying on separate exchanges or wallets. By consolidating asset classes under one platform, Interactive Brokers positions its brokerage model as a bridge between traditional finance and digital assets.

This post Interactive Brokers Adds Bitcoin Trading in European Economic Area first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

U.S. Treasury Launches First GENIUS Act Rulemaking With 87-Page Proposal

The U.S. Department of the Treasury has formally begun implementing the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, releasing its first notice of proposed rulemaking (NPRM) and opening a 60-day public comment period.

The 87-page proposal outlines how the Treasury will determine whether state-level stablecoin regulatory regimes are “substantially similar” to the federal framework—a key threshold allowing smaller issuers to remain under state supervision.

Under the GENIUS Act, stablecoin issuers with less than $10 billion in outstanding supply can opt for state-level regulation, provided those regimes meet or exceed federal standards. The proposed rule establishes broad principles to guide that determination, while leaving states flexibility in areas like licensing, supervision, and enforcement.

According to the document, the Treasury draws a clear distinction between “uniform requirements” — such as reserve backing and anti-money laundering compliance — and “state-calibrated requirements,” where local regulators retain discretion, including capital and risk management standards.

Notably, the proposal anchors the federal benchmark largely to rules and interpretations issued by the Office of the Comptroller of the Currency, signaling its central role in overseeing nonbank stablecoin issuers that transition to federal supervision after crossing the $10 billion threshold.

The rule also clarifies that state frameworks may exceed federal requirements, so long as they do not conflict with federal law or undermine overall comparability.

U.S. crypto legislation progress

The NPRM marks Treasury’s first formal step in translating the GENIUS Act — enacted in July 2025 — into an operational regulatory regime for payment stablecoins, with final rules expected after the public comment period closes.

State regimes would also be barred from weakening core disclosure standards, with issuers required to publish reserve composition reports at least monthly — matching federal frequency requirements.

Naming restrictions would similarly apply across both frameworks, preventing state-regulated issuers from using prohibited terms in stablecoin branding.

The proposal underscores that federal law remains the baseline, noting that any future legislation passed by Congress governing stablecoin issuers would automatically apply to state-regulated firms unless explicitly stated otherwise.

The 2025 passage of the GENIUS Act marked a turning point in U.S. crypto policy, establishing the first federal framework for stablecoins and requiring full reserve backing, AML compliance, and regular disclosures.

The law is widely seen as legitimizing dollar-backed stablecoins while reinforcing U.S. monetary dominance.

Since then, attention has shifted to implementation and follow-on legislation. Treasury reports issued under the GENIUS Act are expanding oversight tools, including measures targeting illicit finance and crypto mixers.

At the same time, disputes between banks and crypto firms, especially over whether stablecoins can offer yield, have slowed broader market structure efforts.

Meanwhile, Congress is advancing complementary bills like the Clarity Act to define SEC and CFTC jurisdiction, signaling a broader push toward a comprehensive regulatory framework for digital assets.

This post U.S. Treasury Launches First GENIUS Act Rulemaking With 87-Page Proposal first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

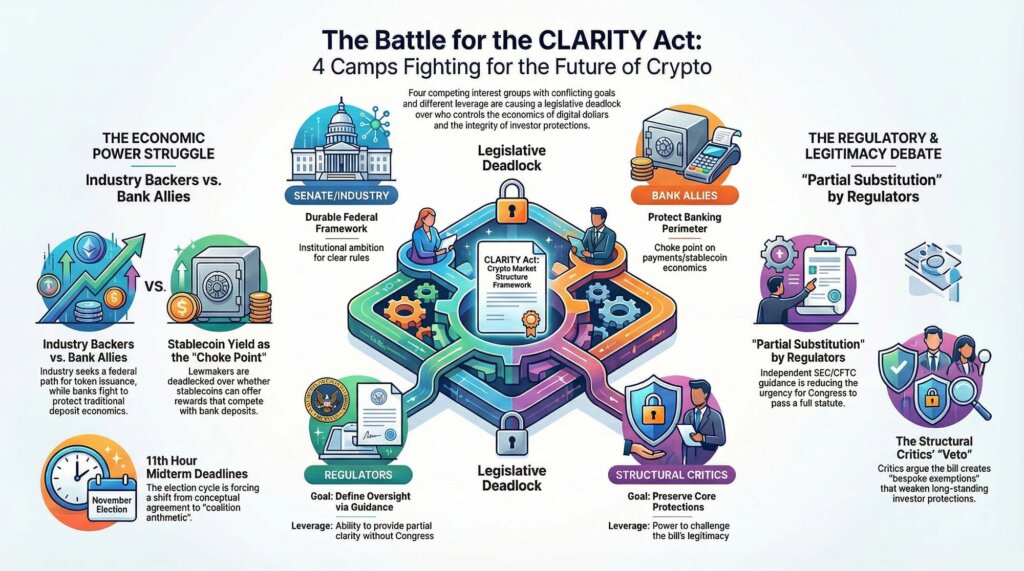

The CLARITY Act entered Washington as a bid to impose a durable market structure on crypto. It now sits at the center of a four-way fight over who gets to define that structure, who gets paid inside it, who supervises it, and how much of the existing financial rulebook survives the rewrite.

The bill still includes broad language for jurisdictional clarity, with the Senate Banking Committee majority outlining a framework that draws lines between the SEC and the CFTC while adding tailored disclosures and anti-fraud protections.

Around that frame, the coalition has fractured into four camps with different definitions of success. Senate and industry backers still want a federal market-structure bill that gives crypto firms a workable path into US regulation.

Bank-aligned critics want to seal off stablecoin yield and keep deposit economics from migrating out of the banking system. Regulators have begun moving through their own channels, with the SEC and CFTC signing a new memorandum of understanding and the SEC issuing a fresh interpretation of crypto assets that begins to deliver some of the clarity Congress had reserved for itself.

Structural critics still argue the bill would carve crypto out of core investor protections, a case advanced by groups such as Better Markets and by former CFTC Chair Timothy Massad in prior congressional testimony.

That collision changed the shape of the bill. What began as a question of statutory design has become a contest over bargaining power.

Each camp can slow the process, each camp can claim some version of consumer protection, and each camp enters the next phase with a different source of leverage. Senate and industry backers hold the broadest institutional ambition.

Why this matters: The CLARITY Act was intended to anchor crypto within US law, with clear rules for exchanges, tokens, and custody. If it stalls or narrows, firms remain in a patchwork regime shaped by enforcement and agency guidance, while banks retain tighter control over dollar-based financial activity. The outcome will determine whether crypto can compete directly with traditional deposits and payment rails, or operate inside a more constrained perimeter.

Banks and their allies hold a choke point around payments, economics, and stablecoin rewards. Regulators hold the power of partial substitution, because every piece of interpretive guidance from the SEC and CFTC narrows the pool of uncertainty that once made CLARITY the singular prize.

Structural critics hold a veto over the debate on legitimacy because their argument speaks to a long-standing Washington fear that crypto bills could create bespoke exemptions that would replace the exemptions older laws once carried.

The calendar tightened the pressure. In January, Senate Banking Chairman Tim Scott said the committee would postpone its markup while bipartisan negotiations continued.

Later that month, the Senate Agriculture Committee advanced related market-structure legislation, keeping momentum alive while underlining that the main bottleneck had shifted into the negotiating room.

By March, the fight over stablecoin rewards had become the central pressure point in the bill, with public reporting and congressional chatter converging on the same conclusion: a framework bill could move forward only if lawmakers found a way to reconcile crypto’s push for broader utility with banking concerns about disintermediation and deposit competition.

That left CLARITY in a familiar Washington posture, broad enough to attract coalitions in theory, specific enough to trigger fracture once the revenue lines came into view.

