Cryptocurrency Posts

Crypto Briefing

The SEC's dismissal may embolden blockchain innovators but raises concerns about regulatory clarity and investor protection in decentralized finance.

The post SEC drops fraud case against BitClout founder Nader ‘Diamondhands’ Al-Naji appeared first on Crypto Briefing.

The Ethereum Foundation's ETH sale to Bitmine highlights its strategic focus on sustainable growth and decentralized network stewardship.

The post Ethereum Foundation sells 5,000 ETH to Bitmine to fund operations and grants appeared first on Crypto Briefing.

The long-term accumulation trend among crypto ETF investors suggests a stabilizing influence on the volatile crypto market landscape.

The post BlackRock says over 90% of Bitcoin ETF investors are long-term accumulators appeared first on Crypto Briefing.

Musk's restructuring of xAI highlights challenges in leadership transitions and the impact of aggressive management on company morale and talent retention.

The post Elon Musk removes more xAI founders during restructuring ahead of potential IPO appeared first on Crypto Briefing.

The launch of Velotrade's crypto prop platform could democratize access to capital for traders, potentially reshaping the crypto trading landscape.

The post Ex-JP Morgan and Dresdner Kleinwort traders launch crypto prop platform appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

AI Pivot Won’t Save Everyone, Wintermute Tells Bitcoin Miners

Bitcoin miners are caught in the tightest squeeze of the network’s history, and a new Wintermute report argues that simply waiting for the next bull run is no longer a strategy.

Instead, the firm says miners will have to reinvent themselves as infrastructure and treasury managers if they want to make it to the next halving.

Wintermute analyst Jasper De Maere says the current mining cycle is structurally different from prior ones in 2018 and 2022. Bitcoin’s design cuts block rewards in half every four years, but this time the price has not doubled over the same window, which means miner revenue is shrinking in real terms.

On a rolling four‑year basis, Bitcoin has only returned about 1.15x in this epoch, far below the 10x–20x multiples seen in earlier cycles.

In past cycles, huge price gains covered up a lot of problems. Miners could count on bull markets to bail out weak margins after each halving.

Today, with institutions, ETFs, and corporate treasuries in the mix, Bitcoin trades more like a mainstream macro asset, and those explosive 20x runs are less likely.

For miners that built their business on the assumption of permanent hypergrowth, Wintermute frames this as a regime change, not a bad quarter.

Margins are getting crushed

Under the hood, Bitcoin mining has a very simple cost structure: energy and compute. That simplicity means there are not many ways to protect profits when revenue falls. Wintermute’s analysis shows gross margins in this epoch peaked around 30%, a level that marked the bottom during prior bear markets, not the top.

Earlier epochs saw long stretches where miners enjoyed 70–80% margins; now, the “good times” look more like prior stress points.

Transaction fees are not saving the day either. Fee spikes tied to hype cycles and mempool congestion show up on charts, but they fade fast and rarely contribute more than a few percent of total miner revenue over time.

Wintermute notes that even when you include fees, the margin lines for each cycle barely move apart, especially in the current epoch. In other words, the protocol’s built‑in “second revenue stream” is not acting as a reliable backstop.

The AI pivot is an opportunity for a few

One path out of the squeeze is getting plenty of attention: pivoting into high‑performance computing (HPC) and AI workloads. Big tech firms and AI startups are racing to lock in power and data center capacity, and they do not want to wait five to ten years for new grid connections and construction.

Miners, who already control cheap power and built‑out sites, are a natural shortcut.

Wintermute points out that sites once valued at roughly 1–7 dollars per watt as pure mining operations have changed hands at close to 18 dollars per watt after being repositioned for AI compute, helped by deals like HUT’s work with Google and Anthropic.

Public‑market investors have rewarded miners that announce credible AI plans with higher valuations and cheaper capital through equity and convertible debt.

The catch is that not every miner has the location quality, balance sheet, or operational capacity to turn into a data‑center business.

Putting “idle” Bitcoin to work

That is where Wintermute sees a second, underused lever: active balance sheet management. Miners together hold close to 1% of all Bitcoin, a legacy of the “HODL” playbook that dominated earlier cycles.

At the same time, many listed miners have been selling down parts of their treasuries to cover tighter margins and debt, with some even wiping out holdings altogether.

Instead of letting reserves sit idle until they are dumped in a liquidity crunch, Wintermute argues miners should treat BTC like a working asset. On the “active” side, that means using derivatives strategies such as covered calls and cash‑secured puts to earn yield on holdings, at the cost of taking some market risk.

On the “passive” side, miners can deploy coins into on‑chain lending markets, including a new wrapped‑BTC market on Wildcat that Wintermute has highlighted, to generate interest income.

Wintermute’s bottom line is that Bitcoin’s design is working, but the easy era for miners is over. Difficulty can still adjust, yet it cannot overcome slower price growth, a fee market that has not scaled, and rising energy costs that eat into every block reward.

The AI pivot will likely reshape the upper tier of the industry, turning some miners into full‑blown infrastructure companies.

This post AI Pivot Won’t Save Everyone, Wintermute Tells Bitcoin Miners first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

South African Eskom Considering Discount Power for Bitcoin Miners as Solar Creates Surplus

Eskom, a South African electricity public utility, is exploring plans to sell excess daytime electricity to Bitcoin mining companies as rooftop solar installations reduce grid demand during daylight hours.

Speaking at the Biznews Conference 2026 in Hermanus, Eskom chairman Mteto Nyati said the utility is evaluating ways to monetize surplus power generated during the middle of the day, according to local reporting.

South Africa’s rapid adoption of rooftop solar systems has begun to reshape the country’s electricity demand profile. Many households and businesses now generate their own power during daylight hours, leaving Eskom with unused capacity once solar panels begin producing electricity.

Nyati said the pattern is increasingly predictable.

Demand spikes in the early morning as households prepare for work and businesses open. As solar generation ramps up later in the day, grid demand falls, leaving Eskom with surplus electricity.

Eskom is looking at creative ways and means of using that capacity. One option under review is offering discounted electricity to Bitcoin mining companies operating in South Africa. The sector runs large data centers that perform energy-intensive computations to secure the Bitcoin network.

Nyati said industries such as Bitcoin mining are contributing to rising global electricity demand. He said that the technology did not exist two decades ago but now represents a growing source of power consumption.

Selling excess electricity to miners could allow Eskom to generate revenue from power that might otherwise go unused during solar-heavy hours.

South African Bitcoin mining opportunities

The idea also builds on earlier comments from Eskom chief executive Dan Marokane, who said the state-owned utility is examining opportunities tied to Bitcoin mining, artificial intelligence infrastructure, and large-scale data centers.

Those sectors require large, continuous electricity supplies and could provide new demand for Eskom’s generation fleet.

Nyati framed the initiative as part of a broader strategy to adapt to structural changes in South Africa’s electricity market.

The country’s power sector is opening to private investment, allowing independent companies to build generation capacity and compete in electricity distribution. At the same time, rising rooftop solar adoption is shifting demand away from the national grid.

Nyati said Eskom must adapt to remain viable in a more competitive environment.

Alongside new revenue strategies, Eskom is pursuing cost reductions. Nyati said the utility plans to eliminate about R112 billion in expenses over the next five years.

Reducing those costs could help lower electricity prices for households and energy-intensive industries such as mining and smelting.

Despite the changes in the energy landscape, Nyati said South Africa still needs a strong national utility.

He argued that Eskom’s coal and nuclear power stations provide the base-load electricity required to support industrial growth and economic development.

The proposal to supply discounted electricity to Bitcoin miners reflects how utilities are beginning to treat flexible energy consumers as tools for balancing supply and demand in an evolving power system.

This post South African Eskom Considering Discount Power for Bitcoin Miners as Solar Creates Surplus first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Price Reclaims $73,000 as War Shakes Markets, Outperforming Gold and Stocks

The Bitcoin price has outperformed gold, silver, and major U.S. equity indexes since the outbreak of the Iran–Israel conflict escalation 2026, climbing above $73,000 even as oil surged and expectations for near-term interest rate cuts faded.

Market data shows Bitcoin price rising about 8% since the first strikes against Iran, reaching a one-month high above $73,000. The move placed the digital asset ahead of several traditional safe-haven and risk assets during a period of geopolitical stress.

Gold declined during the same stretch, falling roughly 3% from levels seen before the conflict began. Silver dropped more than 10%, sliding from above $90 to around $82. U.S. equities also weakened, with the S&P 500 and the Nasdaq Composite each down between 1% and 2%.

The divergence came as global markets responded to a surge in energy prices. Crude oil climbed close to 20%, breaking above $100 per barrel for the first time in nearly four years as tensions threatened supply routes across the Middle East.

