Cryptocurrency Posts

Crypto Briefing

The halt highlights the challenges smaller firms face in emulating large-scale Bitcoin strategies, emphasizing the need for robust capital access.

The post The Bitcoin Society halts plans to build crypto treasury after brutal Q1 appeared first on Crypto Briefing.

Suspending the federal gas tax could offer minor consumer relief but risks underfunding crucial infrastructure projects, impacting long-term growth.

The post Trump proposes temporary suspension of federal gas tax amid rising fuel prices due to Iran war appeared first on Crypto Briefing.

GameStop's failed bid highlights challenges in financing large acquisitions, impacting market confidence and future tech sector consolidation.

The post GameStop’s $56B bid for eBay rejected, market doubts acquisition success appeared first on Crypto Briefing.

Enhanced US-Japan currency coordination may stabilize forex markets, potentially reducing volatility in risk assets and impacting global investments.

The post Scott Bessent reaffirms US, Japan coordination on currency moves appeared first on Crypto Briefing.

A potential BOJ rate hike could strengthen the yen, impacting global carry trades and creating selling pressure across various risk assets.

The post Bank of Japan debates near-term rate hike, eyes June move appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Coinbase CEO Says Crypto Bill Could Rewire American Finance — Senate Votes Thursday

A long-stalled crypto market structure bill is moving through Congress with new momentum — and Coinbase’s top executive says it could reshape the American financial system.

Coinbase CEO Brian Armstrong declared his company’s support for the Digital Asset Market Clarity Act on Wednesday, calling the legislation a “true compromise” that balances the demands of the crypto industry against the interests of the traditional banking sector and signaling the bill is in the best shape he has seen since negotiations began.

The statements, via Fox News, came as the Senate Banking Committee prepared to hold its markup of the CLARITY Act on May 14, the first formal committee vote on the legislation in the Senate after months of procedural delays and two cancelled markups.

Committee Chairman Tim Scott has set a target of June or July 2026 for a full Senate floor vote, while the White House has marked July 4 as its goal for a presidential signature.

JUST IN: Coinbase CEO Brian Armstrong tells Fox Business there was a compromise on the Bitcoin & crypto market structure bill, clearing the way for it to pass the Senate

— Bitcoin Magazine (@BitcoinMagazine) May 13, 2026

"It's in the best place we've seen so far…We're ready to support a markup later this week."pic.twitter.com/U88UfywifU

A legislative marathon is taking place

The CLARITY Act — formally H.R. 3633, the Digital Asset Market Clarity Act of 2025 — cleared the House of Representatives on July 17, 2025, in a 294–134 bipartisan vote, with all 216 House Republicans in support and 78 Democrats crossing the aisle.

Since then, the bill sat in the Senate Banking Committee through two cancelled markups, extended stablecoin negotiations, and an intensifying lobbying war between crypto firms and Wall Street banks.

At its core, the legislation draws a regulatory line between the Securities and Exchange Commission and the Commodity Futures Trading Commission.

Under the bill, the CFTC would hold exclusive jurisdiction over spot and cash markets for digital commodities while the SEC retains authority over investment contract assets and primary market fundraising. Stablecoins are carved out as a separate category under shared oversight.

The Senate version of the bill expanded beyond the House text, growing to nine titles that cover decentralized finance protections, illicit finance provisions, bankruptcy safeguards for crypto customers, and the Blockchain Regulatory Certainty Act, which creates safe harbors for software developers who publish code without controlling customer funds.

The stablecoin standoff

The bill’s most contested provision centered on stablecoin yield. Banks warned that permitting crypto platforms to pay rewards on stablecoin balances would trigger deposit flight from traditional bank accounts and threaten lending operations. Crypto firms, led by Coinbase, argued that restrictions would hand banks a competitive advantage and strip Americans of new financial tools.

The standoff produced a compromise brokered by Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD). Under the final language in Section 404 of the bill, stablecoin issuers and affiliated digital asset service providers cannot pay yield on balances if that yield is the functional or economic equivalent of bank interest.

Activity-based rewards — cashback on payments, transaction-based incentives, and rewards tied to commerce — remain permitted. A stablecoin holder who takes no action generates no return.

Armstrong confirmed his support after the compromise text became public, with Coinbase’s Chief Policy Officer Faryar Shirzad declaring the industry “secured what is important.”

Speaking on Fox, Armstrong credited Senators Tillis, Alsobrooks, and their staffs for bringing both sides to the table. “I’ve got to give a lot of credit to Senators Brooks and Tillis and their staff who worked tirelessly on this,” he said.

Armstrong described a financial sector moving fast toward digital asset integration.

“I go around and I speak with lots of different bank CEOs, and many of them are just leaning into this as an opportunity to grow their business,” he said. “They’re integrating stablecoins as fast as they can.”

More than 100 crypto firms and industry groups, including the Crypto Council for Innovation and the Blockchain Association, wrote to the Senate Banking Committee in April urging the panel to advance the bill, warning that continued delays risk pushing innovation and capital outside the United States.

Treasury Secretary Scott Bessent reinforced that call, telling a Senate panel the legislation is essential to protecting the dollar’s status as the world’s reserve currency.

The Thursday markup is not the finish line. If the Banking Committee approves the bill, it must merge with a version passed by the Senate Agriculture Committee in a party-line 12–11 vote in January 2026.

A full Senate floor vote requires 60 votes, making Democratic support a practical requirement and leaving an ongoing fight over ethics provisions — specifically language addressing President Trump and his family’s crypto holdings — as the bill’s biggest remaining fault line.

This post Coinbase CEO Says Crypto Bill Could Rewire American Finance — Senate Votes Thursday first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Suisse Secures Bermuda Regulatory Approvals for International Digital Asset Expansion

Bitcoin Suisse (International) Ltd., an affiliate of the Switzerland-based Bitcoin Suisse Group, has obtained dual regulatory approvals from the Bermuda Monetary Authority, according to a note shared with Bitcoin Magazine.

The Bermuda Monetary Authority (BMA) granted the entity a Class F license under Bermuda’s Digital Asset Business Act (DABA) and a Class B registration under the Investment Business Act 2003.

The approvals, granted on a pre-operational basis, authorize Bitcoin Suisse to provide regulated digital asset management and investment advisory services to professional and institutional clients. The entity is domiciled in Hamilton, Bermuda, and is a subsidiary of BTCS Holding Ltd., the group’s parent holding company.

The DABA license covers the provision of regulated digital asset business services, while the IBA registration permits investment advisory and discretionary portfolio management.

Clients may fund mandates in Bitcoin, stablecoins, or fiat currency, the company said. The entity operates on a non-custodial basis, relying on regulated custodial providers and partner banks for institutional-grade security.

Andrej Majcen, Co-Founder and Group CEO of Bitcoin Suisse, framed the approvals as a turning point for the firm’s global ambitions.

“Institutional investors recognize digital assets as a permanent part of their portfolios. What they need is a partner who combines deep crypto-native expertise with the governance and regulatory standards they expect from traditional financial services,” Majcen said. “The BMA approvals mark an important step in Bitcoin Suisse’s transition towards a global wealth management platform.”

Multi-region bitcoin expansion strategy

Investment decisions will draw on Bitcoin Suisse’s proprietary Crypto Analysis Framework and its Global Crypto Taxonomy — a classification system covering approximately 600 digital assets across six sectors, developed over more than a decade of research. An experienced CIO Office and dedicated research function will underpin all client mandates.

Bermuda has positioned itself as a global hub for digital asset regulation since introducing the Digital Asset Business Act in 2018, one of the first comprehensive frameworks of its kind in the world. The jurisdiction’s regulatory architecture has attracted crypto-native firms seeking institutional credibility and offshore reach.

The Bermuda approvals build on Bitcoin Suisse’s existing international presence. The group holds an In-Principle Approval from the Financial Services Regulatory Authority of the Abu Dhabi Global Market, establishing a regulated footprint in the Middle East. Together, the two jurisdictions form the foundation of a multi-region expansion strategy targeting ultra-high-net-worth individuals, family offices, external asset managers, and corporate counterparties.

This post Bitcoin Suisse Secures Bermuda Regulatory Approvals for International Digital Asset Expansion first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

The 2036 Issue: Letter From The Editor

None of us can see the future. We don’t know what 2036 will bring.

We all like to tell ourselves that we can, or do, and maybe we do actually see small pieces of it coming before we catch up to them, but none of us see the whole picture. That’s, at the end of the day, part of what it is to be human.

Nevertheless we can’t seem to help ourselves from at least trying.

Going into the second half of the 2020s we are coming out of a time period that marked wild and tumultuous disruption, with the world changing in both big and small ways that none of us could have imagined in our wildest dreams at the start of 2020. As we enter the second half of the decade, events around the world are starting to push us in a direction that seems like it will be even more disruptive and unpredictable than the first half of the decade.

In this issue, we are going to do what we can’t help ourselves doing, we’re going to try to predict the shape of the next decade. I say shape, and not just the future itself, because that is the best that human beings can actually do.

These pages are filled with pieces written by some of the most influential and intelligent people that engage in this space trying to look ahead and provide something of value to you, the reader. Some have given deep analysis of how larger geopolitical trends will unfold, others have written more lighthearted musings on what different aspects of our lives will be like day-to-day, and some have written what I can only call warnings or reminders of what to keep in mind while navigating the coming ten years.

Every few generations, the world seems to go through some tumultuous upheaval. A radical shift that upends the order and institutions that maintained the previous shape of the world. I think we are entering that next period now, and we’ve probably been standing in its doorway since 2020.

Chaos and change are not solely reasons to give in to fear, or anxiety, they are also reasons to have hope and optimism. When things fall apart, it doesn’t just mean the end of what was there before, it means there is space to build something new. It signals the beginning of something new in the exact same moment that it signals the end of something old.

The next ten years are going to be the biggest opportunity yet for Bitcoin. We can either spend them optimistically building, putting our energy into bringing into reality the positive impact we see that Bitcoin can have on the world, or we can squander them doing the opposite.

Ultimately, the shape the future has when it finally arrives at our doorstep will be the shape that all of our individual actions and choices mold it into.

Make them count.

Don’t miss your chance to own The 2036 Issue — featuring articles written by many influential figures in the space pondering the challenges of the next decade!

This piece is the Letter from the Editor featured in the latest Print edition of Bitcoin Magazine, The 2036 Issue. We’re sharing it here as an early look at the ideas explored throughout the full issue.

This post The 2036 Issue: Letter From The Editor first appeared on Bitcoin Magazine and is written by Shinobi.

Bitcoin Magazine

Senate Crypto Bill Faces Over 100 Amendments Ahead of Thursday Markup

Senate Banking Committee members have filed more than 100 proposed amendments to the Digital Asset Market Clarity Act, according to Politico reporting. The panel is set to convene on Thursday for a long-awaited markup vote that crypto and industry leaders say could reshape digital asset regulation in the United States.

The committee scheduled its executive session for 10:30 a.m. on May 14 at Room 538 of the Dirksen Senate Office Building in Washington, D.C., where lawmakers will debate the amendments and vote on whether to send the bill to the full Senate floor.

The flood of filings follows the release of an updated 309-page draft of the bill earlier this week, expanded from the 278-page version proposed in January.

Senator Elizabeth Warren leads the opposition push, submitting more than 40 amendments alone, with the bulk of proposed changes coming from Democratic members of the Banking Committee.

The wave of filings mirrors the January markup session, which drew 137 amendments before that session was cancelled, signaling that resistance to the bill remains strong even as its supporters push for a final vote.

At the center of the dispute is how the bill handles stablecoin yield products — crypto that offer returns to holders. Banking groups argue such crypto products threaten traditional deposit bases; crypto firms counter that reward programs support liquidity and customer activity without functioning as bank deposits.

