Cryptocurrency Posts

Crypto Briefing

The partial reopening of the Strait of Hormuz alleviates immediate oil supply concerns but highlights ongoing market volatility and uncertainty.

The post US confirms partial reopening of Strait of Hormuz, easing oil supply fears appeared first on Crypto Briefing.

Ostium launched a real time decentralized execution layer with Jump as hedging partner after topping $50B in trading volume.

The post Ostium launches decentralized execution layer with Jump as hedging partner appeared first on Crypto Briefing.

Alphabet's increased AI investment may boost long-term growth but risks near-term margin pressure amid regulatory challenges.

The post Alphabet’s $175B-$185B AI capex plan doubles prior levels amid antitrust scrutiny appeared first on Crypto Briefing.

The stalled peace talks and US review signal potential prolonged regional instability, affecting geopolitical dynamics and market confidence.

The post US reviews Iran proposal as Israel-Iran peace talks stall appeared first on Crypto Briefing.

Iran's move suggests potential diplomatic openings, reducing immediate oil supply fears and impacting market predictions on crude prices.

The post Iran allows Japanese supertanker through Strait of Hormuz, easing supply fears appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Blockstream Launches Jade Core to Simplify Bitcoin Self-Custody Without Sacrificing Security

Blockstream has introduced Jade Core, a new hardware wallet designed to expand access to Bitcoin self-custody through a simplified user experience.

The device builds on the company’s existing Jade lineup and retains its open-source security model while targeting a broader base of users.

The launch reflects a shift in hardware wallet design as providers seek to reduce barriers tied to self-custody. Many existing solutions have focused on experienced users, with complex setup processes and technical requirements.

Jade Core addresses this gap through guided onboarding and tighter integration with Blockstream’s mobile and desktop applications.

The device supports Bluetooth pairing and enables users to manage transactions across platforms without relying on custodial services. Private keys remain stored on the device, and all transaction signing occurs offline. This architecture reduces exposure to online threats while preserving user control over assets.

Jade Core includes several core security features tied to Blockstream’s existing framework. These include open-source hardware and firmware, allowing users and developers to audit the system. The device also incorporates Blind Oracle PIN protection, which uses encrypted authentication to guard against unauthorized access, including cases involving physical compromise.

Users can verify device authenticity during setup, a feature designed to address supply chain risks in hardware wallets. The device display has been updated to support clearer transaction verification, reducing the risk of user error during transfers.

Blockstream said Jade Core is part of their broader effort to expand direct ownership of Bitcoin. The company has emphasized counterparty risk tied to centralized exchanges, particularly following a series of failures and security incidents across the digital asset sector. Hardware wallets have gained traction as users seek greater control over funds.

Blockstream: Retail-facing tools, institutional rails

According to Blockstream executives, Jade Core aligns with a wider product strategy that connects retail-facing tools with institutional infrastructure. The company aims to support both individual users and larger market participants through a unified ecosystem built on Bitcoin-native technology.

The release comes at a time when demand for self-custody solutions continues to grow alongside Bitcoin adoption. By reducing complexity without altering core security assumptions, Blockstream is positioning Jade Core as an entry point for users transitioning away from custodial platforms.

Jade Core expands competition in the hardware wallet market, where usability and security remain key differentiators. As adoption increases, providers face pressure to deliver tools that balance ease of use with strong protections tied to open and verifiable systems.

This post Blockstream Launches Jade Core to Simplify Bitcoin Self-Custody Without Sacrificing Security first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Amboss Activates RailsX, Enabling Self-Custody Stablecoin Trading on Bitcoin Lightning

Amboss has activated RailsX, a Lightning-native exchange layer that allows users to trade bitcoin against stablecoins without relinquishing custody, marking a shift in how dollar-denominated liquidity can move across Bitcoin infrastructure.

The launch introduces two trading pairs, USDT-L and USDC-L, issued by Speed Wallet, and opens them to peer-to-peer trading across the Lightning Network. Trades route through existing Lightning channels and settle atomically within seconds, with no centralized order book or intermediary holding user funds.

The release moves stablecoin functionality on Lightning beyond experimentation. While the concept of dollar-pegged assets on Bitcoin’s second layer has circulated for years, implementation has remained limited. Speed Wallet has operated wrapped stablecoins within its own ecosystem for roughly 18 months, providing a closed-loop proof of concept.

RailsX extends that model to the broader network, allowing any compatible node to access the same infrastructure.

Amboss and Thunderhub

RailsX will integrate with Thunderhub, a Lightning node management interface, which serves as the routing layer for these trades. Users execute swaps directly from their own nodes, maintaining control of private keys throughout the transaction lifecycle. Settlement occurs through Lightning’s existing payment channels, removing reliance on bridges or external chains.

Amboss said that RailsX is an extension of its existing Rails product, which focuses on Lightning liquidity provisioning. Together, the two systems form a combined liquidity and trading layer: users can allocate capital to channels, earn yield, and trade against that liquidity without transferring assets to an exchange.

The absence of an order book alters how price discovery occurs. Instead of matching bids and asks in a centralized system, trades execute through routed liquidity across the network. This design mirrors how Lightning processes payments, though applied to asset exchange rather than simple transfers.

Speed Wallet provides issuance and backing for USDT-L and USDC-L, with the assets designed to remain fully reserved. The company’s role introduces a hybrid structure: while trading remains self-custodial and peer-to-peer, stablecoin issuance still depends on a centralized entity.

The development arrives as demand for stablecoin liquidity continues to expand across crypto markets, particularly in regions where dollar access remains constrained. By embedding stablecoin trading within Bitcoin’s payment rails, RailsX offers a pathway for Lightning to compete with alternative ecosystems that have dominated stablecoin activity.

Whether RailsX can scale depends on liquidity depth and node participation. Early trading activity will test whether a routing-based exchange can support consistent pricing and volume without centralized coordination.

For now, the launch represents a functional step toward integrating stablecoin utility into Bitcoin’s native infrastructure.

This post Amboss Activates RailsX, Enabling Self-Custody Stablecoin Trading on Bitcoin Lightning first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Billionaire Tim Draper: You Should Be Scared If You Don’t Own Bitcoin

Speaking on the Nakamoto Stage, Tim Draper told attendees that bitcoin has entered the financial mainstream and that governments now roll out “the red carpet” for the industry. He said the community is “starting to feel like something is happening” as adoption grows, and he cast that shift as the early phase of a larger transition in the money system.

In his view, people will move in stages: first from dollars to stablecoins, then from stablecoins to bitcoin as the final store of value and unit of account.

Draper praised Satoshi Nakamoto’s design of BTC as a system with no government control, no middleman banks, and no traditional account records. He described his own early journey with the asset, including buying large amounts of BTC, then losing those holdings amid front-running and failures at Mt. Gox. That episode led him to question whether the experiment was worth the risk until he watched crypto usage spread in markets around the world and decided to buy again.

To illustrate the fragility of fiat money, Draper told a personal story about a “one–million–dollar bill” that his father gave him when he was young. The bill turned out to be a Confederate note with no value, which he held up as a warning that government currencies can fail, leaving savers with worthless paper.

He connected that story to his decision to purchase bitcoin from the U.S. government in an auction of seized coins, where he paid above market because he viewed bitcoin as a superior long-term asset.

Draper: You should be scared if you don’t own bitcoin

Draper outlined a scenario in which retailers begin by accepting bitcoin alongside other payment methods and then transition to accepting only bitcoin.

In that world, he said, consumers would rush to banks to pull out their money and convert into BTC as trust in national currencies declines. He told the audience that anyone who manages a family “ought to have about six months’ worth of bitcoin” as protection against such a breakdown.

He extended that warning to sovereigns facing inflation or fiscal stress. If a government encounters hyperinflation and holds no BTC on its balance sheet, Draper argued, its currency and the wealth of its officials could become worthless in real terms.

“You should be scared if you don’t own bitcoin,” Draper said he is telling people these days, adding that those without exposure “should be very, very worried.”

Draper closed with a call to action aimed at the entire BTC ecosystem around him. He said that “those of us who have bitcoin are gonna help steer the world” as legacy currencies lose value, and he told attendees to go home and tell their families to buy bitcoin, their governments to buy bitcoin, and their friends to buy BTC.

Addressing founders and builders, he urged entrepreneurs to “push it as hard as you can,” saying that broad BTC ownership is both a hedge against currency risk and a path to a new monetary standard.

This post Billionaire Tim Draper: You Should Be Scared If You Don’t Own Bitcoin first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

House Republicans Warn That the America’s Bitcoin Weakness Will Benefit China

Three members of Congress positioned digital asset regulation as a matter of national security and economic competition during a panel discussion at The Bitcoin 2026 Conference in Las Vegas on Monday.

Reps. Mariannette Miller-Meeks (R-Iowa), Zach Nunn (R-Iowa), and Mike Lawler (R-N.Y.) spoke on “The Bitcoin Bloc: A New Force in American Politics,” moderated by Faryar Shirzad, Chief Policy Officer at Coinbase.

Miller-Meeks described Bitcoin as “financial democracy” and linked cryptocurrency adoption to America’s 250th anniversary, framing support for digital assets as patriotic. She cited the Chinese Communist Party as a threat and characterized crypto policy as a national security issue.

The Iowa congresswoman shared her background working through medical school and highlighted Bitcoin’s potential to protect women experiencing domestic abuse or violence.

She said digital assets can provide women with resources beyond government reach, citing Canada’s trucker protest as an example of government intervention in financial accounts. Miller-Meeks acknowledged that older Americans express concerns about digital asset safety.

Chinese is driving bitcoin policy urgency

Both Miller-Meeks and Nunn emphasized competition with China as a driver for U.S. crypto policy. Miller-Meeks stated that China continues to pursue leadership in the digital asset sector but said the United States remains the best environment for innovation.

Nunn warned that failing to advance American leadership in Bitcoin and digital assets creates national security risks. He called for holding China accountable and said losing the November midterm elections could reverse 18 months of legislative progress, allowing adversaries to gain ground while the U.S. falls behind.