These conditions often pressure crypto markets because higher oil prices and tighter financial conditions raise inflation concerns and reduce risk appetite across global portfolios.

The bitcoin price followed that pattern at first.

In the hours after the conflict began, the asset dropped sharply as traders cut exposure across crypto derivatives markets. Roughly $300 million in leveraged positions were liquidated during the initial weekend selloff. Bitcoin briefly fell toward the mid-$63,000 range as uncertainty spread through global markets.

The selloff matched Bitcoin’s historical behavior during geopolitical shocks, where it often trades in line with other high-beta assets during the first wave of risk reduction.

The market response changed during the following week.

Bitcoin price recovery

Instead of remaining near those lows while energy prices climbed, Bitcoin price recovered steadily and broke back above the $70,000 level. The rebound left it outperforming metals and equities during the same window despite the challenging macro backdrop.

Derivatives data via Bitcoin Magazine Pro shows that part of the recovery followed a reset in market leverage. After the liquidation event cleared large speculative positions, traders began rebuilding exposure.

Open interest across major exchanges climbed back to roughly 88,000 BTC. The increase signals renewed participation without reaching extreme leverage levels that often precede sharp corrections.

Institutional demand also contributed to the rebound.

U.S. spot Bitcoin exchange-traded funds recorded strong inflows during the week. Data from ETF trackers shows the funds attracted about $586 million, marking one of the largest inflow weeks of the year.

The flows represent a steady source of demand entering the market even as geopolitical tensions intensified and inflation concerns returned.

Robert Mitchnick, head of digital assets at BlackRock, said the behavior of ETF investors has remained stable during periods of volatility.

Speaking on CNBC, Mitchnick said ETF flows show a long-term accumulation pattern even during large price declines in Bitcoin price.

He said the investor base across financial advisors, institutions, and direct retail buyers has taken a steady approach to the asset, with many participants using price weakness to add exposure.

He also pointed to the performance of the iShares Bitcoin Trust ETF (IBIT), which continued attracting inflows despite a sharp drop in Bitcoin’s price from its previous peak.

Mitchnick said IBIT ranked among the largest ETF inflows globally during 2025 even while the underlying asset declined, highlighting sustained demand from long-term investors.

NEW: $14 trillion BlackRock says Bitcoin ETF investors are "long term buy and hold fundamental type investors" and flows are positive

— Bitcoin Magazine (@BitcoinMagazine) March 13, 2026

"90% of the investor base" are steadily accumulating during this bear marketpic.twitter.com/ncI3GCyebq

The growth of spot ETFs has expanded Bitcoin’s investor base and deepened market liquidity compared with earlier geopolitical episodes. Institutional capital can now enter the market through regulated products that trade alongside equities.

For now, Bitcoin’s performance during the conflict has reinforced its status as a liquid macro asset that reacts to both global market forces and crypto-native demand.

While oil, inflation expectations, and central bank policy continue to shape the backdrop, the digital asset has managed to recover faster than many traditional benchmarks during one of the most volatile geopolitical episodes of the year.

At the time of writing, Bitcoin price is trading at $72,941.

This post Bitcoin Price Reclaims $73,000 as War Shakes Markets, Outperforming Gold and Stocks first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Strategy (MSTR) Bought Over 4,000 Bitcoin Today via STRC As Strong Week Continues

Strategy appears to have purchased more than 4,000 bitcoin on Thursday, according to estimates derived from real-time trading data and community tracking dashboards monitoring the firm’s preferred equity sales.

Data from STRC.live and market trackers suggests the purchases were funded through heavy issuance of the company’s Variable Rate Series A Preferred Stock (STRC), a perpetual preferred instrument that Strategy has increasingly used to raise capital for bitcoin accumulation.

By end of day in New York, trading activity implied the firm had already raised enough capital to acquire more than 4,000 BTC, marking the largest single-day bitcoin purchase funded through STRC since the instrument launched.

The surge follows unusually strong activity earlier in the week. On March 10, STRC recorded a record $409 million in daily trading volume while maintaining roughly 3% 30-day volatility and a one-month volume-weighted average price near $99.78.

On-chain indicators and community monitoring suggested that day’s activity funded the purchase of more than 2,000 BTC, already one of the largest one-day accumulations tied to the instrument.

Thursday’s pace easily surpassed that figure.

Strategy, already the largest public corporate holder of bitcoin, has increasingly leaned on its preferred equity program to finance additional acquisitions.

Earlier this year the company amended its at-the-market (ATM) program, allowing multiple agents to sell STRC shares simultaneously. The change increased liquidity in the instrument and made it easier for Strategy to raise large amounts of capital quickly, with proceeds directed toward bitcoin purchases.

Real-time dashboards tracking STRC trading attempt to estimate how many shares Strategy itself is issuing versus secondary market trades.

Because the company previously indicated it may sell shares when the price trades above its $100 stated amount, analysts can approximate capital raised when trading occurs above that threshold.

A recent SEC filing disclosed that the company purchased 17,994 BTC between March 2 and March 8 for approximately $1.28 billion. That acquisition lifted the firm’s total holdings to about 738,731 BTC, representing roughly 3.5% of bitcoin’s circulating supply.

The filing showed the purchase was funded through a combination of $377.1 million in STRC sales and $899.5 million raised through common stock issuance.

Based on those figures, STRC accounted for about 29.5% of the funding for that five-day accumulation period, equivalent to roughly 5,300 BTC acquired through preferred share sales.

If Thursday’s estimates prove accurate, the day’s purchases alone could exceed the average daily bitcoin acquisition pace seen during that earlier buying window.

The data remains unofficial. Strategy typically confirms purchases later through SEC filings or public disclosures.

BREAKING: Michael Saylor's Strategy is now estimated to have accumulated 4,038 BTC today via STRC

— Bitcoin Magazine (@BitcoinMagazine) March 12, 2026

Nearly double it's previous daily record!

pic.twitter.com/aFzTtwIE2R

How does Strategy’s STRC work?

STRC acts as a bridge between traditional income investors and Strategy’s Bitcoin-focused balance sheet. Income investors typically seek steady payouts, while Strategy’s large Bitcoin holdings bring long-term upside along with short-term price swings. The preferred stock helps connect these two profiles.

The security is structured to keep demand near its $100 par value while paying a monthly dividend that yields about 11.5% annually. In effect, it converts the economics of a Bitcoin treasury into a format that appeals to fixed-income investors who prioritize regular income.

Strong liquidity and relatively low volatility suggest that the investor base is shifting toward income-focused capital. That shift can help stabilize trading activity compared with instruments driven mainly by speculation.

These early results point to product-market fit. Rather than relying on marketing or hype, the structure appears to meet a clear demand among investors seeking yield tied to Bitcoin exposure.

For corporate leaders considering Bitcoin treasury strategies, STRC offers a way to integrate Bitcoin into broader capital structures. It allows companies to draw funding from multiple investor groups while building a shared strategic reserve around the asset.

At the time of writing, Bitcoin trades near $70,000, while shares of MicroStrategy (MSTR) are down about 0.75% on the day.

Bought Over 4,000 Bitcoin Today via STRC As Strong Week Continues 2")

This post Strategy (MSTR) Bought Over 4,000 Bitcoin Today via STRC As Strong Week Continues first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

David Bailey Confirmed As A Bitcoin 2026 Speaker

David Bailey has been officially confirmed as a speaker at Bitcoin 2026, returning to the conference he helped build to share his perspective on Bitcoin’s expanding role across media, capital markets, and corporate strategy. As the Chairman and CEO of Nakamoto Inc. (NASDAQ: NAKA), Bailey has executed one of the most ambitious consolidation plays in Bitcoin’s history — bringing together BTC Inc., and UTXO Management under a single publicly traded Bitcoin operating company. His vision extends far beyond media: Nakamoto is positioned as a diversified Bitcoin enterprise spanning asset management, advisory services, and institutional infrastructure, with Bitcoin accumulation at its core.

Bailey has long been a central force in shaping how the global Bitcoin community organizes, communicates, and grows. Under his leadership, BTC Inc. became the parent company of Bitcoin Magazine — the longest-running source of Bitcoin news and commentary, first published in 2012 — while also building The Bitcoin Conference into the largest Bitcoin event series in the world, drawing more than 67,000 attendees across U.S., Asia, Europe, and Middle East events in 2025 alone. His work through Bitcoin for Corporations has further accelerated institutional adoption, connecting over 40 member companies with the education and networks needed to integrate Bitcoin into their treasuries.

With the Nakamoto acquisition of BTC Inc. and UTXO now complete, Bailey arrives at Bitcoin 2026 at a defining moment — not just for his own company, but for the broader Bitcoin ecosystem.

