Cryptocurrency Posts

Crypto Briefing

The lawsuit could set a precedent for AI accountability, impacting regulatory approaches and investor confidence in AI technologies.

The post UK MP sues Elon Musk’s xAI over fake sexual images generated by Grok appeared first on Crypto Briefing.

Altman's response highlights the high-stakes gamble on AI's exponential growth, underscoring investor concerns about scalability and profitability.

The post OpenAI CEO Sam Altman responds to investor’s revenue concerns by offering to buy back shares appeared first on Crypto Briefing.

The conclusion of Operation Epic Fury may shift focus to diplomatic efforts, impacting regional stability and global oil markets.

The post Marco Rubio declares Iran war over, citing victory in Operation Epic Fury appeared first on Crypto Briefing.

Rising tensions and military actions could hinder peace efforts and increase regional instability, affecting future geopolitical dynamics.

The post Israeli airstrikes hit southern Lebanon amid rising tensions with Hezbollah appeared first on Crypto Briefing.

Binance's partnership with Alpaca could reshape global stock trading dynamics, but regulatory scrutiny and user risk awareness remain critical.

The post Binance discloses revenue-sharing deal with Alpaca for stock trading appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Kalshi Goes Live With America’s First Regulated Bitcoin Perpetual Futures

Kalshi announced on X today that bitcoin perpetual futures are now live for trading on its platform — one of the first times American investors can access regulated perps on domestic soil, the company claimed.

The Commodity Futures Trading Commission approved Kalshi’s BTCPERP contract on May 29, 2026, issuing an Order for Approval to KalshiEX, LLC under Commission Regulation 40.3. The contract references the spot price of bitcoin and carries no expiration date, making it a structural departure from every futures product the U.S. had previously authorized.

Kalshi CEO Tarek Mansour told CNBC’s Squawk on the Street that perpetuals are “the purest form of trading,” framing the launch as the company’s evolution from prediction market leader to a full-service derivatives exchange. “Onshore, safe, and regulated perps will improve capital allocation and risk management for countless American businesses,” Mansour said.

The scale of the market makes the opening significant. Offshore perpetual futures volume reached $92.9 trillion in 2025, outpacing spot crypto markets and representing a product class that had been entirely inaccessible to U.S. institutions.

That capital flowed to offshore venues like Binance and Hyperliquid, beyond the reach of American regulators. Reuters data puts 2025 perpetual futures volume at $61.7 trillion, up 29% from 2024.

Perpetual futures work through a funding rate mechanism. Rather than settling on a fixed date, a contract stays open indefinitely, and a funding rate — adjusted every eight hours — keeps the contract price tethered to the underlying spot market.

Kalshi makes its funding rate history visible in transaction history on its platform.

America as the crypto capital of the world

CFTC Chairman Michael Selig, appointed by President Trump, signaled the policy shift in March 2026, telling the Milken Institute that U.S.-listed perpetual futures were coming “in the next month or so.”

His statement alongside the Kalshi approval called it “a major step forward in delivering on President Trump’s goal of cementing America as the crypto capital of the world.”

Kalshi, valued at $22 billion following a May 2026 funding round, plans to expand perpetuals to more than a dozen cryptocurrencies pending further regulatory reviews. Agricultural commodities are excluded from the product slate.

The competition is moving fast. Kraken announced plans to list CFTC-regulated perps within 30 days of Kalshi’s approval, covering BTC and other crypto. Robinhood and Gemini have also signaled intent to enter the space. The CFTC said it will evaluate additional perpetual contracts case by case.

This post Kalshi Goes Live With America’s First Regulated Bitcoin Perpetual Futures first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Tether-Backed Adecoagro to Launch Sugarcane-Powered Bitcoin Mining in Brazil

Adecoagro (NYSE: AGRO), the South American agribusiness company with Tether as its majority shareholder, is set to begin Bitcoin mining operations in Brazil using electricity generated from sugarcane waste, with a target launch date of July 1, 2026, according to various local reports.

The project will be based in Ivinhema, in the state of Mato Grosso do Sul, and will start with 10 megawatts of capacity and approximately 1,280 Bitcoin mining machines.

Matheus Lechuga, the project manager at Adecoagro, confirmed the initiative during the “Roots of the Future – Technology and Innovation to Build Tomorrow” forum held on June 1, 2026.

The energy source is bagasse — the fibrous residue left after sugarcane stalks are crushed during sugar and ethanol production. Sugar mills routinely burn bagasse to generate steam and electricity for industrial operations.

In large-scale plants, this process produces surplus electricity beyond what the mill requires, creating an asset that can be redirected to power-intensive operations such as Bitcoin mining.

Adecoagro holds more than 230 megawatts of renewable electricity generation capacity across South America, giving the company an established energy platform before the mining rollout begins.

The 10-megawatt pilot represents a fraction of that installed base, positioning the launch as a commercial test of whether Bitcoin mining can scale as a complement to existing power sales.

Tether, the issuer of the USDT stablecoin and one of the most capitalized companies in the digital asset sector, acquired a controlling stake in Adecoagro, giving it exposure to physical commodities, agricultural land and renewable energy infrastructure. The Bitcoin mining project extends that strategy into digital asset production, with Adecoagro serving as the operational arm.

Surplus energy used for bitcoin mining

Back in September of last year, Adecoagro and Tether signed a memorandum of understanding to explore a partnership focused on Bitcoin mining powered by renewable energy in Brazil. The initiative aims to monetize surplus energy, improve grid stability and support decentralized networks by linking agricultural energy production with digital infrastructure.

Tether said it will contribute expertise in digital assets and sustainable mining, including its proprietary Mining OS, which will manage site operations and is expected to be open-sourced.

The pilot also reflects Adecoagro’s broader strategy to diversify its energy use and potentially add Bitcoin to its balance sheet, positioning it alongside traditional assets like farmland as a long-term store of value.

This post Tether-Backed Adecoagro to Launch Sugarcane-Powered Bitcoin Mining in Brazil first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

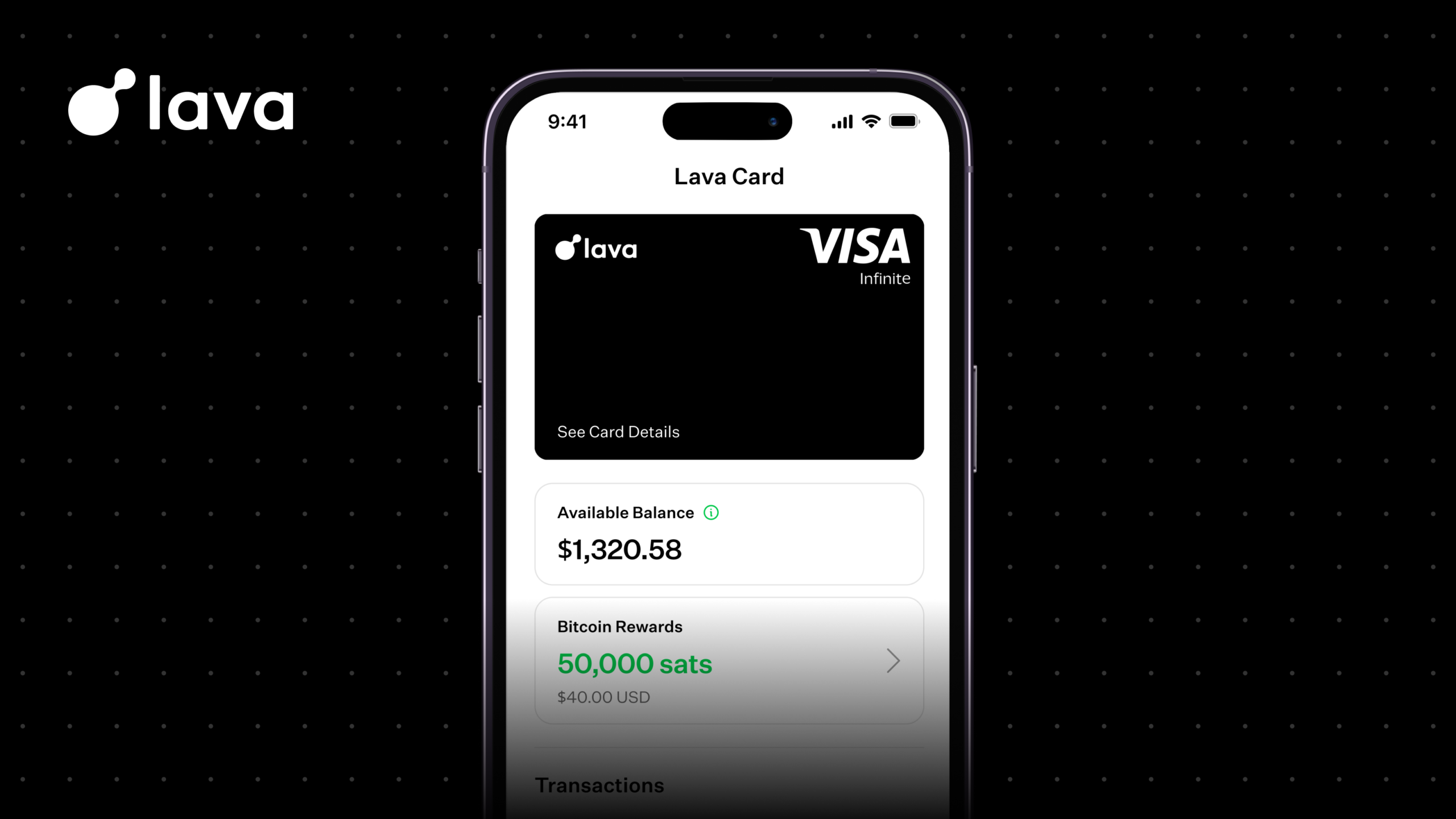

Lava Card Launches Secured Visa Credit Card That Pays Bitcoin Rewards on Every Purchase

Lava has launched its Lava Card, a secured Visa credit card that pays Bitcoin rewards on every transaction and accepts stablecoins as a funding source — a product the company says is built to bring stablecoin payments into the mainstream without asking users or merchants to change how they spend.

The card pays 3% back in Bitcoin for US-based users and 1% for international users on all purchases and 5% back through Lava’s growing network of Bitcoin-aligned merchants. To mark the launch, cardholders earn the elevated 5% rate on Amazon, Apple, and Netflix purchases, Lava told Bitcoin Magazine.

There is no annual fee, no foreign transaction fee, and no markup on Visa’s official exchange rate, making the card viable for both domestic and international use.

Lava is positioning the rewards structure as a deliberate break from the complexity that defines most card programs. Rather than accumulating points that require transfers, conversions, or fee math, users receive Bitcoin — a balance they can track and hold. The use case is pretty straightforward: spend dollars, earn Bitcoin, build savings.

The card is secured, meaning cardholders spend from a USD balance they fund themselves rather than borrowing. Users can move money onto the card via bank transfer, direct deposit, or by sending stablecoins such as USDC directly to Lava.

That stablecoin pathway is one of the product’s more ambitious bets. Stablecoin adoption has grown rapidly at the infrastructure level, but everyday spending has lagged — in part because swiping a card at checkout remains the default behavior for consumers and merchants alike.

Lava Card routes stablecoin balances through standard Visa rails, meaning neither side of the transaction has to adapt.

Users who hold Bitcoin can also fund their spending through Lava’s Bitcoin Line of Credit, borrowing against their BTC rather than liquidating it.

The merchant rewards network, which will offer additional Bitcoin back and exclusive savings to cardholders, is set to expand with partner announcements rolling out over the coming months.

The card is available to users in nearly every country and accepted anywhere Visa is.

Lava’s line of credit and fundraise

Back in November 2025, Lava announced it raised $200 million in a funding round combining venture and debt capital to expand its bitcoin-backed lending platform.