“Decisions and elections have consequences,” Nunn said, pointing to specific anti-crypto Democrats as he discussed the stakes of the upcoming midterm elections.

Nunn highlighted progress in Congress and the crypto sector, noting that the SEC under former Chair Gary Gensler imposed fines in the millions of dollars for violations involving concepts Gensler did not understand. Gensler was fired earlier in the Trump administration.

Lawler referenced the GENIUS Act as a positive step but said Congress must establish a comprehensive federal regulatory framework.

He cited Treasury Secretary Scott Bessent’s op-ed in The Wall Street Journal and stated that passing regulatory clarity will position America at the forefront of the digital asset space. Lawler said SEC regulations should serve the crypto industry’s best interests.

As a New Yorker, Lawler said he wants the crypto industry to remain in New York and feel secure operating in the state.

The ‘double taxation’ of bitcoin mining

Nunn criticized double taxation on Bitcoin mining operations, questioning why the U.S. taxes Bitcoin mining differently than other forms of asset extraction. He said excessive taxation drives innovation to other countries and emphasized the need to avoid making it difficult to conduct business in the United States.

The panel discussion reflected a broader shift in congressional Republican attitudes toward digital assets, with lawmakers framing crypto policy through the lens of geopolitical competition and individual financial freedom rather than consumer protection or financial stability concerns that dominated earlier regulatory debates.

This post House Republicans Warn That the America’s Bitcoin Weakness Will Benefit China first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Lawmakers Warn Crypto Clarity Will Decide U.S. Leadership as 2026 Election Looms

U.S. lawmakers and White House officials used a Nakamoto Stage panel to argue that clear crypto rules will decide whether the United States leads or cedes ground in the next phase of financial innovation.

The discussion, titled “Are We Getting More Clarity?”, focused on the Clarity Act, enforcement under past administrations, and the risk that political swings could undo progress on crypto regulation.

Senator Cynthia Lummis warned that another hostile administration would mean “game over for sensible regulation,” framing the 2026 election cycle as a direct test of whether Congress can lock in a durable framework for digital assets.

She argued that predictable rules are now essential for builders and capital, and said the industry cannot plan around policy that shifts with each change in the White House. Lummis also pushed back on concerns about crypto and crime, saying “it’s easier to solve crimes in digital assets than fiat currencies” because transaction records give law enforcement a trail that cash does not.

Witt:USA should dominate in crypto

White House digital asset adviser Patrick Witt set out an aggressive vision for U.S. leadership. “We want to dominate,” he said, calling crypto “the future of financial infrastructure” and tying that claim directly to passage of the Clarity Act. He said that once lawmakers deliver a clear regime for digital assets, “Bitcoin and crypto will take off like a rocketship,” with greater integration into markets and the banking system.

Witt described the bill’s focus as defining obligations for exchanges that list exchange-traded products, wallet providers, and developers who build on Bitcoin, and said that set of rules is “critically important” so market participants understand their responsibilities and can connect Bitcoin more deeply to the broader financial system.

Witt also criticized earlier policy and enforcement choices. He said the industry “got wrongly targeted and criticized” in recent years, which he argued pushed innovation offshore and let foreign hubs claim core parts of the market.

He pointed to the location of the largest centralized exchanges outside the United States as “a failure of U.S. leadership,” and cast the Clarity Act as a chance to reverse that trend. In his view, the measure could bring trading venues and developers back onshore and support a domestic ecosystem around Bitcoin exchange-traded products, custody, and payments infrastructure.

Across the panel, speakers returned to the same question: whether Washington will offer lasting clarity or continue to rely on fragmented enforcement. Lummis framed the stakes in terms of investor protection and national competitiveness, while Witt stressed the opportunity to anchor the next wave of financial infrastructure in the United States. Both cast the coming legislative window, and the election that follows it, as a turning point for Bitcoin, broader crypto markets, and the country’s role in them.

This post Lawmakers Warn Crypto Clarity Will Decide U.S. Leadership as 2026 Election Looms first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

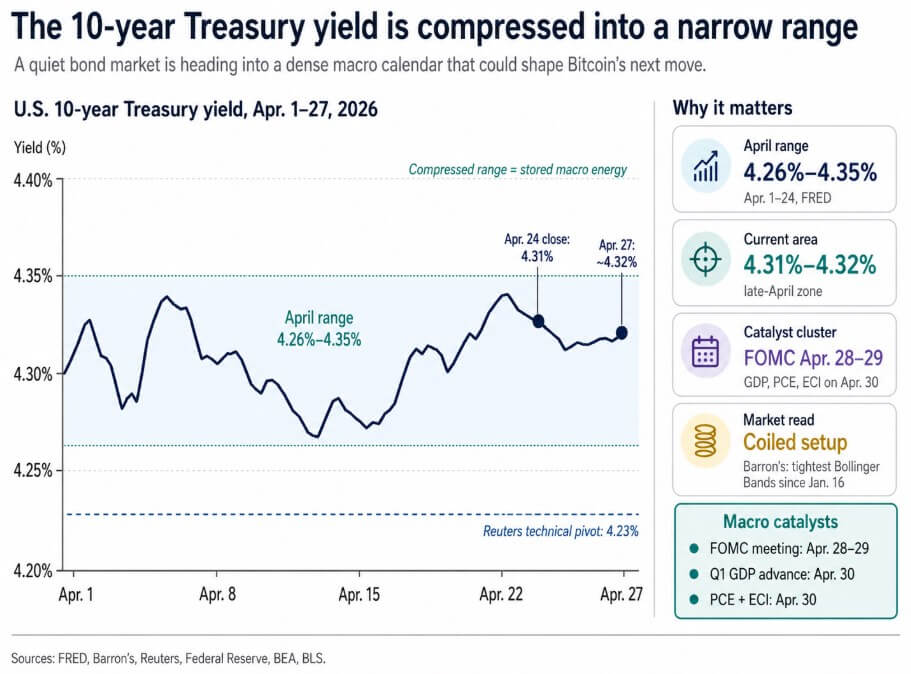

Everyone watching Bitcoin this week is watching the Federal Reserve, while the more important tell may be sitting in the Treasury market, where the 10-year yield has compressed into one of its tightest ranges of the year just as a dense macro calendar opens.

Bitcoin's recovery now rests on renewed institutional inflows and the assumption that liquidity conditions will not tighten again. If Treasuries choose a direction before that assumption is tested, the bond market could drive Bitcoin's next move independently of any crypto-specific catalyst.

The 10-year yield spent Apr. 1 through Apr. 24 inside a band of 4.26% to 4.35%, closing at 4.31% on Apr. 24 per FRED data.

Barron's reported that the 10-year Bollinger Bands had narrowed to their tightest since Jan. 16, a classic coiled setup, and Reuters' technical commentary placed the yield inside a larger symmetrical triangle that frequently precedes a sharp directional move.

On Apr. 27, the 10-year had ticked back toward 4.32%, with commodity prices and geopolitical risk feeding inflation expectations, adding inputs to yield direction that run well outside the Fed's control.

A compressed yield range is a market storing energy before a decision.

The event cluster that could release that energy arrives in rapid succession. The FOMC meets Apr. 28-29, the BEA publishes the advance first quarter GDP estimate alongside March Personal Income and Outlays and the PCE deflator on Apr. 30, while the Employment Cost Index also lands that morning.

That is three macro readings in two days, enough to move Treasuries materially in either direction and enough to change the financial conditions backdrop that Bitcoin is currently relying on.

The key points

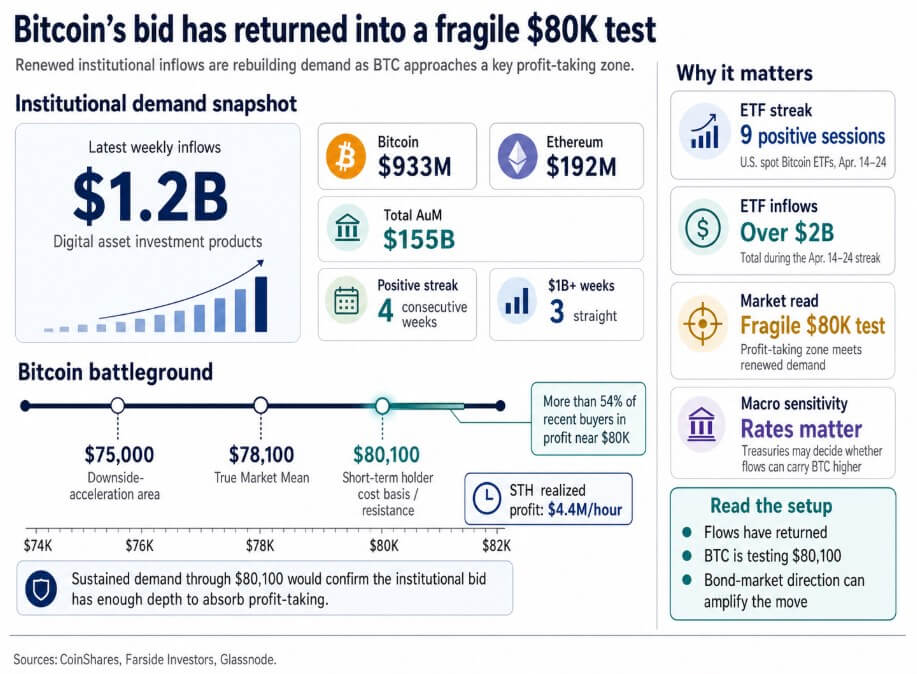

Bitcoin is where a Treasury repricing could first show up, as the crypto bid has rebuilt into an already fragile technical area.

