Cryptocurrency Posts

Crypto Briefing

The lack of a clear US strategy in the Iran conflict heightens geopolitical tensions, reducing prospects for diplomatic resolutions.

The post Criticism mounts over US strategy in Iran conflict amid strained relations appeared first on Crypto Briefing.

Market resilience suggests geopolitical tensions alone may not significantly disrupt oil prices without substantial supply threats.

The post Iran tanker seizures, Trump order fail to impact oil markets appeared first on Crypto Briefing.

Bitcoin's decline and $TRX's rise highlight shifting investor sentiment, impacting market dynamics and future cryptocurrency investment strategies.

The post Bitcoin falls 24% in Q1 2026; $TRX gains 9% appeared first on Crypto Briefing.

The Iran conflict underscores the volatility of oil markets, complicating global efforts to transition away from fossil fuels.

The post Iran conflict drives oil prices above $120 amid global fossil fuel talks appeared first on Crypto Briefing.

Solana's inflow and Bitcoin's surge highlight market volatility, suggesting traders await stronger signals for significant price movements.

The post Solana sees $31.8M inflows as Bitcoin hits $79K, April $150 target unlikely appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Strive Expands Bitcoin Treasury With $61.4 Million Purchase, Holdings Reach 14,557 BTC

Strive Inc. has expanded its Bitcoin treasury with a fresh purchase of 789 BTC valued at roughly $61.43 million. The Nasdaq-listed firm disclosed the acquisition in a recent filing, reporting an average purchase price of about $77,890 per bitcoin.

The transaction lifts Strive’s total holdings to 14,557 BTC as of April 24, 2026, with the stack valued at roughly $1.1 billion based on current market prices.

The latest buy marks a continuation of Strive’s treasury strategy, which centers Bitcoin as a core balance sheet asset rather than a peripheral allocation. The company has framed Bitcoin as a benchmark for capital deployment, positioning it as a hurdle rate for investment decisions and long-term value preservation.

The company’s accumulation comes amid an accelerating trend of corporate Bitcoin adoption. Public companies now hold more than 1.15 million BTC combined, worth an estimated $85 billion, while Bitcoin exchange-traded funds collectively control about 1.28 million BTC, Strive said.

Also today, Strategy bought 3,273 BTC for $255 million, pushing its holdings to 818,334 BTC worth about $63.7 billion while lifting its Bitcoin yield to 9.6% and reinforcing its position as the largest corporate holder.

Strive is stacking BTC

Strive’s balance sheet reflects this shift. Alongside its Bitcoin holdings, Strive reported $90.5 million in cash and cash equivalents and additional exposure to Bitcoin-linked financial instruments, including preferred equity tied to Strategy Inc. This structure indicates an effort to combine direct Bitcoin ownership with yield-generating instruments tied to the broader Bitcoin capital stack.

Strive’s recent activity builds on earlier purchases throughout 2026. In March, the company added 179 BTC, bringing its holdings at the time to over 13,000 BTC, while also expanding its exposure to structured credit products designed to support income generation tied to Bitcoin markets.a

Beyond balance sheet expansion, the company is also investing in education tied to corporate Bitcoin adoption. Its subsidiary, True North, plans to host a “Bitcoin for Business” summit in Oregon aimed at CFOs, founders, and treasury managers seeking to integrate Bitcoin into financial operations.

The initiative reflects a broader push to normalize Bitcoin within corporate finance frameworks.

In March, B. Riley Financial initiated coverage on Strategy Inc. and Strive, Inc., arguing both stocks were undervalued relative to their Bitcoin treasury holdings.

The firm pointed to compressed valuations, with Strategy trading near 1.2x NAV and ASST around 0.9x modified NAV, framing the discounts as an opportunity amid a broader pullback in Bitcoin.

This post Strive Expands Bitcoin Treasury With $61.4 Million Purchase, Holdings Reach 14,557 BTC first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Strategy (MSTR) Expands Bitcoin Holdings by $255 Million as Treasury Yield Surges to 9.6%

Strategy disclosed on April 27, 2026 that it acquired 3,273 Bitcoin for $255 million during the week ending April 26, bringing the company’s total holdings to 818,334 BTC valued at approximately $63.7 billion at current market prices.

The purchase was executed at an average price of $77,906 per Bitcoin, funded through the sale of 1.45 million shares of Class A common stock via its at-the-market (ATM) equity program.

The Virginia-based business intelligence firm reported that its Bitcoin Yield metric reached 9.6% year-to-date 2026, up from 9.5% disclosed in the prior week.

This proprietary metric measures the percentage change in the ratio between Bitcoin holdings and assumed diluted shares outstanding, providing insight into the company’s efficiency in acquiring Bitcoin relative to shareholder dilution. Strategy’s cumulative Bitcoin position carries an average acquisition cost of $75,537 per coin, representing a total investment of $61.81 billion.

Strategy now controls nearly 4% of total bitcoin supply

With 818,334 Bitcoin in its treasury, Strategy now owns approximately 3.9% of the cryptocurrency’s fixed 21 million supply cap. The latest acquisition extends the company’s position beyond the holdings of BlackRock’s iShares Bitcoin Trust (IBIT), which holds approximately 802,823 BTC.

Strategy’s Bitcoin reserves account for over 60% of all Bitcoin held by publicly traded companies worldwide, cementing its status as the dominant corporate holder of the digital asset.

The purchase represents the company’s continued execution of its Bitcoin treasury strategy under executive chairman Michael Saylor, who has stated a goal of accumulating between 5% and 7% of the total Bitcoin supply.

Funding through common stock ATM program

The $255 million purchase was financed through Strategy’s $21 billion Class A common stock ATM program, with no preferred stock issuance during the April 20-26 period.

In March 2026, the company filed to establish dual $21 billion ATM programs for both MSTR common stock and STRC preferred stock, plus an additional $2.1 billion program for STRK preferred shares, providing the firm with $42 billion in total capital-raising capacity.

The common stock ATM program allows Strategy to sell shares into the market gradually without the need for traditional equity offerings, providing flexible funding for ongoing Bitcoin acquisitions.

Strategy’s Class A common stock (MSTR) traded at $172 at the time of writing, reflecting a year-to-date gain of approximately 12.55%. However, the shares have declined roughly 47.5% to 51% over the trailing 12-month period, underperforming Bitcoin’s price movement during the same timeframe.

The stock experienced consistent monthly losses from July through December 2025, including declines of 16.78% in August, 16.36% in October, and 34.26% in November.

Despite the recent volatility, MSTR shares have delivered returns of approximately 134.9% over the past five years.

Michael Saylor, Strategy’s Founder & Executive Chairman, is speaking at The Bitcoin Conference later today and this week.

This post Strategy (MSTR) Expands Bitcoin Holdings by $255 Million as Treasury Yield Surges to 9.6% first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Satori Coin Enters U.S. Market With Physical Bitcoin Collectibles

Satori Club Pte Ltd will enter the U.S. market today, expanding access to physical Bitcoin collectibles as demand for self-custody tools grows among American users.

The Singapore-based company will align the launch with its virtual sponsorship of Bitcoin 2026 in Las Vegas. The event presence includes upcoming flyer distribution during keynote sessions, aimed at introducing attendees to its product lineup and custody model.

Satori Coin offers physical coins embedded with mechanisms that allow users to store or transfer Bitcoin in tangible form. Each product incorporates tamper-evident features and structured redemption processes designed to balance usability with security.

The current lineup reflects a staged rollout over the past year. The Satori Coin Gi, released in September 2025, serves as the flagship model and uses a 2-of-2 multi-signature design. In February 2026, the company introduced the Satori Coin Chi, positioned as an entry model that users can load after delivery. A silver version, the Satori Coin Chi Silver, features .999 fine silver construction and targets collectors seeking a premium format.

The company traces its roots to 2015 and draws on the concept of “satori,” a term associated with awakening and discovery. That theme shapes its approach to product design, which aims to make Bitcoin more accessible through physical interaction while maintaining core security principles tied to private key management.

Satori Coin first emerged in 2016 and has focused on bridging the gap between digital assets and physical ownership. The U.S. expansion reflects rising interest in self-custody following increased awareness of exchange risks and custody failures across the crypto sector.

Satori Coin products

Satori Coin offers a range of physical Bitcoin-themed collectibles designed to merge tangible craftsmanship with digital value. The lineup includes three main models: Chi, Chi Silver, and Gi, each catering to different levels of security, material quality, and Bitcoin storage capacity.

The Chi model is the entry-level option, designed to hold 0.001 BTC. It uses a single-key system concealed under a hologram and ships unloaded, with funds added after delivery. The Chi Silver version upgrades the experience with 1oz of 999 fine silver while maintaining the same Bitcoin capacity and redemption process.

At the higher end, the Gi model is built for 0.01 BTC and emphasizes security through a 2-of-2 multisig structure, where one key is held by the user. It also includes NFC functionality, allowing users to check balance and verify authenticity. Gi ships loaded and uses a dedicated redeem kit for secure transfers, positioning it as a more trustless and advanced option.

Products will be available to U.S. customers through the company’s website starting today. The launch positions Satori Coin within a niche segment that blends collectibles, hardware security, and Bitcoin education.

This post Satori Coin Enters U.S. Market With Physical Bitcoin Collectibles first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Samourai Letter #6: Two Years In

Dear Reader,

I write this letter to you before the sun has made her first appearance. The moon still reigns on this day, April 24th 2026. At this same exact time, 5:00 AM, only two years prior, my wife Lauren and I were both awaken dramatically to sirens, flashing lights, and brisk commands shouted over a megaphone.

“Keonne Rodriguez, this is the FBI, come out with your hands up IMMEDIATELY!” was repeatedly shouted. Over 50 armed FBI tactical agents pointed their assault rifles at our chests. Drones, armored vehicles, assault rifles, men dressed like GI-JOE, all swarmed the quiet humble small town where we lived. Once arrested, handcuffed, placed in the back of a police cruiser, Biden’s lackeys descended on my home like a swarm of ants hopped up on adrenaline.

The drone was flown through the house first to clear the way, the GI-JOEs followed, finally the army of blue haired DEI hires and the puny men who looked like they would be defeated by the thought of a single push-up shuffled their way in. I knew the tech team the moment I saw them.

