Cryptocurrency Posts

Crypto Briefing

Kalshi gets margin approval as its $22 billion valuation and booming event trading volumes push prediction markets further into Wall Street.

The post Kalshi moves toward margin trading with new regulatory approval appeared first on Crypto Briefing.

Codifying SEC-CFTC rules into law could prevent politically motivated crackdowns, fostering innovation and enhancing US crypto competitiveness.

The post Ripple CEO warns against another weaponized Gensler moment if SEC-CFTC rules aren’t codified into law appeared first on Crypto Briefing.

Judge blocks Trump administration from enforcing Anthropic blacklist, handing Claude maker an early win in its fight with the Pentagon.

The post Anthropic wins early court fight over Pentagon blacklist and Trump ban appeared first on Crypto Briefing.

Tech stocks slide as broader market selloff deepens, crypto drops below key levels, and gold rises amid US Iran tensions and rising yields.

The post Tech stocks lead Friday selloff as crypto breaks lower and gold and silver spike appeared first on Crypto Briefing.

Citigroup's potential acquisition could reshape its competitive landscape, leveraging freed capital for strategic growth and digital innovation.

The post Citigroup said to weigh acquisition of US regional bank to strengthen deposits and lending appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Morgan Stanley Set to Undercut Bitcoin ETF Rivals With 0.14% Fee Ahead of Launch

Morgan Stanley is poised to shake up the spot bitcoin ETF market with a sharply lower fee structure, as new filing details show its upcoming Morgan Stanley Bitcoin Trust (MSBT) will charge just 0.14% annually — undercutting every existing U.S. competitor.

The fee, disclosed in updated trust documents shared by Bloomberg analyst Eric Balchunas, comes in 11 basis points below BlackRock’s flagship iShares Bitcoin Trust (IBIT), which currently charges around 0.25%.

The aggressive pricing positions MSBT as the cheapest spot bitcoin ETF on the market at launch, signaling a deliberate push to capture both internal advisory flows and external investor capital.

The move carries particular weight within Morgan Stanley’s own ecosystem. With roughly $8 trillion in wealth management assets and a network of thousands of financial advisors, fee sensitivity has been one of the barriers to broader ETF adoption across advisory channels.

A lower-cost in-house product could remove that friction, allowing advisors to allocate to bitcoin without facing conflicts tied to recommending higher-fee third-party funds.

Industry observers say that dynamic could materially shift flows.

Phong Le, CEO of Strategy, recently described the product as a potential “Monster Bitcoin” catalyst, estimating that even a modest 2% allocation across Morgan Stanley’s platform could translate into roughly $160 billion in demand.

That figure would far exceed the size of any existing spot bitcoin ETF and underscores the importance of distribution, not just product design.

Morgan Stanley’s bitcoin ETF is coming

The fee disclosure arrives as MSBT moves closer to launch. The fund has already received a listing notice from the New York Stock Exchange, a step widely viewed as signaling that trading could begin imminently pending final regulatory clearance. If approved, the product would become the first spot bitcoin ETF issued directly by a major U.S. bank rather than an asset manager.

Structurally, MSBT mirrors existing spot bitcoin ETFs. The trust will hold bitcoin directly, with Coinbase serving as custodian and prime broker, while BNY Mellon will handle administration, transfer agency, and cash custody.

Since their debut in 2024, U.S.-listed spot bitcoin ETFs have easily attracted more than $50 billion in inflows, driven largely by retail and self-directed investors. Adoption within wealth management platforms has been slower, often constrained by internal policies, fee considerations, and portfolio construction guidelines.

At the time of writing, Bitcoin is trading near $66,000.

This post Morgan Stanley Set to Undercut Bitcoin ETF Rivals With 0.14% Fee Ahead of Launch first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Fear and Greed Index Hits Extreme Fear at 13 Out of 100

As of March 27, 2026, the Bitcoin Fear and Greed Index reads 13, placing sentiment in Extreme Fear. The current price of bitcoin is near $66,000.

The index spans 0 to 100, with lower readings tied to fear-driven market conditions and higher readings tied to greed-driven conditions.

The metric compiles inputs across price volatility, market momentum, trading volume, Bitcoin dominance, social sentiment, and Google Trends activity. The combined dataset forms a sentiment gauge used to track emotional conditions across Bitcoin markets.

Readings in the Extreme Fear range have aligned with prior stress phases in BTC market cycles.

Bitcoin Magazine Pro data highlights these zones as periods marked by liquidity contraction, elevated volatility, and forced positioning in derivatives markets.

JUST IN: The #Bitcoin Fear and Greed Index is now at 13, "Extreme Fear"

— Bitcoin Magazine (@BitcoinMagazine) March 27, 2026

Be greedy when others are fearfulpic.twitter.com/rvDHka0Hdn

In prior reporting, deep fear readings have coincided with accumulation behavior among long-term holders, alongside reduced speculative activity across spot and derivatives venues.

Earlier market drawdowns examined in Bitcoin Magazine Pro research show similar sentiment conditions during deleveraging events, where sharp price declines matched rapid sentiment compression.

In those phases, volatility expansion and liquidity withdrawal appeared alongside increased Bitcoin dominance as risk appetite shifted away from altcoin exposure.

Bitcoin uncertainty

Earlier today, Bitcoin price fell to its lowest level in more than two weeks, dropping below roughly $66,000 as liquidations exceeded $300 million in long positions over the previous 24 hours.

Short liquidations were far lower, showing that leveraged bullish traders were primarily forced out of the market. The move followed a broader shift in global risk sentiment as equities weakened and macroeconomic pressure increased.

The decline in BTC coincided with a risk-off environment across traditional markets. Nasdaq 100 futures had fallen about 10% from prior highs, while oil prices rose toward $100 per barrel amid escalating geopolitical tensions involving Iran.

Military activity and missile exchanges between the two countries continued despite diplomatic efforts, and the United States delayed direct escalation while negotiations remained open.

Regional instability contributed to concerns over energy supply routes, including disruptions in the Strait of Hormuz.

BTC had briefly approached higher levels earlier in the week on hopes of diplomatic progress, but those gains reversed as uncertainty returned. Price action remained within a broader range between $60,000 and $75,000 that had persisted for several weeks, following a prior peak above $120,000 in late 2025.

Institutional flows showed mixed signals. Spot BTC exchange-traded funds recorded billions in inflows earlier in March, but more recent sessions saw outflows.

On-chain data showed continued withdrawals from exchanges, suggesting long-term holders moved assets into self-custody. Options markets showed about $14 billion in expirations, which influenced price stability near key strike levels around $75,000.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post Bitcoin Fear and Greed Index Hits Extreme Fear at 13 Out of 100 first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

ICE Announces $600 Million Strategic Investment in Polymarket

Intercontinental Exchange, Inc. Intercontinental Exchange, the parent company of the New York Stock Exchange, has completed a $600 million direct cash investment in prediction market platform Polymarket as part of a broader equity fundraising round, according to a company announcement.

The new investment follows ICE’s previously disclosed $1 billion commitment made in October 2025. With the latest infusion, ICE says it has now fulfilled its obligations under the investment agreement, which also includes plans to purchase up to $40 million in additional Polymarket securities from existing holders.

Polymarket, a blockchain-based prediction market platform that allows users to trade on the outcomes of real-world events, has drawn increasing attention from institutional investors amid growing interest in event-driven data markets and decentralized financial infrastructure.

Polymarket has support for bitcoin deposits, giving users a direct way to fund their accounts with BTC alongside other existing crypto options.

ICE stated that the investment is not expected to materially impact its financial results or capital return plans. Final valuation details of the latest transaction are expected to be disclosed once the fundraising round is fully completed.

The move further signals traditional financial market infrastructure firms expanding into alternative data and crypto-adjacent platforms. ICE, which operates major exchanges including the NYSE, continues to diversify into digital markets, data services, and fintech infrastructure.

Polymarket has become one of the most prominent prediction market platforms globally, leveraging blockchain rails to facilitate trading on political, economic, and cultural outcomes.

The companies emphasized that the announcement does not constitute an offer to sell or solicit securities. Market observers say the scale of ICE’s investment underscores rising institutional interest in prediction markets as both a trading venue and a data source.

Polymarket’s embrace by TradFi

In the past year, the relationship between the crypto-native prediction market and traditional financial powerhouse Intercontinental Exchange (ICE) has become one of the most closely watched intersections of decentralized markets and institutional capital.

Polymarket, launched in 2020 by founder Shayne Coplan, has grown into one of the largest blockchain-based prediction platforms, where users trade shares on the outcomes of future events — from elections to economic indicators and geopolitical developments — using cryptocurrency rails.

In late 2025, Polymarket re-entered the U.S. market under full Commodity Futures Trading Commission (CFTC) regulation after previously being blocked amid enforcement actions, marking a significant shift from its earlier status as an offshore, lightly regulated venue.

In December 2025, Polymarket launched its U.S.-focused app after the CFTC approval, restoring American access to its prediction markets and initially offering sports betting with plans to expand into other categories like propositions and elections.

Editorial Disclaimer: We leverage AI as part of our editorial workflow, including to support research, image generation, and quality assurance processes. All content is directed, reviewed, and approved by our editorial team, who are accountable for accuracy and integrity. AI-generated images use only tools trained on properly license material. In Bitcoin, as in media: Don’t trust. Verify.

This post ICE Announces $600 Million Strategic Investment in Polymarket first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Price Slides to Two-Week Low as Liquidations Top $300 Million and Macro Pressure Builds

Bitcoin price fell below $66,500 on Friday, hitting its lowest level in more than two weeks as a wave of long liquidations and mounting macroeconomic stress weighed on the crypto market..

Data shows nearly $300 million in long positions were liquidated over the past 24 hours, according to Bitcoin Magazine Pro data, compared with roughly $50 million in short liquidations, pointing to an unwind of crowded bullish positioning in crypto futures. The imbalance reflects a market that had leaned heavily long and is now adjusting as sentiment shifts.

The bitcoin price selloff coincided with a broader risk-off move across global markets. Nasdaq 100 futures have fallen about 10% from their January highs, while oil prices climbed near $100 per barrel amid escalating geopolitical tensions tied to the ongoing conflict involving Iran.

Earlier today, Israel said it will escalate strikes on Iran after renewed waves of Iranian missile attacks, while both sides continue exchanging fire despite ongoing diplomatic efforts.

