Cryptocurrency Posts

Crypto Briefing

Google upgrades AI Studio with Antigravity agent, enabling developers to build full apps with backend, auth, and deployment from prompts.

The post Google brings vibe coding to production apps with new AI Studio upgrade appeared first on Crypto Briefing.

TRX/USDC trading pairs debut on Aerodrome, boosting TRON's cross-chain liquidity via LayerZero on Coinbase's Base network.

The post TRX/USDC trading pairs now available on Aerodrome, fueling cross-chain liquidity for TRON’s ecosystem appeared first on Crypto Briefing.

Tight monetary policy and persistent inflation create a challenging environment for risk assets, impacting investor sentiment and strategy.

The post Hawkish Fed and sticky inflation send risk assets sliding appeared first on Crypto Briefing.

Celo proposes a 160M CELO allocation to web browser Opera to deepen partnership and expand global stablecoin adoption.

The post Celo targets deeper ties with popular web browser Opera via 160M token proposal appeared first on Crypto Briefing.

Amundi's tokenized fund launch signifies a shift towards integrating blockchain in institutional finance, enhancing liquidity and operational efficiency.

The post €2.3 trillion asset manager Amundi launches tokenized fund on Ethereum and Stellar appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

5 Ways the Fed’s Basel III Pivot Unlocks Institutional Bitcoin Custody

Today, the Federal Reserve Board released a trio of proposals to modernize the U.S. capital framework which, if adopted, could fundamentally alter the cost and accessibility of institutional Bitcoin services. While the 14-page Board memorandum focuses on the technicalities of the “Basel III Endgame” and “GSIB surcharges,” our analysis suggests the most significant development for corporate treasuries is hidden in the proposed recalibration of operational risk.

1. Shattering the “Toxic Asset” Capital Barrier

For years, the primary hurdle for corporations looking to hold Bitcoin through traditional banks has been the “advanced approaches” to capital requirements. These internal, model-based assessments often resulted in punitive capital hits for digital asset activities, effectively labeling them “toxic” on a bank’s balance sheet. Under previous interpretations of the Basel SCO60 standard, certain digital assets were hit with a 1,250% risk weight… This proposal seeks to move beyond those models by recommending the elimination of the advanced approaches entirely for Category I and II firms. In their place, the Fed proposes a single, “expanded risk-based approach” designed to be more consistent and risk-sensitive across all asset classes.

In practice, a 1,250% risk weight combined with an 8% minimum capital ratio creates a 100% capital requirement. This “dollar-for-dollar” mandate made bank intermediation uneconomic, functioning as a de facto prohibition rather than objective risk management. Today’s proposal recommends eliminating the advanced approaches entirely for Category I and II firms. In their place, the Fed is introducing a single, “expanded risk-based approach” designed to be more consistent and risk-sensitive.

2. The Massive “Custody Service” Win

Critically, the proposed framework for operational risk is designed to “appropriately reflect business activities,” specifically naming custody services as a key area for this recalibration. The Fed staff noted that certain elements of the previous framework resulted in “excessive requirements for traditional banking activities.”

If Bitcoin custody is treated under this broader service definition, it would allow Tier 1 banks to offer these services without the prohibitive capital overhead that has previously driven up fees for corporate clients. By ensuring that operational risk requirements for custody are better aligned with actual historical risk, the Fed is signaling a move away from using punitive weights as a normative judgment.

3. A 4.8% Liquidity Injection and G-SIB Indexing

Got it. Keeping your structure intact, here is the updated Section 3 with the technical refinements (G-SIB indexing and capital relief) and the original bullet formatting you preferred.

3. A 4.8% Liquidity Injection and G-SIB Indexing

Perhaps the most notable projection for institutional adoption is the estimated impact on bank balance sheets. According to the Board memo, the cumulative impact of these proposals—including revisions to stress testing—is projected by staff to decrease the aggregate common equity tier 1 (CET1) capital requirements for Category I and II firms by 4.8 percent.

This reduction provides the nation’s largest banks with the capital “breathing room” necessary to expand into new service lines. For a corporate treasurer, this means:

- Increased Competition: More Tier 1 banks will have the capacity to offer digital asset services without hitting capital ceilings.

- Lower Fees: Reduced capital burdens on banks typically translate to more competitive pricing for fee-based services like custody.

- G-SIB Indexing: By indexing surcharges to economic growth, the Fed prevents “bracket creep,” ensuring banks aren’t penalized simply because the market value of the Bitcoin they hold grows over time.

- Regulatory Predictability: Moving to a “single set of risk-based capital calculations” provides the standardized environment corporate boards require for long-term strategic allocations.

4. Streamlining Through a Single Standard

The proposal aims to “substantially simplify the framework” by subjecting firms to a single set of risk-based capital calculations. This is intended to reduce the “regulatory lottery” where different banks faced vastly different costs for the same custody service due to overlapping or conflicting rules. For a corporation, this could ensure that Bitcoin custody becomes a more transparent, standardized banking product that fits within existing Basel market-risk and operational-risk frameworks.

5. Reversing the “Non-Bank” Migration

The Fed staff explicitly noted that excessive capital requirements in previous years may have accelerated the migration of certain banking activities to unregulated “non-banks.” According to the memo, these proposed revisions are intended to “support on-balance sheet lending and services” by regulated banks, potentially reversing some of that migration.

By bringing activities like high-scale custody back into the regulated banking fold, the Fed appears to be providing the “safe and sound” institutional infrastructure that many corporations have sought. This shift suggests an acknowledgement that transparent and liquid assets—including Bitcoin—benefit from being housed within the oversight of the federal banking system.

Conclusion

The Fed’s proposal represents a significant step toward “increasing the efficiency of capital allocation” and “reducing burden” across the U.S. banking system. By modernizing the risk weights for custody and streamlining the overall capital framework, the Federal Reserve is proposing the removal of several structural barriers that have long separated Wall Street from the digital asset ecosystem. While the final impact will depend on the results of the 90-day public comment period, the path to institutional-grade, bank-provided Bitcoin services appears significantly clearer than it did yesterday.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

This post 5 Ways the Fed’s Basel III Pivot Unlocks Institutional Bitcoin Custody first appeared on Bitcoin Magazine and is written by Nick Ward.

Bitcoin Magazine

Strive (ASST) Accumulates 13,600 Bitcoin Despite $393 Million Loss in First Six Months as Public Company

Strive, Inc., the corporate treasury firm founded by Vivek Ramaswamy, reported that it amassed 13,628 bitcoin as of March 17, 2026, placing the company among the top 10 corporate holders globally.

The accumulation came in the roughly six months following Strive’s September 2025 public listing, even as the company posted a GAAP net loss of $393.6 million for the period ending December 31, 2025.

The bulk of Strive’s bitcoin holdings came from multiple sources. Initial private investment proceeds and stock exchange activity contributed 5,886 bitcoin, while the acquisition of Semler Scientific, Inc. added approximately 5,048 bitcoin, the company said.

Semler Scientific had built its own digital asset reserve prior to the acquisition. An additional 2,694 bitcoin came from capital markets activity, including public offerings of Strive’s Variable Rate Series A Perpetual Preferred Stock (“SATA”), follow-on offerings, and at-the-market issuances.

Strive’s losses

Strive’s financial statements highlighted the tension between aggressive asset accumulation and market volatility. The firm’s GAAP net loss largely stemmed from non-cash items. Unrealized losses on bitcoin holdings accounted for $194.5 million, or nearly 50 percent of the total GAAP deficit.

Impairment of goodwill and intangible assets tied to the Semler acquisition added $140.8 million, and transaction-related expenses contributed $12.4 million. Adjusted for these items, the company’s non-GAAP loss attributable to common shareholders narrowed to $208.2 million, or $4.73 per diluted share.

Management introduced a proprietary metric, “Bitcoin Yield,” to measure the performance of its digital asset portfolio. By that measure, Strive reported a 22.2 percent yield in Q4 2025 and 13.8 percent quarter-to-date through mid-March 2026, equating to bitcoin gains of 1,305 and 1,050 coins, respectively. In dollar terms, these gains translated to $114.3 million and $78.2 million over the same periods.

The company financed its bitcoin strategy largely through structured finance products. Strive raised $148.4 million in net proceeds from its initial SATA preferred stock offering in November 2025, priced at $80 per share.

A follow-on offering in January 2026 generated $109.2 million at $90 per share. Proceeds were used to retire a $20 million loan from Coinbase Credit Inc., assumed as part of the Semler acquisition, and to exchange preferred shares for $90 million of Semler’s convertible debt.

Strive’s acquisition of Semler Scientific also included an operating business now held under a wholly-owned subsidiary, Clinivanta, focused on preventative healthcare.

The company appointed Michelle Fox, formerly Chief Medical Officer of Teleflex, as CEO of Clinivanta in February 2026, signaling an intent to develop the business alongside its primary focus on bitcoin accumulation.

Chairman and CEO Matthew Cole framed the results as a validation of Strive’s structured finance approach. “The most important success in our first six months as a public company was cementing our foundation as a structured finance company laser-focused on digital credit,”

Cole said. He emphasized that the SATA instrument provides a liquid, scalable solution for investors seeking double-digit yield with minimal volatility, aligning with Strive’s strategy of balancing bitcoin accumulation with broader financial operations.

As of March 17, 2026, Strive held $83.7 million in cash and $50.4 million in fair value of STRC preferred stock.

