Cryptocurrency Posts

Crypto Briefing

Trader skepticism highlights the challenges of achieving swift diplomatic resolutions, impacting market confidence and geopolitical stability.

The post GCC and UN call for US-Iran ceasefire as market shows skepticism: FT appeared first on Crypto Briefing.

The low odds of a ceasefire highlight the challenges of diplomatic efforts and the potential for prolonged instability in the region.

The post GCC and UN call for immediate ceasefire in US-Israel-Iran conflict appeared first on Crypto Briefing.

The airstrike's escalation could lead to increased geopolitical tensions, impacting global markets and international diplomatic relations.

The post Airstrike on Iranian site raises odds of US ground forces entering Iran to 66% appeared first on Crypto Briefing.

Iran's military escalation diminishes diplomatic prospects, impacting market confidence and increasing geopolitical tensions in the region.

The post Iran escalates military actions, reducing US-Iran ceasefire odds to 1% by April 7 appeared first on Crypto Briefing.

Escalating tensions and military actions diminish prospects for peace, necessitating significant diplomatic efforts to alter current trajectories.

The post Ceasefire odds drop sharply amid escalating Iran conflict and missile strikes: FT appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

![]()

How Real Is The Quantum Threat?

A new panel has officially been announced to take place at Bitcoin 2026 titled “How Real Is The Quantum Threat?” The conversation will bring together five voices at the center of one of the most actively debated technical questions in Bitcoin today, and the lineup reflects the full range of perspectives the topic demands.

The panel features:

Hunter Beast, a senior protocol engineer for the Anduro sidechain platform incubated by MARA, is the co-author of BIP 360, a proposal that establishes a new Bitcoin wallet address type designed to protect the network from quantum computing threats. BIP 360 was merged into the Bitcoin Core BIP repository in February 2026 and was deployed on the Bitcoin Quantum Testnet v0.3.0 in March, marking significant advancements towards upgrading Bitcoin.

James O’Beirne has been a Bitcoin Core contributor since 2015 and leads multiple projects including OP_VAULT (BIP-345) and assumeutxo, having previously worked at Chaincode Labs.

Brandon Black is a Bitcoin software engineer who has spoken publicly on why quantum computing timelines are often misunderstood by the broader market.

Charles Edwards of Capriole has argued that quantum computing is advancing faster than anticipated and has advocated for a 2026 BIP-360 implementation.

Alex Thorn, head of research at Galaxy Digital, has taken a more measured position arguing the quantum threat to Bitcoin is real but limited today, affecting only certain exposed wallets, and that developers are actively building pathways to address it over time.

The panel will cover one of the most actively discussed technical topics in Bitcoin today — how quantum computing is developing, where Bitcoin’s cryptography stands, and what the path to long-term protocol resilience looks like. Developers are already working on multiple solutions, including quantum-resistant addresses and phased upgrade proposals, and this panel brings together some of the brightest minds working on these upgrades. It takes place April 29 on the Nakamoto Stage at Bitcoin 2026, The Venetian Resort, Las Vegas.

— The Bitcoin Conference (@TheBitcoinConf) March 31, 2026

PANEL ANNOUNCEMENT: "HOW REAL IS THE QUANTUM THREAT?"

This conversation will explore the state of quantum technology, the resilience of Bitcoin’s cryptography, and potential paths to safeguard the protocol in the long term.

APRIL 29 • NAKAMOTO STAGE • BE THEREpic.twitter.com/Vdpm2IlSSh

Bitcoin 2026 is Returning to Las Vegas

Bitcoin 2026 will take place April 27–29 at The Venetian, Las Vegas, and is expected to be the biggest Bitcoin event of the year.

Focused on the future of money, Bitcoin 2026 will bring together Bitcoin builders, investors, miners, policymakers, technologists, and newcomers from around the world. The event will feature a wide range of pass types, including general admission passes designed specifically for those new to Bitcoin, alongside premium passes for professionals, enterprises, and institutions.

With multiple stages, immersive experiences, technical workshops, and headline keynotes, Bitcoin 2026 is designed to serve both first-time attendees and long-time Bitcoiners shaping the next era of global adoption.

Past Bitcoin Conferences in the U.S.

Bitcoin’s flagship conference has scaled dramatically over the past five years:

- 2021 – Miami: 11,000 attendees

- 2022 – Miami: 26,000 attendees

- 2023 – Miami: 15,000 attendees

- 2024 – Nashville: 22,000 attendees

- 2025 – Las Vegas: 35,000 attendees

Get Your Bitcoin 2026 Pass

Get Your Bitcoin 2026 Pass

Bitcoin Magazine readers can save 10% on Bitcoin 2026 tickets using code ‘ARTICLE10‘ at checkout.

Stay at The official hotel of Bitcoin 2026, The Venetian, and get a guaranteed low rate plus 15% off your pass. Be in the middle of where the fun is all happening, and where the networking never ends.

And don’t forget:

Volunteer at Bitcoin 2026 and get Pro Pass access plus exclusive perks.

All students ages 13+ can apply for a Student Pass and get free general admission access to Bitcoin 2026.

Location: The Venetian, Las Vegas

Location: The Venetian, Las Vegas Dates: April 27–29, 2026

Dates: April 27–29, 2026

For more information and exclusive offers, visit the Bitcoin Conference on X here.

Why Attend Bitcoin 2026?

Bitcoin 2026 is the definitive gathering for anyone serious about the future of money. With 500+ speakers, multiple world-class stages, and programming spanning Bitcoin fundamentals, open-source development, enterprise adoption, mining, energy, AI, policy, and culture, the conference brings every corner of the Bitcoin ecosystem together under one roof.

From headline keynotes on the Nakamoto Stage to deep technical sessions for builders, institutional strategy discussions for enterprises, and beginner-friendly Bitcoin 101 education, Bitcoin 2026 is designed for everyone—from first-time attendees to the leaders shaping Bitcoin’s global adoption.

Whether you’re looking to learn, build, invest, network, or influence, Bitcoin 2026 is where Bitcoin’s next chapter is written.

Bitcoin 2026 Pass Types: Something for Everyone

Bitcoin 2026 offers a range of pass options designed to meet the needs of newcomers, professionals, enterprises, and high-net-worth Bitcoiners alike.

Bitcoin 2026 General Admission Pass

Ideal for newcomers and those looking to experience the heart of the conference.

- Limited access on Days 2 & 3

- Entry to Main Stage

- Access to Genesis Stage

- Full access to the Expo Hall

Bitcoin 2026 Pro Pass

Designed for professionals, operators, and serious Bitcoin participants.

Includes all General Admission features, plus:

- Full 3-day access, including Pro Day

- Entry to the Pro Pass Reception

- Access to Enterprise Hall, Enterprise Stage, and Networking Lounge

- Conference App networking features

- Access to the Bitcoin For Corporations Symposium

- Entry to Compute Village and Energy Stage

- Complimentary lunch, coffee, tea, and snacks

- Dedicated registration and check-in

- Reserved seating at Main Stage

- Huge savings when you bundle your hotel and Pro Pass

Bitcoin 2026 Whale Pass

Bitcoin 2026 Whale Pass

The all-inclusive, premium Bitcoin 2026 experience.

Includes all Pro Pass features, plus:

- Reserved seating at Main Stage

- All-inclusive gourmet food and beverages

- Entry to Whale Night and Whale Reception

- Access to all official after-parties

- Networking app access to connect with other Whales

- Premium access to The Deep — an exclusive networking lounge with intimate speaker sessions

- Complimentary stay at The Venetian when you bundle your whale pass and hotel (use promo code ‘WHALEHOTEL’ here)

This is the most immersive way to experience Bitcoin 2026.

Bitcoin 2026 After Hours Pass

Bitcoin 2026 After Hours Pass

Your ticket to the night.

Most deals are done with a drink in your hand. Get exclusive access to 3 official Bitcoin 2026 after-parties across Las Vegas — each with a 2-hour open bar — where the real conversations happen and the best connections are made.

- Access to 3 official Bitcoin 2026 after-parties

- 2-hour open bar at each event

- Evening events across Las Vegas, April 27–29

- Network with Bitcoiners, builders, and industry leaders after hours

More headline speaker announcements are coming soon.

Don’t miss Bitcoin 2026.

This post How Real Is The Quantum Threat? first appeared on Bitcoin Magazine and is written by Jenna Montgomery.

Bitcoin Magazine

MARA Conducts Ongoing Layoffs Following $1.1B Bitcoin Sale and Debt Reduction Push

Bitcoin miner MARA Holdings has begun a series of company-wide layoffs affecting multiple departments, according to reporting from Blockspace Media, marking the latest shift in the firm’s broader restructuring strategy.

Sources familiar with the matter said the layoffs have been “ongoing” and executed in a piecemeal fashion, with at least two rounds taking place this week on Wednesday and Thursday. The total number of employees impacted — as well as the percentage of the workforce affected — has not been disclosed, and the company has not publicly commented on the cuts.

The workforce reduction comes just days after MARA completed a major balance sheet restructuring that involved selling 15,133 bitcoin for approximately $1.1 billion between March 4 and March 25. The proceeds were used to repurchase portions of its outstanding 0.00% convertible senior notes due in 2030 and 2031, allowing the company to retire debt at an average discount of roughly 9% to par.

In total, MARA repurchased $367.5 million of its 2030 notes for $322.9 million and $633.4 million of its 2031 notes for $589.9 million. The transactions are expected to generate approximately $88.1 million in cash savings and reduce the company’s total convertible debt by about 30%, from roughly $3.3 billion to $2.3 billion.