Bitcoin Magazine is published by BTC Inc, a subsidiary of Nakamoto Inc. (NASDAQ: NAKA)

Bitcoin 2026 Returns to Las Vegas Bigger Than Ever

Bitcoin 2026 will take place April 27–29 at The Venetian, Las Vegas, and is expected to be the biggest Bitcoin event of the year.

Focused on the future of money, Bitcoin 2026 will bring together Bitcoin builders, investors, miners, policymakers, technologists, and newcomers from around the world. The event will feature a wide range of pass types, including general admission passes designed specifically for those new to Bitcoin, alongside premium passes for professionals, enterprises, and institutions.

With multiple stages, immersive experiences, technical workshops, and headline keynotes, Bitcoin 2026 is designed to serve both first-time attendees and long-time Bitcoiners shaping the next era of global adoption.

Past Bitcoin Conferences in the U.S.

Bitcoin’s flagship conference has scaled dramatically over the past five years:

- 2021 – Miami: 11,000 attendees

- 2022 – Miami: 26,000 attendees

- 2023 – Miami: 15,000 attendees

- 2024 – Nashville: 22,000 attendees

- 2025 – Las Vegas: 35,000 attendees

Get Your Bitcoin 2026 Pass

Get Your Bitcoin 2026 Pass

Bitcoin Magazine readers can save 10% on Bitcoin 2026 tickets using code ‘ARTICLE10‘ at checkout.

Stay at The official hotel of Bitcoin 2026, The Venetian, and get a guaranteed low rate plus 15% off your pass. Be in the middle of where the fun is all happening, and where the networking never ends.

Bring your whole team to Bitcoin 2026 and get 20% off your entire order, bring more than six in a group and get 25% off for a limited time.

Volunteer at Bitcoin 2026 and get Pro Pass access plus exclusive perks.

Location: The Venetian, Las Vegas

Location: The Venetian, Las Vegas Dates: April 27–29, 2026

Dates: April 27–29, 2026

With tens of thousands of attendees expected and hundreds of major speakers like David Bailey already confirmed, now is the time to lock in your ticket.

Buy Bitcoin 2026 Tickets — Save 10%

Why Attend Bitcoin 2026?

Bitcoin 2026 is the definitive gathering for anyone serious about the future of money. With 500+ speakers, multiple world-class stages, and programming spanning Bitcoin fundamentals, open-source development, enterprise adoption, mining, energy, AI, policy, and culture, the conference brings every corner of the Bitcoin ecosystem together under one roof.

From headline keynotes on the Nakamoto Stage to deep technical sessions for builders, institutional strategy discussions for enterprises, and beginner-friendly Bitcoin 101 education, Bitcoin 2026 is designed for everyone—from first-time attendees to the leaders shaping Bitcoin’s global adoption.

Whether you’re looking to learn, build, invest, network, or influence, Bitcoin 2026 is where Bitcoin’s next chapter is written.

Bitcoin 2026 Pass Types: Something for Everyone

Bitcoin 2026 offers a range of pass options designed to meet the needs of newcomers, professionals, enterprises, and high-net-worth Bitcoiners alike.

Bitcoin 2026 General Admission Pass

Ideal for newcomers and those looking to experience the heart of the conference.

- Limited access on Days 2 & 3

- Entry to Main Stage

- Access to Genesis Stage

- Full access to the Expo Hall

Bitcoin 2026 Pro Pass

Designed for professionals, operators, and serious Bitcoin participants.

Includes all General Admission features, plus:

- Full 3-day access, including Pro Day

- Entry to the Pro Pass Reception

- Access to Enterprise Hall, Enterprise Stage, and Networking Lounge

- Conference App networking features

- Access to the Bitcoin For Corporations Symposium

- Entry to Compute Village and Energy Stage

- Complimentary lunch, coffee, tea, and snacks

- Dedicated registration and check-in

- Reserved seating at Main Stage

- Huge savings when you bundle your hotel and Pro Pass

Bitcoin 2026 Whale Pass

Bitcoin 2026 Whale Pass

The all-inclusive, premium Bitcoin 2026 experience.

Includes all Pro Pass features, plus:

- Reserved seating at Main Stage

- All-inclusive gourmet food and beverages

- Entry to Whale Night and Whale Reception

- Access to all official after-parties

- Networking app access to connect with other Whales

- Premium access to The Deep — an exclusive networking lounge with intimate speaker sessions

- Complimentary stay at The Venetian when you bundle your whale pass and hotel (use promo code ‘WHALEHOTEL’ here)

This is the most immersive way to experience Bitcoin 2026.

Bitcoin 2026 After Hours Pass

Bitcoin 2026 After Hours Pass

Your ticket to the night.

Most deals are done with a drink in your hand. Get exclusive access to 3 official Bitcoin 2026 after-parties across Las Vegas — each with a 2-hour open bar — where the real conversations happen and the best connections are made.

- Access to 3 official Bitcoin 2026 after-parties

- 2-hour open bar at each event

- Evening events across Las Vegas, April 27–29

- Network with Bitcoiners, builders, and industry leaders after hours

More headline speaker announcements are coming soon.

Don’t miss Bitcoin 2026.

This post David Bailey Confirmed As A Bitcoin 2026 Speaker first appeared on Bitcoin Magazine and is written by Jenna Montgomery.