This post Strive (ASST) Accumulates 13,600 Bitcoin Despite $393 Million Loss in First Six Months as Public Company first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

BTQ Deploys First Working BIP 360 Implementation on Bitcoin Quantum Testnet

BTQ Technologies has released the first working implementation of Bitcoin Improvement Proposal 360 (BIP 360), marking an early attempt to bring quantum-resistant transaction infrastructure into a live testing environment.

Announced Thursday, the upgrade is now running on the Bitcoin Quantum testnet v0.3.0, a separate blockchain designed to simulate how Bitcoin could function in a post-quantum world. The release moves BIP 360 beyond theory, offering developers, miners, and researchers a place to test quantum-resistant transactions in practice.

BIP 360 introduces a new transaction format known as Pay-to-Merkle-Root (P2MR), which restructures how transaction data is committed on-chain.

The design removes the need to expose public keys during certain transaction paths, a feature that could become critical if quantum computers advance enough to break current cryptographic protections.

“BIP 360 represents the Bitcoin community’s most significant step toward quantum resistance and we’ve turned it from a proposal into running code,” said Olivier Roussy Newton, CEO of BTQ Technologies, in the company’s press release.

The implementation also preserves key functionality tied to Bitcoin’s scaling roadmap. According to BTQ, P2MR maintains compatibility with scripting features that underpin systems like Lightning and emerging frameworks such as BitVM and Ark, while eliminating the key-path spend mechanism introduced with Taproot that could expose public keys to quantum attacks.

Beyond the core transaction structure, the testnet includes full wallet tooling, allowing users to create, fund, sign, and broadcast P2MR transactions.

BTQ said this end-to-end functionality makes the upgrade immediately testable, rather than remaining a purely academic proposal.

Bitcoin experimentation and quantum-resistance

The company’s broader goal is to accelerate experimentation around quantum-resistant infrastructure at a time when concern over future cryptographic risks is growing. The Bitcoin Quantum testnet currently includes more than 50 miners and has processed over 100,000 blocks, according to the release.

Still, the technical progress highlights a deeper challenge: adoption.

BTQ has effectively bypassed Bitcoin’s traditional governance process by launching its own testing network rather than waiting for consensus within the main ecosystem. That decision reflects longstanding friction around major protocol changes, which historically require broad agreement among developers, miners, and users.

Christopher Tam, BTQ’s head of innovation, framed the issue in human terms. “It’s a social problem,” he told Decrypt, pointing to the difficulty of coordinating change across a decentralized network with entrenched stakeholders.

The approach also raises questions about whether a parallel chain can meaningfully influence Bitcoin’s future.

Bitcoin Quantum does not share Bitcoin’s ledger or balances, instead launching from a new genesis block with its own asset and ruleset. Users would need to opt in rather than automatically inherit the upgrade.

Even with a working implementation, BIP 360 addresses only part of the quantum threat. Tam noted that while the proposal can help secure future transactions, it does not retroactively protect older addresses that may already have exposed public keys.

The urgency, however, remains. Researchers widely expect that sufficiently advanced quantum computers could eventually break the elliptic-curve cryptography that secures Bitcoin, though the timeline is uncertain.

For now, BTQ’s testnet serves as an early proving ground. Whether its work translates into changes on Bitcoin itself may depend less on code—and more on consensus.

This post BTQ Deploys First Working BIP 360 Implementation on Bitcoin Quantum Testnet first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Price Slides Below $70,000 as Oil Spikes, Fed Hold Tightens Financial Conditions

Bitcoin price fell below the $70,000 level on Thursday, pressured by a surge in energy prices and a steady stance from the Federal Reserve that reinforced a stronger dollar and dampened appetite for risk assets.

The largest cryptocurrency traded near $69,500, extending losses from the prior session as crude oil markets spiked amid escalating conflict in the Middle East. Brent crude climbed above $114 per barrel, while Oman crude surged as high as $150, reflecting fears of supply disruptions after attacks on key energy infrastructure tied to tensions between Iran and Israel.

The macro shock rippled across markets. European natural gas futures jumped sharply, while Nasdaq-100 equity futures slipped, signaling broader weakness in risk assets. Bitcoin price declined roughly 4% in the 24-hour period, according to Bitcoin Magazine Pro data.

Pressure on crypto intensified after the Federal Reserve held its benchmark interest rate steady at 3.50%–3.75% following its March meeting.

While the decision was widely expected, policymakers struck a cautious tone as geopolitical risks and rising energy costs threaten to keep inflation elevated.

That shift has altered expectations for monetary policy. Market pricing now reflects limited chances of rate cuts in 2026, with some traders even assigning a small probability to further tightening. Higher-for-longer rates tend to weigh on assets like Bitcoin by increasing the appeal of yield-bearing instruments and strengthening the dollar.

Bitcoin price sell off

Bitcoin price price briefly climbed above $75,000 earlier this week before sliding sharply over the past few days to fall back below $70,000.

The sell-off extended beyond crypto. The S&P 500 and global equities declined, while gold also pulled back from recent highs despite ongoing conflict, suggesting investors are reducing exposure across multiple asset classes.

Geopolitical tensions remain the key driver. Iran’s reported attacks on regional energy infrastructure, including assets linked to Qatar’s liquefied natural gas exports, have raised concerns about supply disruptions.

At the same time, U.S. officials are weighing further military involvement to secure shipping routes through the Strait of Hormuz, a critical artery for global oil flows.

As long as energy prices remain elevated and central banks maintain a restrictive stance, Bitcoin price is likely to trade in line with broader macro conditions rather than idiosyncratic crypto catalysts.

The $70,000 level now stands as a key psychological threshold, with further downside risk if volatility in commodities and geopolitics persists.

This post Bitcoin Price Slides Below $70,000 as Oil Spikes, Fed Hold Tightens Financial Conditions first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

SEC Approves Nasdaq Rule to Trade Tokenized Securities, Paving Way for Blockchain Integration

The U.S. Securities and Exchange Commission (SEC) has approved a Nasdaq rule change that allows certain securities to be traded in tokenized form, a move that integrates blockchain technology into traditional stock market infrastructure.

The approval, issued Wednesday, is part of a broader effort to explore digital representations of regulated assets while maintaining investor protections and market stability.

Under the new framework, eligible securities — including stocks in the Russell 1000 Index and exchange-traded funds (ETFs) tracking major benchmarks such as the S&P 500 — can be represented and traded as tokenized assets on Nasdaq.

These tokenized versions are fully interchangeable with traditional shares, sharing the same ticker symbols, CUSIP numbers, and shareholder rights.

Investors holding tokenized securities retain standard protections, including voting rights, dividend access, and claims on residual assets, ensuring consistency with existing securities laws.

The system operates as a pilot program through the Depository Trust Company (DTC), which handles post-trade settlement and tokenization. Market participants can choose to settle trades in tokenized form via a designated instruction at order entry.

Earlier this month, Nasdaq partnered with Payward, Kraken’s parent company, to enable the trading of tokenized stocks between traditional markets and blockchain networks using Payward’s xStocks platform.

A nod to Bitcoin

This move won’t directly affect Bitcoin’s price or network, but it’s a nod to a growing regulatory comfort with blockchain-based assets, which could indirectly boost institutional interest in digital currencies.

By integrating tokenized securities into mainstream markets, it may pave the way for broader adoption of crypto infrastructure and financial products that interact with Bitcoin.

If tokenization requirements are not met, trades default to traditional settlement. Nasdaq confirmed that its core trading infrastructure — including order types, routing strategies, trading sessions, and market data feeds — remains unchanged, ensuring tokenized securities are fully integrated into existing systems.

JUST IN:

— Bitcoin Magazine (@BitcoinMagazine) March 18, 2026SEC approves Nasdaq rule change to enable tokenized securities trading

pic.twitter.com/FUxP1LKhUU

Settlement continues on a T+1 basis, aligning tokenized trading with current standards.

Nasdaq emphasized that a tokenized share and its traditional counterpart will trade on the same order book, with identical execution priority and market data treatment. Surveillance systems will monitor both forms of the security using the same underlying data, accessible to both Nasdaq and FINRA.

The exchange will issue alerts identifying which securities are eligible for tokenized trading and will notify members at least 30 days before launching any tokenized instruments.

The SEC, in its approval, said the proposal meets regulatory requirements designed to protect investors and maintain fair and orderly markets.

The Commission specifically cited Section 6(b)(5) of the Securities Exchange Act, which requires exchange rules to prevent fraud, promote equitable trading principles, and remove impediments to a free and open market.

According to the document, tokenized securities must mirror traditional shares in rights and privileges, limiting the risk of divergence in value or investor protections.

The DTC pilot provides a controlled framework for blockchain-based trading without introducing new market risks.

The approval reflects growing momentum toward tokenization in regulated markets. Exchanges and infrastructure providers are increasingly exploring blockchain representations of conventional assets while remaining within the bounds of existing law.

Nasdaq has indicated that alternative tokenization methods are under discussion and would require separate filings with the SEC.

This post SEC Approves Nasdaq Rule to Trade Tokenized Securities, Paving Way for Blockchain Integration first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

CryptoSlate

Trading begins on MEXC

Playnance’s G Coin has entered open-market trading, with the G Coin/USDT pair going live on MEXC after the project’s Token Generation Event on March 18.