President Trump has paused U.S. strikes on Iranian energy infrastructure for 10 more days to allow negotiations, even as reports suggest the Pentagon is considering deploying up to 10,000 additional troops to the Middle East.

Meanwhile, the conflict is widening regionally, with shipping disruptions reported in the Strait of Hormuz, Gulf states on alert after strikes, and Iranian casualties reportedly nearing 2,000 as international talks continue in Europe.

The surge in crude has renewed inflation concerns and pressured risk assets, including cryptocurrencies.

Bitcoin price dynamics

Bitcoin price briefly approached $71,500 this week on optimism tied to a potential diplomatic breakthrough in the Middle East. Those gains reversed as uncertainty around negotiations resurfaced, pushing prices lower and reinforcing sensitive market conditions.

Despite the recent decline, bitcoin price continues to trade within a defined range between $60,000 and $75,000 that has held for several weeks, even months. The asset remains well below its October 2025 peak above $126,000 following a broader market correction.

Institutional flows present a mixed picture. U.S.-listed spot bitcoin exchange-traded funds recorded sustained inflows earlier in March, totaling about $2.5 billion over five weeks. That momentum has slowed in recent sessions, with net outflows emerging and signaling a pause in accumulation as investors respond to macro uncertainty.

At the same time, on-chain data indicates continued withdrawals of bitcoin from centralized exchanges over the past month. This trend suggests longer-term holders are moving assets into self-custody, a pattern often associated with accumulation rather than distribution.

Despite this, Morgan Stanley is a step closer to launching its spot Bitcoin ETF, MSBT, after the New York Stock Exchange posted a listing notice — signaling an imminent debut that could make it the first such product from a major U.S. bank, alongside offerings from BlackRock and Fidelity.

Options markets add another layer of complexity. Roughly $14 billion in bitcoin price options are set to expire, representing a significant share of open interest.

Hedging activity tied to these contracts has contributed to subdued volatility, with price action gravitating toward key strike levels near $75,000.

As these contracts roll off, the stabilizing effect from derivatives positioning may fade, leaving bitcoin more exposed to external catalysts.

With geopolitical risks elevated and macro conditions tightening, the market faces a period where price movements may become more reactive and less constrained by structural flows.

This post Bitcoin Price Slides to Two-Week Low as Liquidations Top $300 Million and Macro Pressure Builds first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Simon Gerovich Confirmed As A Bitcoin 2026 Speaker

Simon Gerovich has been officially confirmed as a speaker at Bitcoin 2026. As Chief Executive Officer (CEO) of Tokyo Stock Exchange-listed Metaplanet, he has helped transform the once struggling hospitality company into one of the largest corporate Bitcoin holders in the world. Now, Gerovich arrives in Las Vegas as one of the most closely watched figures in institutional Bitcoin adoption outside of the United States.

Metaplanet closed 2025 with 35,102 BTC, making it the fourth-largest public corporate Bitcoin holder globally. The company has outlined aggressive accumulation targets, aiming to reach 100,000 BTC by the end of 2026 and 210,000 BTC — approximately 1% of Bitcoin’s total supply — by the end of 2027. To fund that ambition, Metaplanet recently secured approximately $255 million from global institutional investors through a placement of new shares, with additional fixed-strike warrants that could lift total funding to roughly $531 million. The company is also expanding beyond treasury accumulation: Metaplanet’s board approved the creation of two subsidiaries — Metaplanet Ventures and Metaplanet Asset Management — targeting companies building Bitcoin financial infrastructure in Japan, including platforms focused on lending, payments, custody, derivatives, and compliance tools.

Gerovich began the company’s EGM in September 2025 by explaining how Metaplanet pivoted from operating as a struggling hotel company to a Bitcoin treasury company in early 2024. The turnaround has been significant. Revenue jumped 738% year-over-year to 8.91 billion yen, with operating profit surging 1,695%, driven primarily by premiums from Bitcoin option transactions, which accounted for about 95% of total revenue. Gerovich has consistently pointed to Bitcoin per share — the company’s primary KPI — rather than net profit as the appropriate metric for evaluating Metaplanet’s performance, noting that Bitcoin per share increased by more than 500% in 2025.

With Metaplanet’s accumulation targets for 2026 still in motion and its expansion into ventures and asset management underway, Gerovich takes the Bitcoin 2026 stage at a pivotal moment for the company and for corporate Bitcoin adoption in Asia.

Bitcoin 2026 is Returning to Las Vegas

Bitcoin 2026 will take place April 27–29 at The Venetian, Las Vegas, and is expected to be the biggest Bitcoin event of the year.

Focused on the future of money, Bitcoin 2026 will bring together Bitcoin builders, investors, miners, policymakers, technologists, and newcomers from around the world. The event will feature a wide range of pass types, including general admission passes designed specifically for those new to Bitcoin, alongside premium passes for professionals, enterprises, and institutions.

With multiple stages, immersive experiences, technical workshops, and headline keynotes, Bitcoin 2026 is designed to serve both first-time attendees and long-time Bitcoiners shaping the next era of global adoption.

Past Bitcoin Conferences in the U.S.

Bitcoin’s flagship conference has scaled dramatically over the past five years:

- 2021 – Miami: 11,000 attendees

- 2022 – Miami: 26,000 attendees

- 2023 – Miami: 15,000 attendees

- 2024 – Nashville: 22,000 attendees

- 2025 – Las Vegas: 35,000 attendees

Get Your Bitcoin 2026 Pass

Get Your Bitcoin 2026 Pass

Bitcoin Magazine readers can save 10% on Bitcoin 2026 tickets using code ‘ARTICLE10‘ at checkout.

Stay at The official hotel of Bitcoin 2026, The Venetian, and get a guaranteed low rate plus 15% off your pass. Be in the middle of where the fun is all happening, and where the networking never ends.

And don’t forget:

Volunteer at Bitcoin 2026 and get Pro Pass access plus exclusive perks.

All students ages 13+ can apply for a Student Pass and get free general admission access to Bitcoin 2026.

Location: The Venetian, Las Vegas

Location: The Venetian, Las Vegas Dates: April 27–29, 2026

Dates: April 27–29, 2026

For more information and exclusive offers, visit the Bitcoin Conference on X here.

Why Attend Bitcoin 2026?

Bitcoin 2026 is the definitive gathering for anyone serious about the future of money. With 500+ speakers, multiple world-class stages, and programming spanning Bitcoin fundamentals, open-source development, enterprise adoption, mining, energy, AI, policy, and culture, the conference brings every corner of the Bitcoin ecosystem together under one roof.

From headline keynotes on the Nakamoto Stage to deep technical sessions for builders, institutional strategy discussions for enterprises, and beginner-friendly Bitcoin 101 education, Bitcoin 2026 is designed for everyone—from first-time attendees to the leaders shaping Bitcoin’s global adoption.

Whether you’re looking to learn, build, invest, network, or influence, Bitcoin 2026 is where Bitcoin’s next chapter is written.

Bitcoin 2026 Pass Types: Something for Everyone

Bitcoin 2026 offers a range of pass options designed to meet the needs of newcomers, professionals, enterprises, and high-net-worth Bitcoiners alike.

Bitcoin 2026 General Admission Pass

Ideal for newcomers and those looking to experience the heart of the conference.

- Limited access on Days 2 & 3

- Entry to Main Stage

- Access to Genesis Stage

- Full access to the Expo Hall

Bitcoin 2026 Pro Pass

Designed for professionals, operators, and serious Bitcoin participants.

Includes all General Admission features, plus:

- Full 3-day access, including Pro Day

- Entry to the Pro Pass Reception

- Access to Enterprise Hall, Enterprise Stage, and Networking Lounge

- Conference App networking features

- Access to the Bitcoin For Corporations Symposium

- Entry to Compute Village and Energy Stage

- Complimentary lunch, coffee, tea, and snacks

- Dedicated registration and check-in

- Reserved seating at Main Stage

- Huge savings when you bundle your hotel and Pro Pass

Bitcoin 2026 Whale Pass

Bitcoin 2026 Whale Pass

The all-inclusive, premium Bitcoin 2026 experience.

Includes all Pro Pass features, plus:

- Reserved seating at Main Stage

- All-inclusive gourmet food and beverages

- Entry to Whale Night and Whale Reception

- Access to all official after-parties

- Networking app access to connect with other Whales

- Premium access to The Deep — an exclusive networking lounge with intimate speaker sessions

- Complimentary stay at The Venetian when you bundle your whale pass and hotel (use promo code ‘WHALEHOTEL’ here)

This is the most immersive way to experience Bitcoin 2026.

Bitcoin 2026 After Hours Pass

Bitcoin 2026 After Hours Pass

Your ticket to the night.

Most deals are done with a drink in your hand. Get exclusive access to 3 official Bitcoin 2026 after-parties across Las Vegas — each with a 2-hour open bar — where the real conversations happen and the best connections are made.

- Access to 3 official Bitcoin 2026 after-parties

- 2-hour open bar at each event

- Evening events across Las Vegas, April 27–29

- Network with Bitcoiners, builders, and industry leaders after hours

More headline speaker announcements are coming soon.

Don’t miss Bitcoin 2026.

This post Simon Gerovich Confirmed As A Bitcoin 2026 Speaker first appeared on Bitcoin Magazine and is written by Jenna Montgomery.

CryptoSlate

Prediction markets spent years trying to present themselves as smarter, better, and more useful than straight-out gambling.

Then sports arrived and did what elections, inflation contracts, and policy wagers never quite managed: it brought scale. They turned what was essentially a niche event trading activity into a mass product, and pushed the industry into a dangerous identity crisis.

Sports made prediction markets popular, but they also made them politically vulnerable.

On March 12, the CFTC opened a formal rulemaking process for prediction markets, putting manipulation, oversight, and contract structure under the federal spotlight.

Since then, Arizona has also filed criminal charges against Kalshi, while a Nevada judge temporarily blocked the company from operating there without a state license. Massachusetts had already moved against Kalshi's sports contracts.

Now Congress is moving, too.

A bipartisan group of senators is preparing legislation that would ban sports bets and casino-style contracts on CFTC-regulated prediction markets, arguing that they're exploiting a legal loophole to bypass state gambling rules and cut across tribal sovereignty.

It's now safe to say that the dispute is no longer confined to a few test cases.