CryptoSlate

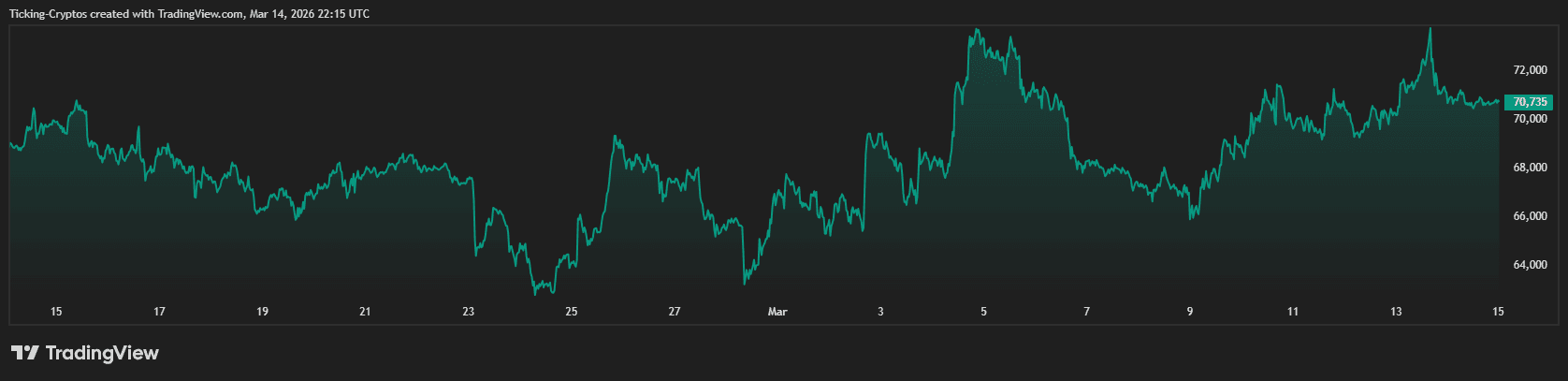

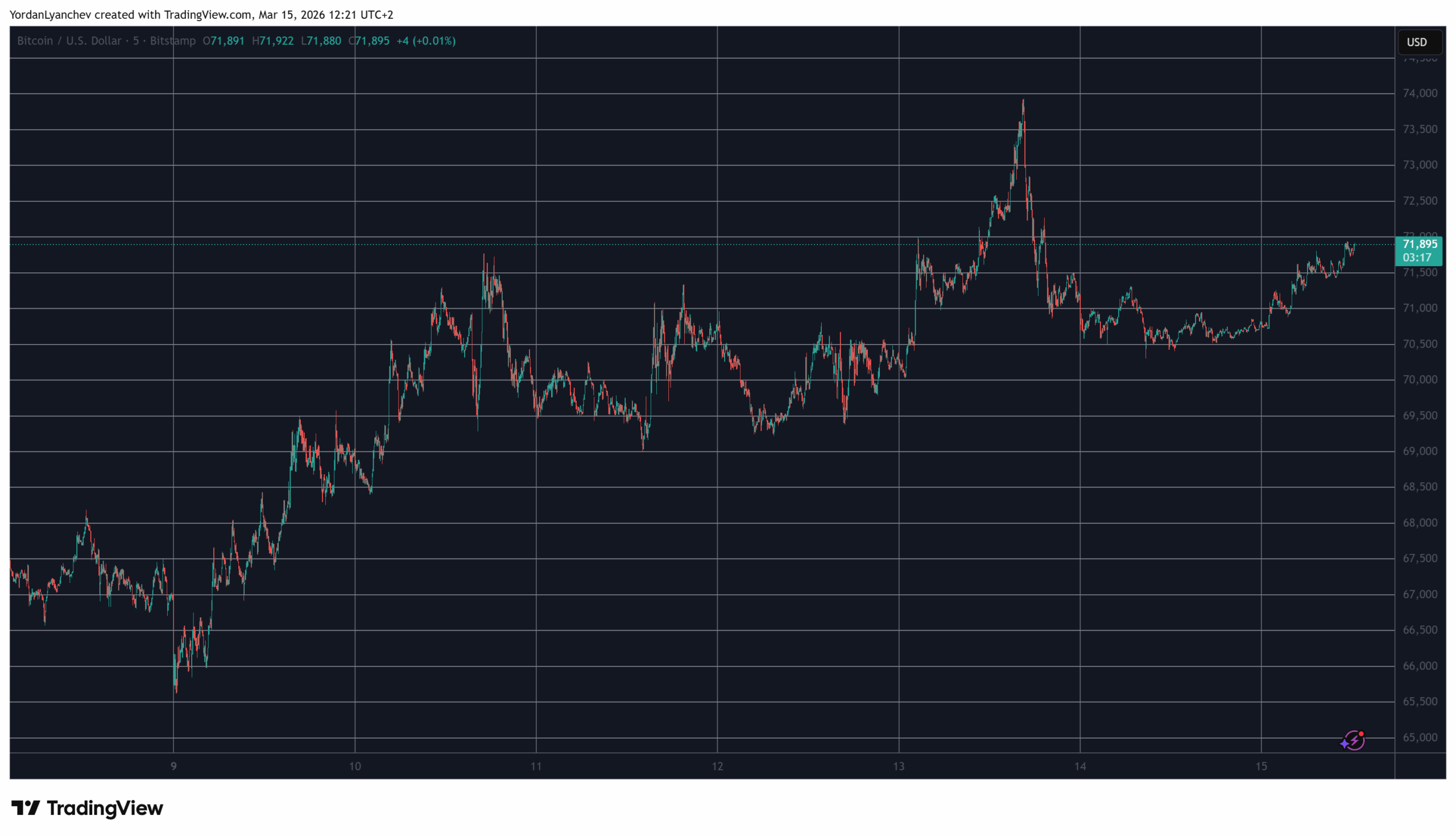

Bitcoin entered the weekend hovering near $71,000, well off the previous week's spike above $74,000, but far below the highs it touched at the beginning of the year. On price alone, the market looks pretty composed.

However, underneath, its structure looks much less comfortable.

Data shows spot activity fading while derivatives keep doing more of the work. Almost every day this month saw derivatives trading at roughly nine times the spot volume, and that's not the profile of a market pushed forward by spot demand. What we're seeing now is a market propped up almost exclusively by leverage.

While the distinction between Bitcoin spiking due to spot demand and spiking due to increased leverage might sound too technical, the consequences of this setup are very simple and affect everyone and everything.

Spot trading means that someone buys BTC that's been put up for sale and takes possession of the coins. It's a very binary way of assessing demand: if a lot of people want to pay to own Bitcoin and keep it, its price will inevitably increase. If nobody wants it, the sellers have to lower their prices until they find willing buyers, decreasing its global value.

But derivatives are different. They're sophisticated financial instruments that enable traders to run complex trading strategies with futures, options, basis trades, and short-term hedges, often with leverage layered on top.

These strategies keep activity high and the price moving, but they create a market that looks deeper than it really is. When too much of the action sits in derivatives, price becomes more volatile, dependent on positioning, and more vulnerable to abrupt air pockets once liquidations start.

A Bitcoin rally built on contracts, not coins

The combined spot and derivatives volume on centralized exchanges fell by around 2.4% to $5.61 trillion in February, its lowest level since October 2024.

Spot trading volume was responsible for a better part of that drop, as trading remained heavily skewed towards derivatives.

The global spot exchange complex saw a notable drop in its volumes while synthetic exposure kept rising. That's a very different backdrop from a rally built on expanding spot demand. While this kind of price spike can look good from a distance, the foundations underneath it are much, much thinner.

The price action we've seen from Bitcoin last week is a perfect illustration of this. BTC recovered back above $70,000, and for a moment, it looked as though buyers were stepping in with much-needed conviction. However, the rebound showed up in leveraged activity more than in spot.

The issue here is not that futures or options volumes are inherently bad. Bitcoin has matured into a market where derivatives are central to price discovery. Nevertheless, when price steadies while spot stays soft, the rally can be much more fragile than it appears.

A move like that is easier to reverse because the support comes from positioning that can be reduced quickly, not just from investors absorbing coins and sitting on them.

The institutional adoption of derivatives has made this bigger than a crypto-native issue.

Earlier in February, CME said that its crypto products were posting record volumes in 2026, with the average daily volume of crypto derivatives up 46% from the previous year. That tells you that there's still room for growth in institutional exposure to Bitcoin. It also tells you where the largest share of that growth is happening: through regulated derivatives.

fInstitutions aren't necessarily expressing weak conviction when they use futures. In most cases, they're doing exactly what large, regulated players prefer to do, which is to gain exposure and hedge risk as efficiently as possible.

However, the effect on the market is still the same. More of Bitcoin’s day-to-day behavior is being shaped through contracts rather than through direct buying of the asset.

Why this gets dangerous for Bitcoin when the outside world turns

That shift wouldn't feel awkward in a calm macro environment. However, Bitcoin is now trading through a period when the outside backdrop has become harder to trust.

On March 13, US equity funds posted a second straight week of outflows as the Iran war and the oil shock darkened sentiment across risk assets. In that kind of atmosphere, leverage stops being a background feature of the market and becomes its main vulnerability.

A market supported by steady spot demand absorbs fear more gradually. But a market supported by derivatives reprices much faster because positions get cut and margins tighten.

That's the real risk now. Bitcoin can keep grinding higher in a derivatives-heavy setup, as it's done many times before.

However, a market carried by leverage depends on these calm conditions staying calm.

That leaves less room for error. A macro scare, another wave of ETF outflows, a jump in yields, a sharp equity selloff, or a sudden hit to sentiment can all produce the same effect: positions unwinding faster than cash buyers can step in.

We saw that in February, when the crypto market was hit by a burst of liquidations during a global risk unwind. While the trigger came from outside crypto, the speed of the reaction was very much a function of how the market was positioned. That's what makes the current imbalance worth watching, as the danger isn't just that Bitcoin is now volatile, because it's always volatile. The danger is that the thing propping up the price is transmitting stress quickly.

There's also a perception problem here.

Bitcoin has spent years building a stronger institutional base. Spot Bitcoin ETFs reached $100 billion in AUM, crypto derivatives on CME are setting records, and more and more corporate treasuries hold BTC.

However, better access to regulated crypto products doesn't automatically produce a sturdier foundation for day-to-day trading. What it does produce is a quick and efficient way to take large leveraged positions. The market is mature because the infrastructure is more mature, but the fragility in behavior is still there.

That's why the spot-versus-derivatives split deserves more attention than it usually gets.

It's one of the best ways to judge what's actually carrying the market at any given moment. Right now, the answer is definitely not spot or retail demand, but leverage, hedging, and synthetic exposure.

Bitcoin remains very liquid, but most of that liquidity is now synthetic, and it's usually the first kind to thin out when the market gets stressed.

That doesn't guarantee a breakdown, though. Bitcoin can stay resilient for longer than skeptics expect, and leverage can keep feeding rallies as long as the flows line up.

Nevertheless, the setup is less sturdy than the price alone makes it look. If spot buying doesn't return in a more visible way, the market may keep climbing with a weaker foundation than many traders realize.

The post Bitcoin’s $71k rally has a problem most traders aren’t watching appeared first on CryptoSlate.

On Mar. 12, the Commodity Futures Trading Commission (CFTC) issued a staff advisory telling exchanges to tighten surveillance on event contracts.

Simultaneously, the regulator opened a 45-day rulemaking process that asks pointed questions about inside information, manipulation, and whether some markets serve the public interest at all.

Two weeks earlier, the agency had spotlighted two Kalshi disciplinary cases involving traders who appeared to hold decisive informational edges.

One is a California gubernatorial candidate who bet on his own race, the other a YouTube editor who traded contracts tied to “Mr. Beast” while likely holding material nonpublic information.

The Mar. 12 move treats prediction markets as a real market-structure problem.

When prices influence news coverage, political narratives, and investor sentiment, insider edges and weak guardrails become public trust issues.

Growth without guardrails

From 2006 through 2020, designated contract markets listed about five event contracts a year on average. That jumped to 131 in 2021 and hit roughly 1,600 event contracts certified for listing in 2025, representing 12 times the 2021 level and 320 times the historical baseline.