Following the repurchases, MARA now has $632.5 million in 2030 notes and $291.6 million in 2031 notes remaining outstanding. Other tranches of convertible debt — including $48.1 million due in 2026, $300 million due in 2031, and $1.025 billion due in 2032 — remain unchanged.

CEO Fred Thiel previously framed the bitcoin sale as part of a deliberate capital allocation strategy aimed at strengthening the company’s balance sheet while preserving long-term shareholder value. He said the move would improve financial flexibility and position the firm for expansion beyond traditional bitcoin mining.

Bitcoin miners are pivoting to AI

That expansion includes a growing focus on artificial intelligence and high-performance computing (HPC), areas where MARA is seeking to leverage its expertise in energy infrastructure and data center operations. The company has increasingly positioned itself as a digital energy and compute provider, rather than a pure-play bitcoin miner.

As part of this shift, MARA has also signaled that selling bitcoin could become a recurring element of its treasury strategy. The company stated it plans to sell BTC “from time to time” throughout 2026 to support liquidity needs and fund corporate initiatives.

The developments come amid a challenging environment for bitcoin miners, who are navigating tighter margins, rising competition, and increasing pressure to diversify revenue streams beyond block rewards.

For MARA, the combination of debt reduction, bitcoin sales, and workforce cuts signals a company in transition — prioritizing balance sheet strength and strategic repositioning as it moves deeper into AI and energy infrastructure.

This post MARA Conducts Ongoing Layoffs Following $1.1B Bitcoin Sale and Debt Reduction Push first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Coinbase Receives Conditional OCC Approval to Form National Trust Company

Coinbase has received conditional approval from the Office of the Comptroller of the Currency to establish Coinbase National Trust Company, according to a statement from the company.

The approval marks a regulatory milestone for Coinbase as it expands its federally supervised custody and market infrastructure operations.

The company emphasized that the approval does not authorize it to operate as a commercial bank. Coinbase stated it will not take retail deposits or engage in fractional reserve banking. Instead, the charter is intended to provide federal oversight for its custody business, which the firm says has been a core part of its operations for years.

Under the conditional approval framework, Coinbase will be required to meet specified regulatory conditions before the charter becomes fully operational. The company said it intends to use the structure to bring uniform federal standards to its digital asset custody services and related institutional infrastructure.

Coinbase framed the decision as validation of its long-standing approach of working within the U.S. regulatory system. The company said it has invested heavily in compliance and engagement with regulators and views the approval as part of a broader evolution in how digital asset firms interface with federal banking supervision.

The charter is expected to provide clearer regulatory consistency across jurisdictions, particularly for institutional custody services. Coinbase said it believes the structure could support future expansion into additional financial services, including payments-related products, while remaining within the bounds of trust company oversight.

OCC is adopting pro-crypto activities

Over the past year, federal banking regulators have taken a more active role in defining the perimeter of digital asset activities within the traditional financial system. The Office of the Comptroller of the Currency has issued updated guidance on how banks may engage with cryptocurrency custody, stablecoin-related services, and blockchain infrastructure, while continuing to evaluate applications from crypto-native firms seeking trust or banking charters.

Industry participants have pursued federal charters in part to reduce reliance on a patchwork of state licensing regimes and to gain clearer access to national banking rails. Trust bank structures, in particular, have become a focal point for firms seeking to offer custody services without engaging in lending or deposit-taking activities.

The OCC has adapted to institutional interest in regulated custody models and the growing overlap between traditional financial infrastructure and digital asset firms. Exchanges, custodians, and fintech firms have got federal oversight and support for institutional adoption and reduce regulatory uncertainty.

At the same time, policymakers have debated how far federal banking regulators should extend oversight into crypto-native business models, particularly as stablecoins and tokenized assets continue to integrate into payments and settlement systems.

The conditional approval for Coinbase’s trust charter reflects this broader regulatory shift toward structured supervision rather than ad hoc enforcement.

If finalized, Coinbase’s national trust status would place it among a small number of crypto-linked firms operating under direct federal trust oversight, signaling continued convergence between digital asset infrastructure and the U.S. regulated banking system.

This post Coinbase Receives Conditional OCC Approval to Form National Trust Company first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Wall Street Firms and Crypto Companies to Review New Market Structure Proposal in Private Sessions

Crypto and banking industry representatives are set to review a revised stablecoin yield proposal crafted by Senators Thom Tillis and Angela Alsobrooks this week, as lawmakers attempt to break a months-long lobbying standoff over how — or whether — stablecoin issuers should be allowed to offer yield.

According to reporting from Politico, a small group of crypto firms and Wall Street institutions will privately review the updated legislative text over the next two days, with crypto companies expected to see the language as early as Thursday and banks on Friday.

The process remains tightly controlled, with stakeholders permitted to view the draft only in restricted settings and barred from taking copies.

The revised proposal follows a series of staff-level negotiations between industry groups and Senate offices aimed at narrowing disagreements over stablecoin yield provisions. While some participants hope the latest draft will serve as a near-final compromise, it remains unclear whether either side will accept the terms as currently written.

Clarity Act and crypto talks are ongoing

The renewed review of a stablecoin yield proposal comes amid a broader effort in Congress to resolve one of the most contested issues in U.S. crypto regulation: whether stablecoin issuers should be permitted to offer yield-bearing products.

Stablecoins — digital tokens typically pegged to the U.S. dollar and backed by cash and short-term securities — have become a core settlement layer in crypto markets, but their regulatory status remains unsettled, particularly around interest and yield.

The fight over a U.S. crypto market-structure bill stems from a broader effort to build on 2025’s landmark stablecoin legislation, the GENIUS Act, which established a federal framework for stablecoins — requiring full backing, transparency and reserve disclosures for digital dollars.

That law was widely seen in the crypto industry as a breakthrough for regulatory clarity while attempting to align digital assets with traditional financial standards.

After the GENIUS Act’s passage, the Senate turned its attention to more expansive digital asset oversight through what’s often referred to as the CLARITY Act or the crypto market-structure bill.

This legislation aims to define how U.S. regulators would police and oversee trading platforms, tokens, custody services and other infrastructure — essentially the backbone of a regulated digital asset ecosystem.

However, negotiations bogged down over one central issue: whether regulated exchanges should be allowed to offer yield-bearing rewards on stablecoin holdings.

Banks and major financial institutions argue that these rewards resemble unregulated deposit-like products that could siphon funds away from FDIC-insured accounts, potentially threatening lending and financial stability.

Crypto firms — including major issuers like Circle and Coinbase — counter that such incentives are crucial for competitive markets and for user adoption of digital money.

The current tentative deal being negotiated between senators and the White House seeks a middle ground — potentially allowing activity-based rewards while restricting passive yield — in hopes of unlocking Senate committee action by April. Whether that compromise holds both bank and crypto support will be decisive for the future of U.S. digital asset regulation.

This post Wall Street Firms and Crypto Companies to Review New Market Structure Proposal in Private Sessions first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

LNVPN Rebrands to Nadanada.me as Privacy Infrastructure Expands with Anonymous eSIMs and Lightning Payments

Offering anonymous eSIM data plans in over 200 countries, disposable and rental phone numbers for SMS verification, WireGuard VPN access and anonymous AI chat tools, LNVPN has outgrown its original brand. The company has grown into a full-spectrum privacy infrastructure service.

The company started in 2022 as LNVPN. It began as a proof-of-concept Lightning Network VPN built for the Oslo Freedom Forum after Alex Gladstein asked the team to create a Lightning-enabled VPN for activists in oppressive regimes. The original focus was short-term VPN access paid with Lightning, allowing users to buy service by the hour or day instead of monthly subscriptions.

The service grew quickly. Users liked the flexibility of short-term access without accounts or contracts. In 2023 the company won a price in the 2023 bolt.fun hackathon and added SMS verification services. Users pay a Lightning invoice for a disposable phone number and receive a one-time confirmation code. The system uses HODL invoices so that if the code does not arrive the payment is refunded automatically.

The company later introduced eSIM data plans available in more than 200 countries. Customers buy fixed data bundles that can activate anonymously. Rental phone numbers followed last November. These let users rent a unique phone number for three, six or nine months to receive unlimited SMS messages without creating an account. At present the rental numbers are available only in the United Kingdom, with United States numbers planned for May. The team also launched anonymous AI chat services that require no sign-up or login and are free to use.

The name nadanada.me comes from the Spanish phrase for “nothing at all.” As the company stated, “What do we know about our users? Nada. What do we log? Nada. The name is the promise.”

This approach stands in contrast to traditional service providers that collect large amounts of user data, a practice that has led to repeated large-scale breaches at major corporations and government contractors.

In November 2025, analytics provider Mixpanel was hacked, exposing names, email addresses and approximate location data of some OpenAI API users. In early 2025, U.S. government contractor Conduent suffered a ransomware attack that compromised personal and health records of more than 25 million Americans. In January 2026, cryptocurrency hardware wallet maker Ledger reported that customer names and contact information were exposed through a breach at its third-party payment processor Global-e. Such incidents frequently enable identity theft, as stolen personal details like names, emails, addresses and health or financial records can be used to open fraudulent accounts, file fake tax returns or impersonate victims.

Nadanada.me represents a new generation of privacy services integrated with Lightning in pay-as-you-go models that leave no trace on the financial system or the blockchain, in defense of user privacy.

This post LNVPN Rebrands to Nadanada.me as Privacy Infrastructure Expands with Anonymous eSIMs and Lightning Payments first appeared on Bitcoin Magazine and is written by Juan Galt.