The industry now faces an awkward fact. Its fastest route to growth came through contracts that look, feel, and are marketed a lot like sports bets. But, its legal defense depends on persuading courts and regulators that those same contracts belong in the world of federally supervised derivatives. The more popular sports became, the harder it became to sustain that argument.

This stopped being a niche fight between startups and gaming boards a long time ago. It's now a national argument over whether a business that behaves like sports betting can claim the legal privileges of financial market law and bypass the state-by-state gambling system that sportsbooks have spent years and billions of dollars entering.

What began as a jurisdiction fight over who regulates these contracts is now turning into something wider and more dangerous for the industry: a fight over whether sports prediction markets should exist in this form at all.

The whole fight turns on one question: bet or swap?

When you strip the dispute down to its core, you get to the main question all current and future regulation efforts are attempting to answer: Are prediction markets bets or swaps?

Linda Goldstein, a partner at CM Law, says that the answer to this question determines who regulates them. If these transactions are bets, states regulate them. If they're swaps or derivatives, then the CFTC has the lead role, she told CryptoSlate.

States argue that the contracts may have the form of derivatives, but function as wagers in substance. This is especially true where there's no credible commercial hedging use, and users are just staking money on the outcome of a game for a payout.

On the other hand, operators say that event contracts have long belonged inside commodities law and that a national market can't function if every state is free to classify the same federal product as illegal gambling.

That's one of the many reasons this fight feels so unstable.

The consumer activity we see on prediction markets is straightforward and familiar. People put money down on uncertain outcomes and get paid if they're right.

The main dispute here is abstract and sits one level higher, in the legal classification of the contract itself. At the center of the fight is a simple problem: the same product can be framed as a derivative by federal regulators and as gambling by the states.

We're now seeing a battle over whether states will keep authority over activity that looks and works like gambling, or whether that authority will get absorbed into federal financial oversight. The legal dispute has gone past Kalshi or one set of contracts, and is now about who governs event-based wagering once it's packaged as a federally supervised market product.

That turns the debate from a branding argument into a real legal conflict over who gets to regulate these markets. Once sports became the dominant use case for prediction platforms, this became a fight over whether a national sports-betting business can operate under commodities law without ever entering the state licensing systems built for sportsbooks.

That's why states such as Utah, Arizona, and Nevada are pushing so hard. They are trying to stop gambling-like activity from migrating into a federal regime they have no control over.

Why product design matters for prediction markets

A significant part of this issue will be resolved in court. However, people underestimate the effect that product design will have on this.

One of the reasons prediction markets run into issues is when they loosen their criteria about what makes a good event contract. The hype that surrounds them makes it tempting to list fast-moving and popular events, because that's what drives volume.

But if these products don't have precise definitions and irrefutable settlement, they quickly turn into entertainment wagering.

This means prediction markets can start acting like sportsbooks even before regulators notice. They start drifting there when spectacle and volume outrun precision, and when contracts are built for attention first, with the settlement depending too much on interpretation.

Binary contracts look simple until users start contesting the settlement. A yes-or-no contract is only as good as the definition inside it. Once the terms that define its outcome become elastic, the market starts depending on judgment calls, arguments, and eventually litigation.

Ross Weingarten, a partner and co-chair of the Sports Integrity Group at Steptoe, said that from the consumer standpoint, prediction markets work differently from traditional sportsbooks because users are trading “yes” or “no” positions against each other, not against a house.

But when the question gets murky, or the answer is not clear, the binary question suddenly isn’t so binary.

“We saw an example of this with bets on whether Cardi B would perform at the Super Bowl. She was on stage, but didn’t have a microphone. Did she perform? The answer probably depends on which side of the bet you took. For the prediction markets, bets like this often lead to litigation.”

That's why sports contracts vary so much in defensibility.

Simple, hard-to-manipulate outcomes are easier to defend, which is why contracts on game winners are so popular. In-game props, performance claims, officiating-dependent outcomes, and anything vulnerable to insider knowledge or integrity distortions sit on thin ice.

It's where the industry's credibility will be won or lost. A platform that looks like a neutral exchange with visible order books, transparent pricing, independent settlement sources, and strong abuse detection has a stronger claim to a federal market status. A platform that looks like a bookmaker has a much weaker one.

The legal question will be resolved in court, but the legitimacy question will be resolved by the architecture of the actual product.

States started this fight, but Congress will decide where it ends

States present this as a consumer-protection and public-policy fight, and there is substance to that claim. Licensed sportsbooks sit inside a regime built around age controls, responsible-gambling funding, integrity monitoring, tax collection, and rules tailored to each jurisdiction. Prediction markets threaten to route the same activity through a federal channel that bypasses much of that system.

Goldstein is especially clear on the states' incentives, saying it's mostly about money and competition.

“Event contracts on sporting events account for the vast majority of transactions on prediction platforms like Kalshi and Polymarket, with some data estimating that it could be as much as 90% of the event contracts,” she explained.

“These contracts are directly competing with licensed sportsbooks. Traditional sports betting generates significant tax revenue for the states because the states receive taxes on the gross gaming revenue. The American Association of Gaming has estimated that, since the beginning of 2025, sports betting platforms have lost over $600 million to prediction markets.”

However, states are also adamant on keeping strict safeguards on all of these platforms. Goldstein explained that prediction markets circumvent many of the safeguards designed to protect consumers, such as age verifications, oversight over the integrity of the games, and mandatory contributions to gambling funds.

The American Gaming Association has made that case bluntly, accusing sports-related prediction markets of bypassing the state-based system that legal sports betting was built on. The leagues are adapting in real time as well. MLB's deal with Polymarket and its memorandum with the CFTC on integrity cooperation amount to an acknowledgment that these markets are now too large to ignore.

The escalation in Arizona and Nevada shows how serious this has become. Arizona's criminal case moved the dispute out of the familiar zone of cease-and-desist letters and into prosecutorial territory. Nevada's restraining order showed that at least one court, for now, is willing to treat these products as unlicensed sports pools under state law. These are both attempts to force the industry back inside state control before federal market law hardens into a permanent workaround.

However, Weingarten explained that not all courts agree that sports event contracts amount to unlicensed sports betting subject to state law.

“Some courts have agreed; others have not,” he told CryptoSlate.

“Courts in New Jersey, California, and Tennessee have found that the contracts qualify as ‘swaps' under the Commodity Exchange Act. But courts in Maryland, Nevada, Massachusetts, and Ohio have emphasized the historic role of states in regulating gambling. As a result, how and by whom prediction markets are regulated is very much in flux.”

That's why the endgame probably won't produce a clean blessing or a clean ban. CFTC has stated unequivocally that it believes it has exclusive jurisdiction over prediction markets like Kalshi and Polymarket, and states continue to claim their oversight.

But the newest turn in the story matters more than all of this, because it now widens the backlash well beyond just individual states. The bipartisan bill announced on Mar. 23 argues that sports and casino-style contracts should be carved out of federally regulated prediction markets altogether.

That's a much more dangerous proposition for the industry because it breaks one of its core assumptions: that if prediction markets win the federal vs. state fight, sports contracts will survive them.

This changes the terrain in a much more fundamental way. The industry will no longer have to worry about whether courts will treat sports contracts as gambling under state laws, but whether Congress will decide whether they should be offered on regulated prediction markets at all.

The endgame is now a fight over categories, not just jurisdiction. States are suing, the CFTC is writing its own rules, and lawmakers have decided that some event contracts shouldn't be allowed in the first place.

That's why the most plausible destination we'll get to is a hybrid regime, with tighter federal rules, more category restrictions, more surveillance demands, more pressure around contract clarity, and tougher expectations around how these products are marketed.

Platforms may still call themselves exchanges, but they'll have to prove it in the way they design, settle, surveil, and present their contracts.

This isn't a temporary flare-up in a niche product that will go away in the next cycle, because, like it or not, prediction markets are here to stay. We're at the beginning of a foundational fight over where finance ends, and gambling begins, and the process could drag on for years.

Prediction markets found their mass audience by moving closer to sports betting. Now they have to answer the question that success created: can they keep that audience while persuading courts, regulators, and the public that they are still something meaningfully different?

The post The bets that made crypto prediction markets popular could now be banned appeared first on CryptoSlate.