Applications for exchange registration have more than doubled over the past year, largely from firms focused on running prediction markets.

Under current rules, an exchange can self-certify a new contract by giving the CFTC written notice just one business day before launch. In a market that can scale overnight, the burden of integrity falls on exchanges before problems become public.

The CFTC is not speaking in the abstract about insider-style abuse.

In the Langford case, Kalshi found a California gubernatorial candidate traded on his own candidacy and imposed a five-year suspension plus a $2,246.36 penalty.

In the Kaptur case, Kalshi found a YouTube editor traded “Mr. Beast” contracts while likely possessing material nonpublic information and imposed a two-year suspension plus a $20,397.58 penalty.

The enforcement division said both fact patterns could implicate the Commodity Exchange Act anti-fraud rules.

The advance notice of proposed rulemaking goes further.

It explicitly asks whether asymmetric information can ever serve the public interest, whether prediction markets are especially vulnerable to cross-market manipulation, whether participants skew younger, and whether self-exclusion programs, monetary or time limits, ad restrictions, disclaimers, and warnings should be factored into the Commission's public-interest analysis.

The line between crowd wisdom and single-actor vulnerability

The Mar. 12 advisory offers the sharpest frame for understanding what the CFTC now considers risky.

Some prediction markets still look like information aggregation, but others resemble insider-sensitive micro-markets.

The advisory says sports and other event contracts are often consistent with anti-manipulation standards when settlement depends on the aggregate performance of multiple participants over an extended period, because breadth makes manipulation harder.

It warns that contracts tied to injuries, unsportsmanlike conduct, physical altercations, officiating actions, or outcomes driven by a single person or small group pose a heightened risk of manipulation or price distortion.

That distinction separates broad contracts, which can plausibly claim price-discovery value, from narrow contracts that begin to look like monetized access to privileged information.

| Contract type | Example | Why it may be useful | Why the CFTC sees more/less manipulation risk |

|---|---|---|---|

| Broad, aggregate markets | Full-game outcomes, macro data, election outcomes | Can reflect dispersed public information | Harder for one person or small group to influence |

| Medium-risk markets | Earnings-adjacent narratives, official-release outcomes | Some forecasting value | Information asymmetries can still matter |

| Narrow, single-actor markets | Injuries, officiating calls, conduct penalties | Limited price-discovery value | Easier for insiders or directly involved actors to exploit |

| Highest-risk micro-markets | Candidate trading on own race, insider-linked creator contracts | Weak public-interest case | Strongest insider/manipulation concern |

Prediction markets are moving into ordinary retail finance distribution. Robinhood offers event contracts through CFTC-regulated partner exchanges across politics, sports, culture, crypto, climate, economics, and health.

Interactive Brokers' ForecastTrader is live for political, economic, finance, and climate contracts.

They are also moving into mainstream media. In January, Dow Jones signed an exclusive deal with Polymarket to bring real-time prediction data to The Wall Street Journal, Barron's, and MarketWatch, and CNBC signed a similar deal with Kalshi.

These prices are becoming headline inputs.

Once market-implied odds are embedded in coverage of elections, company events, the economy, wars, or sports, a distorted market can become a distorted news signal.

The rulemaking request itself asks how event contracts should be judged under the Commodity Exchange Act's public interest goals of price discovery, price dissemination, anti-manipulation, and protection against abusive sales practices.

The CFTC is warning that prediction markets are becoming too important to run on trust-based mechanics.

Reuters Breakingviews framed the risk in classic adverse-selection terms: people may choose not to participate if they think the other side knows more than they do.

The central tension is whether prediction markets can stay useful once insiders know the public is watching the odds.

The regulatory subtext

The CFTC is effectively asking whether prediction markets are a derivatives market, a gambling-adjacent consumer product, or both.

The rulemaking request asks about “gaming,” whether sports competitions should be treated differently from award competitions, whether responsible-gaming tools should matter, and how the Commission should weigh the needs of younger participants.

The language signals a regulator testing how far financial market logic can stretch before it collides with gambling-style consumer protection.

The state-federal fight makes this more urgent. Massachusetts blocked Kalshi's sports markets in January and February, and Nevada sued in February, arguing that the contracts constitute illegal gambling under state law.

The CFTC has insisted it has exclusive federal jurisdiction over many event contracts traded on registered markets.

A recent American Gaming Association analysis said nearly 43% of digital sports betting ads seen by US consumers in the first two months of 2026 came from prediction market operators and therefore were not subject to state gaming rules requiring responsible-gaming messaging.

The same analysis said Kalshi generated about 5.2 billion digital ad impressions this year, versus 2.9 billion for FanDuel.

What comes next

The CFTC says comments are due 45 days after Federal Register publication, and the rulemaking notice was filed for public inspection on Mar. 12, with a scheduled publication date of Mar. 13, which suggests a likely deadline of Apr. 27.

The most natural outcome is that the CFTC allows growth but pushes narrower guardrails.

In this scenario, the market can expect tougher scrutiny of single-person and small-group markets, more explicit restricted-trader lists, stronger settlement-source requirements, and heavier exchange surveillance.

Broad macro, election, climate, and full-game contracts likely survive. At the same time, the most integrity-sensitive micro-markets are squeezed.

The alternative paths are clear. If the process produces durable rules, broker distribution expands, and prediction markets become a normalized retail derivatives category.

Robinhood and IBKR distributions are already live.

Cboe is launching a new prediction market framework in the second quarter, Nasdaq has sought SEC approval for binary index options, and ICE has invested up to $2 billion in Polymarket.

However, if the federal framework remains muddy while states keep litigating, product menus fragment by state, and regulated operators hesitate to list anything that resembles a prop bet or a gambling-adjacent micro-market.

One high-profile scandal could settle the debate overnight. A case involving political insiders, league insiders, military information, or a market-resolution fiasco could trigger emergency freezes, category-level prohibitions, or rapid bipartisan calls for tougher laws.

Broad public forecasting versus narrow, insider-sensitive micro markets may define the future more than the distinction between crypto and traditional finance.

The CFTC acknowledges the potential informational value of informed trading while also asking whether the same asymmetry can lead to unfairness and the misuse of inside information.

The agency's warning is clear: prediction markets are influential enough that the same problems people understand from traditional markets now apply. This includes insider information, weak surveillance, conflicts of interest, and the risk that ordinary users stop trusting the market if they believe they are trading against better-informed insiders.

The post The CFTC starts crackdown on the growing insider problem in prediction markets appeared first on CryptoSlate.

February’s CPI report gave markets a reason to relax. Inflation looked soft enough to keep hopes for rate cuts alive, with consumer prices up 0.3% on the month and 2.4% from a year earlier, while core CPI rose 0.2% in the month and 2.5% annually. Shelter kept cooling, and the overall picture looked manageable for the Fed.

But the relief came with a catch.

By the time the report arrived on March 11, the picture had already changed. The labor market weakened, last year's payroll data was revised lower, and the conflict in Iran pushed oil to record highs.

That's the real issue the Fed has to face. February CPI may have looked calm, but it described an economy that already felt out of date by the time the report was published.

The Fed now heads into its March 17-18 meeting with a soft inflation print in one hand and a rough growth and energy backdrop in the other.

A soft print on a hard backdrop

The market’s first reaction made sense.

February CPI didn't reopen the inflation scare, as core inflation stayed contained on a monthly basis, and the rent components that drove so much of the last two years’ price pressure kept cooling. The BLS said rent rose just 0.1% in February, the smallest monthly increase in the past five years, while the shelter index rose 0.2%.

The report was stable, it felt reassuring, and looked like a clean signal that rates would keep dropping. But it arrived at the wrong time. It gave markets a picture of the economy from before one of the most important inflation inputs started moving again.

A spike in oil prices can't be contained in the energy complex. It feeds into gasoline, transport, logistics, business costs, inflation expectations, and household spending. When tanker attacks in the Strait of Hormuz intensified, crude rose to its highest level since 2022 and dragged global equities lower.

The pressure on the market was large enough that the International Energy Agency called it the biggest supply disruption in oil market history. March supply is expected to fall by around 8 million barrels per day because of the fighting and disruption around the Strait of Hormuz. Brent, which briefly hit $119.50 earlier in the week, was still trading near $97 on March 12.

That leaves February CPI looking like a snapshot of a time before the next inflation risk was fully visible.

The labor market already broke the easy story

The second problem for the Fed is that the labor market stopped supporting the soft-landing narrative just as CPI cooled.

The February jobs report showed payrolls falling by 92,000, after a January gain of 126,000, and the unemployment rate rising from 4.3% to 4.4%.

That alone is enough to complicate the inflation story. A softer CPI print paired with outright job losses isn't the disinflation markets like to celebrate, because it means demand may be cooling for less comfortable reasons.