CryptoSlate

Bitcoin becomes the live market over Easter as oil shocks hit and traditional finance goes dark

The Bitcoin market now has three trading days where it will act as the live venue for geopolitical risk while much of traditional finance is closed.

As of Friday, April 3, Wall Street is closed for Good Friday; several other markets are shut or thinner than normal; and the macro backdrop has become harder, rather than easier, to price.

Iran launched missiles and drones at Israel and the Gulf states. Fires were reported at Kuwait’s Mina al-Ahmadi refinery. The Strait of Hormuz remains the central transmission line through which geopolitical risk is moving into oil, inflation expectations, and broader macro sensitivity.

At the same time, WTI surged 11.4% to $111.54, and Brent rose 7.8% to $109.03 in the latest repricing move.

Bitcoin, by contrast, remains open and is still clearing over $33 billion in volume over the last 24 hours.

It is trading around $67,150 after an intraday range of roughly $65,780 to $67,373.

Availability has become part of the market structure

Throughout 2026, Bitcoin has functioned less like a thesis trade and more like a weekend stress monitor.

So what happens when the world gets a fresh geopolitical shock, oil gaps higher, and many of the usual venues for price discovery are closed for a long weekend?

Put simply, Bitcoin’s role here comes from availability rather than ideology.

When cash equities are closed, parts of the commodities complex are offline, and broader liquidity is fragmented by a holiday calendar, Bitcoin becomes one of the few major liquid assets still offering continuous two-way pricing.

In that sense, the market is using BTC as an immediate expression of changing sentiment.

Thin conditions can amplify moves. Crypto-native positioning can distort the signal. Weekend liquidity is not weekday liquidity. But none of that erases the core point.

If the next leg of geopolitical stress lands while traditional markets are dark, Bitcoin may be the first place investors see an immediate price response rather than the last place they confirm it.

The transmission mechanism is oil, and then rates, inflation expectations, and the dollar.

Oil first, then rates, then validation

That ladder matters. First comes the direct energy shock. Then comes the inflation read-through. Then comes the policy question.

If oil remains elevated because the Strait of Hormuz stays constrained or infrastructure damage widens, the inflation impulse becomes harder to dismiss as temporary.

That can move yields. It can support the dollar. It can also remove some of the macro oxygen that speculative assets need.

Bitcoin sits inside that chain whether crypto investors want it to or not. The move in crude is the mechanism through which geopolitical stress becomes a financing and liquidity question for the wider market.

In that sense, BTC is trading the same macro regime that households, bond markets, and central banks are trying to map. No single directional verdict follows automatically for Bitcoin.

If oil keeps repricing higher and the market starts to harden again around a higher-for-longer policy, BTC will have to show it can absorb a tougher liquidity backdrop rather than merely survive a geopolitical shock.

Holiday calendars are usually treated as scheduling details. This time, they are part of the structure, with a split between assets that can update instantly and those that cannot.

In closure windows, Bitcoin serves as a temporary price-discovery layer for global stress, even if it is not the final destination for defensive capital.

That is a narrower and more defensible claim than saying BTC leads all other markets.

Monday’s reopening can always revise the message.

Equity futures can reopen in a different register. Oil can extend or retrace. Bond desks can reset the macro interpretation. But the availability premium still carries weight.

An open market has the first chance to express fear, relief, or confusion. This weekend, Bitcoin plays a more prominent role in that function than ever before. Even after multiple weekends of Bitcoin absorbing geopolitical developments.

The macro complication is that the geopolitical picture is landing into scheduled economic risk rather than replacing it.

The U.S. March jobs report is due Friday morning, with economists looking for a modest rebound after February’s weather- and strike-distorted weakness.

ADP showed 62,000 private-sector jobs added in March, which is not hot enough to settle the policy debate but not weak enough to clear it either.

Fabian Dori, CIO at Sygnum Bank, told CryptoSlate,

“With US equity markets closed for Good Friday, price discovery indications will be delegated to on-chain markets such as Hyperliquid, or be deferred in traditional markets until Sunday night futures and Monday’s open.

This means traditional markets will need to digest any significant miss or beat simultaneously with the weekend's geopolitical developments tied to the ongoing conflict in Iran.”

That leaves Bitcoin trading into a layered setup.

First, there is a live war risk. Second, there is a live oil shock. Third, there is an incoming labor print that could still affect how quickly the market relaxes on rates.

That is what makes the current weekend different from a routine risk-off spell.

What Bitcoin is showing now, and what still needs confirmation

Bitcoin around $67,000 is a dangerous level for such a potentially volatile long weekend.

BTC has already absorbed a material oil repricing move, a worsening geopolitical backdrop, and the closure of major traditional venues without losing continuous market function.

Bitcoin is acting as an open circuit for macro stress at a moment when other circuits are partially unavailable.

Being an open circuit does not make BTC a safe haven, a superior hedging tool, or predictive in any strong causal sense.

It does mean the asset is temporarily serving a role that goes beyond the usual crypto narrative. It is one of the few major markets still speaking.

The clear way to assess Bitcoin over Easter is through three layers: availability, transmission, and validation.

| Layer | What it shows now | Why it matters |

|---|---|---|

| Availability | Bitcoin is still trading while many traditional markets are closed or thinner than normal | It becomes an immediate venue for price expression |

| Transmission | War risk is moving through oil and Hormuz, not through fear alone | That links BTC to inflation, yields, and liquidity conditions |

| Validation | Monday’s reopening and the post-jobs cross-asset reaction will test whether Bitcoin’s market signal was durable | The first move has value, but acceptance carries more weight |

The framework is historical first and causal second.

It organizes the next 48 to 72 hours without pretending Bitcoin has become an oracle for all global assets.

First comes the live signal. Then comes the cross-asset confirmation. Then comes the question of whether the move will be accepted once the full market returns.

Bitcoin will likely trade reactively to developments around Iran, Hormuz, and oil, while investors treat the market action as an early signal rather than a settled verdict.

If there is de-escalation or at least stabilization from some relief around Gulf infrastructure, fewer signs of direct spillover, and an oil market that stops repricing upward in an orderly fashion, then Bitcoin’s resilience through the closure window could be constructive rather than fragile.

However, if the conflict expands further, refinery damage worsens, or the NATO call on opening the Strait of Hormuz by force goes badly, the market may spend the weekend repricing in light of a more durable inflation shock.

In that environment, Bitcoin faces the harder test. It would have to trade through a rising oil regime and a tightening macro backdrop simultaneously.

That leaves the next test unchanged. The first move will have value, but acceptance on Monday carries more weight.

If Bitcoin continues to absorb the Easter weekend stress while oil, war risk, and the jobs narrative stay unresolved, the market will use BTC price as a barometer for Monday's open. However, anything that happens this weekend could easily be reversed and repriced within moments of Monday's pre-market open.

Until then, the market is left trading signals without confirmation, more of a placeholder than a conclusion.

The question is whether Bitcoin is delivering something real, or just leaving a trail of clues for others to interpret, like an Easter bunny that may or may not have actually passed through.

The post Bitcoin is the financial Easter Bunny this weekend as markets close Friday amid critical jobs report appeared first on CryptoSlate.

XRP is in its deepest losing streak in more than a decade, even as Ripple aggressively expands into corporate finance and institutional infrastructure. The disconnect is forcing a key market question: why isn’t that momentum showing up in price?

XRP price is in its longest losing streak since 2014, a slide that has left one of the market’s oldest large-cap tokens searching for a fresh catalyst even as Ripple accelerates its push into corporate treasury, institutional trading, and cross-border payments.

Why this matters: Ripple is moving XRP closer to real financial workflows rather than speculative use. If treasury systems, trading desks, and payment networks begin integrating the asset at scale, it could change how demand forms. For now, the market is treating that transition as unproven.

According to Cryptorank data, the token has fallen for six straight months since October 2025, losing an average of about 10% each month and shedding more than 55% over that period, trading at $1.33 as of press time.

This represents the longest stretch of monthly declines for XRP since a seven-month skid from December 2013 through June 2014, when it lost an average of 27% per month.

Meanwhile, the current downturn has come during a broader risk-off period across digital assets. Bitcoin has retreated from a peak above $126,000 to around $66,000, dragging sentiment lower across the market and leaving traders less willing to chase assets that lack a clear near-term driver.