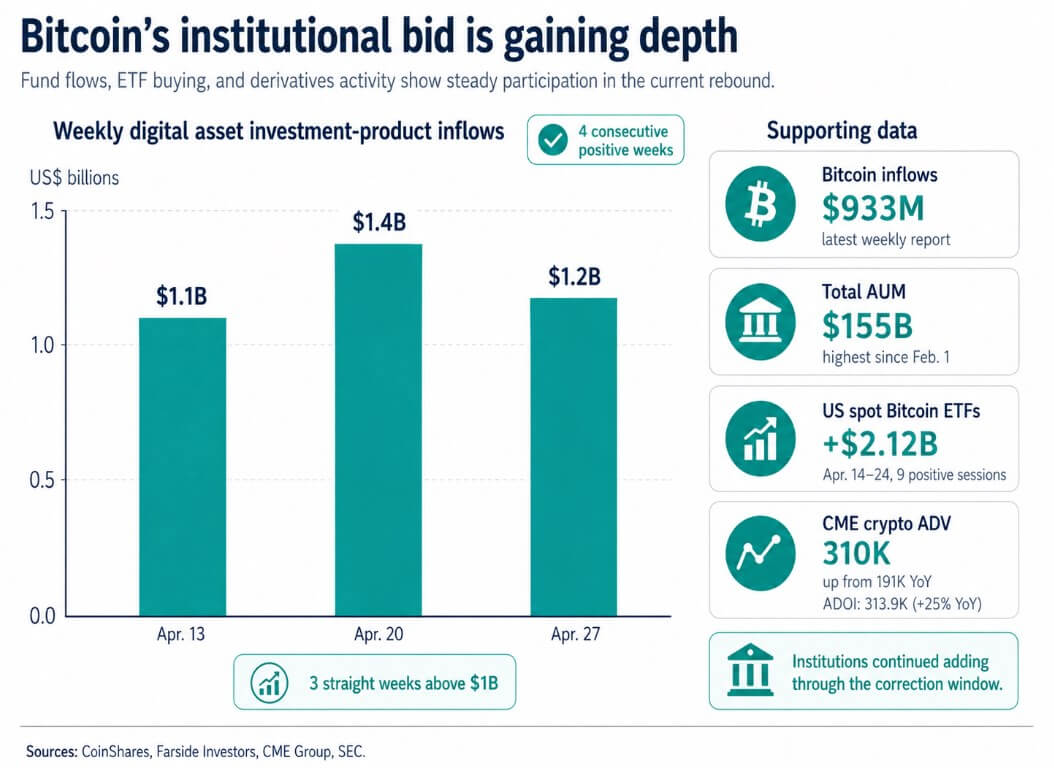

CoinShares' latest weekly report recorded $1.2 billion in crypto investment product inflows, the fourth consecutive positive week and the third straight above $1 billion, with $933 million flowing to Bitcoin, $192 million to Ethereum, and total assets under management climbing to $155 billion.

Farside Investors' daily ETF data show that US spot Bitcoin ETFs posted nine straight positive sessions from Apr. 14 to Apr. 24, totaling over $2 billion in inflows.

The risk is that buyers return just before Treasuries choose a direction. CoinShares' Mar. 23 note shows that weekly inflows slowed sharply and crypto products suffered $405 million in post-FOMC outflows once markets read that meeting as a hawkish pause.

The crypto bid at the time was genuine, and a macro repricing overtook it anyway.

That episode is directly relevant now because Bitcoin is approaching its $80,000 test with the same ingredient in place and the same unresolved variable of what the bond market decides to do next.

What on-chain data shows

Glassnode's Apr. 22 report noted that Bitcoin reclaimed the True Market Mean at $78,100, with the short-term holder cost basis at $80,100 as the immediate resistance ceiling.

ETF flows turned modestly positive again, and spot demand showed early recovery, while the short-term holder realized profit spiked to $4.4 million per hour.

Glassnode also noted that Bitcoin's own implied and realized volatility has compressed, leaving no premium in options pricing. Treasuries and Bitcoin markets are coiled at the same time, and the rates market is the one with more immediate cause to move first, given the macro calendar sitting directly in front of it.

Glassnode's framework gives the battleground its coordinates, as sustained demand through $80,100 would confirm the institutional bid has enough depth to absorb profit-taking.

A failure there that pushes BTC back toward $78,100 would leave the True Market Mean as the last meaningful support before Glassnode's $75,000 downside-acceleration area comes into play.

The bond market's direction will determine which of those outcomes resolves.

Potential outcomes

The bull case flows from yields moving lower. If the 10-year closes below the April floor near 4.26%, and especially if it breaks through Reuters' 4.23% technical pivot, Bitcoin gets the cleanest macro environment its current rally could ask for.

Falling yields reduce the discount-rate drag on risk assets, support the liquidity trade, and give the $1.2 billion weekly inflow pace a better chance of forcing BTC through the $80,100 resistance ceiling, with enough absorption to hold.

In that setup, the nine-session ETF streak and CoinShares' four consecutive positive weeks would read as early evidence of a durable demand regime, and the rally's test period would be over.

The October 2025 total AUM peak of $263 billion serves as the relevant benchmark for how far the institutional re-engagement has yet to go.

The bear case flows from yields breaking higher. If the 10-year pushes above 4.35% and starts moving toward Reuters' 4.6% upside resolution area, financial conditions will tighten at exactly the moment Bitcoin is pressing into a zone where more than 54% of recent buyers are sitting on profit.

BTC stalls at $80,100, the profit-taking that Glassnode is already flagging at $4.4 million per hour accelerates, and sellers test the True Market Mean at $78,100.

If that level fails, Glassnode's $75,000 downside-acceleration area comes into play, and markets would reframe the entire inflow streak as institutional capital that arrived before the bond market closed the door.

The March precedent makes that sequence concrete, as even $1 billion-plus weekly demand could not prevent $405 million in post-FOMC outflows once the macro read turned hawkish. The same mechanism is available again.

| Scenario | What happens in Treasuries | BTC response | Key levels | What it means |

|---|---|---|---|---|

| Bull case | The 10-year closes below the April floor near 4.26% and breaks through Reuters’ 4.23% technical pivot | Bitcoin gets the cleanest macro backdrop, ETF and ETP inflows gain support, and BTC has a stronger chance of clearing and holding above $80,100 | 10-year: below 4.26%, then below 4.23% | BTC: clears $80,100 and stays above $78,100 | Lower yields validate the institutional bid and turn the recent inflow streak into evidence of a more durable demand regime |

| Neutral / flow-dependent case | The 10-year stays inside the April range between 4.26% and 4.35% | Bitcoin remains dependent on continued ETF, ETP, and spot demand to absorb supply around resistance, with no clear macro tailwind or headwind | 10-year: 4.26%–4.35% | BTC: holds between $78,100 and $80,100 | Macro stays unresolved, so the rally lives or dies on whether institutional flows can keep doing the work by themselves |

| Bear case | The 10-year breaks above 4.35% and starts moving toward Reuters’ 4.6% upside resolution area | Financial conditions tighten as BTC presses into a profit-heavy zone, Bitcoin stalls at $80,100, sellers test $78,100, and $75,000 comes into play if support fails | 10-year: above 4.35%, then toward 4.6% | BTC: fails at $80,100, loses $78,100, risks $75,000 | Higher yields reprice liquidity, and the bond market turns Bitcoin’s inflow streak into another macro-driven failed rally |

Bitcoin's next move may originate in the Treasury market. The institutional bid has returned across enough channels to confirm a broad recovery in demand.

However, the bid has returned before the bond market has signaled if macro conditions will help or work against it.

If Treasuries fall, Bitcoin's $80,000 test gets materially easier, and the institutional thesis gets its first real macro confirmation. If Treasuries jump, duration repricing becomes the deciding factor and the rally fails on macro grounds alone.

The post Bitcoin’s $80k test should be decided by the bond market this week appeared first on CryptoSlate.

Cathie Wood built ARK Invest's Bitcoin case on the idea that Bitcoin would become a global monetary layer that is programmable, borderless, resistant to inflation, and eventually dominant in payments.

The latest version of that argument concedes that stablecoins got there first on the payments side.

In a recent interview with The Rollup, the ARK CEO said stablecoins have taken over part of the role that ARK once expected Bitcoin to fill in emerging-market payments. At the same time, ETF-era institutions appear to be averaging down during drawdowns, softening the boom-bust severity that defined prior cycles.

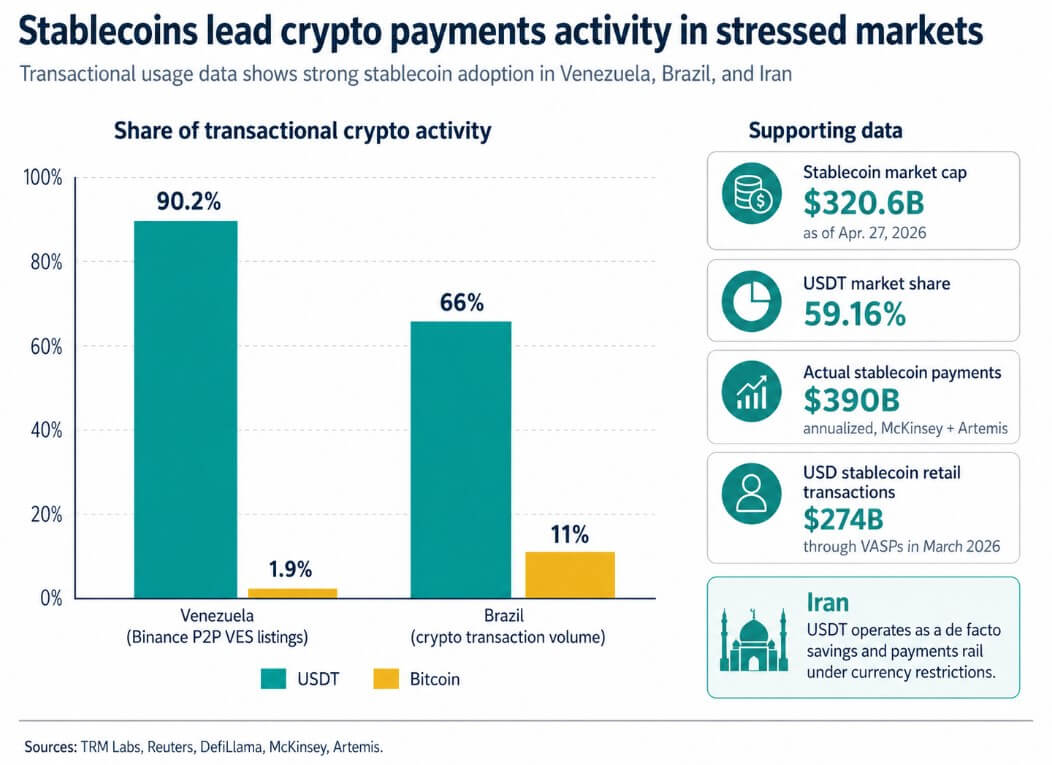

Actual stablecoin payments run at roughly $390 billion annualized per McKinsey and Artemis, about 0.02% of global payments volume. Stablecoins have absorbed much of crypto's transactional lane in the markets where Bitcoin once competed for that role.