Then there are the revisions. In February, the BLS finalized its benchmark revision, showing that the March 2025 payroll level had been overstated by 862,000 jobs. This recast last year’s labor market as much weaker than previously understood. The BLS said the total change in nonfarm employment for 2025 was revised down to 181,000 from 584,000.

That changes the context for everything. It means the economy entered 2026 with less labor-market strength than the headlines implied for months. It also means the Fed isn't weighing a soft CPI print against a strong labor cushion, but against a labor market that may have been weaker all along.

Iran made the CPI print feel old on arrival

The Middle East conflict is what turns this into a policy risk.

If oil had stayed quiet, the Fed could have looked at February CPI and argued that inflation was still bending lower while the economy gradually slowed. That wouldn't solve the policy problem, but it would at least give officials a coherent narrative.

The conflict in Iran changed that. As the war intensified, crude spiked, Wall Street sold off, and bond yields climbed as investors absorbed the risk of a larger supply shock.

That's why the Fed now looks boxed in.

If it leans too much on the softer CPI print, it risks treating stale inflation data as proof that price pressure is fading on its own. If it leans too much on the oil shock and keeps policy tight for longer, it risks pressing harder on an economy where jobs are already deteriorating.

Goldman Sachs pushed back its first Fed cut call to September from June because the Middle East conflict lifted inflation risk even as labor data softened.

Nonetheless, a soft CPI print is still useful. It's real data, and it tells you inflation wasn't accelerating in February. However, it doesn't settle the bigger question facing markets or the Fed.

Was February the start of a durable move lower in inflation, or simply the last calm reading before oil starts feeding into prices and labor weakness gets worse?

Even the Fed’s preferred inflation gauge, PCE, didn't provide much clarity. January consumer spending rose 0.4%, while core PCE increased 0.4% on the month and 3.1% from a year earlier, a much firmer underlying inflation signal than the softer February CPI print implied.

That means the Fed is still looking at sticky price pressure before the latest oil shock is fully visible in the data, which makes any market relief tied to one calm CPI report look even more fragile.

CryptoSlate made that point from the crypto side, and the same logic applies to macro more broadly. When oil, jobs, and inflation stop moving in sync, headline-driven optimism gets shaky fast.

February CPI gave markets relief, but it failed to give the Fed a clean answer. The report looked calm because it described February. The Fed has to make its next decision in a March economy shaped by weaker jobs and a Middle East oil shock. That is why the real risk here is false comfort.

The post The latest US inflation report looked like good news — next week may change that appeared first on CryptoSlate.

A quiet shift is underway in the stablecoin hierarchy. While Tether’s USDT still dominates the digital dollar market, the gap between the two largest issuers is narrowing as USDC steadily expands its footprint and Tether’s growth shows signs of softening.

Additionally, USDC is gaining ground in the places where the next wave of crypto money is likely to show up most clearly: regulated payments, institutional settlement, and high-velocity on-chain transfers.

Tether’s USDT still holds the largest stock of digital dollars in circulation, but the contest is shifting from a simple market-cap race to a fight over which issuer controls the rails that move new capital through crypto.

That split is now visible in both the long-term structure and the last month of market-cap movement. The stablecoin market stands at about $315 billion, giving the sector a much larger base than earlier in the cycle.

Within that pool, USDT still leads with 58% market share by supply, keeping Tether firmly in command of the largest crypto cash reserve.

Supply, however, is only one part of the picture. The more revealing question is where fresh dollars are going, which token they move through, and which issuer is building infrastructure institutions can use at scale.

That is where Circle has started to build a stronger case. Circle's financial statements confirm USDC circulation reached $75 billion at the end of 2025, up 72% year over year, while Q4 on-chain transaction volume climbed to $12 trillion, up 247% from a year earlier. Those figures indicate a stablecoin moving through wallets, venues, and payment flows more quickly.

Tether, for its part, remains too large to dismiss. In its latest quarterly disclosure, Tether stated USDT circulation topped $186 billion, reserve assets approached $193 billion, and its total US Treasury exposure reached $141 billion.

It also said it issued nearly $50 billion in new USDT during 2025. Those figures show a business that still dominates the inventory side of crypto dollars, especially across exchanges, offshore trading venues, and markets where users want a dollar-linked asset without relying on local banking systems.

Over the past month, USDC’s market cap has risen around 8%, pushing it to roughly $79 billion and a fresh all-time high.

Tether has remained far larger, but USDT is still sitting about $3 billion below the roughly $187 billion peak it reached in December 2025, a gap that gives Circle a clearer opening to chip away at Tether’s lead than the headline supply table alone suggests.

So the tension is real. Tether still controls the biggest pile of crypto cash. Circle is building faster in the parts of the market most closely aligned with the next phase of regulation and institutional adoption.

For traders and Bitcoin investors, stablecoins remain the main form of dollar liquidity inside crypto.

Whoever captures more of the next inflow can shape where liquidity thickens, how collateral is posted, and which rails become the default path for new capital entering the market.

USDT still owns supply, while USDC is winning more of the flow

The cleanest way to understand the shift is to separate supply from velocity. USDT still leads in outstanding supply, meaning more dollars are parked in Tether than in any rival stablecoin. But transaction data suggests USDC is gaining influence over how money moves.

Bloomberg, citing Artemis Analytics, reported that stablecoin transaction volume rose 72% to $33 trillion in 2025, with USDC accounting for $18.3 trillion and USDT for $13.3 trillion.

That divergence carries more weight than a simple supply table. A stablecoin that wins more transaction flow can become the preferred medium for settlement, treasury movement, and short-duration capital rotation, even while another token still holds a larger long-term balance.

Put differently, Tether still looks stronger as stored crypto cash, while Circle is making a case to become the preferred token for moving crypto cash.

The market is also assigning the two issuers different jobs. Tether’s edge remains distribution. It has the deepest footprint across global exchanges and a large user base in emerging markets, where demand for dollar-linked assets often reflects local currency weakness, capital controls, or banking friction.

Circle’s edge is legibility. It has built a reserve model and disclosure framework that fit more naturally with banks, regulated payment firms, and institutions that need cleaner lines around custody, compliance, and audits.

Circle’s own transparency page makes that pitch directly. The company says the bulk of USDC reserves sit in the BlackRock-managed Circle Reserve Fund, with the rest primarily in cash at regulated financial institutions, and notes that its financial statements are audited by Deloitte.

That does not erase market competition, and it does not guarantee that USDC will overtake USDT by supply. It does give Circle a stronger position in the regulated lane of the market at a moment when regulation is beginning to sort winners by use case.

The policy backdrop is moving in that direction. A Federal Reserve Bank of St. Louis review of the GENIUS Act framework says payment stablecoin issuers face tight reserve rules, monthly disclosures, and annual audited financial statements once issuance passes $50 billion.

State-qualified issuers above $10 billion would also need to move toward federal oversight within a year. Those thresholds do not decide the market on their own, but they make compliance architecture more important than it was during the earlier, more crypto-native phase of stablecoin growth.

| Metric | USDT | USDC | Why it is relevant |

|---|---|---|---|

| Circulation / supply | $183 billion | $79 billion | Shows where the largest stock of crypto dollars sits |

| 2025 issuance / growth | Nearly $50 billion new issuance in 2025 | 72% year-over-year circulation growth | Shows how quickly each issuer is expanding |

| Transaction volume in 2025 | $13.3 trillion | $18.3 trillion | Shows which token is moving more money |

| Core strategic edge | Exchange distribution and global trading liquidity | Regulated settlement and institutional usability | Points to a split market rather than a single winner |

That split is already visible in payments. Visa launched USDC settlement in the United States with Cross River Bank and Lead Bank and plans broader U.S. expansion through 2026. It also said its monthly stablecoin settlement volume had reached a $3.5 billion annualized run rate as of November 30.

That is not the same as saying USDC will dominate all crypto activity. Circle, however, is gaining share in one of the most important growth lanes outside exchange trading.

The Bitcoin implication centers on liquidity, collateral, and who captures the next inflow

For Bitcoin, the stablecoin contest is not a side issue. Stablecoins fund exchange balances, back collateral positions, and give traders a dollar-linked unit that can move around the clock without leaving the crypto system.

When stablecoin supply grows, the market’s pool of deployable dollar liquidity tends to deepen. When one stablecoin gains more of that growth, the question becomes which venues and user groups will control the new liquidity.

Glassnode has described the Stablecoin Supply Ratio as a gauge of stablecoin-denominated buying power relative to Bitcoin supply, with lower readings implying greater potential purchasing power. That supports a practical point: stablecoins are one of the clearest ways to measure how much dollar liquidity is sitting inside crypto and how ready that liquidity may be to rotate into BTC.