The company also launched a new Bitcoin Line of Credit (BLOC), designed to let users borrow against bitcoin without fixed terms or mandatory monthly payments.

The product offers interest rates starting at 5%, plus additional fees, with loans allowing up to 50% loan-to-value against posted bitcoin collateral.

This post Lava Card Launches Secured Visa Credit Card That Pays Bitcoin Rewards on Every Purchase first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Charles Schwab Launches 24/7 Bitcoin Futures Trading on thinkorswim

Charles Schwab has taken its most direct step yet into around-the-clock cryptocurrency access, announcing that select cryptocurrency futures — including Bitcoin — are now available to trade nearly 24 hours a day, seven days a week, across all thinkorswim platforms.

The move marks a milestone for the Westlake, Texas-based brokerage, which holds $12.61 trillion in total client assets and processed 10.3 million daily average trades in April 2026, the brokerage said.

Bitcoin futures, trading with a $5 multiplier, represent the flagship product in the new round-the-clock offering — one that Schwab calls its first 24/7 product in the firm’s history.

The timing carries weight. Bitcoin’s price has pulled back from an all-time high of $126,198.07 reached in October 2025 to approximately $66,000 as of June 1, 2026 — a decline of roughly 45% from peak levels.

Yesterday, Charles Schwab said it is targeting mid-2027 to launch spot crypto trading, custody, and transfers for registered investment advisors, integrating digital assets into its existing advisory infrastructure.

JUST IN: $12.6 trillion Charles Schwab launches 24/7 Bitcoin futures trading

— Bitcoin Magazine (@BitcoinMagazine) June 3, 2026pic.twitter.com/Yqsa1qbK1g

Schwab launches spot Bitcoin trading

It seems that the cooldown has done little to dampen institutional appetite. Schwab separately launched Schwab Crypto in April 2026, a spot trading service giving retail clients direct access to Bitcoin and crypto through a phased rollout — the firm’s first foray into direct digital asset ownership beyond ETFs and futures-linked products.

in April 2026, a spot trading service giving retail clients direct access to Bitcoin and crypto through a phased rollout — the firm’s first foray into direct digital asset ownership beyond ETFs and futures-linked products.

The 24/7 futures access through thinkorswim builds on that momentum. Unlike spot trading, futures contracts allow clients to gain price exposure to Bitcoin without holding the underlying asset, with both standard and micro-sized contracts available.

CME Micro Bitcoin futures trading with a $0.10 multiplier, lower the barrier for retail participants who want leveraged Bitcoin exposure without the capital requirements of full-sized contracts.

“As retail trading continues to advance, we’re committed to adding features and resources that expand our offering,” said James Kostulias, Managing Director and Head of Trading Services at Charles Schwab.

Beyond crypto, the platform update includes expanded fractional and notional trading across most U.S. stocks and ETFs — down to a $1 minimum — along with expected price range data for marginable securities on Schwab.com and dividend reinvestment through Schwab Mobile.

The fractional trading expansion lets clients place dollar-based orders directly from the standard trade ticket, removing the need for a separate experience.

This post Charles Schwab Launches 24/7 Bitcoin Futures Trading on thinkorswim first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

SEC Highlights Crypto in Its Strategic Plan for Fiscal Years 2026–2030

The U.S. Securities and Exchange Commission on June 2, 2026, published its Draft Strategic Plan for Fiscal Years 2026 through 2030, placing digital assets at the center of a broad regulatory reset under Chairman Paul S. Atkins.

The plan, which is open for public comment through July 2, 2026, charts a course that the agency says will return the SEC to its core three-part mission: protecting investors, maintaining fair and efficient markets, and facilitating capital formation.

Chairman Atkins described the release as “a new day at the SEC,” one aimed at unwinding what his administration views as regulatory overreach from prior years.

The plan is organized around three goals: renewing regulatory policy to support innovation and capital formation, shifting enforcement practices toward established legal violations rather than expansive agency action, and optimizing internal operations through technology and organizational reform.

Atkins said the Commission “will not stray” from its foundational mandate set by Congress in the Securities Exchange Act of 1934.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) June 3, 2026SEC highlights digital assets in its "Strategic Plan" for the next 5 years

"crypto asset technologies have the potential to revolutionize America’s financial infrastructure"pic.twitter.com/K7JVhzaHjl

Crypto gets an SEC shout out

Perhaps the most consequential section of the plan is its treatment of blockchain and cryptocurrency. The document states that “crypto asset technologies have the potential to revolutionize America’s financial infrastructure and deliver new optionality, efficiencies, cost reductions, transparency, and risk mitigation for the benefit of all Americans.”

The SEC frames this not as a caveat, but as a rationale for building a clearer, more coherent framework that gives innovators legal certainty while preserving investor protection.

Objective 1.1 of the plan calls for the SEC to provide “a firm regulatory foundation for digital assets and distributed ledger technologies through a rational, coherent, and principled approach.”

This includes clarifying the boundaries of securities law as they apply to digital assets, enabling compliant capital formation through tokenized offerings, and supporting what the document calls “onchain financial infrastructure.”

The plan also commits to resolving jurisdictional overlap between the SEC and the Commodity Futures Trading Commission — a long-standing point of friction for the crypto industry .

Beyond digital assets, the plan targets capital formation barriers for small businesses and early-stage companies. It calls for modernizing Regulation A, streamlining shelf registration, and reducing disclosure complexity so entrepreneurs can tap both public and private markets with fewer regulatory obstacles.

On enforcement, the SEC signals a shift away from what critics have called regulation-by-enforcement — particularly the approach taken toward crypto firms in recent years.

The new plan instructs staff to focus on “fraud and manipulation” rather than expanding regulatory reach through ad hoc actions, and states that success in enforcement should be measured by deterrence and market clarity, not by case volume or fine totals.

Tech overhaul on the horizon

The third goal of the plan addresses internal operations, with a focus on modernizing the SEC’s decades-old EDGAR filing system and rolling out artificial intelligence across agency functions. The document notes that AI and blockchain could “improve oversight, reduce costs, and unlock new efficiencies” inside the commission itself.

The agency oversees approximately $207 trillion in annual U.S. equity trading and holds roughly 19 terabytes of disclosure data on EDGAR — systems the plan acknowledges need meaningful upgrades.

This post SEC Highlights Crypto in Its Strategic Plan for Fiscal Years 2026–2030 first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

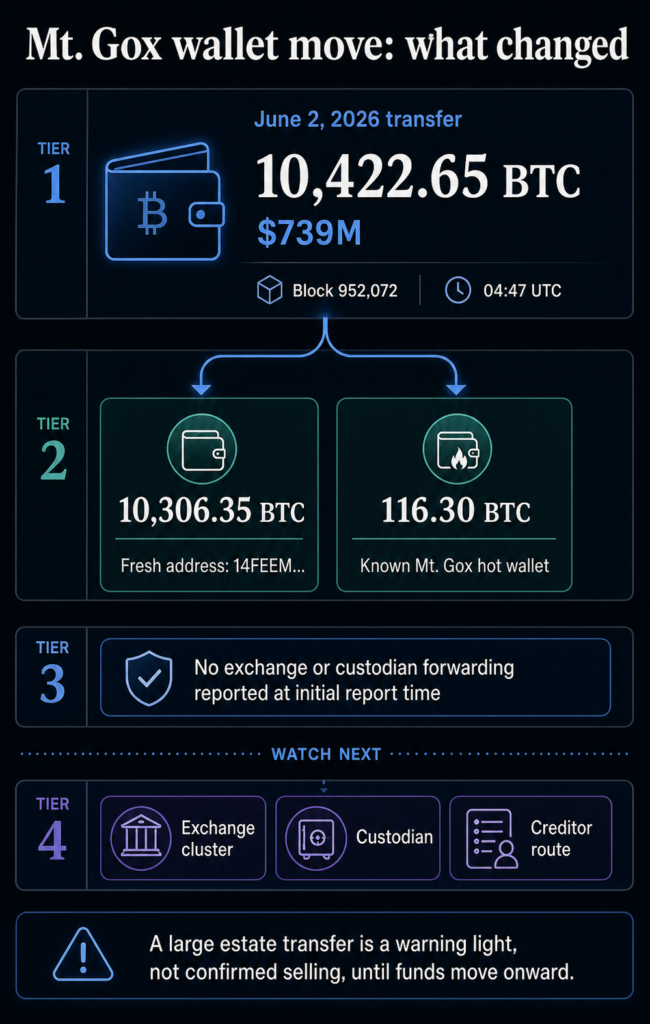

Mt. Gox moved more than $700 million worth of Bitcoin while the market was already under stress, giving traders a familiar reason to ask whether old bankruptcy coins are moving closer to new supply.

The estate-linked wallets moved 10,422 BTC on June 2, worth roughly $739 million at the time of the transfer. Most of the stack, 10,306 BTC, went to a fresh address beginning with 14FEEM, while 116 BTC moved to a known Mt. Gox hot wallet.

The transfer occurred in Bitcoin block 952,072 at around 04:47 UTC, months before the current repayment deadline of Oct. 31, 2026.

So, it seems that Mt. Gox is active again, while immediate sell pressure remains unconfirmed, as no onward movement to a custodian, exchange, liquidity provider, or creditor distribution venue was reported at the time of the initial report.

The transfer revived an old supply problem

Mt. Gox remains one of Bitcoin‘s longest-running market overhangs because the estate still controls a large BTC balance more than a decade after the exchange collapsed. The June 2 transfer carried weight because it reminded the market that a known pool of old coins can still move with little warning.

The remaining estate balance was reported at roughly 34,504 BTC after the move. The visible activity is split across multiple transfers rather than a single visible sell order, and direct exchange-bound flow remains unconfirmed.

Still, a balance of that size is enough to keep traders watching every large estate-linked movement for signs of distribution.

The official trustee process gives that concern a concrete calendar. In an Oct. 27, 2025 notice, the Mt. Gox Rehabilitation Trustee extended the deadline for several repayment categories from Oct. 31, 2025 to Oct. 31, 2026 with court permission.

The notice said many creditors still had not received repayments because some had not completed required procedures or because processing issues remained.

That language points to a drawn-out process rather than a single clean market event. It also explains why wallet movement can be meaningful before immediate selling is visible.

Coins may move for internal wallet management, repayment preparation, custody setup, or liquidity routing before any creditor receives BTC or any exchange sees flow.

| Signal | What it shows | What remains unconfirmed |

|---|---|---|

| 10,422.65 BTC moved on June 2 | Mt. Gox-linked wallets became active again with a large transfer | A confirmed market sale |

| 10,306.35 BTC went to a fresh 14FEEM address | Most coins shifted to a new destination | Whether the destination is an exchange, custodian, or creditor endpoint |

| 116.30 BTC went to a known hot wallet | A smaller slice moved through familiar estate infrastructure | Whether the larger stack is being sold immediately |

| Repayment deadline sits at Oct. 31, 2026 | The bankruptcy process remains active | Whether remaining BTC will be distributed in one batch or staggered flows |

The next signal is onward routing

The practical threshold is simple: the transfer becomes stronger evidence of sell pressure when the coins move from estate-linked wallets toward venues that can distribute, custody, or sell them.

That is why Arkham's Mt. Gox entity page carries more weight than the headline dollar value alone. On-chain labels, destination clustering, and counterparties can indicate whether the fresh address remains part of the estate's wallet structure or begins interacting with exchange and repayment infrastructure.

The distinction is practical. A large internal transfer can still shake sentiment because it changes market expectations for the timeline. But a wallet reorganization is different from coins arriving at a venue where they can be sold or handed to creditors.

The former is a warning light. The latter is closer to actual supply.