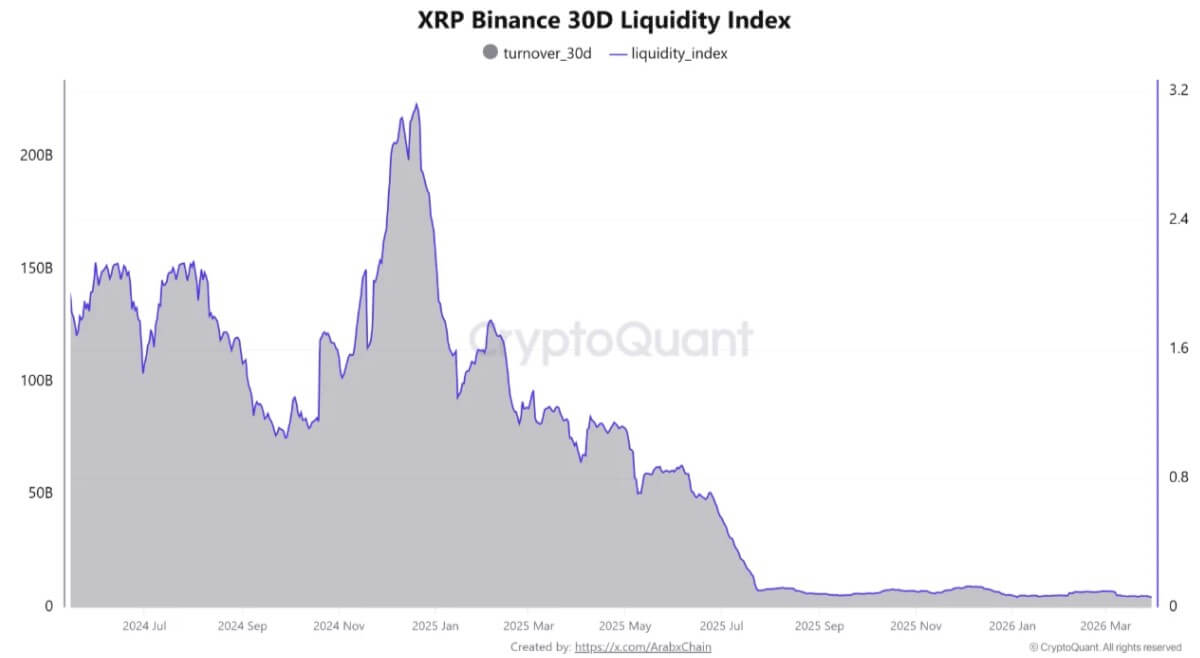

For XRP, the weakness has been compounded by softer market activity. Data from CryptoQuant showed the token’s 30-day liquidity index on Binance fell to about 0.062, one of the lowest readings in recent periods, while the 30-day turnover index stood at about $4.46 billion.

Together, those figures point to thinner order books, lighter participation, and a market that is more vulnerable to sharp price swings when larger trades hit.

That backdrop helps explain why Ripple’s latest corporate and institutional advances are drawing renewed attention.

The company is expanding quickly across treasury management, prime brokerage, payments, and tokenized financial infrastructure, and the question facing the market is whether those gains can eventually translate into stronger demand, deeper liquidity, and a firmer narrative for XRP.

XRP enters corporate treasury workflows

Ripple’s latest move is to place digital assets directly within the software used by corporate finance teams, an area long dominated by fiat-only systems.

On April 1, the company introduced Digital Asset Accounts and Unified Treasury inside GTreasury, the enterprise treasury management platform it acquired in 2025.

The system processed $13 trillion in payments volume last year for clients ranging from small businesses to Fortune 500 companies, giving Ripple an established corporate channel rather than a new one built from scratch.

Digital Asset Accounts allow treasury teams to hold, view, and manage XRP, RLUSD stablecoin, and other supported tokens alongside traditional cash balances inside the same platform.

According to the firm, positions are shown with live fiat valuations, while transactions are recorded automatically with native token amounts, fiat equivalents, and the market price at the time of each event.

Ripple said the system also captures balances to 15 decimal places, aligning internal records more closely with on-chain activity.

On the other hand, unified Treasury extends that approach by linking digital asset holdings from multiple custodians through the same API layer already used for bank connectivity.

For finance teams, this promises a way to bring digital assets into existing approval, reporting, and compliance processes without forcing a separate operational setup.

Renaat Ver Eecke, senior vice president at Ripple Treasury, said the additions give the office of the CFO “a trusted, single place to hold and manage both digital and fiat assets.” He added that Ripple plans to connect that setup to its payments network and prime brokerage capabilities for cross-border settlement and yield generation.

The timing is notable. Ripple’s 2026 survey of more than 1,000 global finance leaders found that 72% said they need a digital asset solution to remain competitive, but many still lack a practical way to integrate that exposure into treasury operations.

By placing XRP within a system used by the CFO's office, Ripple is trying to make the token part of routine corporate finance infrastructure rather than a stand-alone crypto allocation.

Ripple expands its market stack with Hyperliquid

Meanwhile, Ripple is also widening its footprint in institutional trading, a second front that could help strengthen the network around XRP even if the effect on the token is not immediate.

Ripple Prime, the company’s institutional trading platform, extended its HyperliquidX integration to include HIP-3 assets, opening access to on-chain perpetual contracts tied to traditional assets such as gold, silver, and oil.

The offering gives institutional clients exposure to decentralized derivatives through a framework that sits alongside more familiar portfolio and collateral management tools.

The pitch is operational simplicity. Institutions can manage these positions without handling separate Web3 wallets, fragmented collateral pools, or direct smart contract interaction.

Notably, Ripple Prime initially integrated with Hyperliquid in February 2026, becoming the sole counterparty for clients seeking access to the venue’s on-chain crypto liquidity.

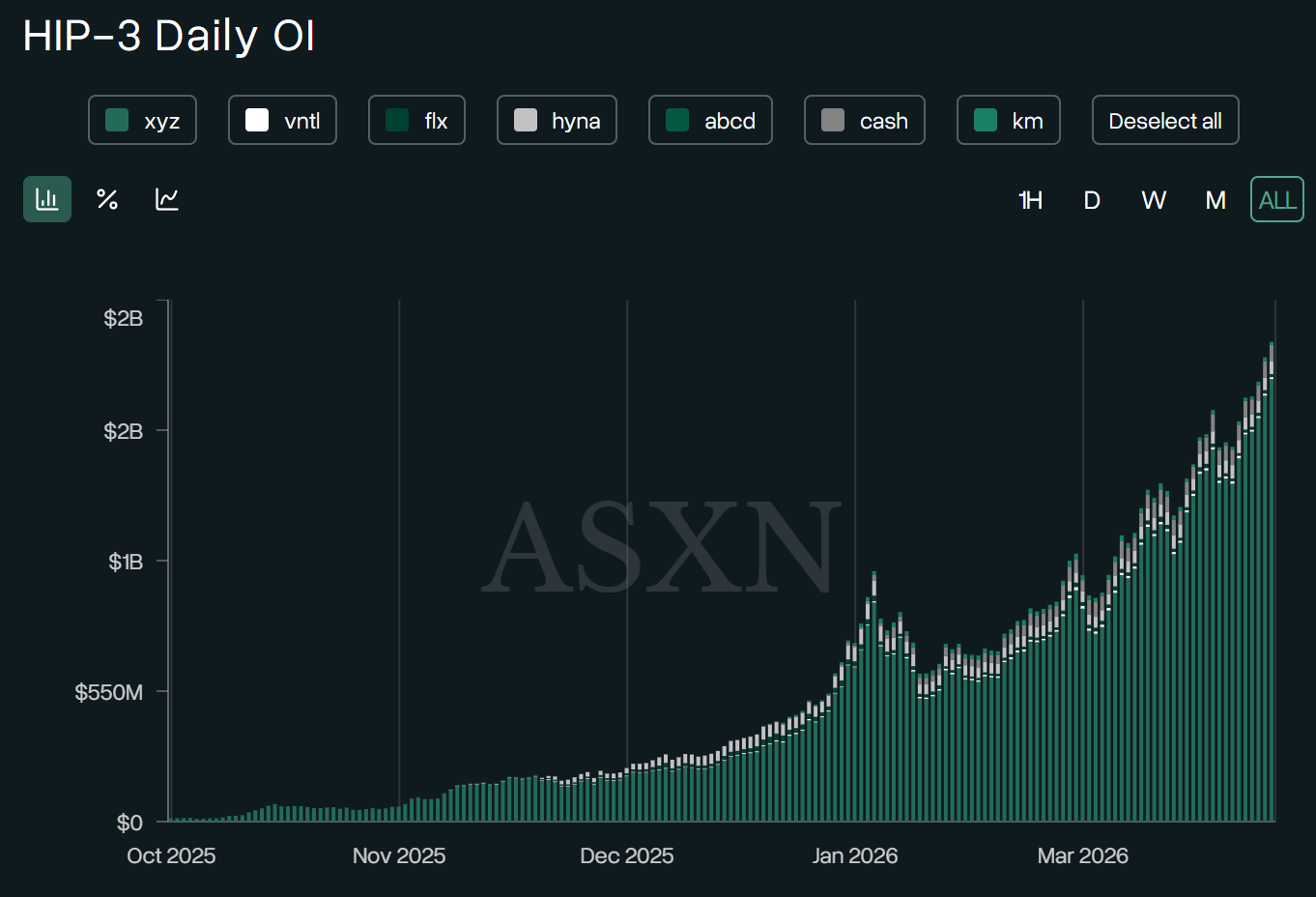

That integration comes as Hyperliquid has grown into the largest decentralized perpetuals platform, with more than $5 billion in open interest and monthly trading volume that regularly exceeds $200 billion.

Data from ASXN shows that HIP-3 daily volume has topped $2 billion, with open interest at $2 billion, and that only seven of Hyperliquid’s top 30 markets are crypto pairs.

Against this backdrop, those steps suggest Ripple is building a broader trading and brokerage stack around digital assets, one designed to appeal to clients who want regulated access to blockchain-based markets without abandoning traditional portfolio structures.

Payments, stablecoins, and permissioned finance

The third leg of Ripple’s expansion is payments, where the company is increasingly tying together RLUSD, XRPL, and its enterprise network.

Ripple Labs and Convera said this week they will work together to improve global payments using stablecoin and blockchain infrastructure. Convera, formerly Western Union Business Solutions, operates across about 200 countries and territories and supports more than 140 currencies.

The partnership is centered on a “stablecoin sandwich” model in which transactions begin and end in fiat, while stablecoins are used in the middle of the payment flow.

That model fits Ripple’s broader strategy as stablecoins move deeper into mainstream finance. Stablecoins processed $33 trillion in volume last year, up 72% from 2024, but only a small share of that activity has so far been tied to practical payment functions such as payroll, treasury transfers, and remittances.