MEXC’s official announcement said deposits were open and withdrawals would begin on March 19, while the exchange’s live G Coin page shows the pair as active. For Playnance, that shifts G Coin from an ecosystem-native utility token into a publicly traded asset with continuous price discovery.

The listing matters because Playnance is not presenting G Coin as a blank-slate token. In its white paper and product documentation, the company describes G Coin as a utility asset tied to gameplay, missions, rewards, loyalty features, and broader participation across its platforms, not as a governance or profit-sharing token.

That gives the MEXC debut more substance than a typical launch, because market access is arriving after utility has already been built into the ecosystem.

Staking becomes the first post-listing signal

The clearest early signal is staking participation. Playnance’s site highlighted a launch phase in which more than 250 million G Coin were locked within hours, and later launch coverage tied to the MEXC debut said staking had already moved above 1 billion G Coin shortly after going live. Playnance’s staking page shows four lockup periods, 6, 9, 12, and 18 months, with reward allocations weighted toward longer commitments.

That matters because lockups can do more than generate a headline number. They can reduce immediately available supply, encourage longer-term alignment, and give the market a measurable signal of confidence just as trading opens.

Playnance’s public G Coin Tracker adds another reference point. Indexed snippets from the tracker show a fixed 77 billion token supply and more than 3.15 billion G Coin in locked supply or treasury categories, alongside live fields for price and holder data.

Utility and token design now face the market

Playnance says its broader ecosystem runs on PlayBlock, a Layer-3 infrastructure built for gaming, trading, betting, and prediction markets, with gasless execution and sub-second finality. Within that framework, G Coin is meant to power gameplay interactions and fees, rewards and incentives, partner revenue distribution, and treasury flows.

That gives the token a clearer operational role than many newly listed assets that reach exchanges before their use cases are live.

Supply design is also central to the pitch. Playnance’s docs and white paper say G Coin has a fixed maximum supply of 77 billion tokens. Tokens lost through gameplay are locked for 12 months before returning to circulation, while unsold tokens at TGE are subject to a 12-month cliff followed by 24-month linear vesting. The white paper also says the token already provided access to an operational ecosystem before admission to trading.

The next test is simple, whether the exchange listing, staking participation, and underlying product activity reinforce each other over time. MEXC gives G Coin liquidity and visibility. Staking gives the market an early demand signal. The tracker gives users a public dashboard. What matters now is whether volume, user growth, and on-chain usage keep moving in the same direction after launch-day attention fades.

The post Playnance’s G Coin goes live on MEXC as staking momentum builds appeared first on CryptoSlate.

For decades, the benchmark for US risk lived on US time. S&P 500 opened at 9:30 a.m. Eastern and closed at 4:00 p.m., with premarket whispers and after-hours fragments filling the gaps.

On Mar. 18, that constraint began to crack. S&P Dow Jones Indices licensed the S&P 500 to Trade[XYZ] to launch the first officially sanctioned perpetual derivative based on the benchmark on Hyperliquid, available to eligible non-US investors using institutional-grade index data.

The ecosystem surrounding the S&P 500 already processes more than $1 trillion in daily trading volume across linked exposures. Now, a piece of that exposure can trade 24/7/365, including the 49-hour window from Friday's 5:00 p.m. close to Sunday's 6:00 p.m. CME futures reopening when traditional US infrastructure goes dark.

The move represents a structural bet that the first tradable reaction to global events may emerge on always-open rails before traditional venues fully reopen.

Trade[XYZ] created a perpetual derivative tied to licensed S&P benchmark data, not direct ownership of the underlying 500 stocks. By midday, the contract held approximately $3.4 million in open positions, a negligible figure relative to the trillions the benchmark represents.

Trade[XYZ] says its markets have processed more than $100 billion in volume since October 2025 and currently run at an annualized pace above $600 billion.

Hyperliquid's broader HIP-3 macro markets grew from roughly $260 million in open interest a month before Jan. 27 to approximately $1.43 billion recently.

The S&P contract enters a venue where non-crypto macro instruments have already gained traction.

The weekend gap and who fills it

CME already offers near-24-hour weekday access to S&P exposure through E-mini S&P 500 futures, which trade from Sunday 6:00 p.m. Eastern to Friday 5:00 p.m. Eastern with a daily one-hour maintenance break.

NYSE Arca and brokers provide premarket and after-hours equity trading windows.

Traditional infrastructure shuts down from Friday evening to Sunday evening, leaving a two-day gap during which a tariff announcement, military escalation, or a central bank leak can land without an official market response.

Kaiko documented this dynamic during the Feb. 27-28 US-Iran escalation. Weekend Bitcoin spot volume surged from a typical $1.5 billion per day to $2 billion, then to $8 billion, while traditional markets remained closed.

Kaiko noted that crypto printed the first move, but deeper institutional liquidity often arrived later when London and US hours resumed.

The pattern suggests crypto can capture initial reactions without yet commanding final pricing authority.

The S&P perpetual on Hyperliquid positions itself to serve that first-draft function with a more precise instrument than Bitcoin, which has historically absorbed weekend macro flow as a blunt proxy for global risk.

The infrastructure supporting this shift is evolving rapidly. Nasdaq is working toward 24/5 trading and has filed to extend equities hours to 23 hours a day, five days a week.

DTCC's NSCC targets 24×5 trade processing from Sunday 8:00 p.m. Eastern to Friday 8:00 p.m. Eastern, with implementation slated for June 28, 2026, subject to regulatory approval.

Incumbents are moving toward continuous availability, but they have not arrived yet. Crypto arrived first.

| Venue | Typical trading window | Weekend access | Public price visibility | Depth today | Main limitation |

|---|---|---|---|---|---|

| U.S. cash equities | Regular session: 9:30 a.m.–4:00 p.m. ET | No | High during regular session | Deepest | Closed outside the official session |

| Premarket / after-hours equities | Typically around 4:00–9:30 a.m. ET and 4:00–8:00 p.m. ET, depending on venue | No | Fragmented across venues; not a single clean tape | Moderate, often thinner than cash hours | Thin liquidity and fragmented price discovery |

| CME E-mini S&P futures | Sunday 6:00 p.m. ET to Friday 5:00 p.m. ET, with a 1-hour daily break | Not through the full weekend gap | High | Deep on weekdays | Closed from Friday 5:00 p.m. ET to Sunday 6:00 p.m. ET |

| Hyperliquid S&P perpetual | 24/7/365 | Yes | Public onchain tape | Early but growing | New market; depth still building; trust depends on stress performance |

Transparency as a competitive advantage

NYSE research shows that overnight US equity trading remains small, accounting for approximately 0.11% of total volume and 0.15% of year-to-date notional in 2025.

More telling, that activity is fragmented. NYSE notes that some prior-day trading does not appear in most public feeds, and Sunday evening matches are not publicly available through the Securities Information Processors.

Hyperliquid's HIP-3 system operates on-chain, enabling deployer actions to be independently analyzed. The emerging contest is over who produces the most legible first print when official infrastructure is offline or opaque.

New York Fed research found that US equity returns are meaningfully positive during the opening hours of European markets, suggesting that price discovery continues even when US venues are closed.

If a licensed S&P perpetual on public crypto rails consistently reflects weekend macro shocks before CME futures reopen, it becomes a signal market.

The bull case assumes the S&P perpetual grows from its current single-digit-million-dollar scale to a tens-of-millions- or hundreds-of-millions-dollar product.

Weekend liquidity deepens. Repeated on-chain moves closely align with Sunday CME reopening levels, leading macro desks to treat the on-chain read as the first serious price reference, and crypto precedes traditional venues in the price discovery sequence.

The bear case treats this as a high-leverage narrative product. Depth stays shallow, funding rates turn noisy, and serious size stays at CME, broker overnight books, or alternative trading systems.

In this scenario, Hyperliquid fails to provide durable price discovery, and the S&P contract becomes a sentiment telemetry tool.

A threshold model helps frame credibility. With under $25 million in S&P-specific open positions, the market remains symbolic. Between $25 million and $100 million, it becomes a credible weekend signal worth charting against Sunday CME reopening.

Above $100 million, it could serve as a reference-grade first-move indicator for macro narratives. Above $250 million, with tight spreads through weekend shocks, it enters a real fight over who prints the first trusted price for US risk.

| S&P perpetual OI | Interpretation | What it means for price discovery |

|---|---|---|

| Under $25M | Symbolic | Useful as sentiment, not trusted first print |

| $25M–$100M | Credible signal | Worth comparing against Sunday CME reopen |

| $100M–$250M | Reference-grade | Serious first-move market |

| Above $250M | Competitive with incumbents | Real contest over first trusted price |

The most serious risk is trust under stress. A geopolitical or policy shock during the weekend could expose thin liquidity or trigger oracle disputes.

HIP-3 assigns operational responsibility to the deployer, who defines the market and the oracle. Traditional US market guardrails are built around regular hours frameworks with circuit breakers, coordinated halts, and regulatory oversight calibrated to established venues.

A weekend gap or liquidation cascade on the S&P perpetual could damage credibility faster than consistent weekend prints could build it.

What the market is pricing in

The official opening and closing still belong to traditional markets.

However, with a US risk proxy trading 24/7, it remains to be seen if the first meaningful reaction to a Friday-night strike, a Saturday tariff leak, or a Sunday central bank surprise starts showing up on-chain before US futures reopen.

The advantage lies in time-plus-tape visibility, as crypto can trade the S&P on weekends with a public record before the US market infrastructure is fully operational.