The American Bankers Association has sent more than 8,000 letters to Senate offices since last Friday, targeting the stablecoin yield compromise brokered by Senators Thom Tillis and Angela Alsobrooks. That compromise, reached after months of negotiations, prohibits stablecoin issuers from paying interest or yield to users who hold tokens passively, while preserving exceptions for rewards tied to genuine platform transactions and payment activity.

Senators Jack Reed and Tina Smith filed amendments to tighten those standards further, targeting products that deliver returns in ways that resemble traditional interest-bearing deposit accounts.

The banking lobby maintains the existing compromise language still leaves room for stablecoin platforms to replicate high-yield savings products without meeting bank-level regulatory requirements.

Senate ethics provisions and developer protections

Senator Chris Van Hollen introduced a proposal that would prohibit senior government officials and their families from owning or promoting crypto-related businesses — a demand Democrats say is non-negotiable given President Trump’s close ties to the crypto industry.

Republican sponsors have resisted the provision, with some warning that ethics riders could fracture the coalition needed for the bill to advance.

A recent draft of the bill already included language shielding noncustodial developers from being classified as money transmitting businesses, with that protection extended retroactively to cover past conduct.

The broader stakes for the crypto industry

The CLARITY Act, formally H.R. 3633, passed the House on July 17, 2025, by a 294–134 bipartisan vote before stalling in the Senate through two cancelled markup sessions and protracted stablecoin negotiations.

At its core, the bill would draw a clear jurisdictional line between the Securities and Exchange Commission and the Commodity Futures Trading Commission, ending years of enforcement-based policymaking that left crypto firms operating under legal ambiguity.

Prediction markets have priced the odds of the bill becoming law in 2026 roughly at 60%, the highest level in months, with the White House setting a July 4 target for a presidential signature.

Committee Chairman Tim Scott had originally targeted a Senate floor vote for September 2025, then pushed that deadline to end-of-year, and most recently said he hoped to reach a full Senate vote by June or July 2026.

Thursday’s markup is the first formal committee vote on the bill in the Senate, and its outcome will determine whether that timeline is still within reach.

This post Senate Crypto Bill Faces Over 100 Amendments Ahead of Thursday Markup first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Blockaid Launches Real-Time Compliance Suite as Institutions Deepen Crypto Exposure

Blockchain security firm Blockaid has introduced Risk Exposure, a real-time compliance infrastructure suite built for institutions that now operate inside crypto and decentralized finance but still answer to regulators.

The launch extends Blockaid’s platform beyond scam and exploit prevention into what the company calls programmable, real-time compliance for institutional onchain finance, a category it argues has no adequate solution today.

The need is real. Banks, asset managers, custodians, and payment processors have moved from occasional crypto experimentation into continuous onchain operations. They hold positions in liquidity pools, run stablecoin settlement across multiple chains, and manage treasury exposure through DeFi protocols around the clock.

A wallet or pool that screens clean at 9 a.m. can carry tainted exposure by noon — without the institution touching a single transaction — as stolen funds move through bridges, mixers, and smart contracts faster than any compliance team can track.

The numbers behind that risk are substantial. Over the past 18 months, North Korean-linked actors moved more than $1.5 billion through the Bybit hack. Exploits at Cetus, Balancer, and KelpDAO pushed combined losses past $600 million. In most cases, tainted funds spread across wallets, liquidity pools, and counterparties before legacy compliance systems flagged anything. The forensic model — tag addresses after the fact, file a report — was not designed for this environment.

Real-time crypto compliance

Risk Exposure is built around three functions. A Risk Screening API evaluates inflows before funds are accepted, returning structured verdicts with exposure categories, dollar amounts, and severity scores formatted for audits and SAR filings. A Cosigner Policy Engine embeds AML thresholds into multisig workflows, rejecting transactions that breach preset limits even after internal approvals have cleared. DeFi Toxicity Monitors track protocols, liquidity pools, and counterparty positions throughout the day, sending alerts when exposure to sanctioned entities, stolen crypto funds, scam infrastructure, or mixers crosses defined thresholds.

Blockaid also points to a parallel threat: AI-driven “pig butchering” fraud has pushed crypto investment scams into the tens of billions of dollars each year. The FBI’s Operation Level Up found that roughly 8 in 10 victims never file a report, which means compliance tools that rely on law enforcement records to tag addresses miss the bulk of that activity.

Blockaid’s system uses transaction simulation, behavioral analysis, and AI-driven threat identification to surface exposure earlier — before scam proceeds enter institutional systems undetected.

The firm screens more than 500 million transactions each month for clients including Coinbase, MetaMask, Uniswap, Fireblocks, Polymarket, and OKX, processing hundreds of transactions per second with verdicts returned in under 300 milliseconds at 99.99% accuracy. Founded in 2022, the company has raised $83 million from Ribbit Capital, Sequoia, Greylock, and others.

For Bitcoin specifically, the implications are pointed. As BTC custody, BTC-backed lending, and Bitcoin treasury strategies move deeper into institutional balance sheets, the compliance infrastructure those institutions carry will determine how far that integration can go.

Risk Exposure is the kind of tooling that lets a regulated bank or asset manager maintain onchain exposure without asking a regulator to accept ambiguity in return.

This post Blockaid Launches Real-Time Compliance Suite as Institutions Deepen Crypto Exposure first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

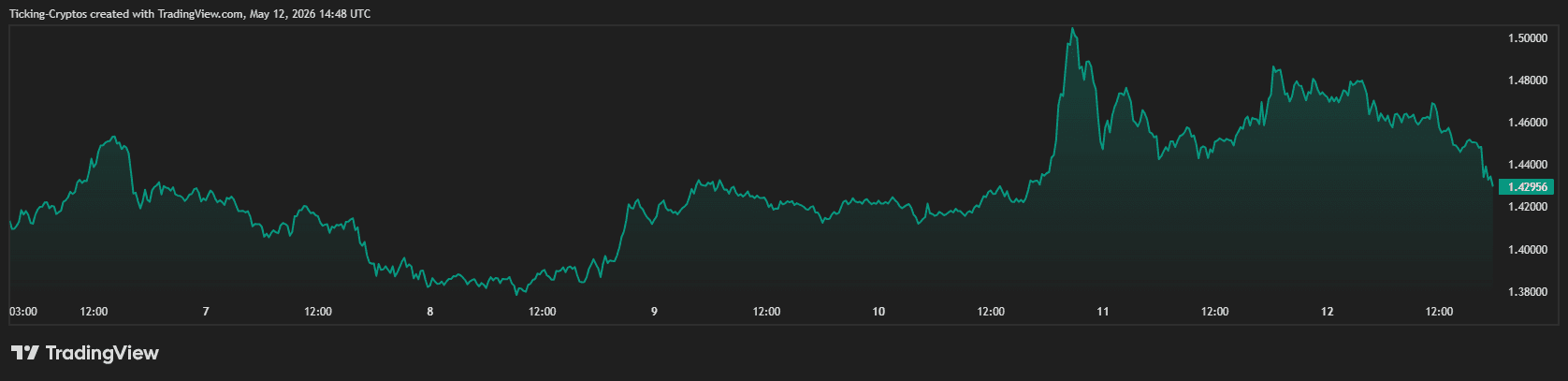

XRP is rising into a market split between traditional finance infrastructure and crypto-native skepticism.

According to CryptoSlate's data, the token recently traded above $1.46 as spot-market indicators improved, exchange-traded funds drew their strongest daily inflows in more than four months, and Ripple expanded the credit capacity behind its institutional prime brokerage business.

However, this came at a time when derivatives traders continue to lean against the move, with Binance futures data showing persistent selling pressure even as leverage rebuilds across major exchanges.

That tension has turned XRP into a test case for whether institutional access, ledger utility, and market infrastructure can overpower a futures market still positioned for weakness.

Spot demand meets futures resistance

The divide between spot demand and derivatives positioning has become the clearest feature of XRP’s market structure.

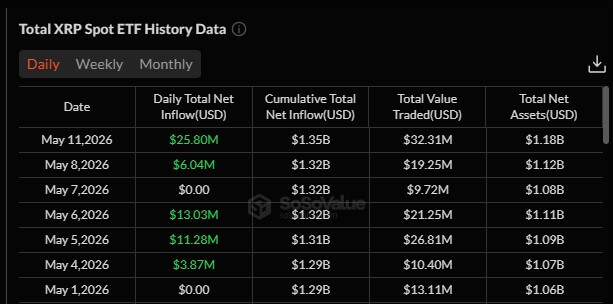

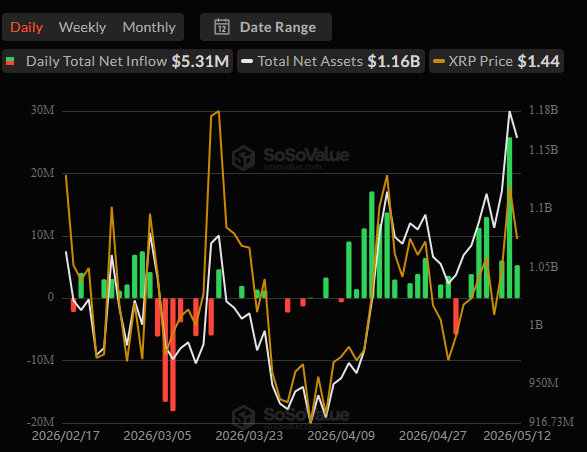

US spot XRP ETFs recorded $25.8 million in net inflows on May 11, their largest daily intake since early January, SoSoValue data show.

This extends the four funds' positive performance this month, attracting more than $60 million in inflows. XRP-focused funds have registered total inflows of over $1.35 billion since their launch last year.

Those inflows give XRP a regulated channel at a time when exchange-based positioning remains conflicted. ETFs allow investors to gain exposure through brokerage accounts and adviser platforms without managing direct custody or trading on crypto exchanges.

That opens the asset to a wider pool of allocators than the offshore derivatives venues that have historically shaped much of XRP’s short-term price action.