They would be going through my hard drives and USB sticks. I was most worried about my wife who at this point was still detained in handcuffs. I was relieved when they let her leave and my worry immediately was directed toward my cat who I knew would quite happily take advantage of the hubbub and the wide open doors to go on one of her unmonitored adventures around the village.

That is how my day started on April 24, 2024. Two years later, I start my day markedly differently. I wake up at FPC Morgantown. Federal prison. I am told when I can sleep, when I can wake, when I can eat, when I can shower, what I can wear, and even to some degree what I can think.

My days are structured around shouted commands over a loud speaker and a book of regulations I am expected to follow. In prison your identity is stripped from you. In here it is ‘us and them’, convicts and guards, inmates and CO’s. Don’t get me wrong, most of the CO’s are decent enough, they are here to do a job, and they do it well. Treat them with respect and don’t mess around with contraband (mostly cellphones and vapes) and they will generally treat you well enough. But at the end of the day, they go home and you don’t. So here I am, inmate # 11404-511, a federal prisoner.

Two years ago today an overzealous and politicized FBI under corrupt leadership, under a corrupt presidential administration, acting under a corrupt Department of Justice that empowered a corrupt US Attorney that delegated authority to corrupt AUSA’s; indicted, raided, and arrested me and Bill, two American software developers. Just another two casualties in the Biden ‘War on Crypto’.

Two small fishes with no political friends or influence. Two guys who wrote software and gave away code that worked so well they had no choice but to change the rules of the game and go after us with the full force and might of the United States government.

And by God, their calculations were correct. Barely anyone cared. Bill and I couldn’t even raise enough money for our legal defense. We were left high and dry to fend for ourselves against an adversary with unlimited resources. The government took out the only effective non custodial, open source, privacy tool in the entire space and there was barely a whimper of protest. From some corners of the industry there was even celebration. This wasn’t a war on crypto, in a war both sides have a fighting chance. This was a massacre.

There is no doubt that the ‘War On Crypto’ was started and waged fiercely under Joe Biden. But Biden himself has proven to be a ship without a rudder. He was clearly a man who did not know his ass from his elbow. He was nothing more than a marionette puppet whose strings were being pulled by aides and henchmen receiving orders in secret from the likes of Elizabeth Warren and her self described ‘anti crypto army’. The War On Crypto truly belongs to her.

The Trump administration inherited this war, and won the election partly because the democrats couldn’t steal it in the same way they did in 2020 – that was a trick that would only work once – but also because Trump appealed to young men of every race.

A major reason for this appeal was 1) His promise to free Ross and 2) his promise to end the war on crypto. In many ways he has made good progress. Ross was freed as promised and the administration began to dismantle the levers of power that were the big guns in the ‘war on crypto’. The SEC was reigned in, the tide had begun to turn against the luddite candlestick makers in favor of the electric lightbulbs.

The deputy attorney general – now the acting attorney general – Todd Blanche issued a memo early in the administration intended to reign in rogue prosecutors, explaining in exquisite detail that America does not regulate by prosecution and does not hold responsible software developers for the acts of their end users. Blanche and the new administration drew a line in the sand. The war appeared to be ending.

What most people miss about this ‘War on Crypto’ is that it is not an ordinary war. It is not an us versus them war. It is very much a civil war. An us versus us war. As such, when Blanche published his memo, when Trump ordered the end of the war, the infantry on the ground tasked with obeying those orders – the line prosecutors, the AUSA’s, the army of unelected bureaucratic lifers – ignored them. Willfully and explicitly.

They continued just as they have always done, perhaps change a charge from (b) to (c), or change the language they use to make sure that they get away with blatant insubordination. The administration has been dealing with this treachery from day one, in all areas, not just crypto.

Trump identified the problem during his first term. He called it the swamp or the deep state. I call it the administrative state. The administrative state was a problem for him during his first term. It orchestrated the biggest election heist ever witnessed in 2020.

It then came after Trump attempting to put him in prison for life. And it continues today unabated during the second administration. Dismantling of the administrative state followed by the full scale liquidation of the army of apparatchiks that lord over us, will be, if he is able to achieve it, Trump’s lasting legacy.

So where do we stand now? The ‘War On Crypto’ is half won. The SEC has largely been reigned in. The DOJ under Bondi and now Blanche has not brought forward new charges under these novel theories conjured up during the last administration, so to some degree Blanche’s memo did work.

Elizabeth Warren and her ‘anti crypto army’ have decidedly lost, just as the luddites did, just as the horse carriage men protesting the automobile did. She was always going to lose, it was just about how much damage she could do on the way down. With the war half won, a problem remains, combatants have been left behind.

One of the US Military’s guiding principles is that no man gets left behind. Heaven and earth will be moved at extraordinary expense to retrieve a single American behind enemy lines (as has just been witnessed in Iran).

Well, in the ‘War on Crypto’, men have been left on the battlefield. Forgotten and left to bleed out. The war will not be won until Bill and myself are extricated from behind enemy lines.

The war will not be won until Roman Storm stops being shot at with ammunition provided by the last corrupt administration and carried forward by the wolves in the hen house of this administration. When we are all home with the threat of retribution by the most powerful and mighty state bearing down on us no longer credible, then we can celebrate the victory of this war.

Until the crypto prisoners are free, none of us are free.

Write to Keonne:

Keonne Rodriguez

11404-511

FPC Morgantown

FEDERAL PRISON CAMP

P.O. BOX 1000

MORGANTOWN, WV 26507

Mailing Guidelines:

Please note: You can only send letters (no more than 3 pages long). No packages or other items are allowed. Books, magazines, and newspapers must be sent directly from the publisher or an online retailer like Amazon. All letters must include a full return address and sender name to be delivered.

This is a guest post by Keonne Rodriguez. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This post Samourai Letter #6: Two Years In first appeared on Bitcoin Magazine and is written by Keonne Rodriguez.

Bitcoin Magazine

UTXO Management Launches Dual-Class Digital Credit Income Fund

UTXO Management, a subsidiary of Nakamoto Inc. (NASDAQ: NAKA), announced the formation of UTXO Preferred Income Strategies LP, a Delaware limited partnership structured to provide access to income from preferred digital credit securities.

The fund introduces a dual-class structure designed to serve different allocator objectives within a single vehicle.

The structure includes a Senior Income Class and a Total Return Class. The Senior Income Class targets a fixed annual coupon paid monthly as return of capital sourced from preferred dividend streams, according to a company release.

Distributions flow first to this class, ahead of fees and junior allocations. The structure seeks to deliver yield above short-term U.S. Treasury bills, supported by a junior equity cushion. This class carries no management or performance fees.

The Total Return Class targets return through residual income after senior distributions. The strategy includes disciplined leverage, relative value positioning across the preferred digital credit stack, and participation in new issuance. This class absorbs first loss and captures upside tied to spread compression and income growth.

The fund’s initial portfolio is expected to include digital credit instruments such as the Strategy Variable Rate Perpetual Stretch Preferred Security (STRC). These instruments form part of a growing segment within capital markets that blends features of fixed income with digital asset exposure.

Chief Investment Officer Tyler Evans said the digital credit market has reached a stage of development that supports structured products, though access remains limited across institutional channels.

“We designed our first structured credit product, UTXO Preferred Income Strategies LP, to give allocators access to these dividend-paying securities, with the capital structure enhancements, institutional servicing, and operational transparency they require,” Evans said.

UTXO’s expansion into credit

Since 2019, UTXO Management and its affiliates have launched and managed several investment vehicles across the Bitcoin ecosystem. These include the Bitcoin Ecosystem Fund, focused on venture investments, and 210k Capital, LP, a hedge fund strategy centered on Bitcoin and related instruments. The launch of UTXO Preferred Income Strategies LP marks the firm’s entry into structured credit, extending its platform into income-oriented strategies.

UTXO Management operates as a Bitcoin-native asset manager across public and private markets. The firm allocates capital across liquid securities, venture investments, and strategic partnerships tied to Bitcoin infrastructure and adoption. Nakamoto Inc., its parent company, holds and operates a portfolio of Bitcoin-native businesses.

The fund will be offered to accredited investors who also meet the definition of qualified purchasers under applicable securities laws. Interests will be sold through private placement and will not be registered under the Securities Act of 1933. Investment decisions must rely on the fund’s offering documents, which contain full details on terms, risks, and structure.

The strategy involves a high degree of risk. Digital credit securities face regulatory uncertainty, liquidity constraints, and valuation challenges. The fund may employ leverage, which can increase losses. The dual-class structure depends on the performance of underlying assets and the sufficiency of the junior equity layer to protect senior distributions.

No capital has been deployed under the strategy at the time of announcement. Target yield and return figures represent internal objectives based on modeled scenarios and do not constitute forecasts or guarantees. Actual performance may differ based on market conditions, issuer credit quality, and broader economic factors.

Disclaimer: Bitcoin Magazine is published by BTC Inc, a subsidiary of Nakamoto Inc. UTXO Management is also a subsidiary of Nakamoto Inc. (NASDAQ: NAKA)

This post UTXO Management Launches Dual-Class Digital Credit Income Fund first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

AAVE, the native token of the Aave DeFi platform, is now available on the Solana blockchain network.

The move will give Solana users access to one of the largest lending protocols in decentralized finance without leaving the network.

This came less than two days after the Solana Foundation revealed that it would deploy part of its treasury into Aave.

Through this action, the non-profit joined a broader industry effort to contain the fallout from the KelpDAO rsETH $292 million exploit and restore confidence in decentralized lending markets.

Solana Foundation aids Aave recovery

On April 25, Lily Liu, chair of the foundation, said the nonprofit is lending USDT to Aave to support recovery efforts after the exploit left major DeFi protocols exposed to unbacked collateral and liquidity stress.

The step marks an unusual cross-chain intervention by Solana, which has spent years building its own DeFi economy around native lending, trading, and liquid staking applications.

It also gives the foundation a direct role in a recovery effort centered on Aave, a protocol more closely associated with Ethereum and its layer-2 networks.

Liu framed the move as support for the broader open-finance market, saying blockchain economies do not operate in isolation and that Solana’s long-term health depends on a functioning DeFi sector beyond its own ecosystem.

For Solana, the intervention signals that competition among chains does not preclude coordination when a failure threatens the market structure on which they all depend.

A bridge failure becomes a DeFi problem

The April 18 $292 million exploit began with KelpDAO’s rsETH, a liquid restaking token, after attackers allegedly exploited a weakness tied to its LayerZero bridge configuration.