DefiLlama data shows that the stablecoin market cap is over $320.6 billion as of Apr. 27, up over 56% since early 2025, with USDT commanding 59.16% of the market.

TRM Labs' first-quarter adoption report found that Venezuela's retail crypto activity primarily runs on stablecoins, with USDT accounting for 90.2% of active Binance P2P Venezuelan bolivar listings and Bitcoin at 1.9%.

In Brazil, roughly 66% of crypto transaction volume was conducted via USDT, with Bitcoin at 11%, and officials noted that stablecoins functioned mainly as payment instruments.

TRM found a similar pattern in Iran, where USDT operates as a de facto savings and payments rail under currency restrictions. The stablecoins pegged to the US dollar processed $274 billion in retail transactions through virtual asset service providers in March 2026 alone.

The payments lane Wood once saw as Bitcoin's future is now stablecoin infrastructure, and the data in stressed, capital-constrained markets makes that case most clearly.

Bitcoin's new lane

What stablecoins left behind for Bitcoin is arguably the better seat. As stablecoins absorbed the transactional utility argument, Bitcoin consolidated around scarcity, institutional allocation, and macro reserve positioning.

CoinShares' latest weekly report recorded $1.2 billion in crypto investment product inflows, the fourth consecutive positive week and the third straight above $1 billion.

Bitcoin took $933 million of that total, Ethereum $192 million, and Solana $31.8 million. Total assets under management climbed to $155 billion, the highest reading since Feb. 1.

At the same time, Strategy's Apr. 27 SEC filing shows another 3,273 BTC purchased during Apr. 20-26, bringing its total to 818,334 BTC at an aggregate cost of $61.8 billion.

CME reported its crypto average daily volume rose from 191,000 to 310,000 contracts year over year in the first quarter, while average daily open interest rose 25% to 313,900 contracts from last year's first quarter.

Farside Investors' daily ETF data provide the clearest picture of Wood's “averaging down” thesis in practice, as US spot Bitcoin ETFs posted nine consecutive positive sessions from Apr. 14 to Apr. 24, with inflows totaling over $2 billion.

Institutions bought through the correction, held through the volatility, and kept adding. Wood's argument that ETF holders are stickier has that nine-session stretch behind it.

The cycle question

Wood's thesis runs ahead of its evidence on the possibility that institutions have fully reshaped the four-year cycle.

NYDIG's research placed retail at 74% of spot Bitcoin ETF AUM as of the fourth quarter of 2024, with institutions and professional advisors at 26%, an expanding share, though still a minority of ownership.

NYDIG's February 2026 note also argued that Bitcoin's recent drawdown still fit a cyclical pattern, even if it looked more orderly.

The ETF era has made the marginal buyer more institutional and more macro-responsive, while retail still generates enough selling volume through drawdowns to drive cyclical moves.

Glassnode's Apr. 22 report adds the market structure layer, noting that Bitcoin reclaimed the True Market Mean at $78,100, with the short-term holder cost basis at $80,100 as the immediate resistance ceiling.

ETF flows turned modestly positive again, and spot demand showed an early recovery, despite short-term holders' realized profits spiking to $4.4 million per hour, nearly three times the $1.5 million threshold that marked prior local tops this year.

Glassnode also noted that Binance's cumulative volume delta led much of the recent spot buying while Coinbase activity stayed muted. Since Coinbase proxies US institutional spot demand most directly, the current bid is genuine, driven more by offshore and mid-tier flows.

Two cases

The bull case for Wood's thesis runs through the Fed.

If the Apr. 28-29 FOMC meeting passes without adding fresh macro stress, weekly inflows hold near or above $1 billion, Coinbase spot participation closes the gap with offshore venues, and Bitcoin clears $80,100 with consistent absorption behind it, Wood's “institutions softening the cycle” argument becomes visible in price structure.

A market that absorbs $4.4 million per hour in realized profit without breaking the reclaimed mean would exhibit exactly the demand depth Wood describes.

ARK's published model projects roughly $710,000 in the base case and $1.5 million in the bull case for Bitcoin by 2030, targets that hold only if the institutional ownership thesis compounds across multiple cycles.

The bear case preserves the four-year cycle. If the Fed re-tightens financial conditions, the weekly flow streak breaks, and Glassnode's realized-profit warning plays out at $80,100, the recent move resolves as a distribution rally.

NYDIG's view that the market stays cyclical, that retail still owns most of the ETF float, and that the cycle's boom-bust mechanics stay stronger than institutional depth can currently get the better of Wood's framing.

Stablecoins would still have won the payments lane, but the halving cycle retains its grip on price structure, with ownership composition playing a secondary role.

Total AUM at $155 billion is 41% below the October 2025 peak of $263 billion, indicating that a large volume of unwound institutional exposure sits above current levels.

| Scenario | What happens | Key signals | What it means for Bitcoin | What it means for Wood’s thesis |

|---|---|---|---|---|

| Bull case | The Fed passes without adding fresh macro stress, the recent demand rebuild holds, and Bitcoin absorbs profit-taking near resistance | Weekly crypto investment-product inflows stay near or above $1B; Coinbase spot participation closes the gap with offshore venues; Bitcoin clears $80,100 with consistent absorption; realized profits stay elevated without breaking the reclaimed mean | Bitcoin shifts from a “rally on trial” to a more durable institutional-demand regime, with ownership mix starting to matter more than the old halving reflex | Supports Wood’s argument that institutions are softening the cycle and that ETF-era buyers are stickier than prior-cycle retail holders |

| Base case | The Fed is broadly neutral, stablecoins keep winning the payments lane, and Bitcoin demand stays positive but uneven | Weekly inflows remain positive but choppy; ETF demand stays constructive but not explosive; Bitcoin holds above $78,100 but struggles to decisively clear $80,100; offshore and mid-tier demand remain stronger than Coinbase-led institutional spot buying | Bitcoin remains supported by macro and institutional flows, but price structure still looks transitional rather than fully reset | Partially validates Wood: the thesis split is real, but institutions have not yet fully reshaped the cycle |

| Bear case | The Fed tightens conditions at the margin, the flow streak breaks, and elevated profit-taking turns the rebound into distribution | Weekly inflows fall back below the recent streak; Glassnode’s realized-profit warning plays out near $80,100; Bitcoin loses support at $78,100; ETF demand fades; retail selling pressure dominates again | The market reverts to a more familiar cyclical pattern, with ownership composition still secondary to drawdown dynamics | Favors NYDIG’s view over Wood’s: stablecoins may have taken payments, but institutions have not yet taken the cycle |

| Structural split outcome | Regardless of short-term price action, stablecoins keep dominating transactional usage while Bitcoin remains the reserve-style asset | Stablecoin market cap stays above $320B; USDT keeps dominant share in stressed payment markets; Bitcoin products continue to capture the bulk of institutional allocation flows | Crypto’s “money” thesis becomes specialized: stablecoins handle payments, Bitcoin handles scarcity and balance-sheet demand | Reinforces Wood’s most durable contribution: Bitcoin did not lose its thesis, it narrowed into a cleaner institutional and reserve-asset role |

What the split actually means

Wood's most durable contribution to the current debate is the argument that Bitcoin's original monetary ambition was divided.

Stablecoins became the working dollar rail in capital-constrained markets, while Bitcoin became the scarcer, harder-to-access asset that institutional balance sheets and regulated products hold at scale.

That division is cleaner and may prove more defensible.

Bitcoin can justify a $710,000 base case price on reserve asset and institutional allocation grounds alone.

The stablecoin layer, by absorbing the transactional utility case, leaves Bitcoin with fewer competing demands on its identity, cleaner store-of-value positioning, and a payments infrastructure that keeps capital circulating in crypto without requiring Bitcoin to serve every role at once.

The Apr. 28-29 Fed decision will tell the market if the institutional bid that has rebuilt over four weeks can absorb what Glassnode is already calling elevated profit-taking.

The post Cathie Wood’s Bitcoin bull thesis concedes stablecoins won the real-world payment fight appeared first on CryptoSlate.