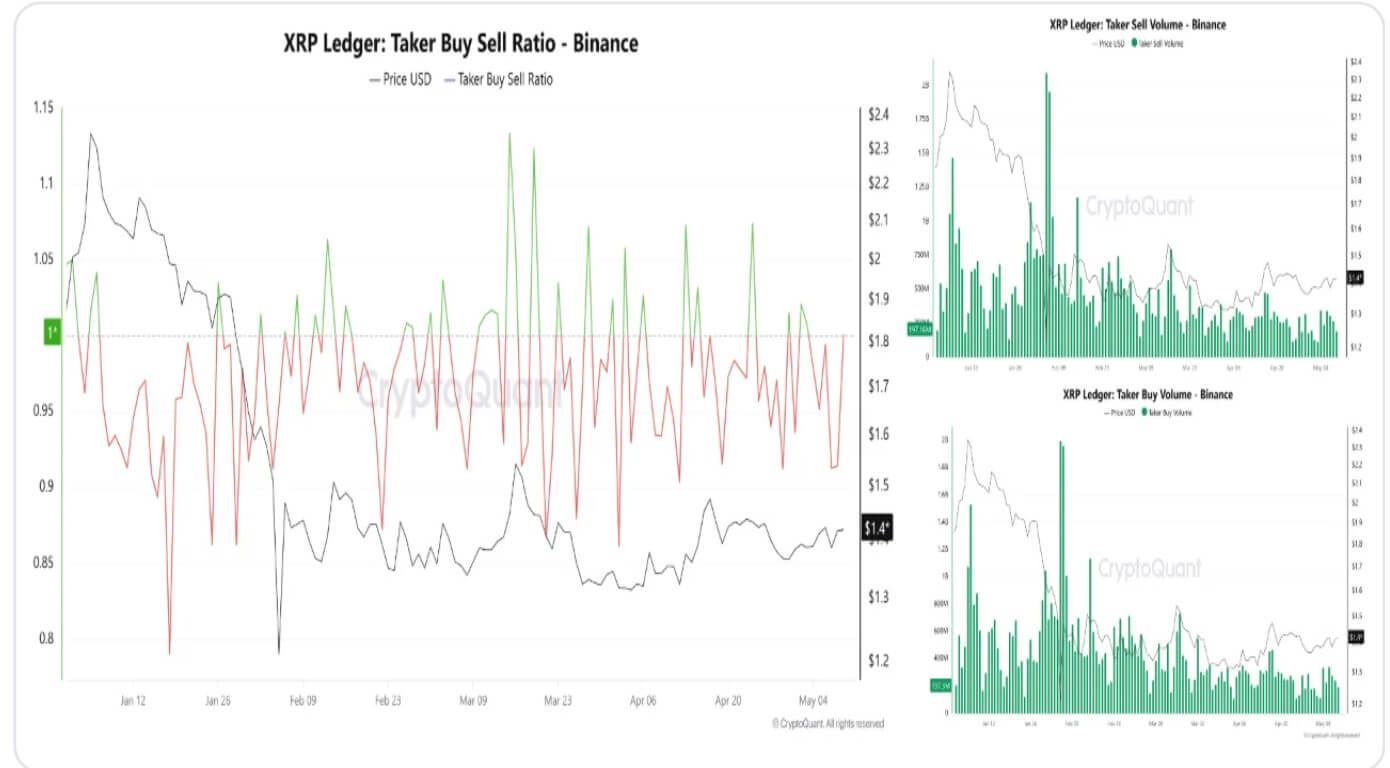

However, the mood in the derivatives market is different.

CryptoQuant data show that the Binance perpetual cumulative volume delta has fallen to about -$434 million, even as XRP has pushed higher. Open interest on Binance has climbed from about 207 million XRP on April 30 to nearly 232 million, showing leverage is returning after the latest reset.

The increase is not limited to Binance. On May 11, open interest rose by about $18 million on Binance, $10.4 million on OKX, and $8.5 million on Bybit, adding almost $36.9 million across the three exchanges.

Ordinarily, rising open interest can confirm a stronger trend when spot demand is also expanding.

However, XRP’s setup is more complicated. Spot estimated cumulative volume delta across centralized exchanges has slipped to about $575 million, even as the token trades higher.

That suggests the rally is not yet being driven by broad, clean spot accumulation.

Notably, XRP funding rates point to the same tension. XRP funding on Binance has carried a bearish bias for nearly three months, CryptoQuant data show, even as the token has gained roughly 27% over the same period.

This negative funding means shorts are paying longs to keep bearish exposure open.

Ripple adds Wall Street credit to the ecosystem

This bearish futures positioning is running headlong into a massive institutional buildout around Ripple.

On May 11, Ripple announced that it had secured a $200 million asset-backed debt facility from funds managed by Neuberger Specialty Finance, the dedicated asset-based investment team within Neuberger.

The firm said the facility would support Ripple Prime's continued growth amid increasing demand for “institutional-grade prime services and margin financing solutions.” The facility is backed by Ripple Prime’s institutional loan portfolio and structured for flexible drawdowns.

Noel Kimmel, president of Ripple Prime, said:

“Dependable access to financing and balance sheet strength are critical to institutional participants in today’s dynamic markets. This facility enables us to grow alongside our clients by delivering increased margin capacity, greater responsiveness, and improved capital efficiency.”

Ripple acquired Hidden Road last year and later rebranded it as Ripple Prime. The Brad Garlinghouse-led company revealed that the brokerage platform's revenue has tripled, driven by “sustained growth in client activity and demand for its prime services.”

Against this backdrop, this new credit facility fundamentally strengthens the market structure surrounding the Ripple ecosystem. Institutions require robust financing, custody, settlement certainty, and reliable counterparties before deploying capital at scale.

By embedding XRP and RLUSD within this broader institutional stack, Ripple is positioning itself directly against heavyweight service providers.

XRPL upgrades lead to increased activity on the ledger

Ripple’s corporate expansion is unfolding alongside a technical buildout of the XRP Ledger (XRPL) that is beginning to show up in network activity.

Over the past several months, the blockchain network developers have added features to meet the needs of regulated financial institutions.

The upgrades are designed to give banks, asset managers, and payment firms the controls they need to use public blockchain infrastructure without sacrificing compliance, privacy, settlement certainty, or auditability.

The new tools include Multi-Purpose Tokens (MPT), which allow issuers to embed compliance features into tokenized assets. Other upgrades, including Permissioned Domains and Permissioned DEX, are designed to create more controlled trading environments.

Additionally, the network recently implemented the Token Escrow feature, which extends escrow functionality beyond XRP to issued currencies, laying the foundation for on-chain delivery-versus-payment settlement.

Meanwhile, the ledger’s development roadmap also includes native lending markets and privacy-focused Smart Escrows.

Together, those changes point to a network being adapted for institutions that want the speed and transparency of shared blockchain rails, but still require permissioning, risk controls, and confidentiality.

Unsurprisingly, that institutional thesis is beginning to find support in ledger activity and institutional adoption.

Last week, Ripple piloted the cross-border redemption of a tokenized US Treasury fund alongside JPMorgan, Mastercard, and Ondo Finance on the XRPL.

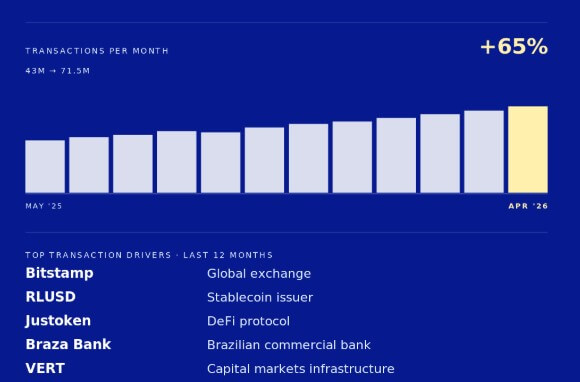

Evernorth, an XRP-focused treasury firm, argued that these institutional activities, alongside rising retail adoption, contributed to XRP transaction activity increasing 65% over the past 12 months to 71 million.

According to the firm, these activities were driven by Bitstamp, Ripple’s RLUSD stablecoin, Justoken, Braza Bank, and VERT.

It stated:

“Speculative volume on a blockchain comes in bursts. Real utility looks different. Steady. Programmatic. Tied to real businesses moving real money.”

What's next for the XRP price?

Considering the above, XRP’s near-term trajectory ultimately hinges on whether spot demand can translate this institutional progress into sustained buying pressure.

If ETF inflows persist, the spot cumulative volume delta improves, and the taker buy-sell ratio remains above parity, the heavily bearish derivatives positioning could backfire, triggering a wave of forced buying.

In that scenario, negative funding and climbing open interest would act as rocket fuel for an XRP rally toward the $1.50 to $1.60 range.

Conversely, if spot demand falters, that same leverage leaves XRP highly vulnerable to a sharp reversal.

A market propped up by rising open interest without underlying spot support can unwind violently, particularly when traders are deeply divided near a contested price range.

This dynamic makes the current market setup less about a single upcoming catalyst and more about a fundamental regime change.

Ultimately, XRP is transitioning from an asset dominated by offshore exchange speculation to one defined by ETFs, institutional credit, ledger utility, and tokenized-asset infrastructure.

The post Wall Street is buying XRP while Binance traders keep betting against it appeared first on CryptoSlate.

Prediction markets have been growing fast, from crypto price bets to election forecasting and sports outcomes. But there's a persistent problem most platforms don't address: users are essentially guessing.

They pick a side based on gut feeling, social media noise, or whatever narrative feels convincing in the moment. Poly Truth is attempting to solve that. Rather than just giving people a place to bet on outcomes, it positions itself as an intelligence layer sitting on top of prediction markets, one that tells you which side the data actually supports. You can explore the project directly on the $PTRUE Coin official website.

The project is currently in presale with its native $PTRUE token, and it's worth understanding what the system actually does before looking at the token economics.

What Is Poly Truth?

Poly Truth is a prediction market intelligence tool. That distinction matters: it's not a trading bot, not a prediction platform itself, and not an automated system that places positions on your behalf. The core idea is to give users data-backed probability analysis on active prediction events, whether those events involve sports results, political races, crypto price movements, or any other outcome-based market.

Think of it like having a research analyst who, instead of giving you a tip, walks you through the reasoning: here's what the data shows, here's the probability each outcome occurs, and here's why. Users still make their own decisions; Poly Truth just gives them more to work with.

How the Poly Truth System Works

The project explains its process through a three-part framework it calls its “characters.” It's a useful framing for understanding how data moves through the system.

The Runners are automated bots that continuously scrape data across the internet (news, odds movements, historical patterns, social sentiment), focused on whatever prediction events are currently active. They're the data collection layer, running in the background without user involvement.

The Starlet is the AI analyst component. Once the Runners pull in raw data, The Starlet cross-references sources, identifies patterns, and produces probability scores. This is where the intelligence layer actually sits: it's not simply aggregating data but interpreting it to determine which outcome has stronger statistical backing.

The Presenter is what users see. It delivers the final output: which events have meaningful data behind them, what the probability breakdown looks like, and the reasoning that led to those numbers.

The flow is clean: collect → analyze → present. Whether the AI analysis proves consistently accurate in live conditions is something that will only be tested over time, but the architecture is logically sound for what it's trying to do.

What Markets Does Poly Truth Cover?

The system is designed to work across several categories of prediction events:

- Sports: match outcomes, player performance, tournament results

- Politics: elections, policy decisions, geopolitical events

- Crypto: price movement predictions, project milestone outcomes

- General events: any outcome-based market with sufficient data to analyze

The breadth of coverage is worth noting. Most prediction market tools that incorporate AI tend to focus narrowly on one vertical. Poly Truth's multi-market approach means The Runners need to scrape and contextualize very different data types depending on the event category, which is a more complex engineering challenge but also a wider potential use case if executed well.

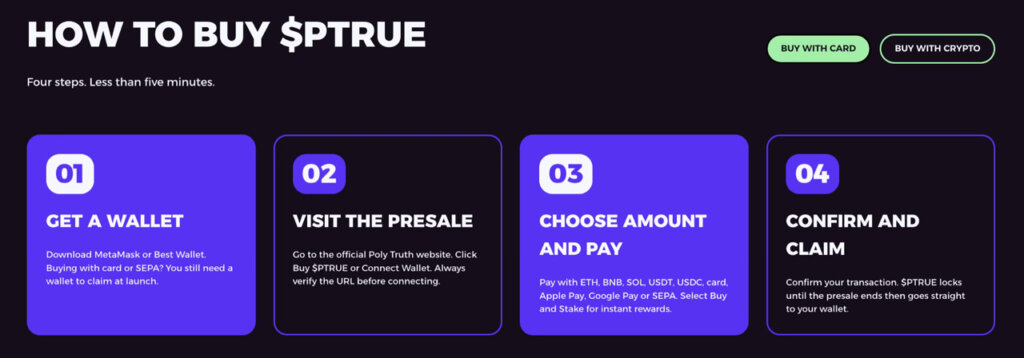

The $PTRUE Token: Key Details

PTRUE is the native token of the Poly Truth ecosystem, currently available in presale. Here's a breakdown of the core numbers:

| Detail | Figures |

|---|---|

| Total Supply | 11.5 billion tokens |

| Presale Price | $0.001190 |

| Blockchain | Ethereum |

| Staking APY | 4,452% |

| Payment Options | ETH, BNB, SOL, USDT, USDC, Card, SEPA |

Token Distribution:

- Presale: 40%

- Liquidity: 17%

- Development: 13%

- Team: 10%

- Staking: 10%

- Marketing: 8%

- Community/Airdrops: 2%

The 40% presale allocation is substantial, which means a significant portion of the total supply is being distributed early. The staking APY of 1,346% is an eye-catching figure — high staking yields are common in early-stage crypto projects as a mechanism to reduce circulating supply and reward early participants, but they are also inherently unsustainable at that rate long-term. Anyone considering staking should factor in how yield rates typically compress as a project matures and token supply dynamics shift.