The June 2 routing, as reported at the initial deadline, sat on the warning-light side of that line. The coins had moved, the process was live, and the repayment deadline was visible.

Yet the key downstream signal was still absent: no confirmed move into a custodian or exchange had been shown in the initial reporting.

The market may care about the transfer even without proof of sale, especially during a weak trading window. It still needs proof of onward routing before treating the move as immediate supply hitting Bitcoin order books.

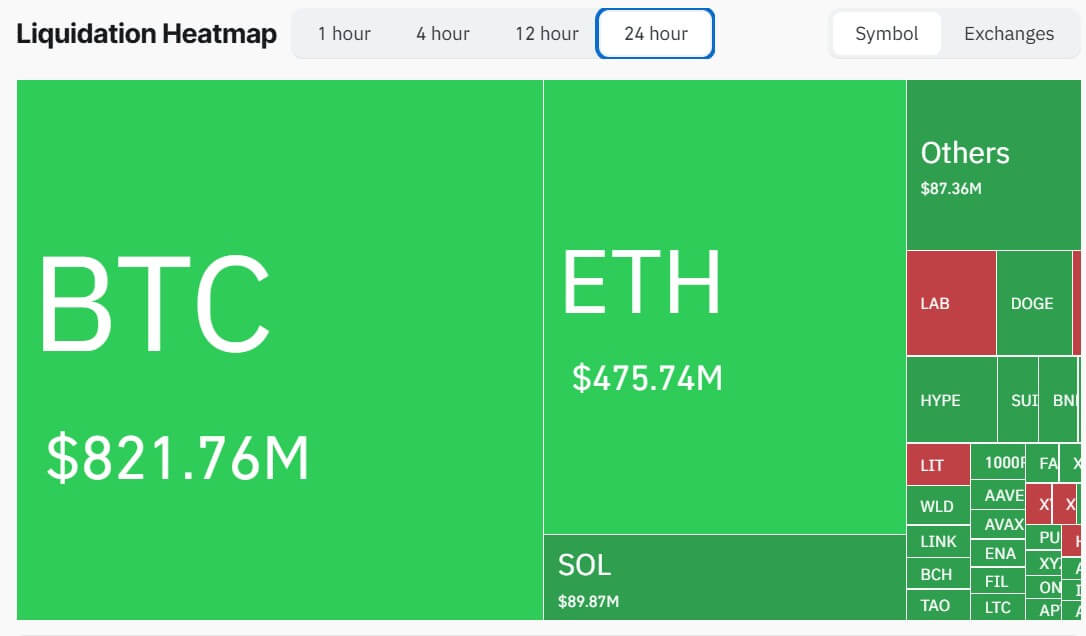

The timing made the movement feel larger. On June 2, Bitcoin fell more than 5% below $68,000, and nearly $400 million in leveraged positions were liquidated within an hour.

That backdrop carries weight because leveraged markets can turn a wallet alert into a sentiment catalyst.

The evidence supports timing, not causation. The Mt. Gox transfer occurred around 04:47 UTC, while the liquidation story describes same-day market pressure.

The cleaner conclusion is that Bitcoin was already vulnerable, and the Mt. Gox movement added another reason for traders to think about supply.

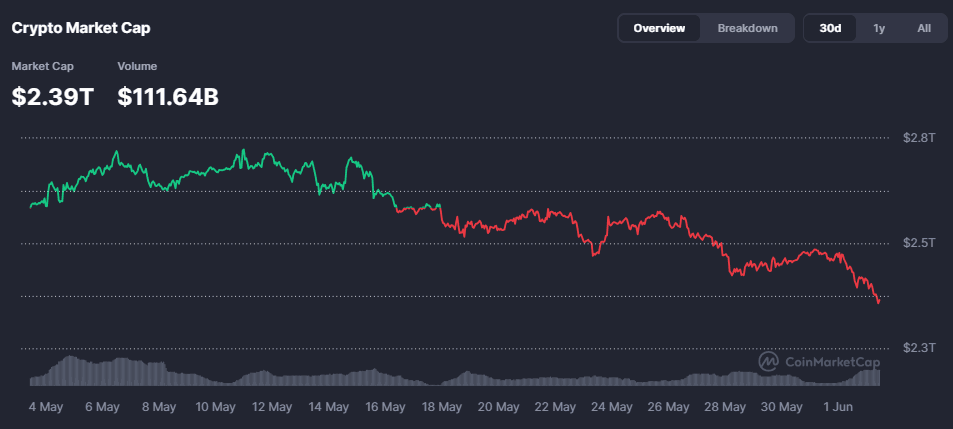

CryptoSlate market data on June 3 showed BTC trading at $66,737, down 3.76% over 24 hours, with $57.34 billion in 24-hour volume.

The broader CryptoSlate coin rankings showed a $2.3 trillion crypto market, $137 billion in 24-hour volume, and 57.9% Bitcoin dominance.

Those numbers cut in both directions. Bitcoin is deep enough that a staggered repayment process does not automatically overwhelm the market.

At the same time, a high-leverage selloff can make any large potential supply source feel more urgent than it would during calmer trading.

That puts the focus on whether a measurable path has opened from the estate to liquid supply. As of the initial reports, that path had not been shown.

Mt. Gox is now a process overhang

CryptoSlate's prior Mt. Gox coverage framed the 2026 repayment extension as a shift from a single-date shock to a recurring process overhang. That remains the best way to read the June 2 movement.

The deadline tells traders when the estate process is supposed to finish. The wallets tell traders whether that process is moving. The exchange, custodian, liquidity provider, or creditor endpoints indicate to traders whether the movement is shifting toward market supply.

Until those later signals appear, the most defensible answer is restrained. The June 2 transfer showed that a bankruptcy estate still holding tens of thousands of BTC is active again, even as Bitcoin is under pressure.

It also left the most important question about sell pressure unanswered.

That distinction is what keeps the move from becoming either complacency or panic. Mt. Gox has enough BTC left to remain a meaningful watch item, and the repayment process has a live deadline.

But the market signal to watch is not the first move into a fresh wallet. It is whether funds move from that wallet toward an exchange, custodian, liquidity provider, or repayment route.

The post Mt. Gox-linked wallets moved 10,422 BTC, worth roughly $739 million as BTC price slides appeared first on CryptoSlate.

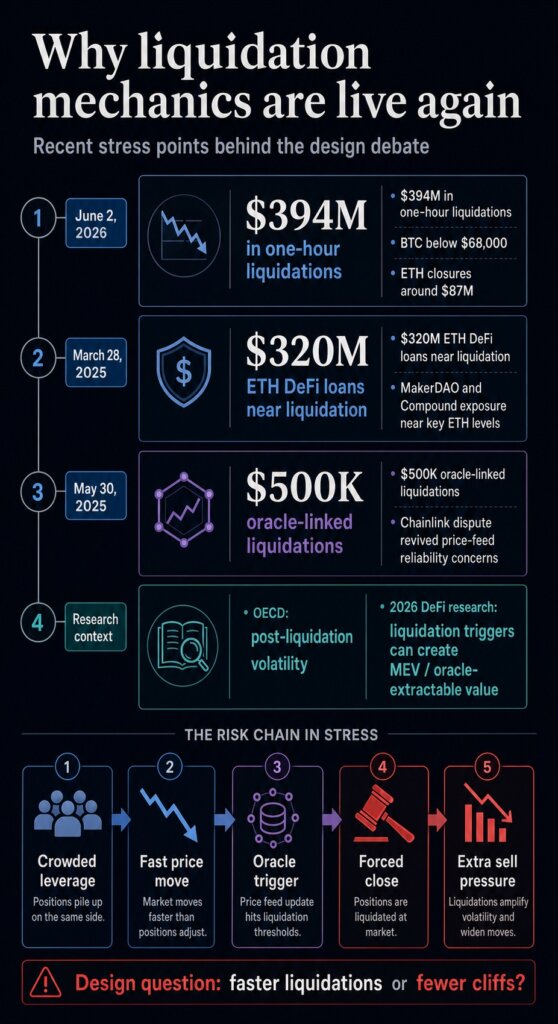

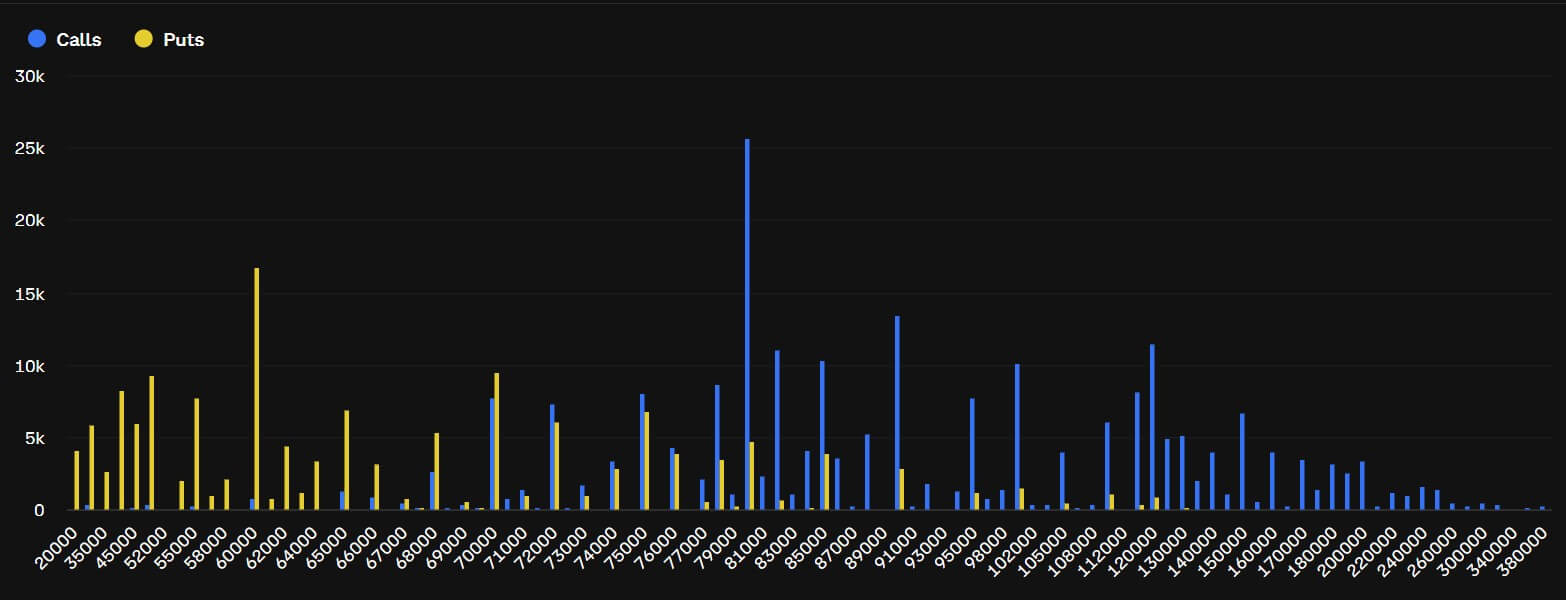

Vitalik Buterin is challenging one of DeFi's most familiar safety mechanisms: the automatic liquidation that closes a debt-backed position when collateral falls below the required backing for the loan.

In a June 1 Ethereum Research post, Buterin proposed building synthetic, index-tracking assets on top of options, with collateralized debt removed from the base design.

The idea would remove the hard liquidation trigger from the base design and replace it with a slower form of risk: the user's exposure drifts away from the target unless the position is rebalanced.

That distinction is important because the old mechanism is still showing up in market stress. Bitcoin‘s fall below $68,000 triggered about $394 million in one-hour liquidations on June 2, including roughly $87 million in ETH positions, as leveraged bets were force-closed across the market.