The first two camps are fighting over the economic core of the bill. The first camp still sees CLARITY as the vehicle that can finally anchor crypto market structure in federal statute.

That camp includes Senate Republicans who have spent months arguing that the industry needs rules written through Congress rather than through case-by-case enforcement, along with a large swath of the industry that wants a lawful path for token issuance, exchange activity, brokerage, custody, and participation in decentralized networks.

The core attraction has always been the same. A federal framework promises a clearer allocation of authority among agencies, a more predictable compliance process, and a narrower zone of ambiguity about what falls under securities law and what falls under commodities regulation.

The Senate Banking majority’s summary reflects that approach, leaning on the idea that a single framework can impose definitional order on a market that has spent years operating inside regulatory overlap.

For crypto firms, the appeal runs deeper than process. A statute holds out the prospect of capital formation under rules that institutions can underwrite, boards can sign off on, and legal teams can defend without having to rebuild the analysis around every enforcement cycle.

Yield politics turned CLARITY into a fight over the economics of digital dollars

The first camp’s ambition runs straight into the second camp, which has focused the fight around stablecoin yield and the economics of digital dollars. The Bank Policy Institute has made the bank-aligned position unusually plain.

Lawmakers, in that view, need to prevent stablecoin structures from recreating deposit-like products outside the traditional banking perimeter, especially if those products begin passing through rewards or yield that look and feel like interest. Under that logic, the danger is structural.

If tokenized dollars can offer returns or functionally similar incentives at scale, then commercial bank deposits face a new form of competition, payments activity migrates, and the prudential perimeter gets thinner exactly where regulators spent years trying to harden it. That is why the stablecoin rewards fight turned into the bill’s main choke point.

It is the place where market structure meets balance-sheet politics.

Those two camps can still describe their goals with overlapping language. Both can say they want consumer protection, operational integrity, and a framework that channels crypto activity into supervised forms.

The overlap ends when the discussion reaches who captures the economics created by digital dollars. The industry camp wants enough room for product development, distribution, and economic pass-through to make federally compliant crypto businesses worth building.

The bank-aligned camp wants a bright barrier around any feature set that could pull value from deposits into tokenized alternatives. That conflict reaches beyond one provision.

It shapes how lawmakers think about payments, exchange design, brokerage economics, wallet architecture, and the degree of freedom crypto firms would have to compete with institutions that already dominate dollar intermediation. Every concession made to one side tends to drain utility from the bill as imagined by the other.

The result is a negotiation whose formal subject is market structure and whose real center of gravity is control over monetary rails. That is why this phase of the CLARITY debate feels more compressed and more political than the earlier debate over jurisdiction.

Jurisdiction can be split in text. Economic control creates winners and losers with organized lobbies, committee relationships, and a direct financial interest in the final wording.

The first camp still wants a durable federal framework. The second camp wants that framework shaped tightly enough that it does not redraw the economics of digital money in a way that benefits crypto firms at the expense of banks.

Both camps can live with progress. Each one defines progress differently, and that difference is what keeps the bill from moving forward.

The third camp sits within the regulatory apparatus itself and introduced a fresh complication into the bill by moving ahead with practical coordination and interpretive guidance. On March 11, the SEC and CFTC announced a new memorandum of understanding designed to improve coordination on crypto oversight.

Days later, on March 17, the SEC issued a new interpretation clarifying how federal securities laws apply to crypto assets, with the CFTC aligning publicly with the effort. By March 20, the CFTC had added crypto-related FAQs that continued the same line of work.

Those actions did not write a statute, and they did not resolve every contested edge case, yet they changed the terrain around CLARITY in a way lawmakers can feel. Congress had been negotiating a bill designed to provide clarity.

Regulators started supplying pieces of that clarity themselves.

Regulators are shaping the field while structural critics keep the legitimacy fight alive

That shift created two immediate effects. First, it gave industry participants some of the operational breathing room they had been seeking, particularly regarding how certain crypto activities are analyzed through the lens of securities law.

Legal practitioners quickly seized on the importance of the change. In a March 19 analysis, Katten described the SEC and CFTC guidance as a major event for the sector, pointing to a more legible treatment of activities such as airdrops, mining, staking, and wrapping.

Second, the guidance changed congressional leverage. Every increment of clarity delivered through agency action reduces the urgency that once surrounded CLARITY as the exclusive route to order.

That creates a subtle but powerful dynamic. A bill under pressure usually gains energy from scarcity.

Once regulators start producing partial substitutes, lawmakers face a harder sell when they ask wavering factions to make politically costly concessions in the name of a breakthrough.

That shift does not weaken the case for statute across the board. A regulatory interpretation sits lower in the durability hierarchy than a congressional framework, and industry participants with long investment horizons still prefer statutory architecture to agency guidance.

Yet the third camp need not erase the case for CLARITY to affect the negotiation. It only needs to be shown that immediate passage is the only way to restore order.

That is already happening. The more the agencies coordinate, the easier it becomes for lawmakers to accept delay, narrower text, or a compromise version of the bill that settles the most acute fights while leaving some larger structural ambitions for another cycle.

For some senators, that can feel like prudence. For some industry players, it can feel like the center of the bill is being negotiated away in real time.

The regulatory camp also exerts pressure in a second way. It offers a political release valve.

Lawmakers who want to say Washington is making progress on crypto can point to the SEC and CFTC without forcing immediate resolution of every issue inside CLARITY. That lowers the cost of postponement and raises the threshold for what kind of final agreement is worth bringing to the floor.

A bill that once looked indispensable now has to demonstrate added value against the backdrop of agency-led adaptation. That is a difficult standard, especially for a coalition already carrying internal conflict over stablecoin rewards, federal preemption, DeFi treatment, and investor-protection language.

The fourth camp continues to ask the question that lies beneath every crypto bill in Washington: Does this framework integrate the sector into existing law, or does it carve out a special lane that weakens protections the rest of finance still carries?

That concern has animated groups such as Better Markets and has appeared in prior testimony from former CFTC Chair Timothy Massad, who argued that proposals such as CLARITY can create artificial distinctions between securities and commodities in ways that reduce the reach of investor protections.

This camp does not have to win the whole argument to shape the bill. It only has to keep the legitimacy challenge alive.

Once that challenge enters the center of the debate, every provision gets viewed through a second lens. A disclosure regime becomes a question about whether disclosure replaces stronger obligations.

A jurisdictional transfer becomes a question about whether oversight is being softened through classification. A pathway for token markets becomes a question about whether the path relies on exemptions that older sectors would never receive.

This is where the four camps collide most sharply. Senate and industry backers want a framework that firms can use at scale.

Bank-aligned critics want to close off yield dynamics that could pressure deposits and payments economics. Regulators are already showing that some clarity can emerge through agency action, reducing the pressure to accept a broad legislative bargain on weak terms.

Structural critics keep pushing on the question of whether the bill preserves the integrity of long-standing protections. A compromise that satisfies the first camp by preserving broad utility may alarm the second and fourth camps.

A compromise that satisfies the second and fourth camps by tightening the perimeter may leave the first camp with a framework that carries less strategic value. A compromise that leans heavily on regulator-led clarity may satisfy lawmakers seeking incremental progress while leaving industry participants with a less durable settlement.

That is why the final question has become a matter of coalition arithmetic rather than conceptual agreement. All four camps can say they want order.

Their conditions for the order point are in different directions.

Midterm pressure is turning a policy negotiation into coalition arithmetic

The midterm calendar sharpens every one of those contradictions. November imposes deadlines on attention, legislative bandwidth, and political appetite for complex financial legislation, generating cross-pressures within both parties.

As the calendar advances, the value of waiting rises for any camp that thinks the current bargain costs too much. Banks can wait if the alternative is stablecoin economics they dislike.

Structural critics can wait if the alternative is a framework they view as too permissive. Regulators can keep moving within their own lane.