The payment flexibility is genuinely broad for a presale; accepting ETH, BNB, SOL, stablecoins, card, and SEPA means the project is trying to reduce friction for buyers coming from different ecosystems. Full presale details are available on the PolyTruth platform.

How to Buy $PTRUE in the Presale

The process is straightforward:

- Visit the official Poly Truth website and connect a compatible wallet (MetaMask or similar)

- Select your preferred payment method — ETH, BNB, SOL, USDT, USDC, card, or SEPA

- Enter the amount you want to purchase

- Confirm the transaction

Since the contract is deployed on Ethereum, buyers using ETH will want to account for gas fees. Those paying with BNB or SOL will likely have lower transaction costs, though the mechanics of cross-chain purchases should be reviewed on the site before committing.

Who Is Poly Truth Actually For?

The most natural audience is people already active in prediction markets who want a research edge. If you're regularly using platforms like Polymarket or similar and making judgment calls based on partial information, a tool that systematically aggregates and scores probability data could be genuinely useful.

It's less directly relevant to passive crypto investors who aren't engaging with prediction markets at all. The token itself offers staking, but the utility case is tied to using the intelligence tool rather than simply holding.

The project sits in an interesting space; prediction markets have seen real growth in visibility and volume over the past few years, and AI-powered analysis layered on top of that trend is a logical product direction. Whether Poly Truth's implementation delivers on that concept is the question any prospective user or token buyer should be asking.

Final Thoughts

Poly Truth is a focused concept, not one trying to be everything, but one specifically targeting the information gap in prediction market participation. The three-part system (Runners, Starlet, Presenter) gives it a clear product identity, and the multi-market coverage broadens its potential reach beyond any single niche.

As with any presale-stage project, the gap between concept and working product is where real evaluation happens. The architecture makes sense on paper; live performance across diverse event categories will be the real test. Anyone wanting to dig into the details, review the smart contract, or participate in the presale can learn more on the Poly Truth coin website.

Disclaimer: This is a sponsored post. CryptoSlate does not endorse any of the projects mentioned in this article. Investors are encouraged to perform necessary due diligence.

The post How to Buy Poly Truth ($PTRUE): The AI Prediction Market Tool Explained appeared first on CryptoSlate.

The Senate Banking Committee’s crypto market structure bill is heading into CLARITY Act markup with more than 100 proposed amendments.

This is turning a long-delayed vote on the CLARITY Act into a test of whether a fragile stablecoin compromise can survive pressure from banks, Democrats, and crypto industry groups.

The final number of amendments has not been formally confirmed. However, the current markup amendment proposal puts it in the same range as the January effort, when 137 amendments were submitted before a planned committee vote was scrapped.

The size of the amendment pile underscores how unsettled the bill remains even after months of negotiations.

Banks force stablecoin rewards vote

The most consequential fight is over stablecoin rewards, the issue that helped stall earlier negotiations and now threatens to reopen the divide between crypto companies and the banking industry.

The Senate compromise would prohibit rewards on idle stablecoin holdings when those rewards resemble interest on bank deposits. It would still allow incentives tied to other stablecoin activity, such as payments or transactions.

That distinction was designed to keep stablecoins from becoming deposit substitutes while allowing firms to reward usage rather than passive balances.

Banks say the language does not go far enough. Their concern is that crypto exchanges and other intermediaries could structure rewards around stablecoin activity in ways that still pull deposits away from insured banks.

Banking groups have pushed senators to close what they view as a loophole and to prevent stablecoin issuers or affiliates from offering yield-like incentives that compete with bank accounts.

Sens. Jack Reed and Tina Smith reportedly filed an amendment to tighten that standard.

Their proposal would target rewards that are “substantially similar” to deposit interest, a formulation that could give regulators more room to block incentive programs that banks see as functionally equivalent to yield.

That amendment could become one of the clearest votes of the markup. Supporting it would move the bill closer to the banking industry’s position. Opposing it would preserve the Tillis-led compromise and signal that committee members are unwilling to use the market structure bill to further restrict stablecoin incentives.

The lobbying campaign around the provision has already intensified. Stand With Crypto, the Coinbase-backed advocacy group, said banking lobbyists sent 8,000 letters seeking to stop stablecoin rewards.

The group said its own advocates made 8,000 calls and sent 300,000 emails in recent months, and that supporters have contacted lawmakers almost 1.5 million times in favor of CLARITY.

On the other hand, traditional finance leaders are actively maintaining the pressure to ensure the amendment's success.

Lorrie Trogden, president and CEO of the Arkansas Bankers Association, recently issued a public call to action. On X, she urged banking industry members to make their voices heard ahead of the Thursday markup.

These efforts reflect an unusually visible outside campaign for a committee markup. They also show how a technical debate over reward language has become a proxy fight over whether banks or crypto platforms will control the next layer of dollar-based payments.

Warren pushes ethics and Fed access limits

Meanwhile, the stablecoin fight is not the only pressure point Democrats are bringing into the markup.

Crypto skeptic Sen. Elizabeth Warren has reportedly filed more than 40 amendments, the largest individual batch among committee members.

Her proposals target several parts of the bill, but one of the most significant would prevent the Federal Reserve from granting master accounts to crypto companies.

A Fed master account gives an eligible institution direct access to the central bank’s payment rails.

Crypto firms have long sought clearer paths into the banking system, while regulators and banks have warned that granting direct access to novel financial firms could create new supervisory and stability risks.

Warren’s amendment would put that fight directly into the CLARITY Act debate. If adopted, it would limit crypto companies' ability to use the market structure bill as a path to deeper integration with the Fed’s core payment infrastructure.

Notably, banking associations such as the Independent Community Bankers of America (ICBA) previously criticized the Federal Reserve Bank of Kansas City’s approval of a master account for the crypto exchange Kraken.

According to the group:

“Granting nonbank entities and crypto institutions access to the master accounts poses risks to the banking system.”

Meanwhile, Warren is also pressing the ethics argument that has become central to Democratic resistance.

The lawmaker has said that new crypto legislation should not move through the Banking Committee without stronger guardrails to address conflicts of interest involving President Donald Trump and his family’s crypto ventures.

That line of attack gives Democrats a broader political frame than just investor protection. It links the bill to concerns that public officials could benefit from policies that expand the digital asset market, especially if the legislation leaves gaps around affiliated projects, stablecoin activity or token holdings connected to political figures.

The ethics push complicates the Republican case for speed. Supporters argue the bill is needed to end regulatory uncertainty.

Warren and other skeptics argue that speed without additional safeguards could entrench conflicts before Congress has built a durable oversight framework.

DeFi and legal tender amendments widen the fight

Other Democratic amendments would expand the debate beyond stablecoins and ethics into the structure of decentralized finance and the legal status of crypto assets.

Sen. Mark Warner filed an amendment that would overhaul the bill’s decentralized finance provisions.

The latest CLARITY Act text attempts to define when a protocol is sufficiently decentralized and when an operator, platform, or intermediary should face bank-like compliance obligations.

That section is among the most technically sensitive parts of the bill because it determines whether some DeFi systems can operate outside traditional intermediary rules or must comply with reporting, monitoring, and anti-money laundering requirements.

Warner’s amendment signals that some Democrats remain uncomfortable with the bill’s treatment of DeFi.

Their concern is that broad exemptions for decentralized protocols could allow firms to avoid oversight by claiming that no central entity controls the system.

Crypto developers counter that rules built for custodial intermediaries cannot be applied cleanly to open-source protocols without forcing some projects offshore or shutting them down.

Reed also filed a separate amendment that would prohibit cryptocurrencies from being used as legal tender, including for tax payments.

That proposal would push against efforts by some crypto-friendly lawmakers to give Bitcoin or other digital assets a more formal role in public payments.

Together, the DeFi and legal tender amendments show that the impending markup will not be limited to one banking dispute.

Senators will also be asked to decide how much autonomy decentralized systems should have, how far crypto assets should be allowed to enter public finance, and whether the bill gives regulators sufficient authority to police risks across the market.

Crypto industry urges senators to hold the line

Despite all of these pressures, crypto industry groups are urging the committee to move the CLARITY Act forward without amendments that would weaken the compromise.

On X, the Blockchain Association and Crypto Council for Innovation have called the markup a defining moment for US leadership in financial technology.

Their argument is that the bill would replace fragmented enforcement-driven oversight with a statutory framework that lets companies build in the US under clearer rules.

Stand With Crypto has taken a more direct political approach, framing the bank-backed push against stablecoin rewards as an attempt to protect incumbents from competition.

The group’s campaign is aimed at showing senators that crypto supporters are organized enough to match the pressure coming from banks and trade associations.

For pro-crypto lawmakers, the challenge is holding together a coalition broad enough to get the bill out of committee while preserving language that can survive the Senate floor.

Republicans control the committee, but the broader bill will still need Democratic support to clear the broader Senate floor. That makes the markup both a policy negotiation and an early vote-counting exercise.

The post CLARITY Act faces 100+ amendments as bankers send 8,000 demand letters against stablecoin rewards appeared first on CryptoSlate.