Ripple is also extending that strategy into public-private financial infrastructure. Last week, the company joined the Monetary Authority of Singapore’s BLOOM initiative to test programmable cross-border trade settlement using the XRP Ledger (XRPL) and RLUSD.

At the same time, XRPL is being adapted for more regulated institutional use through permissioned domains and a permissioned decentralized exchange, tools designed to create controlled venues where access can be limited through credentials and compliance checks.

The common thread is clear. Ripple is trying to position XRPL and its stablecoin infrastructure as part of a regulated operating layer for moving money, managing liquidity, and settling value across borders.

Can Ripple’s momentum lift XRP?

That still leaves the central market question unanswered. Ripple’s business is broadening, but XRP remains under pressure.

The token’s weak liquidity and lower turnover suggest that market participants have yet to treat Ripple’s expansion as a decisive reason to reprice XRP higher.

In part, that reflects the distinction investors continue to make between Ripple’s enterprise progress and the token’s direct utility. Treasury integration, brokerage services, and stablecoin partnerships can strengthen the company’s strategic position without immediately changing spot demand for XRP.

Even so, the longer-term case is that these efforts could deepen the conditions XRP needs to recover. More treasury usage can increase familiarity with the asset inside corporate finance. Broader institutional access can improve market structure. Greater use of XRPL and RLUSD in payments and settlement can reinforce the network’s relevance at a time when tokenized money movement is becoming more competitive.

Bitrue Research argued that XRP is expanding beyond its legacy payments identity into a broader stack that includes stablecoins, decentralized finance, sidechains, and cross-chain settlement.

The firm outlined a base case that could see XRP rise to $2.00 by September, with a stronger scenario of $2.50 if RLUSD adoption accelerates, XRPFi expands, and regulation becomes more supportive.

For now, those targets remain a forward bet rather than a confirmed shift. XRP is still in its deepest losing run in more than a decade.

However, as Ripple pushes deeper into treasury management, institutional trading, and regulated payment infrastructure, the market is being forced to consider whether the company’s gains can eventually become the token’s turning point.

The post XRP’s longest slump in a decade collides with Ripple’s $13 trillion institutional push appeared first on CryptoSlate.

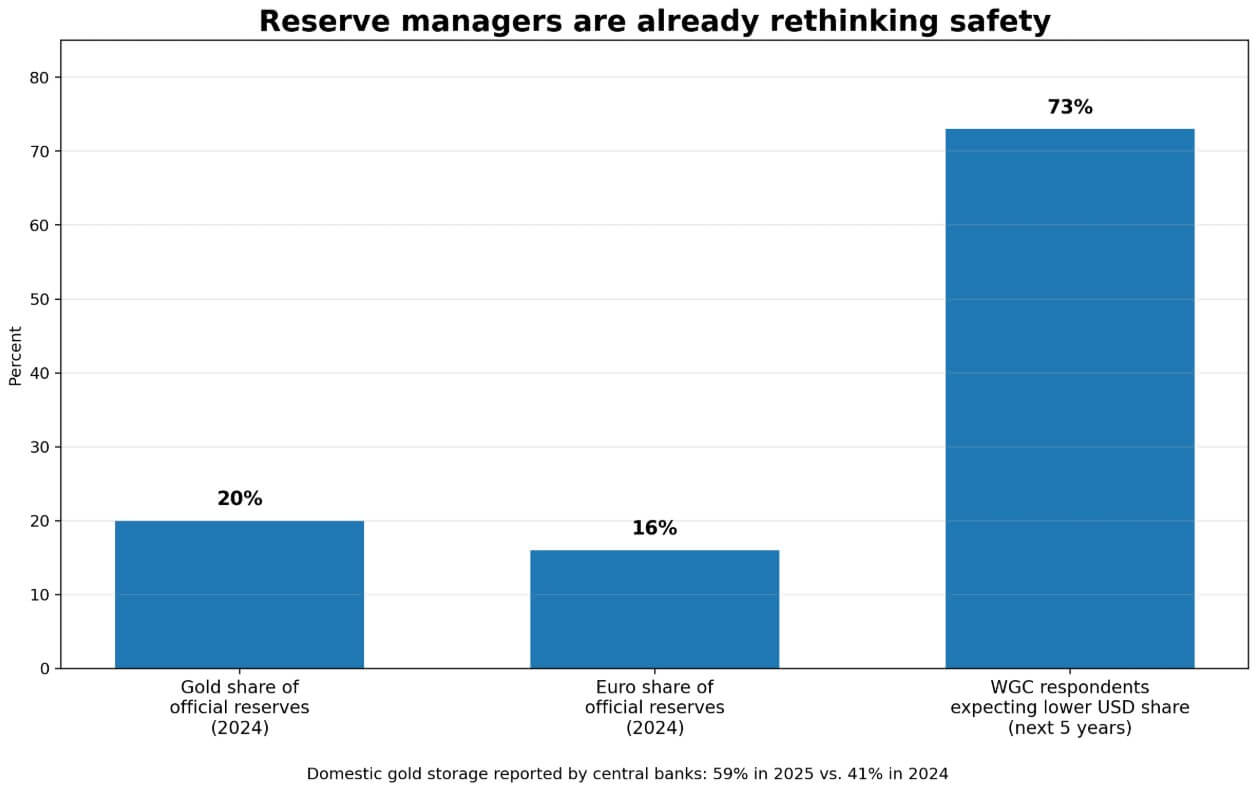

A new sovereign-reserve argument is gaining traction: an asset does not truly function as a reserve if it cannot be accessed during a crisis. That shift is pushing Bitcoin into policy debate not as a growth bet, but as a hedge against sanctions, custody risk, and geopolitical disruption.

A recent paper by the Bitcoin Policy Institute on Taiwan opens with a familiar argument that the country's reserves are overconcentrated in dollars. Gold underperforms its potential, and Bitcoin could complement both.

Readers who stop there miss the more consequential claim buried in the blockade-and-invasion framework on pages 5 through 7, where the paper is trying to redefine what makes a reserve asset fail.

Traditional reserve analysis judges assets on liquidity, price stability, and credit quality. The BPI paper adds a fourth test: can the asset still be moved, spent, or mobilized when shipping lanes are blocked, the host state withdraws custodial access, or another state becomes politically hostile?

By that measure, gold can be stranded, dollar reserves can become conditional, and Bitcoin can stay electronically portable regardless of physical access or diplomatic standing.

That is a larger conceptual move than advocating for a Taiwanese BTC position.

Why this matters: Reserve policy is no longer just about returns, liquidity, or stability in normal conditions. If governments begin treating access under stress as a core reserve test, Bitcoin moves closer to the discussion as a contingency asset rather than a speculative one.

From macro bet to sovereignty insurance

For years, the state-level Bitcoin argument ran on a single track: hedge monetary debasement, diversify reserves, capture upside from adoption momentum.

That argument still appears in the BPI paper, particularly in its pages on US debt accumulation and the Federal Reserve's balance sheet expansion. The more original contribution sits elsewhere, where the paper ranks reserve assets by whether they stay accessible under coercion.

A government only needs to accept that Treasuries, correspondent banking networks, physically stored metal, and foreign sovereign paper each carry distinct dependencies.

The policy question centers on which asset stays reachable when custody, transport, or host-country politics go wrong.

Official reserve behavior already confirms that framing extends well beyond Bitcoin advocates. The IMF reports that total international reserves, including gold, reached 12.5 trillion SDR at the end of 2024.

The ECB reported that gold's share of global official reserves reached 20% by market value in 2024, surpassing the euro's 16%, and that central banks bought more than 1,000 tonnes that year.

The World Gold Council's 2025 survey found 73% of respondents expect lower US dollar holdings in global reserves over the next five years, and the share of central banks reporting domestic gold storage jumped to 59% from 41% a year earlier.

Reserve managers are already broadening the definition of reserve risk, and the BPI paper extends that logic to Bitcoin.

| Asset | Normal-times strength | Crisis vulnerability | Failure mode under stress | Why it matters in the article |

|---|---|---|---|---|

| U.S. dollar reserves / Treasuries | Deep liquidity, high credit quality, global reserve standard | Can become politically constrained by host-country policy, sanctions, or custodial leverage | Freeze / conditional access / political pressure | Shows that a reserve can remain “safe” on paper but become less usable in practice |

| Gold | Longstanding reserve ballast, inflation hedge, widely accepted by official institutions | Hard to move quickly, physically trappable, vulnerable to seizure or transport bottlenecks | Stranding / seizure / logistics failure | Explains why portability and physical control now matter more in reserve analysis |

| Bitcoin | Digitally portable, bearer-like, can be moved without shipping lanes or physical transport | High volatility, governance burden, limited official-sector acceptability | Institutional reluctance / policy hesitation, rather than physical immobilization | Enters the story as a potential asset of last-resort accessibility rather than a conventional safe reserve |

| Diversified non-dollar sovereign paper | Reduces reliance on a single reserve issuer, still fits conventional reserve frameworks | Still depends on external sovereign systems, settlement infrastructure, and market access | External dependency / reduced neutrality | Serves as the bear-case alternative: reserve managers may prefer this over BTC even after accepting access risk |

| Domestically vaulted gold | Improves control over custody while preserving gold’s reserve role | Still suffers from transport friction and limited portability in acute crises | Mobility constraint rather than pure custody risk | Shows why gold can benefit from the same access-risk logic without fully solving it |

This is the real shift underneath the debate: reserve assets can still look safe on paper while becoming harder to use in practice. Once that gap enters policy thinking, Bitcoin is being evaluated less against return and more against access.