Industry groups can keep arguing that delay carries a cost, yet that message weakens if the agencies continue to supply enough guidance to keep large parts of the market functioning.

The coalition that can pass CLARITY, therefore, needs more than a shared talking point around clarity. It needs a settlement that provides the first camp with enough usable structure, the second camp with enough protection around dollar economics, the third camp with a role that fits the statute rather than competes with it, and the fourth camp with enough assurance that core protections remain intact.

That path is narrow. It is still navigable, although the room for error has tightened.

A workable reconciliation would likely require lawmakers to frame the bill less as a maximal rewrite and more as a disciplined allocation of authority, paired with narrow guardrails on stablecoin rewards and stronger language on anti-fraud, disclosure, and supervisory obligations. Even then, the politics stay hard.

Each camp would have to accept a result that falls short of its preferred endpoint. The first camp would accept tighter limits than many crypto firms want.

The second camp would accept a federal framework that still gives compliant crypto business lines room to grow. The third camp would accept that agency guidance is a bridge into statute rather than a substitute for it.

The fourth camp would accept that integration can occur without dismantling the regulatory perimeter. Whether that bargain is possible before November is now the central test around CLARITY.

The bill can still move. The harder question is whether these four camps can converge on a version of movement that each side can live with once the votes are counted.

The post A four-way deadlock is now blocking the US Clarity Act crypto bill — and each side can stop it appeared first on CryptoSlate.

Bitcoin spent the past 24 hours returning to the key levels on my channel map rather than continuing its breakout. It tested a boundary, failed to convert that test into acceptance, and rotated lower into the next pocket of support memory.

Bitcoin price slid from the upper $68,000s and low $69,000s to around $66,400 by late morning in Europe on April 2. The 24-hour move came in at roughly 3%, with the high near $69,170 and the low near $66,218.

Over 48 hours, the net change stayed close to flat, yet the path inside that window shifted the balance of the chart lower. Price gave up the white shelf near $66,894, rejected a retest, and left the market trading beneath a level that had previously held the local structure together.

Why this matters: What changed is not just the price move but the level it broke. Bitcoin lost a support zone that had been holding the recent structure together, and failed to reclaim it on the first retest. At the same time, the dollar and oil moved higher together, a combination that tends to pressure liquidity and risk appetite. That pairing raises the bar for any immediate recovery and puts the next lower support zones back into focus.

That pattern sits squarely inside the 2024 channel framework, first laid out in Bitcoin channel predictions, aligning with market movements over 6 months. The premise was simple and practical.

Repeating close prices on the 30-minute chart can identify where leverage, stop placement, and spot liquidity tend to cluster. Those shelves have kept showing up at the turning points.

They have framed rebounds, capped rallies, and guided the path between them with more consistency than many of the more elaborate narratives built around Bitcoin.

The last two days developed in three steps. First, Bitcoin spent time in the upper half of the near-term range, pushing back toward the yellow boundary near $67,995.

Second, the move stalled before any real acceptance could build above that shelf. Third, the chart rolled over sharply and carried price through the white line at $66,894 before finding a temporary footing in the mid $66,000s.

That sequence shows where control sits right now. Buyers still have a path back into the range, though that path starts with repair.

Price needs a reclaim of $66,894, then a push back through $67,995, before the structure looks constructive again.

Bitcoin lost the shelf it needed to hold, and the near-term structure turned lower

The same logic that led Bitcoin to fail 7 times to break $71,500. Repeated failure at a level adds weight to the next test.

A ceiling becomes a lid when sellers step down and meet price earlier, and a floor becomes vulnerable when buyers lose the urgency to defend it on first contact. In that February piece, the key level was $71,500, with the next friction zones above at around $72,000 and then $73,700 to $73,800.

Below, I flagged the same shelves visible on the current chart: $68,000, then $66,900, with deeper support in the low $61,000s. That ladder remains intact today.

The difference is that Bitcoin has now moved one rung lower.

The practical sequence is straightforward. The market had room to recover while it held above the white shelf.

Once it lost that level and failed the retest, the burden shifted to buyers to prove that the drop was a flush rather than a new acceptance at a lower level. So far, the rebound has lacked authority.

A brief pop back toward the broken shelf printed the kind of weak retest that usually accompanies a market still under pressure. The candles after the drop look smaller, the bounce looks labored, and the range compression is taking place under resistance rather than above support.

The 24-hour numbers reinforce that view. Bitcoin fell around 3.02% from the close 24 hours earlier, while the 48-hour change stayed only marginally positive.

That combination often appears when a market has spent one day building a base and the next day giving it back. In other words, the chart preserved the wider range while damaging the near-term structure.

For a general audience, that distinction keeps the analysis anchored to thresholds rather than emotion. The market remains inside a ladder of known shelves.

It has moved from one shelf to the next. The immediate job for bulls is to recover $66,894, then $67,995.

The immediate risk for anyone leaning bullish is that continued trading below those levels draws attention to the lower white boundary around $61,726.

That lower target should already be familiar from my original channel work, where the channels were built to identify support and resistance rather than force a single directional call. It also lines up with the roadmap in “Bitcoin to $73k? Be prepared with the price levels to watch during a bear market“, where the key point was to treat lower shelves as historical liquidity pools.

The chart here fits that framework closely. Bitcoin is trading beneath a broken support shelf, and the next meaningful repair level sits above the current price.

Until that changes, the burden of proof remains on the upside.

Support memory still follows the same channel logic that shaped the earlier calls

These levels have held up well because they are built from where the market repeatedly closed, paused, and built positioning. Some zones carry memory because they spent hours or days there.

Other zones looked dramatic on the way up or down, yet offered weaker support because Bitcoin moved through them quickly, and the market built less inventory there.

That distinction shaped my October 2024 analysis in “Above the all-time high of $73.7k these could be the new resistance levels to watch”, where I argued that Bitcoin was trading at the top of a core price channel between $67.9k and $71.5k and that the zone between $71.5k and $73.7k had relatively little historical price action.

The implication was clear. Above the well-traded shelf, the market entered thinner territory where movement could become more abrupt.

The same logic applied later on the downside. In “It’s foolish to pretend Bitcoin’s story doesn’t include $79k this year”, I described the green band around $79,000 as a more substantial region because Bitcoin had spent time consolidating there during earlier legs of the cycle.

Below that sat the deeper structural supports in the red and blue channels, roughly $49,000 to $56,000, the area Bitcoin defended repeatedly before the move toward six figures. Then, in “Akiba’s medium-term $49k Bitcoin bear thesis – why this winter will be the shortest yet“, I framed $49,000 as a cyclical support case tied to miner stress, fee share, hashprice, and ETF flow elasticity.

Those longer-horizon calls operate on a different scale than the current 30-minute move, though they all rely on the same discipline: identify the shelf, assess how well the price is holding it, and define the next level that becomes relevant when it breaks.

The current move fits that sequence cleanly. Bitcoin approached the lower yellow boundary near $67,995 and could not hold it.

It then slid beneath the white shelf near $66,894. A 30-minute breakdown candle early on April 2 accelerated the move from the high $68,000s into the upper $67,000s, and follow-through selling pulled the price down toward the low $66,000s.

Once there, the market printed a small rebound and then drifted sideways beneath broken support. That behavior usually signals a market still negotiating lower inventory rather than preparing for an immediate reversal.

Anyone following the latter channel work through the six-figure phase will recognize the same design principle in “Bull or Bear? Today’s $106k retest decided Bitcoin’s fate” and “Bitcoin price next move: $92k or $79k? Let’s break it down”. The exact prices changed as Bitcoin moved through new territory, yet the method stayed the same.

A retest that holds opens the next band. A retest that fails hands control to the lower shelf.