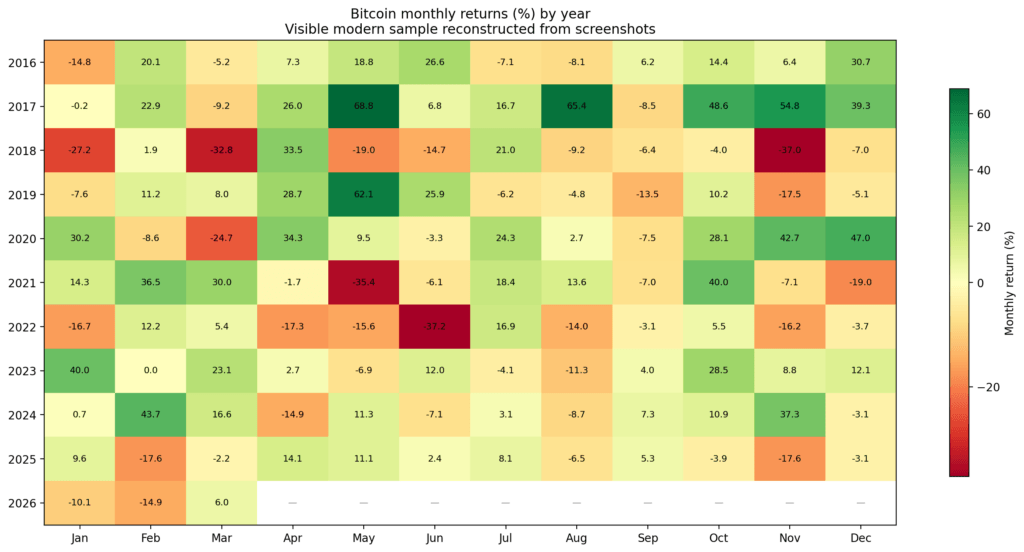

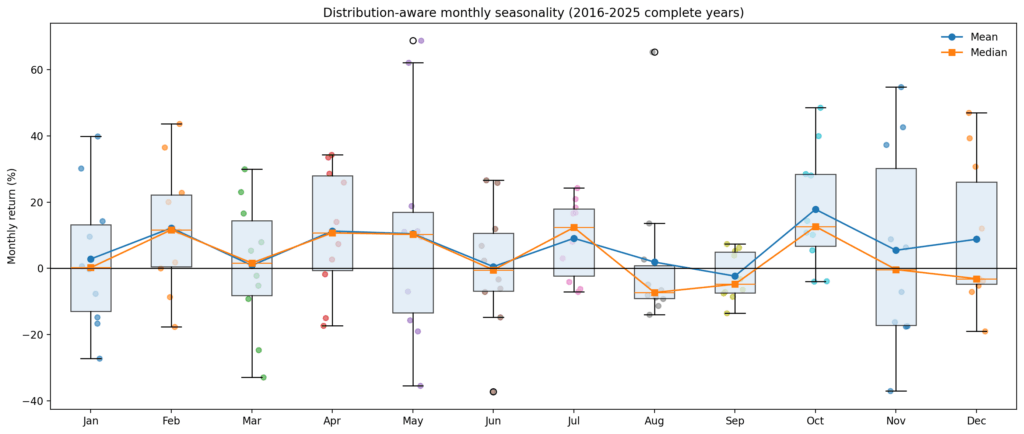

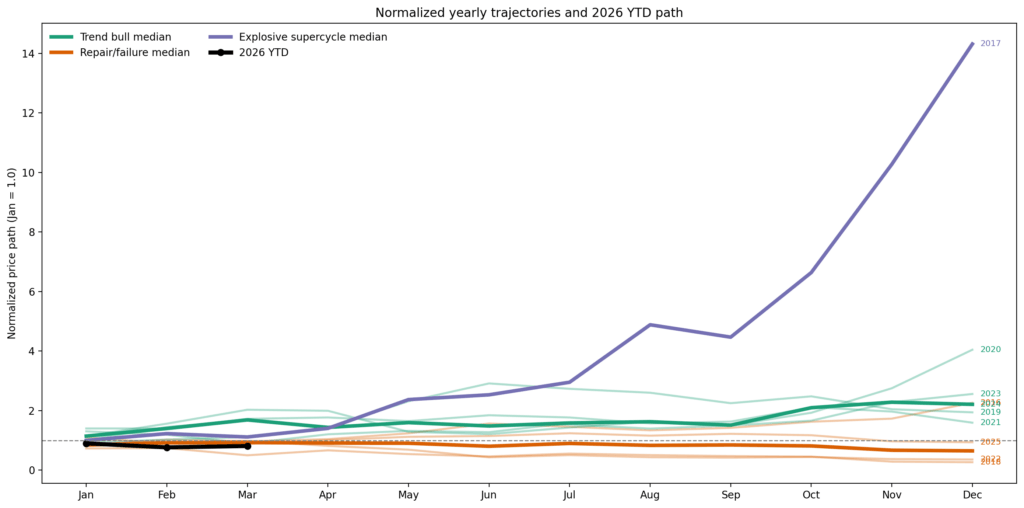

Bitcoin price has never finished a year positive after a start this bad

Bitcoin seasonality is one of those market narratives that stays alive because the average is easy to screenshot. The problem is that the average often hides the only thing that matters: the state.

A strong “Uptober” inside a healthy bull trend is not the same trade as a strong October after a year that spent the first quarter underwater. A positive December mean is not an edge if the median month is still negative. And a hot Q1 is not automatically a continuation signal if the market has already pulled forward most of its upside.

That is the core result here. The useful part of Bitcoin price seasonality is not the calendar alone. The interaction between month, regime, and path is far more important.

The first problem with the seasonality story is that averages flatter the distribution

If you only look at mean monthly returns, Bitcoin price appears to offer a menu of recurring bullish windows.

In the modern sample, October stands out with a mean return of 17.8%, a median of 12.7%, and an 80% win rate. July also holds up well, with a 9.1% mean return, a 12.4% median, and a 70% win rate. February and April look reasonably constructive, too.

But once you move beyond averages, the picture changes fast.

August is the cleanest example. The mean return is slightly positive at 1.9%, which sounds benign until you look underneath it: the median is -7.3%, the win rate is just 30%, and the distribution is positively skewed.

In plain English, August has not been a dependable “up month.” It has been a low-hit-rate month, occasionally rescued by a few large upside outliers.

December has the same problem in a softer form. The mean is positive, but the median is negative, and the win rate is only 40%. November is similar: a headline-positive average, but a distribution with enough variance and downside tail to make the average far more flattering than the lived experience of holding risk through it.

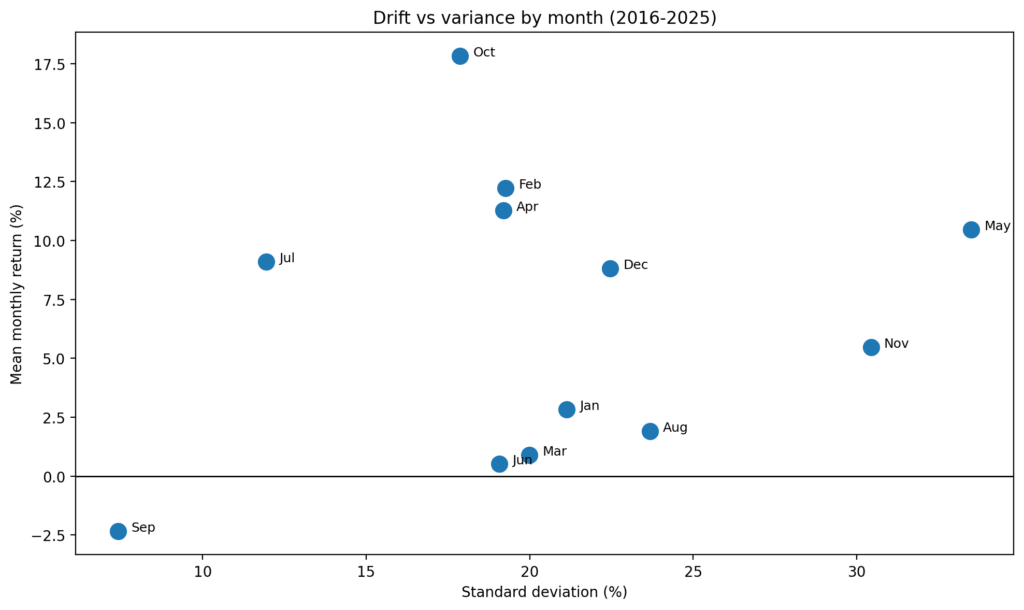

May is another trap. The average return looks healthy, but dispersion dominates the month. The upside tail is large, the downside tail is large, and the standard deviation is high enough that “May is positive on average” tells you very little about what kind of risk you are actually taking.

Some months are drift-dominant, where the mean, median, and win rate broadly line up. Others are variance-dominant, where the average is doing more storytelling than forecasting.

The months that look most usable are not the ones most people talk about

The cleanest month is October. Not because it always works (it does not), but because its average, median, and win rate all point in the same direction.

July is the next-best example. Those are the closest things in the data to stable seasonal windows.

By contrast, some of the more familiar seasonal talking points look fragile.

August’s positive mean is mostly an artifact of skew. November and December can work, but they are not clean trend months in the statistical sense. They are conditional months that need confirmation from regime and path.

That is the first big line between edge and illusion. A month with a positive average is not necessarily a month with a repeatable edge.

If the median is negative and the win rate is weak, what you have is not seasonality. What you have is optionality disguised as consistency.

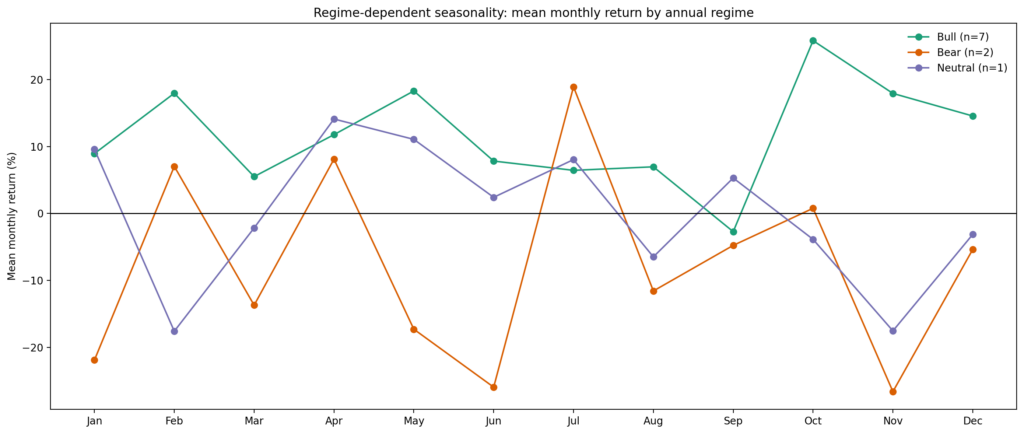

Regime changes the sign of the seasonal signal

The next step was to split years into objective regimes: bull years with annual returns above 50%, bear years below -20%, and neutral years in between.

Once you do that, unconditional seasonality starts to look less like structure and more like a blended average of opposite states.

Several months flip sign depending on regime, including January, March, May, June, August, November, and December.

In other words, the same month that looks constructive in the full sample can turn negative once you isolate a weaker macro backdrop.

That is exactly what you would expect if seasonality is downstream of market state rather than independent of it.

There are only a few months that look relatively resilient across regimes. July is the strongest candidate. April is somewhat constructive as well, though less cleanly. September, meanwhile, remains weak enough across major regimes to merit respect as a recurring soft patch rather than a one-off anomaly.

The caveat is obvious: the bear sample is small. But that is also the point. If a seasonal claim falls apart the moment you ask whether it survives different states of the world, it was probably never a robust claim to begin with.

The real edge is path dependency, not calendar mythology

The strongest signals are not monthly averages at all. They are state variables tied to the year’s path.