The live evidence for access risk

The access-risk argument draws force from concrete recent events.

In March, Russia's central bank challenged the EU freeze affecting approximately $300 billion in sovereign funds. That dispute keeps the central premise operational: reserve assets can become politically immobilized while retaining their face value.

An asset owned on paper yet frozen in practice has already failed as a reserve, regardless of its credit rating.

Brazil's central bank drew a parallel conclusion. On Mar. 31, Brazil lifted gold's share of reserves to 7.19% from 3.55% in a single year, while cutting the US dollar share to 72, citing diversification as the driver.

The BPI paper argues Bitcoin belongs in that same diversification calculus, specifically for reserve decisions driven by geopolitical logic.

The US Strategic Bitcoin Reserve adds a distinct data point. The White House order prioritizes the reserve with forfeited BTC, prohibits outright sale, and contemplates additional acquisition only on a budget-neutral basis.

That pulls Bitcoin reserve language into an actual sovereign administrative structure, setting a precedent regardless of its unconventional funding source.

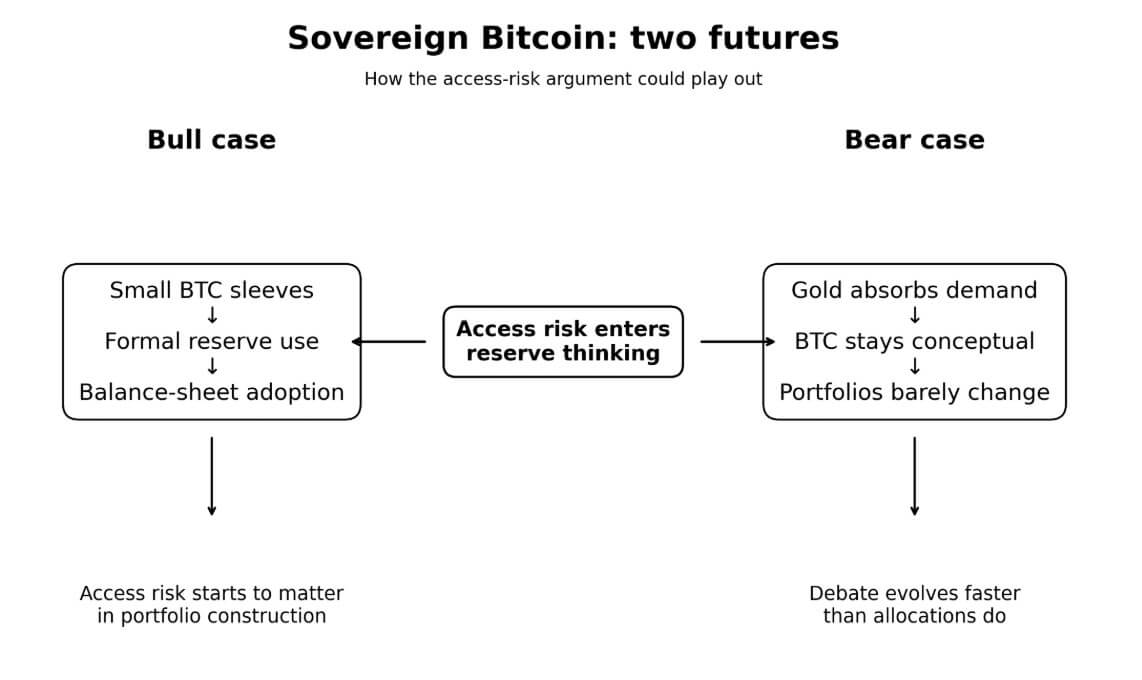

Two futures for the sovereign Bitcoin argument

Scale makes the bull case concrete. Taiwan's reserves total roughly $602 billion, and a 1% Bitcoin sleeve would be about $6 billion, while a 5% sleeve would be $30 billion.

The broader math is starker: 0.1% of global reserves, roughly $16.25 billion, would represent about 1.2% of Bitcoin's entire market cap at current prices near $68,000.

Reserve system participation, even at a marginal scale, would have price consequences well before any central bank made a headline allocation decision.

The bull case requires a handful of politically exposed or sanctions-conscious states first to formalize small BTC positions in the 0.25% to 1% range, or to treat already-held seized or mined Bitcoin as a reserve asset before buying more.

Ferranti's sanctions risk modeling supports the direction: in one sanctions scenario, his model produces an optimal Bitcoin share of around 5% for exposed sovereigns. The sovereign Bitcoin discourse would then move from advocacy papers to actual balance sheet entries.

The bear case accepts the access risk critique and still concludes that Bitcoin loses.

Reserve managers acknowledge that physical gold carries logistical dependencies and that dollar reserves carry political ones, and then decide that Bitcoin's volatility, governance burden, and near-zero official-sector acceptability make it a weaker hold than domestically vaulted gold and diversified non-dollar sovereign paper.

Gold absorbs the diversification demand that the access-risk argument was supposed to generate for BTC, and Bitcoin's role as a reserve asset stays conceptual. The debate evolves while portfolios hold their composition.

Where the argument holds and where it strains

The BPI paper is strongest when it treats portability and seizure resistance as genuine reserve characteristics, grounded in observable reserve behavior.

That framing tracks official data: geopolitics now visibly influences reserve composition, and the desire to hold assets outside concentrated single-counterparty dependency is real and already moving portfolios.

The paper overreaches when adoption momentum or price appreciation enters as evidence that the policy case is settled. Official institutions still weigh acceptability, legal clarity, and operational habit alongside access risk, and those factors carry weight that portability rankings leave unaddressed.

The most credible version of the paper's argument is its own stated position: Bitcoin as a small insurance sleeve alongside gold, optimized for access.

For most of Bitcoin's history as a reserve policy topic, the central question in official circles was whether Bitcoin was safe enough to hold. That framing consistently disadvantaged BTC because its volatility kept it below Treasuries and gold on every conventional measure.

Reserve managers are now focused on which assets stay deployable in the event of a hostile geopolitical environment. Gold's resurgence, domestic vaulting preferences, sanctions-driven reserve disputes, and payment-infrastructure fragmentation all show that reserve managers are already seeking conventional assets.

Bitcoin advocates are inserting BTC into that same conversation, and the BPI paper shows how that argument works at its most sophisticated.

The next test is whether this logic stays confined to papers and strategic rhetoric or begins to alter real reserve behavior. If even a small number of geopolitically exposed states start treating access risk as a formal reserve criterion, Bitcoin moves from theoretical hedge to policy variable, and that would matter well beyond Taiwan.

The post Sanctions risk is forcing a rethink of reserve safety — and Bitcoin is now in the debate appeared first on CryptoSlate.

XRP is entering a more revealing phase of the cycle. The token’s core pitch is that global payment stress should make its cross-border use case more valuable, yet the latest oil shock and dollar rebound are still pushing it to trade like a conventional risk asset.

XRP enters an identity crisis as oil, inflation fears, and dollar strength hit the market all at once

The market is now forcing that contradiction into the open, turning XRP from a narrative-driven trade into a real-time test of whether its utility can translate into price under macro stress.

CryptoSlate has already tracked institutional migration into Ripple-linked products, ETF resilience tied to Ripple’s expanding footprint, and the growing tension between XRPL adoption and token value capture. The setup has now tightened.

A sharp overnight jump in oil, stronger dollar conditions, and renewed inflation anxiety have pulled XRP into a macro test that feels more direct than the themes that carried it through the first quarter.

That shift came quickly. Following President Donald Trump’s latest remarks on Iran, AP reported that oil surged more than 6%, while a separate market wrap from Business Insider put Brent near $108.

Brent crude pushed to roughly $108, the U.S. Dollar Index climbed back to about 100, and Bitcoin slid toward $66,666.

XRP price held near $1.35 to $1.36, according to CryptoSlate data, though the weekly move still carried visible pressure. 24-hour volume is near $1.32 billion.

Why this matters: XRP’s core pitch hinges on stress in the global financial system. If higher costs, tighter liquidity, and cross-border friction are increasing, the token should be moving closer to its use-case value. Instead, it is still reacting like a high-beta asset, which raises a more practical question for investors: when does utility start to matter in price?

The connection to XRP runs deeper than broad crypto weakness. Bitcoin usually absorbs the first layer of geopolitical and liquidity shock. XRP sits closer to the payment, liquidity, and settlement conversation.

Ripple has spent months building that frame. The company’s GTreasury acquisition and subsequent Ripple Treasury launch widened its reach into corporate cash management, while earlier reporting on Ripple’s trust-bank ambitions and broader licensing footprint gave XRP holders a practical reason to view the asset through a financial-infrastructure lens.

That lens now cuts both ways. When oil climbs, freight and energy input costs rise, and inflation expectations stiffen, the case for faster, cheaper movement of money gains urgency.

The same macro shock also boosts the dollar, tightens financial conditions, and usually pushes risk assets into a tougher zone. XRP now sits at the intersection of those two forces.

The tension is direct because it touches household budgets, portfolio drawdowns, and the cost of moving capital across borders.

Oil and the dollar have turned XRP’s payments pitch into a real-time stress test

XRP’s use-case narrative has always leaned on efficiency. Cross-border transfers, on-demand liquidity, and enterprise settlement create a cleaner economic pitch when payment rails are under strain.

That pitch becomes easier to grasp during a week when the world suddenly has to price a higher energy bill, a firmer dollar, and the risk of another inflation impulse. The macro map on the chart is blunt.

Brent jumped, DXY rose, and Bitcoin rolled over. XRP followed the pressure lower through the week, even though its long-term pitch should, in theory, become more relevant as global money flows grow more expensive and more fragile.