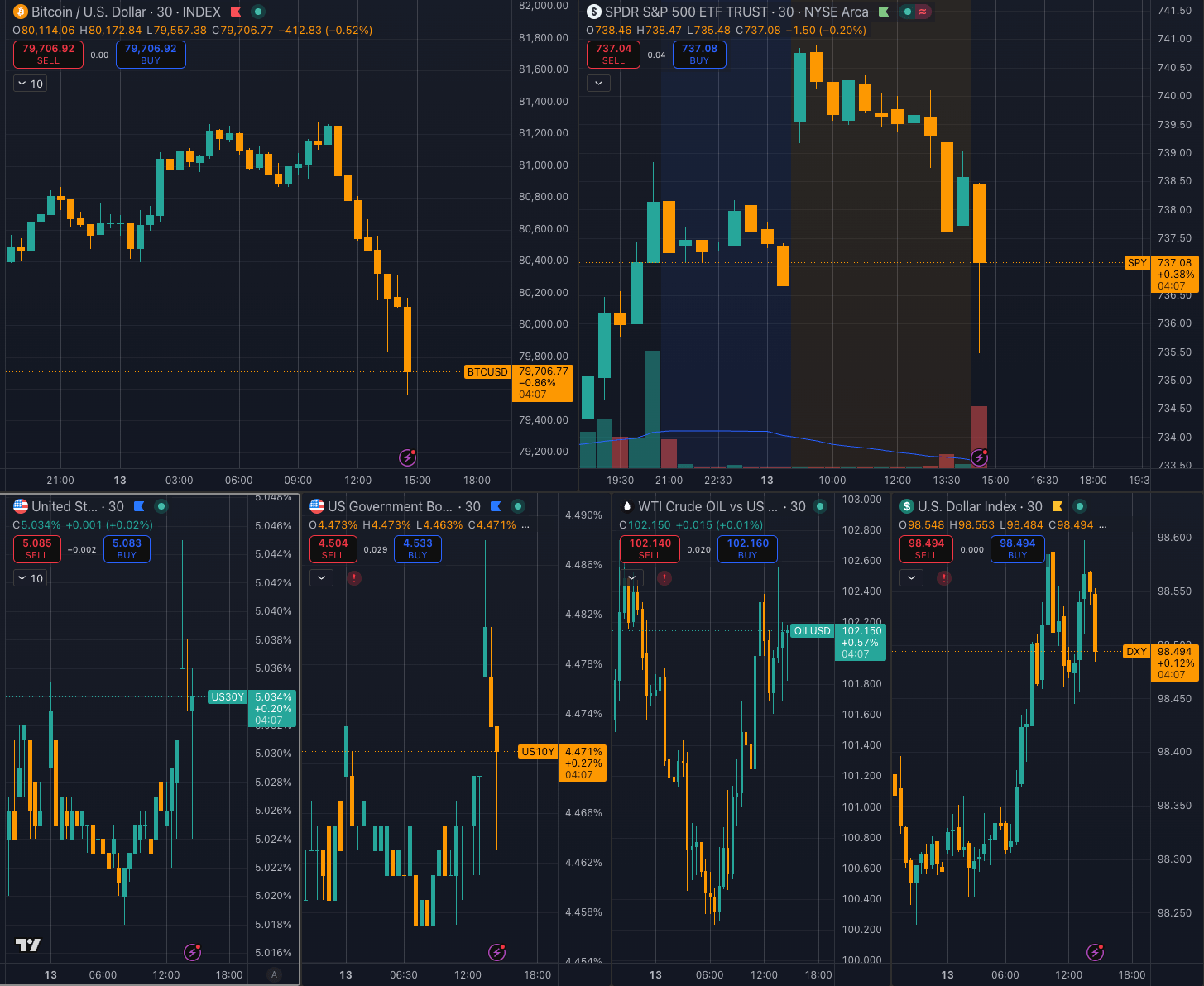

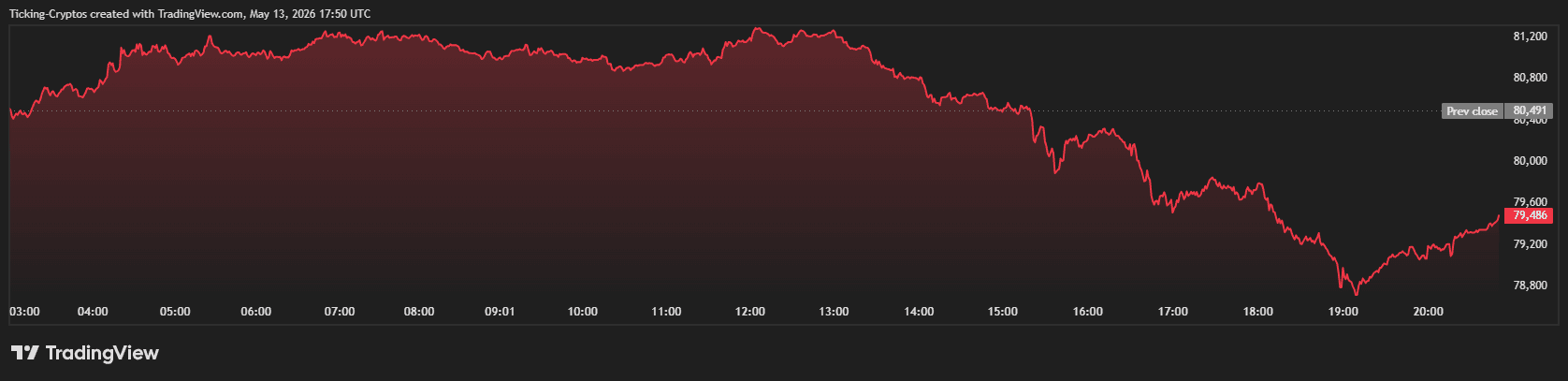

Bitcoin just fell below $80,000 as a hotter-than-expected US inflation print pushed crypto and equities lower.

BTC price slipped from the low $81,000 area into $79,706, with the session low marked near $79,557. The break turned $80,000 from a round-number reference into the first tactical line for intraday structure.

The move followed the April US Producer Price Index. Final demand PPI rose 1.4% month over month, far above the 0.5% consensus and the prior 0.7% reading.

The annual rate accelerated to 6.0% from 4.3%, above the 4.9% consensus. Core PPI rose 1.0% month over month against expectations for 0.3%, while core PPI year over year moved to 5.2% from 4.0%.

Trading Economics data also shows the narrower measure excluding food, energy, and trade services also firmed, rising 0.6% month over month and 4.4% year over year.

The PPI surprise followed yesterday’s CPI report, in which headline consumer inflation accelerated to 4.8% year over year from the prior 3.3% reading, above expectations of 4.5%.

That mix changes the market’s inflation map. A broad upside miss in producer prices pressures the Fed's path because it feeds directly into the cost pipeline and parts of the PCE calculation. It also reduces room for a benign rate reaction when energy is rising at the same time.

The cross-asset response clearly showed the repricing. SPY sold off from above $740 to $737, with a lower wick extending toward $735.48. Long-end rates moved higher, with the 30-year Treasury yield around 5.034% and the 10-year yield around 4.471%. The US Dollar Index held near 98.49, while WTI crude traded around $102.15.

Bitcoin’s immediate price issue is acceptance below $80,000. A quick reclaim would narrow the damage to an event-driven flush. Continued trade below that level leaves the $79,557 low exposed and makes every failed bounce into the prior support zone a test of seller control.

Markets attempted a modest stabilization after the initial post-PPI selloff, but the rebound remained fragile. Bitcoin briefly recovered from the $79,557 low, rising toward $79,700, while SPY bounced off the $735 area and Treasury yields pulled back slightly from session highs.

However, renewed buying in crude and a firm US dollar are still keeping broader macro pressure elevated, leaving cross-asset price action reactive rather than decisively recovered.

The next signal is simple: BTC needs to recover $80,000 while SPY stabilizes and yields stop rising. Until that sequence appears, the PPI shock remains the active driver, and Bitcoin’s intraday structure stays broken.

The post Bitcoin price just lost $80k because US PPI hit 6% matching 2022 levels, stoking inflation fears appeared first on CryptoSlate.

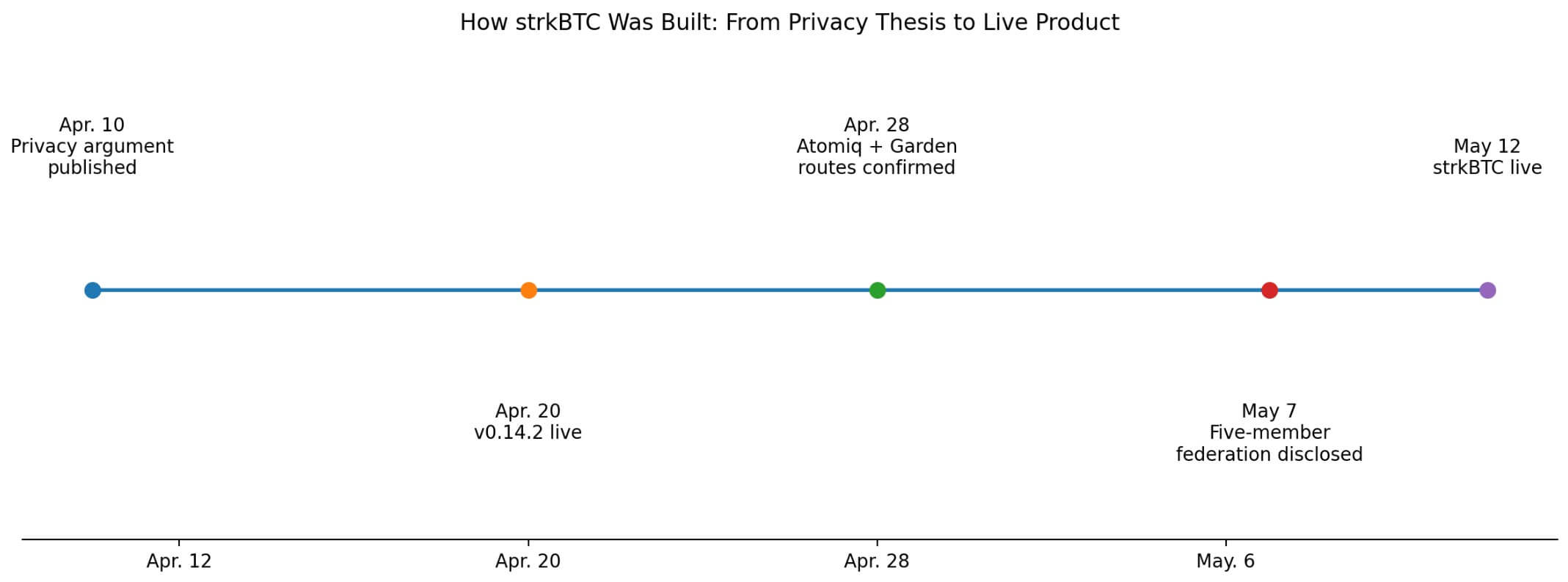

Starknet launched strkBTC on May 12, locking BTC on Bitcoin's base layer to back an ERC-20 token that brings shielded balances into a smart contract environment at scale.

The token runs in the public mode, where it behaves like any other wrapped Bitcoin asset, and shielded mode, where users can hide selected balances and transfers from outside observers.

Starknet routes viewing keys to an independent third-party auditor, preserving selective disclosure when regulators or counterparties require it.

A five-member federation handles BTC movement between Bitcoin and Starknet, with its roadmap pointing to greater trust minimization. Atomiq and Garden provide bridge routes from BTC and WBTC into the new token.

Starknet published its privacy argument on Apr. 10, framing on-chain visibility as incompatible with real financial use.

By Apr. 20, v0.14.2 was live, with native in-protocol proof verification and the infrastructure layer for encrypted balances. On Apr. 28, Starknet confirmed that Atomiq and Garden would wire BTC and WBTC liquidity directly into strkBTC.

On May 7, it disclosed the five-member federation, and seven days later, the product went live.

That build sequence reflects that the most active Bitcoin privacy development is happening outside the Bitcoin protocol, in environments designed for rapid iteration.

Bitcoin built transparency into its ledger by design. Every transaction is verifiable, every address is traceable, and the complete payment history of any wallet is visible to anyone with a block explorer.

For corporate treasury managers, large-value OTC desks, or any entity that prefers not to broadcast its full wallet balance to the market on every outbound payment, it creates a real operational problem.

The market response has been to build privacy into adjacent systems that can move faster than Bitcoin's base layer.

Private Bitcoin built elsewhere

Liquid, Blockstream's Bitcoin sidechain, has operated on this principle for years.

Users lock BTC into the peg and receive L-BTC on a network where Confidential Transactions hide both the asset type and amount from outside observers, making third-party inspection of amounts impossible.

Liquid's functionaries sign the blocks, federation infrastructure handles peg-outs, and users trade Bitcoin's security model for Liquid's in the process. Real privacy, available inside Liquid's federated architecture, with its own trust assumptions baked into every peg transaction.

WBTC paired with RAILGUN shows the same pattern in EVM territory. WBTC brings Bitcoin exposure to Ethereum, and RAILGUN shields ERC-20 assets in private 0zk balances, where users can send, swap, and interact with DeFi without those actions appearing on a public ledger.