According to reports, the attackers were able to redeem 116,500 unbacked rsETH tokens on Ethereum before depositing the assets as collateral across Aave, Compound, and Euler, then borrowing roughly $292 million in ETH and other assets.

This action caused broader contagion, especially in Aave's lending markets, where platform users exited en masse, and resulted in WETH utilization reaching 100% within hours of the exploit.

Galaxy Research explained:

“At full utilization, Aave's design doesn't allow withdrawals, because there is no idle liquidity in the pool to redeem against. Whoever withdraws first is made whole, while whoever comes later must wait for new supply to arrive or borrowers to repay.”

Oak Research, a crypto intelligence firm, said the mass exit led to a 17% decline in total value locked in DeFi, with Aave experiencing more than $12 billion in outflows.

The firm argued the episode could have become a defining failure for DeFi because it combined a bridge misconfiguration, a systemically important lending venue, and lenders unable to withdraw funds from depleted pools.

The liquidity crunch also showed how lending protocols can operate as designed while still importing risk from outside infrastructure.

Aave pools depend on borrowers, collateral, and liquidations functioning normally. When collateral quality collapses suddenly, lenders can be left waiting for liquidity until borrowers repay, liquidations occur, or new deposits enter the market.

Can ‘DeFi United' restore investors' confidence?

In response to the incident, Aave and KelpDAO helped organize DeFi United, a recovery vehicle aimed at replenishing rsETH reserves and making affected users whole.

According to DeFi United's official website, the effort has drawn commitments of nearly $240 million from several major DeFi participants, including Aave DAO, Arbitrum DAO, Mantle, Ether.fi, Lido, Kelp, Golem Foundation, and individual contributors.

Oak Research said this recovery effort is working because Aave was the protocol at risk.

In its view, the response may have been different if the losses had been isolated to a smaller restaking protocol or a bridge without broader systemic importance. Aave, as the largest DeFi lending venue, had stronger incentives to preserve its reputation and avoid a precedent in which lenders take losses from collateral accepted by the protocol.

That is what makes Solana’s support notable. The foundation is stepping into a sector-wide effort to prevent a bridge-linked collateral failure from damaging confidence in DeFi’s largest lending venue.

The move also gives Solana a strategic opening. Bringing AAVE to Solana could deepen cross-chain liquidity, broaden access for Solana users, and give Aave another distribution channel at a time when lending protocols are reassessing collateral risk, bridge dependencies, and emergency backstops.

Meanwhile, the recovery may still leave governance questions unresolved. Aave tokenholders must weigh the cost of using treasury assets against the reputational risk of allowing users to absorb losses.

While DeFi United can help close the immediate shortfall, the KelpDAO exploit has already shown that collateral standards, bridge design, and protocol risk controls are no longer separate issues.

The post Latest $290M exploit hit DeFi so hard it forced Aave onto Solana as part of rescue efforts appeared first on CryptoSlate.

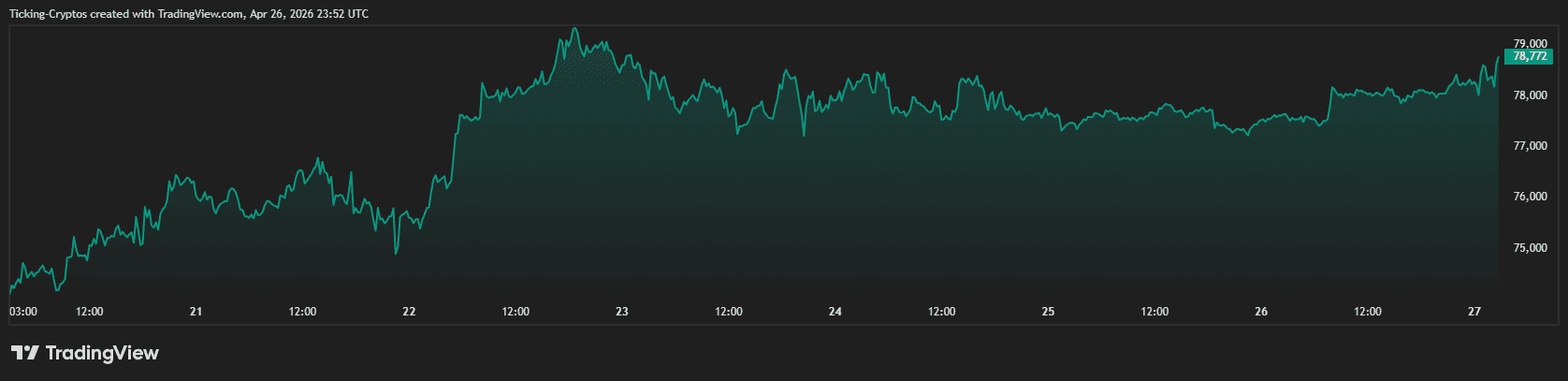

Bitcoin traded below $78,000 on Monday as EU markets opened for the week.

BTC price hit $77,819, down 0.28% over 24 hours, with a market capitalization near $1.56 trillion and 24-hour volume of around $32.1 billion. Total crypto liquidations stood near $295 million over the previous 24 hours on CoinGlass.

Bitcoin had been pressing the $80,000 decision area, then quickly slipped back under $78,000 before any clear fresh macro, regulatory, exchange, ETF, or issuer headline had emerged.

The immediate test is whether the drop was a short-lived leverage flush or the start of a broader risk-off move.

The distinction is substantive. A leverage flush can reset crowded positioning while leaving the larger market structure intact. A broader risk-off move usually needs follow-through across risk assets, weaker liquidity, or a new catalyst that changes how traders price the next several sessions.

For now, the evidence points to market structure first. Liquidation pressure was evident, the price level was fragile, but the cause has yet to be resolved into a single clear explanation.

The $80,000 area was already loaded

The latest move landed in a zone that had already drawn attention. On Apr. 23, Bitcoin traded as high as $79,470 while moving toward the $80,000 threshold, before retracing to about $78,200.

The push was linked to forced liquidations and a more constructive macro and geopolitical setup.

Bitcoin was already testing a level where recent buyers, short sellers, and macro-sensitive traders had reasons to react. When price moves into that kind of area, the first rejection often says more about positioning than conviction.

A later CryptoSlate market-structure analysis gives the same zone a more tactical map. Bitcoin had failed to hold the upper-$78,000s after reaching the $80,000 level, while risk appetite and equities were doing more immediate work than crude oil.

The same analysis placed the constructive path around a hold of the $77,000 to $77,500 area followed by a reclaim of the upper-$78,000s.

That gives Monday's move a clean test. If buyers absorb the drop near the mid-$77,000s, the decline can remain a clearing event. If price fails there, the break starts to point to a broader reduction in risk.

The pattern also helps separate price action from explanation. Traders did not need a new headline to see why stops, hedges, or fast exits could cluster around a round-number level that had just rejected momentum. A market that has challenged $80,000 can reverse quickly when leverage is high, and the next buyer is waiting for a lower price.

That makes the first response around $77,000 to $77,500 more important than the search for a tidy headline. A fast reclaim would show demand absorbing forced flows. A stalled bounce would tell traders that the drop was spilling into spot conviction and broader risk appetite.

Recent CryptoSlate coverage explains why the $80,000 zone was crowded, why liquidations had helped shape the prior move, and why risk appetite could influence the next leg. It leaves the Apr. 27 drawdown as a live test, rather than a settled reaction to one event.

That framing separates the level from the narrative. The price zone can be real, and the catalyst can remain unresolved. Bitcoin had a clear technical pressure point, while the available evidence still leaves the trigger open.

Liquidations define what the evidence can support

The liquidation data adds pressure to that interpretation. Total crypto liquidations reached about $294.9 million over 24 hours, up sharply from the prior reading on the page.

CoinGlass also showed 89,011 traders liquidated and the largest single order on Binance's ETHUSDT pair at about $11.98 million.

The Bitcoin-specific page was more nuanced. BTC liquidations were about $95.55 million, split between about $38.8 million in longs and $56.75 million in shorts.

That split complicates the easy version of the move. A falling Bitcoin price often invites a simple long-liquidation explanation. The BTC-specific reading was short-heavy at the time checked, which suggests the liquidation backdrop was mixed and not a one-direction wipeout.

Still, liquidations were large enough to show forced position closure across the market, while the Bitcoin page showed activity clustered around the same hours as the European open. That supports a leverage and liquidity frame, with the immediate trigger still unresolved.

Market-cap data sets a second boundary. Global crypto market capitalization is near $2.59 trillion, and Bitcoin's dominance was around 60%. CryptoSlate's coins page shows Bitcoin's market capitalization is around $1.559 trillion.

Macro pressure sets the next test

The macro backdrop gives the move context. The Federal Reserve calendar shows a two-day FOMC meeting scheduled for Apr. 28 and 29, with a press conference on Apr. 29.

A separate Federal Reserve notice shows an Apr. 28 closed Board meeting to discuss monetary policy issues.

CryptoSlate's macro preview also framed the week as unusually compressed. Traders would get the Fed first, then GDP and PCE data shortly after, creating a tight test for rates, growth, inflation, and risk appetite.

That setup can explain why buyers may be less willing to step in aggressively. Bitcoin often trades as a liquidity-sensitive asset over short macro windows. When the market is heading into a packed policy and data sequence, traders have fewer reasons to add risk into a fast drop.

Still, the calendar is background pressure. During the Apr. 27 review window, no new Fed decision, fresh inflation print, regulatory action, exchange failure, ETF shock, or issuer announcement had emerged to explain the move.

The market had a plausible reason to be cautious, while the visible move looked more consistent with positioning and liquidity stress than a fully explained headline response.

The most defensible reading is that Bitcoin's drop below $78,000 looks like a leverage flush inside a risk-sensitive market, with no obvious fresh catalyst. That holds if the move stabilizes near the mid-$77,000s and buyers can push price back toward the upper-$78,000s.

A reclaim would suggest the market cleared excess exposure while preserving the larger range. It would also fit the pattern CryptoSlate mapped earlier: hold the $77,000 to $77,500 area, regain the upper-$78,000s, and put $80,000 back into play.

A deeper break would change the question. If Bitcoin loses the mid-$77,000s while equities weaken, yields firm, or the Fed week turns more hostile for risk assets, the same liquidation data would begin to resemble the first leg of a broader risk reduction.