The flash crash came one day after Buterin's post and serves as a market reminder: when price moves hit crowded leverage, automatic closures can turn a drop into a wider market event.

The proposal is research-stage architecture: a design argument separate from any protocol launch, Ethereum roadmap commitment, or direct replacement for Aave, Maker, or existing stablecoins. It shifts the focus from collateral buffers and faster price feeds to a more fundamental design choice: whether instant liquidation should remain DeFi's central means of surviving a crash.

Why the safety switch can amplify stress

Most DeFi lending systems are built around the same basic problem. A user locks in collateral, borrows against it, and must keep the position above a required safety level.

In Aave's borrowing documentation, that level is expressed through a health factor. When it falls below 1, the position can be liquidated: a liquidator repays debt on the borrower's behalf and receives collateral plus a bonus.

That structure protects the protocol's solvency, but it also concentrates action at the worst possible moment. If ETH or another collateral asset falls fast enough, users do not choose when to sell. The system chooses for them.

Liquidators compete to close eligible positions, and the collateral can be pushed into markets already short on liquidity.

The record supports that concern. An OECD working paper on DeFi liquidations found a positive relationship between liquidation activity and post-liquidation price volatility across major decentralized exchange pools.

The paper also emphasized that liquidators rely on available liquidity during stress, which means the mechanism designed to restore balance can run into the same liquidity shortage as everyone else.

CryptoSlate has previously covered the operational version of that risk. A 2025 Chainlink-related oracle dispute led to more than $500,000 in liquidations on Euler Finance and revived questions about how protocols should interpret pricing data in illiquid markets.

Separately, a 2025 ETH decline put nearly $320 million in Ethereum-based DeFi loans within 20% of liquidation, with MakerDAO and Compound exposure concentrated near key price levels.

The common thread is the cliff. DeFi needs a way to handle undercollateralized positions, but the current method often waits until a number is breached and then requires immediate action.

That creates a crowded moment for borrowers, liquidators, oracle feeds, and liquidity providers simultaneously. It also gives sophisticated actors a clear trigger to watch, because the protocol rule announces when a position becomes profitable to close.

For users, the practical consequence is straightforward. A liquidation system can protect a lending pool while still giving the individual borrower the worst possible execution window.

The user may have intended to keep long-term ETH exposure, hedge a cash need, or wait out a sharp wick. Once the threshold is crossed, the system's priority becomes solvency, and the user's timing preference disappears.

How options turn a cliff into drift

Buterin's alternative starts by changing the primitive. A position that can become undercollateralized gives way to a split ETH claim: the proposal divides 1 ETH into two option-like assets, called P and N, tied to a price index, strike price, and maturity date.

At maturity, an oracle resolves the index value and determines how much of the ETH claim each side receives.

The key property is simple: P and N always add back up to 1 ETH. Because the system is dividing a fixed ETH claim between two sides, it can avoid seizing collateral from a borrower to close a deficit.

In Buterin's framing, the design removes the liquidation event by construction.

For a user trying to hold synthetic dollar exposure, the practical experience differs from a debt-backed stablecoin. In the debt model, a user can appear fully hedged until the collateral threshold is breached, at which point the position is force-closed.

In the options model, the holder avoids the sudden close, but the position can gradually stop behaving as the user intended.

Buterin's example uses a user who wants some level of dollar exposure while ETH is trading around $2,500. The user could buy a deep option tied to a lower strike, such as $1,500, and rotate into lower-strike options if ETH falls toward the original strike.

If the user does not rebalance, the exposure drifts. The user keeps a claim, but the hedge becomes less exact.

That is the central tradeoff. The design keeps risk in the system, and changes who controls the timing and what form the damage takes.

Liquidation-based systems outsource the decision to a protocol rule and liquidator bots. The options-based design pushes more of that decision toward users, wrappers, market makers, or automated rebalancing systems.

Buterin also acknowledged a limit for stablecoin use. A medium amount of annualized drift may be acceptable for someone seeking price stability relative to future expenses.

It is much less useful for an accounting stablecoin, where users want to treat the token as a dollar for payments, bookkeeping, or tax reporting.

The oracle tradeoff

The oracle argument may be the proposal's most important protocol-design claim.

Debt-backed liquidations depend on real-time price feeds. A protocol needs a binding price quickly enough to determine when a position is unsafe and to allow liquidators to act.

Buterin argues that this constraint makes real-time oracles hard to secure because they rely on automated actors watching live signals and leave little room for slower dispute resolution.

Options move the critical oracle call to maturity. Oracle risk remains, but the time pressure changes.

If a system can wait to resolve a contract, it can use slower, more contestable mechanisms, including prediction-market-style approaches or expensive fallback oracles that would be impractical for instant liquidation.

That is why the proposal is more than a stablecoin tweak. It shifts DeFi's risk architecture away from a single live price that can trigger irreversible action.

Recent research on liquidation dynamics in DeFi shows why that surface is central: liquidation mechanics can create incentives around price manipulation, MEV, and oracle-extractable value when a profitable closure depends on a market price crossing a trigger.

The benefit still depends on implementation. A wrapper that automatically rebalances for users could make the product easier to hold, but it could also recreate visible timing rules that sophisticated traders can anticipate.

A purely local user agent could hide some timing choices, but would raise its own usability and execution questions. An onchain DAO wrapper would need deterministic rules and deep markets to avoid becoming another predictable target.

Slow oracles help only if the rest of the design avoids forcing the same problem elsewhere. That is the tension Buterin's post leaves for builders.

A slower oracle can give a system more time to settle disputed information, but users still need markets deep enough to rotate exposure and rules strong enough to avoid turning every rebalance into an exploitable signal.

The comparison with prior oracle disputes is useful here because the risk arises when bad data meets a rule that must act immediately.

The options design reduces the need for that instant decision, while builders still have to decide who watches the index, who provides liquidity, and who absorbs losses when the market moves faster than the hedge.

What developers still have to prove

The next test is whether the market structure around Buterin's idea can be competitive with the debt systems it would challenge.

The proposal itself flags slippage as a major risk. Rebalancing through ordinary automated market makers could be expensive, especially if users need to rotate option exposure repeatedly during volatile periods.

Buterin suggested that rebalancing might need a different market structure, closer to patient one-sided market making than an instant sell.

That requirement is the adoption test. If users avoid liquidation but bleed too much value through drift, slippage, or operational complexity, the model becomes elegant research rather than useful DeFi infrastructure.

If builders can make rebalancing cheap and less exposed to attack, the idea could become a serious alternative for users who want price stability without signing up for a liquidation cliff.

The same test applies to stablecoin framing. The proposal is most defensible when described as a way to hold a stability-oriented exposure or personal hedge.

It becomes weaker if marketed as a simple dollar replacement. A token that drifts away from its target and needs periodic rotation is a different user promise from a redeemable dollar, an overcollateralized stablecoin, or a conventional CDP-backed synthetic.

For Ethereum, the significance is that one of its most influential designers is treating liquidation as an architectural choice rather than an unavoidable fact of DeFi.

The next signal is whether any protocol team turns the options model into a tested wrapper, simulation, or live market with sufficient liquidity to demonstrate the trade-off in practice.

Until then, the proposal is best read as a direct challenge to DeFi's crash mechanics: the industry can keep trying to make liquidations faster and better collateralized, or it can test designs built without sudden forced sales.

The post Vitalik wants DeFi price crashes to stop triggering automatic liquidations appeared first on CryptoSlate.

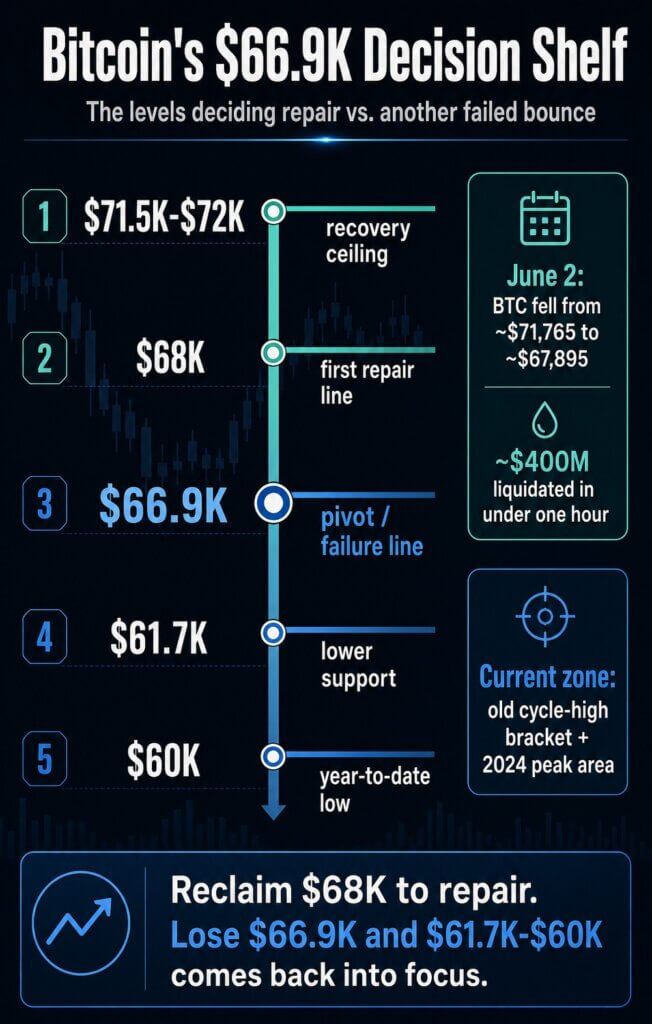

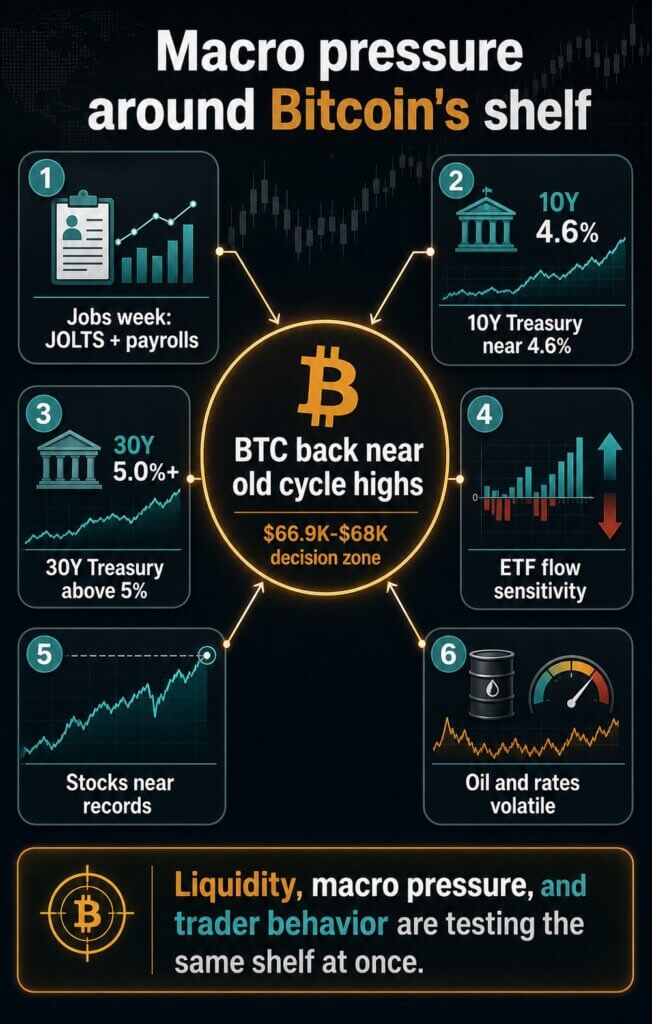

Bitcoin is back at a crossroads it has navigated multiple times in prior cycles, and this may be where the real test begins in this cycle.