RAILGUN requires assets to be in ERC-20 form before it can shield them. The privacy covers a Bitcoin-derived instrument that has already crossed into Ethereum, with WBTC's issuer and bridge touching the Bitcoin before RAILGUN can shield it.

Fedimint and Cashu build privacy through custody, as users deposit Bitcoin into a federated system and receive private payment claims in return.

Fedimint's federation guardians cannot trace individual members' balances or transaction histories, and Cashu uses Chaumian blind signatures, allowing users to spend privately against a mint without the mint seeing who holds what.

Both deliver genuine payment privacy, and both carry the same cost of making trust a third-party responsibility.

0xbow's Privacy Pools add a compliance layer to that same pattern, vetting deposits and providing users with zero-knowledge proofs that their funds are not connected to flagged addresses before admitting them into an association set.

That parallels Starknet's viewing-key architecture closely enough to show that selective disclosure is becoming a design standard across the sector.

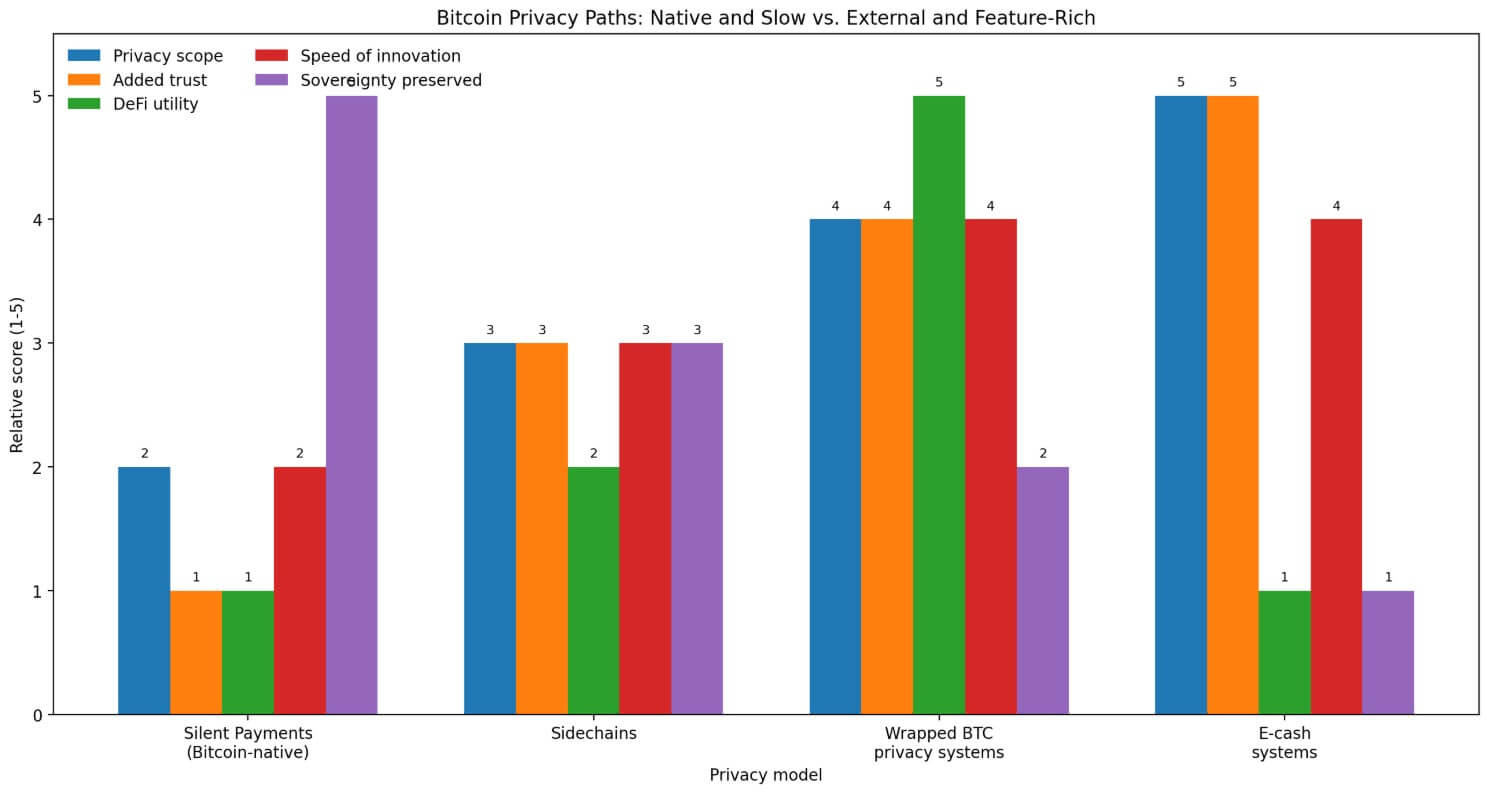

What each model trades for privacy

Every solution solves a distinct problem and adds a distinct assumption.

Liquid hides amounts and asset types through Confidential Transactions, but users have accepted federation governance and peg mechanics to access that privacy. strkBTC layers a five-member federation, a bridge, smart contracts, and a third-party auditor underneath its shielded mode.

RAILGUN's DeFi privacy reaches users only once WBTC's issuer and bridge have already touched the Bitcoin, and Fedimint's strong transactional privacy inside a community mint vanishes if the federation does.

Cashu is the most transparent about its terms, offering fast private payments at the explicit cost of mint custody. Across all of them, the privacy improvement is real and attached to bridge, federation, or mint assumptions.

| Model | Privacy gain | Main trust/risk layer | Best fit |

|---|---|---|---|

| Liquid / L-BTC | Hides asset type and amount through Confidential Transactions | Federation governance and peg mechanics | Users who want Bitcoin privacy inside a sidechain environment |

| strkBTC | Shielded balances and transfers in a smart-contract environment | Five-member federation, bridge, smart contracts, third-party auditor | BTCFi users and institutions seeking auditable privacy |

| WBTC + RAILGUN | Private balances, transfers, and DeFi interactions for Bitcoin-derived assets | WBTC issuer risk, bridge risk, smart-contract/privacy-layer risk | EVM DeFi users who want privacy after wrapping BTC |

| Fedimint | Strong transactional privacy inside a federated system | Federation/community custody risk | Community or local payment networks |

| Cashu | Fast, private Bitcoin-backed payments using blind signatures | Mint custody and redemption risk | Users prioritizing lightweight private payments |

| Silent Payments | Reusable payment address without onchain linkability | Minimal added trust, but narrower privacy scope | Native BTC holders who want receiver privacy without leaving Bitcoin |

Bitcoin-native privacy is advancing toward narrower goals on a longer timeline.

BIP 352, which addresses Silent Payments, lets receivers publish a single reusable off-chain address while each incoming payment lands at a unique on-chain address, removing the address-reuse linkability that makes wallet tracking straightforward.

Bitcoin Optech has documented steady progress in scanning performance and wallet integration, and the privacy gain adds almost no new trust. Users keep their BTC on the Bitcoin network, use no bridges or federations, and maintain Bitcoin's full base-layer security.

Silent Payments deliver receiver-level privacy, with each incoming payment reaching a unique on-chain address, making wallet clustering difficult and requiring no BTC movement.

The scope stops at the payment layer. Shielded portfolio balances, private DeFi execution, and concealed smart-contract interactions belong to wrapped and sidechain systems that are outpacing Bitcoin's own development.

That difference between Bitcoin-native privacy primitives and the shielded environments that wrapped and sidechain systems can build is where the market is currently filling in with external solutions.

The bull case for strkBTC-style architectures is that auditable privacy is exactly what institutions need.

Selective disclosure through viewing keys, association sets, and view-only wallets provides compliance officers with a workable audit trail without publicly exposing every transaction.

In this scenario, wallets make shielding a one-tap option, federations mature toward trust minimization as Starknet's roadmap describes, and Bitcoin privacy becomes a competitive feature in BTCFi.

That would attract treasury managers and market makers who need transaction privacy for counterparty reasons but cannot accept opacity for regulatory ones.

The bear case is that the trust stack proves too thick. A five-member federation, a bridge, a smart contract environment, and a viewing-key auditor each introduce trust layers absent from Bitcoin's base chain.

Users who understand those layers, or who watch one of them fail, may decide the sovereignty cost exceeds the privacy gain.

In that world, demand for private Bitcoin transactions splinters. Cashu and Fedimint serve communities comfortable with mint or federation custody, while wrapped asset DeFi privacy stalls short of institutional scale.

Bitcoin's base-layer privacy work continues in either scenario. Whether users wait for it or adopt a new trust layer to get something functional today is the decision now facing every BTC holder who needs financial privacy.

The post Bitcoin holders can now hide more of their activity, but only by trusting new middlemen appeared first on CryptoSlate.

Cryptoticker

The digital asset market has been hit by a wave of intense volatility, leaving traders and long-term holders in a state of shock. After a period of bullish consolidation where Bitcoin ($BTC) appeared to be building a base for a six-figure run, the tide has turned. Today, the leading cryptocurrency plummeted below the psychological $80,000 mark, dragging the rest of the market, including Ethereum ($ETH), down with it.

Bitcoin Price Crash Today

Bitcoin is currently trading at approximately $79,100, having officially lost the $80,000 support level that bulls defended for weeks. This 5% intraday drop has triggered over $300 million in liquidations, primarily affecting over-leveraged long positions. The sudden move has shifted market sentiment from "Greed" to "Fear" almost instantly.

Why did Bitcoin Price Crash?

The primary catalyst for today's market crash is the release of the U.S. Producer Price Index (PPI) for April 2026. The data, published this morning by the Bureau of Labor Statistics, revealed that wholesale inflation is surging at its fastest pace in years.

The PPI Shock by the Numbers

- Headline PPI: Increased by 1.4% month-over-month, vastly exceeding the 0.5% forecast.

- Year-over-Year PPI: Hit 6.0%, the highest level in 3.5 years (since late 2022).

- Core PPI (ex-food & energy): Jumped 1.0% MoM, signaling that inflation is broad-based and not just tied to volatile sectors.

A significant driver of this spike was a 15.6% surge in gasoline prices and a 7.8% rise in energy goods, largely due to the escalating geopolitical tensions in the Middle East affecting global supply chains.

Why High PPI Destroys the Crypto Narrative

Bitcoin is often touted as an "inflation hedge," but in practice, it behaves as a high-beta liquidity asset. When the US PPI comes in this high, it forces the Federal Reserve to maintain a hawkish stance.

The market is now pricing in a "higher-for-longer" interest rate environment. Higher rates make the US Dollar stronger and Treasury yields more attractive, which naturally sucks liquidity out of risk assets like Bitcoin and Ethereum.

Technical Analysis: Is $75k the Next Stop?

From a technical perspective, the Bitcoin kurs has broken below its 50-day Exponential Moving Average (EMA). This is a major bearish signal for swing traders.

- Crucial Resistance: For any hope of a recovery, BTC must reclaim $80,500 on the daily candle.

- Support Levels: The next major "liquidity pocket" is located at $75,000. If the selling pressure continues, analysts expect a rapid descent to this level as stop-losses are triggered.

- Ethereum Impact: ETH cours has also broken its support at $2,275, currently eyeing the $2,100 zone.

To manage the current volatility, many investors are moving their funds to safety. You can compare the most secure storage options in our hardware wallets comparison or look for exchanges with higher liquidity on our exchange comparison page.