The outcome depends on the S&P perpetual on Hyperliquid sustaining depth, maintaining tight spreads, and surviving its first weekend stress test without a credibility crisis.

The post Crypto just opened S&P 500 trading for the weekend while Wall Street shuts down appeared first on CryptoSlate.

The stablecoin debate in Washington is increasingly becoming a fight over a single question: who gets to keep deposit insurance on-chain?

FDIC Chair Travis Hill signaled that payment stablecoins under the GENIUS Act should not qualify for pass-through insurance, while tokenized deposits that meet the legal definition of a deposit would retain the same insurance treatment as traditional bank accounts.

That distinction may prove decisive.

If banks can offer on-chain dollars that preserve deposit insurance while stablecoins cannot, the competitive balance shifts. Stablecoins may still dominate open networks, but banks would retain the core advantage that has always anchored the financial system: insured money.

In that scenario, the stablecoin battle is no longer just about technology or distribution. Whether users prefer open, programmable dollars without insurance or bank-issued tokens that carry the full weight of the existing safety net will be the deciding factor.

In a Mar. 11 speech at the ABA Washington Summit, Hill said the agency plans to propose that payment stablecoins subject to the GENIUS Act are not eligible for pass-through insurance.

In the same section of the speech, he said the FDIC also plans to clarify that tokenized deposits that satisfy the statutory definition of a deposit should receive the same regulatory and deposit insurance treatment as non-tokenized deposits.

Hill also said the agency wants to comment on how existing pass-through rules should apply to tokenized deposit arrangements involving third parties.

The FDIC Chair's speech effectively sketches a two-tier map of on-chain dollars.

Under that map, payment stablecoins can be regulated and widely used, yet would lack federal insurance marketing rights and, if Hill's proposal sticks, would not get pass-through insurance.

On the other hand, tokenized deposits remain within the legal category of bank deposits when they qualify, which means they can retain the core advantage of bank money: access to the existing deposit-insurance regime.

| Feature | Payment stablecoins | Tokenized deposits |

|---|---|---|

| Legal category | Payment token under GENIUS framework | Bank deposit, if it meets deposit definition |

| Insurance treatment | No FDIC pass-through insurance under Hill’s proposal | Same treatment as ordinary deposits, if structured as deposits |

| Who can issue | Banks or nonbanks | Banks |

| Core advantage | Open-network usability | Deposit status and insurance framework |

| Core weakness | No deposit-insurance wrapper | May stay permissioned / bank-controlled |

This divide feeds into the broader legislative fight over the Clarity Act in Washington, where banks and crypto firms are clashing over whether stablecoins should be allowed to offer yield.

Same blockchain rails, different legal reality

This is part of a broader regulatory thaw. In March 2025, the FDIC said FDIC-supervised institutions may engage in permissible crypto and digital asset activities without prior approval, provided the risks are appropriately managed.

In 2025, the FDIC also withdrew from several interagency crypto statements, including one that had suggested public distributed-ledger activity was likely inconsistent with safe and sound banking.

Then, in December 2025, the FDIC proposed an application framework for FDIC-supervised banks that want to issue payment stablecoins through subsidiaries under GENIUS.

In March 2026, the FDIC, the Fed, and the OCC also clarified that tokenized securities generally receive the same capital treatment as their non-tokenized counterparts.

Put together, those moves amount to a much clearer path back into blockchain-based finance for banks.

The US is now separating on-chain dollars into at least two buckets.

Payment stablecoins are designed for payment and settlement, can be issued by banks or nonbanks under GENIUS, and are attractive because they can run on open blockchain networks.

Hill is drawing a bright line around insurance.

Tokenized deposits fall under traditional deposit regulation when they meet the deposit definition, which gives them a different legal footing. The competition becomes stablecoins versus bank money made portable on-chain.

The banking industry's concern is concrete. A February 2026 New York Fed staff report argued that stablecoins can erode banks' deposit franchises and also transmit liquidity stress into the banking system, forcing partner banks to hold more reserves and potentially reducing lending.

Standard Chartered estimates said US banks could lose about $500 billion in deposits by the end of 2028 if stablecoin adoption accelerates.

Hill's distinction offers banks a way to answer stablecoins with a form of on-chain money that still counts as bank funding.

What tokenized deposits look like today

On Jan. 9, BNY said it had taken the first step in a strategy to tokenize deposits by enabling an on-chain, mirror representation of client deposit balances on its Digital Assets platform.

BNY also made clear what kind of product this is: it runs on a private, permissioned blockchain, begins with collateral and margin-workflow use cases, and represents participating clients' existing demand-deposit claims against the bank.

The likely near-term winner for tokenized deposits is institutional settlement.

This development sits within a growing market for tokenized finance. McKinsey estimates tokenized market capitalization could reach around $2 trillion by 2030 in its base case, with a range of $1 trillion to $4 trillion, excluding stablecoins to avoid double-counting.

McKinsey also identifies cash and deposits among the likely front-runners.

At the same time, an IMF paper from March 2026 found that shocks to stablecoin demand can push down short-term Treasury yields, weaken the US dollar, and spill over into crypto and equity markets.

The form of digital dollars is becoming a macro-relevant market infrastructure.

What stablecoins still have

New York Fed research argues that the real edge of stablecoins lies in their use on global, open-access, permissionless systems.

The same research says the stablecoin market capitalization recently exceeded $260 billion and that annual organic stablecoin transaction volume rose from $3.29 trillion in 2021 to $5.68 trillion in 2024.

Stablecoins still have distribution, reach, and composability advantages that bank tokens may struggle to match, especially if bank products launch first in private or permissioned environments.

A second New York Fed staff report, published in February 2026, provides a framework for understanding the endgame. It found that the optimal outcome depends on regulatory costs and bank incentives.

The bull case for banks and tokenized deposits assumes that Hill's proposal becomes final substantially as described.

More banks would launch tokenized-deposit products, and these tokenized deposits would become the preferred on-chain cash leg for regulated tokenized securities and funds by combining programmability with deposit status and existing compliance infrastructure.

That outcome is strengthened by the Mar. 5 capital-neutral treatment for tokenized securities and by recent bank product launches, such as BNY's.

The bull case for stablecoins assumes the insurance distinction weighs less than network effects.

| Market function | Likely winner | Why |

|---|---|---|

| Open, borderless payments | Stablecoins | Wallet access, composability, global reach |

| Cross-border internet-native transfers | Stablecoins | 24/7 transferability and open-network distribution |

| Institutional settlement | Tokenized deposits | Deposit status, compliance, bank integration |

| Collateral and margin workflows | Tokenized deposits | Fits permissioned institutional systems |

| Regulated tokenized-asset markets | Tokenized deposits | Better fit with bank/legal infrastructure |

Stablecoins keep winning where universal wallet access, composability, 24/7 transferability, and cross-border use dominate.

Banks still participate, but through stablecoin subsidiaries under GENIUS rather than through deposit-token products, especially if tokenized deposits stay mostly permissioned and institution-only.

The market segmentation ahead

If both stablecoins and tokenized deposits can move on-chain, with only one category keeping ordinary deposit treatment, the market may start segmenting by function.

Open, borderless, internet-native payments may lean toward stablecoin-heavy solutions. Institutional settlement, collateral movement, and regulated tokenized-asset markets may tilt toward tokenized deposits.

Hill described a forthcoming proposal and said the FDIC is interested in comments, especially on the stablecoin pass-through issue and on tokenized-deposit arrangements involving third parties.

Hill tied deposit treatment to whether the product actually satisfies the statutory definition of a deposit, and the FDIC still wants comment on third-party structures. The design risk is real.

Banks can compete by keeping deposit status on-chain. Stablecoins may dominate open networks, and tokenized deposits may dominate regulated settlement.

The outcome depends on whether the insurance advantage outweighs the network advantage, and whether banks can build deposit products that work across the same open systems that stablecoins already operate in.

The post Stablecoins just lost key battle as insurance protection to be reserved only for bank-issued tokens appeared first on CryptoSlate.

FTX's fourth round of distributing bankruptcy recoveries arrives at a different moment. The estate will begin sending roughly $2.2 billion to eligible creditors on Mar. 31, just as Bitcoin (BTC) pushed back above $70,000 into what Glassnode called a thin $72,000-$82,000 on-chain zone.

FTX announced on Mar. 18 that its fourth distribution will begin Mar. 31 and end Apr. 3, with eligible creditors expected to receive funds via BitGo, Kraken, or Payoneer within 1 to 3 business days.

Dotcom customer claims receive an incremental 18% to reach 96% cumulative recovery, US customer claims receive 5% to reach 100%, and general unsecured and digital asset loan claims each receive 15% to reach 100%. Convenience claims stay at 120% cumulative.

This is the largest FTX distribution since the more than $5 billion second round in May 2025 and is 37.5% larger than the $1.6 billion third distribution in September 2025.

The nominal size alone makes it a real liquidity event, even though it falls short of half the scale of the May round.

Bitcoin's current structure

Bitcoin currently trades around $70,000 with an intraday low of $69,500, after yesterday's high of $74,603

Glassnode's Mar. 18 report said BTC had broken above $70,000 and entered a thinly accumulated $72,000 to $82,000 zone with limited on-chain resistance.

The market has probed into that zone but sits right on or just below the lower boundary, still working to hold the breakout cleanly.