That leaves the market with a precise test. The liquidation wave has shown where leverage was vulnerable. The next price reaction will show whether spot demand is strong enough to absorb the damage.

The post Bitcoin flash crashes below $78,000 at Europe market open with nearly $295 million in crypto liquidations appeared first on CryptoSlate.

The Bitcoin ETF trade sold investors a simple promise: crypto exposure inside a wrapper that looked and felt like mainstream finance. Advisors could buy it, compliance teams could understand it, and institutions could route capital into digital assets through a product that fits the rest of their strategy.

That promise worked, and the US spot Bitcoin ETF complex had reached $91.71 billion in assets under management by April 8, according to CryptoSlate data.

Given the size of the spot Bitcoin ETF market, we can clearly see that there's no lack of demand. The main problem the industry is faced with now is infrastructure.

On April 20, Grayscale amended its proposed Hyperliquid ETF filing and named Anchorage Digital Bank as custodian in place of Coinbase.

On its own, that looks like a modest filing change tied to a newer crypto product, but in context, it's a sign that issuers are starting to think harder about how much of the regulated crypto ETF market still runs through one back-office gatekeeper.

As CryptoSlate reported on April 12, funds whose launch documents name Coinbase as custodian or primary custodian account for about $77.10 billion of the market, or 84.1% of total US spot Bitcoin ETF AUM. A stricter method that excludes multi-custodian arrangements or unclear split allocations still leaves roughly $74.06 billion, or 80.8%, tied to Coinbase in some custody role. Those numbers make custody concentration part of the institutional appetite for Bitcoin, not a side detail buried in the documents.

A single filing doesn't establish a migration trend, and the market shouldn't turn one amendment into a sweeping break. Even so, custody choices inside ETFs carry real informational value because issuers, lawyers, and boards tend to repeat the safest available template. When a market that has spent years making the same custody decision starts to show variation, it's worth paying attention.

The ETF boom built a custody market around one default choice: Coinbase

Coinbase became dominant in crypto ETF custody for practical reasons that made sense from the start.

When spot Bitcoin ETFs won approval in January 2024, issuers needed a provider with a recognizable compliance profile, institutional operating history, and an infrastructure stack that already looked credible to boards, auditors, market makers, and regulators. Coinbase had that advantage. Once the largest issuers chose it, the rest of the market inherited a strong template effect.

That pattern kept extending into 2026. Morgan Stanley’s updated filing in March named Coinbase Custody and BNY as custodians for its proposed Bitcoin exchange-traded product, which later launched as the Morgan Stanley Bitcoin Trust.

Another blue-chip institution entered the market and plugged into the same custody backbone already supporting much of the ETF complex. That's how concentration deepens in financial infrastructure, with each new entrant reinforcing the same operational standard.

Coinbase’s own regulatory trajectory has only strengthened that position. On April 2, the company said it had received conditional approval from the Office of the Comptroller of the Currency to charter Coinbase National Trust Company. That was an important milestone, because a federal trust framework offers a cleaner supervisory map for the custody business that sits underneath products like ETFs.

Coinbase’s scale reflects institutional trust, launch readiness, and regulatory familiarity. Those strengths are also what made it the market’s central operational node. Crypto has spent years arguing about decentralization at the asset layer, while the institutional wrapper built around Bitcoin moved toward a highly concentrated custody structure. We can now clearly see that product variety expanded faster than infrastructure variety.

ETF investors spend most of their time looking at inflows, fees, and price action, though it's custody that shapes how the system functions day to day. If the wrapper is supposed to make digital assets legible to mainstream finance, then the resilience of that wrapper matters almost as much as the underlying asset. The live question now is whether the market has reached the point where resilience requires more redundancy.

Grayscale’s Anchorage switch points to a market thinking harder about redundancy

Grayscale’s amended Hyperliquid ETF proposal names Anchorage Digital Bank as custodian in place of Coinbase. Anchorage brings a different regulatory and institutional profile to crypto custody. It's the first federally chartered crypto-native bank in the United States, and it's already been moving deeper into the institutional stack. Grayscale had previously tapped Anchorage as a secondary custodian for part of its Bitcoin and Ethereum trusts, while BlackRock added Anchorage in April 2025 to support its spot crypto ETFs.

That makes the Grayscale amendment look like part of a slow broadening in the custody field. The important point is that issuers now have stronger reasons to add alternatives into the mix as the category grows larger and the cost of concentration becomes easier to quantify. A market carrying more than $90 billion in spot Bitcoin ETF assets starts to look different when more than four-fifths of that exposure still depends on one custody provider in some form.

The biggest risks are in operations, reputation, and market-wide spillover.

ETF assets are segregated, custody agreements impose fiduciary duties, and the legal structure around these funds differs sharply from the exchange failures and balance-sheet collapses that shaped crypto’s earlier crises.

That architecture is important, but so is the fact that a dominant provider can still become a choke point if it faces outages, settlement disruption, licensing complications, or regulatory pressure. The larger Coinbase’s role becomes, the larger the consequences become for any event that interrupts its ability to perform that role across multiple issuers at once.

Markets mature by building backups, widening their vendor maps, and reducing the number of points where one institution’s disruption can spill across an entire category. Crypto ETFs have already done the first part of institutionalization by attracting demand and embedding themselves in mainstream portfolios.

The next part is about whether the system underneath those products can carry that growth without leaning so heavily on a single provider, even when that provider remains strong and increasingly well connected to regulators.

Hyperliquid is a newer and more politically sensitive product than a plain spot Bitcoin ETF, and its core perpetuals venue remains ring-fenced in the US.

That alone may have given Grayscale an extra reason to lean on a federally chartered custodian. Even if that turns out to be the narrow explanation, the choice still reveals something important: when issuers encounter a product with more regulatory edge, they may see value in bringing a different type of custodian into the structure. And once that habit enters the market, broader diversification becomes easier to imagine.

That is why this launch belongs in the bigger conversation around Coinbase, Anchorage, and the institutional path of Bitcoin ETFs. The category no longer needs to prove that investors want regulated crypto exposure. It needs to show that the infrastructure underneath that exposure can evolve beyond the first template that worked.

Wall Street’s relationship with crypto keeps moving through familiar stages. First came access, then came legitimacy, and the next stage is resilience. Grayscale’s switch to Anchorage doesn't settle that transition, but

it does make the direction easier to see. The ETF boom made Bitcoin legible to traditional finance. What comes next will determine how durable that wrapper looks at scale.

The post Grayscale moves away from Coinbase for new ETF product – Is Wall Street building a post-Coinbase custody map? appeared first on CryptoSlate.

Bitcoin is heading into a rare macro window where the first reaction may age fast.

The Federal Reserve is scheduled to conclude its April meeting on April 29, with the FOMC decision and press conference landing that afternoon. The next morning, the US Bureau of Economic Analysis is scheduled to release the first quarter GDP and March Personal Income and Outlays, the report that includes PCE inflation.

That gives traders a two-step test with almost no pause between the steps. First, they get the Fed's view on rates, growth, and inflation. Then they get fresh data that can support that view, complicate it, or force a quick rewrite.

For Bitcoin, this setup is much more important than a regular Fed preview.

Bitcoin traders watch the central bank for the same reason equity traders do: rates shape liquidity, liquidity shapes risk appetite, and risk appetite shapes how much investors are willing to pay for volatile assets. When easier policy looks closer, Bitcoin usually gets a better backdrop. When rates look higher for longer, the market starts charging more for risk.

Next week compresses that entire process into roughly 48 hours. The Fed will speak first, but the data will get the last word.

This is a sequence trade

A normal Fed week gives markets time to build a take, but this time the market gets a much shorter runway.

GDP tells traders how strong the economy looked in the first quarter. Strong growth can support the idea that the economy can handle tight policy. Weak growth can raise concerns that the Fed is staying restrictive into a slowdown.

PCE gives traders the inflation read the Fed watches most closely. Hotter PCE pushes the market toward a higher-for-longer rate path. Cooler PCE gives rate-cut expectations more room.

Bitcoin is exposed to both. Growth affects risk appetite, and inflation affects rate expectations. A strong economy with sticky inflation can tighten financial conditions. A soft economy with cooling inflation can make easier policy feel more plausible. A messy combination can create volatility because traders have fewer clean signals to price.

The danger for Bitcoin is being right on the Fed and wrong the next morning.

A dovish Fed followed by soft data is the easiest bullish mix. The central bank sounds open to easing, and the data gives it cover. A dovish Fed followed by hot data is the dangerous version. Traders hear patience on Wednesday, then get numbers on Thursday that make that patience hard to defend.

A cautious Fed followed by soft data creates confusion, and the market may start asking whether policymakers are moving too slowly. A cautious Fed followed by hot data is the clean higher-for-longer setup, and likely the hardest version for Bitcoin.

We’ve seen this sensitivity around prior FOMC windows, PCE releases, and inflation surprises. Next week puts those pressure points into one tight sequence.

The second reaction to PCE may decide the move

Bitcoin is a scarce digital asset with its own long-term thesis. But in short macro windows, it also trades like a high-beta expression of liquidity expectations.

It’s that second identity that will get tested next week.

If the Fed sounds comfortable and Thursday's data cooperates, traders can lean back into the idea that rate relief remains alive for later in the year. That would support bitcoin through the same channel that often supports growth stocks: lower expected rates, easier financial conditions, and a stronger appetite for risk.

If the Fed sounds calm and the data arrives hot, the market has to revise quickly. Rate-cut expectations move further out, and Bitcoin has to absorb that reset alongside the broader risk complex.

If the Fed sounds cautious and the data is weak, the reaction can get choppy. Traders may price more cuts while also worrying about slower growth. Bitcoin can benefit from the liquidity side of that trade, then struggle if risk appetite fades.

The bearish version is simple: cautious Fed, resilient growth, sticky PCE. That gives traders fewer reasons to expect near-term relief. It suggests the economy still has enough strength to keep inflation pressure alive, while the Fed has little reason to soften its stance.

The bullish version runs the other way: Fed language leaves room for cuts, GDP shows cooling demand, and PCE gives policymakers more confidence on inflation. We've already seen how cooler inflation data can support Bitcoin. A compressed version of that trade could move fast if the numbers line up.

Bitcoin is heading into a week where markets may price the Fed, sleep on it, and wake up to data that changes the meaning of the first move. That creates a 48-hour stress test of rates, growth, inflation, and the near-term case for risk.