After weeks of trying to turn the low-$80,000s into a new recovery zone, BTC has returned to the $66,900-$68,000 area, the same band I have used through several recent CryptoSlate pieces as the difference between repair and renewed downside.

A June 2 break below $68,000 sent Bitcoin from roughly $71,765 to $67,895 and triggered about $400 million in liquidations in under an hour.

By Wednesday morning in London, CryptoSlate's Bitcoin price page showed BTC near $66,942, putting spot price directly inside the shelf.

The price point overlaps with Bitcoin's old cycle highs, the 2024 peak zone, and the failure line from the earlier channel work.

We must now ask ourselves: did Bitcoin revisit a known support shelf before rebounding, or has the market confirmed that the prior bounce failed?

The old map is back in control

My level map always depended on acceptance across sessions over one candle.

In March, my CryptoSlate analysis treated the $68,000-$71,500 area as the range Bitcoin needed to hold and identified $66,900 as the failure line below it.

The idea was that BTC had avoided a larger drop only if it could keep trading above the lower edge and rebuild toward the top of the range.

That same framework came back after the late-March drop toward $65,000. At the time, the recovery case needed Bitcoin to reclaim $68,000 first, then prove it could work back toward the $71,500-$72,000 ceiling.

If it failed there, $66,900 stayed active as the line that kept the downside path open.

That is where the market is again. The June 2 liquidation move dragged price back into the bracket that has separated recoveries from failed bounces throughout the recent channel work.

In practical terms, $68,000 has become the first line Bitcoin has to reclaim to show that the flush was a support test, not the start of another leg lower.

The upper side of the map is just as important. I have repeatedly treated $71,500 as the area where recovery attempts had to prove themselves.

My March 5 analysis warned that repeated rejection there raised the risk of rotation down through $68,000 and $66,900 toward the low-$60,000s.

That sequence gives the current market a cleaner signal. A wick into the band can be noise; a failure to reclaim the band changes behavior.

For bulls, the job is to turn $68,000 back into traded acceptance. For bears, the confirmation is sustained weakness through $66,900.

Until one side gets that, the market remains in the middle of an unresolved argument.

What actually panned out

The useful part of revisiting these levels is the sequence of decision points, more than perfect tick-by-tick precision.

On that test, the roadmap held up better than it may have felt in real time. Bitcoin held around $70,000 in early March, delaying the $49,000 path as the market tested the upper range again.

The follow-up asked whether the downside call had been invalidated. The market then failed to cleanly clear the upper side of the range.

The repeated inability to turn $71,500-$72,000 into support kept the old risk path alive.

The next phase looked better for bulls. In early May, Bitcoin was back in the low-$80,000s, with the market asking whether a new 2026 high was coming.

That was the V-shaped move from the late-March lows: roughly $65,000 at the end of March, back toward the low-$80,000s by early May.

Even that upside framework kept the $65,000-$70,000 area as the first support zone if risk appetite faded.

The move back to this band follows the first major support region that was supposed to come into play if the low-$80,000s could not hold.

The current price action has therefore answered part of the earlier question. The market delayed the deep-bear case, but it also failed to establish enough acceptance above $71,500-$72,000 to retire it.

The rally stretched higher, lost altitude, and returned to the same shelf that was marked as the next test if momentum broke.

That is the point of looking backward here. The prior framework only had to tell readers which levels would decide whether strength was real.

So far, Bitcoin has respected the order of the map: first the ceiling near $71,500-$72,000, then the repair line at $68,000, and now the $66,900 edge.

Macro did not give Bitcoin much cover

The chart levels gained force as the macro backdrop stopped helping.

In mid-May, I linked Bitcoin's retreat from the low-$80,000s to Treasury yields, ETF-flow dependence, oil, the dollar, and broader risk appetite.

The June breakdown is happening during a jobs-data week, with traders watching labor-market data, Fed expectations, and long-end yields alongside crypto-native positioning.

CryptoSlate's June jobs-week setup noted that Bitcoin was facing JOLTS and payrolls with the 10-year Treasury yield near 4.6%, the 30-year above 5%, ETF outflow pressure, and a market still pricing a Fed hold.

That gives the current level a macro catalyst. It is a support zone being tested as the bond market continues to pressure long-duration risk assets.

The tension is sharper because equities have held up better. US stocks are near record highs even as oil-driven volatility and rate pressure remained in the background.

Bitcoin, by contrast, has given back the early-May rally and moved back toward the same old all-time-high bracket that once defined the upper end of prior cycles.

That divergence changes the tone of the level test. If stocks are still near records while Bitcoin is losing the low-$80,000s and revisiting old-cycle highs, the weakness points to more than a broad risk-off washout.

It points back to crypto-specific pressure, ETF flow sensitivity, and the failure to build acceptance above the recovery ceiling.

Bitcoin is weakening into a known technical shelf without an obvious macro relief valve.

If yields keep pushing higher or ETF flows fail to absorb the selling, the chart levels become harder to defend. The same price shelf is being tested by liquidity, macro pressure, and trader behavior at once.

The next test is acceptance over one wick

This is why $66,900 and $68,000 carry more weight than the exact low from a single overnight move.

If Bitcoin can defend the $66,900 area and reclaim $68,000, the first repair target is acceptance back inside the prior range, followed by another attempt to rebuild toward $71,500-$72,000.

That would leave the liquidation shock on the chart, but it would show that the market treated the move as a flush into support rather than a confirmed breakdown.

If Bitcoin loses that defense, the lower path becomes the cleaner signal. A March CryptoSlate overlap piece directly connected $66,900 resistance or failure to a possible move toward $61,700, and the broader roadmap keeps the yearly low near $60,000 in focus, with that level beneath.

From the current $67,000 area, that is close enough to keep in view while still requiring BTC to lose the shelf first.

That's why I tend to work with roadmaps rather than predictions.

$71,500-$72,000 was the zone that would have shown recovery strength. $68,000 was the first repair line. $66,900 was the lower edge. $61,700-$60,000 was the next area if the edge failed.

Bitcoin is now sitting on that edge again.

The market can answer without drama. A sustained reclaim of $68,000 would put the range-repair case back on the table.

Failure to hold $66,900 would bring the return to $61,700 and the yearly low near $60,000 into question. Until one of those happens, the most honest conclusion is that Bitcoin has returned to the exact bracket that was supposed to decide whether the prior bounce was real.

The post Bitcoin returns to the price that capped 2021, defined 2024, and now tests the rally again appeared first on CryptoSlate.

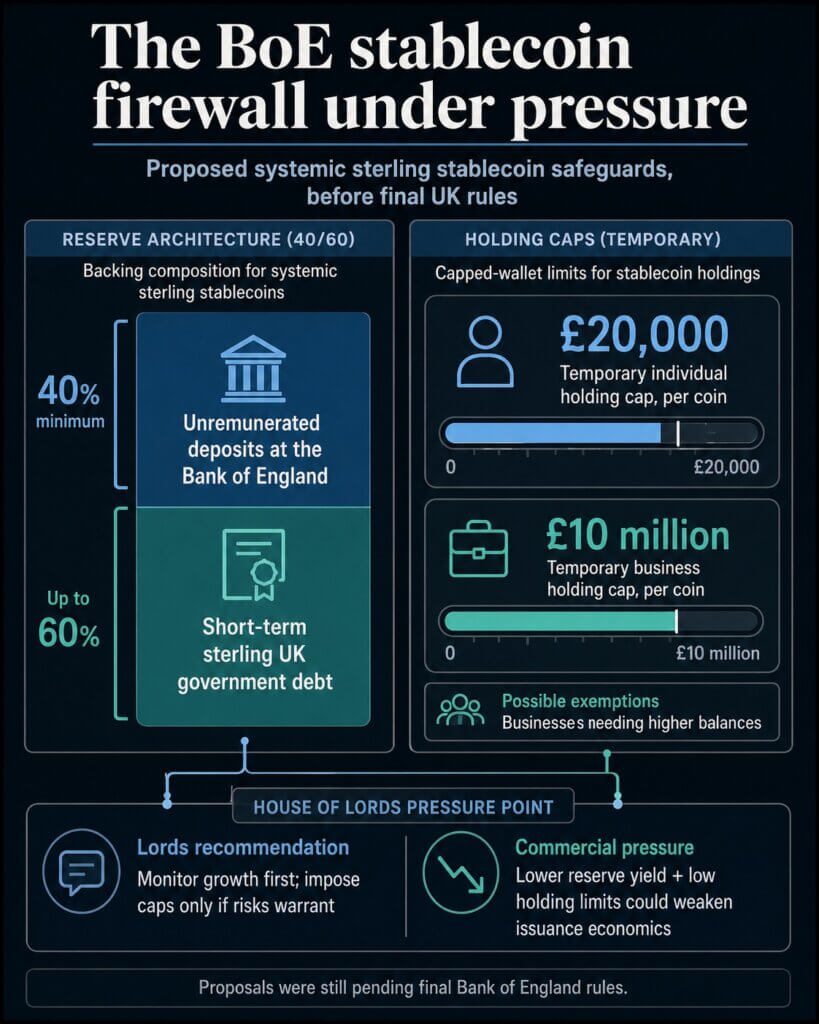

A House of Lords committee has told the Bank of England to rethink stablecoin caps before the UK's regime is finalized.

The Financial Services Regulation Committee published its report, Stablecoins: waiting for regulation, on June 3, turning a technical debate over reserve design into a test of whether the UK can build a pound-denominated stablecoin market without making it uneconomic from the start.

The pressure point is the design of the safeguards. The committee supports 1:1 backing and accepts that stablecoins can create risks around financial stability, consumer protection, and illicit finance.

Its challenge is more specific: the Bank's proposed safeguards may be calibrated for a market that does not yet exist in the UK.

Two measures sit at the center of that critique. The Bank has proposed temporary per-coin holding limits of £20,000 for individuals and £10 million for businesses.

It has also proposed requiring systemic sterling stablecoin issuers to keep at least 40% of backing assets as deposits at the Bank of England that do not earn interest.

The Lords report says those choices could shape whether a GBP stablecoin market develops at all. If a pound stablecoin cannot be held in useful amounts or generate enough reserve income to support the issuer's business, the UK could end up with clear rules, but few firms willing to build the products those rules are meant to govern.

The Rules Under Pressure

The Bank of England's November 2025 consultation proposed a split backing model for systemic sterling stablecoins.

At least 40% of backing assets would sit as deposits at the Bank, while up to 60% could be held in short-term sterling-denominated UK government debt.

The Bank's case is that central-bank deposits provide immediate liquidity if holders seek large redemptions in a short period. In its consultation, it said the threshold aligned with estimates of possible short-term redemption requests drawn from stress events in traditional and crypto markets.

The 60% government-debt allowance was meant to improve issuer viability compared with an earlier model that would have placed all backing assets in unremunerated central-bank deposits.

That compromise is now under pressure. The Lords committee concluded that remuneration and liquidity requirements for backing assets could have a significant effect on issuer viability and UK competitiveness.

It urged the Bank to consider the impact of requiring a proportion of unremunerated assets and to reconsider whether deposits held at the Bank should be remunerated at Bank Rate.

The committee also pushed the Bank toward a more flexible approach to backing-asset composition. It said the Bank should be open to a principles-based and less prescriptive model, with requirements adjusted as market behavior and risks become clearer.

The same logic applies to holding limits. The Bank's proposal would cap each individual's holdings of a systemic stablecoin at £20,000 per coin and each business's holdings at £10 million, with possible exemptions for businesses that need higher balances in normal operations.

In a November news release, the Bank framed those limits as temporary tools to protect access to credit while the financial system adapts to new forms of money.