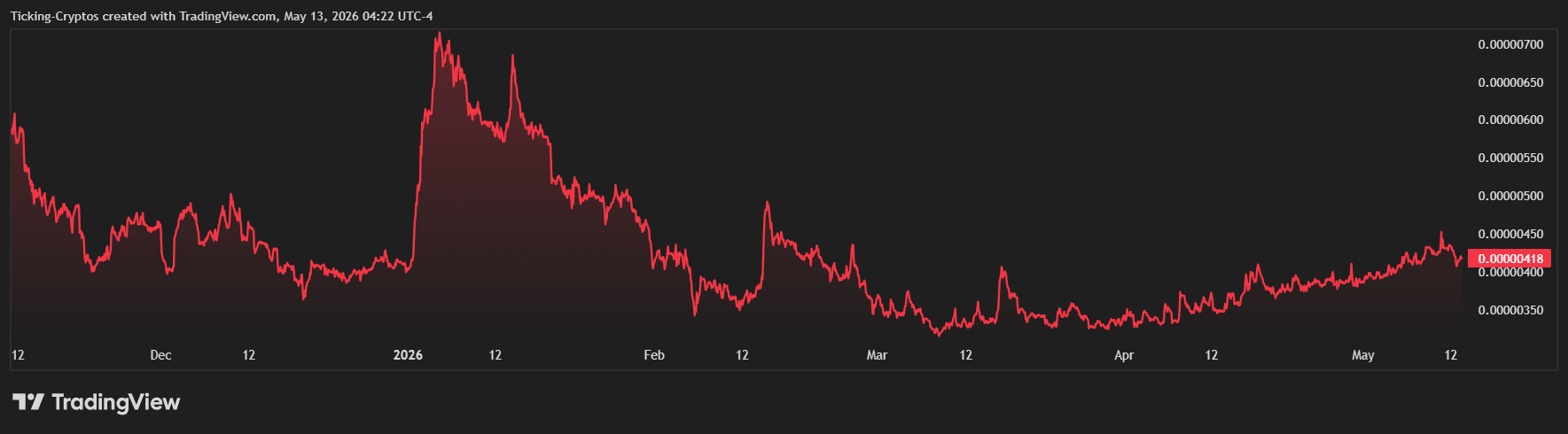

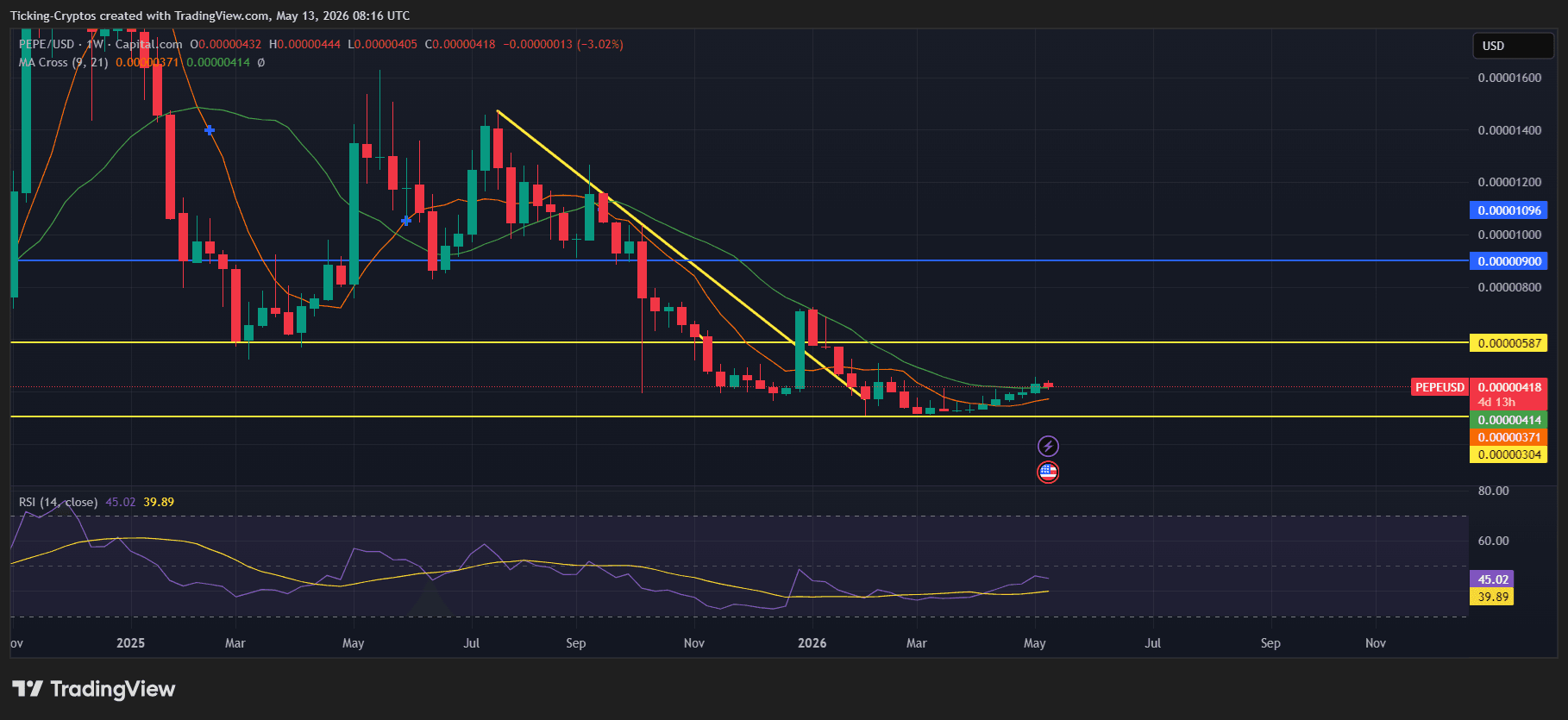

As of May 13, 2026, PEPE remains a central figure in the meme coin landscape. While many expected the "frog" to fade into obscurity, it has maintained a significant market presence. However, the 2026 market is vastly different from the speculative frenzy of years past. With $Bitcoin dominance rising to over 58.5%, the question for retail investors is simple: Is PEPE a hidden gem or a falling knife?

Is PEPE Worth Buying?

Currently trading at $0.00000418, PEPE is in a "make or break" consolidation phase.

- The Bull Case: If PEPE breaks the current descending resistance, it could target $0.00000580 in the short term.

- The Bear Case: Analysts warn that if support at $0.00000304 fails, PEPE could see a further 23% drop by mid-May.

For those seeking high-risk, high-reward plays, PEPE is still "worth it" as a speculative tool, but it is no longer the "easy money" it was during its inception.

PEPE as a High-Beta Asset

In 2026, professional traders treat PEPE as a High-Beta asset. This means PEPE tends to move in the same direction as Bitcoin but with much greater intensity. When the market is "Risk-On," PEPE outperforms; when the market consolidates—as it is doing now in May 2026—PEPE often bleeds value faster than major coins.

Performance Comparison: PEPE vs. The Giants

To determine if PEPE is worth buying, we must look at how it stacks up against the "Serious" assets in May 2026.

| Asset | Price (May 13, 2026) | Market Outlook | Risk Level |

|---|---|---|---|

| Bitcoin (BTC) | $81,016 | Consolidating (Dominance up) | Low |

| Ethereum (ETH) | $2,301 | Bearish Momentum | Medium |

| XRP | $1.46 | Neutral / Regulatory Stability | Medium |

| PEPE | $0.00000418 | Neutral / Speculative | High |

PEPE vs. Bitcoin (BTC)

Bitcoin is currently the preferred choice for institutional capital, with funds flowing back into BTC as altcoins struggle. PEPE is only a superior buy if you anticipate a massive retail surge that lowers Bitcoin's dominance.

PEPE vs. XRP

XRP has found a floor at $1.40, backed by its utility in cross-border payments. PEPE lacks this fundamental "floor," making it more susceptible to total retracements if community interest dips.

PEPE Price Analysis: Key Levels for PEPE Coin

The weekly chart shows a tightening wedge. The RSI is at 45.02, which is firmly in "no man's land."

Key Support and Resistance

- Resistance ($0.00000479 - $0.00000592): PEPE has failed to break this level four times in 2026. A daily close above this is the primary "Buy" signal for trend followers.

- Support ($0.00000304): This is the ultimate "safety net." According to recent crypto news, a breach here would likely invalidate the 2026 bull thesis.

2026 Market Catalysts

- Other Frogs Threat: New competitors are siphoning liquidity from the original PEPE community, posing a significant threat to PEPE's "meme-king" status.

- Institutional Moves: While JPMorgan is launching tokenized funds on Ethereum, meme coins like PEPE rely entirely on social media virality and potential "Spot Meme ETF" rumors.

IS PEPE Coin Worth Buying in 2026?

PEPE is worth buying in 2026 only if you are using "play money." It remains a powerful tool for catching volatility, but it is underperforming compared to the stability of Bitcoin.

JPMorgan Chase intensified its foray into the decentralized finance (DeFi) ecosystem by filing for a new tokenized money-market fund on the Ethereum blockchain. This move, identified through recent SEC filings, underscores a major shift in how "Global Systemically Important Banks" (GSIBs) view public blockchain infrastructure not just as an experiment, but as a primary settlement layer for institutional liquidity.

JPMorgan’s Ethereum Strategy

The bank’s latest vehicle, the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX), follows the successful late-2025 launch of its first public-chain fund, MONY (My OnChain Net Yield Fund). Unlike early permissioned experiments, these funds leverage the public Ethereum network, allowing for greater interoperability with the broader digital asset ecosystem.

Tokenized Money Market Funds

A tokenized money-market fund is a traditional financial product—typically investing in short-term U.S. Treasury bills and repurchase agreements—where ownership is represented by digital tokens (often ERC-20 on Ethereum).

- Yield on-chain: Investors earn dividends that accrue daily and are distributed as additional tokens.

- 24/7 Liquidity: Unlike traditional banking hours, these tokens can be transferred or redeemed near-instantaneously.

- Programmability: The fund’s "shares" can be integrated into smart contracts to serve as collateral.

Bridging Traditional Finance and Stablecoins

The timing of this launch is strategic. With the implementation of the GENIUS Act (the 2025 U.S. stablecoin legislation), stablecoin issuers are now required to hold high-quality liquid assets as reserves. JPMorgan is positioning JLTXX specifically to satisfy these legal requirements, effectively turning Ethereum into a bridge between the $240 billion stablecoin market and U.S. Treasury yields.

Institutional Competition: JPMorgan vs. BlackRock

JPMorgan is moving into a space currently dominated by BlackRock’s BUIDL fund, which recently surpassed $2.5 billion in Assets Under Management (AUM). While BlackRock has a head start, JPMorgan’s deep integration with corporate treasury desks through its Morgan Money platform gives it a unique distribution advantage.

| Feature | JPMorgan JLTXX | BlackRock BUIDL |

|---|---|---|

| Blockchain | Ethereum | Multi-chain (ETH, Arbitrum, etc.) |

| Platform | Kinexys Digital Assets | Securitize |

| Target Audience | Institutions / Stablecoin Issuers | Accredited Institutional Investors |

| Primary Assets | U.S. Treasuries / Repo | U.S. Treasuries / Cash |

Services and Utility on Ethereum

The launch of JLTXX on Ethereum entails several key services that were previously manual or siloed within internal bank ledgers:

- Atomic Settlement: Subscriptions and redemptions can happen in real-time using stablecoins or tokenized deposits, eliminating the T+1 or T+2 settlement lag.

- Collateral Mobility: Through JPMorgan’s Tokenized Collateral Network (TCN), these fund tokens can be used as collateral for derivatives or repo trades without moving the underlying assets.

- Transparent Registry: While identity is verified off-chain to meet KYC/AML standards, the record of ownership exists on a transparent, immutable ledger, reducing audit friction.