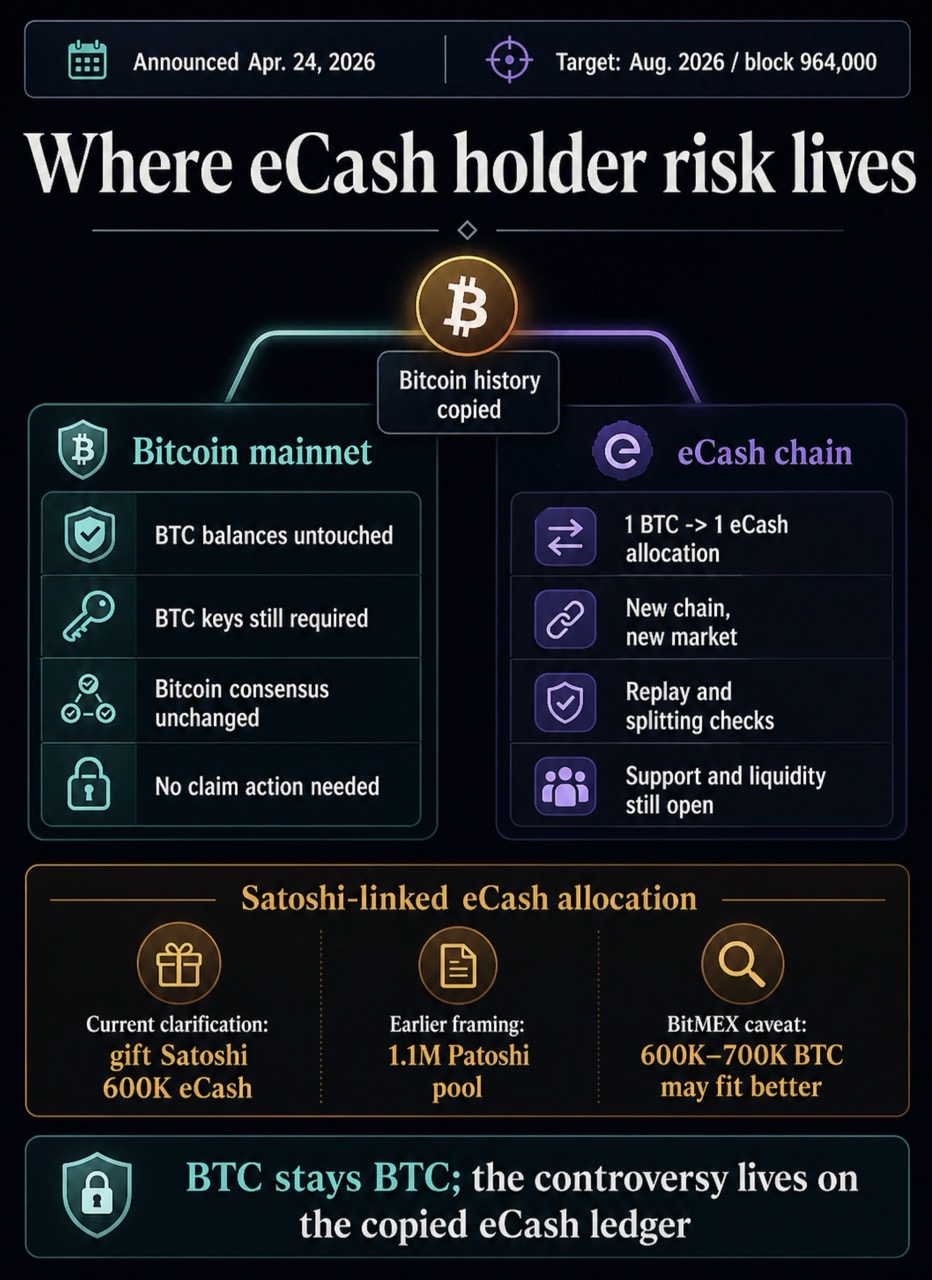

Paul Sztorc, LayerTwo Labs CEO and longtime Bitcoin developer, is planning an August 2026 Bitcoin hard fork called eCash, targeted around Bitcoin block 964,000.

His April 24 announcement described a new chain that would copy Bitcoin history, give holders 1 eCash for every 1 BTC at the split, and launch with a Bitcoin-Core-like base layer mined with SHA-256d alongside Drivechain-style sidechains.

For ordinary Bitcoin holders, the practical question is more specific than the backlash. The fork can create a new asset, new confusion, and new operational decisions, while BTC balances remain governed by Bitcoin software, Bitcoin consensus, and Bitcoin private keys.

In a later clarification, Sztorc said the current eCash plan would give Satoshi Nakamoto 600,000 eCash rather than 1.1 million eCash. He also repeated that BTC balances are untouched by eCash and that moving BTC always requires Bitcoin software plus the relevant Bitcoin private key.

That distinction sets the holder map. A Bitcoin holder can ignore a fork and still keep the same BTC.

The unresolved issue is whether eCash becomes a supported asset that exchanges, wallets, custodians, miners, and tax records have to process. Until that happens, the controversy is mostly about legitimacy, incentives, and precedent on a new ledger.

What eCash would copy from Bitcoin

The proposed chain starts from a familiar hard-fork mechanic. At the fork height, Bitcoin history would be copied into a new network.

A wallet holding 4.19 BTC at the split would have 4.19 eCash on the new chain, according to Sztorc's announcement. Holders could keep, sell, or ignore those coins if the new chain launches and if they can safely access them.

The base-chain pitch is intentionally close to Bitcoin. Sztorc described the eCash layer 1 as a near-copy of Bitcoin Core, mined with the same SHA-256d algorithm, with a one-time difficulty reset to its minimum value at launch.

He also said the chain would activate BIP300 and BIP301 through CUSF, a route meant to bring Drivechain-style sidechains into eCash without changing Bitcoin itself.

The Drivechain component should stay in the background for holders. BIP300 describes hashrate escrows for sidechains, while BIP301 describes blind merged mining, a design under which SHA-256d miners can collect revenue from other chains without running those chains' full software.

Those mechanics explain why Sztorc wants a separate eCash network. BTC remains governed by Bitcoin mainnet rules.

Code readiness is a separate threshold. The public LayerTwo Labs CUSF enforcer repository showed active development, while LayerTwo Labs' download page offered BitWindow software related to the Drivechain stack.

Final eCash launch software, replay rules, and user-grade splitting tools still need verification before ordinary holders can treat the fork as operational.

Preserving BTC requires no claim action during the proposal phase. Holders can leave seed phrases private, avoid importing keys into new software, and ignore claim pages while the chain remains unlaunched.

The chain has to exist first, then the ecosystem has to decide whether it will recognize the forked coins. That sequencing is the difference between a theoretical allocation and a usable asset.

Those same practical gates determine whether the 1:1 allocation becomes anything more than a paper balance in a copied ledger.

The Satoshi allocation fight lives on the new chain

The controversy grew out of the initial funding design. Reporting and Sztorc's own post described a plan to manually reassign fewer than half of the eCash coins corresponding to the presumed Patoshi-pattern coins, often framed around 1.1 million BTC, to early investors or supporters.

The Bitcoin mainnet coins would stay where they are. The dispute is over whether a fork should edit the copied version of those balances before launch.

Sztorc's latest clarification sharpens that point instead of removing it. He says eCash would gift Satoshi 600,000 eCash rather than 1.1 million, a figure closer to the lower Patoshi estimate than the common million-plus framing.

That still leaves the core objection. A straight 1:1 copy would assign every copied coin to the same keys that held the BTC at the split, while the current eCash proposal would choose a different treatment for part of the dormant copied balance.

Bitcoin's social contract treats signatures and private keys as the boundary of control. A new chain can choose different rules, but a chain that reallocates dormant copied coins tells users something about how its own ledger treats old balances.

Critics see that as a precedent problem. Sztorc has argued that a pure fork can leave contributors undercapitalized before launch, creating a chain that starts as a zombie project.

The size of the Satoshi-linked pool also deserves care. BitMEX Research found strong evidence of a dominant early miner, but argued that the evidence is less robust than the common million-plus framing suggests.

Its analysis said 600,000 to 700,000 BTC may be a better estimate than roughly 1 million or 1.1 million. That means the exact denominator behind any eCash reassignment claim is uncertain.

Earlier coverage described a possible version that did not involve Satoshi's coins. The later Sztorc clarification supplied for this update points to a different current posture: Satoshi would receive 600,000 eCash, while BTC itself remains outside the fork's control.

The eCash project site and related Satoshi Half-Airdrop material is still moving through public clarification rather than a final release package.

| Claim | Current read | Holder consequence |

|---|---|---|

| BTC holders receive eCash 1:1 on the forked chain | Sztorc's announcement and current coverage describe that allocation | A claimable asset may exist, subject to safe access and market support |

| BTC balances move on Bitcoin mainnet | The fork would create a separate chain while BTC remains under Bitcoin consensus | BTC stays under Bitcoin keys and Bitcoin mainnet rules |

| Satoshi-linked eCash allocation | Sztorc now says Satoshi would receive 600,000 eCash rather than 1.1 million | Legitimacy and precedent risk sits on the new chain |

| Replay protection and coin splitting are ready | Sztorc says default eCash software should block eCash spends from replaying on Bitcoin; final tooling still needs verification | Holders should wait for trusted wallet or exchange guidance |

| Major infrastructure support exists | Reviewed sources did not establish major miner, exchange, custodian, or wallet support | Liquidity and usability remain open tests |

The holder checklist starts with replay and custody

A fork becomes operational when people try to move coins. Replay protection is central because a transaction valid on one chain can sometimes be copied to another chain after a split.

Contentious forks without replay protection can expose exchanges and holders to replay attacks, according to Coinbase's hard-fork guidance.

Sztorc's replay clarification said default eCash software should block an eCash spend, such as a sale, from replaying on Bitcoin. He also said moving BTC may also move the corresponding eCash, and that behavior could depend on the software a holder uses.

That leaves a simple behavioral rule. Holders should avoid random claim tools, unofficial wallets, and links that promise early access.

A badly designed splitter, a malicious wallet, or a phishing site can create more risk than the fork itself. The safer threshold is public guidance from reputable wallets, exchanges, and custodians after final code and replay behavior are visible.

Custodial holders face a different decision tree. Large platforms tend to evaluate forked assets case by case, using security, liquidity, developer activity, roadmap, compliance, and engineering workload as filters.

Coinbase has described that approach in its own fork policy. That is the lens to apply here.

Even if eCash launches, a platform holding BTC for customers may decline to support the forked asset, may support withdrawals only, or may delay access until the network is stable.

Tax treatment adds another layer for US holders. Under IRS Revenue Ruling 2019-24, a hard fork without receipt of new cryptocurrency does not create gross income, while a hard fork followed by an airdrop can create ordinary income when the taxpayer receives units and has dominion and control.

For eCash, that means the tax answer may depend on whether the holder can actually access, transfer, sell, or otherwise dispose of the forked coins. It is a professional-advice question, especially for coins held through exchanges or custodians.

Miner support is the first infrastructure signal because the new chain needs security and block production separate from Bitcoin's own social consensus. Exchange support is the next signal because a forked coin with no venue, no withdrawals, and no market depth has little practical use for most holders.

Wallet and custodian policies sit beside those two signals. They determine whether ordinary users can see, split, move, or ignore the forked asset without taking on unnecessary key-management risk.

Names and market scale add another source of confusion

The proposed fork also runs into name overlap. There is already an eCash network with the ticker XEC, maintained around Bitcoin ABC software.