The committee's recommendation was sharper. Given the early stage of the GBP stablecoin market, it said the Bank should monitor growth and impose holding limits only if financial stability risks clearly warrant them.

If limits become necessary, the committee said the Bank should consult to ensure they can be implemented in a practical way that still meets the Bank's objectives.

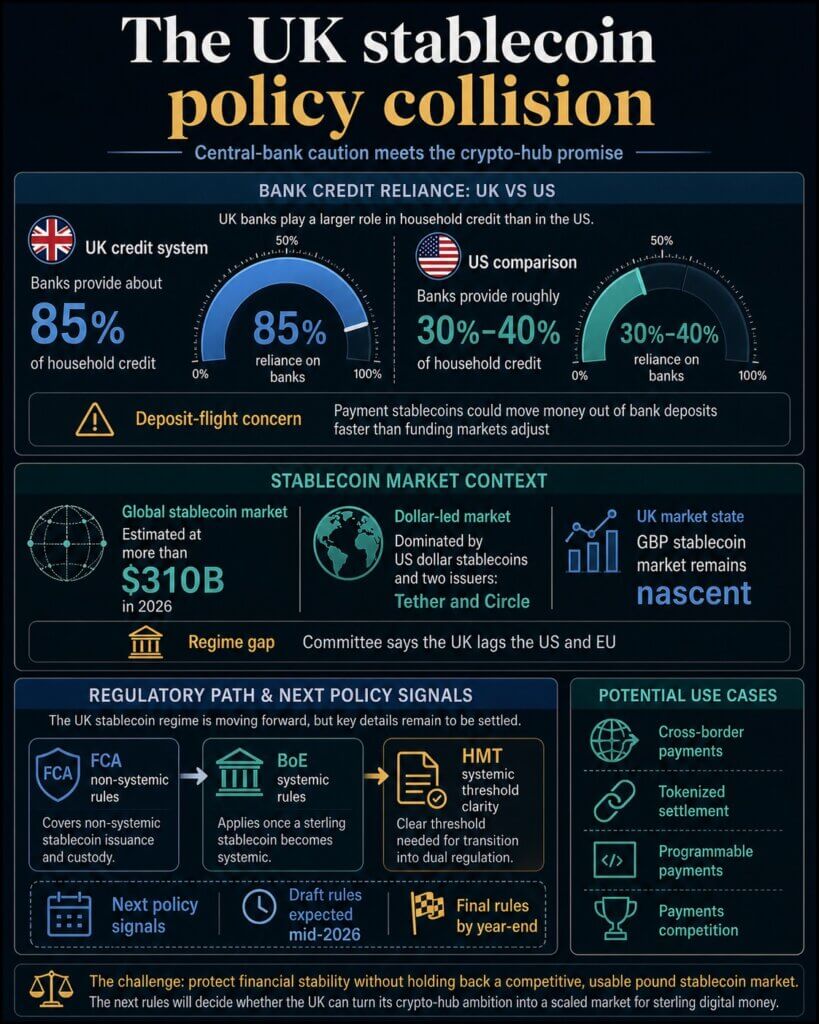

Why The Bank Is Cautious

The Bank's concern goes beyond competition with banks. In the UK, bank deposits do more work inside the credit system than they do in some other major markets.

In oral evidence to the committee in March, Sarah Breeden, the Bank's deputy governor for financial stability, said banks provide about 85% of household credit in the UK, compared with roughly 30% to 40% in the US.

Her argument was that if deposits moved rapidly into payment stablecoins and that funding was not replaced, the result could be a drop in credit for households and businesses.

That is the financial-stability case for a circuit breaker. The Bank is designing for a future in which stablecoins are widely used as money for everyday payments, beyond their current use in crypto trading.

If adoption moved quickly through social media platforms, e-commerce networks, wallets, or automated payment tools, the Bank worries that money could leave deposits faster than banks and funding markets could adjust.

The committee accepts that risk. Its report says stablecoins can pose challenges around financial stability, illicit finance, and consumer protection.

It also welcomes 1:1 backing, audited reserves, disclosure, statutory trust protections, and the proposed Bank backstop lending facility for systemic issuers.

The disagreement is about timing and prescription. Lawmakers are asking whether the Bank should impose caps and reserve economics before there is enough evidence about how a pound stablecoin market would behave.

A protective rulebook could reduce the chance of a disorderly shift out of bank deposits. It could also make the regulated version of the product less attractive than offshore, dollar-denominated, or non-systemic alternatives.

The stakes are higher because the report describes the UK stablecoin market as nascent while the global market is already large and dollar-led.

It says the global stablecoin market was estimated at more than $310 billion in 2026, overwhelmingly dominated by US dollar stablecoins and two issuers, Tether and Circle.

For the UK, that creates a strategic problem. A sterling stablecoin market could support cross-border payments, tokenized settlement, programmable payments, and competition in payments.

It could also reduce the risk that UK users and businesses default to dollar stablecoins because pound alternatives never get enough regulatory clarity or commercial scale.

The committee says the UK is already lagging the US and EU in developing a stablecoin regime, though it says the country is now moving in the right direction.

The FCA's stablecoin issuance and crypto custody consultation covers the non-systemic side of the regime, while the Bank's rules apply once a sterling stablecoin becomes systemic.

The transition between those regimes remains one of the areas issuers need to understand before they can build durable business plans.

The Next Signal Is The Draft Rulebook

The timing makes the Lords report more than a retrospective critique. Breeden told the committee in March that the Bank expected draft rules in the middle of 2026, final rules by year-end, and applications from stablecoin issuers by the end of the year.

That means the next policy document will show whether the Bank treats the report as a reason to change the design or as a challenge to explain the existing model more clearly.

The signals to watch are specific: whether per-holder caps remain, whether the Bank shifts toward aggregate issuance guardrails or monitoring triggers, whether the 40% deposit share is adjusted, and whether any Bank deposits receive remuneration.

Rewards will count, too. The committee noted relatively little demand for issuers to pay interest on stablecoins, but said the treatment of rewards, rebates, or other incentives could affect the creation of a GBP stablecoin market and the UK's international competitiveness.

That question connects stablecoin rules to the broader payments market, where card networks and financial apps already compete through reward structures.

The report also asks for more clarity from HM Treasury on when a stablecoin becomes systemic. That threshold is central for issuers because it determines when a firm moves from the FCA-only track into dual regulation by the Bank and FCA.

If the transition is too uncertain, scaling may become a risk in itself.

CryptoSlate has already covered adjacent UK payment infrastructure moves, including Revolut's pound stablecoin sandbox trial and the Bank's 24/7 settlement plans.

The Lords report moves the debate to a different point: whether the UK's stablecoin rulebook will let a sterling market become commercially meaningful once tokenized payments enter the system.

The Bank is still finalizing the regime, and the committee is still asking for financial-stability protections. The new pressure is for the Bank to show that its safeguards will not stop a pound stablecoin market before it has a chance to form.

That is the live test for the UK's crypto-hub promise. The next draft rules will show whether the Bank's stablecoin firewall is a temporary guardrail, a redesign in progress, or a cost issuers decide the pound market cannot absorb.

The post Bank of England stablecoin caps may choke the UK’s pound-token market before launch appeared first on CryptoSlate.

Bitcoin’s aggressive break below $70,000 has shifted the market from a debate over dip-buying to a more defensive question of how far traders now need to insure against the next leg lower.

Data from CryptoSlate showed that the largest cryptocurrency fell to as low as $65,404 over the past day, triggering $1.8 billion in liquidations and wiping out bullish leverage that had built around hopes of a quick recovery.

This failed rebound has pushed traders toward protection at levels that only recently looked distant.

Options positioning now shows demand building around the $60,000 and $50,000 strikes, a sign that investors are preparing for a deeper reset as Strategy’s first Bitcoin sale in years, ETF outflows, AI-driven capital rotation and unresolved macro pressure weaken the sources of support that carried the market earlier in the year.

How BTC's failed bounce turned $70,000 into resistance

Analysts at BIT Official noted that Bitcoin was already trading defensively after sliding towards $72,000 last week, when geopolitical tensions tied to the Strait of Hormuz prompted a broad retreat from risk assets.

The firm noted that a brief reprieve materialized after President Donald Trump suggested the US would lift a naval blockade, while April core PCE inflation aligned with expectations at 3.3% year-over-year.

This data and political development eased immediate macroeconomic anxieties and forced over-leveraged bears to cover their shorts.

As a result, Bitcoin briefly spiked toward $73,400 over the weekend, giving bulls leverage to argue the selloff was exhausted.

However, that narrative collapsed when the recovery failed to attract meaningful spot volume.

When Iran’s foreign ministry explicitly denied nuclear talks, disputed Trump’s uranium claims, and insisted the strait would reopen strictly on its own timeline, the geopolitical relief trade vanished. Without a formal de-escalation, Bitcoin was left entirely exposed.

Consequently, the market was quickly dragged back to $70,000, which is a critical juncture where options positioning, market psychology, and short-term holder cost bases converged.

Indeed, that level had served as both a psychological floor for bulls and a prime target for bears hunting for forced liquidations.

Once Bitcoin sliced through that support, automated liquidation engines began aggressively unwinding undercollateralized long positions.

The decline further accelerated rapidly into a vacuum, as spot buyers proved unwilling to absorb the selling pressure.

Strategy’s sale gives bears a cleaner script

BTC's decline under $70,000 also came at a highly vulnerable moment when the corporate treasury narrative fractured.

This week, Strategy confirmed that it sold 32 BTC for $2.5 million to fund cash distributions and dividend payments on its high-yield perpetual preferred stock.

The sale came as a shock to the market because Strategy had positioned itself as the definitive corporate proxy for the Bitcoin accumulation trade.

Over the past years, the Michael Saylor-led company business model relied heavily on equity issuance, preferred stock, and uninhibited access to capital markets to construct the largest public-company Bitcoin treasury in existence.

To the broader market, the company was not just a major holder but also a symbol of permanent, price-agnostic demand.

However, that perception is now under enormous strain as the firm most synonymous with the “never sell” philosophy liquidated coins to meet a routine cash obligation.

Jeff Dorman, the CIO of Arca, noted:

“From a sentiment standpoint, how do you think the average Bitcoin investor is going to react when every major news outlet and social media influencer starts writing that “MicroStrategy is now a seller of BTC”? This company has bought over $50 bn of Bitcoin, and currently owns roughly 4% of the total 21 million outstanding.”

That pivot armed bears with a clean, simple argument right as Bitcoin slipped below major support.

Market observers argued that the sale complicates the market’s base-case assumption that Strategy will act as an uninterrupted buyer in all macroeconomic environments.

In fact, some have postulated that the firm could make more sales in the future in order to actively manage its balance sheet.

AI’s liquidity pull leaves Bitcoin without its ETF cushion

This structural shift in sentiment coincides with the evaporation of Bitcoin’s most reliable safety net: the institutional ETF bid that anchored the earlier stages of the bull run.

According to SoSoValue data, Bitcoin ETFs have bled more than $4 billion over the trailing four weeks. This marks the most aggressive redemption cycle since the spot products debuted, starving the market of the steady inflows required to absorb routine selloffs.

Market analysts attribute this severe capital flight to a generational rotation into artificial intelligence.

Institutional allocators are actively liquidating crypto positions to free up dry powder for a looming wave of tech mega-IPOs, primarily targeting high-growth ventures like SpaceX, Anthropic, and OpenAI.

Pierre Rochard, CEO of the Bitcoin Bond Company, pointed out that this AI boom has added $19 trillion in market capitalization to the top 50 public equities over the past 12 months, roughly 13 times Bitcoin’s total market value.

He said that capital expenditure cycle is drawing liquidity and attention away from Bitcoin, making the asset’s resilience notable despite the pressure.