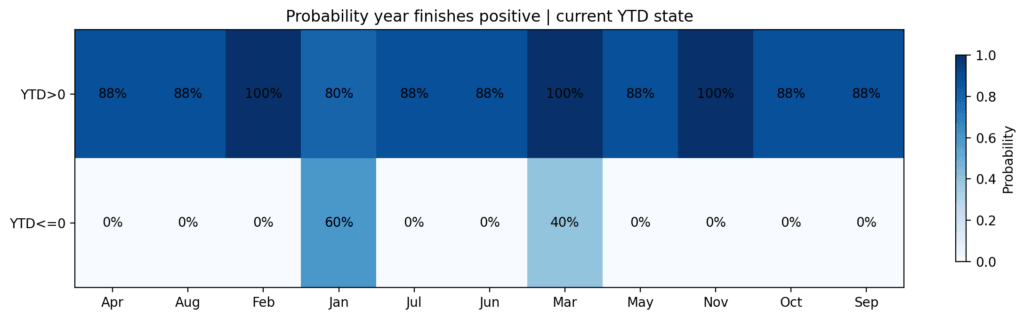

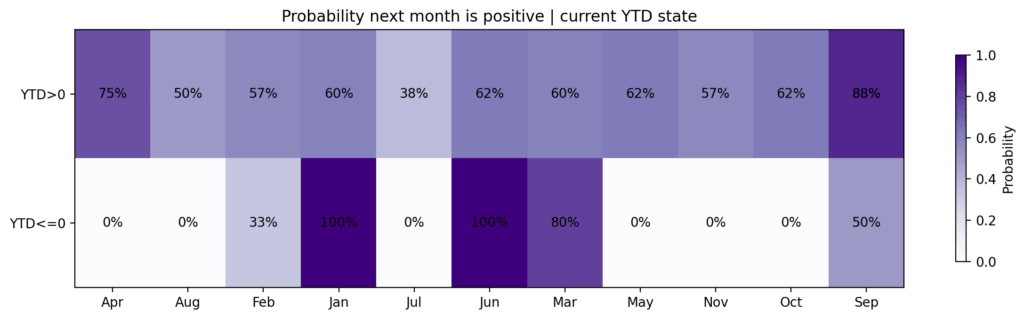

In the 2016–2025 sample, if Bitcoin was positive year-to-date after February, it finished the year positive seven out of seven times.

If it was negative year-to-date after February, it finished positive zero out of three times.

After March, the split was still material: positive YTD years finished positive five out of five times, while negative YTD years only finished positive two out of five times.

That is not a trivial distinction. It suggests that by late Q1, Bitcoin’s seasonal profile is already being filtered by whether the year is in a healthy trend or in repair mode.

The market is not simply entering “good” or “bad” months. It enters them from a specific state, which changes the forward distribution.

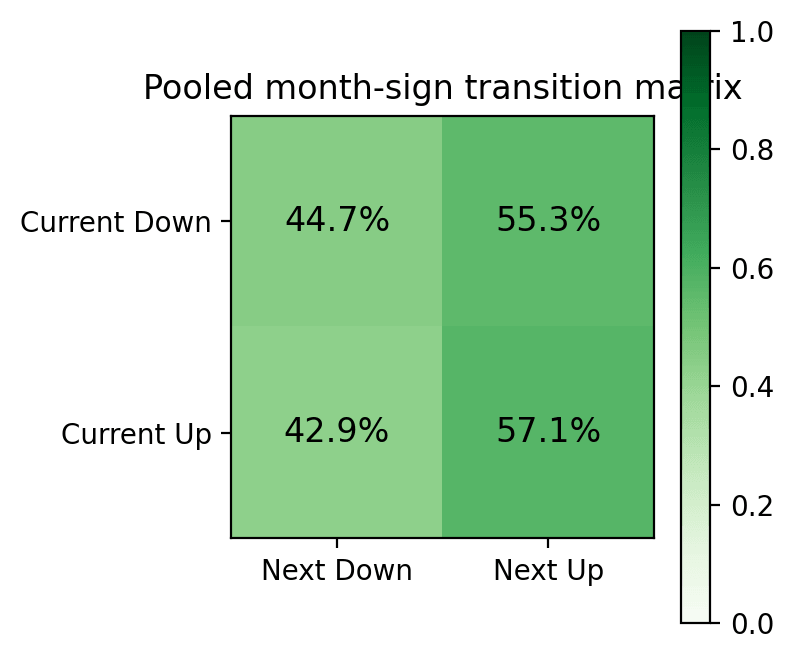

Just as important, simple month-to-month sign momentum does not hold up. After an up month, the next month was positive 57.1% of the time. After a down month, the next month was positive 55.3% of the time. That is not a serious edge.

The useful signal only emerges once you condition on the broader path, the YTD trajectory, the Q1 outcome, and whether the year is repairing or breaking.

A strong Q1 helps the year, but often hurts the next quarter

One of the more interesting findings is that strong early-year performance is not a clean continuation signal.

Years with Q1 returns above 20% did go on to finish positive every time. But Q2 in those years was weak on average, with a mean decline of 15.1%.

That's important because it separates direction from timing.

A hot Q1 improved the odds of a positive full-year outcome, but it also tended to pull forward returns and raise the probability of spring digestion.

In other words, the market could remain structurally constructive while still becoming tactically harder to own into Q2.

The data here does not support the leap that a positive year-level tendency is a positive entry signal for the next month or quarter.

June looks like the real decision node

If there is a practical seasonal checkpoint in the data, it is not a single month but the year’s condition by midyear. Years with first-half returns at or below zero never finished positive. Years with positive first-half returns finished positive seven times out of eight, with 2025 as the notable exception.

The same logic shows up in negative-Q1 years. If a weak first quarter was followed by a Q2 rebound greater than 20%, the full-year outcome improved materially.

If the rebound failed to clear that threshold, the year did not finish positive. That does not make Q2 destiny, but it does make it the most useful repair window in the annual path.

The implication is straightforward. Once a year opens damaged, the burden of proof shifts to Q2.

If the market cannot meaningfully recover by June, the case for leaning on second-half seasonal optimism becomes much weaker.

Why 2026 matters now

That framework is especially relevant for 2026 because the year has already broken one of the cleaner modern path templates.

Every year, a negative January has been followed by a positive February — until now.

2026 opened with a 10% decline in January, fell another 14.8% in February, and then rebounded 6% by mid-March, leaving Q1 down around 19%.

That negative-negative-positive sequence is unusual in the modern sample, and it places 2026 in what is best described as a repair-or-failure state.

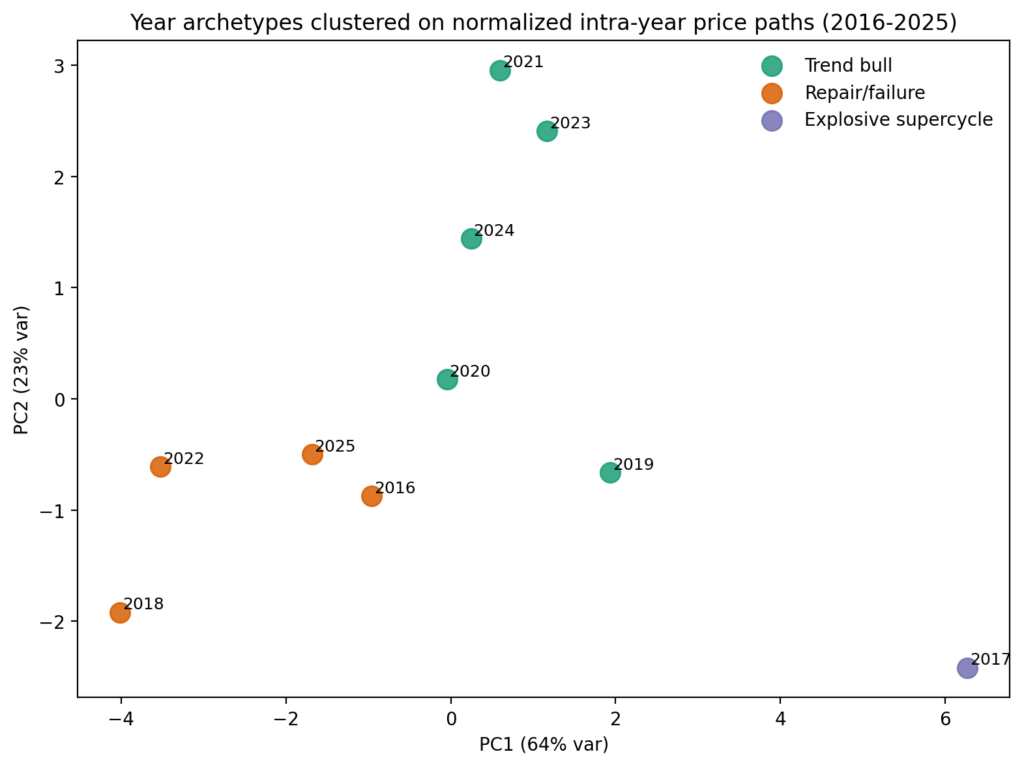

Cluster analysis maps the current year closest to a group that includes 2016, 2018, 2022, and 2025.

The correct frame for 2026 is one successful repair year, two failure years, and one rebound-without-trend year. Not “Bitcoin is usually good in Q4,” and not “the worst is over because March bounced,” but rather: can Q2 do enough work to move the year out of a damaged state?

The 2026 scenario tree is a repair test, not a seasonal layup

The most bullish likely direction from here is a genuine repair regime. That would look like a forceful Q2 recovery, some summer digestion, and then renewed upside into the back half of the year.

Historically, the closest analog is 2016, with 2020 as a more explosive upside outlier.

To even get the first half of 2026 back above flat from current levels, Bitcoin would need to compound by over 20% in Q2. To make the year look like a strong repair rather than a partial bounce, it would need substantially more.

The bearish path is a continuation failure, with 2018 and 2022 as the obvious reference points. In that path, spring strength proves tactical rather than structural, the market reopens downside later in Q2 or Q3, and the usual “good months” fail to do the heavy lifting investors expect of them.

2026 is not in a state where unconditional seasonality should be trusted. The year needs to earn a better seasonal profile through repair.

Today's sell-off is not helping the case for a bullish rebound, suggesting Bitcoin's 2026 ceiling is around $88,000.

So where is the edge?

Bitcoin seasonality provides the most value in a narrow set of situations. It is useful when a month already has a strong historical distribution and the year enters that month from a healthy state. October and July are the best examples in the modern sample. They look more like genuine drift windows than variance accidents.

Seasonality is also useful as a filter on damaged years. If Bitcoin is still negative year-to-date into spring, the calendar by itself is not enough. What matters is whether Q2 can repair the year’s path. If it can, the second half becomes materially more credible. If it cannot, the market’s more optimistic seasonal narratives start to look like wishful extrapolation.

Where seasonality becomes an illusion is in regime-blind averages and outlier-driven means. A positive average month with a negative median and weak win rate is not a clean edge.