Only about 60% of the supply is back in profit. Glassnode says a sustained move above 75% would be needed to confirm a genuine early bull transition.

The report still treated this as an early conviction rather than a fully validated bull regime.

As a result, the current setup is defined by absorption. Short-term holders realized profit spiked to $18.4 million per hour as BTC approached $74,000, echoing the same sell-into-strength behavior seen in February.

If the market can digest that selling and stay above $70,000, higher levels like the True Market Mean near $78,000 and the upper air-gap band near $82,000 become more plausible.

However, if absorption fails, the move still looks like a fragile bear market recovery rather than a durable trend change.

The current recovery looks more spot-led than leverage-led.

Glassnode says ETF allocations have rebounded, spot cumulative volume delta has turned higher, Coinbase spot activity has stabilized and turned positive, and CME futures positioning stays subdued.

CoinShares adds that digital asset investment products took in $1.06 billion last week, with Bitcoin accounting for $793 million, extending the three-week Bitcoin inflow run to $2.2 billion.

Derivatives present a constructive but restrained picture, as Glassnode sees the market emerging from negative funding and defensive hedging.

Deribit says BTC funding has moved back to roughly neutral, BTC futures-implied yields are flat at around 2% to 3% across tenors, and seven-day BTC implied volatility sits near 52%.

That profile fits a recovering market lacking aggressive speculative conviction.

Why FTX cash can have an impact now

CoinShares says Bitcoin investment products absorbed $2.2 billion over the last three weeks.

FTX is distributing $2.2 billion in cash. The two flows differ in nature: one represents direct Bitcoin fund inflows, while the other represents bankruptcy cash distributed to many creditors. Yet, their nominal size is identical.

The payout tests recycled liquidity, but it is unclear if even a small recycling ratio is enough to matter in a market trying to hold above $70,000 while absorbing $18.4 million per hour in short-term holder profit-taking.

Besides, Glassnode flagged that the FTX cash lands after the March options expiry tailwind. About $4.5 billion of negative dealer gamma sits around $75,000, with $3.9 billion expiring this month.

The report warns that once quarter-end expiry passes, the unwinding of dealer hedges could create headwinds or consolidation. FTX cash may hit just as a key supportive market mechanism fades.

A recycling model

At a 5% recycle rate, $110 million represents about 13.9% of last week's Bitcoin fund inflows and roughly 6 hours at the current $18.4 million-per-hour short-term holder realized profit pace.

Important, though likely insufficient to drive direction alone.

At a 10% recycle rate, $220 million equals about 27.7% of last week's Bitcoin fund inflows and about 12 hours of current short-term holder profit realization. Large enough to affect the price action over a short window, especially if ETF flows stay positive.

At a 20% recycle rate, $440 million represents about 55.5% of last week's Bitcoin fund inflows and nearly 24 hours of current short-term holder profit realization. At that point, the payout becomes a meaningful marginal bid.

At a 30% recycle rate, $660 million equals about 83.2% of last week's Bitcoin fund inflows. This is the level at which an FTX-driven re-risking wave would become visible relative to recent institutional spot demand.

If the full $2.2 billion were spread evenly over three days, that would be $733 million per business day.

Spread mechanically over 72 hours, it amounts to about $30.6 million per hour, versus the current $18.4 million per hour short-term holder realized profit rate. Even modest recycling rates become worth watching amid thin liquidity, where absorption capacity determines direction.

| Recycle rate | Cash potentially rotating back | Share of last week’s BTC fund inflows | Equivalent at $18.4M/hour STH profit-taking | Takeaway |

|---|---|---|---|---|

| 5% | $110M | 13.9% | ~6 hours | Noticeable, but likely not enough alone |

| 10% | $220M | 27.7% | ~12 hours | Can affect short-term price action |

| 20% | $440M | 55.5% | ~24 hours | Becomes a meaningful marginal bid |

| 30% | $660M | 83.2% | ~36 hours | Large enough to show up clearly in the tape |

The bull case assumes a 10% to 20% recycling rate, combined with positive ETF demand and a continued spot-led bid. BTC reclaims and holds the lower air-gap boundary, digests short-term holder selling, and starts trading toward the $78,000 True Market Mean, then $82,000.

The key tell would be price strength without a big re-leveraging in futures, validating the healthier spot-led recovery narrative.

The bear case assumes most recipients de-risk, hold cash, or redeploy elsewhere. BTC loses the lower air-gap boundary and drifts back toward the prior $64,000-$72,000 accumulation cluster.

The market effectively votes that returned FTX cash cannot overpower existing profit-taking and post-expiry headwinds.

The late-March window becomes a test of recycled liquidity landing in a spot-led market before leverage has fully returned.

What dictates the outcome is how much of the returned FTX money becomes fresh crypto demand.

The post Over $2B in “lost” Bitcoin to hit markets this month creating sell pressure within fragile $67k–$74k range appeared first on CryptoSlate.

The US Securities and Exchange Commission (SEC) has drawn its clearest line yet around which parts of crypto it views as outside securities law, a move that hands the industry a new map of regulatory winners while opening a narrower lane for privacy-focused technology.

However, the SEC’s new crypto taxonomy does more than just redraw markets. Quietly, the new approach blocks a regulatory path that could have forced developers and software providers into KYC-heavy broker-dealer regimes.

By classifying much of crypto activity as securities brokerage, the SEC’s earlier approach could have forced developers and software companies to register as broker-dealers, thereby requiring them to comply with strict identity checks (KYC) and anti-money-laundering (AML) rules.

In an interpretive release issued on March 17, alongside the Commodity Futures Trading Commission, the SEC categorized crypto assets into five categories: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities.

The agency said digital commodities, digital collectibles, and digital tools are not themselves securities, while stablecoins may or may not be securities depending on their structure, and digital securities remain inside the SEC’s core jurisdiction.

Chair Paul Atkins framed the shift in broad terms. In remarks announcing the policy, he said the commission was implementing a token taxonomy under which digital commodities, digital collectibles, digital tools, and payment stablecoins under the GENIUS Act are not deemed securities, while digital securities, meaning tokenized traditional securities, remain subject to federal securities law.

The CFTC said it would administer the Commodity Exchange Act in a manner consistent with the SEC’s interpretation, giving the guidance immediate weight beyond a single-agency speech.

Named commodities move to the front

The digital commodity bucket is the most important part of the release because it reaches the largest pool of liquid crypto assets and provides a clearer path away from the securities hostilities overhang that defined the Gary Gensler era.

The SEC describes a digital commodity as a fungible crypto asset linked to the programmatic operation of a functional crypto system, with value tied to utility and supply and demand rather than the essential managerial efforts of others.

That definition strengthens the policy position around Bitcoin and Ethereum, but it also extends formal comfort to networks that have sat in a more contested middle ground, including Solana, Cardano, XRP, and Avalanche. XRP stands out because it spent years at the center of one of the industry’s highest-profile securities fights.

Stuart Alderoty, Ripple's chief legal officer, noted:

“We always knew XRP wasn't a security – and now the SEC has made clear what it is: a digital commodity.”

Solana, Cardano, and Avalanche also gain because the SEC release does more than classify tokens. It also addresses the network activities that help secure them.

For proof-of-work networks, the SEC said covered protocol mining activities do not involve the offer and sale of a security, which supports Bitcoin, Litecoin, Dogecoin, and Bitcoin Cash. For proof-of-stake networks, the commission said covered protocol staking activities do not involve the offer and sale of a security either.

Meanwhile, that interpretation extends to staking by token holders, the roles of third-party validators and custodians, and the issuance and redemption of staking receipt tokens, which serve as one-for-one receipts for deposited non-security crypto assets.

That gives another layer of support to ETH, Solana, Cardano, Avalanche, Polkadot, Tezos, and Aptos.

The release also says redeemable wrapped tokens backed one-for-one by deposited non-security crypto assets and redeemable on a fixed one-for-one basis do not involve the offer and sale of a security in the circumstances described by the SEC.

Collectibles, memes, and utility tokens gain a lane

The second group of winners is smaller in market value but more surprising in political and cultural terms.

The SEC’s digital collectible category includes assets designed to be collected or used and lacking rights to income, profits, or assets of a business enterprise. Its examples include CryptoPunks, Chromie Squiggles, Fan Tokens, WIF, and VCOIN.

The inclusion of WIF, a meme coin, signals to markets that some community-driven tokens can be analyzed less as capital-raising instruments and more as cultural or collectible assets, though the SEC notes that hybrid structures can still raise securities questions.

The digital tools category is another beneficiary. The SEC defines digital tools as crypto assets that perform practical functions such as memberships, tickets, credentials, title instruments, or identity badges. Its examples include Ethereum Name Service (ENS) domain names and CoinDesk’s Microcosms NFT Consensus Ticket.

The commission says digital tools are on-chain analogues to physical utilities and that people acquire them for functional use rather than a claim on a business enterprise.

This is significant beyond the listed examples because it gives a clearer route for builders working on identity, access, naming, and credential systems. For a sector that has often had to explain why a token is a tool rather than an investment product, the SEC has now supplied its own framework.

Stablecoins also move into a stronger position, though with more conditions than the commodity bucket.

The release states that, once the GENIUS Act becomes effective, payment stablecoins issued by permitted payment stablecoin issuers under the GENIUS Act are excluded from securities status by statute. It also says other stablecoins may or may not be securities depending on the facts and circumstances.