The current chart falls into the second category. Price still sits below the broken shelf, which keeps the lower ladder in play.

Dollar strength and higher oil arrived at the same time as the breakdown, leaving reclaim levels above and deeper support below

The broader market context over the last 24 to 48 hours adds another layer to the chart. Alongside Bitcoin moving lower, the comparison view showed the U.S. Dollar Index rebounding above 100 while Brent crude pushed toward $108.

That combination tightens conditions around risk assets. A firmer dollar usually weighs on global liquidity at the margin, and higher oil prices can amplify inflation concerns, rate sensitivity, and geopolitical caution.

Bitcoin tends to trade with greater friction when both markets are moving in the same direction, against a softer risk backdrop.

That setting sits comfortably inside the framework of the later channel pieces. In the $79k piece, I wrote that liquidity could become the problem if ETF outflows intensified and risk appetite faded.

In the $49k bear thesis, I argued that negative 20-day ETF flows, alongside weaker miner economics, would increase the probability of sharper downside legs. In the seven failures at $71,500 analysis, I pointed to a macro environment where yields remained high enough to keep conditions tight.

The current move reflects that same type of pressure from a shorter time frame; a structurally important shelf gave way while the macro backdrop offered little relief.

For the practical map, the levels now do the heavy lifting. Resistance begins with $66,894, then expands to $67,995.

If Bitcoin regains both and spends time above them, the near-term damage begins to heal, and the next higher levels come back into view: $71,523, then $72,017, then the pair around $73,519 and $73,764, and then the upper extension near $77,056. Those higher levels are already familiar from the price discovery work above the old all-time high.

Support begins with the intraday low in the low $66,000s, though the stronger structural memory sits much lower, near $61,726. That leaves Bitcoin in a narrow but important condition.

It is close enough to reclaim broken support if buyers return with urgency, and close enough to invite a deeper sweep if they do not.

The conclusion remains the same one the chart has been offering since these channels were first drawn in early 2024. Bitcoin respects shelves until one gives way, and when one breaks, the next shelf tends to become the destination.

Over the last 24 hours, Bitcoin lost the shelf it needed to hold to keep the bounce credible. Over the last 48 hours, it preserved the wider range while shifting the short-term structure lower.

The next move now hinges on whether the price can climb back above $66,894 and $67,995 quickly enough to change the feel of the chart. Failing that, the lower white boundary near $61,726 moves back into focus as the next serious test on the ladder.

The post Bitcoin breaks critical support as dollar and oil move together, raising risk of a deeper drop appeared first on CryptoSlate.

Treasury's first proposed GENIUS rule landed on April 1 as a notice of proposed rulemaking.

The text inside it builds the operational architecture for US stablecoin governance, addressing which institutions may issue payment stablecoins, under what conditions, and at what scale before federal oversight becomes mandatory.

Why this matters: This shifts stablecoins from a fragmented regulatory patchwork toward a nationally coordinated system. For users, it affects how safely dollars can be redeemed and moved. For issuers, it defines whether they can scale independently or must transition into a federal regime as they grow.

By defining when a state licensing regime qualifies as “substantially similar” to the federal framework, Treasury is now defining those terms.

The stablecoin market already holds roughly $316 billion, with USDT accounting for about 58% of the supply, per DeFiLlama.

Retail-sized volume for USDC, USDT, and PYUSD grew from $500 million to $69.8 billion between 2019 and 2025. FSOC's 2025 annual report described the GENIUS framework as a federal prudential system designed to onshore stablecoin innovation, protect holders in the event of insolvency, and support the US dollar's international role.

Treasury's NPRM now shows how that prudential vision operates on the ground.

The hidden fight over who governs

The Treasury chairs the interagency review committee that certifies state stablecoin regimes, which includes leadership from the Fed and the FDIC.

That committee's judgment rests on the “substantially similar” test, and Treasury's proposal defines that test to include the GENIUS Act itself, as well as the implementing regulations and interpretations issued by federal agencies over time.

Treasury says that substantial similarity would be hard to administer, and state and federal standards could “starkly deviate.”

As OCC, Treasury, the Fed, FinCEN, and OFAC add implementing rules, the standard Washington uses to measure states shifts with them. State regimes approved today must track a benchmark that Washington keeps building.

Treasury organizes the rule around two categories. The first, called uniform, covers the parts that establish trust in the instrument itself: reserve assets, redemption, monthly reserve publication, limits on rehypothecation, accountant examinations, BSA/sanctions compliance, lawful-order capability, and core activity limits.

State implementation of each uniform requirement must be consistent with the federal framework “in all substantive respects,” with no material deviations in definitions or scope. For BSA and sanctions specifically, states must cross-reference federal rules directly, with no room for state-drafted substitutes.

The second category allows calibration around some capital, liquidity, reserve diversification, risk management, applications, licensing, and certain redemption mechanics. Treasury still constrains that room, and state choices in the flexible bucket must produce outcomes “at least as stringent and protective” as the federal framework.

For example, a state may allow additional reserve assets only if the OCC has already approved them as similarly liquid federal government-issued assets. That is federal pre-clearance administered through state paperwork.

| Category | Requirement area | Treasury standard | State discretion | Why it matters |

|---|---|---|---|---|

| Uniform | Reserve assets | Must align with the federal framework in all substantive respects | No material deviation | Defines trust in the stablecoin itself |

| Uniform | Redemption | Must track the federal baseline closely | No narrower state substitute | Protects holders’ ability to redeem |

| Uniform | Monthly reserve publication | Must match federal expectations | Very limited room to vary | Supports transparency and market confidence |

| Uniform | Limits on rehypothecation | Must conform to the federal framework | No meaningful carve-out | Prevents riskier use of backing assets |

| Uniform | Accountant examinations | Must be consistent with federal requirements | Little to no variation | Standardizes verification of reserves |

| Uniform | BSA / AML / sanctions | States must cross-reference federal rules directly | No state-drafted alternative | Keeps compliance under national control |

| Uniform | Lawful-order capability | Must track federal expectations | Minimal discretion | Preserves enforcement and legal access |

| Uniform | Core activity limits | Must align with the federal framework | No material divergence | Keeps issuers inside a nationally defined model |

| Flexible / calibrated | Capital | Outcomes must be at least as stringent and protective as the federal framework | Some calibration allowed | Lets states tune prudential standards without weakening them |

| Flexible / calibrated | Liquidity | Must be at least as protective as the federal baseline | Some calibration allowed | Gives limited room for state tailoring |

| Flexible / calibrated | Reserve diversification | May vary, but only within outcomes at least as protective as the federal framework | Narrow flexibility | States can adjust, but not create a looser reserve regime |

| Flexible / calibrated | Risk management | State framework can differ in form | Must still meet protective federal-equivalent outcomes | Allows administrative variation, not a different philosophy |

| Flexible / calibrated | Applications / licensing | State administration is allowed | Cannot create a genuinely different regime | Keeps the state lane administrative, not alternative |

| Flexible / calibrated | Certain redemption mechanics | Some room to calibrate | Must remain at least as protective as the federal system | States can adjust process, not weaken substance |

| Flexible / calibrated | Additional reserve assets | Allowed only if the OCC has already approved comparable assets | Federal pre-clearance still governs | Shows state flexibility is still bounded by Washington |

The $10 billion ceiling and what it produces

The GENIUS Act caps the state option at issuers with no more than $10 billion in consolidated outstanding payment stablecoins.

Treasury adds that state transition rules cannot impede a move to federal oversight once an issuer crosses that line, and issuers in a state that fails certification must either stop issuing payment stablecoins or move into the federal licensing framework.

The $10 billion ceiling is the structural tell, since the state lane functions as an entry point for smaller issuers. At scale, the federal framework becomes the only durable home.