A favorable calendar month inside a damaged annual path is not a setup on its own. And a strong Q1 is no license to assume uninterrupted continuation into Q2.

The bottom line

The market moves through January, July, and October, not in a vacuum, but in different regimes, with different YTD trajectories, after different types of first-quarter behavior.

Once you account for that, most of the broad seasonal story gets weaker, but the parts that survive become more actionable.

Bitcoin seasonality is not dead. It is just mostly conditional. The real edge is not in memorizing the “best months.” Recognizing when the market has earned the right for those months to matter is the real skill.

For 2026, that means one thing above all else: Q2 is the test.

If Bitcoin can repair enough damage by June, the second half deserves the benefit of the doubt. If not, then whatever the calendar says, the path is telling you something else.

The post Bitcoin price has never ended a year higher after a start this bad — is $88k the 2026 ceiling now? appeared first on CryptoSlate.

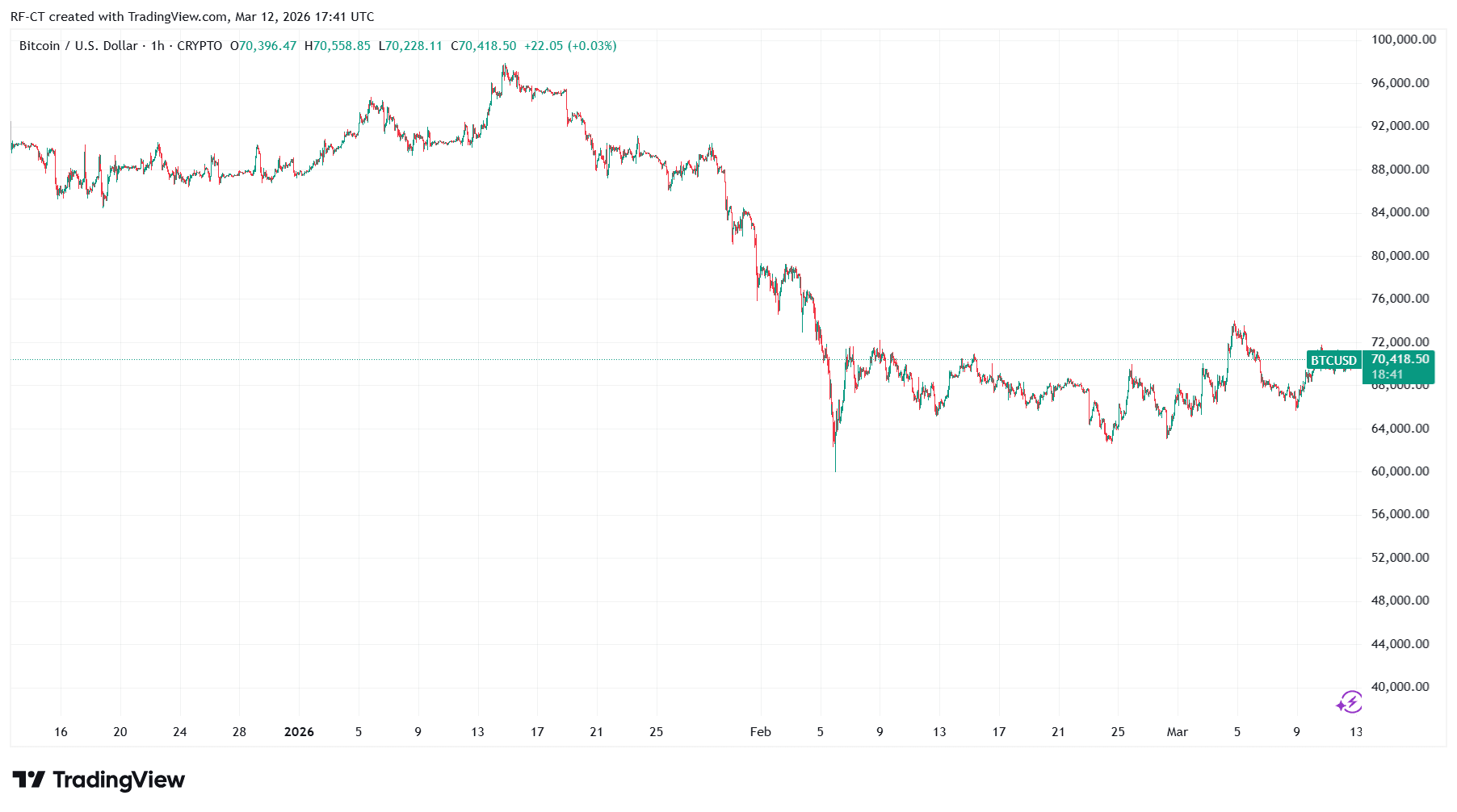

Bitcoin is heading into the weekend with broken near-term structure, elevated macro pressure, and a political catalyst that now sits close to the center of the market’s risk map.

The technical setup has deteriorated in steps over the past two weeks. The macro backdrop has stayed tight as Treasury yields press higher and Middle East risk continues to filter through oil, inflation expectations, and rate-sensitive assets.

Layered on top of both is a familiar variable from recent months, President Donald Trump’s public messaging on Iran, which has repeatedly shifted sentiment across stocks, bonds, oil, and crypto.

His prior weekend social media forays on Tariffs, Venezuela, and Greenland all had similar effects on the market. Trump has done most of his major announcements this year while markets are closed, and right now, things are set up for another intervention.

Within the channel framework tracked since the spot Bitcoin ETF launch period, BTC price has already done the hard part of a bearish rotation. It lost the upper $73,000s, failed to reclaim $71,500 with conviction, rolled through $68,000, and then slipped below $66,900. That sequence leaves the market in a lower value area as Friday trading gives way to the weekend.

In this structure, the next defined support channel lies between $61,700 and $61,100. For now, $61,700 stands out as the next major level that could come into play if macro pressure stays firm and no fresh de-escalation signal arrives from Washington.

Across 400 total interactions with the defined channel boundaries, 304 were bounces, 44 were breaks higher, and 52 were breaks lower. That distribution shows a market that still respects structure. Bitcoin continues to react to these zones in a disciplined way, which gives the current breakdown more analytical value.

The market is not drifting randomly through the map. It is moving from one channel to the next, with each failed reclaim changing the role of the prior boundary.

The clearest example is $71,500. That line served as a key floor during the mid-March sequence, then turned into the strongest visible ceiling once the price broke lower on March 18.

BTC returned to that area several times around March 23 and March 25. Each attempt stalled. That pattern turned $71,500 into the main repair threshold for any bullish recovery. Below it, $68,000 became the next pivot.

BTC briefly re-entered that channel after the first breakdown around March 22, keeping the possibility of stabilization open. That possibility narrowed sharply on March 27 when the price lost $68,000 again, then broke through $66,900 and failed the first retest from below.

That leaves the market with a clean ladder

The first resistance is now $66,900. The next resistance, and the more important reclaim line, is $68,000. Above that sits $71,500, where broader structural repair would begin.

On the downside, the next defined support channel is $61,700 to $61,100. When a market loses one channel and cannot recover its lower boundary, the next channel below becomes the practical draw. That is the state BTC is entering the weekend in now.

The macro overlay has strengthened that downside pull. In its March 18 policy statement, the Federal Reserve kept rates unchanged and said inflation remained somewhat elevated. The central bank’s updated projections preserved a backdrop of restrained policy flexibility and ongoing uncertainty.

Crypto can rally under those conditions, though the burden on market structure increases when long-duration yields are climbing and oil is feeding inflation risk back into the rates complex.

That stress has been visible in the bond market all week. On Friday, the 10-year Treasury yield touched its highest level since July, at 4.48% in early trading before retreating slightly lower.

The precise intraday high matters less than the broader point. Yields have climbed back toward the week’s upper range, and that move has been accompanied by a market that is still pricing geopolitical risk into energy and growth expectations.

That is where Trump’s messaging becomes relevant for Bitcoin over the weekend.

Earlier this week, risk assets responded positively after Trump signaled progress in talks tied to Iran. Stocks rallied, and oil fell after Trump suggested the U.S. and Iran were engaged in talks and hinted at a possible end to the conflict.

Treasury yields also eased briefly on hopes of de-escalation as markets leaned into peace expectations. That relief did not hold for long. Stocks fell again on Friday as markets gave back most of the optimism tied to Trump’s latest delay, and renewed concern over the conflict pushed oil higher.

The pattern is now familiar enough to matter for weekend framing

Trump’s public comments on Iran have repeatedly served as short-term volatility inputs for broader markets, especially when they signal either de-escalation or renewed confrontation.

His social media influence can still sway markets briefly, even as confidence in each new intervention has become more conditional.

For Bitcoin, that means a weekend post that leans toward diplomacy could help produce a relief move into the Monday open. A weekend post that hardens the rhetoric, or no calming message at all, while yields and oil remain firm, would leave the broken structure exposed to another leg lower.

That is the case for keeping $61,700 front and center. The technical path toward that level does not require a new panic event.

The market has already lost the near-term floors that would have contained prices in a higher bracket. The first breakdown through $68,000 around March 22 looked vulnerable to mean reversion, and BTC did in fact re-enter the channel.

The latter break carried more weight because it followed several days of failed recovery attempts. Then came the break through $66,900. Once that level failed and the first retest did not hold, the next support channel below became the relevant destination inside the existing map.

I believe that is also the cleanest way to think about the weekend setup. Bitcoin is no longer trading as though the market is trying to rebuild the damage from March 18. It is trading as though the market is deciding how much lower the next balance area should sit.

I'm not asking whether BTC can rally at all. It can. What I'm looking at now is whether any rally can recover a broken boundary and keep it as support. Until that happens, upside moves serve mainly as tests of resistance.

The thresholds are clear right now

A quick $66,900 reclaim would reduce the immediacy of the latest breakdown. A stronger move back above $68,000 would reopen the argument for a weekend mean-reversion bounce, especially if it coincided with softer yields, calmer oil, or another Trump message that markets read as de-escalatory.

A recovery that reaches $71,500 would carry more significance because that is where the last several rebound attempts failed. Those are the conditions that would force a wider reassessment.

If BTC remains capped below $66,900 and fails to recover $68,000, the lower channel remains active. In that case, $61,700 becomes the next major support to monitor through the weekend, with $61,100 as the deeper boundary of the same bracket.

A move into that zone would fit the logic of the recent structure, the backdrop of present rates, and the political-event risk that now hangs over the weekend.