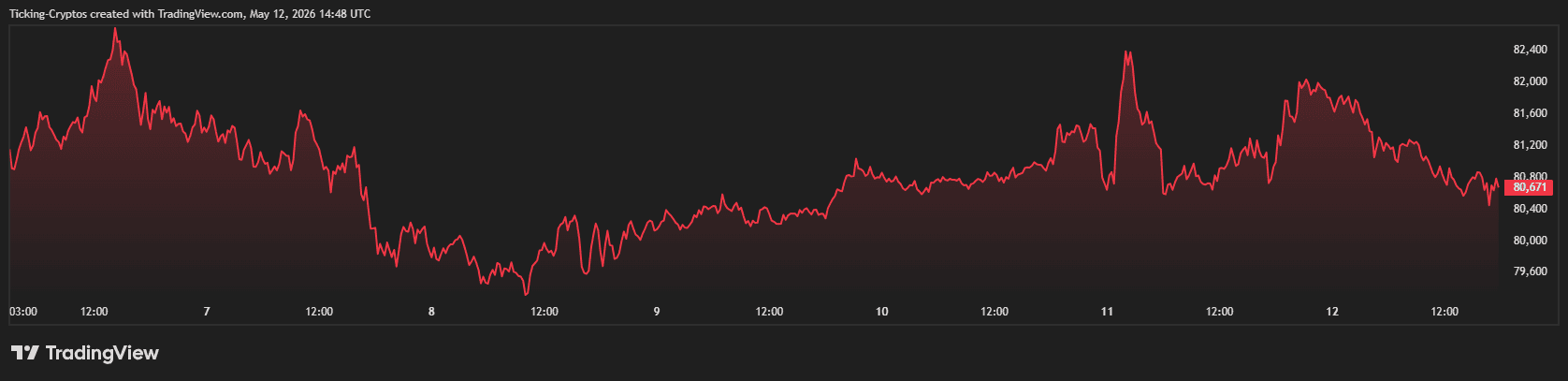

Bitcoin (BTC) continues to oscillate above the critical $80,000 psychological barrier, supported by a historic six-week streak of ETF inflows. Meanwhile, XRP has emerged as a top performer, outshining both Bitcoin and Ethereum (ETH) in recent trading sessions.

Market Snapshot: Bitcoin and XRP Performance

Investors are currently witnessing a Divergence in momentum across the board. While Bitcoin faces slight selling pressure near its local highs, Ripple's XRP has captured the market's attention with a significant breakout.

1. Bitcoin (BTC) Price Stability

As of May 12, 2026, Bitcoin is trading at approximately $80,750, down slightly by 0.20% over the last 24 hours. The asset has established a firm trading range between $80,400 and $82,100. This consolidation is widely viewed as healthy by analysts, especially following the massive surge in late April.

2. XRP Leads the Altcoin Charge

The most notable move comes from XRP, which successfully breached the $1.45 resistance level on high trading volume. Although sellers stepped in near the $1.50 mark, XRP's ability to outpace Ethereum and Bitcoin suggests a shifting appetite toward high-utility altcoins.

Institutional Era: The ETF Inflow Phenomenon

A major catalyst for the current price floor is the relentless demand from U.S. spot Bitcoin ETFs. According to recent, these funds have recorded their longest inflow streak since 2025.

- Six-Week Inflow Streak: ETFs have attracted over $3.4 billion since early April.

- AUM Records: Total Assets Under Management (AUM) for Bitcoin ETFs reached $109 billion this week, the highest level recorded in 2026.

- Supply Shock: ETFs are currently absorbing between 4,500 and 5,000 BTC daily, while only 450 BTC are mined per day—a 10:1 demand-to-supply ratio.

This "institutional era" of crypto investing is fundamentally different from previous retail-driven cycles. Wall Street wholesalers are now acting as a stabilizing force, preventing deep drawdowns even when market sentiment wavers.

What’s Next for Crypto in May 2026?

The current market structure suggests that while Bitcoin provides the foundation, the real "alpha" is currently found in selective altcoins like $XRP and $Solana. Investors are no longer buying the entire market; instead, they are rewarding projects with clear regulatory standing and technical strength. As we look toward the second half of May, the sustainability of the $80,000 level for Bitcoin will be the ultimate litmus test for the next leg toward $100,000.

The US Senate Banking Committee has officially released an expanded 309-page draft of the Digital Asset Market Clarity Act, commonly referred to as the Clarity Act. This updated version, which grew from a 278-page draft seen in January, marks a significant step forward in establishing a federal regulatory framework for digital assets. The bill arrives at a critical juncture as the industry seeks to move beyond "regulation by enforcement" and toward statutory certainty.

Jurisdictional Split: SEC vs. CFTC Authority

Investors and industry participants asking whether the new draft changes the core jurisdictional split can rest assured: the fundamental division of labor remains. The Securities and Exchange Commission (SEC) is slated to oversee most initial token sales, while the Commodity Futures Trading Commission (CFTC) will govern the spot markets and trading of tokens once they are deemed sufficiently decentralized or "mature."

What is the "Clarity" in the Act

The Clarity Act is designed to be the "ultimate rulebook" for the US digital asset market. It seeks to define three main categories:

- Digital Commodities: Under CFTC jurisdiction.

- Digital Asset Securities: Under SEC jurisdiction.

- Payment Stablecoins: Governed by a combination of the Federal Reserve and state regulators.

By creating these legal buckets, the bill aims to eliminate the gray areas that have led to years of litigation between the SEC and major exchanges.

Expanded Investor Protections and Antifraud Measures

A major addition to the 309-page text is the strengthening of investor-protection language. The draft explicitly grants the SEC enhanced authority to pursue insider trading and antifraud cases involving specific crypto offerings. This move is seen as a compromise to win over skeptical lawmakers who argue that the crypto market remains a "Wild West" for retail investors.

The Stablecoin Yield Crackdown: No More "Bank-Style" Interest

One of the most contentious sections of the bill focuses on stablecoins. The draft aims to prevent crypto platforms from operating like unregulated banks. Under the new rules:

- Passive Yield Prohibited: Platforms are barred from offering "bank-style" interest just for holding payment stablecoins (like USDC or USDT) in an account.

- Activity-Based Rewards Allowed: The bill leaves the door open for rewards tied to staking, liquidity provision, governance, or loyalty programs.

This distinction ensures that while simple "interest-bearing" accounts are restricted to licensed banks, the functional utility of DeFi and blockchain ecosystems remains intact.

Refined Focus on Tokenization and the "Build Now" Surprise

The section regarding tokenization has been narrowed. While earlier versions used broad "real-world assets" (RWA) terminology, the current draft focuses more precisely on tokenized securities. This adjustment provides clearer pathways for traditional financial institutions to bring equities and bonds on-chain.

In a move clearly designed to garner broader political support, the draft now incorporates the "Build Now Act." This housing-related legislation has no direct connection to cryptocurrency but is a strategic "rider" intended to attract votes from senators focused on urban development and affordable housing.

What’s Next for the Clarity Act?

The Senate Banking Committee is expected to move toward a formal markup session soon. For the latest updates on how these regulations might affect specific assets, you can monitor the $Bitcoin price and other major tokens on our live tickers.

Decrypt

Metaplanet CEO Simon Gerovich acknowledged that preferred shares unveiled in November have yet to be issued.

The Economic Secretary to the Treasury highlighted an upcoming consultation on payments encompassing digital assets and AI agents.

Peter Jackson says Hollywood’s fears around AI could hurt recognition for performance-capture acting, as debates about how the technology will reshape the movie industry grow.

As digital assets make inroads into the mainstream, crypto lender Figure is helping to turn them into viable collateral for credit.

Charles Schwab started allowing select users to trade Bitcoin and Ethereum directly alongside their other investments.

U.Today - IT, AI and Fintech Daily News for You Today

Galaxy Digital founder Mike Novogratz is sounding the alarm for his own party, urging Democrats to "seize the center of the ring" by immediately passing the CLARITY Act.

Dogecoin maintains positive futures activity while other top cryptocurrencies flip negative in their open interest.

Legendary trader warns Bitcoin hasn't bottomed, predicting a bear channel drop as surging 6% US PPI inflation shatters market optimism.

On-chain data from CryptoQuant reveals the largest corporate XRP treasury is facing a $389 million unrealized loss after buying near the market top.

Metaplanet CEO reveals company’s plans to expand its Bitcoin treasury by introducing a Bitcoin-backed product that could become Japan’s first-ever perpetual preferred shares.

Blockonomi

TLDR

- Transit Finance lost $1.8 million in DAI after attackers exploited the cross-chain swap protocol.

- Blockchain security firm PeckShield traced the stolen funds to a single Ethereum wallet.

- The exploit adds to more than $600 million in DeFi losses recorded in April alone.

- Kelp DAO and Drift Protocol accounted for most of April’s hacking losses.

- TRM Labs estimates that Lazarus Group represents about 76% of crypto hack losses in 2026 through April.

Transit Finance, a cross-chain swap aggregator, has suffered a $1.8 million exploit involving DAI stablecoins. Blockchain security firm PeckShield flagged the incident on Wednesday and traced the funds to one Ethereum address. The breach adds to a wave of DeFi attacks that have pushed 2026 losses toward $2.3 billion.

Transit Finance Breach Exposes $1.8 Million in DAI

PeckShield reported that attackers drained about $1.8 million in DAI from Transit Finance. The firm said it identified a single Ethereum wallet holding the stolen assets. It shared the alert publicly and tracked the movement on-chain.

Transit Finance operates as a cross-chain swap aggregator across more than a dozen networks. The platform routes trades between blockchains to offer pricing efficiency and execution speed. However, its interconnected design increases exposure to multiple attack surfaces.

PeckShield did not disclose the exact technical vector used in the exploit. However, it confirmed the loss amount and wallet address linked to the funds. Transit Finance has not released a detailed public statement at the time of reporting.

The exploit follows a series of high-value breaches across decentralized finance platforms. April alone recorded more than $600 million in losses across various protocols. Two major cases accounted for most of that figure.

DeFi Losses Surge as Transit Finance Joins April Breach List

Kelp DAO lost $293 million on April 19 after attackers drained its liquid restaking contracts. Drift Protocol lost $280 million on April 1 in a separate exploit affecting its Solana-based exchange. Together, those two attacks drove April’s total losses.

Security researchers now project full-year 2026 DeFi hack losses could reach $2.3 billion. TRM Labs reported that North Korea-linked Lazarus Group accounts for roughly 76% of crypto hack losses through April 2026. The firm based its estimate on blockchain tracing and forensic analysis.

Cross-chain protocols remain frequent targets because they bridge assets across networks. Transit Finance fits that category since it connects more than a dozen blockchain ecosystems. Attackers often exploit smart contract weaknesses or approval mechanisms in such systems.

Transit Finance faced a major breach in October 2022 that resulted in $28.9 million in losses. Attackers exploited improper input validation within its swap function. That flaw enabled unauthorized transfers from users who had granted token approvals.

Following that 2022 incident, the team recovered a portion of the stolen funds. The platform implemented security updates and reviewed its validation logic. However, the latest $1.8 million exploit shows attackers continue to target the protocol.

PeckShield continues to monitor the Ethereum address holding the stolen DAI. The firm has not reported any movement of funds since the initial alert. Transit Finance has yet to disclose further operational details as of Wednesday.

The post Transit Finance Hit by $1.8M DAI Exploit, PeckShield Says appeared first on Blockonomi.

Key Takeaways

- UNH reached a 52-week peak of $404.14 mid-week, climbing approximately 30% in the last 30 days

- First quarter revenues totaled $111.7 billion, representing a 2% annual increase, while adjusted EPS exceeded forecasts at $7.23