Citi's updated 2026 forecast puts its base-case estimate for the 2030 stablecoin market at $1.9 trillion. Standard Chartered projected the market could reach $2 trillion by the end of 2028.

A market at that scale runs on uniform reserve, redemption, and compliance standards and rewards issuers capable of absorbing national-style regulatory overhead.

Visa's concentration data already reflects the current destination: as of October 2025, more than 97% of the stablecoin supply had converged on USDT and USDC. Treasury's design standardizes the conditions that large, compliant issuers are already built to meet.

Standard Chartered estimated stablecoins could pull roughly $500 billion in deposits out of US banks by the end of 2028.

The number frames the context correctly: stablecoins are becoming claims on dollar liquidity that sit alongside traditional bank deposits, and the institution that governs the terms of stablecoin issuance governs an expanding piece of dollar infrastructure.

Treasury's proposal positions Washington as that institution.

| Scale marker | Amount | What it represents | Regulatory implication | Why it matters |

|---|---|---|---|---|

| State-lane ceiling | $10 billion | Maximum consolidated outstanding payment stablecoins for an issuer to remain in the state option | Above this line, the issuer must transition to federal oversight or stop issuing new payment stablecoins | Shows the state path is a limited entry lane, not the durable home for large issuers |

| Current stablecoin market | ~$316 billion | Approximate current total stablecoin market size | The market is already far larger than the state-lane threshold | Suggests Treasury is designing rules for a systemically meaningful market, not a niche one |

| Citi base case (2030) | $1.9 trillion | Citi’s updated 2026 base-case estimate for the stablecoin market by 2030 | A market at this scale would likely rely on uniform national standards rather than fragmented state variation | Reinforces the article’s argument that scale points toward federalization |

| Standard Chartered forecast (end-2028) | $2 trillion | Standard Chartered’s projection for stablecoin market size by the end of 2028 | Implies that if growth continues, large issuers will almost inevitably end up in the federal framework | Supports the view that the state lane functions more like a launch ramp than a long-term alternative |

| Bank deposit migration estimate | ~$500 billion | Standard Chartered estimate of deposits stablecoins could pull from U.S. banks by end-2028 | Stablecoin issuance becomes a question of dollar-system governance, not just crypto regulation | Helps mainstream readers see this as a financial-architecture story, not a niche policy update |

Two paths through the same architecture

The bull case runs from clarity to scale. Uniform national rules on reserves, redemption, and compliance remove the uncertainty that has kept banks, card networks, and enterprise treasury teams cautious about deep integration with stablecoins.

Along that path, supply tracks toward the Citi and Standard Chartered forecasts, Visa's 130-plus card programs are overlaid on stablecoin wallets, and the state lane serves as a launch ramp for smaller issuers before they graduate to federal supervision.

Treasury's tight architecture then reads as the operating manual for US digital dollar expansion, which is a framework that made the market credible enough to absorb institutional demand at scale.

The bear case runs the same architecture in reverse. The forthcoming BSA/AML and lawful order rules, which both Treasury and the OCC have flagged as still pending in separate rulemakings, could entail heavy operational requirements.

If certification proves slow, costly, or politically fraught, smaller issuers may find the state lane functionally inaccessible even before they approach the $10 billion threshold.

The result would be a market that is legally cleaner but structurally oligopolistic, with innovation relocating to distribution and infrastructure, away from issuance.

Treasury frames a different goal. The predictable market response to high uniform compliance floors and a hard ceiling on state-lane scale is concentration, and Visa's existing market data shows the market was already moving in that direction before the rule arrived.

Washington holds the baseline

This NPRM is part of a larger regulatory framework. OCC's February proposal covered the required GENIUS regulations, except those tied to BSA, AML, and OFAC sanctions, which will be addressed in a separate rulemaking coordinated with Treasury.

Treasury's own NPRM flags that rules on lawful-order compliance are forthcoming as well. The full compliance map for stablecoin issuers awaits completion.

The $316 billion market and $10 trillion transaction volume settled the question of stablecoins belonging in the US finance. Treasury is deciding who gets to shape them as they enter it.

The first proposed GENIUS rule makes the answer clear: Washington accepts state participation in stablecoin issuance within a federal architecture that the Treasury continues to build, on Washington's terms.

The post US Treasury’s first GENIUS rule now redraws who controls stablecoins at scale appeared first on CryptoSlate.