That also fits the broader character of this decline. The chart shows stepwise deterioration rather than disorder.

First, the market lost the $73,800 to $73,500 zone. Then $72,000 and $71,500 gave way. Then the market spent time failing beneath those levels before slipping through $68,000 and $66,900. Each stage narrowed the market’s room to stabilize higher.

Each failed reclaim added weight to the next lower support channel.

As Friday closes out, Bitcoin is therefore sitting in a narrow but readable setup. Near-term structure is broken. Macro pressure remains elevated as Treasury yields stay near recent highs and Middle East risk continues to influence oil and inflation expectations.

A political catalyst still exists because Trump’s comments on Iran have shown they can move cross-asset sentiment quickly, even if the effect has become less durable with each iteration.

That leaves BTC with a simple weekend map. Reclaim $66,900 and then $68,000, and the market can argue for relief. Stay below them, and $61,700 remains the next obvious level to watch.

The post Bitcoin price is heading for weekend collapse to $61k – will a social media post from Trump save it? appeared first on CryptoSlate.

David Sacks leaves office with wins for crypto infrastructure, while Bitcoin holders are still waiting

David Sacks is out of the formal White House crypto czar role after exhausting the 130-day limit attached to his special government employee status.

The change closes the clearest window for a scorecard. The record is substantial, yet it falls well short of the campaign mood that surrounded Sacks’ appointment and the early industry enthusiasm that followed.

Sacks leaves behind a policy footprint that favored institutional crypto plumbing, bank access, dollar stablecoins, custody, and tokenized financial infrastructure.

The Bitcoin community is now questioning whether Sacks delivered on expectations, with some influential traders declaring,

“Nothing that we elected him for was accomplished.”

Bitcoin holders received a Strategic Bitcoin Reserve through Trump’s March 6, 2025 executive order, yet the reserve arrived as a ring-fencing exercise around seized coins rather than a federal accumulation program.

The distinction sits at the center of the current frustration. The administration delivered movement around crypto. The direct economic gain for Bitcoin holders remained limited.

The most durable critique is straightforward. Sacks helped produce a regime that lowered friction for banks, custodians, issuers, and politically connected capital, while leaving Bitcoin investors with mostly symbolic progress and a widening gap between campaign rhetoric and policy economics.

CryptoSlate’s own coverage traces that arc clearly. Early reporting on Sacks’ appointment captured the industry’s optimism around legal clarity and a friendlier White House.

By March 2025, Sacks was already damping market assumptions after Trump mentioned altcoins for a government stockpile, telling Bloomberg the market was “reading too much” into the move.

More recently, CryptoSlate documented how the policy premium embedded into Trump’s crypto rally evaporated as the market repriced the administration’s actual deliverables.

The sequence leads to a clear conclusion. Washington improved the operating environment for crypto intermediaries. Washington did far less to create a fresh federal demand engine for Bitcoin.

What Sacks actually achieved

In March 2025, the Office of the Comptroller of the Currency confirmed that national banks and federal savings associations could engage in crypto custody, certain stablecoin activities, and distributed ledger participation without first obtaining supervisory non-objection.

Later that month, the FDIC rescinded its earlier approval requirement and stated that FDIC-supervised institutions could engage in permissible crypto-related activities without prior signoff. The SEC’s SAB 122 also rescinded the guidance in SAB 121, reducing one of the accounting burdens that had made institutional custody less attractive.

Those changes were real. They loosened key chokepoints. They improved the economics for regulated incumbents. They also shifted the center of gravity toward institutions that already controlled distribution, compliance, balance sheet capacity, and customer onboarding.

Crypto-native firms gained a less hostile environment, while the immediate beneficiaries sat closer to the banking perimeter than to the Bitcoin holder, who had expected a more direct policy dividend.

The second item is stablecoin legislation. CryptoSlate’s coverage of the GENIUS Act and its analysis of the stablecoin boom that followed makes it clear where Washington found urgency. The bill gave dollar-backed issuers a clearer operating path and reinforced the Treasury-market role that large stablecoin issuers are expected to play.

That is a strategic win for dollar distribution. It is also a strategic win for the firms positioned to warehouse reserves, manage compliance, and package digital dollars into mainstream finance.

The third item is market-structure progress. The CLARITY Act and the broader fight over stablecoin reward definitions show where the administration and Congress invested negotiating capital.

The conflict centered on who gets to control distribution economics around tokenized dollars, how close those products can come to bank deposits, and how much room exchanges and wallets retain to offer reward layers around stablecoins. The subject is meaningful. It also sits one level removed from Bitcoin’s core policy asks.

Viewed together, those wins form a coherent block.

Sacks helped move crypto from a defensive posture under Gary Gensler-era enforcement into a more investable policy architecture for institutions.

Banks, custodians, issuers, exchanges, and tokenization platforms can do more today than they could before Trump returned. The achievement is clear.

The beneficiary base is also clear, and it differs from the constituency that expected a Bitcoin-first White House.

Where the Bitcoin side falls short

The administration can point to the Strategic Bitcoin Reserve as a historic move, and on a formal level, that claim is justified.

The United States designated Bitcoin as a strategic reserve asset and separated it from the broader digital asset stockpile. Sacks stressed that the reserve would focus on long-term stewardship of seized Bitcoin, while altcoins in the stockpile could be sold, rebalanced, or staked at Treasury discretion.

The reserve never moved into the zone that most Bitcoin holders cared about. The administration did not launch an immediate federal buying program.

It did not announce a schedule for open-market accumulation. It did not create a standing mechanism that would pull supply from the market in size.

The administration’s digital asset roadmap highlighted the same limitation. The reserve existed, while the acquisition path remained opaque.

The distinction is where disappointment hardens. A reserve built from forfeited Bitcoin changes custody and future sale behavior. It leaves the market’s demand profile largely untouched compared with the campaign language many Bitcoin holders had priced in. Preservation and accumulation produce very different outcomes for price formation.

That difference explains why some of the anger on crypto feeds is directionally understandable. Bitcoin holders were promised something more forceful than what arrived.

Stablecoins, tokenized finance, and institutional rails moved faster through Washington than Bitcoin-specific demand policy.

The administration’s most visible crypto progress also aligned neatly with constituencies that monetize issuance, distribution, custody, and compliance.

The administration delivered enough for institutions to monetize the next phase of digital finance. Bitcoin holders still lack a federal policy catalyst with direct market impact.

Why the market has re-priced the promise

Markets eventually force rhetoric to clear. CryptoSlate’s coverage of the collapse in the post-election policy premium captures that shift.

Investors who once priced a pro-crypto White House as a broad tailwind later discovered that not every crypto win maps onto Bitcoin in the same way. Stablecoin legislation can favor dollar liquidity and tokenized settlement.

Bank guidance can favor custody and compliance capacity. Those developments help the ecosystem. They do far less to create a new marginal buyer for BTC.

The market backdrop today underlines the point. Bitcoin trades around $66,569, down about 3.9% on the day. Spot ETF flows have also shown a more selective institutional appetite than the campaign-era narrative implied.

March data from Farside Investors shows sharp swings between inflow and outflow sessions, a pattern that fits tactical allocation and de-risking behavior more than a simple policy-driven repricing higher.

Bitcoin remains in a familiar place. Price is still governed by liquidity conditions, rates, ETF demand, and macro positioning. Washington can improve the operating environment.

Washington has not yet rewritten Bitcoin’s demand curve.

The week ahead, Bitcoin stays in focus

The coming week is more likely to shape Bitcoin through macro channels than through additional post-Sacks messaging.

Friday, April 3 brings the March employment report. Earlier in the week, the market will also parse fresh labor and activity signals, including the usual month-turn growth and employment data that feed directly into rate expectations, Treasury yields, and broader risk appetite.

That sequence feeds into crypto through a straightforward transmission path. Softer labor data can ease yield pressure and help duration-sensitive risk assets.

Firmer labor data can push yields higher, tighten financial conditions, and pressure the assets that benefited from liquidity optimism. Bitcoin continues to trade inside that macro framework even while crypto policy remains a live political theme.

The gap between symbolic and economic progress is therefore becoming harder to ignore.

A reserve announcement built on seized coins can support sentiment. A banking reset can improve access. Stablecoin law can strengthen dollar-based crypto rails.

None of those developments guarantee stronger Bitcoin demand into a macro-heavy week.

The market still needs sustained ETF absorption, improving liquidity conditions, or an actual federal accumulation mechanism that removes supply from circulation in size.

Sacks leaves office having helped build the legal and regulatory lanes for the next phase of crypto finance in the United States. Banks got clearer permission. Custodians got relief. Stablecoin issuers got a path. Tokenized capital markets moved closer to the center of the American financial stack.

Bitcoin holders got recognition, a reserve label, and fewer fears around forced government selling.

They did not get the forceful federal accumulation program that campaign rhetoric had implied.

Sacks leaves a policy architecture that works best for institutional crypto, dollar tokenization, and the firms positioned to collect fees at the system’s chokepoints.

Bitcoin remains the political symbol. Stablecoins and tokenized finance have been the operational priority.

Until that hierarchy changes, frustration among Bitcoin holders is likely to keep rising, especially in weeks when macro data, ETF flows, and yield pressure continue to drive price more than Washington does.

The post White House crypto czar leaves office after securing crypto wins for banks and institutions instead of Bitcoin appeared first on CryptoSlate.