If USDT remains the main store of offshore trading cash while USDC gains ground in regulated settlement and enterprise finance, Bitcoin liquidity could become more segmented over the next year. Offshore spot and derivatives venues may remain heavily USDT-centric.

Meanwhile, institutionally mediated Bitcoin activity could lean more toward USDC as banks, payment firms, and treasury desks choose the stablecoin that best fits compliance, reserve transparency, and settlement requirements.

That would not weaken Bitcoin. Tether would still matter most for the largest reservoir of crypto-native trading capital, and it could broaden the set of rails that feed Bitcoin demand.

Circle would matter more for the next tranche of regulated capital seeking a stablecoin bridge to digital assets without stepping outside traditional financial guardrails.

Standard Chartered has projected that the stablecoin market could reach $2 trillion by the end of 2028. From a base of roughly $315 billion today, that implies about $1.7 trillion of additional room for growth.

The key question is which issuer, reserve model, and regulatory framework will capture the next $1.7 trillion.

There are several plausible paths from here.

- USDT keeps the largest share of outstanding supply because its exchange and international distribution remain hard to replace, while USDC continues to gain in institutional payments and regulated settlement.

- Policy clarity and more bank integrations allow USDC’s lead in transaction velocity to translate into much bigger gains in outstanding supply.

- The market keeps assigning USDT the role of dominant crypto trading cash, and USDC’s gains remain meaningful but narrower, concentrated in regulated channels rather than across the full market.

The evidence today supports the first path more than the others. Tether is still too large, too embedded, and too useful across crypto’s global trading stack to call this an imminent overthrow.

Circle, though, has enough momentum in transactions, reserve design, and institutional integrations to argue that the next phase of stablecoin growth may not belong to the same issuer that dominated the last one.

Circle’s case also rests on recency, not just structure. USDC has hit a new market-cap high near $79 billion after roughly 8% monthly growth, while USDT has yet to reclaim the peak it reached in December 2025.

The broader takeaway for Bitcoin and the wider market is straightforward. USDT still owns the largest share of crypto’s cash inventory. USDC is making a stronger claim on crypto’s future cash plumbing.

If stablecoins are heading toward a multi-trillion-dollar market, the fight is no longer just about who is biggest now. It is about who captures the next wave of money, and which version of the dollar becomes the preferred bridge into Bitcoin, exchanges, payments, and on-chain finance.

The post Stablecoins in 2026: USDC surges 8% to $79B as Circle captures institutional flow from Tether appeared first on CryptoSlate.

Washington is getting ready to potentially make life easier for the biggest US banks.

That can sound pretty abstract if you don't strip it down to the mechanics. Regulators decide how much capital banks must keep to absorb losses and how much liquidity they need if funding starts to disappear.

More capital and more liquidity make banks sturdier, though they also limit how much money banks can lend, trade, or return to shareholders. Less of both gives banks more room to move while leaving a thinner cushion when conditions turn.

That tradeoff is now back at the center of US bank policy. On March 12, Federal Reserve Vice Chair for Supervision Michelle Bowman said regulators are preparing a softer rewrite of the long-disputed Basel III endgame rules, the post-2008 capital package Wall Street has spent years trying to weaken.

The new version could leave large-bank capital requirements roughly flat or slightly lower than current levels once related changes are included, and could free up more than $175 billion in excess capital across the industry. Surcharges for the largest global banks may also fall by about 10%.

That is a sharp turn from where the debate stood less than three years ago.

The earlier draft, pushed under Bowman's predecessor, Michael Barr, in 2023, would have raised capital requirements at the biggest banks by about 19%. Banks argued that the proposal would make credit more expensive, reduce market-making capacity, and push activity out of the regulated system.

Their critics argued the opposite: years of easy money, concentrated asset exposures, and repeated stress episodes had made thicker buffers necessary. The new draft lands much closer to the banks' side of that argument.

The contrast is especially striking for Bitcoin: while Washington appears ready to give large banks more flexibility on capital and liquidity, direct crypto exposure can still attract far harsher treatment, suggesting regulators remain more comfortable backstopping traditional balance-sheet risk than normalizing Bitcoin on bank books.

The real policy turn is bigger than capital

On its own, that would already be a major banking story. What gives it wider reach is the second piece moving alongside it: liquidity.

Earlier this month, Treasury officials said they were taking a fresh look at liquidity rules and floated an idea that would give banks some regulatory credit for collateral they have already prepositioned at the Federal Reserve's discount window.

In plain terms, regulators may start treating part of a bank's ability to borrow emergency cash as usable liquidity. Treasury described that borrowing capacity as “real, monetizable liquidity.”

That means banks may no longer need to carry quite as much dead weight if they can show they already have assets lined up at the Fed and can turn them into cash quickly. The system, in other words, is being redesigned around a more direct role for the central bank backstop.

For years, regulators tried to build a framework that would make banks self-reliant in a panic. They were supposed to hold enough liquid assets to survive a run and treat the Fed's discount window as an emergency tool of last resort.

But in practice, banks have long avoided the window because using it is seen as a clear sign of distress. Treasury is now openly saying that this stigma is a problem and that the rules should better reflect the reality that the discount window exists to be used.

That lands differently only three years after the regional bank failures of 2023.

Silicon Valley Bank, Signature Bank, and First Republic collapsed because confidence vanished fast, depositors moved faster, and liquidity that looked available in theory proved much harder to mobilize in real time.

The Fed's own review of SVB said the bank had serious weaknesses in liquidity risk management and that supervisors failed to fully grasp how exposed it had become as it expanded. The official answer then was straightforward: banks needed better oversight, better preparation, and stronger resilience.

The 2026 rewrite says the system also needs lighter capital requirements, a less punitive treatment of discount-window readiness, and fewer constraints on the biggest institutions.

More room for banks, less friction in the system

If the new framework goes through, large banks would have more room to extend credit, increase trading capacity, repurchase shares, and support deal activity.

Supporters say that's exactly the point. Bowman argued that excessive capital requirements carry real economic costs and can interfere with banks' basic job of supplying credit to the broader economy. Industry groups made the same case, saying the revised plan would align requirements more closely with actual risk.

The other side of that trade is just as clear.

Capital rules are a shock absorber, and liquidity rules are a form of brake. Ease both at the same time and banks get more freedom while the system carries less built-in friction. It moves the official balance away from maximum safety and toward efficiency, credit creation, and smoother access to Fed funding.

However, the Fed's biggest problem now is timing.

Senator Elizabeth Warren warned against weaker capital standards while geopolitical and credit risks are already climbing. While her objection is political, it still nails the contradiction at the center of the debate.

After SVB, Washington said bank resilience had to come first. Now, with growth fears, market volatility, and funding sensitivity back in view, Washington is preparing to give the largest banks more room to breathe.

The consequences are simple.

This is a decision about how much slack to keep in the financial system before the next stress event arrives. A stricter framework will force banks to carry more idle protection. A softer one will accept a little more vulnerability in exchange for more lending, more market activity, and less drag on profitability.

Bitcoin's critique of the banking system has always been strongest when policymakers expand the role of emergency support while presenting the overall structure as stable and self-contained.

The discount window isn't a side detail in that story, but part of the infrastructure that keeps confidence from breaking all at once.

When Treasury starts arguing that prepositioned Fed collateral should count more directly in bank liquidity rules, it's acknowledging that the system still depends on central-bank rescue architecture even in periods sold as normal.

A crisis isn't near, but Washington is set on rewriting the post-SVB rulebook. This time, it wants to base it on a very pragmatic assumption, which is that when the next panic hits, the biggest banks need to have more flexibility and the Fed's backstop needs to be easier to use without hesitation.

It's certainly a much-needed relief for Wall Street.

For everyone else, though, it's a reminder that the banking system is still being tuned around the same old problem: private risk-taking works best when public liquidity is always close at hand.

The post Washington prepares $175B break for big banks — weakening protections against financial crisis appeared first on CryptoSlate.

Cryptoticker

The crypto market is finally back in the green. After weeks of boring sideways trading and scary news headlines, Bitcoin ($BTC) blasted back past $71,500 this week. When the "Big Brother" of crypto pumps like this, it usually pulls the rest of the market up with it. Right now, everyone is talking about "Altseason" again, as traders start moving their money into smaller coins to chase even bigger gains.

Here are the five tokens that made the most noise over the last seven days.

1. River (RIVER)

$River has emerged as the breakout star of the week, leading the pack with a massive rally that caught many traders by surprise.

- 7-Day Gain: ~41%

- The Catalyst: On March 11, the project reached a major milestone with over $1 million in tokens staked, creating a supply shock that effectively reduced exchange liquidity.

- Market Move: The price successfully cleared the $20 resistance zone, with technical indicators suggesting a strong trend reversal after months of accumulation.