That gives regulated dollar-linked issuers a clearer federal lane while keeping yield-bearing and more structured designs under closer scrutiny.

Privacy gets a quiet opening

While the SEC’s taxonomy creates no standalone privacy bucket, it narrows the range of crypto assets and crypto activity that sit inside securities treatment.

In the release, the agency says digital commodities, digital collectibles, and digital tools are not themselves securities, while also stating that the interpretation does not itself create new legal obligations. The commission separately says the Bank Secrecy Act and the Anti-Money Laundering Act are outside the scope of the action.

That language is why privacy advocates are treating the move as an opening for the sector, which had come under increased scrutiny over the past few years.

Independent journalist L0la L33tz argued in a post on X that the interpretation is a major privacy win because a broader broker-dealer framing for digital-asset developers and software-linked services could have pushed more of the sector toward KYC and AML obligations under securities law.

Her reading captures the shift in jurisdictional terms: a narrower SEC perimeter leaves more room for crypto software and non-security asset activity to exist outside the commission’s core registration regime.

The practical benefit of this is strongest around self-custody, open-source development, and non-custodial tools. The SEC’s digital tools category supports that view because it treats functional on-chain assets as utilities acquired for use rather than as claims on a business enterprise.

For privacy-focused builders, wallet software, credential layers, and related infrastructure, the release offers a clearer argument that software-linked crypto activity should be analyzed in terms of function and control rather than automatically through an investment-product lens.

Meanwhile, the remaining compliance boundary sits with Treasury and FinCEN. FinCEN’s 2019 guidance says an anonymizing software provider is not a money transmitter because supplying software differs from accepting and transmitting value.

In the same guidance, FinCEN says an anonymizing services provider that accepts and retransmits value is a money transmitter under its rules.

That leaves privacy advocates with a meaningful policy gain inside securities law while AML and money-transmission obligations continue to be handled through a separate federal framework.

The deeper market message

The broader significance of the SEC release is that it offers a sorting mechanism the industry has wanted for years without dissolving every legal question around token issuance and distribution.

The commission says a non-security crypto asset can still be offered and sold, subject to an investment contract that remains a security.

In practice, that means classification helps most when a token is closely tied to a functioning network, a practical use case, or a decentralized system rather than to a promoter’s ongoing promises about enterprise value.

That leaves the winners from this framework easier to identify. Bitcoin, ETH, Solana, XRP, and other named digital commodities gain the clearest immediate boost. Staking networks, wrapped non-security assets, digital tools, and payment stablecoins receive stronger legal framing.

Meanwhile, privacy-focused crypto projects gain a narrower but still important opening because the SEC has drawn a firmer boundary around its own authority.

So, the next chapter for the market will turn on how exchanges, issuers, developers, and Treasury-led compliance agencies respond to that new map.

The post SEC drastically reduces KYC pressure on Bitcoin, XRP, and Solana with revamped crypto rules appeared first on CryptoSlate.

Cryptoticker

Bitcoin news today is dominated by a sudden reversal in market sentiment. After a spectacular rally that saw the $Bitcoin price push toward the $76,000 resistance level earlier this week, the primary cryptocurrency has experienced a sharp correction. On Thursday, March 19, 2026, Bitcoin slipped below the psychologically significant $70,000 mark, trading as low as $69,400 during the European session.

This downward move follows a period of intense optimism fueled by institutional ETF inflows and the SEC’s recent classification of 16 digital assets as commodities. However, the combination of a "hawkish hold" by the Federal Reserve and escalating geopolitical tensions in the Middle East has forced investors back into a defensive posture.

Why is Bitcoin Crashing?

The core reason for the Bitcoin price drop today is a "perfect storm" of macroeconomic factors. Specifically, the Federal Reserve’s decision to keep interest rates in the 3.50%–3.75% range, paired with a surge in global oil prices (Brent crude exceeding $114), has strengthened the US Dollar and dampened the appetite for "risk-on" assets like cryptocurrencies.

The "Hawkish Hold" and Risk Appetite

In financial terms, a "Hawkish Hold" occurs when a central bank keeps interest rates unchanged but uses rhetoric that suggests rates will stay higher for longer or could even rise.

For Bitcoin, this is a significant headwind. Because BTC is often viewed as a high-growth, speculative asset, its valuation is highly sensitive to liquidity. When the Fed signals that it is not ready to pivot to rate cuts, the "cost of carry" for holding Bitcoin remains high compared to "safe" yields like US Treasuries.

The Fed Effect: High Rates and Inflation Fears

The Federal Reserve's March meeting was the primary catalyst for the volatility seen in today's bitcoin news. While the market expected rates to remain steady, the updated "dot plot" and comments from Chair Paul Atkins (who took over the SEC and influenced broader policy) suggested that inflation remains a stubborn foe.

- Inflation Forecast: The Fed raised its 2026 PCE inflation outlook to 2.7%.

- Growth Outlook: Projected growth for 2026 was upgraded to 2.4%, giving the Fed more room to keep rates high without immediate fear of a recession.

- Market Reaction: The probability of an April rate cut has plummeted to near zero, with some traders now pricing in a 4% chance of a rate hike if energy costs continue to spiral.

Geopolitical Tensions: The Oil Factor

Beyond the Fed, the escalating conflict in the Middle East has sent shockwaves through the energy markets. Attacks on energy infrastructure have caused oil prices to spike, which historically leads to higher transport and production costs, further fueling inflation.

In previous cycles, Bitcoin was occasionally touted as "digital gold" or a safe haven. However, recent crypto news shows that in times of acute geopolitical stress, BTC often moves in lockstep with the Nasdaq-100, which also saw significant losses today. Investors are currently seeking the safety of the US Dollar and actual physical gold over digital assets.

Institutional Sentiment: ETF Inflows Turn to Outflows

A key pillar of the recent rally was the consistent demand from US-listed spot Bitcoin ETFs. According to data from CoinGlass, a seven-day streak of inflows—totaling over $1.1 billion—was snapped on Wednesday.

| Metric | Detail |

|---|---|

| Trend Change | 7-day inflow streak broken |

| Wednesday Outflow | ~$129 million |

| Key Support Level | $69,000 - $70,000 |

| Next Resistance | $74,500 |

From a technical perspective, Bitcoin's failure to reclaim the $76,000 level is a bearish signal in the short term. The price is currently testing the 100-hourly simple moving average. If the $69,000 support level fails to hold, analysts warn of a potential slide toward the $66,500 zone, which acted as a floor earlier in March.

As of March 19, 2026, the global financial markets are witnessing a rare and counter-intuitive phenomenon. Despite an escalation in the Middle East conflict—including strikes on critical energy infrastructure—both Gold (XAU/USD) and Bitcoin (BTC/USD) are trading in the red. Traditionally, these assets serve as the world’s primary "disaster hedges," yet they have both succumbed to a broader market sell-off following the Federal Reserve’s hawkish stance on Wednesday.

This "double drop" is not a sign that the safe-haven narrative is dead. Instead, it is a textbook example of a liquidity squeeze driven by a resurgent US Dollar and rising bond yields. As oil prices surge above $110 per barrel, the market is pricing in "sticky" inflation, forcing the Fed to keep interest rates high, which historically creates a temporary headwind for non-yielding assets like Gold and high-beta assets like Bitcoin.

Why are Gold and Bitcoin Falling Today?

The primary reason Gold and Bitcoin are dropping today is the Federal Reserve’s decision to hold interest rates at 3.5%–3.75% while signaling fewer rate cuts for the remainder of 2026. This move strengthened the US Dollar Index (DXY), making dollar-denominated assets more expensive. Furthermore, investors are selling "winning" positions in Gold and Bitcoin to cover margin calls in the plummeting equity and energy markets.

Gold Price Analysis: XAU/USD Rejects the $5,000 Milestone

After flirting with the psychological resistance of $5,000 earlier this week, Gold has entered a sharp corrective phase. On the morning of March 19, spot gold slipped toward the $4,800 region, marking its most significant losing streak in over a year.

Critical Support and Resistance Levels

- Major Support: $4,840 – $4,750. This zone represents a historical "buy-the-dip" area for central banks.

- Major Resistance: $5,000. Reclaiming this level is essential for the bullish trend to resume.

The "Oil Shock" of 2026 has been a double-edged sword for Gold. While it fuels long-term inflation (bullish for Gold), it also increases the likelihood of a "higher-for-longer" interest rate environment (bearish for Gold). Currently, the market is prioritizing the interest rate risk over the inflation hedge.

Bitcoin Technical Analysis: Is $70,000 the New Floor?

Bitcoin has shown relative resilience compared to the broader "Risk-On" sector, yet it was unable to sustain its push toward $76,000. On Thursday, $BTC dropped below $71,000, tracking the general weakness in global liquidity.

The "Digital Gold" Decoupling

Interestingly, the 2026 correlation between Gold and Bitcoin has shifted. According to recent data from Investing.com, Bitcoin is increasingly behaving as a "Global Liquidity Sponge." It thrives when money is cheap. With the Fed’s hawkish tone, Bitcoin is facing a temporary outflow. However, institutional demand via Bitcoin ETFs remains a structural floor that prevented a crash below $66,000.

- BTC Immediate Support: $70,200.

- BTC Resistance: $74,500.