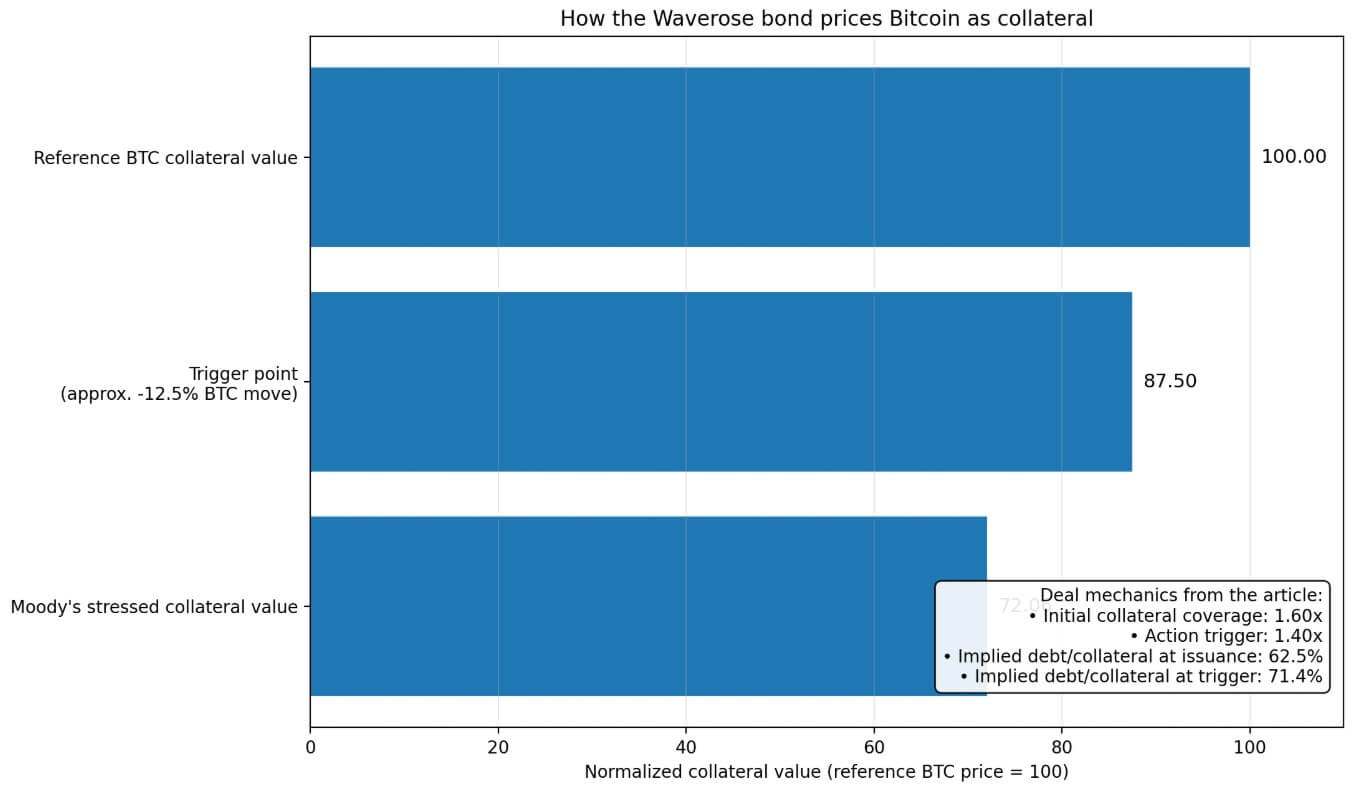

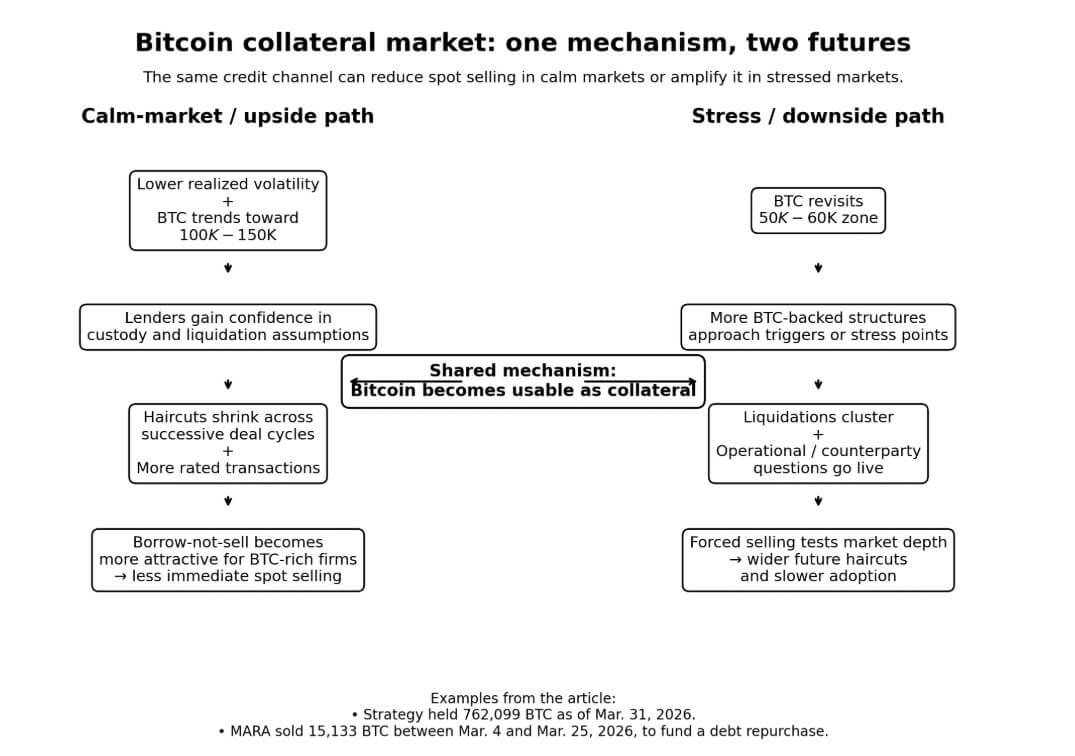

On Mar. 31, Moody's assigned provisional Ba2 ratings to up to $100 million in taxable revenue bonds for the Waverose Finance Project. The bonds are secured by a loan to NH CleanSpark Borrower Trust 2026-1, with Bitcoin (BTC) as the pledged collateral.

Those numbers set the conditions under which traditional finance agreed to work with Bitcoin at all: 72.06 cents of credit for every dollar of collateral value, a two-day exposure window to act on price moves, and 1.60x initial collateral coverage, which forces action when it drops to 1.40x.

Bitcoin has spent years auditioning for legitimacy as a store of value, a corporate treasury reserve, and an ETF asset. The New Hampshire deal points to Bitcoin as collateral.

Collateral is where an asset earns credit utility, something institutions can borrow against inside structures that credit markets can understand, price, and, when necessary, liquidate fast. That is the line Bitcoin just crossed.

Why this matters: This is the first time Bitcoin has been formally translated into credit terms that public markets understand. Instead of being held or traded, BTC is now being assigned a borrowing value, a liquidation threshold, and a stress price, turning it from an asset into usable financial collateral. That shift opens a new source of liquidity for holders, but also introduces a system where price drops can trigger automatic selling across multiple structures at once.

The opening price of trust

The Waverose structure is a taxable conduit revenue bond.

New Hampshire’s role ends at the conduit, and bondholders carry all loss risk. This is limited-recourse, institutional plumbing.

Two things follow from that structure. First, it keeps risk quarantined: if the collateral breaks down, bondholders absorb the loss. Second, it lays out the precise terms on which traditional finance decided Bitcoin could enter the credit system.

At 1.60x initial collateral coverage, the bond starts with debt equal to about 62.5% of collateral value. The 1.40x trigger, at which automatic action kicks in, implies a debt of roughly 71.4%.

The structure hits its wire trip when BTC falls by approximately 12.5% from issuance pricing, a move Bitcoin has executed routinely.

Moody's stressed the collateral value at 72.06% of the market price. Mapped to Bitcoin's Apr. 1 price in the $68,000 zone, the stress zone lands near $49,600.

Standard Chartered put its near-term bear case for Bitcoin at $50,000, and the traditional finance firms calibrated their first public finance haircut on Bitcoin almost exactly on top of a downside path that one of the world's largest banks still considers reachable.

From owned to pledged

New Hampshire arrived alongside two other recent moves pointing in the same direction.

In February, S&P assigned the first-ever rating to a structured finance transaction backed by Bitcoin. The transaction was the Ledn Issuer Trust 2026-1, with roughly $199.1 million in loans secured by 4,078.87 BTC, carrying a fair market value of approximately $356.9 million, implying an LTV of about 55.8% at inception.

In March, Better and Coinbase launched what they called the first crypto-backed conforming mortgage, in which a borrower pledges $250,000 in BTC to fund a $100,000 down payment, while the first lien stays Fannie Mae-backed.

Bitcoin received three credit wrappers in roughly six weeks, each with different haircuts, liquidation mechanics, and regulatory constraints. Together, they describe a process in which Bitcoin enters credit markets through multiple doors at once, and those doors are edging closer to ordinary household finance.

| Structure | Date | Wrapper type | Collateral / pledge | Haircut / Lationale | Who bears risk | Why it matters |

|---|---|---|---|---|---|---|

| Waverose / New Hampshire | Mar. 31, 2026 | Taxable conduit revenue bond | Bitcoin pledged as collateral for bonds secured by a loan to NH CleanSpark Borrower Trust 2026-1 | Moody’s stressed collateral at 72.06% of market value; 1.60x initial collateral coverage; action triggered at 1.40x; implied debt-to-collateral starts around 62.5% and rises to 71.4% at trigger | Bondholders absorb losses if collateral fails; no New Hampshire public funds pledged | Shows Bitcoin entering public-finance-adjacent credit as rated collateral, not just as an owned asset |

| Ledn Issuer Trust 2026-1 | February 2026 | Structured finance / ABS | Roughly $199.1 million in loans secured by 4,078.87 BTC with fair market value of about $356.9 million | About 55.8% LTV at inception | Investors in the structured-finance deal; risk tied to collateral, operations, and liquidation mechanics | Marks Bitcoin’s entry into rated structured finance |

| Better / Coinbase mortgage product | March 2026 | Crypto-backed conforming mortgage / down-payment loan | Borrower pledges $250,000 in BTC to obtain a $100,000 loan for a home down payment, while the first lien remains Fannie Mae-backed | Example implies a 40% advance rate on pledged BTC | Risk sits with the crypto-backed loan structure, while the first mortgage remains separately conforming/Fannie-backed | Pushes Bitcoin collateral closer to household finance and mainstream mortgage plumbing |

The US municipal market carried $4.4 trillion in outstanding bonds as of the fourth quarter of 2025. Households held 48% directly and about 21% through mutual funds.

Munis occupy a specific psychological slot in American savings culture, sitting where advisors park money for clients who want safety adjacent to tax efficiency.

The Waverose bond lands in the taxable conduit corner. Taxable muni issuance ran only about $33 billion in 2025, less than 6% of the market total. At $100 million, this deal represents roughly 0.0023% of the outstanding muni market.