Independent Bitcoin analyst Matthew Case described the move as an “AI IPO liquidity vacuum,” arguing that institutions that rode Bitcoin and crypto exposure higher now have a rare chance to position for major private-market and pre-IPO opportunities tied to SpaceX, Anthropic and OpenAI.

This capital rotation aggressively starves Bitcoin of its marginal buyer. During periods of robust ETF inflows, institutional demand acts as a shock absorber, cushioning the blow from macroeconomic friction, geopolitical headlines, and derivatives volatility.

With that bid suddenly sidelined, the market is dangerously exposed; a standard technical decline can cascade much further before encountering strong spot support.

$60,000 becomes the market’s next insurance level

Consequently, traders have fundamentally repriced their risk models. The market is no longer structured around highly leveraged bets anticipating a swift return to $70,000.

Instead, capital is aggressively repositioning for the reality that Bitcoin’s next durable line of defense may reside significantly lower.

Deribit data shows traders have built roughly $1.2 billion in open interest around the $60,000 strike, while the $50,000 strike has attracted about half that amount. Cumulatively, $1.8 billion worth of open interest are situated at these strike prices.

The positioning marks a change from the structure that dominated earlier in the rally. When ETF inflows were strong and Strategy remained an unquestioned buyer, pullbacks were treated as opportunities to add exposure.

After the liquidation wave, ETF redemptions and Strategy’s sale, the same pullbacks are being treated as events that need to be insured.

As a result, traders with material Bitcoin exposure are moving toward puts and collar structures designed to preserve some upside while limiting losses if the drawdown accelerates.

The post Bitcoin’s plunge to $65,000 has traders paying to protect against a fall to $50,000 appeared first on CryptoSlate.

CryptoTicker.io

The boundary between traditional payment networks and decentralized infrastructure is dissolving. Global payment leaders Visa, Mastercard, and Stripe are in advanced stages of launching a collaborative, institutional-grade stablecoin platform.

The joint initiative aims to standardize digital currency routing across legacy financial systems and capture the rapidly expanding market share of programmable, dollar-pegged digital assets.

The Push for Native Onchain Settlement

The cooperative project signals a collective strategic pivot. Stablecoin networks processed an unprecedented $33 trillion in total transaction volume last year, pushing past the cumulative settlement figures of standard credit card processors. Rather than competing against decentralized protocols externally, the payments triumvirate is building a native layer to absorb and route these token flows directly through their own ledgers.

The platform's primary utility centers on institutional settlement, business-to-business (B2B) cross-border routing, and programmatic liquidity provisioning. According to industry insiders, top-tier U.S. cryptocurrency exchange Coinbase is also positioned to participate in the joint launch, adding a deep consumer liquidity foundation to the network.

Integrating Bridge Infrastructure for Merchant Scale

The move leverages major corporate infrastructure plays executed recently. Stripe’s ongoing integration of its $1.1 billion acquisition, Bridge—a leading stablecoin orchestration network—supplies the technological backbone for the system. Concurrently, Visa has expanded its pilot programs with Bridge to enable programmatic, stablecoin-backed card issuance across 18 countries, targeting growth to over 100 countries.

The architecture addresses three core corporate payment bottlenecks:

- Instant Currency Authorization: Automated conversion mechanisms that allow digital asset balances to clear instantly at terminal points-of-sale without price slippage.

- Direct Acquiring Settling: Enabling international merchants to receive business revenues directly in major fiat-backed tokens like USDC or EURC, completely bypassing traditional banking intermediaries.

- Low-Cost B2B Remittances: Providing international supply chains with cross-border rails that cut standard transaction fees from the standard 1.5% to 3% down to sub-0.1% levels.

By pooling their technical reach, the participants create an insulated payment system that prevents capital flight from legacy banking systems toward entirely non-intermediated, decentralized payment architectures.

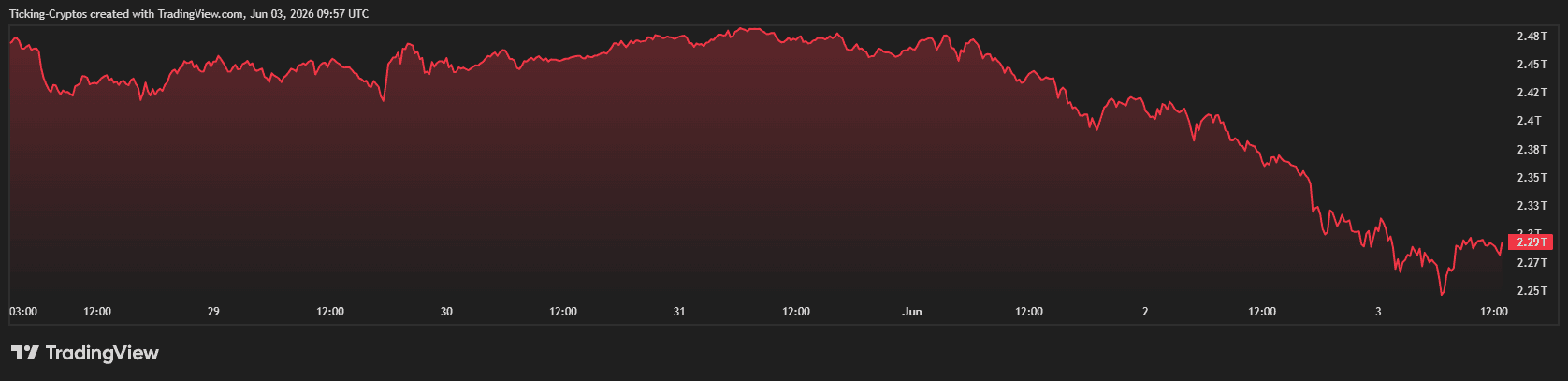

The digital asset market is experiencing heavy selling pressure today. The total cryptocurrency market capitalization has fallen to $2.29 trillion, marking a significant 8.7% decline over the past week.

As liquidations mount across major exchanges, traders are assessing whether this downward trajectory is a temporary correction or the start of a prolonged bearish phase.

Why is the Crypto Market Crashing Today?

The current market downturn stems from a combination of macroeconomic data releases, shifting monetary policy expectations, and heavy derivatives liquidations.

1. Macroeconomic Pressures and Interest Rate Outlook

Risk assets, including cryptocurrencies, are reacting to recent economic data indicating sticky inflation. This has led market participants to price in a "higher-for-longer" interest rate environment by global central banks. When interest rates remain elevated, capital typically rotates out of speculative assets like cryptocurrencies and into yields guaranteed by government bonds.

2. Cascading Derivatives Liquidations

The breach of key technical support levels for Bitcoin triggered an automated wave of long liquidations. According to data tracking platforms like Coinglass, hundreds of millions of dollars in leveraged bullish positions were wiped out within a 24-hour window. This forced selling accelerated the downward momentum across all major altcoins.

3. Institutional Capital Outflows

Data from institutional fund managers reveals a slowdown in net inflows into spot Bitcoin and Ethereum ETFs. A multi-day streak of net outflows indicates that institutional appetite has cooled off temporarily, reducing the baseline buying pressure required to sustain higher price levels.

Top Cryptocurrencies Price Analysis

Large-cap digital assets are flashing red, with layer-1 protocols suffering the sharpest intraday losses.

Bitcoin (BTC) Price Update

$Bitcoin is currently trading at $66,600, reflecting a 3% drop over the last 24 hours. BTC failed to sustain its position above the $68,000 psychological threshold. The immediate horizontal support now sits at $65,000. If buyers fail to defend this zone, a deeper retest of the $62,000 macro level is likely.

Ethereum (ETH) Price Update

$Ethereum has underperformed Bitcoin today, dropping 5% in the last 24 hours to trade at $1,880. The asset has broken below its short-term moving averages. Analysts monitor the $1,800 support level closely, as breaking below it could invalidate the current medium-term bullish structure.

Solana (SOL) Price Update

$Solana has matched Ethereum's downside, falling 5% over the past 24 hours to sit at $75.00. Despite strong network activity, SOL remains highly sensitive to broader market liquidity drains. Resistance is now firmly established at $82.00, while structural support rests near $70.00.

Ripple (XRP) Price Update

$XRP has shown relative resilience compared to its peers, down just 1.5% in the last 24 hours to trade at $1.23. Ongoing regulatory developments and liquidity patterns unique to the asset have decoupled its short-term price action slightly from the broader market dump, though it remains capped by overhead resistance at $1.30.

Market Outlook

The crypto market structure is currently undergoing a leverage flush. While the immediate intraday trend remains bearish, historical data shows that corrections of 10% to 15% are common structural occurrences during broader market cycles. Market participants are advised to monitor institutional fund flows and upcoming regulatory announcements, which can be tracked on major financial networks like Bloomberg.

Institutional Capital Rotates Out of Crypto Into Artificial Intelligence

$Bitcoin experienced a sharp 5.6% decline, dropping to the $67,400 mark following major corporate developments in the tech and traditional finance sectors. The market sell-off aligns with a massive capital allocation shift after Google launched an $80 billion artificial intelligence (AI) capital raise.

The initiative is notably backed by Warren Buffett's Berkshire Hathaway. This collaboration marks one of the largest institutional capital rotations from digital assets into AI infrastructure in recent financial history. Asset managers and corporate treasuries are rebalancing portfolios to fund these high-conviction AI initiatives, pulling liquidity directly out of the cryptocurrency ecosystem.

Crypto Treasury Inflows Collapse by 95% in May

The pressure on digital asset prices follows a broader liquidity drought that intensified over the last month. Data reveals that crypto treasury inflows collapsed by 95% throughout May, recording their lowest operational levels since 2024.

This drastic slowdown in capital entering crypto funds signaled an early warning of the institutional pivot. The sudden emergence of the mega-cap Google-Berkshire fund has accelerated this trend, leaving Bitcoin to test key support levels as buy-side pressure from corporate treasuries temporarily dries up.

Latest Cryptocurrency Prices

- Bitcoin ($BTC): $67,400 (-5.6%)

- Ethereum ($ETH): $1,920 (-3.2%)

- Solana ($SOL): $76.50 (-4.8%)

- $XRP: $1.23 (-4.7%)