The 2026 Correlation: Safe Havens vs. Liquidity Hedges

Traders often mistake Bitcoin and Gold for the same type of asset. In 2026, the distinction has become clear:

- Gold: A geopolitical "bunker" asset. It drops when the Dollar is strong but rises when sovereign trust fails.

- Bitcoin: A "technological" hedge. It performs best when the financial system seeks an alternative rail for 24/7 global liquidity.

| Asset | 24h Trend | Key Driver | Long-term Outlook |

|---|---|---|---|

| Gold (XAU) | Bearish | Fed Hawkishness / DXY Strength | Bullish (Target $5,500) |

| Bitcoin (BTC) | Neutral-Bearish | Liquidity Withdrawal / ETF Flows | Highly Bullish (Target $100k+) |

How to Navigate the Bitcoin and Gold Crash

For investors looking to capitalize on this volatility, diversification remains the key. While the short-term trend is downward, the macro fundamentals—high debt, war, and energy shortages—historically favor both assets.

- For Gold: Look for stability around the $4,800 mark.

- For Bitcoin: Utilize the best crypto exchanges to set limit orders near $68,500, which has acted as a strong institutional accumulation zone.

- Security: Ensure your assets are safe by using a hardware wallet during these high-volatility periods.

Bitcoin Future: The Path Ahead for March 2026

The "Great Decoupling" of 2026 is in full swing. Gold is fighting the weight of a high-interest-rate environment, while Bitcoin is consolidating its gains after a massive Q1 rally. Despite the current price drops, the geopolitical unrest in the Middle East suggests that the "safe haven" trade is merely resting, not retreating. Traders should keep a close eye on the US Dollar Index (DXY); a reversal there will likely trigger a massive "relief rally" for both XAU and BTC.

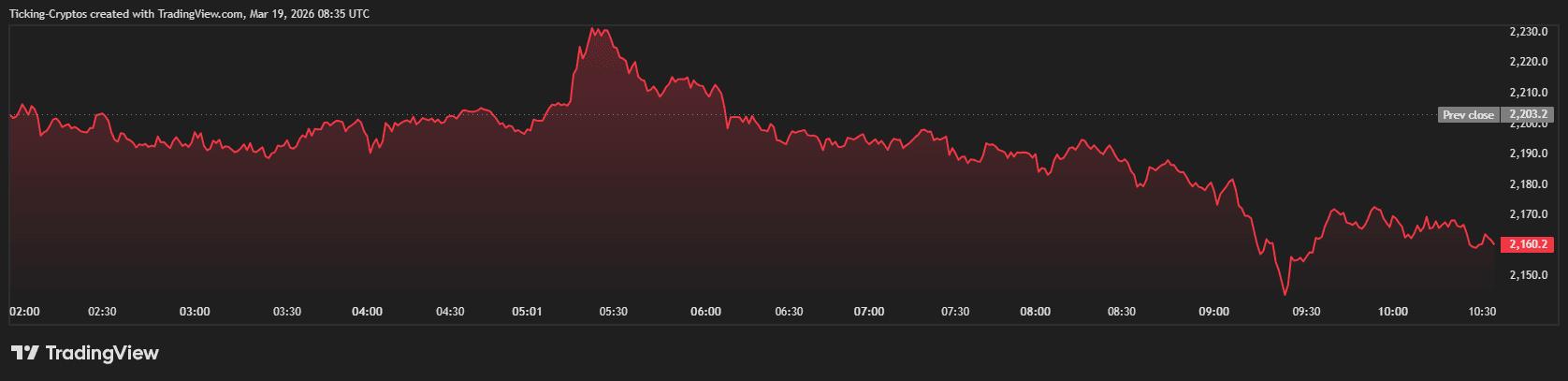

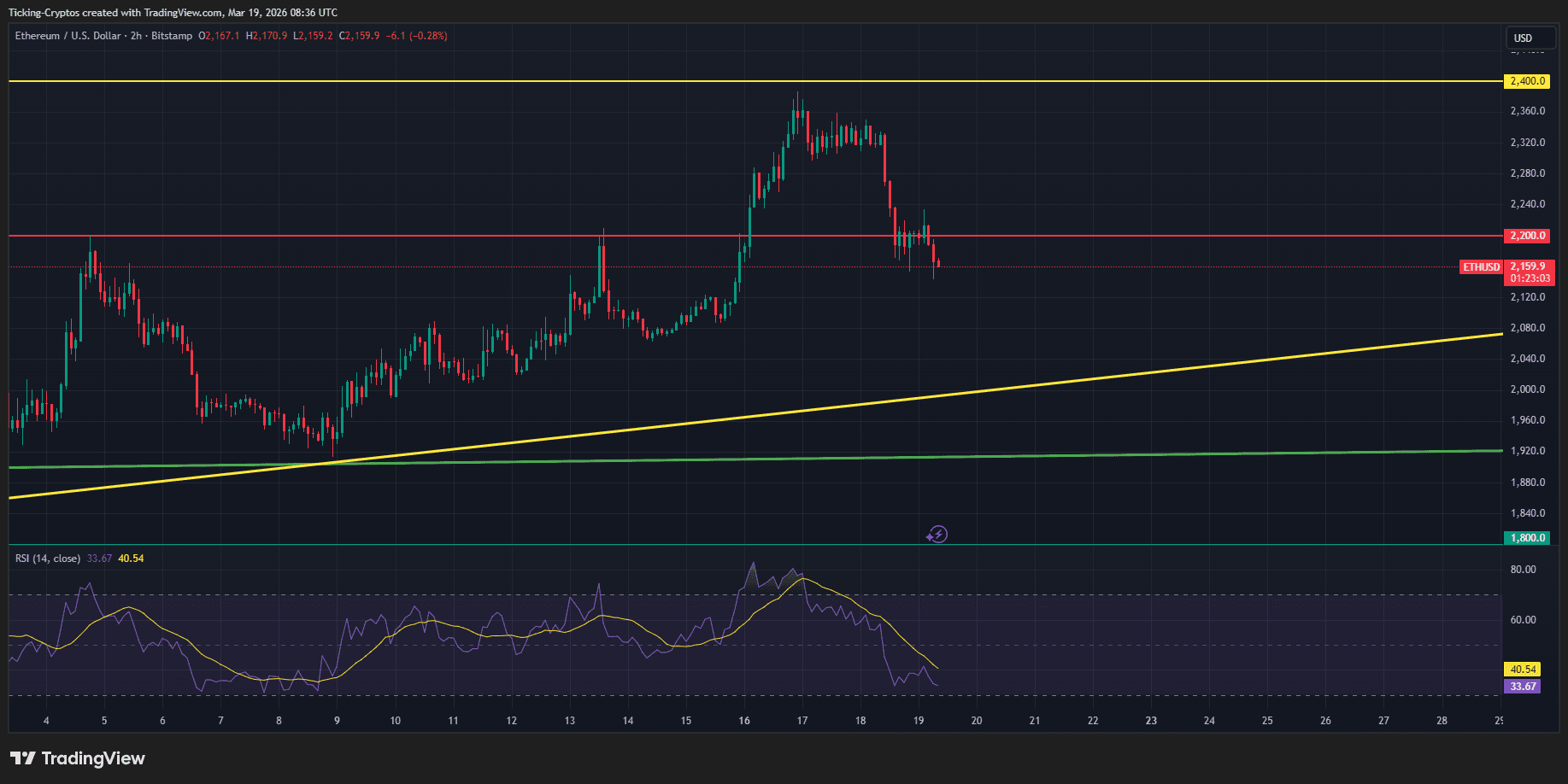

After a brief rally earlier this week, Ethereum ($ETH) is now testing the critical breakout-turned-support zone between $2,180 and $2,200.

This price action comes as a direct response to three simultaneous global shocks: a major military escalation in the Middle East, a hotter-than-expected US inflation report, and a stern warning from Federal Reserve Chair Jerome Powell. For ETH bulls, the mandate is clear: hold the $2,200 line or risk a deep correction toward the psychological support of $1,900.

Ethereum Analysis: Why Are Cryptos Crashing

The sudden reversal in risk appetite isn't just a technical correction; it is a fundamental shift driven by three massive catalysts.

1. Middle East Conflict Hits Global Energy

Geopolitical tensions reached a breaking point today following reports that Israel targeted Iran’s South Pars gas facility, the world’s largest gas field. In immediate retaliation, Iranian strikes reportedly caused extensive damage to Qatari LNG infrastructure at Ras Laffan.

This "energy war" sent crude oil prices soaring toward $99 per barrel almost instantly. For Ethereum and the broader crypto market, rising energy costs act as a double-edged sword: they increase the cost of living (reducing retail liquidity) and fuel long-term inflation fears.

2. PPI Data: The Inflation Pipeline is Refilling

Adding fuel to the fire, the Producer Price Index (PPI) for February 2026 came in significantly hotter than anticipated at 3.4% year-on-year. This suggests that wholesale inflation is accelerating even before the full impact of the recent oil price surge hits the data.

When "factory gate" prices rise, they inevitably trickle down to consumers, making the path to the Fed’s 2% target look increasingly impossible.

3. Powell’s Hawkish Pivot

Federal Reserve Chair Jerome Powell held interest rates steady at 3.5%–3.75% today, but it was his tone that rattled the cages. For the first time in the Fed's history, the committee explicitly acknowledged the Middle East situation as a primary economic risk.

Powell’s refusal to commit to a timeline for rate cuts, combined with the acknowledgment of "uncertain" implications for the US economy, led markets to price out a summer pivot.