That contradiction is the center of the setup. XRP rallied for much of this cycle on the idea that Ripple’s regulated expansion, enterprise positioning, and capital-market traction were building a more durable floor under the token.

CryptoSlate covered that process through pieces on institutional DeFi ambitions, legacy financial integration, and recent ETF flow softening. Those themes still carry weight.

They now face a harder question. If a stronger dollar and higher oil create deeper friction across the global economy, why has XRP behaved like a pressured altcoin instead of a market leader?

That is the real split now confronting XRP. Ripple’s business narrative points toward infrastructure relevance, but the token is still being priced by traders as exposure to tighter liquidity and weaker risk appetite.

Part of the answer sits in the liquidity hierarchy. Bitcoin still commands the first response in macro stress, because it carries the deepest liquidity, the broadest institutional recognition, and the strongest reflex move during periods of geopolitical uncertainty.

XRP has a narrower lane. It needs investors to believe that utility can translate into token demand on a timeline that the market can price.

That challenge has shown up repeatedly in the split between Ripple’s business traction and XRPL activity and on XRP’s amplified beta during broad crypto drawdowns. The current move forces that same issue into a macro context.

Ripple can broaden into custody, treasury management, and regulated financial software, yet XRP still trades within a market structure that responds quickly to dollar strength and falling crypto risk appetite.

Bitcoin spent the last several sessions slipping back toward the mid-$66,000s, a visible loss of altitude from the higher zones traders had defended earlier in the week.

The dollar index reclaimed the 100 handle, a psychological level that usually feeds tighter global liquidity conditions. Brent then accelerated back above $108. XRP held around the mid-$1.30s.

That set of moves creates a clean economic message. Payment friction may be rising in the real world, but capital is still seeking safety before it seeks efficiency.

For XRP, that leaves the asset in an identity crisis. Its strongest fundamental narrative says a fractured, expensive, slow-moving global financial system should increase the value of its use case.

Its current market behavior suggests investors still classify it as part of the higher-beta branch of crypto exposure.

The coming macro calendar will press on XRP’s weakest seam

The coming week further compresses the issue, as the macro calendar offers three direct tests. The Bureau of Labor Statistics employment report arrives on Friday, April 3.

The Federal Reserve’s April calendar shows the minutes from the March 17-18 FOMC meeting arriving on Wednesday, April 8. The BLS release calendar then places March CPI on Friday, April 10.

Those releases land directly on top of the new oil shock. They will shape whether markets see the latest rise in energy as a temporary disruption or the start of another inflation leg that keeps policy tighter for longer.

XRP’s response to that sequence could define the next phase of its cycle. A hotter payrolls print would strengthen the view that labor conditions remain firm enough to keep the Federal Reserve cautious.

Hawkish signals in the minutes would add another layer of restraint. A hotter CPI print next Friday would confirm that the oil move has arrived inside an already sensitive inflation backdrop.

That combination usually supports the dollar and squeezes speculative assets. XRP would then enter a zone where every part of its identity gets tested at once.

The company behind it has spent months expanding its institutional reach. The token itself would still need to show that investors are willing to price it as a beneficiary of payment-system stress.

There is a sharper retail hook inside that setup. Many people understand inflation as the price of groceries, gasoline, travel, and borrowing.

Far fewer think about what a stronger dollar and higher energy costs do to cross-border settlements, corporate treasury decisions, and the movement of liquidity through financial rails. Ripple’s own enterprise push, as reflected in its treasury platform strategy, brings XRP closer to that conversation, whether the token captures all the value today or not.

That gap between corporate utility and token pricing is where the emotional trigger sits. People with market exposure can see oil jumping and Bitcoin sliding.

They can see the dollar catching a bid. The harder question then comes into focus: if the world is becoming more expensive and more fragmented, why is the best-known payments token still struggling to trade like a payment asset?

The answer over the next week may come down to acceptance levels in price and acceptance levels in narrative. If oil cools, DXY softens, and payrolls or CPI relieve some pressure, XRP has room to reclaim its enterprise-infrastructure frame, especially with Ripple’s broader footprint still giving investors a structural reason to stay engaged.

If oil holds firm, the dollar extends, and inflation anxiety deepens, XRP may keep trading as macro beta first and payments infrastructure second. That outcome would widen the contradiction between Ripple’s strategic progress and the token’s market role.

It would also leave holders facing a more uncomfortable conclusion. XRP has spent years being sold as a bridge asset for an imperfect global financial system.

The next move matters less as a one-day price reaction than as a classification test. If the coming payrolls, Fed minutes, and CPI sequence keeps the dollar elevated and pressure on risk assets, XRP will have to prove it can hold an infrastructure narrative when macro conditions turn hostile. If it cannot, the market may be forced to admit that Ripple’s strategic progress and XRP’s price identity are still not the same trade.

The post Oil, dollar strength, and inflation fears are exposing XRP’s biggest market contradiction appeared first on CryptoSlate.

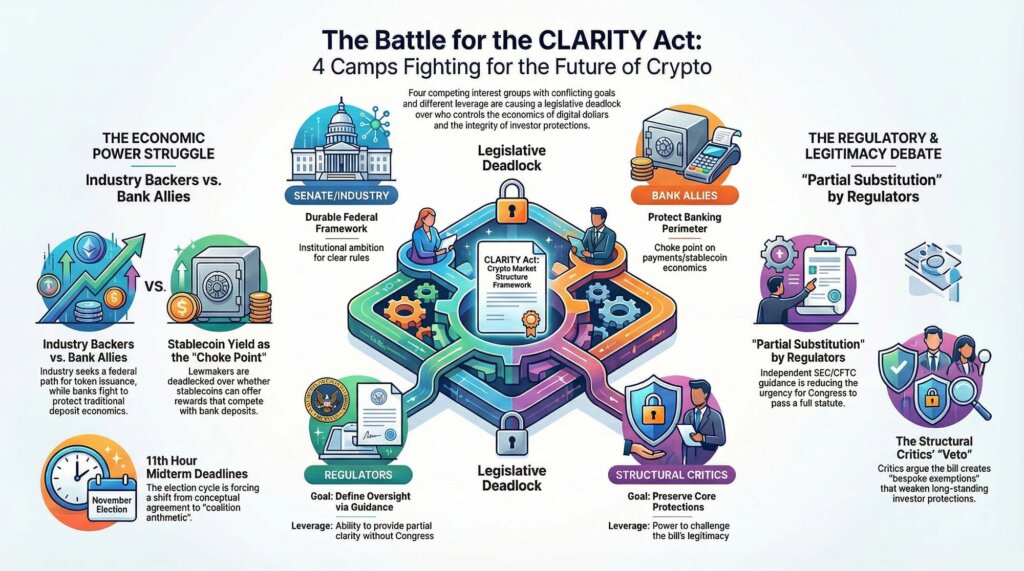

The CLARITY Act entered Washington as a bid to impose a durable market structure on crypto. It now sits at the center of a four-way fight over who gets to define that structure, who gets paid inside it, who supervises it, and how much of the existing financial rulebook survives the rewrite.

The bill still includes broad language for jurisdictional clarity, with the Senate Banking Committee majority outlining a framework that draws lines between the SEC and the CFTC while adding tailored disclosures and anti-fraud protections.

Around that frame, the coalition has fractured into four camps with different definitions of success. Senate and industry backers still want a federal market-structure bill that gives crypto firms a workable path into US regulation.

Bank-aligned critics want to seal off stablecoin yield and keep deposit economics from migrating out of the banking system. Regulators have begun moving through their own channels, with the SEC and CFTC signing a new memorandum of understanding and the SEC issuing a fresh interpretation of crypto assets that begins to deliver some of the clarity Congress had reserved for itself.

Structural critics still argue the bill would carve crypto out of core investor protections, a case advanced by groups such as Better Markets and by former CFTC Chair Timothy Massad in prior congressional testimony.

That collision changed the shape of the bill. What began as a question of statutory design has become a contest over bargaining power.

Each camp can slow the process, each camp can claim some version of consumer protection, and each camp enters the next phase with a different source of leverage. Senate and industry backers hold the broadest institutional ambition.

Why this matters: The CLARITY Act was intended to anchor crypto within US law, with clear rules for exchanges, tokens, and custody. If it stalls or narrows, firms remain in a patchwork regime shaped by enforcement and agency guidance, while banks retain tighter control over dollar-based financial activity. The outcome will determine whether crypto can compete directly with traditional deposits and payment rails, or operate inside a more constrained perimeter.

Banks and their allies hold a choke point around payments, economics, and stablecoin rewards. Regulators hold the power of partial substitution, because every piece of interpretive guidance from the SEC and CFTC narrows the pool of uncertainty that once made CLARITY the singular prize.

Structural critics hold a veto over the debate on legitimacy because their argument speaks to a long-standing Washington fear that crypto bills could create bespoke exemptions that would replace the exemptions older laws once carried.

The calendar tightened the pressure. In January, Senate Banking Chairman Tim Scott said the committee would postpone its markup while bipartisan negotiations continued.

Later that month, the Senate Agriculture Committee advanced related market-structure legislation, keeping momentum alive while underlining that the main bottleneck had shifted into the negotiating room.

By March, the fight over stablecoin rewards had become the central pressure point in the bill, with public reporting and congressional chatter converging on the same conclusion: a framework bill could move forward only if lawmakers found a way to reconcile crypto’s push for broader utility with banking concerns about disintermediation and deposit competition.

That left CLARITY in a familiar Washington posture, broad enough to attract coalitions in theory, specific enough to trigger fracture once the revenue lines came into view.