The post This week Bitcoin will face major volatility across a key 48 hour period: Fed first, GDP and PCE right after appeared first on CryptoSlate.

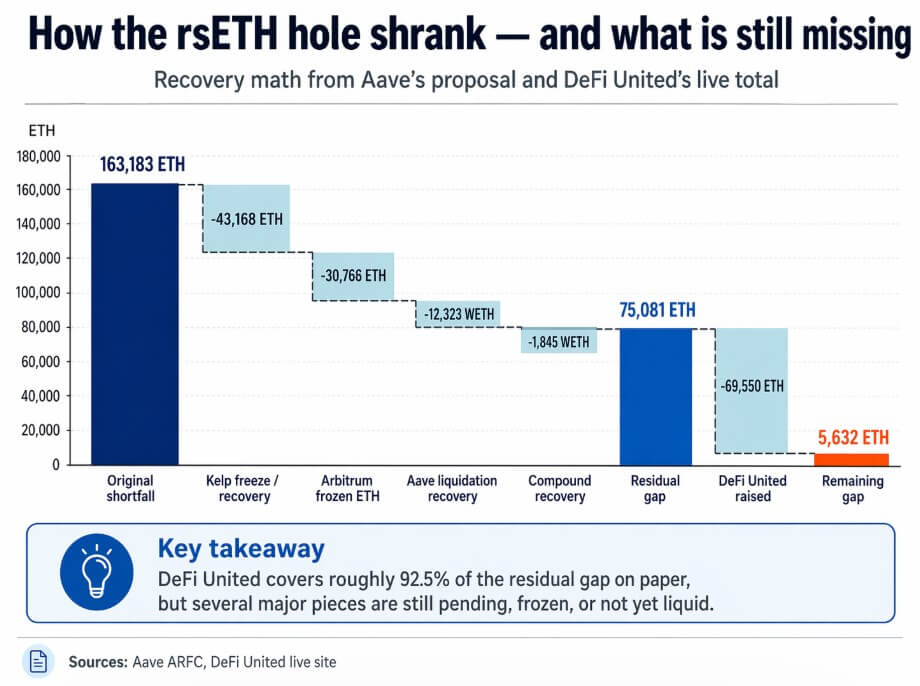

The official DeFi United site shows over 69,550 ETH raised from 222 wallets across 1,623 transfers, all aimed at restoring rsETH backing, acting as DeFi's emergency recapitalization desk.

The effort is the closest thing the industry has built to a lender of last resort, assembled without a regulator, a central bank, or a mandate.

Aave's governance proposal puts the original rsETH shortfall at approximately 163,183 ETH.

Recoveries and freezes, which include 43,168 ETH from Kelp, 30,766 ETH frozen by the Arbitrum Security Council, up to 12,323 WETH from Aave liquidations, and 1,845 WETH from Compound, reduce the residual funding gap to about 75,081 ETH.

DeFi United's current top line covers roughly 92.5% of that residual, leaving approximately 5,632 ETH. A broader tracker snapshot shows 100,200 ETH committed against a 116,500 ETH target when the Arbitrum frozen recovery path is included, putting total coverage at about 86%.

Both numbers carry the same caveat that the fund is close on paper, while most of the largest pieces are still pending governance votes, and several key contributions carry no disclosed amount.

How the hole got this large

KelpDAO's rsETH bridge ran a 1-of-1 configuration with LayerZero Labs as the sole verifier.

Galaxy's research found that the attacker exploited that setup to unlock 116,500 rsETH from Ethereum mainnet escrow, then used the stolen tokens as collateral across Aave, Compound, and Euler to borrow an estimated $236 million in WETH and wstETH.

Within 48 hours, DeFi's total value locked fell by roughly $13 billion. Aave alone shed about $8.45 billion in TVL, with WETH utilization hitting 100% as users rushed for the exits, simultaneously pushing USDT and USDC pools to full utilization.

LayerZero's own incident statement characterized the attack as RPC poisoning targeting infrastructure used by its decentralized validator network (DVN), stopping short of identifying a flaw in the LayerZero protocol itself.

The bridge route still depended on LayerZero Labs as the sole verifier, a configuration that concentrated trust in a single point. DeFi United lists LayerZero as “Confirmed, TBD.”

Because the entire incident ran through that bridge configuration, LayerZero's undisclosed contribution is one of the most consequential missing numbers in the recovery.

| Contributor | Status | Amount | Why it matters |

|---|---|---|---|

| Mantle | Pending vote | 30,000 ETH | Largest disclosed contribution; central to closing the gap |

| Aave DAO | Pending vote | 25,000 ETH | Core treasury backstop and the clearest test of DAO willingness to absorb losses |

| Stani Kulechov | Committed | 5,000 ETH | Personal founder-level signal that adds credibility to the effort |

| EtherFi | Pending vote | 5,000 ETH | Major ecosystem support before the full governance package is finalized |

| Lido | Pending vote | 2,500 ETH | Important because it opens a precedent debate around covering losses outside Lido’s own protocol |

| Golem Foundation | Committed | 1,000 ETH | Confirmed support from a recognized ecosystem participant |

| Emilio Frangella | Committed | 500 ETH | Visible individual contribution that reinforces the public-coordination angle |

| BGD Labs + Ernesto | Committed | 350 ETH | Service-provider support tied closely to Aave’s risk and governance machinery |

| LayerZero | Confirmed, TBD | TBD | Most consequential undisclosed number because the incident centered on the bridge route using LayerZero infrastructure |

| Ethena | Confirmed, TBD | TBD | Material participant, but amount not yet disclosed |

| Ink Foundation | Confirmed, TBD | TBD | Material participant, but amount not yet disclosed |

| Frax Finance | Confirmed, TBD | TBD | Material participant, but amount not yet disclosed |

The coordination case

DeFi United assembled without a regulatory mandate, a central bank, or an order from anyone.

Before Aave's treasury proposal even entered governance, EtherFi, Lido, Mantle, Ethena, Ink, BGD Labs, Emilio Frangella, Ernesto, and Aave's founder Stani Kulechov had already assembled 14,570 ETH in pledges.

The fund's named contributors now include Mantle with 30,000 ETH pending vote, Aave DAO with 25,000 ETH pending vote, Kulechov personally committing 5,000 ETH, EtherFi at 5,000 ETH pending vote, Lido at 2,500 ETH pending vote, Golem Foundation at 1,000 ETH, Frangella at 500 ETH, and BGD Labs plus Ernesto at 350 ETH.

LayerZero, Ethena, Ink Foundation, and Frax Finance are confirmed, with amounts still undisclosed.

Aave's ARFC frames its participation under a “No Ghost Left Behind” posture, citing the DAO's prior decision to cover CRV-related bad debt directly, shielding suppliers from socialized losses.

That framing of voluntary, cross-protocol, and publicly visible is the strongest argument the industry can make for its own self-governance capacity.

The centralization embedded in the rescue

Aave's proposal authorizes Aave Labs to negotiate loans, settlements, indemnities, under-collateralized lending arrangements, warrants, token sales, and deployment of future protocol revenue.

The Mantle contribution is structured as a credit facility, with later donations earmarked to repay Mantle, leaving Aave's treasury ask unchanged.

Aave's math treats the Arbitrum Security Council's 30,766 ETH as a recoverable stream that requires further governance action to release and sits outside DeFi United's control, as the site explicitly acknowledges. The same applies to KelpDAO reopening withdrawals and LayerZero reopening the bridge.

The Arbitrum intervention cuts to the center of the decentralization contradiction. A security council with emergency powers froze tens of thousands of ETH linked to the exploit and moved it into a controlled intermediary wallet.

That action helped contain the damage, and also required someone with the power to say no and to use it unilaterally in a crisis. In a system built around credible neutrality, the freeze both saved and complicated the narrative.

What governance is actually debating

Aave's forum has already produced the backlash the situation invites. One commenter argues the recovery math is sound but says the DAO should not move to a Snapshot vote until governance adopts a collateral-risk framework that would have blocked rsETH from being listed at those parameters.

Paying the bill without fixing the kitchen solves the immediate crisis and creates conditions for the next one.

Another voice in the same thread argues that the parties most responsible for the configuration are contributing proportionally less than the burden they impose on Aave.

Lido's parallel forum debate sharpens the question of precedent. Its proposal authorizes up to 2,500 stETH but only as part of a fully funded recovery package, with Lido noting that the alternative could expose its EarnETH vault to roughly 9,000 ETH in losses.

Delegates are openly debating if the contribution is a donation, if it should carry better terms, and if participation sets a precedent for covering losses originating outside Lido's own protocol.

Two paths forward

In the bull case, the pending governance votes clear quickly, Kelp and bridge-side mechanics reopen in an orderly sequence, Arbitrum governance releases the frozen ETH, and the remaining TBD participants close the gap.

The recovery becomes a working model for cross-protocol crisis coordination, proof that DeFi can self-insure without external backstops, and that the governance layer functions even when composability fails at the infrastructure level.

The backlash about collateral risk reform gets folded into the next governance cycle, leaving the rescue intact.

In the bear case, one or more of the largest pending votes or external recovery steps slip. The Arbitrum freeze stays politically contested.

LayerZero's contribution, once disclosed, falls short of what the bridge's structural role in the incident warrants. Aave's balance sheet absorbs more of the residual for longer than the proposal anticipates, and the governance backlash hardens around who decided that a 1-of-1 bridge-backed token qualified as acceptable collateral at those parameters.

DeFi United still exists in this version, but it becomes the case study in how the industry coordinates around downside on terms set by the largest actors.

| Scenario | What goes right or wrong | What it means for users | What it says about DeFi |

|---|---|---|---|

| Bull case | Pending votes pass, Arbitrum releases frozen ETH, Kelp and bridge-side mechanics reopen in order, and TBD contributors close the remaining gap | rsETH backing normalizes and users avoid a longer, messier recovery | DeFi shows it can coordinate fast enough to self-insure against a nine-figure exploit |

| Bear case | One or more major votes or external recovery steps slip, LayerZero’s disclosed contribution disappoints, and Aave carries more of the residual for longer | Recovery drags out, uncertainty lingers, and affected users remain dependent on protocol politics | DeFi looks less like neutral infrastructure and more like a system governed by the largest actors under stress |

| Key dependency | The outcome still depends on Arbitrum governance, KelpDAO actions, LayerZero bridge-side steps, and DAO approvals outside DeFi United’s direct control | Users are exposed not only to funding risk but also to timing and coordination risk | The rescue is decentralized in branding but centralized at key decision points |

| Governance lesson | Rescue money arrives before collateral-risk reform is fully settled | Users may be made whole now, but future listing standards remain contested | DeFi can mobilize for recovery faster than it can agree on prevention |

| Long-term consequence | The rescue succeeds and reforms follow | Confidence stabilizes, but the market becomes more skeptical of bridge-backed collateral | Bailout politics become part of the operating reality of “decentralized” finance |

DeFi United may close the gap, restore rsETH backing, and demonstrate that decentralized protocols can absorb a nine-figure exploit without systemic collapse. The recovery effort so far gives genuine grounds for that conclusion.