The existing XEC asset traded near $0.00000704 with a market capitalization around $140.9 million on April 28, 2026. Separately, Cashu describes itself as a free and open-source Chaumian ecash protocol built for Bitcoin.

That overlap has practical consequences. Search results, fake support pages, copied tickers, and social links can blur the difference between Sztorc's proposed fork, the existing XEC asset, and Bitcoin ecash tools such as Cashu.

The right user response is boring and important: verify domains, tickers, wallet instructions, and exchange notices before interacting with any fork-related asset.

The scale difference is also useful. BTC traded around $76,824.95 on April 28, with a market capitalization near $1.54 trillion and 59.9% dominance.

Any eCash fork would be trying to attach a new asset and a contested rule set to the largest crypto network by market value. That scale raises the bar for infrastructure support because even small confusion around Bitcoin balances can draw significant attention.

The fork's first test is therefore external to the argument over Satoshi's coins. It needs code that users can inspect, replay behavior that wallets can trust, a splitter that works, miners willing to secure the chain, exchanges willing to list or process it, custodians willing to explain their policy, and enough liquidity to give the forked coins a market price.

Until those pieces appear, ordinary holders have little reason to act. Their BTC remains BTC.

The risk today is mostly informational: mistaking eCash for Bitcoin, mistaking one eCash for another, or treating an evolving launch proposal as an asset they must immediately claim.

If the infrastructure arrives, the question changes. Holders would then need to decide whether to claim, split, sell, hold, or ignore the forked coins, and custodial platforms would need to explain how they handle customer entitlements.

The Satoshi-coin controversy would still be a fight over the legitimacy of the new chain. The holder risk would become operational.

The post Top Bitcoin dev is launching a new BTC fork giving holders new eCash, but claiming it may be a real risk appeared first on CryptoSlate.

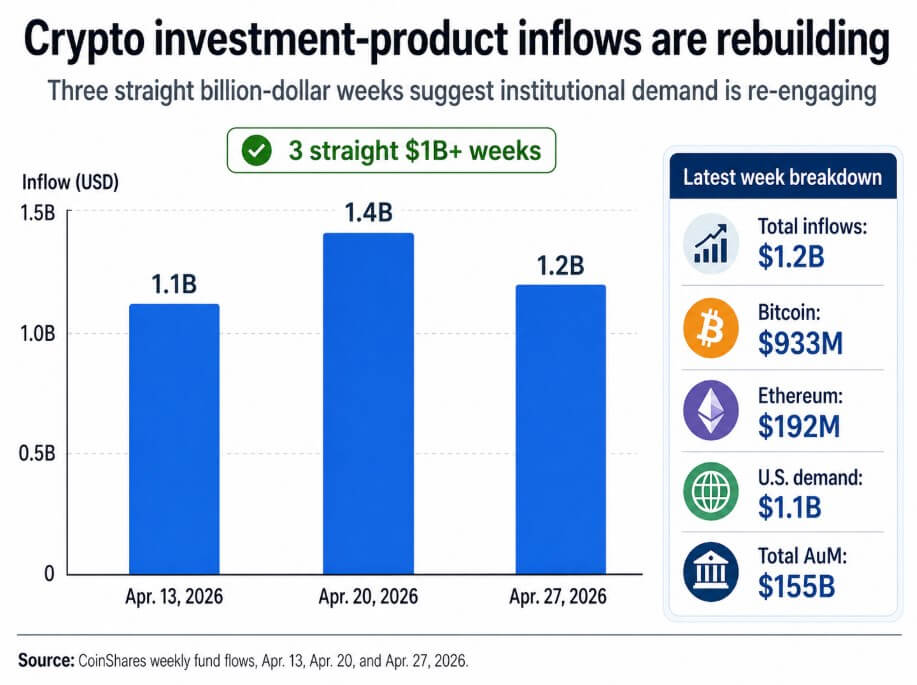

Crypto investment products recorded $1.2 billion in inflows last week, capping three straight weeks above $1 billion and a fourth consecutive positive week overall.

According to CoinShares data, Bitcoin pulled $933 million of that total, Ethereum added $192 million, and the US accounted for $1.1 billion of regional demand. Total assets under management climbed to $155 billion, the highest reading since Feb. 1, though still below the October 2025 peak of $263 billion.

CoinShares attributed the three-week streak to improving institutional demand while flagging the Apr. 28-29 FOMC decision as a source of marginal caution.

The demand stack

The inflow data converges with signals from several other channels simultaneously, which is what distinguishes it from a single-report anomaly.

On regulated derivatives, CME reported that its average daily volume of crypto rose from 191,000 to 310,000 contracts year over year in the first quarter, with average daily open interest reaching 313,900 contracts, up 25% from the first quarter of 2025.

Open interest at that level means capital is staying in the marketplace, pointing to a longer-horizon positioning posture.

The CoinShares report noted that blockchain equity ETFs have taken in $617 million over the past three weeks, reinforcing the view that institutions are buying infrastructure exposure alongside direct coin positions.

Corporate treasury accumulation has continued on its own track. Strategy's Apr. 27 SEC filing shows another 3,273 BTC purchased during Apr. 20-26, bringing its total to 818,334 BTC at an aggregate cost of $61.8 billion, according to Bitcoin Treasuries.

Hong Kong-listed Bitfire is targeting over 10,000 BTC for a regulated “Alpha BTC” strategy within a year, while Avenir held $908 million of BlackRock's IBIT at the end of 2025.

The geographic spread, comprising US corporate treasuries, regulated Asian asset management, and global investment products all moving in the same direction, gives the demand recovery a structural quality that a single weekly inflow report could not establish on its own.

DefiLlama puts the total stablecoin market cap at roughly $320.7 billion, up 1.73% over 30 days, meaning the on-ramp infrastructure for deploying capital into Bitcoin is expanding.

Beyond demand

Market structure adds a layer that prevents demand recovery from being read as settled.

Glassnode's Apr. 22 report placed Bitcoin back above the True Market Mean at $78,100, with the short-term holder cost basis at $80,100 now serving as the immediate resistance ceiling.

ETF flows had turned modestly positive again, and spot demand showed early signs of recovery. Glassnode also reported that short-term holders realized profit had spiked to $4.4 million per hour, nearly three times the $1.5 million threshold that marked prior local tops this year.

At that rate, recent buyers are locking in gains at a pace the market has historically struggled to absorb without a pause or pullback.

Glassnode's spot breakdown noted that Binance's cumulative volume delta (CVD) drove much of the recent buying, while Coinbase activity stayed comparatively muted.

Coinbase is the primary venue for US institutional spot activity, and a recovery driven more by offshore retail and mid-tier funds leaves the bid less anchored than the headline inflow figures imply.

Farside Investors' daily US ETF data makes the same point from a different angle. Spot Bitcoin ETFs posted positive flows for nine trading sessions, surpassing $2 billion, before turning negative on Apr. 27.

Three weeks of billion-dollar inflow readings and a single-day reversal can both be true at once, and together they describe a demand recovery that is directionally real but still fragile enough to break on a macro catalyst.

| Improving signals | Fragility signals |

|---|---|

| ETF flows turned modestly positive again | $80.1K remains immediate resistance |

| Spot demand showed early recovery | Realized profit rose to $4.4M/hour |

| Bitcoin reclaimed $78.1K True Market Mean | Coinbase activity remained muted |

| Three straight $1B+ weekly product inflow weeks | Profit-taking risk rises as buyers move into gain |

The Apr. 28-29 FOMC meeting is now the first hard test to see if the institutional bid that has been built over four weeks can hold its ground.

CoinShares explicitly tied current investor caution to that decision window, and the market structure data from Glassnode explains that Bitcoin is pressing into the $80,100 zone, where over 54% of recent buyers would be sitting on profit, historically the zone where distribution selling has exhausted bear market rallies.

A Fed outcome that leaves financial conditions roughly unchanged removes the largest near-term macro headwind.

A hawkish surprise, or language that tightens the rate-cut timeline further, hands sellers exactly the external trigger they need to act on those elevated profit readings.

The two paths forward

The bull case rests on the Fed passing without adding fresh macro stress, weekly product inflows holding near or above $1 billion, US ETF demand re-accelerating past the Apr. 27 wobble, and Coinbase spot activity closing the gap with offshore venues.

The demand recovery becomes self-reinforcing, and Bitcoin clearing $80,100 with consistent spot absorption behind it would shift the market structure from “rally on trial” to a confirmed demand regime, pulling in the next layer of institutional allocators who have been waiting for the price structure to confirm the flow data.

In that scenario, the October 2025 AUM peak of $263 billion becomes the relevant reference point, and the three-week inflow streak gets read as the early phase of a durable re-engagement.

The bear case turns on the same variables running in reverse. If the Fed re-tightens financial conditions at the margin, the weekly flow streak breaks, and Glassnode's realized profit warning starts to dominate price action, the recent move resolves as another distribution rally, particularly if ETF demand fades and price cannot hold above the reclaimed mean.

Glassnode's own record shows that prior rallies this year have struggled at exactly that point, and with liquidity conditions still thin, a breakdown at $78,100 could accelerate faster than inflow data would predict.