One mechanism for two potential futures

For Bitcoin holders and treasury-heavy firms, collateral utility cuts in opposite directions depending on where the price goes.

Strategy held 762,099 BTC as of Mar. 31. Between Mar. 4 and 25, MARA sold 15,133 BTC for about $1.1 billion to fund a debt repurchase, which were outright spot sales to cover a balance sheet obligation.

A functioning BTC-collateral market sits between the two postures of full accumulation and outright liquidation, while providing credit against reserves that lets holders raise capital while keeping their Bitcoin position.

Fidelity noted in March that public companies and ETFs together hold roughly 12% of Bitcoin's circulating supply, and that 2025 was Bitcoin's least volatile year on record, based on annualized realized volatility.

If that holds and Bitcoin trades toward the $100,000-$150,000 range Bernstein projected for late 2026, the collateral channel becomes genuinely attractive. BTC-rich firms carry large reserves at lower realized volatility, lenders build confidence in liquidation assumptions, and the haircut required to access credit shrinks across successive deal cycles.

Each rated transaction adds data to Bitcoin's nearly empty track record as pledged collateral. A second deal, a third, a cluster, and the pricing of trust starts to compress.

The bear case runs through the opposite direction of the same mechanism. Bitcoin revisiting $50,000, near Standard Chartered's downside projection and close to the Moody's stress zone from current prices, turns the operational question live.

Firms start to wonder whether the liquidation mechanics work cleanly when every BTC-backed structure needs to exit at once.

S&P's rating work on the Ledn ABS flagged operational and counterparty risk, event risk, and liquidation mechanics as the core uncertainties for Bitcoin-backed credit. It noted the market's ability to absorb forced selling from multiple structures tripping triggers inside the same price window.

A structure that reduces forced selling in calm markets can concentrate it in turbulent ones. That is the inherent geometry of collateralized credit, and Bitcoin's volatility makes the geometry sharper than it would be for any conventional pledged asset.

The first version of Bitcoin-backed public finance is small, speculative-grade, and built for taxable conduit territory. The architecture is constrained because those constraints were the only terms on which the credit system would engage.

What Moody's released on Mar. 31 was a pricing schedule for Bitcoin's entry into credit markets: the conditions under which bond investors set for accepting it as collateral.

Future deals will be negotiated on that schedule, tightening haircuts if volatility falls, widening them if it rises, testing different custody arrangements, and pushing toward the investment-grade boundary.

Each iteration adds institutional memory to a market that currently has almost none.

Bitcoin took years to become something institutions could buy through regulated channels. Becoming something they can lend against will follow the same logic of incremental, conditional growth, built on an accumulating track record.

The post Moody’s prices Bitcoin at a 28% haircut — and sets the trigger for forced selling appeared first on CryptoSlate.

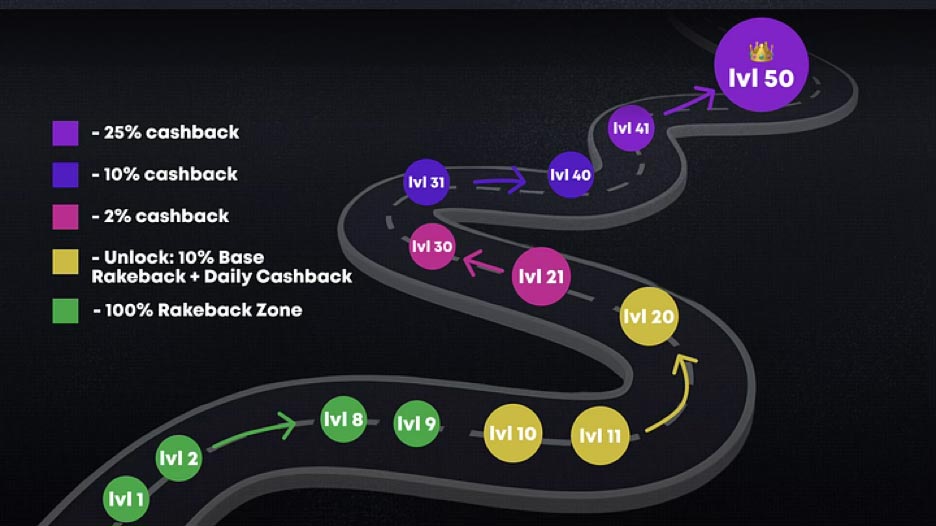

The core change is a 100% rakeback mechanic applied to the first nine loyalty levels. During this introductory window, which covers up to $1,000 in cumulative wagers, the platform returns the entirety of its house margin to the player. The expected casino profit during this phase is effectively zero, with Rakebit covering the cost as a user acquisition incentive.

Once players advance past Level 9, the system transitions to a permanent 10% base rakeback paired with daily cashback rewards. Cashback begins at 2% and increases through the remaining tiers, reaching a maximum of 25% at the highest levels.

The redesigned progression curve addresses what the platform described as issues with the previous model, where early levels progressed too slowly and top-tier players reached the cap prematurely. The expanded 50-level structure distributes rewards more evenly across the full player lifecycle.

Rakebit casino continues to operate without mandatory identity verification, supporting account registration via email, Google, Telegram, or X. The platform accepts over 30 cryptocurrencies and maintains a catalog of more than 7,000 games from established providers including Pragmatic Play, Hacksaw, NetEnt, and Red Tiger. Sixteen in-house titles use provably fair mechanics with RTP up to 99%.

The rakeback promotion requires no activation code and applies automatically to every new account upon first deposit.

Key Updates in Loyalty System v2

- Loyalty tiers expanded to 50 (previously 20)

- Full rakeback across levels 1–9, up to $1,000 wagered

- House edge reduced to zero during introductory progression

- Permanent 10% rakeback unlocked at level 10

- Daily cashback scaling from 2% to 25% based on tier

- Over 7,000 third-party games and 16 provably fair originals

- Support for 30+ cryptocurrencies

- No identity verification required for account creation

Disclaimer: This was a sponsored post brought to you by Rakebit.

The post Rakebit Upgrades Rewards Program to 50 Levels, Offers Full Rakeback on First $1,000 Wagered appeared first on CryptoSlate.

Cryptoticker

Bitcoin ($BTC) plummeted below the critical $66,000 threshold on April 2, 2026. This sudden downward movement has sent shockwaves through the derivatives market, resulting in the liquidation of over $251,940,000 worth of long positions within the last 24 hours.

Why is Bitcoin Dropping Today?

The current decline is fueled by a "perfect storm" of fundamental and technical factors. Reports indicate that rising geopolitical tensions in the Middle East and a hawkish shift in U.S. trade policy—specifically recent tariff announcements—have pushed investors toward a "risk-off" stance.

Furthermore, institutional demand through spot $Bitcoin ETFs has cooled significantly. Data shows net outflows exceeding $170 million in recent sessions, suggesting that the aggressive buying pressure seen in previous months is tapering off. This lack of immediate demand has left the market vulnerable to the "long squeeze" we are currently witnessing.

Bitcoin Price Analysis: Why is Bitcoin Down?

Analyzing the 4-hour chart of BTC/USD, several bearish signals are evident that traders should monitor closely.

1. The Descending Resistance Line

A prominent yellow trend line (descending resistance) has been capping Bitcoin's price action since mid-March. Every attempt to break above this line has been met with aggressive selling pressure. As of April 2, Bitcoin remains trapped beneath this diagonal resistance, currently situated near the $67,500 – $68,000 zone.

2. Immediate Support Levels

Bitcoin is currently testing a horizontal support zone identified on the chart at $65,581.

- Crucial Support: The $65,500 – $65,800 range is acting as the primary line of defense for bulls.