The rescue's architecture of pending votes, a private credit facility, a security council's freeze button, undisclosed negotiations, and legal instruments authorized by a DAO also describes a financial system that runs on credible neutrality until the losses are large enough, and then runs on whoever has the keys.

The post DeFi lost $13B this month as the KelpDAO rescue shows both the best and worst of DeFi appeared first on CryptoSlate.

Cryptoticker

Tangem is heating up the self-custody market this spring with the launch of its exclusive Prize Draw Campaign, running from May 5 to June 6, 2026. This campaign offers users a chance to win a share of over 100 prizes, including a grand prize of $5,000 in BTC.

How to Participate in the Tangem Draw

To participate in the Tangem Prize Draw, users simply need to purchase a Tangem wallet directly through our exclusive promo link here during the promotion period. Participation is entirely automatic; every wallet item purchased counts as one entry—for example, a 3-pack order equals three tickets—with no additional sign-up required.

Prize Pool Breakdown: What Can You Win?

The campaign features a robust selection of 104 individual prizes. Beyond the headline Bitcoin rewards, Tangem is giving away the latest tech and specialized hardware security gear.

| Prize | Quantity |

|---|---|

| $5,000 in $BTC | 1 winner |

| iPhone 17 (256GB) | 3 winners |

| Tangem Pro Kit | 5 winners |

| Tangem Ring | 10 winners |

| $50 in BTC | 25 winners |

| $10 in BTC | 60 winners |

Winners will be announced on July 5, 2026, following a 30-day "cooldown" period used to verify that only non-refunded purchases are eligible. The announcement will take place on the Tangem blog and via a live stream on the Tangem Discord.

Bonus Offer: Double Your Entries and Save 50%

Running concurrently with the prize draw is a significant discount on high-capacity storage. Users who purchase a Family Pack (two 3-card sets) starting with a Black or Stealth wallet can receive the second set at 50% off by using our official discount link.

Notably, both sets in the Family Pack count as separate entries for the prize draw, effectively doubling your chances to win while securing your assets at a lower cost. Eligible collections for the discounted second set include popular designs like Bitcoin, White Stealth, and the "Hold Your Freedom" series.

Why Hardware Security Matters in 2026

In an era where Bitcoin prices are pushing toward six-figure milestones, the security of your private keys is paramount. Modern hardware wallets have evolved to address sophisticated 2026 threats like AI-enabled phishing and "pig butchering" scams.

Tangem's unique approach utilizes EAL6+ certified secure element chips within a card-shaped form factor. Unlike traditional devices, Tangem is battery-free and requires no cables; users simply tap the card to their smartphone to sign transactions. This eliminates the vulnerability of a written seed phrase, as the keys are generated and stored exclusively on the card's chip.

Safety and Anti-Scam Precautions

Tangem has issued a strict warning regarding security during this campaign. Official winners will only be contacted via email from the @tangem.com domain.

- No Payment Required: Tangem will never ask for payment to claim a prize.

- Privacy First: Official staff will never ask for your private keys or seed phrases.

- Verify Sources: If you receive messages from other addresses claiming you have won, it is a scam.

While Bitcoin ($BTC) remains in a choppy consolidation range near $77,500, a handful of high-beta assets have posted double-digit gains, diverging significantly from the broader index.

Historically, vertical moves of this magnitude—often exceeding 30% in seven days—invite a period of rebalancing. For traders, this week is less about chasing the "pump" and more about identifying where the floor sits. Here are 3 tokens that soared high and need to be on every trader's radar.

1. Humanity Protocol (H): The "Vesting Choice" Volatility

Humanity Protocol (H) has been the week's standout performer, surging over 45% following a massive spike in on-chain whale activity. Large-scale transactions for $H$ recently hit a five-month high, signaling that institutional players are positioning themselves within its "Proof of Humanity" ecosystem.

However, a fundamental headwind is peaking right now. The Humanity Foundation recently presented early backers with a difficult choice: extend their vesting schedules until late 2026 or accept a 70% haircut for immediate liquidity by April 26. This creates a complex supply dynamic for the remainder of this week.

- The Bull Case: If whales continue to defend the current breakout support at $0.12, a test of the $0.18 resistance level is likely.

- The Bear Case: A significant "cliff" token unlock is approaching on June 25 for those who chose the haircut. In the immediate term, the market is pricing in this "death spiral" risk. If $H$ fails to hold $0.14, expect a retracement toward the $0.11 EMA.

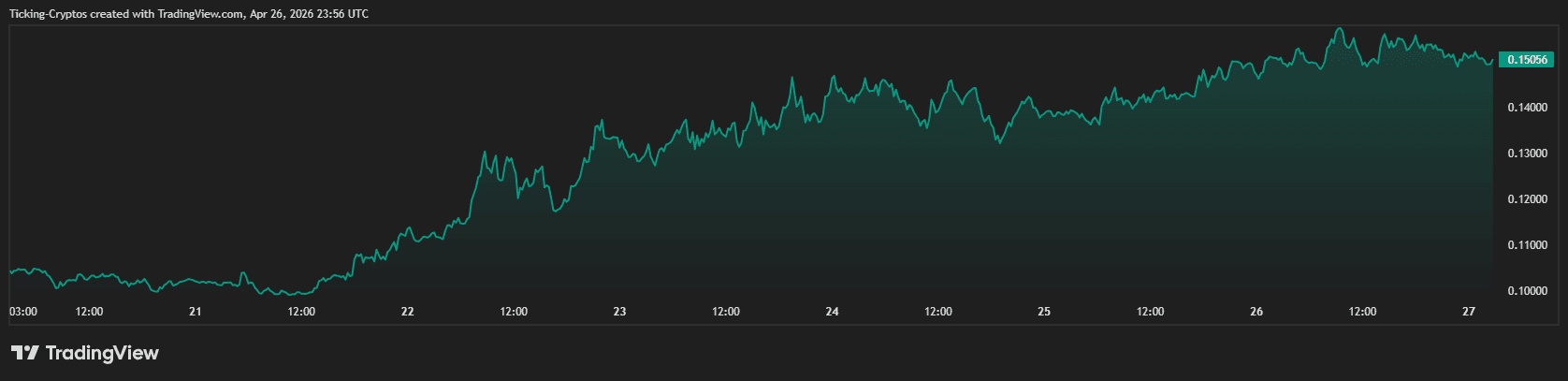

2. Stable (STABLE): Navigating Regulatory Momentum

Stable (STABLE) has climbed over 30% this week, reaching a market capitalization of approximately $742 million. This rally is fueled by the evolving regulatory landscape in the United States, specifically following the GENIUS Act guidelines and new institutional reserve portfolios from major banks.

Unlike purely speculative tokens, STABLE is positioning itself as a compliance-first asset. However, after such a rapid ascent, the token is showing signs of exhaustion.

- Key Levels: STABLE is currently hovering near a psychological resistance point of $0.035. A failure to break through this week could see profit-taking dominate the mid-week sessions, leading to a healthy retracement toward $0.028.

- Watch for: New Treasury Department rules regarding stablecoin AML frameworks, which could either solidify this rally or trigger a "sell the news" event.

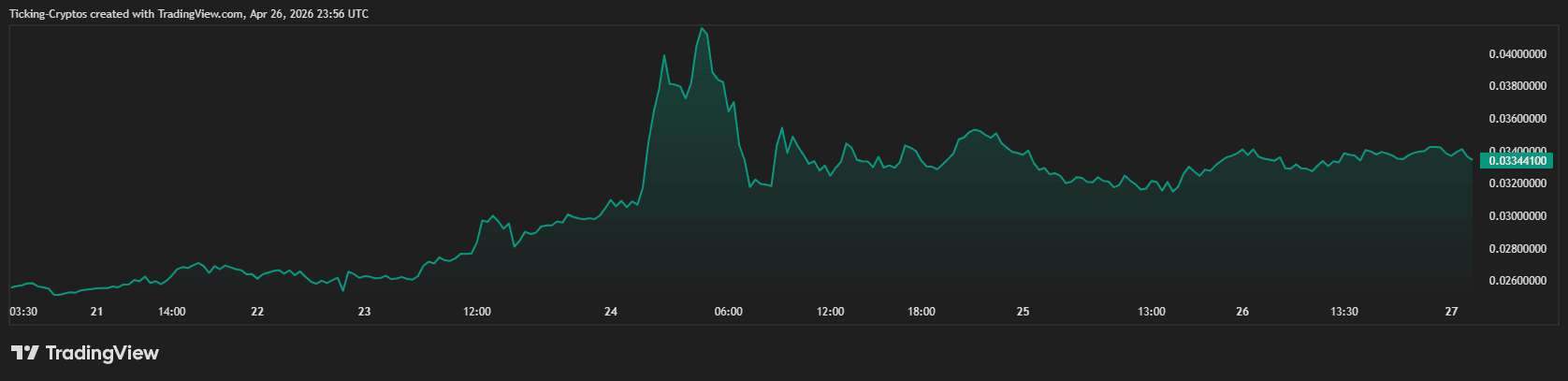

3. MemeCore (M): High Gains vs. Thin Liquidity

The third asset on our radar, MemeCore (M), has been the "moonshot" story of the month, gaining nearly 30% this week and pushing its valuation into the multi-billion dollar range. While the price of $M is sitting near its local highs of $4.38, technical analysts are sounding the alarm.

The project recently executed a hardfork that reduced gas fees by 99%, attracting a wave of retail interest. However, on-chain scrutiny highlights a potential risk: a discrepancy between the high market cap and relatively thin liquidity in decentralized exchange (DEX) pools.

- Risk Factor: The volume-to-market cap ratio remains low. In thin markets like MemeCore's, even small sell orders can have an outsized impact on the price.