Ethereum Price Analysis: Will Ethereum Price Recover?

Despite the macro negativity, Ethereum's chart shows a technical battle that is currently being fought at the "Line in the Sand."

Critical Support at $2,180–$2,200

As seen in recent trading data, Ethereum has retraced to its previous breakout zone. This area was formerly a heavy resistance level throughout early 2026. In technical analysis, a successful "retest" of this zone as support would be a massive bullish signal.

- The Bull Case: If ETH closes the daily candle above $2,200, it confirms that buyers are still defending the trend despite the macro noise. This could lead to a relief rally back toward $2,320.

- The Bear Case: A breakdown below $2,180 would invalidate the recent recovery. Given the lack of intermediate liquidity, the next major "safety net" sits at $1,900.

Market Sentiment and Correlation

Ethereum’s correlation with the S&P 500 and Bitcoin remains high. With the US dollar index (DXY) strengthening on the back of safe-haven flows, ETH faces significant selling pressure. Investors looking to hedge against this volatility often turn to hardware wallets to secure their assets during periods of extreme exchange uncertainty.

Ethereum Prediction: What to Watch Next

The next 48 hours are crucial for the ETH/USD pair. Investors should monitor:

- Oil Price Stability: If oil breaks $105, expect further downside in equities and crypto.

- The $2,180 Closing Price: A daily close below this level often triggers stop-loss cascades.

- Strait of Hormuz Developments: Any further disruption to global trade will likely keep the crypto market in a defensive crouch.

Bitcoin Price Crash: Crypto Market Faces a Sudden Reversal

The cryptocurrency market has entered a period of intense volatility today, March 18, 2026, with Bitcoin ($BTC) tumbling from its recent highs near $76,000 to the $72,000 range. This sudden "sea of red" has caught many retail traders off guard, especially following the bullish momentum seen earlier this week.

While the digital asset space often moves independently, today’s crash is a direct result of a "perfect storm" involving geopolitical escalations, disappointing US inflation data, and a necessary technical cooling period.

1. Middle East Escalation: Energy Infrastructure Under Attack

The primary driver of the "risk-off" sentiment across global markets is the dramatic escalation in the Middle East. Following Israeli strikes on Iran’s South Pars gas field—the world’s largest natural gas reserve—Tehran has officially declared its intent to retaliate against Gulf energy sites.

Key Geopolitical Developments:

- Target List: Iran’s Revolutionary Guards have identified key infrastructure in Saudi Arabia, the UAE, and Qatar as potential targets.

- Energy Disruption: Iraq has already reported a total halt of gas supplies from Iran, leading to a loss of approximately 3,100 megawatts of power.

- Oil Prices Surge: Brent crude has spiked toward $110 a barrel, fueling fears of global stagflation.

In times of war and energy insecurity, investors typically flee "risk assets" like cryptocurrencies in favor of "safe havens" like gold or the US Dollar. This flight to safety is putting massive downward pressure on the $Bitcoin price.

2. US Core PPI Hits 3.9%: Inflation Remains "Sticky"

Macroeconomic data released today has further dampened hopes for a dovish pivot from the Federal Reserve. The US Core Producer Price Index (PPI), which excludes volatile food and energy costs, came in at 3.9% year-over-year.

This figure significantly overshot market expectations of 3.7%. For crypto investors, this is a bearish signal because:

- Higher for Longer: Hotter-than-expected wholesale inflation suggests the Fed will keep interest rates elevated to cool the economy.

- Yield Pressure: Treasury yields have climbed following the report, making non-yielding assets like Bitcoin less attractive to institutional players.

- Liquidity Crunch: High interest rates reduce the "cheap money" that typically flows into speculative markets.

3. Technical Adjustment: The $76,000 Rejection

From a purely technical perspective, many analysts argue that a correction was overdue. Bitcoin recently hit a peak of $76,000, a level that acted as a psychological and technical glass ceiling.

The "Overheated" Market

Leading up to today’s drop, several on-chain indicators suggested the market was "overextended." Funding rates in the derivatives market had reached unsustainable levels, meaning long-positioned traders were paying high premiums to keep their bets open.

When the news of the Iranian retaliation broke, it triggered a "long squeeze," forcing leveraged traders to liquidate their positions. This mechanical selling accelerated the drop, pushing BTC toward its immediate support levels.

What’s Next for Bitcoin and Altcoins?

The market is currently looking for a floor. While the $72,000 level is providing some initial support, the upcoming Federal Reserve meeting will be the next major catalyst. If the Fed adopts a hawkish tone due to the PPI data and rising energy costs, we could see further testing of the $68,000–$70,000 zone.

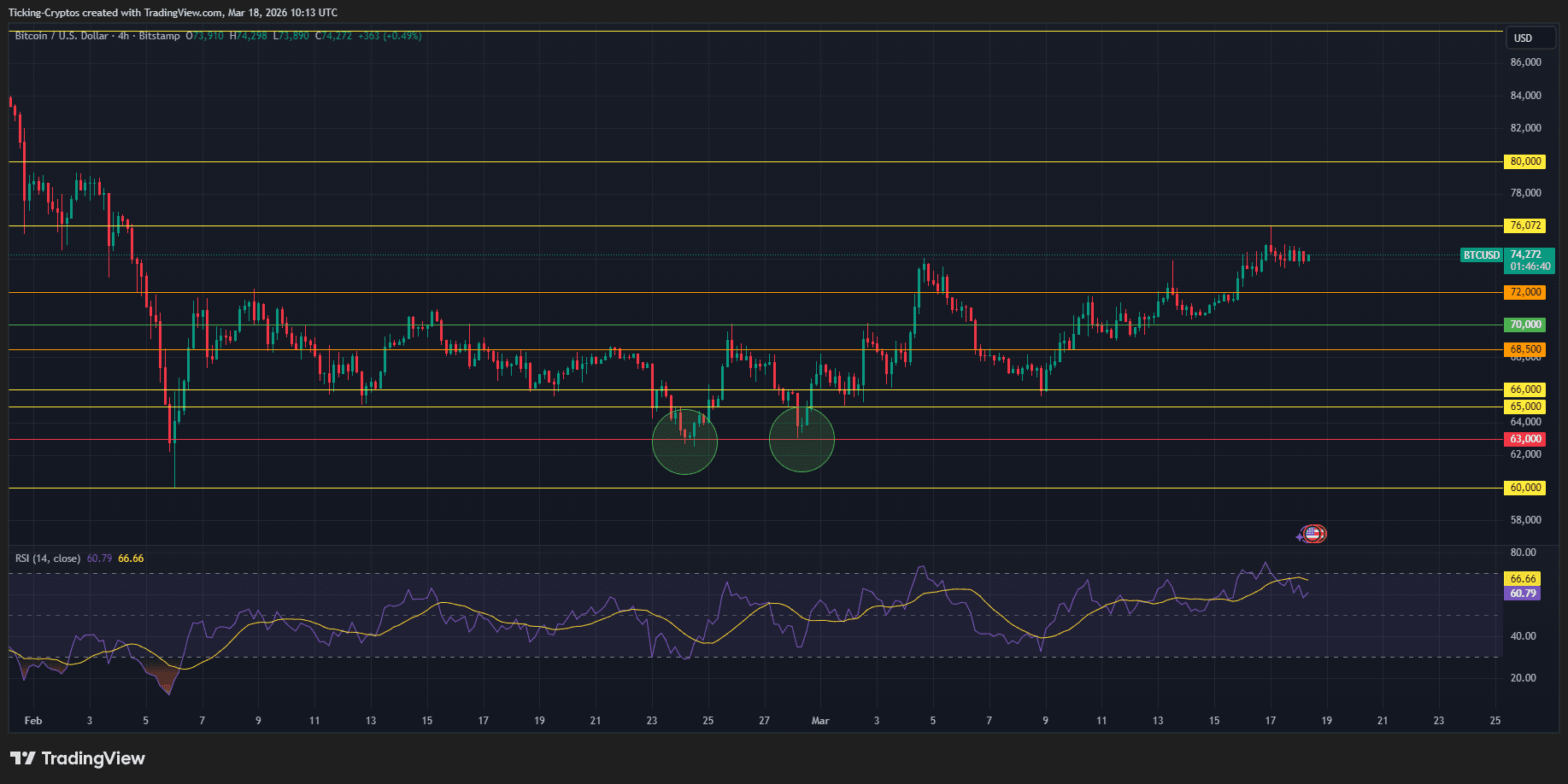

The Bitcoin price is currently navigating a high-stakes consolidation phase, trading at approximately $74,272 during the March 18, 2026, session. After a period of bearish dominance that saw the asset retreat from its 2025 record highs, the market is now testing the resilience of the $74,000 resistance zone.

Bitcoin Price Analysis: Why is BTC Price UP?

Analyzing the BTC/USD 4-hour chart, we observe several key technical patterns that define the current trend.

Double Bottom Recovery

The chart highlights two significant "troughs" (marked with green circles) near the $63,000 level. This Double Bottom formation served as a powerful reversal signal in late February and early March, allowing Bitcoin to climb back above the psychological $70,000 mark.

Key Resistance and Support Levels

The price action is currently sandwiched between tightly defined horizontal levels:

- Immediate Resistance: $74,500 – $76,000. A decisive break above this yellow-lined zone is required to target the next major hurdle at $80,000.