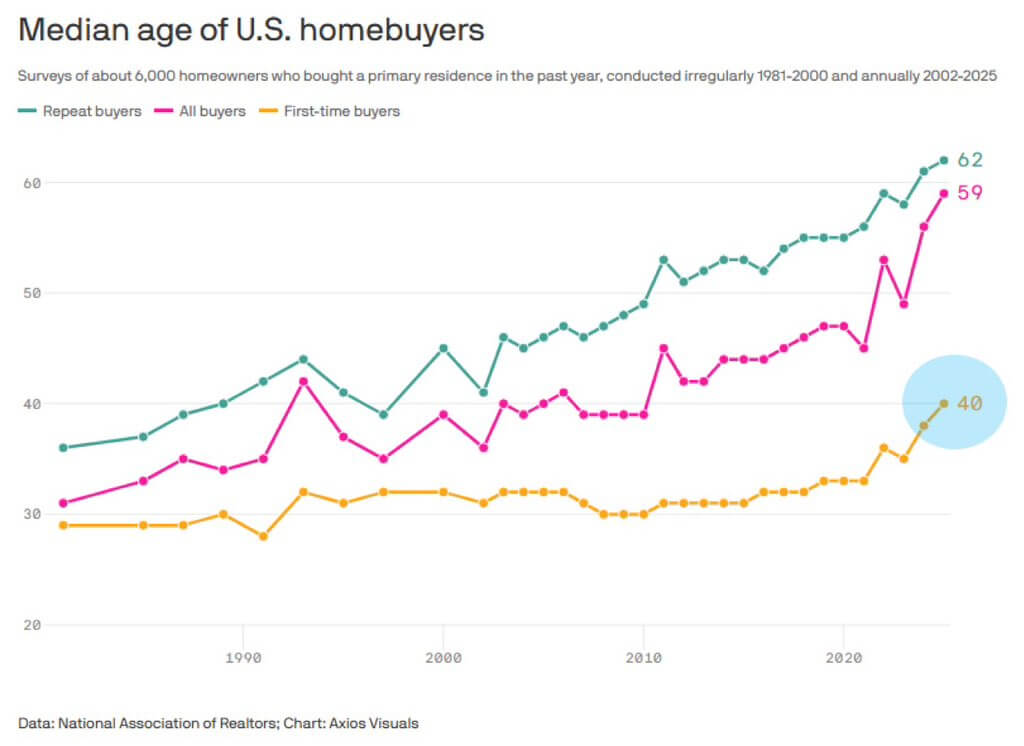

Bitcoin is moving deeper into US household finance as homebuyers squeezed by high borrowing costs and limited supply look for new ways to fund a down payment without selling their digital assets.

On March 26, Better Home & Finance and Coinbase launched a structure that lets eligible borrowers pledge Bitcoin or USD Coin (USDC) stablecoin to secure a separate loan for a down payment while still taking out a standard conforming mortgage on the home.

The arrangement brings crypto into one of the most closely watched parts of the U.S. credit system at a time when affordability pressures are already reshaping who can buy a house and when.

The timing is central to the pitch as Realtor.com’s 2026 report put the US housing supply gap at 4.03 million homes.

This comes as the average 30-year mortgage rate recently climbed to 7%, while total mortgage applications fell 10.5%, and purchase applications dropped 5.4%. At the same time, first-time buyers accounted for just 21% of the market in the latest National Association of Realtors profile.

Against that backdrop, lenders and crypto firms are betting that a growing class of would-be buyers has wealth in digital assets but lacks the cash liquidity needed to clear one of the biggest barriers to homeownership.

A new route into the mortgage market

The Coinbase-backed product is aimed at borrowers who want to retain exposure to crypto markets instead of liquidating holdings to raise cash for a down payment.

For many, that decision is about more than market timing. Selling crypto can also trigger a tax bill and force investors to reduce positions they view as long-term holdings.

Considering this, the structure is built around two loans at closing. The first is a standard mortgage on the property. The second is a privately financed loan secured by pledged crypto and used to fund the cash down payment.

Better says the 15-year and 30-year fixed mortgage options will be available, subject to credit approval, and that the loans are designed in accordance with Fannie Mae guidelines so that the mortgage remains a conforming loan.

That distinction is important. The product does not replace the traditional mortgage with a crypto loan. Instead, it wraps a crypto-secured financing layer around the down payment while leaving the main mortgage in a conventional format.

For borrowers using Bitcoin, the initial collateral value must be at least 250% of the loan amount in fiat. For borrowers using USDC, the initial collateral value must be at least 125%.

In practical terms, a borrower could pledge $250,000 in Bitcoin to unlock a $100,000 cash-down-payment loan, or $125,000 in USDC for the same result.

The companies are promoting the arrangement as a way to preserve ownership of digital assets while gaining access to the housing market. Better says both loans can share the same interest rate and amortization term, creating a single combined monthly payment.

Housing strain creates an opening

The product's appeal is tied directly to a housing market that has become harder to enter, especially for younger buyers.

The median age of a first-time homebuyer reached 40 in 2025, according to the National Association of Realtors, reflecting the combined effect of high mortgage rates, elevated home prices, and limited inventory.

The pressure is even more severe for households lower on the income scale. The NAHB/Wells Fargo Cost of Housing Index for the second quarter of 2025 showed that a typical family needed 36% of its income for a mortgage payment on a median new home. For lower-income households, that share rose above 71%.

Those figures help explain why companies see an opportunity in linking digital assets to housing finance. Traditional underwriting relies heavily on documented income, credit history, and cash reserves.

That framework tends to favor households that have already built wealth through home equity, rising incomes, or long-established financial assets.

At the same time, millions of Americans have built positions in crypto. For context, around 20% of US adults, equivalent to 52 million people, hold some form of crypto asset, and the majority of them are young.

The NCA 2025 State of Crypto Holders report confirmed that 67% of token holders are 45 or younger, and 26% earn less than $75,000 a year.

That gives the product a clear target market: younger buyers with meaningful crypto exposure but limited willingness, or ability, to convert those holdings into cash at the point of purchase.

How the crypto pledge works

The companies have tried to structure the product to look less like a volatile crypto loan and more like a mortgage-compatible financing tool.

Borrowers who pledge Bitcoin or USDC are not subject to margin calls or top-up requirements if the market value of their collateral falls.

Better says market movements alone do not trigger liquidation. Instead, the pledged assets are only at risk if a borrower becomes 60 days delinquent on payments, a threshold the companies say mirrors the treatment of payment stress in conforming mortgages.

The crypto is held in custody for the life of the down payment loan and returned once that obligation is repaid. Borrowers cannot trade the pledged assets while they are locked up, which preserves ownership but restricts flexibility.

For USDC borrowers, the stablecoin can continue to earn rewards, which could help offset mortgage servicing costs and reduce the borrower’s net effective financing burden.

Meanwhile, the broader ambition goes beyond one mortgage product. Better and Coinbase say they intend, over time, to expand the range of eligible digital assets to include tokenized equities, fixed income, and other tokenized real estate assets.

This represents a sign that they see the mortgage offering as an early step in bringing on-chain wealth into mainstream consumer finance.

Policy support and political resistance

Meanwhile, this launch is arriving in a political climate that has become more receptive to crypto, but not without resistance.

Fannie Mae’s role, along with oversight from the Federal Housing Finance Agency, could help make such products more mainstream than earlier crypto-linked mortgage offerings.

Last year, FHFA Director Bill Pulte directed Fannie Mae and Freddie Mac to prepare to count crypto as an asset on mortgage applications, reflecting broader support for the digital-asset industry from the Trump administration.

That policy opening created room for commercial products built around crypto wealth, but it also drew criticism from lawmakers who view the idea as a new source of risk for housing finance.

Democratic senators, led by Elizabeth Warren, objected to the proposal, arguing that the current policy does not permit federally backed mortgage channels to consider cryptocurrency unless it has first been converted into US dollars and properly documented.

They warned that expanding underwriting criteria to include unconverted crypto could introduce fresh risks to both the housing market and the broader financial system.

That criticism goes to the heart of the debate around products like Better’s.

Supporters see them as a way to translate digital wealth into real-world access without forcing borrowers to sell assets and leave the market. Critics see a danger in bringing a volatile and still-developing asset class closer to the foundations of US home lending.

So, the final outcome may depend on whether crypto-backed mortgages remain a niche tool for affluent digital-asset holders or evolve into a broader financing channel for buyers shut out by the traditional down payment hurdle.

The post Homebuyers can now borrow against Bitcoin to get a mortgage without selling or liquidation risk appeared first on CryptoSlate.

Cryptoticker

Global financial markets are once again facing rising geopolitical uncertainty. Oil prices are climbing as tensions escalate across key energy regions, while governments and energy companies move quickly to protect critical infrastructure.

A new development illustrates how rapidly the global energy landscape is evolving. The world’s largest oil producer, Saudi Aramco, is reportedly in talks with Ukrainian firms to purchase specialized interceptor drones designed to defend oil facilities from potential Iranian drone attacks.

At the same time, President Donald Trump has stated that rising oil prices could benefit the United States because the country has become one of the world’s largest oil producers.

Together, these developments highlight how energy security is becoming a central issue for global markets — and why crypto investors are paying attention.

Oil Infrastructure Is Becoming a Strategic Target

Energy facilities have increasingly become targets during geopolitical conflicts. Drone attacks on refineries, pipelines, and export terminals can disrupt global oil supply within hours.

For companies like Saudi Aramco, protecting infrastructure is therefore a top priority.

Ukraine has developed sophisticated drone defense systems during the Russia–Ukraine War, including interceptor drones capable of stopping incoming unmanned aerial vehicles before they reach critical targets.

Reports indicate Saudi Aramco is now exploring these technologies to strengthen its defenses against potential attacks.

This reflects a broader shift in modern warfare, where relatively inexpensive drones can threaten infrastructure worth billions of dollars.

Oil Prices React to Rising Risk

Energy markets are extremely sensitive to geopolitical tensions. Even the threat of disruption to major producers can push oil prices sharply higher.

Recent headlines have already contributed to volatility in financial markets, with billions of dollars wiped from global stock valuations as investors reacted to rising geopolitical risk and oil prices moving higher.

One of the most sensitive energy chokepoints remains the Strait of Hormuz, through which roughly 20% of global oil exports pass.

Any disruption to shipping in this region could trigger major price spikes and ripple effects across global markets.

Trump Highlights the U.S. Energy Advantage

President Donald Trump has also weighed in on the situation, noting that the United States benefits from high oil prices due to its status as a major producer.

Over the past decade, the U.S. has dramatically increased production through shale extraction, transforming the country into one of the world’s largest oil suppliers.

If geopolitical tensions push oil prices higher, American energy exports could play an increasingly important role in stabilizing global markets.

However, higher oil prices can also contribute to inflation and market volatility.

Why Crypto Investors Are Watching Oil

For cryptocurrency markets, developments in energy markets often serve as early signals of macroeconomic changes.

When oil prices surge, several effects tend to follow:

- Inflation expectations increase

- Central banks may delay interest rate cuts

- Global financial markets become more volatile

These conditions can initially pressure risk assets such as cryptocurrencies.

At the same time, prolonged geopolitical instability can strengthen Bitcoin’s narrative as a hedge against global uncertainty.

As traditional markets react to geopolitical shocks, some investors begin exploring alternative stores of value.

Is Bitcoin Becoming a Crisis Hedge?