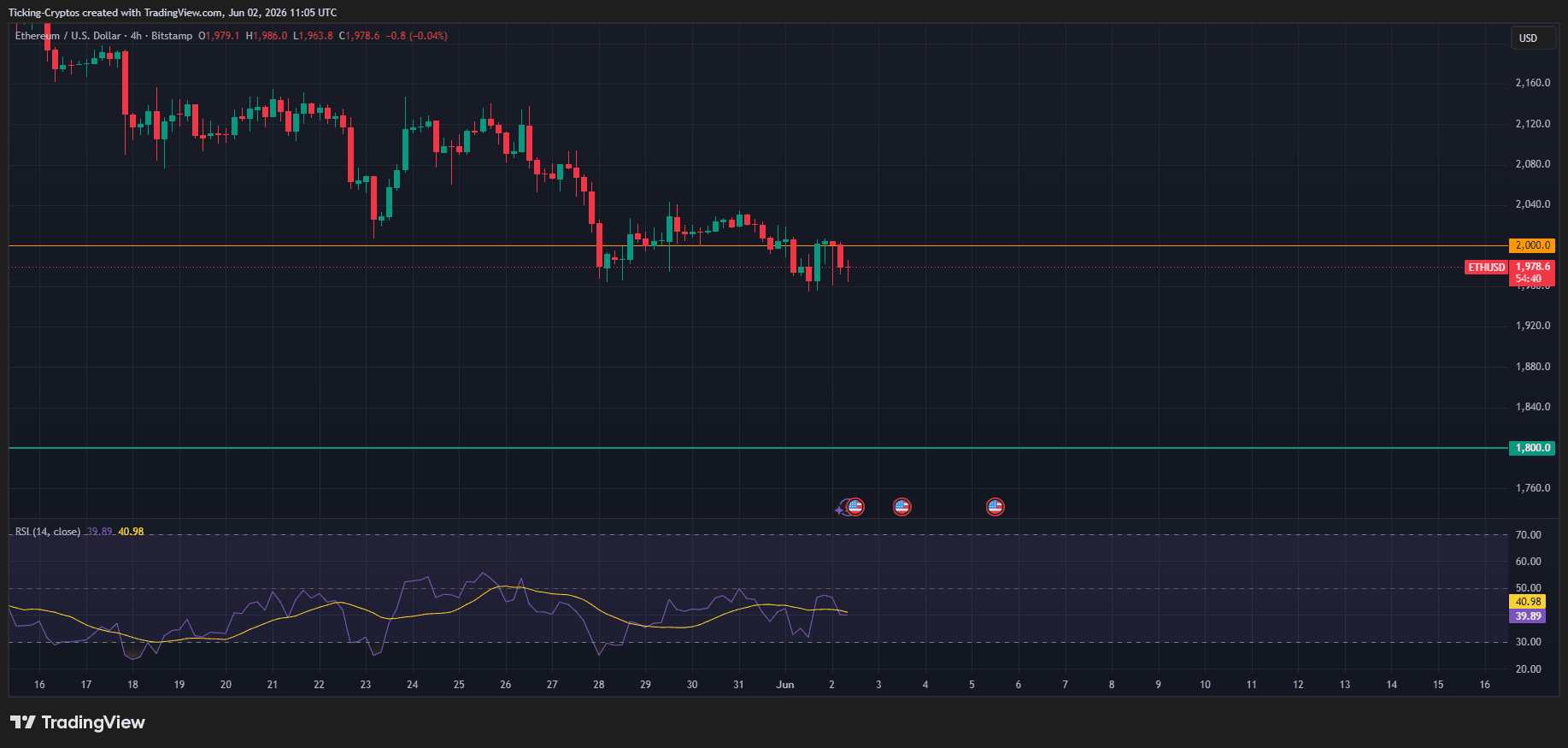

Ethereum Fails to Hold $2,000 as Bitcoin Plummets

The cryptocurrency market is experiencing a severe intraday correction on June 2, 2026. Ethereum ($ETH) has officially breached its critical $2,000 psychological support zone, hitting an intraday low near $1,963. This macro markdown follows a systemic bleed-out led by Bitcoin ($BTC), which cascaded below the definitive $70,000 threshold for the first time in nearly two months.

The downside momentum accelerated during early European trading hours, triggering automated stop-losses and derivative liquidations across major digital asset exchanges like Bitstamp and Binance.

Why is the Crypto Market Crashing Today?

The driving force behind Ethereum’s sudden decline is entirely tied to the negative structural shift in Bitcoin’s price action. The leading cryptocurrency faced dual headwinds that crushed buyer sentiment over the last 24 hours:

- Strategy’s Surprise Token Sale: MicroStrategy (disclosed on markets simply as Strategy) revealed its first $Bitcoin liquidation since late 2022. The corporate treasury sold $2.5 million worth of BTC to satisfy preferred shareholder dividends. While the nominal amount is small, the break in Michael Saylor's strict "HODL" playbook heavily spooked market participants.

- Massive ETF Outflows: According to institutional data compiled by Bloomberg, US spot Bitcoin ETFs are currently on a record-breaking 11-day streak of net capital outflows, with investors yanking nearly $3.5 billion from fund vehicles amid escalating geopolitical tensions between the US and Iran.

As capital aggressively rotated out of Bitcoin, the wider altcoin landscape collapsed. Since $Ethereum remains tightly correlated with BTC's market dominance, the drop under $70,000 forced an immediate technical breakdown in Ethereum.

Ethereum Technical Analysis: $1,800 is the Next Defensive Line

Looking at the 4-hour ETH/USD chart, the price action paints an intensely bearish picture for short-term holders.

Key Technical Indicators to Watch:

- The $2,000 Pivot: The horizontal orange line represents the critical psychological barrier. By failing to sustain liquidity above $2,000, this zone has officially flipped from an active support floor into a major overhead resistance level.

- Relative Strength Index (RSI): The 14-period RSI has slid down to 39.89, signaling that while the market is approaching oversold conditions, there is still clear room for momentum-driven downside before a technical bounce can be sustained.

- The $1,800 Baseline: If the selling pressure intensifies, the primary macro support targeted by bears sits at the green horizontal line of $1,800.0. Traders should monitor daily and weekly closes closely; a structural failure to defend $1,800 could risk a deeper retest toward late 2024 macro lows.

Bitcoin Price Slips Below Psychological $70,000 Support

The cryptocurrency market faced severe downward pressure on Tuesday morning as the Bitcoin price officially broke below the critical $70,000 psychological baseline. $BTC dropped by nearly 4% over a 24-hour window, hitting intraday lows near $69,371.

This unexpected correction has disrupted weeks of sideways momentum and triggered a cascade of automated sell orders. Total crypto market liquidations surged past $766 million within a matter of hours, with over $600 million consisting of overleveraged long positions being wiped out.

Why Is Bitcoin Crashing? Two Major Catalysts

The sudden breakdown below $70,000 is primarily attributed to a combination of institutional sell pressure and the sudden awakening of long-dormant wallets.

1. MicroStrategy Breaks Its "Never Sell" Stance

Market anxiety intensified following a Securities and Exchange Commission (SEC) 8-K filing revealing that MicroStrategy sold 32 Bitcoins between May 26 and May 31 to fund shareholder dividends. While the dollar amount of the sale was minor—valued at approximately $2.5 million—the psychological impact on retail and institutional investors was massive. MicroStrategy’s departure from its strict buy-and-hold narrative ignited widespread FUD (Fear, Uncertainty, and Doubt), accelerating a $483 million capital flight from U.S. spot $Bitcoin ETFs.

2. Mt. Gox Awakens with $739 Million On-Chain Transfer

Adding fuel to the fire, blockchain tracking firm Arkham Intelligence flagged a massive movement of 10,306 BTC (worth roughly $739 million) out of Mt. Gox cold storage into new active wallets. This represents the largest estate movement in over two months, raising investor concerns that imminent creditor distributions are about to hit the open market.

Bitcoin Prediction: What Is the Next BTC Support Level?

With the $70,000 floor officially invalidated, Bitcoin's short-term technical structure looks increasingly bearish. If the daily candle fails to close back above $70,000, market analysts warn of an extended correction. Weakening spot ETF inflows coupled with escalating macroeconomic uncertainties could pave the way for a deeper retest of the $65,000 macro support zone over the coming weeks.

Decrypt

With STRC trading under $100, experts are at odds over whether the sale has exposed a “structural crack” in Strategy’s Bitcoin flywheel.

A Zcash vulnerability could have allowed double-spending within the network's flagship privacy pool, though no exploitation occurred.

MoonPay's new desktop app connects AI assistants to crypto wallets and blockchain services through a graphical interface.

The fallout from Saylor’s first Bitcoin sale in years keeps spreading, while Bernie Sanders and Elizabeth Warren want crypto out of your 401(k).

The vulnerability in Trezor's TROPIC01 Secure Element chip was uncovered by an audit carried out by the Ledger Donjon team.

U.Today - IT, AI and Fintech Daily News for You Today

An $18 million liquidation cascade flushes XRP to $1.22, exposing a 1,614% margin imbalance and putting the $0.95 floor in focus.

Michael Saylor defends Strategy's 843K BTC war chest with 'Back to Work' cry as Bitcoin flushes $792 million in leverage.

XRP’s historical data suggests that the asset may face further price declines this month as June proves to be one of XRP’s weakest-performing months.

Cardano founder Charles Hoskinson explains what might be at stake amid economic challenges facing the ecosystem.

Barry Silbert brings back his viral 1% Bitcoin market cap prediction for Zcash (ZEC) as institutional inflows into Grayscale spike.

Blockonomi

Key Highlights

- Applied Aerospace & Defense (AADX) set its initial public offering price at $20 per share, securing $650 million in capital

- The defense contractor carries a market valuation near $3.5 billion, representing approximately 6x its projected 2025 revenue of $604 million

- First-quarter results showed a $57 million operational deficit, though revenue surged almost 40% compared to the prior year

- Product portfolio spans space launch equipment, unmanned aircraft systems components, and solid rocket propulsion elements

- Major clients feature Anduril Industries, Boeing, and GE Aerospace

Applied Aerospace & Defense (AADX) commenced public trading on the New York Stock Exchange this Wednesday following an initial public offering priced at $20 per share, bringing in $650 million in fresh capital.

120+ years of heritage. 11 facilities. 1,500 experts. @applied_ad aims to unleash the power of advanced manufacturing at scale to enable mission success for leading and next-generation space and defense technology companies. Welcome to the NYSE Community

$AADX pic.twitter.com/LNeVJX6EZm

— NYSE

The Huntsville, Alabama-headquartered manufacturer offered 32.5 million shares to investors, settling on a price within its previously announced $18 to $21 range. Should underwriting banks fully exercise their greenshoe option, the company could collect approximately $750 million in total proceeds.

The public market debut assigns AADX an enterprise value around $3.5 billion — roughly six times its anticipated 2025 sales figure of $604 million.

The path to profitability remains a work in progress. During the first quarter, the business recorded a $57 million operating shortfall and failed to achieve positive earnings for the complete 2025 fiscal year.

Revenue expansion tells a different story. First-quarter sales jumped nearly 40% on a year-over-year basis, capturing investor attention and enthusiasm.

AADX manufactures an extensive array of components. The product lineup encompasses propellant storage tanks and additional space vehicle parts, structural components for unmanned aerial vehicles, solid rocket motor casings, engine drive shafts, airframe assemblies, and aerodynamic control surfaces.

The customer roster represents premier names in defense and aerospace manufacturing. Anduril Industries, Boeing, and GE Aerospace count among the company’s key accounts.

Private Equity Origins and M&A Strategy

AADX emerged from consolidation rather than organic growth. Private investment firm Greenbriar Equity Group orchestrated a merger between Applied Aerospace — established in 1954 — and PCX Aerosystems, which traces its roots to 1900, forming the combined entity in the previous year.

Chief Executive James “Trip” Ferguson formerly headed the Space, Cyber, and Directed Energy business unit at AeroVironment (AVAV) prior to assuming leadership of the organization.

The market entry timing appears strategic. Multiple defense technology enterprises have accelerated their path to public markets in New York recently, with numerous listings completed over recent weeks — such as aerospace component producer Arxis (ARXS), unmanned systems developer AEVEX (AVEX), and radio frequency monitoring specialist Hawkeye 360 (HAWK).

Industry Momentum and Market Dynamics

Investor demand for space-related and defense equities has maintained strong momentum. Rocket Lab (RKLB) climbed more than 55% during the month preceding Wednesday’s market action, fueled primarily by anticipation surrounding the SpaceX public offering expected to assign that enterprise an approximately $1.8 trillion valuation.

Unmanned aerial systems have attracted increased attention following escalating tensions in the U.S.-Israeli confrontation with Iran. The Pentagon’s emphasis on affordable anti-drone technologies has sustained sector visibility among the investment community.

AADX’s diversified offerings — space infrastructure, drone subsystems, missile components — align directly with these prevailing investment themes.

Morgan Stanley and Jefferies served as primary underwriting banks for the transaction. AADX began NYSE trading Wednesday using the ticker designation “AADX.”

The post Applied Aerospace & Defense (AADX) Debuts on NYSE After $650M IPO appeared first on Blockonomi.

Key Takeaways