Total AUM at $155 billion is 41% below the October peak, meaning far more unwound institutional exposure above current levels.

| Scenario | Trigger | What confirms it | What breaks it | Why it matters |

|---|---|---|---|---|

| Bull case | The Fed passes without adding fresh macro stress | Weekly digital-asset investment-product inflows stay near or above $1B; U.S. spot Bitcoin ETF demand re-accelerates after the Apr. 27 wobble; Coinbase spot activity closes the gap with offshore venues; Bitcoin clears $80,100 with sustained spot absorption | Hawkish Fed language, fading ETF flows, renewed offshore-only buying, or failure to break $80,100 | Confirms the recent inflow streak as the start of a more durable institutional re-engagement and opens the way for Bitcoin to challenge higher reference levels, including the $263B October 2025 AuM peak |

| Base case | The Fed is broadly neutral and does not materially change financial conditions | Weekly flows remain positive but below the recent $1B+ pace; ETF flows stay mixed; Bitcoin holds above $78,100 but struggles to decisively clear $80,100 | A sharp deterioration in ETF demand, rising profit-taking, or a breakdown below $78,100 | Suggests institutions are re-engaging, but not yet with enough conviction to shift the market into a fully confirmed demand regime |

| Bear case | The Fed tightens conditions at the margin or signals a less supportive rate path | Weekly flow streak breaks; ETF demand fades; Glassnode’s realized-profit warning starts to dominate price action; Bitcoin fails at $80,100 and loses $78,100 | A dovish or benign Fed outcome, resumed $1B+ weekly inflows, stronger Coinbase participation, and a reclaim of $80,100 | Recasts the recent move as another distribution rally rather than a durable recovery, with thin liquidity making downside sharper than inflow data alone would suggest |

CoinShares' three straight billion-dollar weeks, CME's higher open interest, Strategy's continued accumulation, and a deeper base of stablecoin liquidity all point to capital returning to Bitcoin with greater conviction.

The recovery runs across enough channels simultaneously to rule out a single-venue anomaly, and the Fed now decides if the market can keep this movement.

The post Bitcoin’s comeback is now in the Fed’s hands after big investors piled back in appeared first on CryptoSlate.

South Korea's Kbank has signed a strategic partnership with Ripple to test blockchain-based overseas remittances, placing a bank with a central role in Upbit's KRW account access beside one of crypto's longest-running payments infrastructure firms.

Local reports describe the work as a technical verification, or proof-of-concept, focused on whether Ripple's infrastructure can improve the speed, cost, and transparency of overseas remittances. ZDNet Korea separately described the test as part of a phased push around bank-linked overseas remittance infrastructure.

For now, the commercial pieces remain open: launch date, customer access, fees, live volume, and the exact settlement asset.

Kbank already sits inside South Korea's crypto market through Upbit's real-name account system. Its Ripple pilot, therefore, lands as more than a remittance experiment: it tests whether bank-side crypto infrastructure can move from exchange access toward ordinary cross-border payments while the product design and rulebook remain unfinished.

What Kbank and Ripple are testing

The Kbank-Ripple agreement points to bank integration rather than a standalone crypto app. Local reports said Kbank CEO Choi Woo-hyung and Ripple APAC head Fiona Murray attended a signing ceremony at Kbank's Seoul headquarters, with the companies discussing a Ripple digital-wallet proof-of-concept, support for Kbank's overseas remittance model, and broader digital-asset cooperation.

The sequence starts with a separate app-based remittance structure. The next step virtually links customer accounts and internal systems to test remittance stability, checking whether blockchain remittance rails can be mapped onto account and operations layers that resemble the systems a regulated bank would actually use.

That second phase also reportedly tests on-chain transfers involving corridors such as the UAE and Thailand. The corridor detail makes the PoC more operationally specific than a generic partnership announcement while keeping the commercial model open.

Palisade brings the wallet and custody layer into the test. Global Economic said the second phase uses or evaluates Ripple's SaaS-based digital wallet Palisade, while Ripple's own Palisade acquisition announcement describes the platform as wallet-as-a-service and custody tooling with features aimed at institutional digital-asset operations.

That makes the test a wallet and key-management exercise as much as a transfer-speed exercise. Production deployment by Kbank remains unannounced.

The technical focus is still meaningful. A bank remittance product has to solve compliance, custody, account linkage, settlement, and broader regulatory requirements. The PoC appears to test parts of that stack, while the full commercial design remains open.

Why Upbit changes the stakes

Kbank's role in Upbit's fiat access gives the Ripple test its market-structure relevance. The bank was moving to extend its real-name deposit and withdrawal account partnership with Upbit through October 2026, according to ChosunBiz.

Upbit's own real-name account verification guide says deposit and withdrawal account verification is possible only with Kbank.

Taken together, the partnership report and Upbit's guide make Kbank the bank behind Upbit's KRW real-name deposit and withdrawal account verification rail. They do not show Upbit participating in the Ripple PoC or Kbank running the test on Upbit's behalf.

The size of the Upbit relationship explains why the context has force. Upbit-linked funds accounted for about 24% of Kbank's 30.4 trillion won deposit balance as of the third quarter of 2025, according to Korea JoongAng Daily.

The same report quoted Choi discussing Kbank's need to reduce reliance on Upbit while positioning stablecoins and cross-border payments as future opportunities.

Kbank's crypto-linked banking role has been built around exchange access. The Ripple test examines whether similar bank-side plumbing can be used for payments.

The first use case is account access for trading. The next possible use case is cross-border money movement. Between those two sits the unresolved question of regulation.

That context should not be stretched into Upbit participation. Upbit explains why Kbank's banking role matters to South Korea's crypto rails; the Ripple agreement remains a Kbank-side remittance PoC.

CryptoSlate's prior coverage helps define the surrounding terrain. A June 2025 article covered South Korean banks pursuing a won-backed stablecoin push, while an April 2026 CryptoSlate report on Ripple's RLUSD in Japan showed how bank trust can shape Asian stablecoin adoption.

Regulation keeps the test provisional

South Korea's bank-led stablecoin debate gives the remittance test a policy edge. The Kbank pilot is already being tied to South Korea's stablecoin rulemaking debate, while Seoul Economic Daily reported that delayed digital-asset legislation has kept some Korean blockchain and remittance infrastructure from moving into actual operations.

Banks can test the mechanics before they know the final rulebook. They can examine wallet architecture, account linkage, compliance controls, and cross-border flows. They can also build optionality without committing to a product launch.

Note: Kbank, the South Korean internet-only bank in the Ripple partnership, should be kept separate from Thailand's KASIKORNBANK, often branded KBank.

KASIKORNBANK has appeared in related Korea-Thailand digital-asset remittance discussions, including a February cooperation announcement with Orbix and BPMG. The connection is corridor context and naming clarity, while the South Korean Kbank and Thailand's KASIKORNBANK remain separate institutions.

The practical split is straightforward: what the pilot tests, what remains undecided, and why Kbank's Upbit rail gives the work market weight.

| Confirmed | Still open | Operational implication |

|---|---|---|

| Kbank and Ripple signed a strategic partnership for remittance technical verification. | No production launch date or customer rollout has been confirmed. | The work remains a bank-side PoC before customer rollout. |

| The current phase virtually links customer accounts and internal systems and tests UAE/Thailand on-chain transfers. | The exact settlement asset, fee model, and live transaction volume remain undisclosed. | The test targets bank integration, but the commercial model is still undefined. |

| Upbit account verification for deposits and withdrawals is available only with Kbank, according to Upbit's guide. | Upbit has not been identified as a participant in the Ripple PoC. | Kbank's exchange-rail position gives the test relevance while exchange integration remains unsupported. |

| South Korea is still working through stablecoin and digital-asset payment rules. | The final rule set for bank-led digital remittances remains unsettled. | Regulation is a key gate between technical readiness and commercial launch. |

The next test is commercial proof

Kbank is now sitting between two roles. One is already visible: banking access for Upbit's KRW deposit and withdrawal verification.

The other is being tested: blockchain-based overseas remittances that connect with bank accounts and internal systems.

That bridge has strategic value because South Korea's crypto market already depends on tightly controlled bank-account rails. If a bank tied to those rails can also make blockchain remittances operational, the boundary between exchange access and payment infrastructure becomes less fixed.

The same compliance-heavy banking layer could become a place where crypto-linked infrastructure moves from trading access into cross-border money movement.

For now, the PoC covers testing, corridors, account-system simulation, and Palisade evaluation. It does not yet provide the commercial pieces that would turn the work into a live remittance business.

The next threshold is concrete: a named product, a live customer flow, a settlement asset, a fee model, and regulatory clearance.

Until those pieces arrive, Kbank's Ripple partnership is best read as a readiness test with unusually important surroundings. It shows that one of South Korea's key crypto-linked banking rails is examining the payments infrastructure.

It also shows how much still depends on regulation before a technical pilot can become a real remittance business.

The post The South Korean bank powering Upbit is testing Ripple integration for cross-border payments appeared first on CryptoSlate.

Cryptoticker

Ethereum vs. NVIDIA: Which is the Better Investment in 2026?

Title: Ethereum vs NVIDIA: Which Asset is the Better Long-Term Investment? slug: ethereum-vs-nvidia-investment-comparison teaser: Ethereum or NVIDIA? We compare the 5-year and 10-year returns of ETH and NVDA to see which asset wins the battle for your portfolio in 2026. keywords: ethereum vs nvidia, eth price performance, nvda stock returns, crypto vs stocks, investing in ai, ethereum investment 2026, nvidia price today

Protocol vs. Processor

The investment debate in 2026 centers on two powerhouses: Ethereum ($ETH), the backbone of decentralized finance, and NVIDIA (NVDA), the hardware engine of the AI revolution. While both represent "frontier" technology, their returns vary wildly depending on your entry point.

Which ROI Comparison

NVIDIA has dominated the last five years due to the AI boom. Conversely, Ethereum remains the superior long-term play for those who entered a decade ago.

- 5-Year Winner: NVIDIA (+1,300%)

- 10-Year Winner: Ethereum (+459,900%)

The 5-Year Window: NVIDIA’s AI Dominance

Since 2021, NVIDIA has outperformed almost every major asset class, including Bitcoin.

- NVIDIA: A $100,000 investment in 2021 is now $1,400,000. Growth is driven by Blackwell chip demand and a $4.5 trillion market cap.

- Ethereum: A $100,000 investment in 2021 is worth $85,000 today. Despite the 2024 ETF launch, ETH has faced significant price stagnation compared to high-growth equities.

The 10-Year Window: The Power of Early Crypto

When extending the horizon to 2015, the "crypto multiplier" becomes evident.

- ETH: $100,000 invested in 2015 = $460 Million.

- NVDA: $100,000 invested in 2015 = $60 Million.

While NVIDIA’s 600x return is legendary for a stock, Ethereum’s 4,600x return highlights the asymmetric upside of successful blockchain protocols compared to centralized corporations.

Cash Flow vs. Network Utility

- NVIDIA (NVDA): A centralized company with record revenues ($215B in FY2026). Its value is tied to hardware sales and AI compute demand.