- Technical Outlook: Watch for a "double top" pattern near $4.65. If $M fails to sustain volume above its 24-hour average of $25M, a sharp correction toward the $3.89 support level is probable.

Summary: 3 Cryptocurrencies to Watch This Week

| Asset | 7d Performance | Market Cap | Key Sentiment Trigger |

|---|---|---|---|

| Humanity Protocol ($H) | +45.48% | ~$415M | Token Unlock Decisions |

| Stable ($STABLE) | +30.12% | ~$742M | Institutional Reserve News |

| MemeCore ($M) | +29.19% | ~$5.68B | Liquidity & Social Hype |

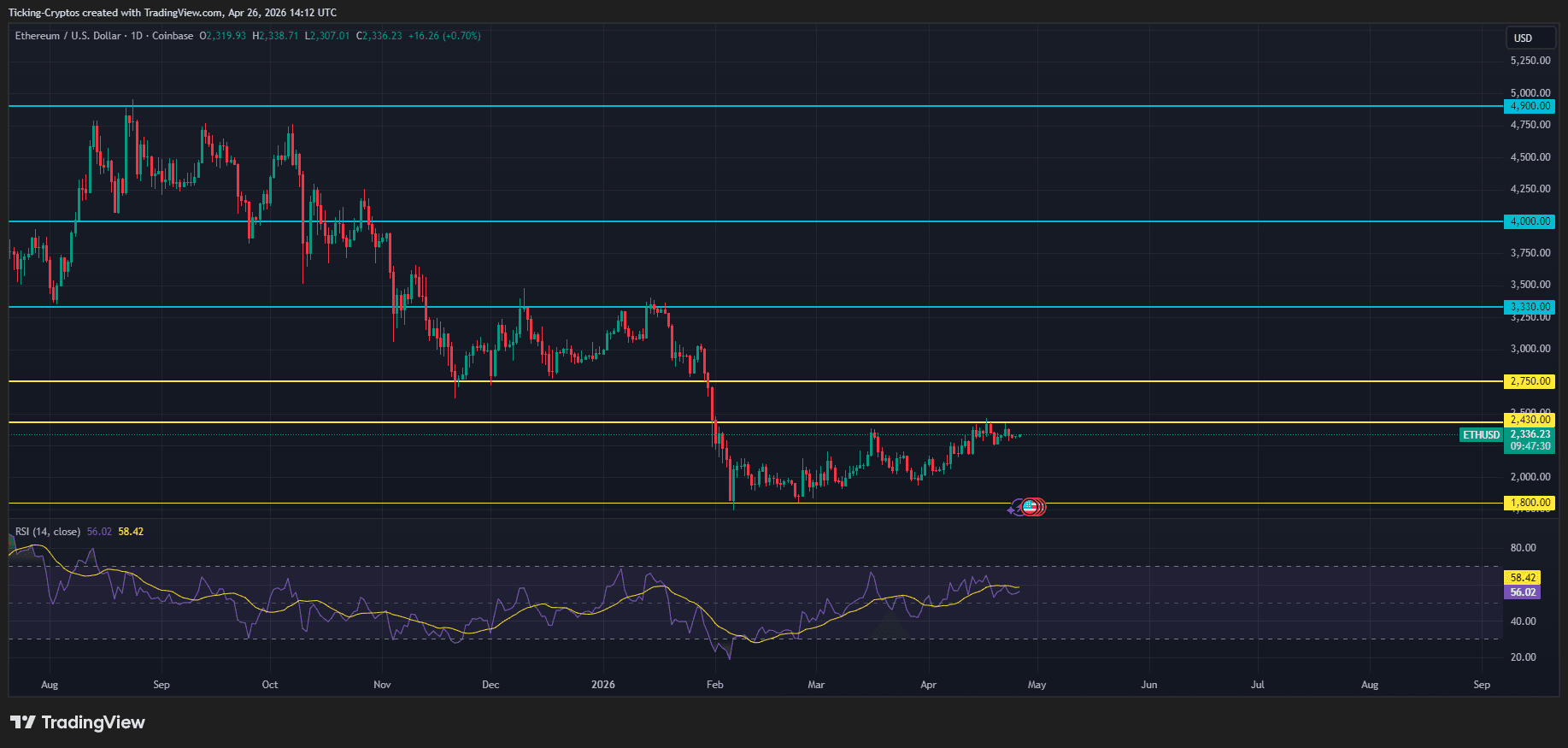

Ethereum ($ETH) has spent much of 2026 consolidating, leading many investors to ask the golden question: will Ethereum break its previous all-time high (ATH) of $4,900? A series of technical "ceilings" and shifting macroeconomic factors are currently dictating its pace toward a new record.

Can Ethereum Break its $4,900 ATH?

While a break above $4,900 is technically possible in 2026, it remains an optimistic target rather than a guaranteed outcome for the first half of the year. Analysts from major institutions like Standard Chartered and JPMorgan have set year-end targets ranging from $5,440 to as high as $10,000, contingent on a successful breakout from the current $2,300–$2,800 accumulation zone. However, as of April 26, 2026, ETH is trading near $2,333, indicating that the bulls still have significant work to do.

What Defines an "ATH Breakout"?

In technical analysis, an All-Time High (ATH) breakout occurs when an asset surpasses its highest ever recorded price—in Ethereum's case, approximately $4,878 (often rounded to $4,900). This event is significant because it enters a "price discovery" phase where no historical sell-side resistance exists. For ETH, the $4,900 mark isn't just a number; it is the final psychological barrier that separates the current range-bound market from a parabolic bull run.

Ethereum Price Prediction fr 2026

The journey to $4,900 is currently blocked by several key technical layers.

- The $2,750 Pivot: This is the immediate "line in the sand." Ethereum must reclaim this level to flip the medium-term trend from neutral to bullish.

- The $3,300 Resistance: A major supply zone. Historically, significant profit-taking occurs here, which could lead to temporary corrections back to $2,000.

- The Golden Cross: Traders are watching for the convergence of the 50-day and 200-day Moving Averages. A definitive "Golden Cross" in mid-2026 could be the catalyst for the final push toward the $4,900 ceiling.

Major Institutional Forecasts for 2026

| Institution | 2026 Target | Key Driver |

|---|---|---|

| Citi | $5,440 | Sustained Spot ETF Inflows |

| Standard Chartered | $7,500 | Institutional Pension Allocations |

| JPMorgan | $10,000 | L2 Fee Slashes & Scalability |

| DigitalCoinPrice | $5,301 | Post-Halving Momentum |

The Role of External Catalysts

While internal technicals are vital, Ethereum's trajectory is heavily influenced by Bitcoin ($BTC). Bitcoin is currently trading near $78,000, maintaining high dominance. For Ethereum to lead the market toward its ATH, we typically look for a "rotation" of capital where investors move profits from BTC into ETH. Furthermore, news regarding US-Iran geopolitical de-escalation and energy price stability—often reported by Reuters—plays a silent but massive role in risk-on sentiment for 2026.

Bitcoin price successfully reclaimed the $78,000 level within the last 24 hours. While broader sentiment remains cautious, major tokens suggest a robust underlying demand even in the face of international diplomatic friction.

Crypto News Today

As of April 26, 2026, the market is showing a clear "flight to quality."

- Bitcoin (BTC): Trading at $78,000, up from the mid-$77k range seen earlier.

- Ethereum (ETH): Stabilizing at $2,330, tracking Bitcoin's recovery closely.

- Solana (SOL): Holding firm at $86, despite being one of the more volatile assets in recent weeks.

Geopolitical Impact on Digital Assets

In the context of modern finance, "geopolitical impact" refers to how international conflicts and diplomatic negotiations influence investor behavior. While Bitcoin was once considered purely a risk-on asset, it is increasingly behaving like a neutral reserve. As noted by analysts, Bitcoin has managed to hold stability even as other cryptocurrencies face a "phase of indecision" caused by global uncertainty.

US-Iran Tensions and the $344 Million Seizure

The most significant driver of the crypto news today is the escalating financial pressure from the Trump administration on Tehran. In a major move, the U.S. Treasury recently froze approximately $344 million in cryptocurrency allegedly linked to Iranian financial lifelines.

Secretary of the Treasury Scott Bessent confirmed that the agency is targeting multiple wallets to cut off financial avenues used to bypass international sanctions. This news has created a dual-effect:

- Short-term Fear: Initial concerns over regulatory crackdowns on "unhosted" wallets.

- Long-term Stability: A market realization that Bitcoin remains a transparent and trackable ledger, which may actually invite further institutional adoption under clear enforcement.

Crypto Analysis: Resistance and Support Levels

Despite the geopolitical stalemate, Bitcoin's technical structure remains intact. The RSI (Relative Strength Index) is currently hovering slightly above 50, indicating that bullish momentum has not fully disappeared.

- $BTC Key Resistance: The $84,000 zone remains the most relevant level for a major bullish breakout.

- $BTC Immediate Support: $76,000 is the near-term barrier; staying above this level is crucial for maintaining the current recovery.

World News Integration: The "Stalemate Premium"

Traditional markets are currently pricing in a "stalemate premium" as the US and Iran remain at an impasse. While oil prices and the Nasdaq have seen fluctuations, $Bitcoin has capitalized on its status as a "borderless" asset. The cancellation of high-profile diplomatic trips has not triggered the massive sell-off many feared, largely because institutional Bitcoin ETFs continue to see consistent, albeit smaller, inflows.