2. Bittensor (TAO)

Continuing its dominance in the Decentralized AI sector, Bittensor has once again proven why it is a favorite among institutional investors.

- 7-Day Gain: ~38.6%

- The Catalyst: Optimism surrounding General Tensor’s $5M funding round and the news that the Grayscale Bittensor Trust is now an SEC-reporting company has provided the "institutional seal of approval" for $TAO.

- Market Move: TAO surged past the $260 level, with open interest hitting a yearly high as the network scales to 256 subnets.

3. Render (RENDER)

$Render continues to benefit from the global demand for decentralized compute power and its close ties to the AI hardware narrative.

- 7-Day Gain: ~30%

- The Catalyst: Bullish sentiment ahead of major AI conferences (like Nvidia's GTC) has kept RENDER in the spotlight. Furthermore, increased network usage for AI training has led to a significant uptick in RENDER token burning.

- Market Move: Despite some weekend profit-taking, Render remains one of the strongest infrastructure plays, comfortably holding above its 50-day moving average.

4. DeXe (DEXE)

The $DeXe protocol has become a focal point for the "Governance-as-a-Service" trend, attracting significant volume from DeFi enthusiasts.

- 7-Day Gain: ~20.1%

- The Catalyst: A series of Marketing SubDAO initiatives and high-volume buying—up over 100% in 24 hours—indicated that "whales" are actively accumulating the token.

- Market Move: DEXE broke out of its long-term descending channel, now targeting the $5.50 psychological level as its next major objective.

5. Artificial Superintelligence Alliance (FET)

The $FET token (representing the merged Fetch.ai, SingularityNET, and CUDOS ecosystem) is showing renewed strength as its unified vision takes shape.

- 7-Day Gain: ~16%

- The Catalyst: Positive market reaction to the ASI:Cloud infrastructure expansion and the rollout of new autonomous agent tools that lower the barrier for AI development.

- Market Move: FET reclaimed the $0.18 level, a key support-turned-resistance zone. A sustained hold here could signal the start of a multi-month recovery.

As Operation Epic Fury enters its third week, the global financial landscape is being rewritten in real-time. For decades, the "War Playbook" was simple: sell stocks, buy Gold, and hide in U.S. Treasuries.

However, as the conflict between the U.S. and Iran escalates in March 2026, that playbook has been set on fire. While traditional markets face a staggering $5 trillion evaporation, Bitcoin ($BTC) and the broader crypto ecosystem are doing something unprecedented: they are holding the line.

Why is Institutional Money Flowing to BTC?

In 2026, the "War Discount" that usually drags down risk assets is failing to suppress the Bitcoin price. Institutional investors are no longer viewing BTC as a "risk-on" tech trade, but as a "risk-off" sovereign asset. While the S&P 500 has plummeted since the February 28th strikes, Spot Bitcoin ETFs recorded over $760 million in net inflows this week alone.

The $5 Trillion Collapse of the "Old Guard"

The numbers coming out of Wall Street and the London Bullion Market this week are nothing short of apocalyptic. The massive capital flight is no longer rotating into traditional safety nets.

- Equities in Freefall: Over $2.4 trillion has been wiped from U.S. stocks since the conflict began. With oil prices surging past $110/bbl due to the Strait of Hormuz blockade, the industrial and tech sectors are bleeding out.

- The Gold Anomaly: In a shock to "boomer" investors, Gold and Silver have seen a combined $2.5 trillion in value destroyed. While physical gold remains a store of value, the "Paper Gold" market is facing a massive liquidity crunch as institutional players dump everything to cover margin calls.

Bitcoin’s "Safe Haven" Graduation

While the S&P 500 and Gold have cratered, Bitcoin (BTC) has shown remarkable resilience. After a brief "flash crash" to $62,400 on Day 1 of the invasion, BTC has surged back, currently consolidating firmly above $70,000.

Why Bitcoin is a Good Investment

- Censorship-Resistant Capital: As the U.S. and Israel tighten the noose on Iranian financial networks, and global banks brace for cyber-retaliation, the "unseizable" nature of on-chain assets has become the ultimate insurance policy.

- Institutional "Diamond Hands": BlackRock and Fidelity aren't selling; they are treating this geopolitical dip as a generational accumulation zone.

- The Scarcity Narrative: On March 10, 2026, the 20 millionth Bitcoin was officially mined. In a world of infinite war spending and fiat debasement, the 21-million-cap has never looked more attractive to those seeking to preserve purchasing power.

Altcoin Watch: Beyond the King

It’s not just Bitcoin. We are seeing a "Flight to Utility" across the board as users seek refuge from failing crypto exchanges and traditional banking infrastructures.

- Ethereum ($ETH): Currently holding above $2,100. The new BlackRock ETHB ETF provides a yield-bearing sanctuary for institutional cash seeking smart contract exposure.

- $XRP: On-chain payments on the XRPL have surged to 2.7 million daily transactions as businesses scramble for alternative settlement layers outside of the threatened SWIFT system.

- Stablecoins: Demand for USDC and USDT has hit all-time highs in the Middle East as citizens seek to preserve their wealth against collapsing local currencies.

Note on Self-Custody: During times of global instability, reliance on centralized platforms can be risky. Many investors are migrating their assets to verified hardware wallets to ensure 24/7 access to their funds regardless of the geopolitical climate.

The Bottom Line

The image of the "$5 Trillion Loss" isn't a warning for crypto—it’s a eulogy for the old financial system. In 2026, the market has rendered its verdict: In times of kinetic war, digital assets provide a level of sovereignty and portability that physical gold simply cannot match. The "Digital Gold" thesis is no longer a theory; we are watching its global implementation in real-time.

The institutional appetite for digital assets is showing renewed vigor as BlackRock’s iShares Bitcoin Trust (IBIT) recorded a substantial purchase of approximately $147.7 million worth of Bitcoin. This latest acquisition is not an isolated event; it marks the third consecutive week of net inflows for the world’s largest spot Bitcoin ETF, signaling a decisive shift in market sentiment.

Institutional Confidence Returns to BTC

After a period of stagnant price action and cooling interest in early 2026, the tide appears to be turning. The consistent inflow into IBIT suggests that institutional allocators are viewing current price levels as a strategic entry point. This "three-peat" of weekly gains provides a necessary cushion for the Bitcoin price, which has faced significant volatility in recent months.

Market Impact and "Giga-Bullish" Signals

The magnitude of these inflows often serves as a leading indicator for broader market movements. When a behemoth like BlackRock consistently accumulates, it reduces the available liquid supply on exchanges, creating a "supply shock" environment.

- Sustained Momentum: Three weeks of inflows suggest this is a trend, not a "dead cat bounce."

- Liquidity Concentration: BlackRock now manages a significant portion of the total crypto news cycle, often dictating the daily momentum of the entire asset class.

- Wider Adoption: This streak coincides with BlackRock's expansion into other products, such as their recently launched staked Ethereum ETF (ETHB), further cementing their dominance in the digital asset space.

Strategic Outlook for Traders

While the "giga-bullish" narrative is gaining steam, traders should remain aware of macroeconomic headwinds that could impact the pace of these inflows. However, for now, the data is clear: BlackRock is buying, and the institutional gate is wide open.

The stablecoin sector has officially crossed a historic threshold, reaching a total market capitalization of $320 billion as of March 2026. This vertical climb represents more than a mere recovery from previous cycles; it marks the "industrialization" of digital dollars. Unlike the retail-driven spikes of the past, the current momentum is fueled by multi-billion dollar inflows from traditional finance (TradFi) giants and the implementation of the GENIUS Act in the United States.

What is Driving the Stablecoin Surge?

The primary driver behind the $320 billion market cap is the rapid transition of stablecoins from speculative trading tools to global payment infrastructure. In January 2026 alone, stablecoin networks moved over $10 trillion in transaction volume—a figure that now rivals legacy settlement systems like Visa. This "vertical" adoption is led by institutional demand for 24/7 settlement and the legislative "green light" provided by federal regulators.

Market Composition: The Rise of Regulated Giants

While Tether (USDT) remains the liquidity heavyweight with a market cap of approximately $184 billion, the narrative in 2026 has shifted toward compliant, onshore alternatives.

- Circle (USDC): Has seen explosive growth, reaching $78 billion, outperforming the broader sector in monthly growth due to its status as the "compliance-first" choice for U.S. institutions.

- BlackRock BUIDL: The tokenized liquidity fund has surged 36% recently, hitting $2.46 billion, proving that yield-bearing institutional "stable-assets" are a core growth pillar.

- USAT: Tether’s newly launched, U.S.-regulated stablecoin is already challenging the status quo, aiming to capture the institutional market governed by the GENIUS Act.

The Impact of the GENIUS Act