- Ethereum (ETH): A decentralized settlement layer. Its value is tied to network usage, the EIP-1559 burn mechanism, and its role as the primary platform for tokenized Real World Assets (RWA).

Performance Drivers in 2026

NVIDIA’s current lead is fueled by tangible earnings and the race for "AI Sovereignty." Major tech firms continue to buy GPUs at scale, keeping NVDA margins high.

Ethereum, however, is transitioning from a speculative asset to a utility-driven one. While the exchange comparison shows lower retail trading volume for ETH compared to previous cycles, institutional staking and Layer-2 scaling are at all-time highs. For long-term holders, securing these assets in hardware wallets remains the priority as the network matures.

Ethereum vs. NVIDIA: Growth or Moonshot?

- Better for Stability: NVIDIA. Its growth is backed by massive institutional contracts and a clear monopoly on AI hardware.

- Better for Asymmetric Gains: Ethereum. As the world’s financial rails move on-chain, ETH’s potential to repeat its "10-year" style growth remains higher than a stock already valued in the trillions.

Dogecoin (DOGE) Faces a Moment of Truth

Dogecoin (DOGE) is currently at a technical crossroads. After months of range-bound trading between $0.086 and $0.118, the world's most famous meme coin is showing signs of a potential "short squeeze." As of April 28, 2026, Dogecoin is trading at $0.099, precisely at a level that has historically acted as both a psychological and technical ceiling.

Dogecoin Price Analysis: The Squeeze is On

The daily chart reveals a clear period of volatility compression. Since February, DOGE has been printing higher lows, forming a gradual ascending support structure.

- Resistance: The immediate hurdle is the $0.099 – $0.100 zone. A daily close above this level is essential to confirm a trend reversal.

- Support: The green support line at $0.086 remains the "line in the sand" for bulls.

- RSI Indicator: The Relative Strength Index (RSI) is currently sitting at 58.67, trending upward. This suggests that while momentum is positive, there is still significant "overbought" headroom before the rally becomes overextended.

Why is Dogecoin Trending Today?

The recent price action isn't happening in a vacuum. Several fundamental catalysts are converging to keep DOGE in the headlines of crypto news.

1. The "X Money" Factor

Speculation is reaching a fever pitch regarding Elon Musk's X platform and its upcoming payment feature, X Money. While initial reports suggest a fiat-based system in partnership with Visa, the DOGE community is betting on a future crypto integration. Historically, any mention of payments on X (formerly Twitter) has led to massive spikes in $DOGE price.

2. Institutional Adoption: The Dogecoin ETF

In a surprise move for 2026, institutional interest has shifted toward meme coins. Following the success of Bitcoin and Ethereum ETFs, Nasdaq began listing the 21Shares Dogecoin ETF (ticker: TDOG) earlier this year. This provides a regulated pathway for institutional capital to flow into DOGE, reducing the "joke" stigma and treating it as a legitimate digital asset.

3. SpaceX and the Lunar Mission

Elon Musk recently reignited interest in the DOGE-1 mission, a satellite project funded entirely by Dogecoin. During a talk with the Tesla Owners Club, Musk hinted that the project, which faced several delays, is back on track.

Strategic Trading Levels to Watch

For traders looking to capitalize on this movement, the following levels are critical:

| Level Type | Price (USD) | Significance |

|---|---|---|

| Major Resistance | $0.118 | The high from early February; breaking this confirms a bull market. |

| Pivot Point | $0.100 | Psychological barrier; requires high volume to break. |

| Immediate Support | $0.095 | Local support to maintain the current short-term uptrend. |

| Critical Support | $0.086 | Must hold to avoid a deeper crash toward $0.07. |

Is the $1.00 Dream Still Alive?

While the $1.00 target remains a long-term goal for the fading "Doge Army," the immediate focus is reclaiming the $0.12 territory. The combination of technical compression and institutional products like the TDOG ETF suggests that Dogecoin is maturing beyond a simple pump-and-dump asset.

Kevin Warsh has emerged as the clear frontrunner to succeed Jerome Powell as the Chair of the Federal Reserve. Warsh is widely considered the most "pro-Bitcoin" candidate to ever be nominated for the role. However, historical data casts a long, dark shadow over Fed leadership changes. In every major transition over the last decade, Bitcoin has suffered double-digit percentage collapses.

The "Fed Chair Curse": A History of Bitcoin Crashes

To understand the current market anxiety, one must look at the precedent set by previous appointments. Historically, the uncertainty surrounding a new Fed Chair’s "hawkish" or "dovish" stance has triggered massive sell-offs.

| Date | Fed Chair Event | Bitcoin Performance |

|---|---|---|

| Jan 2014 | Janet Yellen takes office | -82.77% |

| Feb 2018 | Jerome Powell takes office | -73.89% |

| May 2022 | Jerome Powell’s 2nd Term | -61.06% |

In 2014, Janet Yellen's arrival coincided with the post-2013 bubble burst and the Mt. Gox collapse. By 2018, Powell took the reigns just as the ICO craze deflated. Most recently, in 2022, his second term confirmation aligned with the start of aggressive interest rate hikes that fueled the "Crypto Winter."

Who is Kevin Warsh? The Pro-Crypto Nominee

Kevin Warsh is not your typical central banker. A former Fed Governor (2006–2011) and Morgan Stanley veteran, Warsh has a track record of acknowledging Bitcoin as a legitimate financial asset. During his recent confirmation hearings, Warsh stated that "digital assets are already part of the fabric of our financial services industry."

Unlike his predecessors, Warsh’s personal financial disclosures revealed significant exposure to the sector, including holdings in Web3 infrastructure and DeFi protocols.

Key Policy Stances:

- Opposition to CBDCs: Warsh has explicitly called a retail U.S. Central Bank Digital Currency a "bad policy choice," citing privacy concerns.

- Private Innovation: He favors letting the private sector lead in stablecoins and digital payments rather than government-led initiatives.

- Inflation Hedge: He has previously referred to Bitcoin as an "important asset" that informs policymakers on inflation and dollar strength.

Why 2026 Might Be Different: The Case for a Bitcoin Pump

While the "Fed Chair Curse" suggests a crash is imminent by May 2026, several factors suggest we might see a "Warsh Pump" instead of a "Powell Dump."

- Regulatory Clarity: Unlike 2014 or 2018, the U.S. now has a maturing regulatory framework. Investors are no longer trading in a vacuum; institutional products like Spot Bitcoin ETFs have stabilized liquidity.

- The "Shadow" Mandate: Warsh is expected to prioritize "Sound Money" and market-led growth. If the market perceives him as more "dovish" or less likely to weaponize the banking system against crypto (Operation Choke Point 2.0), capital could flood back into crypto exchanges.

- Institutional Sentiment: According to reports from The Wall Street Journal, Wall Street views Warsh as a candidate who understands market volatility, potentially leading to a more predictable interest rate path.

The Risks: Political Friction and the "Sock Puppet" Narrative

It hasn't been all smooth sailing. Senator Elizabeth Warren and other critics have raised concerns about Warsh’s independence, fearing he may act as a "sock puppet" for the executive branch to facilitate specific crypto ventures. Any perception that the Fed is losing its independence could lead to dollar volatility, which historically sends tremors through all risk assets, including hardware wallets and cold storage holdings.

Ethereum drops below $2,300 as crypto momentum fades

Ethereum fell below the important $2,300 level after Bitcoin failed to hold its recent pump toward $79K. The move came during a broader crypto market pullback, where Bitcoin dropped below $77K and several major altcoins turned red within a short period.

The latest market data shows ETH trading around $2,277, down nearly 3% over 24 hours. This drop is important because Ethereum had recently been supported by bullish institutional headlines, including reports of major ETH accumulation by BitMine. However, the market reaction shows that short-term traders are still focused more on Bitcoin’s price action, liquidations and weak market structure than on long-term accumulation news.

In simple terms, Ethereum did not drop because of one isolated ETH-specific event. It dropped because the broader crypto market lost momentum.

Why did Ethereum drop below $2,300?

The main reason Ethereum dropped is that Bitcoin rejected a key resistance zone. BTC briefly pushed toward $79K, but the move failed quickly. Once Bitcoin lost strength and fell back below $77K, Ethereum followed with a sharper decline.

This is normal during fast market reversals. ETH often behaves like a higher-beta version of Bitcoin, meaning it can rise faster during bullish momentum but also fall harder when the market turns. When BTC rejected the breakout, traders quickly reduced exposure across major crypto assets, and ETH became one of the first large-cap altcoins to feel the pressure.

The loss of the $2,300 level then made the move worse. For many traders, $2,300 is both a psychological level and a short-term technical support zone. Once Ethereum fell below it, stop-losses and leveraged long liquidations likely accelerated the decline.

Liquidations hit Ethereum after Bitcoin’s failed breakout

The speed of the drop suggests that liquidations played a major role. Social media reports pointed to a sharp amount of value being wiped from the crypto market in a very short time, with both BTC and ETH falling almost simultaneously.

This matters because Ethereum is heavily traded with leverage. When the market moves against crowded long positions, traders are forced to close positions or get liquidated. That selling pressure can push ETH lower even if there is no major negative news about Ethereum itself.

This is why ETH can drop despite bullish long-term headlines. Institutional accumulation may support the broader narrative, but short-term leverage can still control intraday price action.

BitMine buying Ethereum was not enough to stop the selloff

One of the more bullish headlines around Ethereum was the report that Tom Lee’s BitMine bought a large amount of ETH. This should normally support confidence in Ethereum’s long-term outlook, especially as institutional interest in ETH continues to grow.

However, today’s move shows the difference between long-term accumulation and short-term trading pressure. Big buyers can strengthen the investment case for Ethereum, but they do not automatically prevent sudden corrections. If Bitcoin rejects resistance, the market deleverages, and altcoins weaken, ETH can still drop below key levels.

That is exactly what happened here. The BitMine headline helped the Ethereum narrative, but it was not strong enough to stop the market-wide selloff.

Ethereum weakens as altcoins flash warning signs