Crypto News Today April 26, 2026 Prices

| Asset | Current Price | 24h Trend | Market Context |

|---|---|---|---|

| Bitcoin (BTC) | $78,000 | 🟢 Bullish | Reclaiming psychological support |

| Ethereum (ETH) | $2,330 | 🟡 Neutral | Correlation with BTC remains high |

| Solana (SOL) | $86 | 🟡 Neutral | Consolidating after weekly dip |

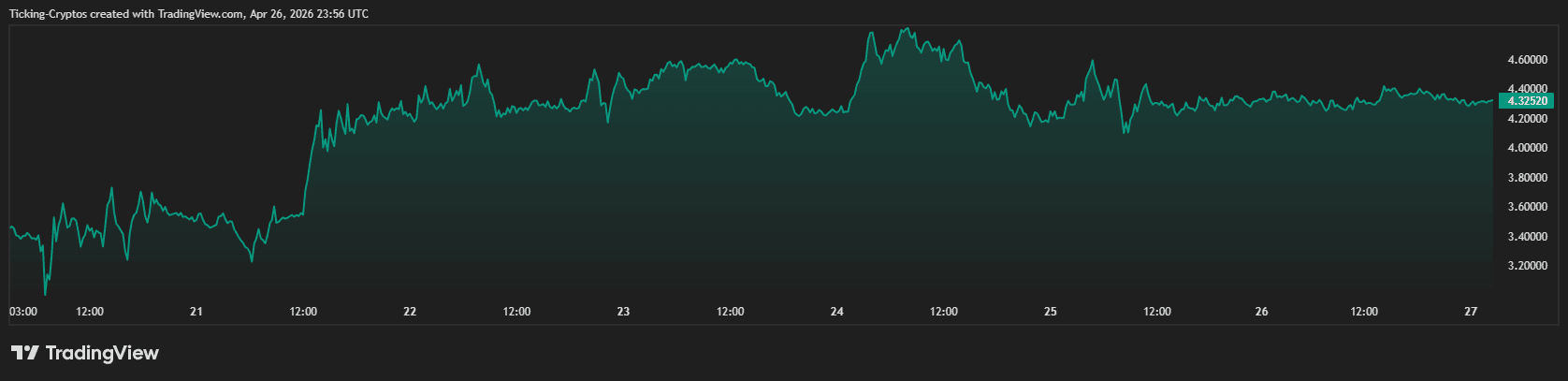

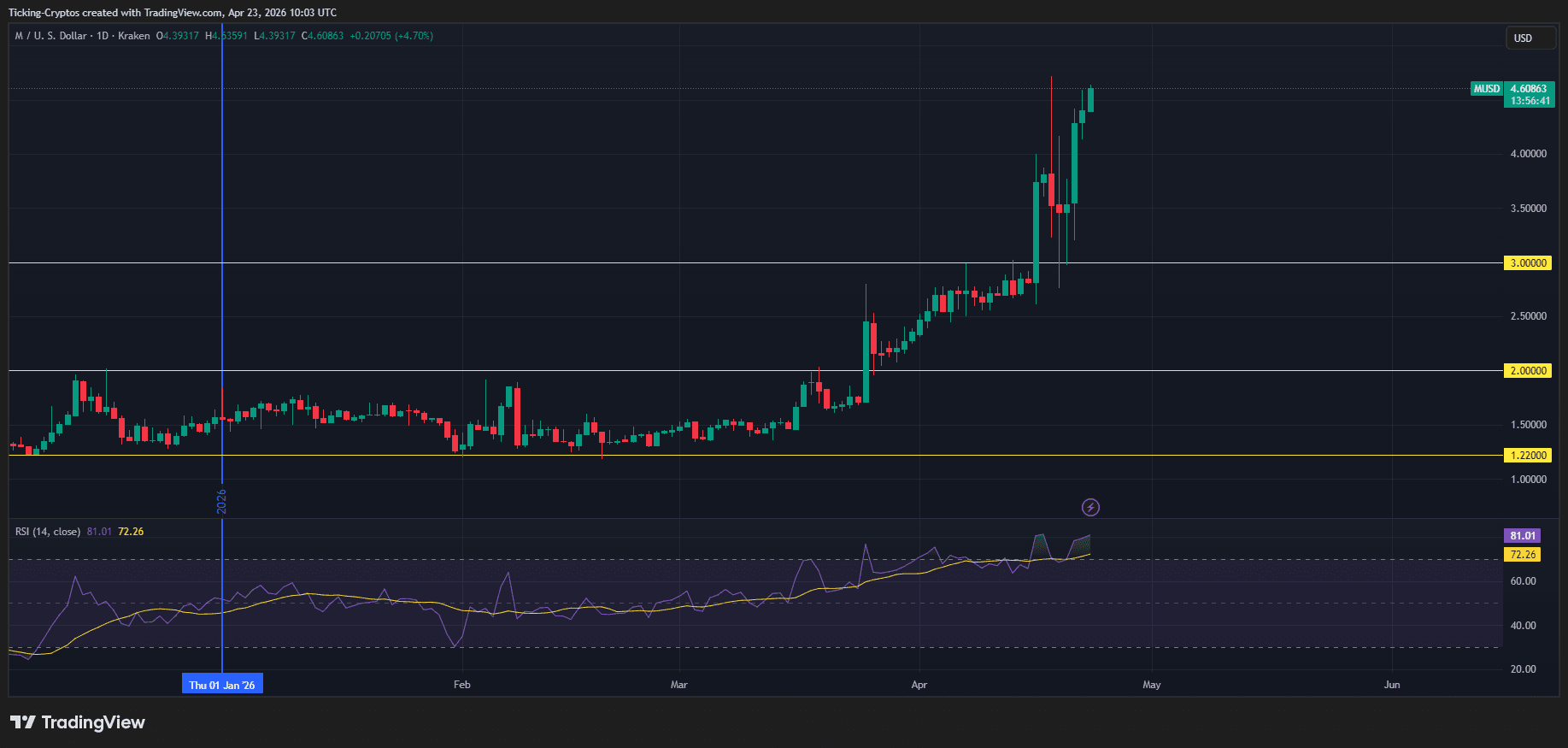

MemeCore ($M) has surged into the spotlight, but for all the wrong reasons. While the token’s price action on the daily charts looks like a dream for bulls, a series of onchain investigations have pulled back the curtain on a troubling reality: extreme supply concentration.

Recent reports suggest that over 90% of MemeCore’s supply is held by a tight cluster of insider wallets, creating what experts call a "ghost market cap." This structure mimics the architectural flaws seen in RaveDAO (RAVE), which recently suffered a catastrophic 95% wipeout.

What is a "Ghost Market Cap"?

The term "ghost market cap" refers to a project with a multi-billion dollar valuation on paper, but with very little actual liquidity or "free float" (tokens available for the public to trade).

- Valuation: MemeCore currently boasts a market cap north of $5.5 billion.

- The Discrepancy: Despite this massive valuation, its 24-hour trading volume often struggles to stay above $30 million.

- The Risk: When insiders control the vast majority of tokens, they can manipulate the price with relatively small amounts of capital. This allows for artificial "short squeezes" that trap retail traders before the eventual exit.

Will M Price Crash like RaveDAO (RAVE)?

The warning signs for MemeCore are nearly identical to those seen in the RaveDAO (RAVE) collapse. RAVE was touted as a "Live-to-Earn" revolution, surging from $0.25 to nearly $28 in April 2026. However, onchain sleuth ZachXBT revealed that insiders controlled 95% of the supply.

Once the "pump" was exhausted, a single multisig wallet moved millions of tokens to exchanges, causing a liquidity vacuum. RAVE plummeted from its peak to sub-$1 levels in less than 48 hours, wiping out $6 billion in market value. MemeCore’s current structure suggests it is walking the same tightrope.

MemeCore Price Analysis: Is the Rally Sustainable?

Based on the current M/USD price data, the token is showing classic signs of a "low-float" pump.

- Parabolic Growth: Since early March 2026, M has climbed from $1.50 to its current levels around $4.60.

- RSI Divergence: The Relative Strength Index (RSI) is currently sitting at 81.01, deep in overbought territory. Historically, an RSI this high without significant volume growth is a precursor to a "blow-off top."

- Support Levels: The yellow lines on the chart indicate critical psychological supports at $3.00 and $2.00. A break below $3.00 could trigger a cascade of liquidations similar to the RAVE event.

Should you Sell MemeCore TODAY?

If you are holding or considering M, these are the "red flag" signals to monitor:

- Wallet Movement: Sudden transfers from top-100 wallets to exchange deposit addresses.

- Liquidity Depth: If the "buy-side" orders on order books begin to thin out while the price stays high, a "liquidity rug" may be incoming.

Decrypt

The restructured deal with Microsoft removes exclusivity provisions and revenue-sharing arrangements, freeing OpenAI to pursue additional allies.

BitMine Immersion Technologies now holds over 5 million ETH, following the leading Ethereum treasury firm's biggest buy since December.

The Bitcoin-buying firm leaned on common shares to grow its holdings after STRC powered its largest purchase in 16 months.

California money launderer Evan Tangeman admitted to having processed millions in stolen cryptocurrency proceeds.

The nine-day inflow streak saw spot Bitcoin ETFs draw in $2.1 billion, but experts warn of “net negative” on-chain demand.

U.Today - IT, AI and Fintech Daily News for You Today

Shiba Inu ecosystem records impressive growth in its onchain movements as new users continue to massively onboard the network.

A collision of $108 oil, a projected 1.5% GDP gap, and the Fed’s neutral stance puts $2.5 billion in BTC and XRP ETF inflows in April at risk ahead of May.

Major hardware crypto wallet Ledger sounds alert as impersonation and phishing scams increase across the crypto ecosystem..

Shiba Inu's market performance is far from being positive, but the selling pressure is decreasing at least.

XRP's Ledger mysterious growth that didn't make sense considering the price performance has ended.

Blockonomi

Key Highlights

- Nvidia’s fiscal 2026 revenue reached $215.9 billion, representing a 65% year-over-year surge

- The company’s Data Center division delivered $193.7 billion in annual revenue

- AMD reported $34.6 billion in total 2025 revenue, with its Data Center segment climbing 32% to $16.6 billion

- Nvidia’s Data Center business exceeds AMD’s by more than 11-fold

- Export restrictions forced AMD to absorb $440 million in charges related to its MI308 GPU lineup

While both Nvidia and AMD play pivotal roles in the AI semiconductor landscape, their financial profiles reveal dramatically different business trajectories and market positions.

Nvidia disclosed fiscal 2026 revenue of $215.9 billion, marking a robust 65% climb compared to the previous fiscal year. The company maintained an impressive gross margin of 71.1%. During the fourth quarter alone, revenue totaled $68.1 billion, with the Data Center division accounting for $62.3 billion of that figure.

NVIDIA Corporation, NVDA

Across the entire fiscal year, Nvidia’s Data Center operations accumulated $193.7 billion in revenue. This segment has become the company’s primary growth engine, fueled predominantly by AI infrastructure investments from major cloud providers and technology enterprises.

Nvidia offers much more than standalone processors. The company delivers comprehensive solutions encompassing accelerators, networking infrastructure, complete systems, and a software ecosystem that enables customers to develop their AI applications. This integrated approach creates significant switching costs for clients considering alternatives.