The first two camps are fighting over the economic core of the bill. The first camp still sees CLARITY as the vehicle that can finally anchor crypto market structure in federal statute.

That camp includes Senate Republicans who have spent months arguing that the industry needs rules written through Congress rather than through case-by-case enforcement, along with a large swath of the industry that wants a lawful path for token issuance, exchange activity, brokerage, custody, and participation in decentralized networks.

The core attraction has always been the same. A federal framework promises a clearer allocation of authority among agencies, a more predictable compliance process, and a narrower zone of ambiguity about what falls under securities law and what falls under commodities regulation.

The Senate Banking majority’s summary reflects that approach, leaning on the idea that a single framework can impose definitional order on a market that has spent years operating inside regulatory overlap.

For crypto firms, the appeal runs deeper than process. A statute holds out the prospect of capital formation under rules that institutions can underwrite, boards can sign off on, and legal teams can defend without having to rebuild the analysis around every enforcement cycle.

Yield politics turned CLARITY into a fight over the economics of digital dollars

The first camp’s ambition runs straight into the second camp, which has focused the fight around stablecoin yield and the economics of digital dollars. The Bank Policy Institute has made the bank-aligned position unusually plain.

Lawmakers, in that view, need to prevent stablecoin structures from recreating deposit-like products outside the traditional banking perimeter, especially if those products begin passing through rewards or yield that look and feel like interest. Under that logic, the danger is structural.

If tokenized dollars can offer returns or functionally similar incentives at scale, then commercial bank deposits face a new form of competition, payments activity migrates, and the prudential perimeter gets thinner exactly where regulators spent years trying to harden it. That is why the stablecoin rewards fight turned into the bill’s main choke point.

It is the place where market structure meets balance-sheet politics.

Those two camps can still describe their goals with overlapping language. Both can say they want consumer protection, operational integrity, and a framework that channels crypto activity into supervised forms.

The overlap ends when the discussion reaches who captures the economics created by digital dollars. The industry camp wants enough room for product development, distribution, and economic pass-through to make federally compliant crypto businesses worth building.

The bank-aligned camp wants a bright barrier around any feature set that could pull value from deposits into tokenized alternatives. That conflict reaches beyond one provision.

It shapes how lawmakers think about payments, exchange design, brokerage economics, wallet architecture, and the degree of freedom crypto firms would have to compete with institutions that already dominate dollar intermediation. Every concession made to one side tends to drain utility from the bill as imagined by the other.

The result is a negotiation whose formal subject is market structure and whose real center of gravity is control over monetary rails. That is why this phase of the CLARITY debate feels more compressed and more political than the earlier debate over jurisdiction.

Jurisdiction can be split in text. Economic control creates winners and losers with organized lobbies, committee relationships, and a direct financial interest in the final wording.

The first camp still wants a durable federal framework. The second camp wants that framework shaped tightly enough that it does not redraw the economics of digital money in a way that benefits crypto firms at the expense of banks.

Both camps can live with progress. Each one defines progress differently, and that difference is what keeps the bill from moving forward.

The third camp sits within the regulatory apparatus itself and introduced a fresh complication into the bill by moving ahead with practical coordination and interpretive guidance. On March 11, the SEC and CFTC announced a new memorandum of understanding designed to improve coordination on crypto oversight.

Days later, on March 17, the SEC issued a new interpretation clarifying how federal securities laws apply to crypto assets, with the CFTC aligning publicly with the effort. By March 20, the CFTC had added crypto-related FAQs that continued the same line of work.

Those actions did not write a statute, and they did not resolve every contested edge case, yet they changed the terrain around CLARITY in a way lawmakers can feel. Congress had been negotiating a bill designed to provide clarity.

Regulators started supplying pieces of that clarity themselves.

Regulators are shaping the field while structural critics keep the legitimacy fight alive

That shift created two immediate effects. First, it gave industry participants some of the operational breathing room they had been seeking, particularly regarding how certain crypto activities are analyzed through the lens of securities law.

Legal practitioners quickly seized on the importance of the change. In a March 19 analysis, Katten described the SEC and CFTC guidance as a major event for the sector, pointing to a more legible treatment of activities such as airdrops, mining, staking, and wrapping.

Second, the guidance changed congressional leverage. Every increment of clarity delivered through agency action reduces the urgency that once surrounded CLARITY as the exclusive route to order.

That creates a subtle but powerful dynamic. A bill under pressure usually gains energy from scarcity.

Once regulators start producing partial substitutes, lawmakers face a harder sell when they ask wavering factions to make politically costly concessions in the name of a breakthrough.

That shift does not weaken the case for statute across the board. A regulatory interpretation sits lower in the durability hierarchy than a congressional framework, and industry participants with long investment horizons still prefer statutory architecture to agency guidance.

Yet the third camp need not erase the case for CLARITY to affect the negotiation. It only needs to be shown that immediate passage is the only way to restore order.

That is already happening. The more the agencies coordinate, the easier it becomes for lawmakers to accept delay, narrower text, or a compromise version of the bill that settles the most acute fights while leaving some larger structural ambitions for another cycle.

For some senators, that can feel like prudence. For some industry players, it can feel like the center of the bill is being negotiated away in real time.

The regulatory camp also exerts pressure in a second way. It offers a political release valve.

Lawmakers who want to say Washington is making progress on crypto can point to the SEC and CFTC without forcing immediate resolution of every issue inside CLARITY. That lowers the cost of postponement and raises the threshold for what kind of final agreement is worth bringing to the floor.

A bill that once looked indispensable now has to demonstrate added value against the backdrop of agency-led adaptation. That is a difficult standard, especially for a coalition already carrying internal conflict over stablecoin rewards, federal preemption, DeFi treatment, and investor-protection language.

The fourth camp continues to ask the question that lies beneath every crypto bill in Washington: Does this framework integrate the sector into existing law, or does it carve out a special lane that weakens protections the rest of finance still carries?

That concern has animated groups such as Better Markets and has appeared in prior testimony from former CFTC Chair Timothy Massad, who argued that proposals such as CLARITY can create artificial distinctions between securities and commodities in ways that reduce the reach of investor protections.

This camp does not have to win the whole argument to shape the bill. It only has to keep the legitimacy challenge alive.

Once that challenge enters the center of the debate, every provision gets viewed through a second lens. A disclosure regime becomes a question about whether disclosure replaces stronger obligations.

A jurisdictional transfer becomes a question about whether oversight is being softened through classification. A pathway for token markets becomes a question about whether the path relies on exemptions that older sectors would never receive.

This is where the four camps collide most sharply. Senate and industry backers want a framework that firms can use at scale.

Bank-aligned critics want to close off yield dynamics that could pressure deposits and payments economics. Regulators are already showing that some clarity can emerge through agency action, reducing the pressure to accept a broad legislative bargain on weak terms.

Structural critics keep pushing on the question of whether the bill preserves the integrity of long-standing protections. A compromise that satisfies the first camp by preserving broad utility may alarm the second and fourth camps.

A compromise that satisfies the second and fourth camps by tightening the perimeter may leave the first camp with a framework that carries less strategic value. A compromise that leans heavily on regulator-led clarity may satisfy lawmakers seeking incremental progress while leaving industry participants with a less durable settlement.

That is why the final question has become a matter of coalition arithmetic rather than conceptual agreement. All four camps can say they want order.

Their conditions for the order point are in different directions.

Midterm pressure is turning a policy negotiation into coalition arithmetic

The midterm calendar sharpens every one of those contradictions. November imposes deadlines on attention, legislative bandwidth, and political appetite for complex financial legislation, generating cross-pressures within both parties.

As the calendar advances, the value of waiting rises for any camp that thinks the current bargain costs too much. Banks can wait if the alternative is stablecoin economics they dislike.

Structural critics can wait if the alternative is a framework they view as too permissive. Regulators can keep moving within their own lane.

Industry groups can keep arguing that delay carries a cost, yet that message weakens if the agencies continue to supply enough guidance to keep large parts of the market functioning.

The coalition that can pass CLARITY, therefore, needs more than a shared talking point around clarity. It needs a settlement that provides the first camp with enough usable structure, the second camp with enough protection around dollar economics, the third camp with a role that fits the statute rather than competes with it, and the fourth camp with enough assurance that core protections remain intact.

That path is narrow. It is still navigable, although the room for error has tightened.

A workable reconciliation would likely require lawmakers to frame the bill less as a maximal rewrite and more as a disciplined allocation of authority, paired with narrow guardrails on stablecoin rewards and stronger language on anti-fraud, disclosure, and supervisory obligations. Even then, the politics stay hard.

Each camp would have to accept a result that falls short of its preferred endpoint. The first camp would accept tighter limits than many crypto firms want.

The second camp would accept a federal framework that still gives compliant crypto business lines room to grow. The third camp would accept that agency guidance is a bridge into statute rather than a substitute for it.

The fourth camp would accept that integration can occur without dismantling the regulatory perimeter. Whether that bargain is possible before November is now the central test around CLARITY.

The bill can still move. The harder question is whether these four camps can converge on a version of movement that each side can live with once the votes are counted.

The post A four-way deadlock is now blocking the US Clarity Act crypto bill — and each side can stop it appeared first on CryptoSlate.

Cryptoticker

Coinbase has officially received conditional approval from the Office of the Comptroller of the Currency (OCC) to establish the Coinbase National Trust Company. This move brings the largest U.S. exchange under federal oversight, effectively bridging the gap between Silicon Valley innovation and Wall Street’s regulatory rigors.

Is Coinbase a Bank?