- Secondary Target: If $65,500 fails to hold, the next significant psychological and technical floor is at $63,000.

3. RSI and Momentum

The Relative Strength Index (RSI) is currently hovering around 38.02. This indicates that while the market is approaching "oversold" territory (typically below 30), there is still room for further downside before a relief bounce becomes a high-probability event. The momentum is clearly in favor of the bears in the short term.

| Metric | Value (Approx.) |

|---|---|

| Current Price | $65,879 |

| 24h Liquidations | $251.94 Million (Longs) |

| Major Resistance | $67,500 |

| Primary Support | $65,581 |

| RSI (14) | 38.02 |

Market Sentiment and Liquidation Heatmap

The $251 million in long liquidations suggests that many retail traders were positioned for a breakout that failed to materialize. When these positions are forcibly closed (liquidated), it adds "sell-side" pressure to the market, often leading to a cascading effect where the price drops further, hitting more stop-losses.

According to data from CoinGlass, the majority of these liquidations occurred on major exchanges like Binance and OKX.

Bitcoin Future Outlook: Bull Trap or Consolidation?

The big question is whether this is a "healthy correction" before a move toward $100,000 or the start of a deeper bearish phase. For a bullish reversal to be confirmed, Bitcoin must:

- Hold the $65,500 support on a daily closing basis.

- Break out above the yellow descending trend line with significant volume.

- Reclaim $70,000 to shift the narrative back to a positive bias.

Safe Havens Are Failing — What’s Happening Right Now?

Global markets are entering an unusual phase where traditional safe havens are no longer behaving as expected. Despite escalating geopolitical tensions and ongoing military threats involving Iran, assets like gold and silver are declining instead of rising.

Silver has dropped below $70, losing nearly 7–8% in a single day, while gold has fallen under $4,600, wiping out over $1 trillion in market value. At the same time, oil prices are surging above $100, reflecting growing fears of supply disruptions.

Meanwhile, crypto markets are also under pressure, with Bitcoin struggling to hold key levels and altcoins seeing sharper declines.

👉 This is not a normal market reaction.

Why Gold and Silver Are Dropping During a War

In a typical risk-off environment, investors rotate into safe-haven assets like gold. However, this time the opposite is happening.

The reason lies in inflation expectations and interest rate pressure.

Rising oil prices are increasing fears of sustained inflation. When inflation rises:

- Central banks are less likely to cut rates

- Interest rates remain higher for longer

- Yield-bearing assets become more attractive

Gold and silver, which do not generate yield, become less appealing in this environment.

👉 As a result, even traditional safe havens are being sold.

The Oil Shock Is Driving Everything

The key driver behind this market behavior is the surge in oil prices.

Following statements that the US will continue strikes on Iran for the next 2–3 weeks, markets are now pricing in prolonged geopolitical instability. At the center of this risk is the Strait of Hormuz — a critical global oil route responsible for nearly 20% of the world’s oil supply.

Any disruption in this region could push oil prices significantly higher.

👉 And higher oil means higher inflation.

This creates a chain reaction across all markets.

Why Crypto Is Falling Despite Bullish News

Under normal conditions, recent developments should support crypto markets:

- Progress on stablecoin regulation

- Continued institutional involvement

- Growing adoption narratives

Yet, crypto is declining.

This is because macro conditions are overriding crypto-specific fundamentals.

When liquidity tightens and uncertainty increases, investors reduce exposure to risk assets — and crypto is one of the first to be sold.

👉 Bitcoin is not trading on news — it is trading on macro.

The Real Risk: A Liquidity Shock

What markets are facing now is not just geopolitical uncertainty — it is the risk of a broader liquidity tightening cycle.

The sequence is clear:

- Oil prices rise

- Inflation expectations increase

- Rate cuts get delayed

- Liquidity shrinks

This environment puts pressure on all major asset classes simultaneously — including stocks, commodities, and crypto.

👉 That’s why everything is falling together.

What Investors Should Watch Next

The next phase of the market will depend on a few critical developments:

- Escalation or stabilization in the Iran conflict

- Movement in oil prices above or below $100

- Signals from central banks regarding rate policy

If oil continues to rise, markets could see further downside across both traditional and digital assets.

Conclusion: This Is No Longer a Normal Market

The current environment marks a shift from isolated market movements to a fully interconnected macro-driven system.

Safe havens are failing. Risk assets are under pressure. And geopolitical uncertainty is dictating market direction.

👉 This is no longer a crypto market — it’s a macro battlefield.

As tensions in the Middle East reached a boiling point, risk assets—including $Bitcoin and major altcoins—faced a sharp "risk-off" liquidation. However, as diplomatic channels begin to signal a potential de-escalation, savvy investors are looking at the "blood in the streets" as a generational entry point.

Historically, markets overreact to geopolitical shocks. If a resolution is reached in early April, the pent-up liquidity currently sitting in stablecoins is expected to flood back into high-conviction projects that were unfairly hammered during the panic.

Is April a Good Time to Buy Crypto?

Potentially, as April 2026 is shaping up to be a prime recovery month. With many tokens trading at 20-30% discounts from their Q1 highs, the current "oversold" conditions on the RSI (Relative Strength Index) suggest a relief rally is imminent.

1. Ethereum (ETH): The Race Back to $3,000

$Ethereum remains the backbone of the decentralized economy. During the recent March turbulence, ETH slipped below its psychological support, but the fundamentals remain unshaken.

- Recovery Catalyst: The successful implementation of the "Prague" upgrade earlier this year has further reduced Layer-2 costs.

- Price Target: Analysts expect a swift recovery to the $3,000 mark as institutional ETH ETFs see renewed inflows once the global macro outlook stabilizes.

Investors should monitor the ETH price closely, as its recovery usually leads the broader altcoin market.

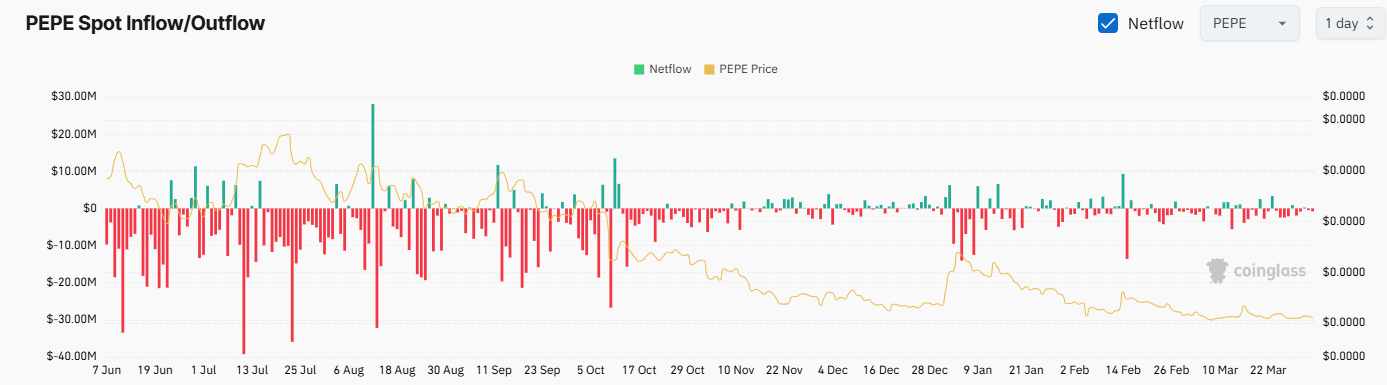

2. PEPE: The Volatility King

For those with a higher risk appetite, $PEPE remains the go-to memecoin for catching rapid bounces. Memecoins often act as high-beta plays on market sentiment; when the market turns green, PEPE tends to move twice as fast as the majors.

- Current State: PEPE lost significant ground in March but has maintained a strong community floor.